Comprehensive Analysis of Vodafone's International Finance Report

VerifiedAdded on 2022/09/05

|17

|3342

|24

Report

AI Summary

This report provides a comprehensive analysis of Vodafone's international financial performance, examining the impact of various external factors and incidents on the company's operations. It delves into the company's dividend policy, sources of finance, and the influence of financial ratios on its overall performance. The report includes a detailed discussion of liquidity, efficiency, profitability, and investment ratios, calculated using data from Vodafone's financial statements, comparing the company's performance across different financial years. The analysis highlights the significance of financial ratios in assessing the company's solvency, efficiency, and profitability, providing insights into its financial health and strategic decisions, and the impact of global economic uncertainties and regulatory changes. The report also touches upon Vodafone's risk management strategies, accounting standards, and competitive landscape, offering a holistic view of its financial standing within the telecommunications industry.

Running head: INTERNATIONAL FINANCE

INTERNATIONAL FINANCE

Name of the student

Name of the university

Author’s note

INTERNATIONAL FINANCE

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL FINANCE

Executive summary

The paper aims to highlight the recent international financial development and incidents which

has impacted the company’s performance. The paper studies how different external factors affect

the company’s dividend policy and the sources of finance of the company. The paper concludes

that financial ratios play a crucial role in studying the performance of the company. It concludes

that the financial ratios help to compare one business performance with its competitors as well as

in comparison to the whole industry.

Executive summary

The paper aims to highlight the recent international financial development and incidents which

has impacted the company’s performance. The paper studies how different external factors affect

the company’s dividend policy and the sources of finance of the company. The paper concludes

that financial ratios play a crucial role in studying the performance of the company. It concludes

that the financial ratios help to compare one business performance with its competitors as well as

in comparison to the whole industry.

2INTERNATIONAL FINANCE

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Answer a......................................................................................................................................4

Answer b......................................................................................................................................5

Answer c......................................................................................................................................6

Liquidity Ratio.............................................................................................................................6

Efficiency Ratio...........................................................................................................................8

Profitability Ratio......................................................................................................................10

Investment Ratio........................................................................................................................13

Conclusion.....................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Answer a......................................................................................................................................4

Answer b......................................................................................................................................5

Answer c......................................................................................................................................6

Liquidity Ratio.............................................................................................................................6

Efficiency Ratio...........................................................................................................................8

Profitability Ratio......................................................................................................................10

Investment Ratio........................................................................................................................13

Conclusion.....................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL FINANCE

Introduction

Any international business which is conducting its business operations in several

countries is generally affected by the change in the environmental and economic changes

happening in all those countries. The change in the external environment usually affects the

internal environment of the company. The external factors can be in terms of the change in the

technology, rules and regulations, new product development, creation of new demand, change of

government, subsidies and tariffs or restriction and allowance of free trade can have a direct or

indirect effect on the business. The change in the environment directly affects the internal

environment in which the business is operating. Companies prepare financial statements to show

the financial position of the business. The financial statements are prepared with the objective of

providing financial information about the performance of the company. It is prepared basically

for the use of stakeholders so that they can make decisions concerning the company for their

Introduction

Any international business which is conducting its business operations in several

countries is generally affected by the change in the environmental and economic changes

happening in all those countries. The change in the external environment usually affects the

internal environment of the company. The external factors can be in terms of the change in the

technology, rules and regulations, new product development, creation of new demand, change of

government, subsidies and tariffs or restriction and allowance of free trade can have a direct or

indirect effect on the business. The change in the environment directly affects the internal

environment in which the business is operating. Companies prepare financial statements to show

the financial position of the business. The financial statements are prepared with the objective of

providing financial information about the performance of the company. It is prepared basically

for the use of stakeholders so that they can make decisions concerning the company for their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL FINANCE

benefits. The financial statements include income statements, balance sheet and the cash flow

statements. The company also prepare annual reports at the end of an accounting period to show

the overall performance of the business and to show their strategic plans for future growth. The

company uses financial ratios to show the company’s performance. Besides, financial analysts

calculate these financial ratios to know the true financial position of the company. The financial

ratios are very useful for the investors as they can use these ratios as the indicator of the

company’s solvency or insolvency. The ratios are very significant for the investors as it helps

them to make decisions concerning investment in the company.

Discussion

Answer a

Vodafone plc. is a multinational telecommunication company. it was established in the

year 1982 in Newbury, United kingdom. Vodafone plc started operating together with its

subsidiary Vodafone India. The Vodafone Corporation collaborated with the Idea cellular

limited. This created a new business known as the Vodafone India limited. This is a company

which is owned by the Vodafone and Aditya Birla Group. The business collaborations using

acquisitions and mergers affects the financial performance of the business. Big businesses

always adopts the method of acquisitions and mergers to gain synergy and improve the

performance and revenue with wider economies of scale. After acquiring the company, it

becomes important to seek every financial information concerning the performance of the taken

benefits. The financial statements include income statements, balance sheet and the cash flow

statements. The company also prepare annual reports at the end of an accounting period to show

the overall performance of the business and to show their strategic plans for future growth. The

company uses financial ratios to show the company’s performance. Besides, financial analysts

calculate these financial ratios to know the true financial position of the company. The financial

ratios are very useful for the investors as they can use these ratios as the indicator of the

company’s solvency or insolvency. The ratios are very significant for the investors as it helps

them to make decisions concerning investment in the company.

Discussion

Answer a

Vodafone plc. is a multinational telecommunication company. it was established in the

year 1982 in Newbury, United kingdom. Vodafone plc started operating together with its

subsidiary Vodafone India. The Vodafone Corporation collaborated with the Idea cellular

limited. This created a new business known as the Vodafone India limited. This is a company

which is owned by the Vodafone and Aditya Birla Group. The business collaborations using

acquisitions and mergers affects the financial performance of the business. Big businesses

always adopts the method of acquisitions and mergers to gain synergy and improve the

performance and revenue with wider economies of scale. After acquiring the company, it

becomes important to seek every financial information concerning the performance of the taken

5INTERNATIONAL FINANCE

over subsidiary entities. Vodafone also included the major change in the organizational system.

It presented the annual report incorporating all the facts of these business activities and also

presented the segment financial reporting.

The other development in the international financial framework that affected the

company is depicted in its 2019 annual reports. The company states that the frequent changes in

the financial regulatory framework have developed many challenges to the company. The

adoption of IFRS 9 in 2018 is new challenge for the company’s financial reporting team. The

company included it in the key matters that affected the company’s performance reporting.

All these limits the company’s growth. There was a decrease in the prepaid services, and

thus it affected the revenue of the company badly. The company has overseas clients who

account for more than 50% of clients. The whole world is seeing the economic uncertainties, and

since the company has 50% global clients, the business faces many unknown challenges. The

company develops action plans to face these continuous challenges and increase the demand for

its various networking services. Risk management strategies of the company are based on the

upcoming challenges that the business sees as a hurdle. The company specifies that the

derivative instruments can help the company to attain growth in the financial market. The

strategic position is to develop a hedge position which can help the company to reduce the

financial risk and sustain growth. However company specifies that it does not use the derivative

instrument for speculative purposes.

There weretwo major accounting standards adopted by the Vodafone in 2018 ans those

were; IFRS 15 “Revenue from Contracts with Customers” and IFRS 9 which specifies the

standards of financial instrument. As per IFRS 9, company made so many changes and the

financial statement of the company was influenced significantly. The cash and cash equivalent

over subsidiary entities. Vodafone also included the major change in the organizational system.

It presented the annual report incorporating all the facts of these business activities and also

presented the segment financial reporting.

The other development in the international financial framework that affected the

company is depicted in its 2019 annual reports. The company states that the frequent changes in

the financial regulatory framework have developed many challenges to the company. The

adoption of IFRS 9 in 2018 is new challenge for the company’s financial reporting team. The

company included it in the key matters that affected the company’s performance reporting.

All these limits the company’s growth. There was a decrease in the prepaid services, and

thus it affected the revenue of the company badly. The company has overseas clients who

account for more than 50% of clients. The whole world is seeing the economic uncertainties, and

since the company has 50% global clients, the business faces many unknown challenges. The

company develops action plans to face these continuous challenges and increase the demand for

its various networking services. Risk management strategies of the company are based on the

upcoming challenges that the business sees as a hurdle. The company specifies that the

derivative instruments can help the company to attain growth in the financial market. The

strategic position is to develop a hedge position which can help the company to reduce the

financial risk and sustain growth. However company specifies that it does not use the derivative

instrument for speculative purposes.

There weretwo major accounting standards adopted by the Vodafone in 2018 ans those

were; IFRS 15 “Revenue from Contracts with Customers” and IFRS 9 which specifies the

standards of financial instrument. As per IFRS 9, company made so many changes and the

financial statement of the company was influenced significantly. The cash and cash equivalent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL FINANCE

and short term investment which were recorded at amortized cost is classified as fair value in the

income statement. However company mentions that these do not have material impact on the

business materiality. The carrying amount of account receivables and contractual assets are

decresed by lifetime estimated future credit losses on the date of recognition while earlier the

credit losses were not used to be recognized on such assets. The new IFRS 9 has changed the

requirements of accounting reporting of some assets. However, it do not affect much the

financial reporting of the company.

Answer b

Through successful risk management activities, the company continue to increase its

revenue and generated 7071 million euros in cash from the operating activities in 2019. The

optimum cash generation helped the company to conduct capital improvement plans. It also

distributed a dividend which showed the company’s solvent and healthy position. In addition to

this, in 2019 the company also paid dividend of amount 4022 million euros to keep the interest of

the stakeholders a priority. As per the annual report of the company, there are several factors that

determine the dividend policy of the company. All the dividends paid by Vodafone Corporation

are declared by the company in euros. The dividend payable by the company depends on many

factors such as earnings of the company, liquidity position, financial conditions of the company

etc. the share pricing trends and the consumer developing interest to use digitalization helps to

determine the overall revenue of the Vodafone corporations. The company states that the share

prices may rise or fluctuate by the company’s recent strategic positions of investments in other

businesses. The company mentions that the revenue of the business has gone down by 10%

because it is facing tough competition in the prepaid market. The company fails to develop the

successful planning which can create a competitive advantage and helps the business to deal with

and short term investment which were recorded at amortized cost is classified as fair value in the

income statement. However company mentions that these do not have material impact on the

business materiality. The carrying amount of account receivables and contractual assets are

decresed by lifetime estimated future credit losses on the date of recognition while earlier the

credit losses were not used to be recognized on such assets. The new IFRS 9 has changed the

requirements of accounting reporting of some assets. However, it do not affect much the

financial reporting of the company.

Answer b

Through successful risk management activities, the company continue to increase its

revenue and generated 7071 million euros in cash from the operating activities in 2019. The

optimum cash generation helped the company to conduct capital improvement plans. It also

distributed a dividend which showed the company’s solvent and healthy position. In addition to

this, in 2019 the company also paid dividend of amount 4022 million euros to keep the interest of

the stakeholders a priority. As per the annual report of the company, there are several factors that

determine the dividend policy of the company. All the dividends paid by Vodafone Corporation

are declared by the company in euros. The dividend payable by the company depends on many

factors such as earnings of the company, liquidity position, financial conditions of the company

etc. the share pricing trends and the consumer developing interest to use digitalization helps to

determine the overall revenue of the Vodafone corporations. The company states that the share

prices may rise or fluctuate by the company’s recent strategic positions of investments in other

businesses. The company mentions that the revenue of the business has gone down by 10%

because it is facing tough competition in the prepaid market. The company fails to develop the

successful planning which can create a competitive advantage and helps the business to deal with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCE

the price competition within the international market. However, company shows in the latest

annual report that it has generated good revenue from the fixed line services. The revenue from

the fixed line services has increased to 12%. The reason behind increasing higher revenue from

these fixed line service is the increase in the customer base which reached to 307000 broadband

consisting of 2.5 million of customers. The company faced tough competition from strong

organic growth and revenue of the company hit by the continuously fluctuating financial market

(Halff, Younes and Boersma 2019).

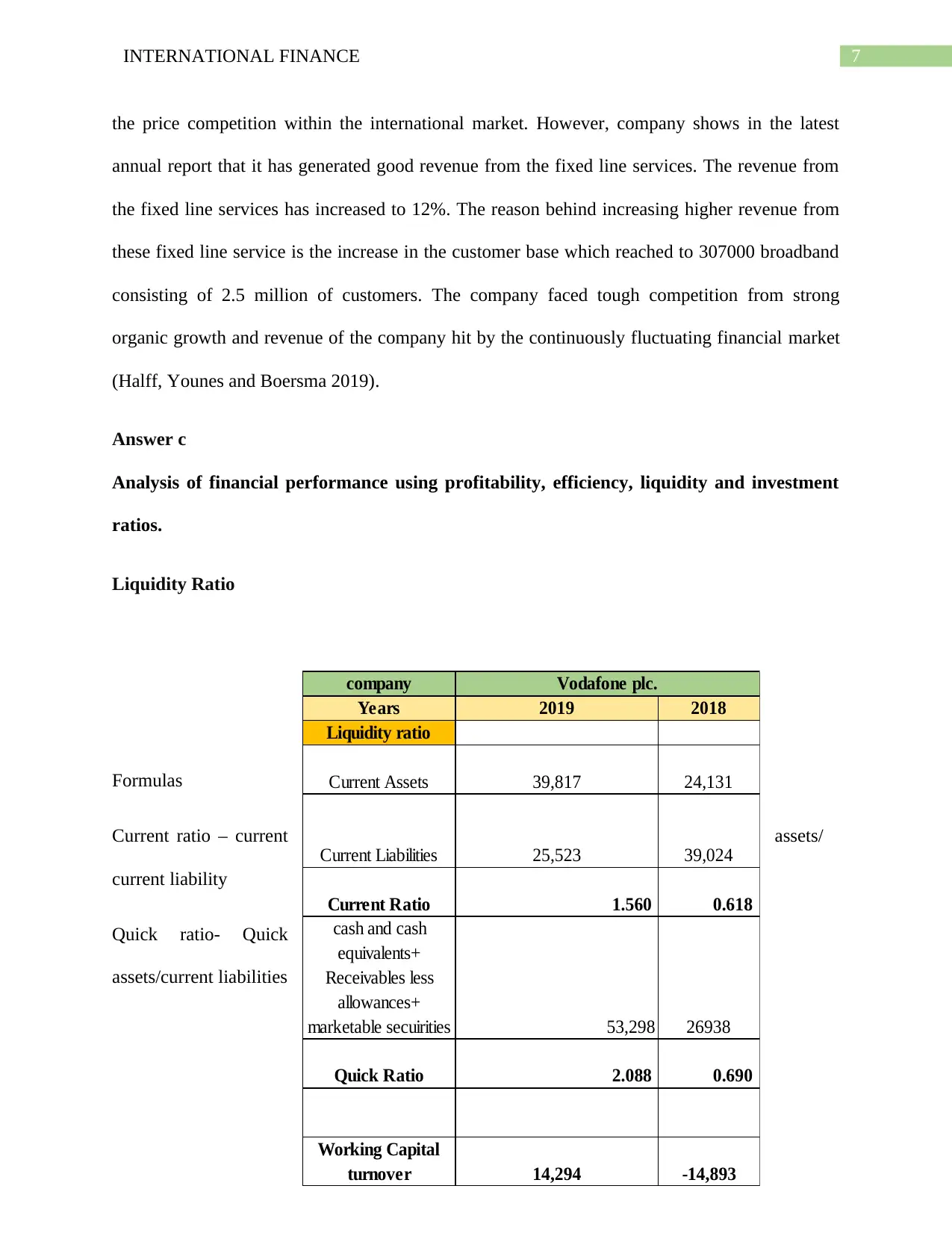

Answer c

Analysis of financial performance using profitability, efficiency, liquidity and investment

ratios.

Liquidity Ratio

Formulas

Current ratio – current assets/

current liability

Quick ratio- Quick

assets/current liabilities

company

Years 2019 2018

Liquidity ratio

Current Assets 39,817 24,131

Current Liabilities 25,523 39,024

Current Ratio 1.560 0.618

cash and cash

equivalents+

Receivables less

allowances+

marketable secuirities 53,298 26938

Quick Ratio 2.088 0.690

Working Capital

turnover 14,294 -14,893

Vodafone plc.

the price competition within the international market. However, company shows in the latest

annual report that it has generated good revenue from the fixed line services. The revenue from

the fixed line services has increased to 12%. The reason behind increasing higher revenue from

these fixed line service is the increase in the customer base which reached to 307000 broadband

consisting of 2.5 million of customers. The company faced tough competition from strong

organic growth and revenue of the company hit by the continuously fluctuating financial market

(Halff, Younes and Boersma 2019).

Answer c

Analysis of financial performance using profitability, efficiency, liquidity and investment

ratios.

Liquidity Ratio

Formulas

Current ratio – current assets/

current liability

Quick ratio- Quick

assets/current liabilities

company

Years 2019 2018

Liquidity ratio

Current Assets 39,817 24,131

Current Liabilities 25,523 39,024

Current Ratio 1.560 0.618

cash and cash

equivalents+

Receivables less

allowances+

marketable secuirities 53,298 26938

Quick Ratio 2.088 0.690

Working Capital

turnover 14,294 -14,893

Vodafone plc.

8INTERNATIONAL FINANCE

Working capital- current assets- current liabilities

The liquidity ratio of the company denotes the amount of liquid assets with the company that

helps the company to deal with the short term obligation and working capital requirements. The

current assets of the company in the year 2019 is at 39817euros million, and the current assets of

the company in the year 2018 is 24131 euros million. The current liabilities of the company is

25523 euros million in the year 2019 and 39024 euros million for the year 2018. The current

ratio calculated by dividing the current assets by current liabilities (Gurr 2018). The current ratio

for the financial year 2019 is 1.560, and for the financial year, 2018 is 0.618. The quick assets of

the company are 53298 euros million for the year 2019 and 26938 euros million for the financial

year 2018. The quick ratio calculated using the financial data available in the latest annual

reports of the company. The quick assets ratio for the FY 2019 is 2.088 and 0.690 in the FY

2018. The working capital of the company in both financial years is showing dissimilar state

which is negative. The working capital of the firm is 14294 euros million in the FY 2019 while

the working capital of the company for the year 2018 is 14893 euros million. The liquid ratio of

the company is equal to1.5 in the financial year 2015, which is equal from the standard current

assets ratio (Farfan et al. 2017). The telecom industry runs on large economies of scale and the

investments of the company are basically in fixed assets like towers and majority expenses are

on the technology. The lower current assets ratio can predict that the company can be in trouble

and facing difficulty in repaying short term debts within 12 months. However, the profitability

ratio is also not showing the company’s financial position as good. The reason for the lower

liquidity ratio in 2018 is the short term assets. The company has optimum short term assets for

paying its liabilities within 12 months. Moreover, it can be said that the current ratio, quick

assets ratio and the working capital has been deteriorated by the previous financial year 2018.

Working capital- current assets- current liabilities

The liquidity ratio of the company denotes the amount of liquid assets with the company that

helps the company to deal with the short term obligation and working capital requirements. The

current assets of the company in the year 2019 is at 39817euros million, and the current assets of

the company in the year 2018 is 24131 euros million. The current liabilities of the company is

25523 euros million in the year 2019 and 39024 euros million for the year 2018. The current

ratio calculated by dividing the current assets by current liabilities (Gurr 2018). The current ratio

for the financial year 2019 is 1.560, and for the financial year, 2018 is 0.618. The quick assets of

the company are 53298 euros million for the year 2019 and 26938 euros million for the financial

year 2018. The quick ratio calculated using the financial data available in the latest annual

reports of the company. The quick assets ratio for the FY 2019 is 2.088 and 0.690 in the FY

2018. The working capital of the company in both financial years is showing dissimilar state

which is negative. The working capital of the firm is 14294 euros million in the FY 2019 while

the working capital of the company for the year 2018 is 14893 euros million. The liquid ratio of

the company is equal to1.5 in the financial year 2015, which is equal from the standard current

assets ratio (Farfan et al. 2017). The telecom industry runs on large economies of scale and the

investments of the company are basically in fixed assets like towers and majority expenses are

on the technology. The lower current assets ratio can predict that the company can be in trouble

and facing difficulty in repaying short term debts within 12 months. However, the profitability

ratio is also not showing the company’s financial position as good. The reason for the lower

liquidity ratio in 2018 is the short term assets. The company has optimum short term assets for

paying its liabilities within 12 months. Moreover, it can be said that the current ratio, quick

assets ratio and the working capital has been deteriorated by the previous financial year 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL FINANCE

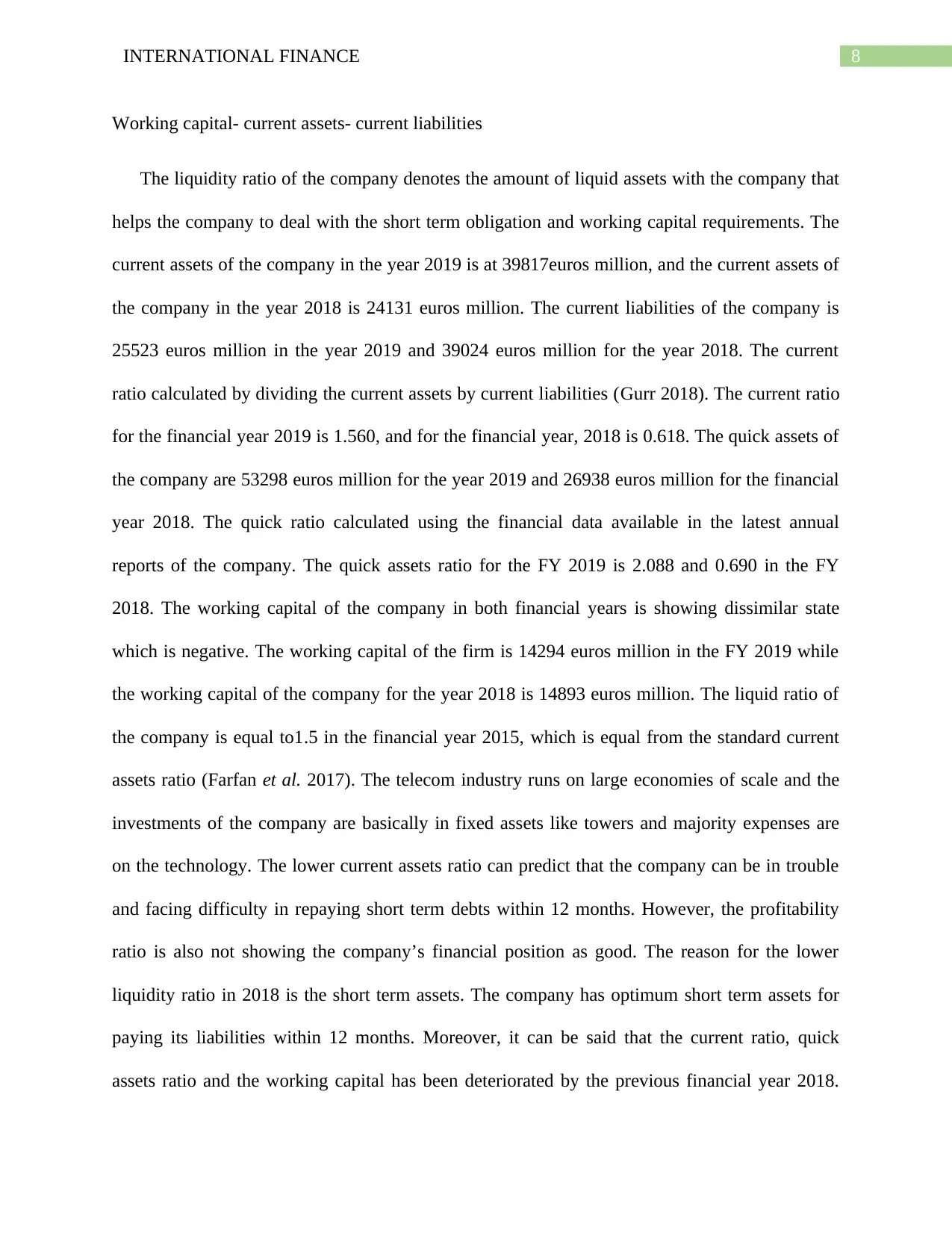

The other competitors of Vodafone plc shows greter liquidity position. This is a trait that the

company has made heavy investments in fixed assets and growth plans (Arkan 2016).

Efficiency Ratio

Account receivable turnover ratio- revenue or net credit sales/ Average account receivables

Average collection period- 365/ Account receivable turnover ratio

Total asset turnover ratio- revenue or net credit sales/ Average total assets

company

Years 2019 2018

Efficiency ratio

Revenue 21,870 23,496

Account Receivables 11,995 9,795

Account Receivable

Turnover Ratio 1.823 2.399

Number of days in

the period 365 365

Average Collection

Period 200.19 152.16

Revenue or net sales 21,870 23,496

Average Total Asset 142,862 145,611

Total Asset

Turnover Ratio 0.15 0.16

Days to sale the

average inventory 2384.30 2262.00

Vodafone Plc.

Account receivable turnover ratio- revenue or net credit sales/ Average account receivables

Average collection period- 365/ Account receivable turnover ratio

Total asset turnover ratio- revenue or net credit sales/ Average total assets

The other competitors of Vodafone plc shows greter liquidity position. This is a trait that the

company has made heavy investments in fixed assets and growth plans (Arkan 2016).

Efficiency Ratio

Account receivable turnover ratio- revenue or net credit sales/ Average account receivables

Average collection period- 365/ Account receivable turnover ratio

Total asset turnover ratio- revenue or net credit sales/ Average total assets

company

Years 2019 2018

Efficiency ratio

Revenue 21,870 23,496

Account Receivables 11,995 9,795

Account Receivable

Turnover Ratio 1.823 2.399

Number of days in

the period 365 365

Average Collection

Period 200.19 152.16

Revenue or net sales 21,870 23,496

Average Total Asset 142,862 145,611

Total Asset

Turnover Ratio 0.15 0.16

Days to sale the

average inventory 2384.30 2262.00

Vodafone Plc.

Account receivable turnover ratio- revenue or net credit sales/ Average account receivables

Average collection period- 365/ Account receivable turnover ratio

Total asset turnover ratio- revenue or net credit sales/ Average total assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNATIONAL FINANCE

The account receivable turnover ratio helps to know how frequently the company is able

to recover the amounts from its debtors with respect to the net credit sales of the company

(Andjelic and Vesic 2017). The Account receivable turnover ratio of the Vodafone Corporation

has declined from the year 2019 to 2018. The account receivable turnover ratio of the financial

year 2019 was 1.823, while the account receivable turnover ratio for the financial year 2018 was

2.399 approx. However, the average collection period has improved from the previous year

average collection period. The ratio was 200.19 in the financial year 2019 while it was 152.162

in the FY 2018. The asset turnover ratio of the company helps the investors know how efficiently

the company is utilizing its assets to generate sales. The higher turnover ratio shows that the

company is efficient in utilizing its assets. The total asset turnover ratio has improved from the

financial year 2018 to 2019. It shows Vodafone Corporation has efficiently utilized its current

assets as well as fixed assets efficiently (www.vodafone.com 2020).

Profitability Ratio

Formula

Gross profit – (gross profit/ net sales)*100

Operating profit – (operating profit/ net sales)*100

ROA (%)- (net income / average total assets)*100

ROE (%) – (net income/ total shareholders’ equity)*100

The account receivable turnover ratio helps to know how frequently the company is able

to recover the amounts from its debtors with respect to the net credit sales of the company

(Andjelic and Vesic 2017). The Account receivable turnover ratio of the Vodafone Corporation

has declined from the year 2019 to 2018. The account receivable turnover ratio of the financial

year 2019 was 1.823, while the account receivable turnover ratio for the financial year 2018 was

2.399 approx. However, the average collection period has improved from the previous year

average collection period. The ratio was 200.19 in the financial year 2019 while it was 152.162

in the FY 2018. The asset turnover ratio of the company helps the investors know how efficiently

the company is utilizing its assets to generate sales. The higher turnover ratio shows that the

company is efficient in utilizing its assets. The total asset turnover ratio has improved from the

financial year 2018 to 2019. It shows Vodafone Corporation has efficiently utilized its current

assets as well as fixed assets efficiently (www.vodafone.com 2020).

Profitability Ratio

Formula

Gross profit – (gross profit/ net sales)*100

Operating profit – (operating profit/ net sales)*100

ROA (%)- (net income / average total assets)*100

ROE (%) – (net income/ total shareholders’ equity)*100

11INTERNATIONAL FINANCE

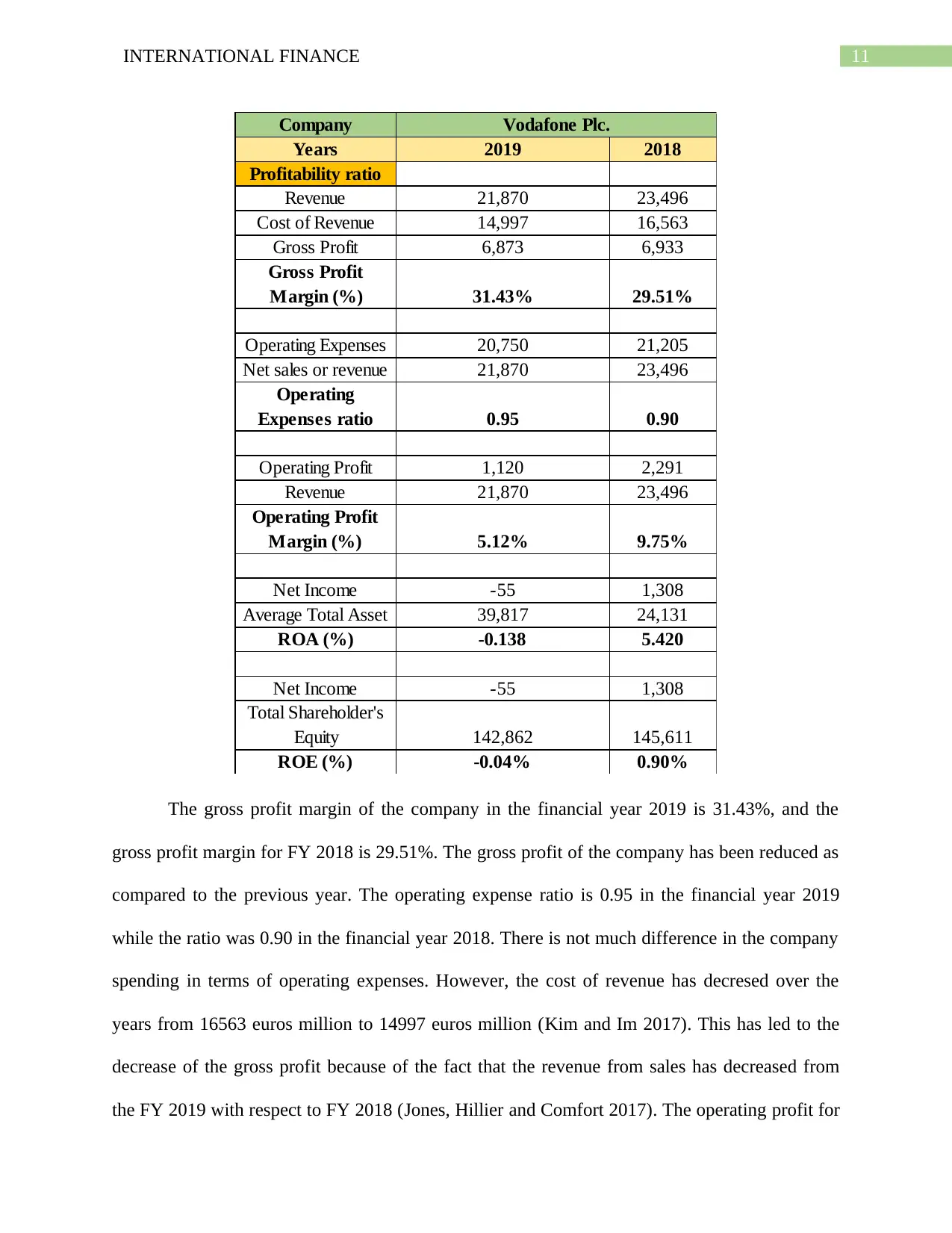

Company

Years 2019 2018

Profitability ratio

Revenue 21,870 23,496

Cost of Revenue 14,997 16,563

Gross Profit 6,873 6,933

Gross Profit

Margin (%) 31.43% 29.51%

Operating Expenses 20,750 21,205

Net sales or revenue 21,870 23,496

Operating

Expenses ratio 0.95 0.90

Operating Profit 1,120 2,291

Revenue 21,870 23,496

Operating Profit

Margin (%) 5.12% 9.75%

Net Income -55 1,308

Average Total Asset 39,817 24,131

ROA (%) -0.138 5.420

Net Income -55 1,308

Total Shareholder's

Equity 142,862 145,611

ROE (%) -0.04% 0.90%

Vodafone Plc.

The gross profit margin of the company in the financial year 2019 is 31.43%, and the

gross profit margin for FY 2018 is 29.51%. The gross profit of the company has been reduced as

compared to the previous year. The operating expense ratio is 0.95 in the financial year 2019

while the ratio was 0.90 in the financial year 2018. There is not much difference in the company

spending in terms of operating expenses. However, the cost of revenue has decresed over the

years from 16563 euros million to 14997 euros million (Kim and Im 2017). This has led to the

decrease of the gross profit because of the fact that the revenue from sales has decreased from

the FY 2019 with respect to FY 2018 (Jones, Hillier and Comfort 2017). The operating profit for

Company

Years 2019 2018

Profitability ratio

Revenue 21,870 23,496

Cost of Revenue 14,997 16,563

Gross Profit 6,873 6,933

Gross Profit

Margin (%) 31.43% 29.51%

Operating Expenses 20,750 21,205

Net sales or revenue 21,870 23,496

Operating

Expenses ratio 0.95 0.90

Operating Profit 1,120 2,291

Revenue 21,870 23,496

Operating Profit

Margin (%) 5.12% 9.75%

Net Income -55 1,308

Average Total Asset 39,817 24,131

ROA (%) -0.138 5.420

Net Income -55 1,308

Total Shareholder's

Equity 142,862 145,611

ROE (%) -0.04% 0.90%

Vodafone Plc.

The gross profit margin of the company in the financial year 2019 is 31.43%, and the

gross profit margin for FY 2018 is 29.51%. The gross profit of the company has been reduced as

compared to the previous year. The operating expense ratio is 0.95 in the financial year 2019

while the ratio was 0.90 in the financial year 2018. There is not much difference in the company

spending in terms of operating expenses. However, the cost of revenue has decresed over the

years from 16563 euros million to 14997 euros million (Kim and Im 2017). This has led to the

decrease of the gross profit because of the fact that the revenue from sales has decreased from

the FY 2019 with respect to FY 2018 (Jones, Hillier and Comfort 2017). The operating profit for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.