International Financial Management Report: Financial Analysis

VerifiedAdded on 2022/12/15

|16

|2847

|338

Report

AI Summary

This report delves into the core concepts of international financial management (IFM), exploring topics such as expected Net Present Value (NPV), standard deviation of NPV, and Internal Rate of Return (IRR). The report analyzes financial decisions within an international context, including capital budgeting, risk management, and the impact of privatization on financial performance. It examines cash flow analysis, probability of avoiding liquidation, and the ranking of investment projects based on financial metrics. The analysis incorporates numerical examples and calculations to illustrate key concepts and provide insights into making informed financial decisions. The report also compares and contrasts NPV and IRR, and calculates the probability of negative NPV under varying conditions. This report serves as a comprehensive guide to understanding and applying IFM principles.

International Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3......................................................................................................................................10

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3......................................................................................................................................10

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION

Main objective of this report is to understand the concept of international financial

management which is also known as the international finance. It is related to the management of

finance in an international business environment. Main objective of international finance

management is to maximize the shareholders wealth (Andreeva and et. al. 2018). An

international finance manager will require to effectively study the concept of exchange rate and

currency markets, various risk such as political, exchange rate risk, interest rate risk, various risk

management techniques, cost of capital and capital budgeting in international context, working

capital management, balance of payment and so on. With the increase in globalization

entrepreneurs are free to operate their business in any corner of world (Shapiro and Hanouna,

2019). There are various factors which play an important role in international finance

management such as cross-boarder sharing, multi-currency shares, currency swaps, foreign

mutual funds and so on. This report includes various aspects of financial management through

different numeric task such as expected NPV, standard deviation of NPV, Net present value and

internal rate of return.

MAIN BODY

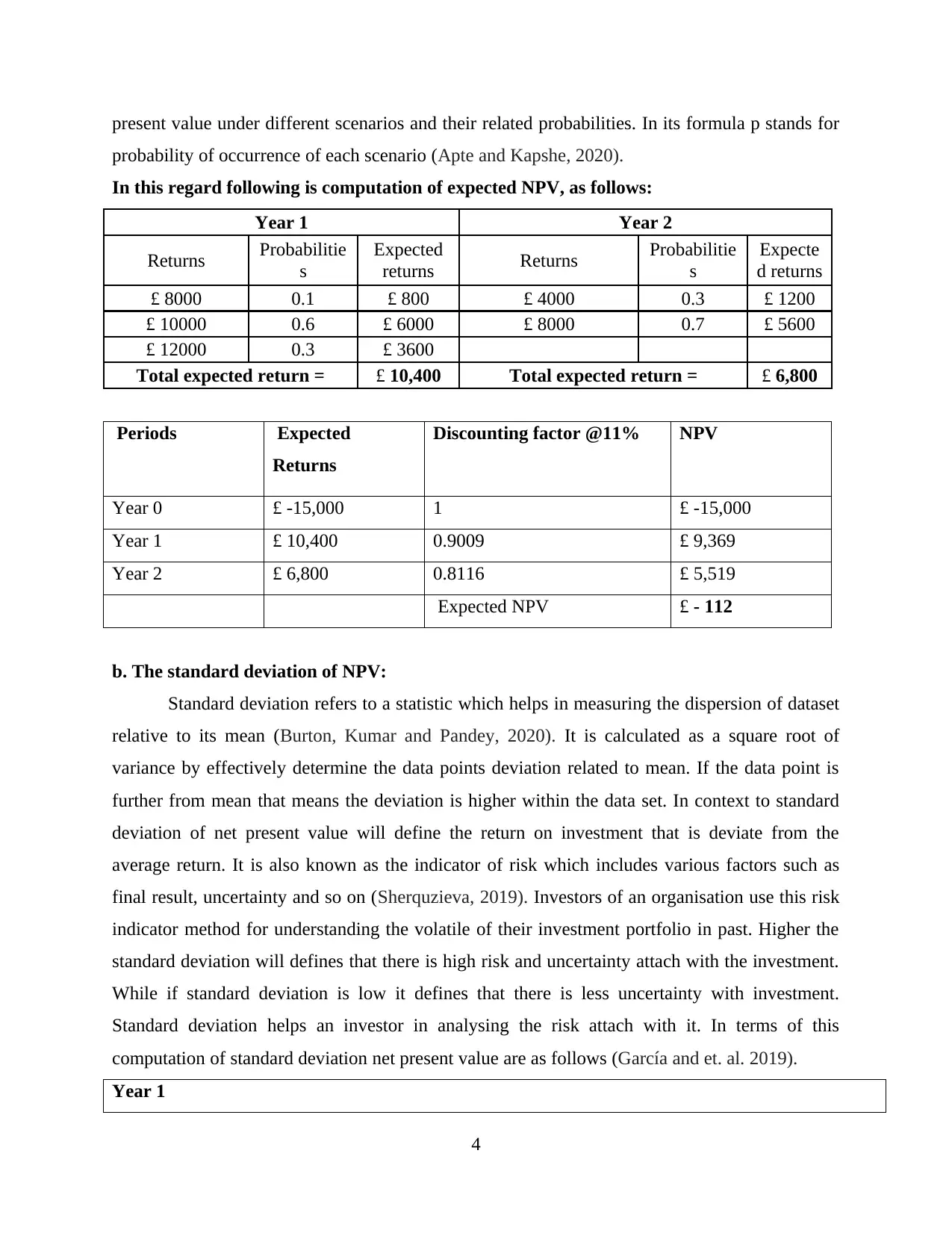

Question 1

a. The expected NPV:

Expected net present value refers to a capital budgeting technique which helps in

adjusting uncertainty and effectively calculating the net present value under various different

situations and profitability (Angrick, 2018). It helps in predicting future outcome and it provide

more accurate result as compare to traditional NPV method. It is a method of capital budget

which provide effective weightage for identifying the best net present value. It is a method which

is used for effective finance analysis which determine the feasibility of investment in a particular

project or business. This define the present value of future cash flow as compared to initial

investment of investors. In this method instead of depending on a single net present value

company calculate NPV under different situations such as best case, worst case, base case,

estimated profit of each scenario, weights of NPV are calculated according to related

probabilities and the expected NPV is find out. Expected NPV is the sum of total products of net

3

Main objective of this report is to understand the concept of international financial

management which is also known as the international finance. It is related to the management of

finance in an international business environment. Main objective of international finance

management is to maximize the shareholders wealth (Andreeva and et. al. 2018). An

international finance manager will require to effectively study the concept of exchange rate and

currency markets, various risk such as political, exchange rate risk, interest rate risk, various risk

management techniques, cost of capital and capital budgeting in international context, working

capital management, balance of payment and so on. With the increase in globalization

entrepreneurs are free to operate their business in any corner of world (Shapiro and Hanouna,

2019). There are various factors which play an important role in international finance

management such as cross-boarder sharing, multi-currency shares, currency swaps, foreign

mutual funds and so on. This report includes various aspects of financial management through

different numeric task such as expected NPV, standard deviation of NPV, Net present value and

internal rate of return.

MAIN BODY

Question 1

a. The expected NPV:

Expected net present value refers to a capital budgeting technique which helps in

adjusting uncertainty and effectively calculating the net present value under various different

situations and profitability (Angrick, 2018). It helps in predicting future outcome and it provide

more accurate result as compare to traditional NPV method. It is a method of capital budget

which provide effective weightage for identifying the best net present value. It is a method which

is used for effective finance analysis which determine the feasibility of investment in a particular

project or business. This define the present value of future cash flow as compared to initial

investment of investors. In this method instead of depending on a single net present value

company calculate NPV under different situations such as best case, worst case, base case,

estimated profit of each scenario, weights of NPV are calculated according to related

probabilities and the expected NPV is find out. Expected NPV is the sum of total products of net

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

present value under different scenarios and their related probabilities. In its formula p stands for

probability of occurrence of each scenario (Apte and Kapshe, 2020).

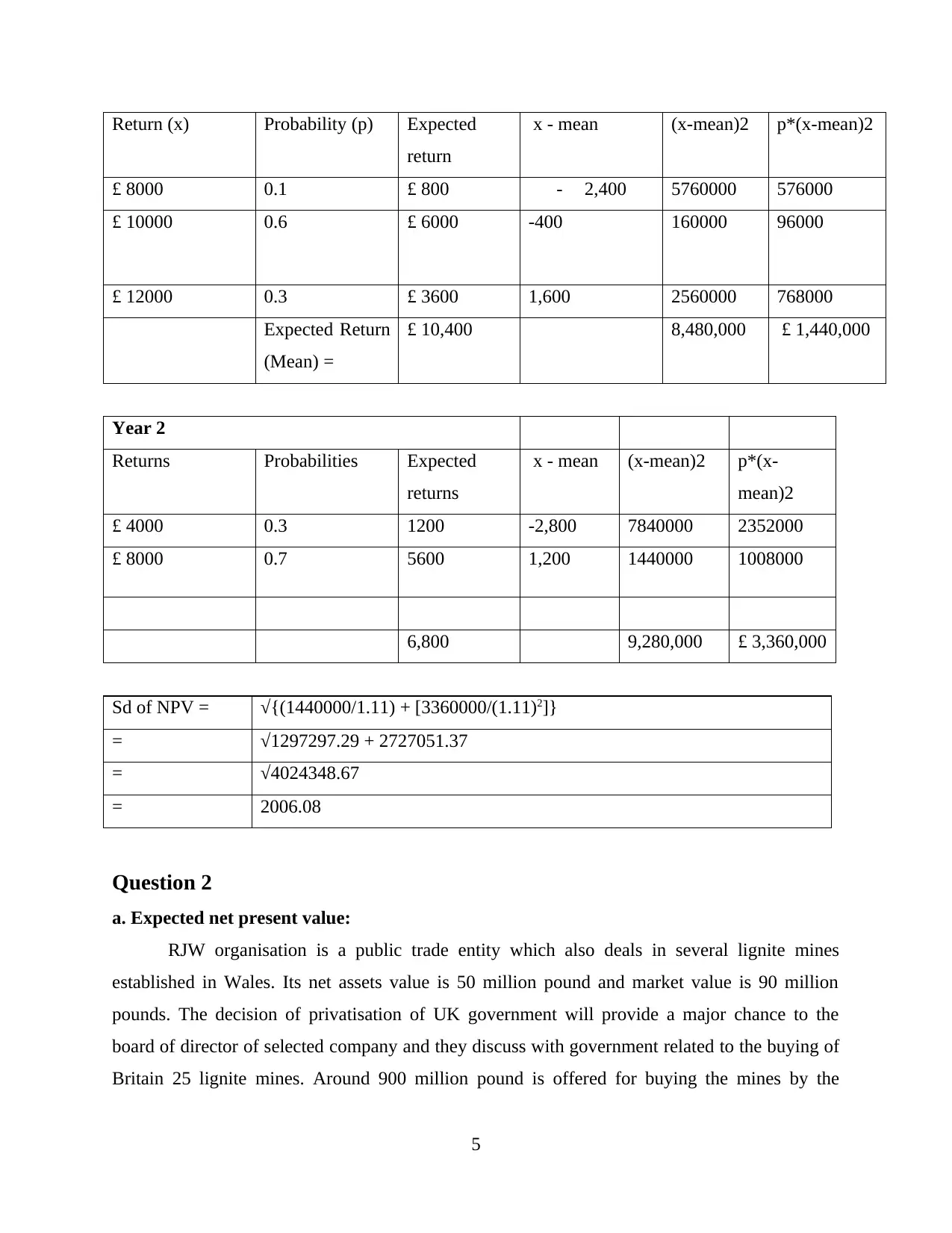

In this regard following is computation of expected NPV, as follows:

Year 1 Year 2

Returns Probabilitie

s

Expected

returns Returns Probabilitie

s

Expecte

d returns

£ 8000 0.1 £ 800 £ 4000 0.3 £ 1200

£ 10000 0.6 £ 6000 £ 8000 0.7 £ 5600

£ 12000 0.3 £ 3600

Total expected return = £ 10,400 Total expected return = £ 6,800

Periods Expected

Returns

Discounting factor @11% NPV

Year 0 £ -15,000 1 £ -15,000

Year 1 £ 10,400 0.9009 £ 9,369

Year 2 £ 6,800 0.8116 £ 5,519

Expected NPV £ - 112

b. The standard deviation of NPV:

Standard deviation refers to a statistic which helps in measuring the dispersion of dataset

relative to its mean (Burton, Kumar and Pandey, 2020). It is calculated as a square root of

variance by effectively determine the data points deviation related to mean. If the data point is

further from mean that means the deviation is higher within the data set. In context to standard

deviation of net present value will define the return on investment that is deviate from the

average return. It is also known as the indicator of risk which includes various factors such as

final result, uncertainty and so on (Sherquzieva, 2019). Investors of an organisation use this risk

indicator method for understanding the volatile of their investment portfolio in past. Higher the

standard deviation will defines that there is high risk and uncertainty attach with the investment.

While if standard deviation is low it defines that there is less uncertainty with investment.

Standard deviation helps an investor in analysing the risk attach with it. In terms of this

computation of standard deviation net present value are as follows (García and et. al. 2019).

Year 1

4

probability of occurrence of each scenario (Apte and Kapshe, 2020).

In this regard following is computation of expected NPV, as follows:

Year 1 Year 2

Returns Probabilitie

s

Expected

returns Returns Probabilitie

s

Expecte

d returns

£ 8000 0.1 £ 800 £ 4000 0.3 £ 1200

£ 10000 0.6 £ 6000 £ 8000 0.7 £ 5600

£ 12000 0.3 £ 3600

Total expected return = £ 10,400 Total expected return = £ 6,800

Periods Expected

Returns

Discounting factor @11% NPV

Year 0 £ -15,000 1 £ -15,000

Year 1 £ 10,400 0.9009 £ 9,369

Year 2 £ 6,800 0.8116 £ 5,519

Expected NPV £ - 112

b. The standard deviation of NPV:

Standard deviation refers to a statistic which helps in measuring the dispersion of dataset

relative to its mean (Burton, Kumar and Pandey, 2020). It is calculated as a square root of

variance by effectively determine the data points deviation related to mean. If the data point is

further from mean that means the deviation is higher within the data set. In context to standard

deviation of net present value will define the return on investment that is deviate from the

average return. It is also known as the indicator of risk which includes various factors such as

final result, uncertainty and so on (Sherquzieva, 2019). Investors of an organisation use this risk

indicator method for understanding the volatile of their investment portfolio in past. Higher the

standard deviation will defines that there is high risk and uncertainty attach with the investment.

While if standard deviation is low it defines that there is less uncertainty with investment.

Standard deviation helps an investor in analysing the risk attach with it. In terms of this

computation of standard deviation net present value are as follows (García and et. al. 2019).

Year 1

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Return (x) Probability (p) Expected

return

x - mean (x-mean)2 p*(x-mean)2

£ 8000 0.1 £ 800 - 2,400 5760000 576000

£ 10000 0.6 £ 6000 -400 160000 96000

£ 12000 0.3 £ 3600 1,600 2560000 768000

Expected Return

(Mean) =

£ 10,400 8,480,000 £ 1,440,000

Year 2

Returns Probabilities Expected

returns

x - mean (x-mean)2 p*(x-

mean)2

£ 4000 0.3 1200 -2,800 7840000 2352000

£ 8000 0.7 5600 1,200 1440000 1008000

6,800 9,280,000 £ 3,360,000

Sd of NPV = √{(1440000/1.11) + [3360000/(1.11)2]}

= √1297297.29 + 2727051.37

= √4024348.67

= 2006.08

Question 2

a. Expected net present value:

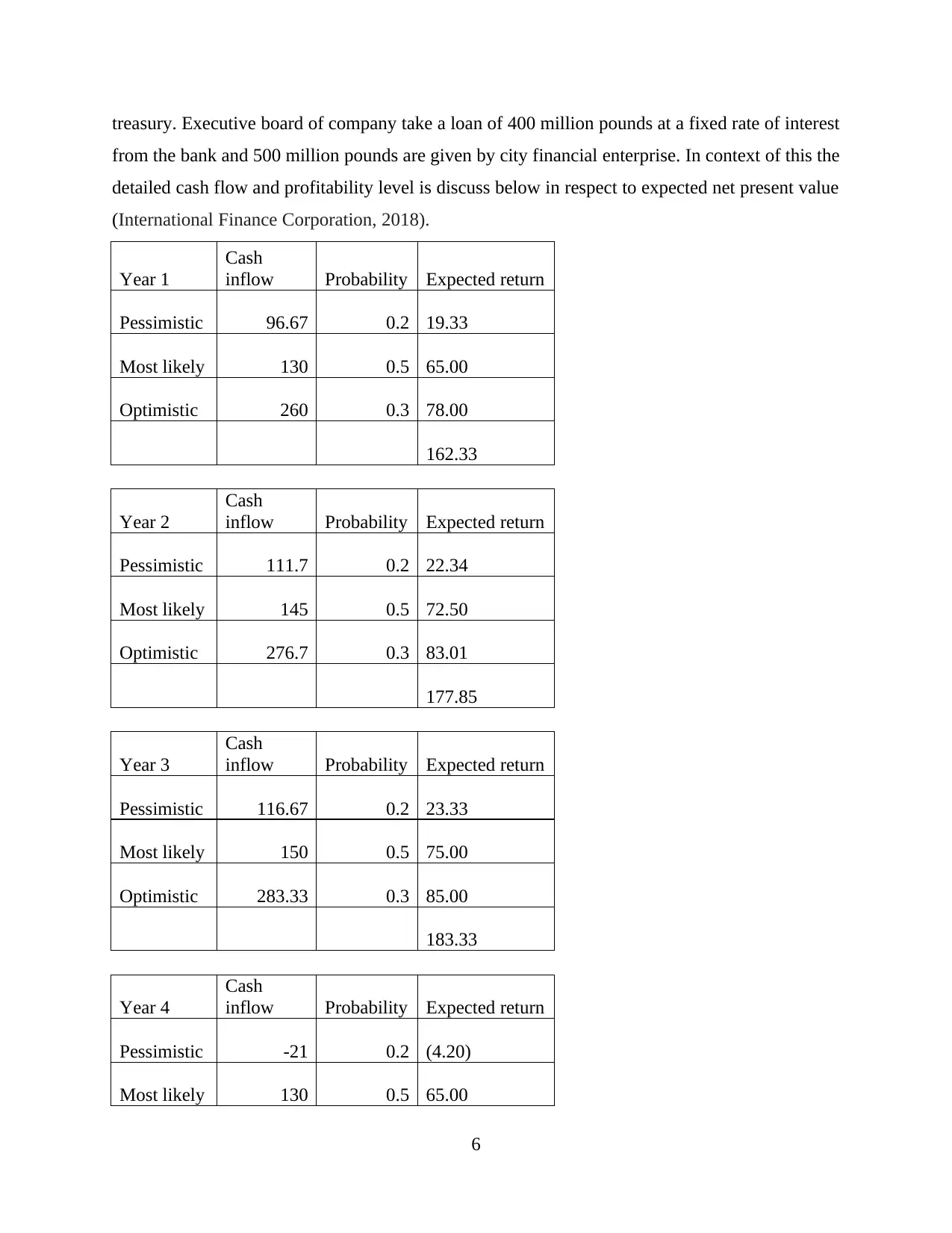

RJW organisation is a public trade entity which also deals in several lignite mines

established in Wales. Its net assets value is 50 million pound and market value is 90 million

pounds. The decision of privatisation of UK government will provide a major chance to the

board of director of selected company and they discuss with government related to the buying of

Britain 25 lignite mines. Around 900 million pound is offered for buying the mines by the

5

return

x - mean (x-mean)2 p*(x-mean)2

£ 8000 0.1 £ 800 - 2,400 5760000 576000

£ 10000 0.6 £ 6000 -400 160000 96000

£ 12000 0.3 £ 3600 1,600 2560000 768000

Expected Return

(Mean) =

£ 10,400 8,480,000 £ 1,440,000

Year 2

Returns Probabilities Expected

returns

x - mean (x-mean)2 p*(x-

mean)2

£ 4000 0.3 1200 -2,800 7840000 2352000

£ 8000 0.7 5600 1,200 1440000 1008000

6,800 9,280,000 £ 3,360,000

Sd of NPV = √{(1440000/1.11) + [3360000/(1.11)2]}

= √1297297.29 + 2727051.37

= √4024348.67

= 2006.08

Question 2

a. Expected net present value:

RJW organisation is a public trade entity which also deals in several lignite mines

established in Wales. Its net assets value is 50 million pound and market value is 90 million

pounds. The decision of privatisation of UK government will provide a major chance to the

board of director of selected company and they discuss with government related to the buying of

Britain 25 lignite mines. Around 900 million pound is offered for buying the mines by the

5

treasury. Executive board of company take a loan of 400 million pounds at a fixed rate of interest

from the bank and 500 million pounds are given by city financial enterprise. In context of this the

detailed cash flow and profitability level is discuss below in respect to expected net present value

(International Finance Corporation, 2018).

Year 1

Cash

inflow Probability Expected return

Pessimistic 96.67 0.2 19.33

Most likely 130 0.5 65.00

Optimistic 260 0.3 78.00

162.33

Year 2

Cash

inflow Probability Expected return

Pessimistic 111.7 0.2 22.34

Most likely 145 0.5 72.50

Optimistic 276.7 0.3 83.01

177.85

Year 3

Cash

inflow Probability Expected return

Pessimistic 116.67 0.2 23.33

Most likely 150 0.5 75.00

Optimistic 283.33 0.3 85.00

183.33

Year 4

Cash

inflow Probability Expected return

Pessimistic -21 0.2 (4.20)

Most likely 130 0.5 65.00

6

from the bank and 500 million pounds are given by city financial enterprise. In context of this the

detailed cash flow and profitability level is discuss below in respect to expected net present value

(International Finance Corporation, 2018).

Year 1

Cash

inflow Probability Expected return

Pessimistic 96.67 0.2 19.33

Most likely 130 0.5 65.00

Optimistic 260 0.3 78.00

162.33

Year 2

Cash

inflow Probability Expected return

Pessimistic 111.7 0.2 22.34

Most likely 145 0.5 72.50

Optimistic 276.7 0.3 83.01

177.85

Year 3

Cash

inflow Probability Expected return

Pessimistic 116.67 0.2 23.33

Most likely 150 0.5 75.00

Optimistic 283.33 0.3 85.00

183.33

Year 4

Cash

inflow Probability Expected return

Pessimistic -21 0.2 (4.20)

Most likely 130 0.5 65.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

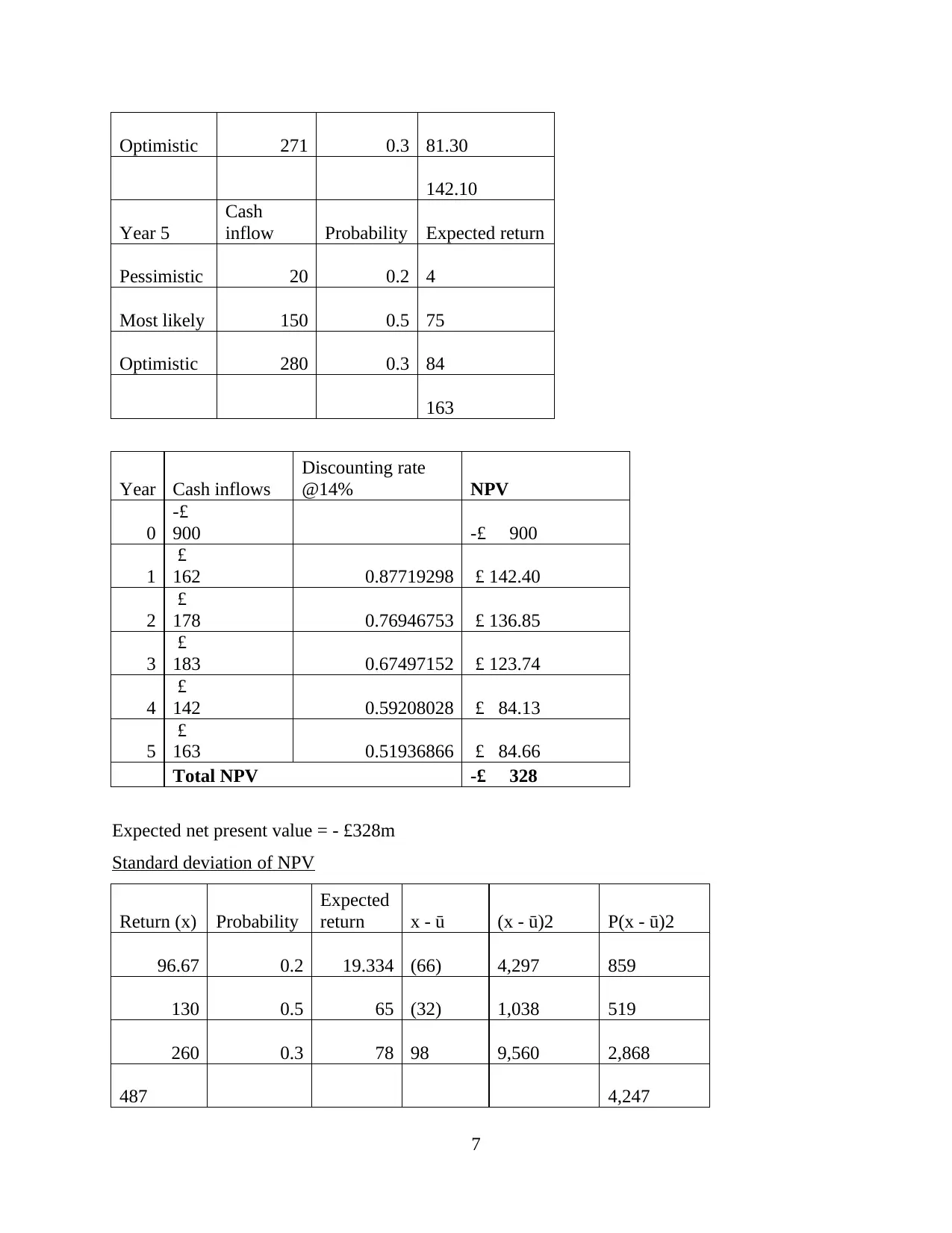

Optimistic 271 0.3 81.30

142.10

Year 5

Cash

inflow Probability Expected return

Pessimistic 20 0.2 4

Most likely 150 0.5 75

Optimistic 280 0.3 84

163

Year Cash inflows

Discounting rate

@14% NPV

0

-£

900 -£ 900

1

£

162 0.87719298 £ 142.40

2

£

178 0.76946753 £ 136.85

3

£

183 0.67497152 £ 123.74

4

£

142 0.59208028 £ 84.13

5

£

163 0.51936866 £ 84.66

Total NPV -£ 328

Expected net present value = - £328m

Standard deviation of NPV

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

7

142.10

Year 5

Cash

inflow Probability Expected return

Pessimistic 20 0.2 4

Most likely 150 0.5 75

Optimistic 280 0.3 84

163

Year Cash inflows

Discounting rate

@14% NPV

0

-£

900 -£ 900

1

£

162 0.87719298 £ 142.40

2

£

178 0.76946753 £ 136.85

3

£

183 0.67497152 £ 123.74

4

£

142 0.59208028 £ 84.13

5

£

163 0.51936866 £ 84.66

Total NPV -£ 328

Expected net present value = - £328m

Standard deviation of NPV

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

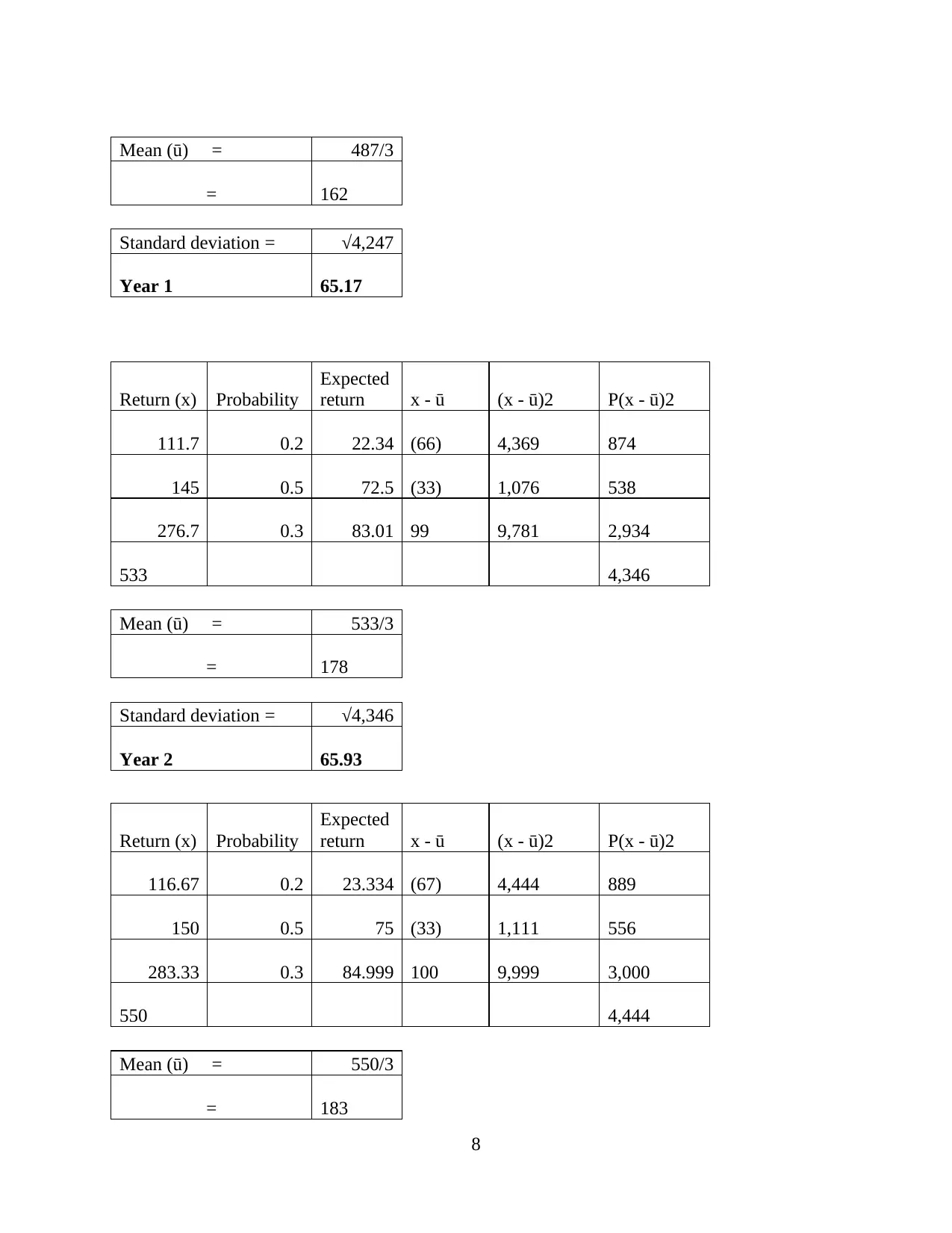

Mean (ū) = 487/3

= 162

Standard deviation = √4,247

Year 1 65.17

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

8

= 162

Standard deviation = √4,247

Year 1 65.17

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

8

Standard deviation = √4,444

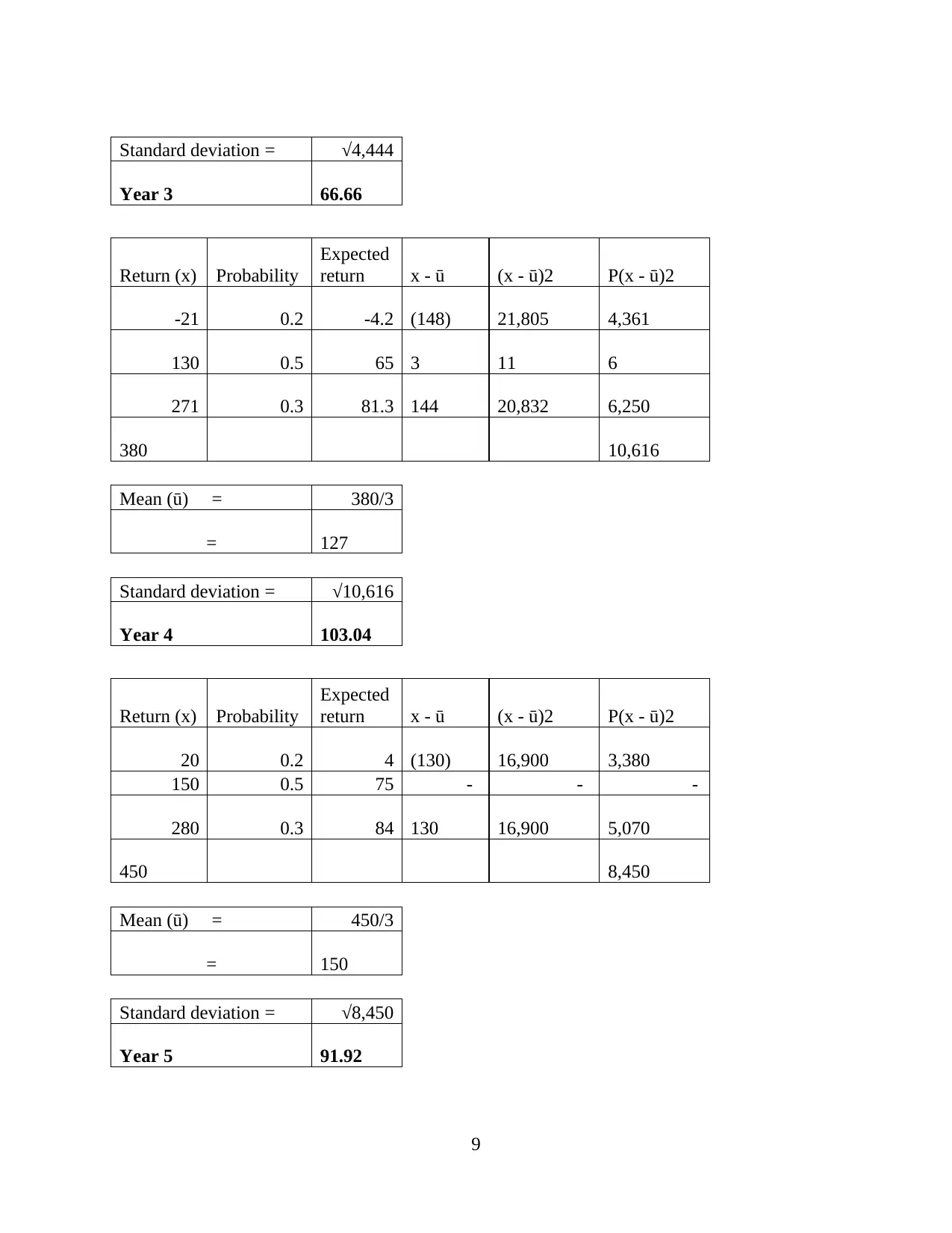

Year 3 66.66

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

9

Year 3 66.66

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

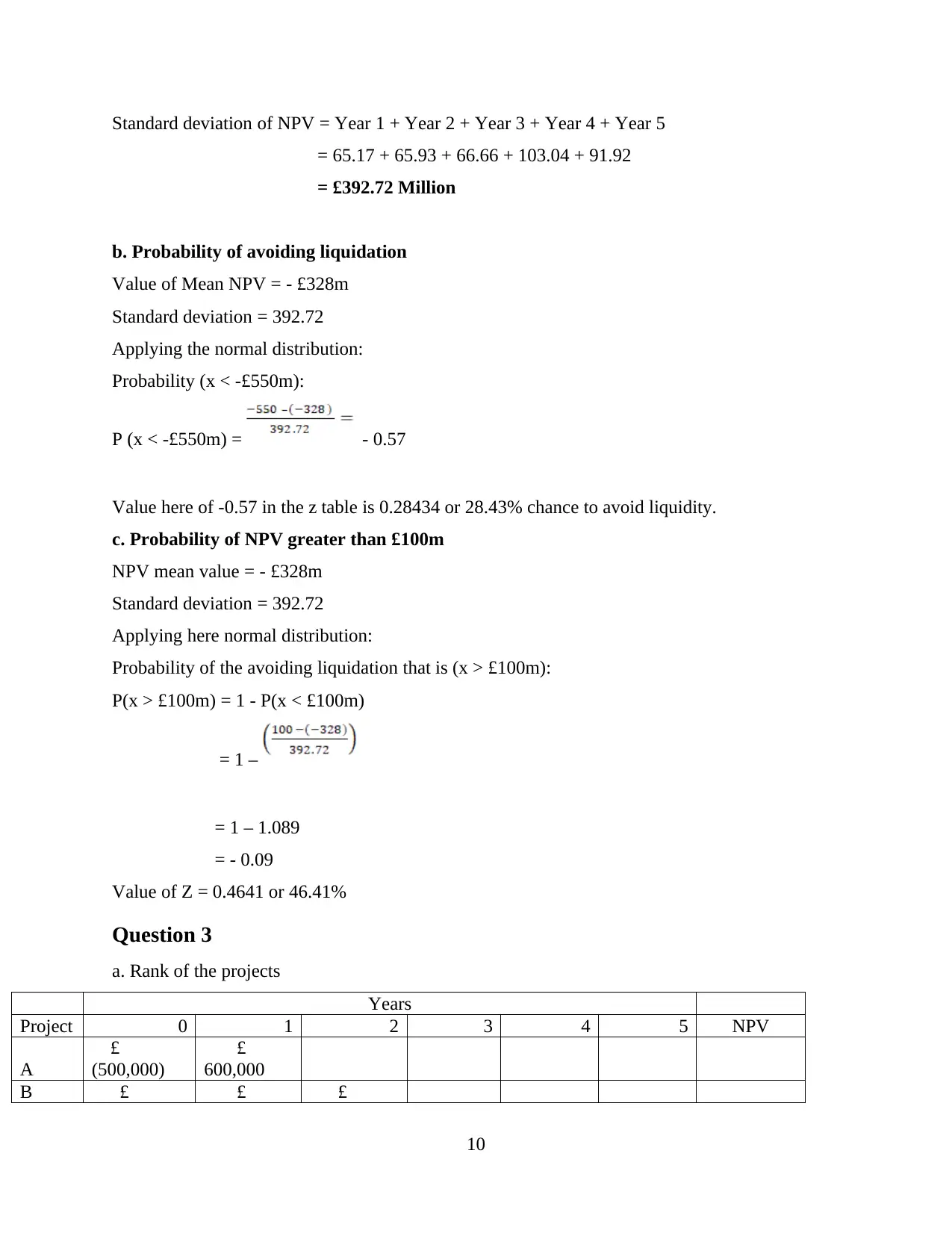

Standard deviation of NPV = Year 1 + Year 2 + Year 3 + Year 4 + Year 5

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

b. Probability of avoiding liquidation

Value of Mean NPV = - £328m

Standard deviation = 392.72

Applying the normal distribution:

Probability (x < -£550m):

P (x < -£550m) = - 0.57

Value here of -0.57 in the z table is 0.28434 or 28.43% chance to avoid liquidity.

c. Probability of NPV greater than £100m

NPV mean value = - £328m

Standard deviation = 392.72

Applying here normal distribution:

Probability of the avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 –

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Question 3

a. Rank of the projects

Years

Project 0 1 2 3 4 5 NPV

A

£

(500,000)

£

600,000

B £ £ £

10

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

b. Probability of avoiding liquidation

Value of Mean NPV = - £328m

Standard deviation = 392.72

Applying the normal distribution:

Probability (x < -£550m):

P (x < -£550m) = - 0.57

Value here of -0.57 in the z table is 0.28434 or 28.43% chance to avoid liquidity.

c. Probability of NPV greater than £100m

NPV mean value = - £328m

Standard deviation = 392.72

Applying here normal distribution:

Probability of the avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 –

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Question 3

a. Rank of the projects

Years

Project 0 1 2 3 4 5 NPV

A

£

(500,000)

£

600,000

B £ £ £

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(200,000) 200,000 150,000

C £ (700,000)

£

100,000

D

£

(150,000)

£

60,000

£

60,000

£

60,000

£

60,000

£

60,000

Discou

nt

factor

@10% 0.90909091 0.82644628

0.751314

8 0.6830135 0.6209213

A

£

(500,000)

£

545,454.55

£

45,455

B

£

(200,000)

£

181,818.18

£

123,966.94

£

105,785

C

£

(700,000)

£

82,644.63

£

(617,355)

D

£

(150,000)

£

54,545.45

£

49,586.78

£

45,078.89

£

40,980.81

£

37,255.28

£

77,447

Ranks Project NPV

1 B £ 105,785

2 D £ 77,447

3 A £ 45,455

4 C £ (617,355)

b. Net present value vs. internal rate of return

NPV refer to the difference between the present value of cash inflows and the present value of

cash outflow in a specific period of time (Maxfield, 2019). By contrast, IRR refers to a

calculation which helps in estimating the profitability of the potential investment. Both the

methods are used in capital budgeting (Schmidpete and et. al. 2019). It refers to a process

through which company effectively analysis where they can make investment. For determining

net present value a company needs to analysis its cash flow of project and discount them from

the present value amount with the help of using a discount rate which represent the project cost

of capital and risk. Than whole investment future positive cash flow is reduces from the present

value number and subtracting it from the initial cash outlay required for investment. While

internal rate of return is determine by simply recalculating the NPV equation and this time the

11

C £ (700,000)

£

100,000

D

£

(150,000)

£

60,000

£

60,000

£

60,000

£

60,000

£

60,000

Discou

nt

factor

@10% 0.90909091 0.82644628

0.751314

8 0.6830135 0.6209213

A

£

(500,000)

£

545,454.55

£

45,455

B

£

(200,000)

£

181,818.18

£

123,966.94

£

105,785

C

£

(700,000)

£

82,644.63

£

(617,355)

D

£

(150,000)

£

54,545.45

£

49,586.78

£

45,078.89

£

40,980.81

£

37,255.28

£

77,447

Ranks Project NPV

1 B £ 105,785

2 D £ 77,447

3 A £ 45,455

4 C £ (617,355)

b. Net present value vs. internal rate of return

NPV refer to the difference between the present value of cash inflows and the present value of

cash outflow in a specific period of time (Maxfield, 2019). By contrast, IRR refers to a

calculation which helps in estimating the profitability of the potential investment. Both the

methods are used in capital budgeting (Schmidpete and et. al. 2019). It refers to a process

through which company effectively analysis where they can make investment. For determining

net present value a company needs to analysis its cash flow of project and discount them from

the present value amount with the help of using a discount rate which represent the project cost

of capital and risk. Than whole investment future positive cash flow is reduces from the present

value number and subtracting it from the initial cash outlay required for investment. While

internal rate of return is determine by simply recalculating the NPV equation and this time the

11

NPV factor is set as zero and solved with the discount rate. The rate which is produces from the

solution is the rate of return (Tan and et. al. 2018).

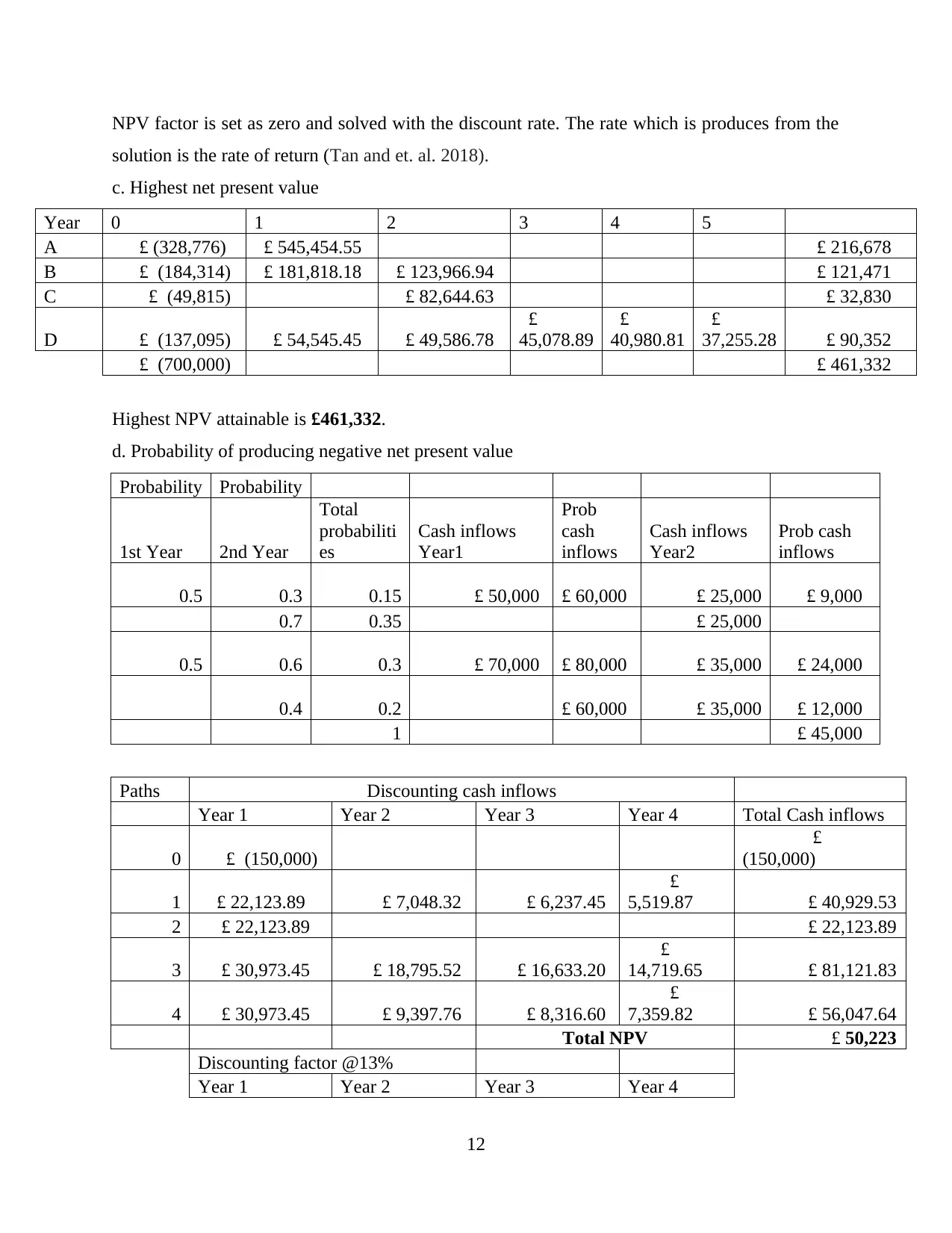

c. Highest net present value

Year 0 1 2 3 4 5

A £ (328,776) £ 545,454.55 £ 216,678

B £ (184,314) £ 181,818.18 £ 123,966.94 £ 121,471

C £ (49,815) £ 82,644.63 £ 32,830

D £ (137,095) £ 54,545.45 £ 49,586.78

£

45,078.89

£

40,980.81

£

37,255.28 £ 90,352

£ (700,000) £ 461,332

Highest NPV attainable is £461,332.

d. Probability of producing negative net present value

Probability Probability

1st Year 2nd Year

Total

probabiliti

es

Cash inflows

Year1

Prob

cash

inflows

Cash inflows

Year2

Prob cash

inflows

0.5 0.3 0.15 £ 50,000 £ 60,000 £ 25,000 £ 9,000

0.7 0.35 £ 25,000

0.5 0.6 0.3 £ 70,000 £ 80,000 £ 35,000 £ 24,000

0.4 0.2 £ 60,000 £ 35,000 £ 12,000

1 £ 45,000

Paths Discounting cash inflows

Year 1 Year 2 Year 3 Year 4 Total Cash inflows

0 £ (150,000)

£

(150,000)

1 £ 22,123.89 £ 7,048.32 £ 6,237.45

£

5,519.87 £ 40,929.53

2 £ 22,123.89 £ 22,123.89

3 £ 30,973.45 £ 18,795.52 £ 16,633.20

£

14,719.65 £ 81,121.83

4 £ 30,973.45 £ 9,397.76 £ 8,316.60

£

7,359.82 £ 56,047.64

Total NPV £ 50,223

Discounting factor @13%

Year 1 Year 2 Year 3 Year 4

12

solution is the rate of return (Tan and et. al. 2018).

c. Highest net present value

Year 0 1 2 3 4 5

A £ (328,776) £ 545,454.55 £ 216,678

B £ (184,314) £ 181,818.18 £ 123,966.94 £ 121,471

C £ (49,815) £ 82,644.63 £ 32,830

D £ (137,095) £ 54,545.45 £ 49,586.78

£

45,078.89

£

40,980.81

£

37,255.28 £ 90,352

£ (700,000) £ 461,332

Highest NPV attainable is £461,332.

d. Probability of producing negative net present value

Probability Probability

1st Year 2nd Year

Total

probabiliti

es

Cash inflows

Year1

Prob

cash

inflows

Cash inflows

Year2

Prob cash

inflows

0.5 0.3 0.15 £ 50,000 £ 60,000 £ 25,000 £ 9,000

0.7 0.35 £ 25,000

0.5 0.6 0.3 £ 70,000 £ 80,000 £ 35,000 £ 24,000

0.4 0.2 £ 60,000 £ 35,000 £ 12,000

1 £ 45,000

Paths Discounting cash inflows

Year 1 Year 2 Year 3 Year 4 Total Cash inflows

0 £ (150,000)

£

(150,000)

1 £ 22,123.89 £ 7,048.32 £ 6,237.45

£

5,519.87 £ 40,929.53

2 £ 22,123.89 £ 22,123.89

3 £ 30,973.45 £ 18,795.52 £ 16,633.20

£

14,719.65 £ 81,121.83

4 £ 30,973.45 £ 9,397.76 £ 8,316.60

£

7,359.82 £ 56,047.64

Total NPV £ 50,223

Discounting factor @13%

Year 1 Year 2 Year 3 Year 4

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.