International Financial Management Analysis Report

VerifiedAdded on 2022/12/09

|18

|3576

|54

Report

AI Summary

This report delves into the core concepts of international financial management, offering a comprehensive analysis of investment strategies and risk assessment. It begins by calculating the expected net present value (NPV) and standard deviation of a project, evaluating its profitability and associated risks. The report then assesses the feasibility of acquiring English lignite mines, determining the expected NPV, standard deviation, and probabilities of avoiding liquidation and achieving positive returns. Furthermore, it compares the NPV of different projects, explaining the superiority of NPV over the internal rate of return (IRR) for investment appraisal, and calculates the highest achievable NPV under resource constraints. The report concludes by examining the probability of a product generating a negative NPV, providing a thorough examination of financial decision-making under uncertainty.

International Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

QUESTION 1..................................................................................................................................3

(a) Calculation of expected net present value..............................................................................3

(b) Calculation of standard deviation of NPV.............................................................................4

QUESTION 2..................................................................................................................................5

(a) Calculation of expected NPV and standard deviation of the NPV for the project to buy

English lignite mines...................................................................................................................5

(b) Calculation of probability of avoiding liquidation.................................................................8

(c) Calculation of probability of occurring..................................................................................9

QUESTION 3..................................................................................................................................9

(a) Calculation of Net Present Value of each project on the assumption that the cash flows are

not subject to any risk..................................................................................................................9

(b) Reason of why NPV is being superior to internal rate of return for investment appraisal. .11

(c) Calculation of Highest Net Present Value achievable on the assumption that each project is

divisible......................................................................................................................................12

(d) Calculation of probability of the product producing a negative net present value..............13

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

QUESTION 1..................................................................................................................................3

(a) Calculation of expected net present value..............................................................................3

(b) Calculation of standard deviation of NPV.............................................................................4

QUESTION 2..................................................................................................................................5

(a) Calculation of expected NPV and standard deviation of the NPV for the project to buy

English lignite mines...................................................................................................................5

(b) Calculation of probability of avoiding liquidation.................................................................8

(c) Calculation of probability of occurring..................................................................................9

QUESTION 3..................................................................................................................................9

(a) Calculation of Net Present Value of each project on the assumption that the cash flows are

not subject to any risk..................................................................................................................9

(b) Reason of why NPV is being superior to internal rate of return for investment appraisal. .11

(c) Calculation of Highest Net Present Value achievable on the assumption that each project is

divisible......................................................................................................................................12

(d) Calculation of probability of the product producing a negative net present value..............13

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION

Financial management is the part of the business if they want to run their company smoothly

and efficiently. Financial decision is the decision which became impossible to change if the

manages take such decision in a wrong way. The loses the company need to bear may be to that

extent that the company might dissolve their business. So, this report will cover the concept of

expected return the company can expects from their investment plans and the probability of

losing the amount. The report also covers the standard deviation concept which need the

attention of company and their managers which making any finance related decision.

MAIN BODY

QUESTION 1

(a) Calculation of expected net present value

Initial cash outlay = 15000

Year 1

Returns Probability Expected value

8000 0.1 800

(8000* .1)

10000 0.6 6000

(10000* .6)

12000 0.3 3600

(12000* .3)

Expected value of returns

in year 1

10400

Year 2

Returns Probability Expected value

4000 0.3 1200

(4000* .3)

8000 0.7 5600

(8000* .7)

Financial management is the part of the business if they want to run their company smoothly

and efficiently. Financial decision is the decision which became impossible to change if the

manages take such decision in a wrong way. The loses the company need to bear may be to that

extent that the company might dissolve their business. So, this report will cover the concept of

expected return the company can expects from their investment plans and the probability of

losing the amount. The report also covers the standard deviation concept which need the

attention of company and their managers which making any finance related decision.

MAIN BODY

QUESTION 1

(a) Calculation of expected net present value

Initial cash outlay = 15000

Year 1

Returns Probability Expected value

8000 0.1 800

(8000* .1)

10000 0.6 6000

(10000* .6)

12000 0.3 3600

(12000* .3)

Expected value of returns

in year 1

10400

Year 2

Returns Probability Expected value

4000 0.3 1200

(4000* .3)

8000 0.7 5600

(8000* .7)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected value of

returns in year 1

6800

Present value of cash inflows in year 1 = 10400 / [ 1/ (1+11%) ^ 1] = 9369.36

Present Value of cash inflows in year 2 = 6800 / [ 1/ (1+11%) ^ 2] = 5521.6

Present value of cash inflows = 14891

Net present value of the project = present value of cash inflows – initial cash outlay

= 14891 - 15000

= (109).

Interpretation: From the above calculation it is interpretate that the net present value of the

project is negative. And it is stated that if a company want to earn profit on their investment, they

have to select those projects only that have positive expected net present value. Here, the present

value of the cash inflow is less than the initial cash outlay. That’s why it is advisable to the

company that they should reject this project (Attridge and Engen, 2019).

(b) Calculation of standard deviation of NPV

The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of σ2 = σ = 1200.

Interpretation: The above calculation clearly indicates that the standard deviation of the net

present value of year one is 1200. And this means that cash flow the different events are

returns in year 1

6800

Present value of cash inflows in year 1 = 10400 / [ 1/ (1+11%) ^ 1] = 9369.36

Present Value of cash inflows in year 2 = 6800 / [ 1/ (1+11%) ^ 2] = 5521.6

Present value of cash inflows = 14891

Net present value of the project = present value of cash inflows – initial cash outlay

= 14891 - 15000

= (109).

Interpretation: From the above calculation it is interpretate that the net present value of the

project is negative. And it is stated that if a company want to earn profit on their investment, they

have to select those projects only that have positive expected net present value. Here, the present

value of the cash inflow is less than the initial cash outlay. That’s why it is advisable to the

company that they should reject this project (Attridge and Engen, 2019).

(b) Calculation of standard deviation of NPV

The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of σ2 = σ = 1200.

Interpretation: The above calculation clearly indicates that the standard deviation of the net

present value of year one is 1200. And this means that cash flow the different events are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deviating and it is happening because of the expected return by 1200 in the year 1 (Han, K. M.,

Park and Lee, 2020).

Year 2

Returns (X) Returns (X) Returns (X) Returns (X) Returns (X)

4000 4000 4000 4000 4000

8000 8000 8000 8000 8000

Variance of returns in year 2 = σ2 Variance of

returns in year 2

= σ2

Year 2 Year 2

Standard deviation of returns in year 2 = square root of σ2 = σ = 1833.

Interpretation: In the year 2, the standard deviation of expected return from the different event

is 1833. This interpretate that the deviation between the cash flow and expected return of the

year 2 is with the value of 1833 (MOLONEY, 2018).

QUESTION 2

(a) Calculation of expected NPV and standard deviation of the NPV for the project to buy

English lignite mines

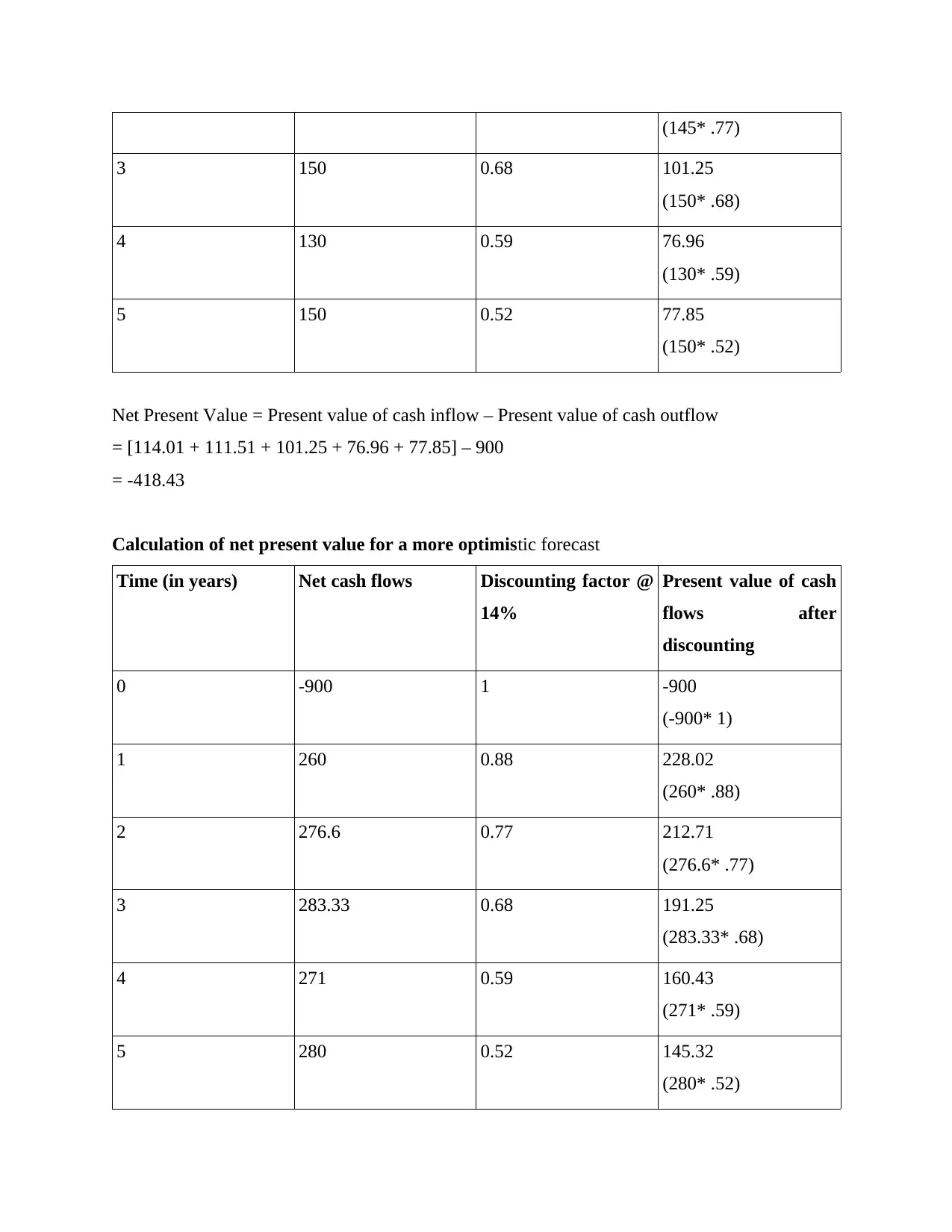

Calculation of net present value of RJW's estimates

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 130 0.88 114.01

(130* .88)

2 145 0.77 111.51

Park and Lee, 2020).

Year 2

Returns (X) Returns (X) Returns (X) Returns (X) Returns (X)

4000 4000 4000 4000 4000

8000 8000 8000 8000 8000

Variance of returns in year 2 = σ2 Variance of

returns in year 2

= σ2

Year 2 Year 2

Standard deviation of returns in year 2 = square root of σ2 = σ = 1833.

Interpretation: In the year 2, the standard deviation of expected return from the different event

is 1833. This interpretate that the deviation between the cash flow and expected return of the

year 2 is with the value of 1833 (MOLONEY, 2018).

QUESTION 2

(a) Calculation of expected NPV and standard deviation of the NPV for the project to buy

English lignite mines

Calculation of net present value of RJW's estimates

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 130 0.88 114.01

(130* .88)

2 145 0.77 111.51

(145* .77)

3 150 0.68 101.25

(150* .68)

4 130 0.59 76.96

(130* .59)

5 150 0.52 77.85

(150* .52)

Net Present Value = Present value of cash inflow – Present value of cash outflow

= [114.01 + 111.51 + 101.25 + 76.96 + 77.85] – 900

= -418.43

Calculation of net present value for a more optimistic forecast

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 260 0.88 228.02

(260* .88)

2 276.6 0.77 212.71

(276.6* .77)

3 283.33 0.68 191.25

(283.33* .68)

4 271 0.59 160.43

(271* .59)

5 280 0.52 145.32

(280* .52)

3 150 0.68 101.25

(150* .68)

4 130 0.59 76.96

(130* .59)

5 150 0.52 77.85

(150* .52)

Net Present Value = Present value of cash inflow – Present value of cash outflow

= [114.01 + 111.51 + 101.25 + 76.96 + 77.85] – 900

= -418.43

Calculation of net present value for a more optimistic forecast

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 260 0.88 228.02

(260* .88)

2 276.6 0.77 212.71

(276.6* .77)

3 283.33 0.68 191.25

(283.33* .68)

4 271 0.59 160.43

(271* .59)

5 280 0.52 145.32

(280* .52)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Present Value = Present value of cash inflow – Present value of cash outflow

= [228.02 + 212.71 + 191.25 + 160.43 + 145.32] – 900

= 37.73

Calculation of net present value for a pessimistic forecast

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 96.67 0.88 84.78

(96.67* .88)

2 111.7 0.77 85.9

(111.7* .77)

3 116.67 0.68 78.75

(116.67* .68)

4 -21 0.59 -12.43

(-21* .59)

5 20 0.52 10.38

(20* .52)

Net Present Value = Present value of cash inflow – Present value of cash outflow

= [84.78 + 85.9 + 78.75 + (12.43) + 10.38] – 900

= -652.62

Calculation of expected NPV

Net Present Value Probability Expected value

-418.43 50% -209.21

= [228.02 + 212.71 + 191.25 + 160.43 + 145.32] – 900

= 37.73

Calculation of net present value for a pessimistic forecast

Time (in years) Net cash flows Discounting factor @

14%

Present value of cash

flows after

discounting

0 -900 1 -900

(-900* 1)

1 96.67 0.88 84.78

(96.67* .88)

2 111.7 0.77 85.9

(111.7* .77)

3 116.67 0.68 78.75

(116.67* .68)

4 -21 0.59 -12.43

(-21* .59)

5 20 0.52 10.38

(20* .52)

Net Present Value = Present value of cash inflow – Present value of cash outflow

= [84.78 + 85.9 + 78.75 + (12.43) + 10.38] – 900

= -652.62

Calculation of expected NPV

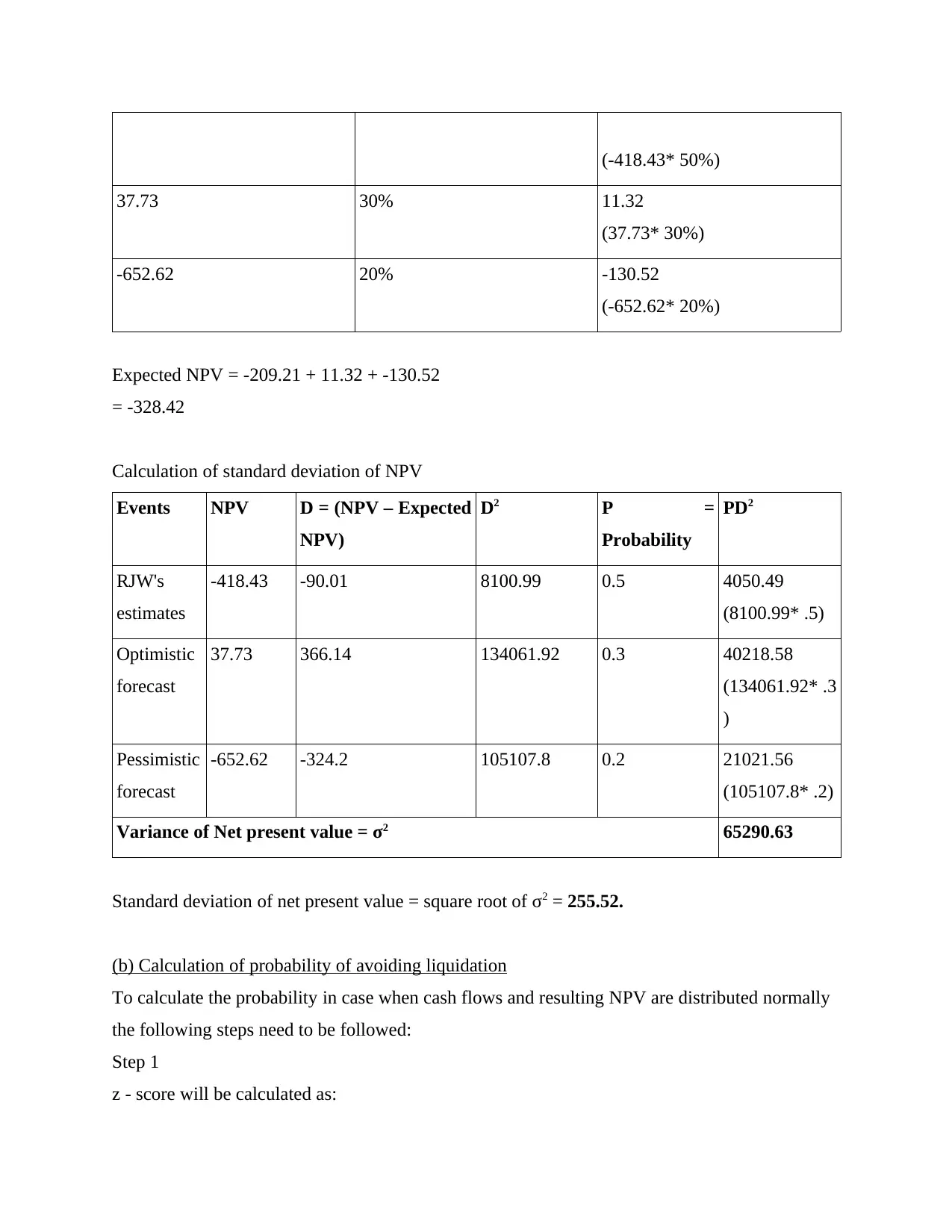

Net Present Value Probability Expected value

-418.43 50% -209.21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(-418.43* 50%)

37.73 30% 11.32

(37.73* 30%)

-652.62 20% -130.52

(-652.62* 20%)

Expected NPV = -209.21 + 11.32 + -130.52

= -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

(8100.99* .5)

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

(134061.92* .3

)

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

(105107.8* .2)

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

(b) Calculation of probability of avoiding liquidation

To calculate the probability in case when cash flows and resulting NPV are distributed normally

the following steps need to be followed:

Step 1

z - score will be calculated as:

37.73 30% 11.32

(37.73* 30%)

-652.62 20% -130.52

(-652.62* 20%)

Expected NPV = -209.21 + 11.32 + -130.52

= -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

(8100.99* .5)

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

(134061.92* .3

)

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

(105107.8* .2)

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

(b) Calculation of probability of avoiding liquidation

To calculate the probability in case when cash flows and resulting NPV are distributed normally

the following steps need to be followed:

Step 1

z - score will be calculated as:

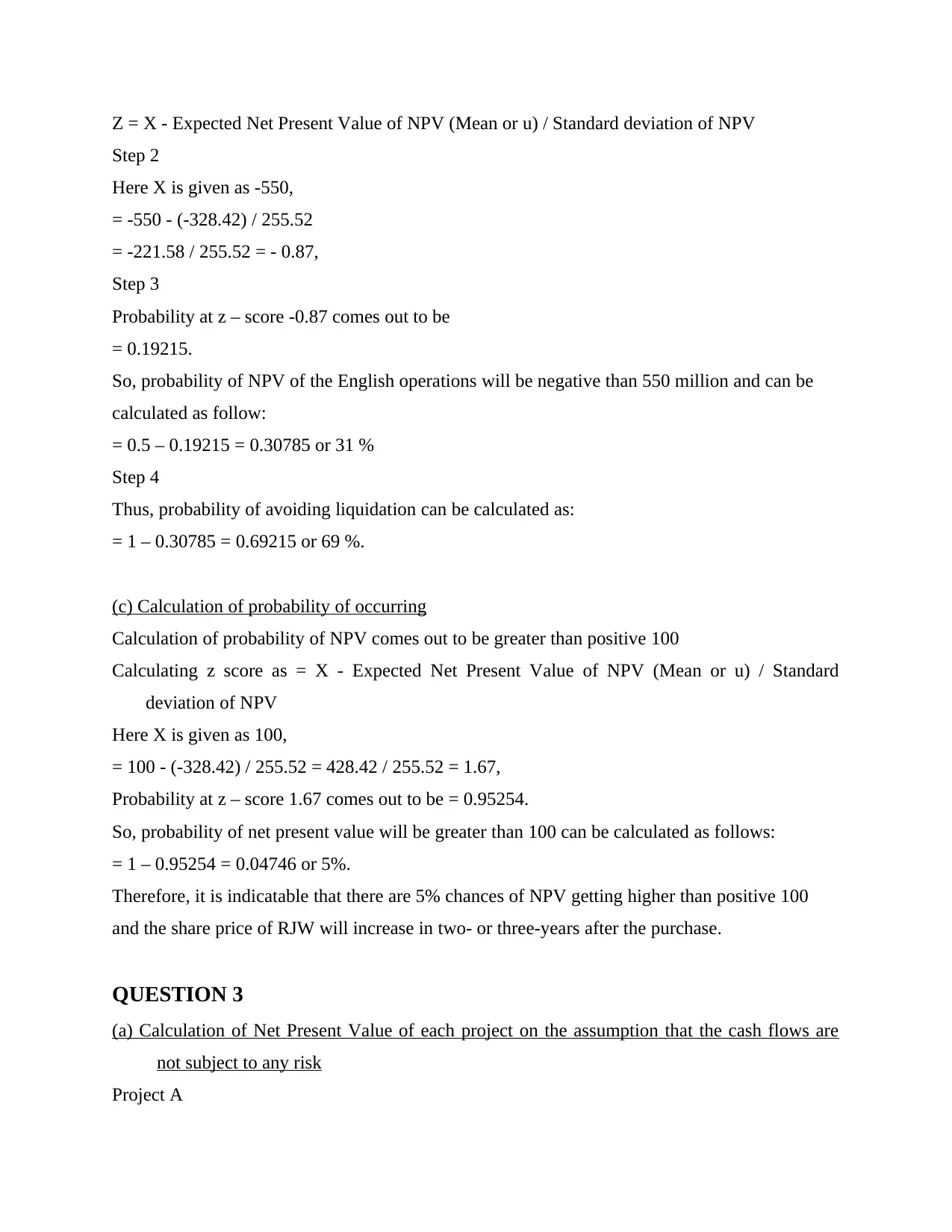

Z = X - Expected Net Present Value of NPV (Mean or u) / Standard deviation of NPV

Step 2

Here X is given as -550,

= -550 - (-328.42) / 255.52

= -221.58 / 255.52 = - 0.87,

Step 3

Probability at z – score -0.87 comes out to be

= 0.19215.

So, probability of NPV of the English operations will be negative than 550 million and can be

calculated as follow:

= 0.5 – 0.19215 = 0.30785 or 31 %

Step 4

Thus, probability of avoiding liquidation can be calculated as:

= 1 – 0.30785 = 0.69215 or 69 %.

(c) Calculation of probability of occurring

Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, it is indicatable that there are 5% chances of NPV getting higher than positive 100

and the share price of RJW will increase in two- or three-years after the purchase.

QUESTION 3

(a) Calculation of Net Present Value of each project on the assumption that the cash flows are

not subject to any risk

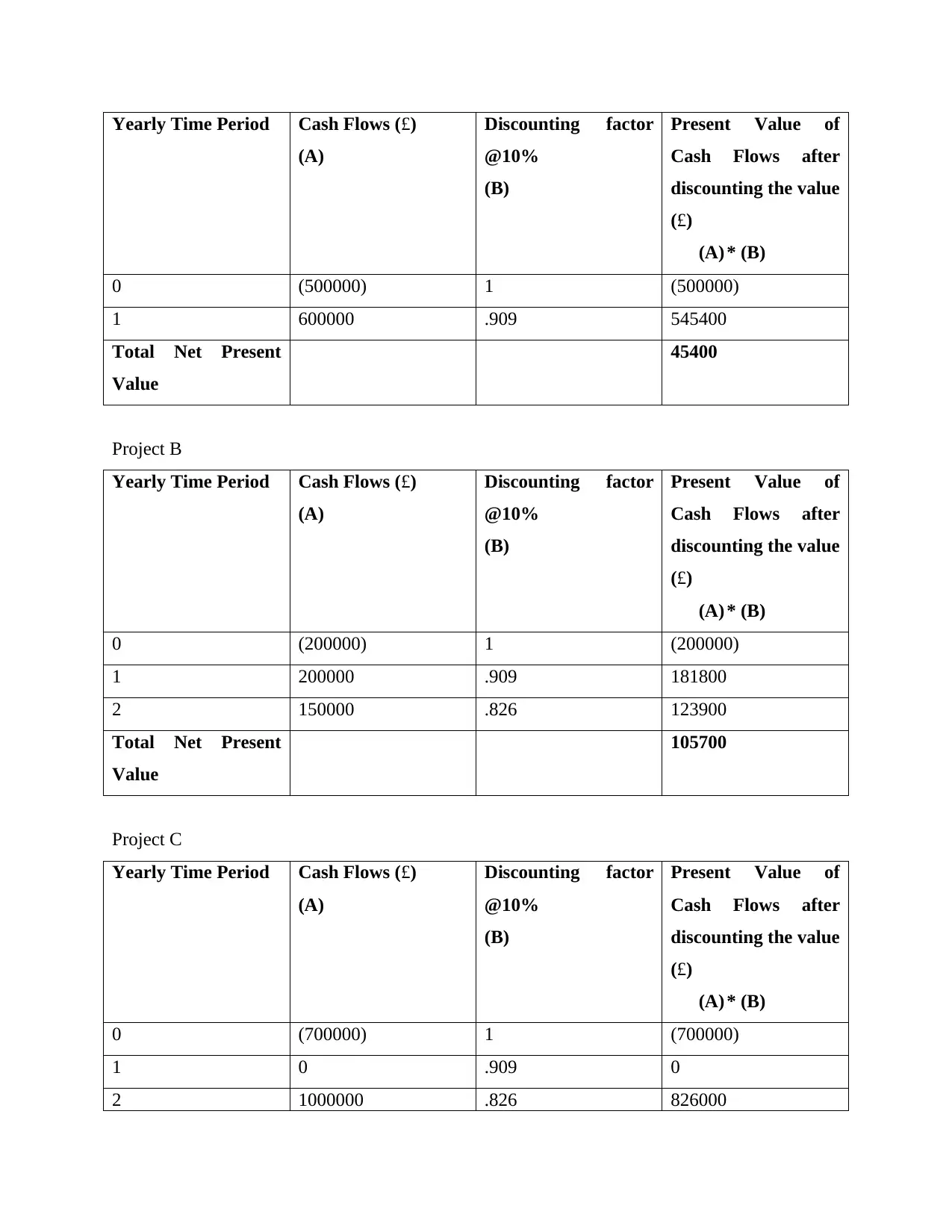

Project A

Step 2

Here X is given as -550,

= -550 - (-328.42) / 255.52

= -221.58 / 255.52 = - 0.87,

Step 3

Probability at z – score -0.87 comes out to be

= 0.19215.

So, probability of NPV of the English operations will be negative than 550 million and can be

calculated as follow:

= 0.5 – 0.19215 = 0.30785 or 31 %

Step 4

Thus, probability of avoiding liquidation can be calculated as:

= 1 – 0.30785 = 0.69215 or 69 %.

(c) Calculation of probability of occurring

Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, it is indicatable that there are 5% chances of NPV getting higher than positive 100

and the share price of RJW will increase in two- or three-years after the purchase.

QUESTION 3

(a) Calculation of Net Present Value of each project on the assumption that the cash flows are

not subject to any risk

Project A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (500000) 1 (500000)

1 600000 .909 545400

Total Net Present

Value

45400

Project B

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (200000) 1 (200000)

1 200000 .909 181800

2 150000 .826 123900

Total Net Present

Value

105700

Project C

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (700000) 1 (700000)

1 0 .909 0

2 1000000 .826 826000

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (500000) 1 (500000)

1 600000 .909 545400

Total Net Present

Value

45400

Project B

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (200000) 1 (200000)

1 200000 .909 181800

2 150000 .826 123900

Total Net Present

Value

105700

Project C

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (700000) 1 (700000)

1 0 .909 0

2 1000000 .826 826000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Net Present

Value

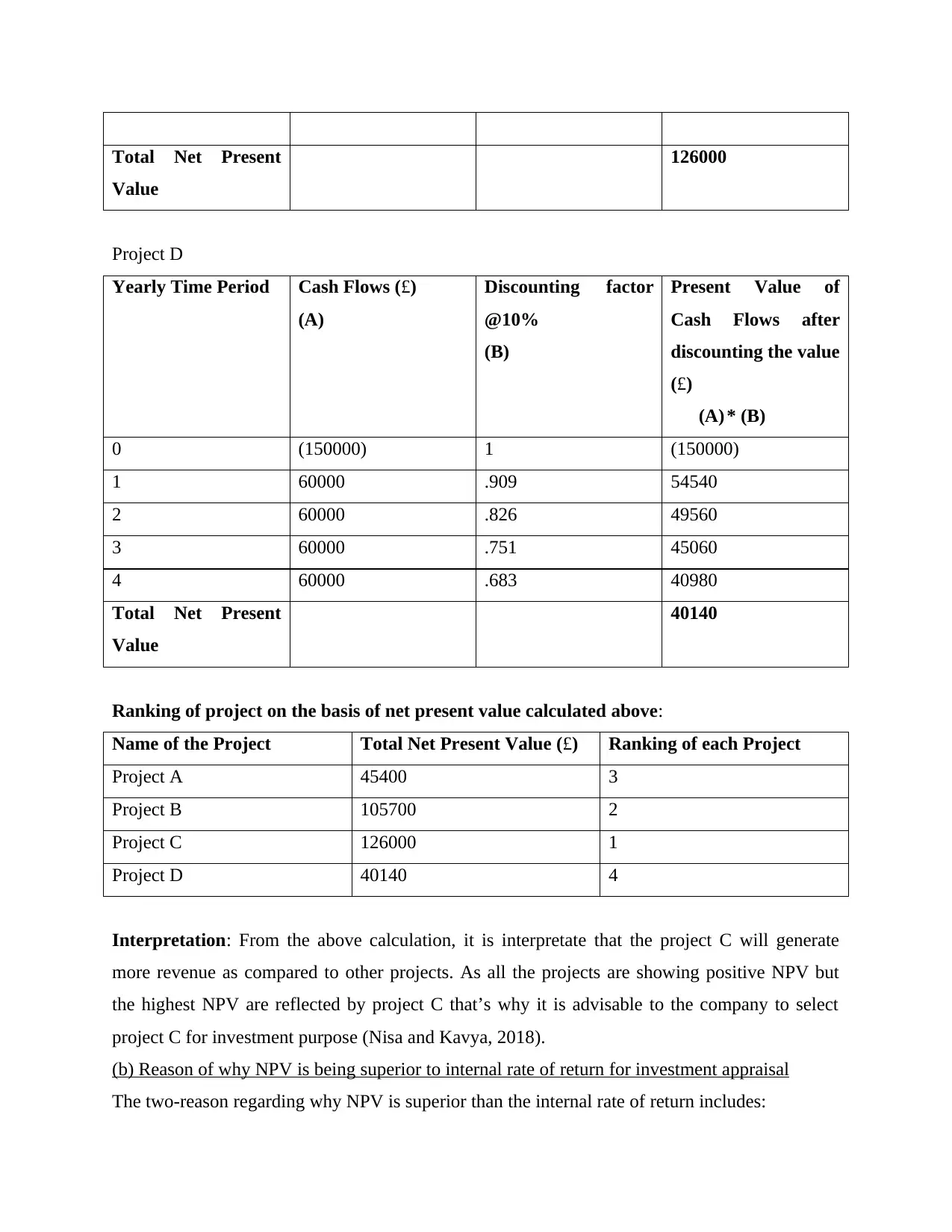

126000

Project D

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (150000) 1 (150000)

1 60000 .909 54540

2 60000 .826 49560

3 60000 .751 45060

4 60000 .683 40980

Total Net Present

Value

40140

Ranking of project on the basis of net present value calculated above:

Name of the Project Total Net Present Value (£) Ranking of each Project

Project A 45400 3

Project B 105700 2

Project C 126000 1

Project D 40140 4

Interpretation: From the above calculation, it is interpretate that the project C will generate

more revenue as compared to other projects. As all the projects are showing positive NPV but

the highest NPV are reflected by project C that’s why it is advisable to the company to select

project C for investment purpose (Nisa and Kavya, 2018).

(b) Reason of why NPV is being superior to internal rate of return for investment appraisal

The two-reason regarding why NPV is superior than the internal rate of return includes:

Value

126000

Project D

Yearly Time Period Cash Flows (£)

(A)

Discounting factor

@10%

(B)

Present Value of

Cash Flows after

discounting the value

(£)

(A) * (B)

0 (150000) 1 (150000)

1 60000 .909 54540

2 60000 .826 49560

3 60000 .751 45060

4 60000 .683 40980

Total Net Present

Value

40140

Ranking of project on the basis of net present value calculated above:

Name of the Project Total Net Present Value (£) Ranking of each Project

Project A 45400 3

Project B 105700 2

Project C 126000 1

Project D 40140 4

Interpretation: From the above calculation, it is interpretate that the project C will generate

more revenue as compared to other projects. As all the projects are showing positive NPV but

the highest NPV are reflected by project C that’s why it is advisable to the company to select

project C for investment purpose (Nisa and Kavya, 2018).

(b) Reason of why NPV is being superior to internal rate of return for investment appraisal

The two-reason regarding why NPV is superior than the internal rate of return includes:

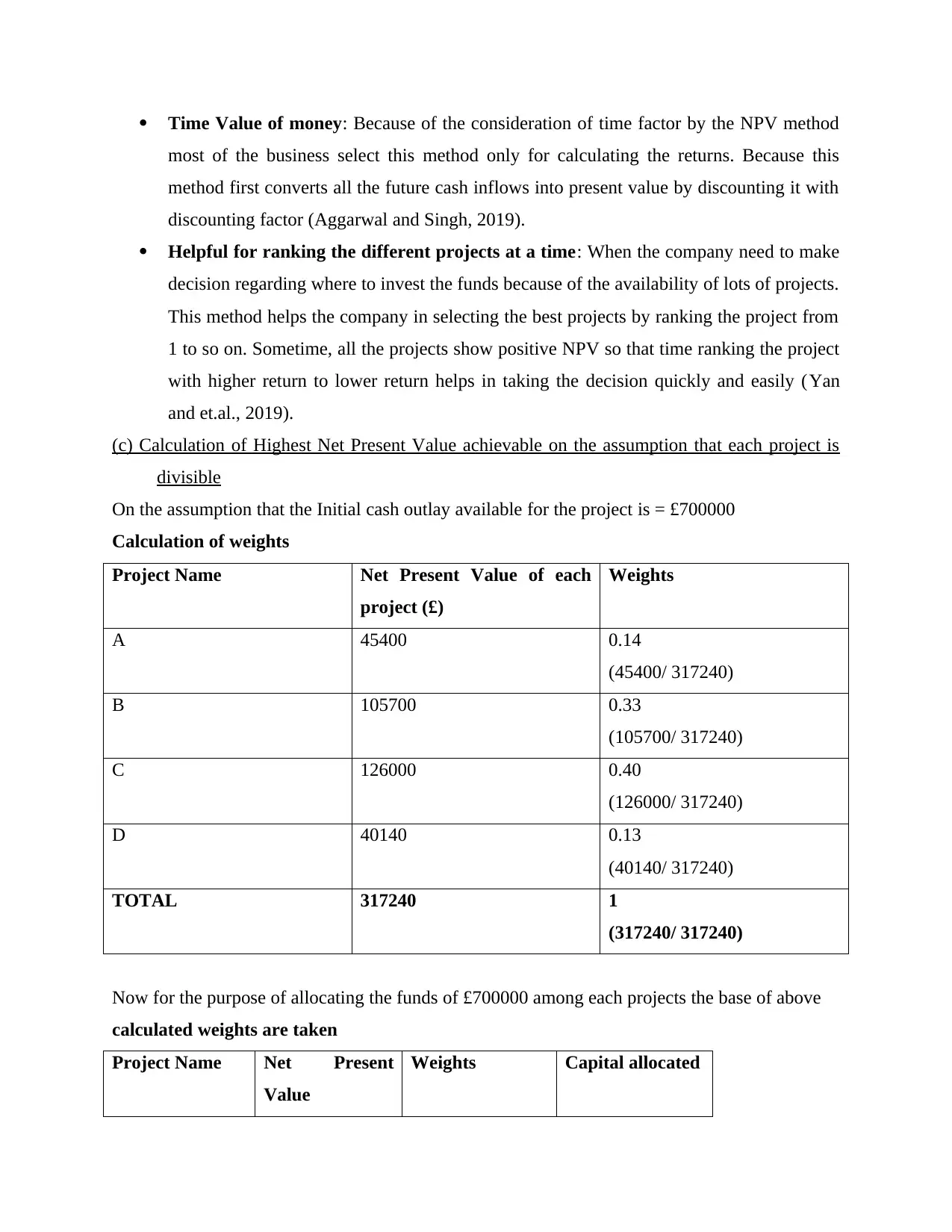

Time Value of money: Because of the consideration of time factor by the NPV method

most of the business select this method only for calculating the returns. Because this

method first converts all the future cash inflows into present value by discounting it with

discounting factor (Aggarwal and Singh, 2019).

Helpful for ranking the different projects at a time: When the company need to make

decision regarding where to invest the funds because of the availability of lots of projects.

This method helps the company in selecting the best projects by ranking the project from

1 to so on. Sometime, all the projects show positive NPV so that time ranking the project

with higher return to lower return helps in taking the decision quickly and easily (Yan

and et.al., 2019).

(c) Calculation of Highest Net Present Value achievable on the assumption that each project is

divisible

On the assumption that the Initial cash outlay available for the project is = £700000

Calculation of weights

Project Name Net Present Value of each

project (£)

Weights

A 45400 0.14

(45400/ 317240)

B 105700 0.33

(105700/ 317240)

C 126000 0.40

(126000/ 317240)

D 40140 0.13

(40140/ 317240)

TOTAL 317240 1

(317240/ 317240)

Now for the purpose of allocating the funds of £700000 among each projects the base of above

calculated weights are taken

Project Name Net Present

Value

Weights Capital allocated

most of the business select this method only for calculating the returns. Because this

method first converts all the future cash inflows into present value by discounting it with

discounting factor (Aggarwal and Singh, 2019).

Helpful for ranking the different projects at a time: When the company need to make

decision regarding where to invest the funds because of the availability of lots of projects.

This method helps the company in selecting the best projects by ranking the project from

1 to so on. Sometime, all the projects show positive NPV so that time ranking the project

with higher return to lower return helps in taking the decision quickly and easily (Yan

and et.al., 2019).

(c) Calculation of Highest Net Present Value achievable on the assumption that each project is

divisible

On the assumption that the Initial cash outlay available for the project is = £700000

Calculation of weights

Project Name Net Present Value of each

project (£)

Weights

A 45400 0.14

(45400/ 317240)

B 105700 0.33

(105700/ 317240)

C 126000 0.40

(126000/ 317240)

D 40140 0.13

(40140/ 317240)

TOTAL 317240 1

(317240/ 317240)

Now for the purpose of allocating the funds of £700000 among each projects the base of above

calculated weights are taken

Project Name Net Present

Value

Weights Capital allocated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

![International Finance Management Assignment - Finance [Course Code]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Ffd%2F69271dad5c5f4f2c8ab93e7e6daf77ee.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.