International Financial Management Assignment: IMF and Derivatives

VerifiedAdded on 2022/08/23

|14

|3628

|156

Report

AI Summary

This report analyzes the challenges faced by the International Monetary Fund (IMF), as discussed in the article "The IMF’s Unmet Challenges" by Eichengreen and Woods. The IMF plays a crucial role in stabilizing global economic conditions, advising countries, and promoting financial literacy, but it faces difficulties in uniform surveillance, conditionality, sovereign debt management, and aligning policies with national objectives. The report also explores the concepts of Purchasing Power Parity (PPP) and International Fisher Effect (IFE) and their relationship to derivatives. PPP suggests that exchange rates adjust to equalize purchasing power across countries, while IFE links interest rate differentials to expected exchange rate changes. The report also explains how derivatives can be used to mitigate risks associated with exchange rate fluctuations and protect against financial market volatility. The report also examines the role of derivatives in hedging against financial risks. The analysis highlights the importance of understanding these concepts for effective international financial management and the role of derivatives in mitigating financial risks.

Running head: INTERNATIONAL FINANCIAL MANAGEMENT

International financial management

Name of the student

Name of the university

Author’s note

International financial management

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL FINANCIAL MANAGEMENT

Table of Contents

Part a................................................................................................................................................2

Summary......................................................................................................................................2

Part b................................................................................................................................................5

Answer i).....................................................................................................................................5

Answer ii)....................................................................................................................................8

References......................................................................................................................................13

Table of Contents

Part a................................................................................................................................................2

Summary......................................................................................................................................2

Part b................................................................................................................................................5

Answer i).....................................................................................................................................5

Answer ii)....................................................................................................................................8

References......................................................................................................................................13

2INTERNATIONAL FINANCIAL MANAGEMENT

Part a

Summary

IMF has a crucial role in stabilizing the economic environment of countries, international

fiscal conditions, and conditions of the financial system all over the world. The organization

plays the role of an advisor to other countries. It mainly analyses the information which is

available from organizations such as rating agencies. The IMF helps in creating awareness

among the members about financial literacy. It also helps people to know about the cross border

spillovers. Any particular government does not have sufficient means to analyze this information

and provide it to the countries. The IMF has the means to make different countries aware of

different externalities. It saves the countries from opting for wrong options of fund generation

and acts as an emergency banker for various countries.

To carry out all the functions stated above, it is also mandatory that the countries follow the

rules of the organization and see the organization as a viable one who helps them in need. Some

of the challenges that the organization faces in conducting its functions are:

Firstly, the IMF remained unsuccessful in organizing a uniform surveillance system that can

monitor all its member countries' financial policies. This practice is the reason the IMF fails

to recognize the risk to stability.

Secondly, the IMF has yet not made proper conditions which will apply to the borrowers of

the IMF. There are different viewpoints concerning it as to why an independent nation will

follow the conditions made when both of them have some similar objectives. And if they

have a different objective, they why the IMF would be providing the loans.

Thirdly, IMF is argued that it lags while managing the sovereign debt crises.

Part a

Summary

IMF has a crucial role in stabilizing the economic environment of countries, international

fiscal conditions, and conditions of the financial system all over the world. The organization

plays the role of an advisor to other countries. It mainly analyses the information which is

available from organizations such as rating agencies. The IMF helps in creating awareness

among the members about financial literacy. It also helps people to know about the cross border

spillovers. Any particular government does not have sufficient means to analyze this information

and provide it to the countries. The IMF has the means to make different countries aware of

different externalities. It saves the countries from opting for wrong options of fund generation

and acts as an emergency banker for various countries.

To carry out all the functions stated above, it is also mandatory that the countries follow the

rules of the organization and see the organization as a viable one who helps them in need. Some

of the challenges that the organization faces in conducting its functions are:

Firstly, the IMF remained unsuccessful in organizing a uniform surveillance system that can

monitor all its member countries' financial policies. This practice is the reason the IMF fails

to recognize the risk to stability.

Secondly, the IMF has yet not made proper conditions which will apply to the borrowers of

the IMF. There are different viewpoints concerning it as to why an independent nation will

follow the conditions made when both of them have some similar objectives. And if they

have a different objective, they why the IMF would be providing the loans.

Thirdly, IMF is argued that it lags while managing the sovereign debt crises.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL FINANCIAL MANAGEMENT

Fourthly, the government of some countries finds themselves neglected when policies of the

IMF do not match their objective of national policy.

IMF remained unsuccessful in mitigating these challenges. This failure raised many

questions on the competency of the organization. The legitimacy of the fund was in question too.

Two sources of legitimacy are output legitimacy and input legitimacy.

The original constitution of IMF obliged each member country to follow a single and

fixed par value for foreign exchange. In 1977, the exchange rates were stabled, and this change

influenced the stability of the full system of economy. The reason behind it is that the national

economies were extended to accept the change of stability. There was an influence of different

stability measures of one developed nation on the other developing and underdeveloped nations.

There remained an inadequacy in the cross border spill-overs too, which led to the need for the

correction of IMF surveillance. The surveillance required a full analysis of the individual

country-wise and the whole economy-wise evaluation. IMF ignored the full evaluation of the

fund at the time of the sub-prime crisis also. Later on, it is argued it failed because of several

political limitations. There is no magic formula to attain growth, rather complete analysis of the

market is the only solution considering both macro and microeconomic variables. The argument

of complete surveillance continues among economists because complete financial information

about countries can reduce the level of confidence among investors.

Exchange rates and capital flows

Exchange rates of currencies have a significant effect on the country’s financial position.

The impact that the exchange rate puts on a small and free economy is strong as it affects the

growth and financial environment of the country while it has a strong spillover effect on large

Fourthly, the government of some countries finds themselves neglected when policies of the

IMF do not match their objective of national policy.

IMF remained unsuccessful in mitigating these challenges. This failure raised many

questions on the competency of the organization. The legitimacy of the fund was in question too.

Two sources of legitimacy are output legitimacy and input legitimacy.

The original constitution of IMF obliged each member country to follow a single and

fixed par value for foreign exchange. In 1977, the exchange rates were stabled, and this change

influenced the stability of the full system of economy. The reason behind it is that the national

economies were extended to accept the change of stability. There was an influence of different

stability measures of one developed nation on the other developing and underdeveloped nations.

There remained an inadequacy in the cross border spill-overs too, which led to the need for the

correction of IMF surveillance. The surveillance required a full analysis of the individual

country-wise and the whole economy-wise evaluation. IMF ignored the full evaluation of the

fund at the time of the sub-prime crisis also. Later on, it is argued it failed because of several

political limitations. There is no magic formula to attain growth, rather complete analysis of the

market is the only solution considering both macro and microeconomic variables. The argument

of complete surveillance continues among economists because complete financial information

about countries can reduce the level of confidence among investors.

Exchange rates and capital flows

Exchange rates of currencies have a significant effect on the country’s financial position.

The impact that the exchange rate puts on a small and free economy is strong as it affects the

growth and financial environment of the country while it has a strong spillover effect on large

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL FINANCIAL MANAGEMENT

economies too. Large economies like the USA and China have failed to adopt surveillance and

were providing loans to other countries without any proper specification of exchange rates. There

are different views concerning this situation. Large economies can either adopt flexible rates that

are market-determined. Options are recommended for countries that face restrictions in

international trade. Another option is to decide fixed exchange rates. However, the IMF keeps on

reviewing the policies and take efforts to stabilize the monetary scenario. IMF's main role was

how to control the capital flows, which involves maximum national and international risks. The

control was crucial for putting restrictions on the banks and financial institutions concerning the

exchange rate.

Lending and conditionality

IMF conditionality is a major issue while discussing the role of IMF contribution to

international trade. Conditions are important while rendering loans, which can increase the

possibility of repayments. Therefore the IMF can conduct a important role in safeguarding the

interest of the member nations. The importance of conditionality increase when both the IMF

and the government want this conditionality, but a domestic country disagrees the importance.

The conditionality is a good way, which ensures that the chances of the default payment of the

loan will be less. The feeling of safety among the investors increases if a country and the IMF

mainly focus on conditionality.

Resolution of sovereign debt problems

The sovereign debts are provided security until the country's performance is sustainable.

If the situation goes wrong, restructuring of debt becomes difficult. IMF faces a situation of

dilemma whether to provide a loan to a country or helps them in restructuring the loan. In 2002,

economies too. Large economies like the USA and China have failed to adopt surveillance and

were providing loans to other countries without any proper specification of exchange rates. There

are different views concerning this situation. Large economies can either adopt flexible rates that

are market-determined. Options are recommended for countries that face restrictions in

international trade. Another option is to decide fixed exchange rates. However, the IMF keeps on

reviewing the policies and take efforts to stabilize the monetary scenario. IMF's main role was

how to control the capital flows, which involves maximum national and international risks. The

control was crucial for putting restrictions on the banks and financial institutions concerning the

exchange rate.

Lending and conditionality

IMF conditionality is a major issue while discussing the role of IMF contribution to

international trade. Conditions are important while rendering loans, which can increase the

possibility of repayments. Therefore the IMF can conduct a important role in safeguarding the

interest of the member nations. The importance of conditionality increase when both the IMF

and the government want this conditionality, but a domestic country disagrees the importance.

The conditionality is a good way, which ensures that the chances of the default payment of the

loan will be less. The feeling of safety among the investors increases if a country and the IMF

mainly focus on conditionality.

Resolution of sovereign debt problems

The sovereign debts are provided security until the country's performance is sustainable.

If the situation goes wrong, restructuring of debt becomes difficult. IMF faces a situation of

dilemma whether to provide a loan to a country or helps them in restructuring the loan. In 2002,

5INTERNATIONAL FINANCIAL MANAGEMENT

it agreed on large scale financing without drawing any room for debt restructuring if the loan is

provided to a country with high sustainability and high profitability.

Governance reforms

The governance of the country and the IMF ensures the legitimacy and competency of the

IMF. Under the system, the US has the veto power for voting concerning major decisions of the

IMF. Any reforms need to be accepted by the 85% majority voting by the member countries. The

support and favor of a country like the US are important for bringing any reform in the system.

Continuous reforms and improvements are going on in different countries and IMF, such as the

governance reforms in the year 2010. The governance structure of the IMF must be reformed.

Jack Lew, who is a union secretary of the US treasury, expressed his views on the importance of

the reforms of the IMF. The essential reforms can only make the IMF fit for the future

development of the credit environment.

Part b

Answer i)

The purchasing power parity explains the likelihoods of arbitrage while trading amid two

countries should be made negligible. This means that the prices of alike and identical things must

be equal in the two states, but it does not imply that the exchange rate must be equal. The

concept of PPP helps to understand that the ratio of price to exchange rate must be equivalent to

1 to lessen the chance of arbitrage between two nations to a minimum. This implies that the PPP

should ensure the constant purchasing power required to purchase a specific commodity.

International financial management looks at the effect of IFE on international trade. The

international fisher effect reflects the change in rate of interest rather than the inflation rate. The

it agreed on large scale financing without drawing any room for debt restructuring if the loan is

provided to a country with high sustainability and high profitability.

Governance reforms

The governance of the country and the IMF ensures the legitimacy and competency of the

IMF. Under the system, the US has the veto power for voting concerning major decisions of the

IMF. Any reforms need to be accepted by the 85% majority voting by the member countries. The

support and favor of a country like the US are important for bringing any reform in the system.

Continuous reforms and improvements are going on in different countries and IMF, such as the

governance reforms in the year 2010. The governance structure of the IMF must be reformed.

Jack Lew, who is a union secretary of the US treasury, expressed his views on the importance of

the reforms of the IMF. The essential reforms can only make the IMF fit for the future

development of the credit environment.

Part b

Answer i)

The purchasing power parity explains the likelihoods of arbitrage while trading amid two

countries should be made negligible. This means that the prices of alike and identical things must

be equal in the two states, but it does not imply that the exchange rate must be equal. The

concept of PPP helps to understand that the ratio of price to exchange rate must be equivalent to

1 to lessen the chance of arbitrage between two nations to a minimum. This implies that the PPP

should ensure the constant purchasing power required to purchase a specific commodity.

International financial management looks at the effect of IFE on international trade. The

international fisher effect reflects the change in rate of interest rather than the inflation rate. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL FINANCIAL MANAGEMENT

correlation amid the interest rate and inflation rate shows that it is considering the inflation rate.

The currency which has a higher nominal interest rate depreciates and loses its value against the

currency of lesser interest rate. It states that the variance between the future spot rate of the

currency and the spot rate of the currency differs from each other from a percentage of the

amount that is the rate of interest.

When the rate of inflation in a country like the US is greater than the inflation rate of the

country like the UK, then the number of imports from the country, the UK will increase to the

US. Similarly, the exports from the US will increase to the UK, but it will have an adverse

impact on the current account as the drainage of the resources will be much more.

The international parity shows that if the purchasing power of one country increases due

to the difference in exchange rates and the interest rate offered on the currency, then the foreign

goods may be considered as cheaper. When the inflation differentials are drawn in the graph, and

along with it, the spot exchange rates are also drawn respectively, the result shows that points

deviate from the purchasing power parity graph line. In this scenario, the PPP theory does not

verify the result. It shows that the relationship between the two variables is inflation differentials,

and the exchange rates are not perfect in the long run (Dixon et al. 2016).

The other result shows that when the inflation differentials are used, it helps in the

forecast of the future movements of the exchange rates. The period, which is taken as the base

period, is considered important for evaluating the result. Moreover, in the long run, the real

exchange rate is taken as the actual exchange rate. The relative purchasing power parity is the

addition of the PPP model. Under this concept, the difference in any two countries' rate of

inflation is affected by the change in the exchange rates. For example- if the goods in the US

increase by 4%, the prices of country France increase by 7%. This means France faces a higher

correlation amid the interest rate and inflation rate shows that it is considering the inflation rate.

The currency which has a higher nominal interest rate depreciates and loses its value against the

currency of lesser interest rate. It states that the variance between the future spot rate of the

currency and the spot rate of the currency differs from each other from a percentage of the

amount that is the rate of interest.

When the rate of inflation in a country like the US is greater than the inflation rate of the

country like the UK, then the number of imports from the country, the UK will increase to the

US. Similarly, the exports from the US will increase to the UK, but it will have an adverse

impact on the current account as the drainage of the resources will be much more.

The international parity shows that if the purchasing power of one country increases due

to the difference in exchange rates and the interest rate offered on the currency, then the foreign

goods may be considered as cheaper. When the inflation differentials are drawn in the graph, and

along with it, the spot exchange rates are also drawn respectively, the result shows that points

deviate from the purchasing power parity graph line. In this scenario, the PPP theory does not

verify the result. It shows that the relationship between the two variables is inflation differentials,

and the exchange rates are not perfect in the long run (Dixon et al. 2016).

The other result shows that when the inflation differentials are used, it helps in the

forecast of the future movements of the exchange rates. The period, which is taken as the base

period, is considered important for evaluating the result. Moreover, in the long run, the real

exchange rate is taken as the actual exchange rate. The relative purchasing power parity is the

addition of the PPP model. Under this concept, the difference in any two countries' rate of

inflation is affected by the change in the exchange rates. For example- if the goods in the US

increase by 4%, the prices of country France increase by 7%. This means France faces a higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCIAL MANAGEMENT

inflation rate as compared to the US because prices in France have risen more rapidly in France

than the US. This will have a direct impact on the exchange rate of the countries. The France

currency will depreciate at a rate of 3% while the US currency will appreciate at the rate of 3%.

The IFE says that the currencies with a higher rate of interest tend to depreciate because the

greater nominal rate will have greater expected inflation (Ogolla 2018).

The international parity relationship helps to understand that the return generated on the

investment in the host country and return generated on the investments made in the foreign

currency but on home currency are always equal. This shows the market is efficient, and it

knows everything. Arbitraging is possible until both the countries do not receive the complete

information, and the two sides remain unequal. When both the market observes the difference,

the arbitraging becomes impossible (Ariff and Zarei 2018).

The IFE theory suggests that if a firm wants to earn a capital profit on his foreign interest,

then as per market volatility, he may earn high return sometimes and sometimes lower return,

too, as compared to the return in the domestic market. However, if the return of overall

performance is compared, the average return earned on foreign interest will be similar to another

firm, which is investing in the domestic market. The empirical study has explained that the

inflation differential and exchange rate do not go along perfectly. The relationship between both

variables is always not perfect in the longer run. Although the exchange rate is affected by the

income levels, exchange rates, and inflation rates, etc. the real exchange rate is also not constant

in the long run. This is the reason that PPP makes derivatives unnecessary since it does not hold

for the long run.

As per the IFE, the nominal risk-free interest rate shows presence of a real rate of return

and also contains expected inflation. If investors want to earn some real return on the assets of

inflation rate as compared to the US because prices in France have risen more rapidly in France

than the US. This will have a direct impact on the exchange rate of the countries. The France

currency will depreciate at a rate of 3% while the US currency will appreciate at the rate of 3%.

The IFE says that the currencies with a higher rate of interest tend to depreciate because the

greater nominal rate will have greater expected inflation (Ogolla 2018).

The international parity relationship helps to understand that the return generated on the

investment in the host country and return generated on the investments made in the foreign

currency but on home currency are always equal. This shows the market is efficient, and it

knows everything. Arbitraging is possible until both the countries do not receive the complete

information, and the two sides remain unequal. When both the market observes the difference,

the arbitraging becomes impossible (Ariff and Zarei 2018).

The IFE theory suggests that if a firm wants to earn a capital profit on his foreign interest,

then as per market volatility, he may earn high return sometimes and sometimes lower return,

too, as compared to the return in the domestic market. However, if the return of overall

performance is compared, the average return earned on foreign interest will be similar to another

firm, which is investing in the domestic market. The empirical study has explained that the

inflation differential and exchange rate do not go along perfectly. The relationship between both

variables is always not perfect in the longer run. Although the exchange rate is affected by the

income levels, exchange rates, and inflation rates, etc. the real exchange rate is also not constant

in the long run. This is the reason that PPP makes derivatives unnecessary since it does not hold

for the long run.

As per the IFE, the nominal risk-free interest rate shows presence of a real rate of return

and also contains expected inflation. If investors want to earn some real return on the assets of

8INTERNATIONAL FINANCIAL MANAGEMENT

similar risk and maturity, the interest differentials may be the result of expected inflation. As per

PPP model, the exchange rate movements are triggered by the differences in inflation rates of

different nations. The IFE theory is centered on the PPP theory (Machobani, Boako and

Alagidede 2017). Thus it can be assumed that if PPP theory will not verify any case or hold the

equation, then definitely IFE will not hold the case. There are many other factors other than

inflation, which affect the exchange rates and cannot be adjusted the same as the inflation

differential. Since IFE is based on PPP, IFE also makes derivatives unnecessary when it does not

hold true in case PPP does not hold true.

Answer ii)

Purchasing power parity attains to find the association between exchange rate and

inflation. The purchasing power parity theorem is of two types which are, relative form of

purchasing power parity and absolute form of purchasing power parity (Lothian 2016). Absolute

PPP is based on the notion that without international barriers, the consumer shifts their demand

to wherever prices are lower. The theory is based on the theory of one price.

The theory of one price states that the price of any goods in the home country equals its

foreign price quoted in the same currency. For example:

The USD value of a commodity * value of USD = AUSD value of a product.

The above equation states that foreign price multiplied by foreign currency will be equal

to domestic price in case of the law of one price. The absolute version holds good if the same

commodities are included in the same proportion in the domestic market basket and world

market basket. If the complete version of PPP will not hold good, the earlier statement is not true

while, in this case, the law of price may hold good. From the above statement, it is clear that if

similar risk and maturity, the interest differentials may be the result of expected inflation. As per

PPP model, the exchange rate movements are triggered by the differences in inflation rates of

different nations. The IFE theory is centered on the PPP theory (Machobani, Boako and

Alagidede 2017). Thus it can be assumed that if PPP theory will not verify any case or hold the

equation, then definitely IFE will not hold the case. There are many other factors other than

inflation, which affect the exchange rates and cannot be adjusted the same as the inflation

differential. Since IFE is based on PPP, IFE also makes derivatives unnecessary when it does not

hold true in case PPP does not hold true.

Answer ii)

Purchasing power parity attains to find the association between exchange rate and

inflation. The purchasing power parity theorem is of two types which are, relative form of

purchasing power parity and absolute form of purchasing power parity (Lothian 2016). Absolute

PPP is based on the notion that without international barriers, the consumer shifts their demand

to wherever prices are lower. The theory is based on the theory of one price.

The theory of one price states that the price of any goods in the home country equals its

foreign price quoted in the same currency. For example:

The USD value of a commodity * value of USD = AUSD value of a product.

The above equation states that foreign price multiplied by foreign currency will be equal

to domestic price in case of the law of one price. The absolute version holds good if the same

commodities are included in the same proportion in the domestic market basket and world

market basket. If the complete version of PPP will not hold good, the earlier statement is not true

while, in this case, the law of price may hold good. From the above statement, it is clear that if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL FINANCIAL MANAGEMENT

the absolute version holds good, the law of one price has to be valid, and if the absolute version

of PPP does not hold good, then the law of one price may or may not hold good. There are some

limitations of the absolute version of PPP; the theory does not cover non-traded goods and

services where transaction cost is high.

The relative version of PPP depicts that the exchange rate between home currency and

any foreign currency will adjust to reflect changes in the price level of the two countries (Manzur

2020). In other words, the percentage variation in the exchange rate should be equal to the

percentage change in the ratio of price indices in the two countries.

International Fisher's effect that currencies with low-interest rates are expected to

increase relative to currencies with the high-interest rate in the spot market also. The theory

states that interest rate differential will be equal to the expected change in the spot market in

equilibrium. If the interest rate differential is not equal to the expected change in spot market,

then the arbitrage between international financial markets will arise.

the absolute version holds good, the law of one price has to be valid, and if the absolute version

of PPP does not hold good, then the law of one price may or may not hold good. There are some

limitations of the absolute version of PPP; the theory does not cover non-traded goods and

services where transaction cost is high.

The relative version of PPP depicts that the exchange rate between home currency and

any foreign currency will adjust to reflect changes in the price level of the two countries (Manzur

2020). In other words, the percentage variation in the exchange rate should be equal to the

percentage change in the ratio of price indices in the two countries.

International Fisher's effect that currencies with low-interest rates are expected to

increase relative to currencies with the high-interest rate in the spot market also. The theory

states that interest rate differential will be equal to the expected change in the spot market in

equilibrium. If the interest rate differential is not equal to the expected change in spot market,

then the arbitrage between international financial markets will arise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNATIONAL FINANCIAL MANAGEMENT

The international fisher effect mainly studies and analyzes the interest rate with risk-free

investment. The theory state that by evaluating the differences in the nominal interest rates amid

two countries, one can measure the charges incurred in the exchange rates (Bjørnland and

Halvorsen 2014). The basic concept of IFE is that the country having a higher nominal interest

rate will experience a high rate of inflation that will result in depreciation of the home currency

against other currencies. Mainly the theory takes into consideration the present and future risk-

free nominal interest rate instead of pure inflation to evaluate and understand the movement in

spot currency both in terms of present and future times.

The relationship between the inflation rate differential and the expected variation in spot

rate is known as purchasing power parity. In equilibrium, condition both the inflation rate and

the expected change in spot rate must be equal. If both factors are not equal, then arbitrage arises

in the case of real goods and services. However, arbitrage is not acceptable in case of a parity

relationship, as it will affect the exchange rate instead of the market prices. Even in the case of a

transaction, cost purchasing power parity will not be valid, and in the case of PPP, it is assumed

that all goods are traded internationally. It is evident that price levels are different for each

country, and even the inflation rate is based on diverse commodity group. This is the reason that

the exchange rate does not balance official measures of inflation changes as forecasts are made

The international fisher effect mainly studies and analyzes the interest rate with risk-free

investment. The theory state that by evaluating the differences in the nominal interest rates amid

two countries, one can measure the charges incurred in the exchange rates (Bjørnland and

Halvorsen 2014). The basic concept of IFE is that the country having a higher nominal interest

rate will experience a high rate of inflation that will result in depreciation of the home currency

against other currencies. Mainly the theory takes into consideration the present and future risk-

free nominal interest rate instead of pure inflation to evaluate and understand the movement in

spot currency both in terms of present and future times.

The relationship between the inflation rate differential and the expected variation in spot

rate is known as purchasing power parity. In equilibrium, condition both the inflation rate and

the expected change in spot rate must be equal. If both factors are not equal, then arbitrage arises

in the case of real goods and services. However, arbitrage is not acceptable in case of a parity

relationship, as it will affect the exchange rate instead of the market prices. Even in the case of a

transaction, cost purchasing power parity will not be valid, and in the case of PPP, it is assumed

that all goods are traded internationally. It is evident that price levels are different for each

country, and even the inflation rate is based on diverse commodity group. This is the reason that

the exchange rate does not balance official measures of inflation changes as forecasts are made

11INTERNATIONAL FINANCIAL MANAGEMENT

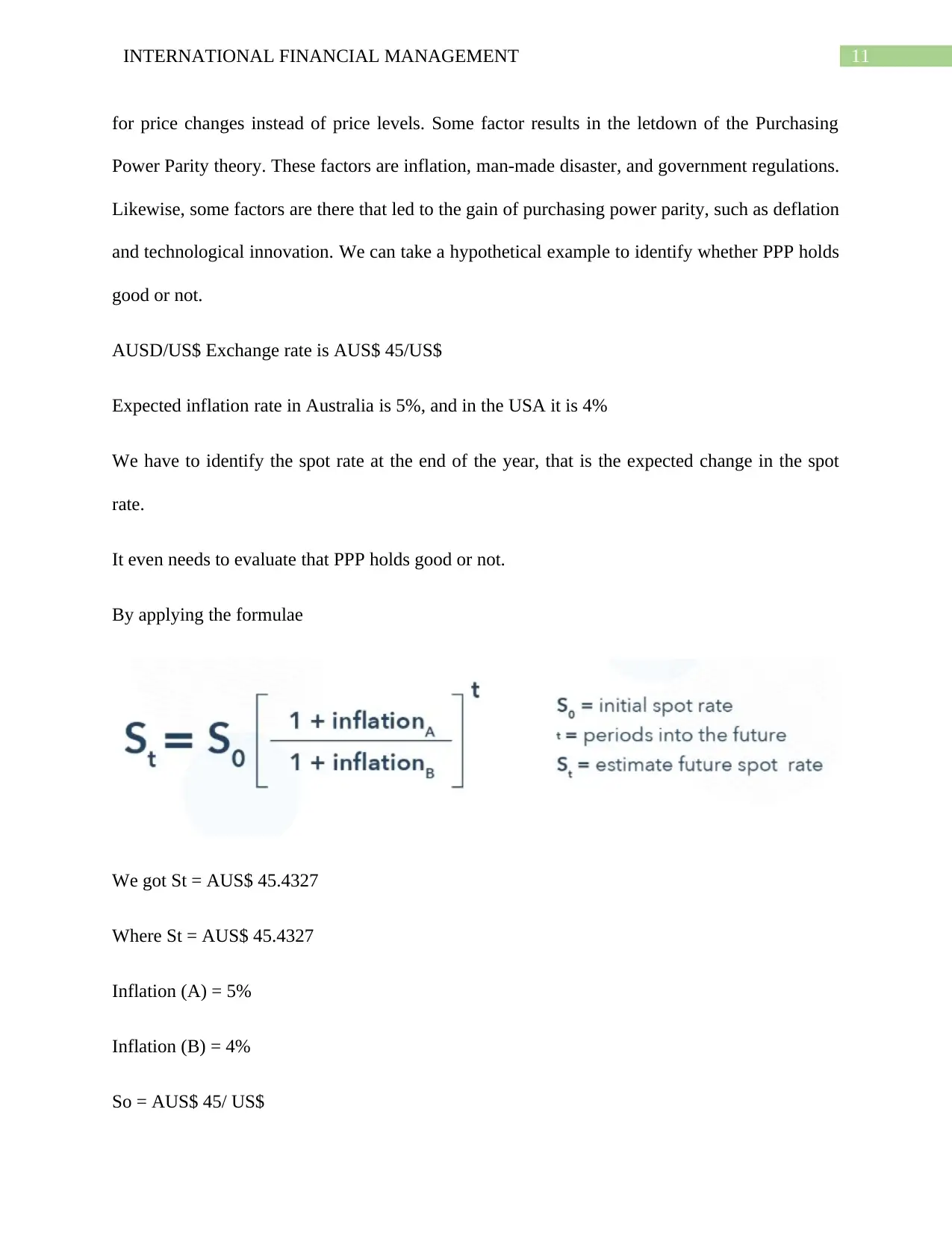

for price changes instead of price levels. Some factor results in the letdown of the Purchasing

Power Parity theory. These factors are inflation, man-made disaster, and government regulations.

Likewise, some factors are there that led to the gain of purchasing power parity, such as deflation

and technological innovation. We can take a hypothetical example to identify whether PPP holds

good or not.

AUSD/US$ Exchange rate is AUS$ 45/US$

Expected inflation rate in Australia is 5%, and in the USA it is 4%

We have to identify the spot rate at the end of the year, that is the expected change in the spot

rate.

It even needs to evaluate that PPP holds good or not.

By applying the formulae

We got St = AUS$ 45.4327

Where St = AUS$ 45.4327

Inflation (A) = 5%

Inflation (B) = 4%

So = AUS$ 45/ US$

for price changes instead of price levels. Some factor results in the letdown of the Purchasing

Power Parity theory. These factors are inflation, man-made disaster, and government regulations.

Likewise, some factors are there that led to the gain of purchasing power parity, such as deflation

and technological innovation. We can take a hypothetical example to identify whether PPP holds

good or not.

AUSD/US$ Exchange rate is AUS$ 45/US$

Expected inflation rate in Australia is 5%, and in the USA it is 4%

We have to identify the spot rate at the end of the year, that is the expected change in the spot

rate.

It even needs to evaluate that PPP holds good or not.

By applying the formulae

We got St = AUS$ 45.4327

Where St = AUS$ 45.4327

Inflation (A) = 5%

Inflation (B) = 4%

So = AUS$ 45/ US$

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.