International Financial Management Assignment: Company Analysis

VerifiedAdded on 2023/01/09

|14

|3993

|42

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of two companies' financial performance using various financial ratios, including profitability, investor, efficiency, and gearing ratios. It calculates and compares the Return on Capital Employed (ROCE), Gross Profit Margin, Net Profit Margin, Return on Equity (ROE), Asset Turnover, Inventory Turnover, Accounts Receivable Turnover, and Interest Cover ratios. The analysis evaluates the financial health and efficiency of each company, highlighting strengths and weaknesses. Furthermore, the assignment delves into the calculation of the Weighted Average Cost of Capital (WACC) and the Book Value Weighted Average Cost of Capital. It discusses the circumstances where WACC is applicable in investment appraisal techniques and its limitations. Finally, the assignment explores the objectives of working capital management and its central role in financial management, providing a holistic view of financial analysis and management concepts.

INTERNATIONAL FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION ONE............................................................................................................................1

a) Calculation of the ratios...........................................................................................................1

b) Financial performance of both the companies........................................................................2

c) Limitations of the analysis.......................................................................................................5

QUESTION TWO...........................................................................................................................6

a) Calculation of the Weighted Average Cost of Capital and Book value weighted average cost

of capital of Art Co......................................................................................................................6

b) Circumstances where the weighted average cost of capital of company could be used in the

investment appraisal techniques and limitations as discount rate...............................................8

QUESTION THREE.......................................................................................................................9

Objectives of the working capital management and central role of working capital in financial

management.................................................................................................................................9

REFERENCES..............................................................................................................................12

TABLE OF CONTENTS................................................................................................................2

QUESTION ONE............................................................................................................................1

a) Calculation of the ratios...........................................................................................................1

b) Financial performance of both the companies........................................................................2

c) Limitations of the analysis.......................................................................................................5

QUESTION TWO...........................................................................................................................6

a) Calculation of the Weighted Average Cost of Capital and Book value weighted average cost

of capital of Art Co......................................................................................................................6

b) Circumstances where the weighted average cost of capital of company could be used in the

investment appraisal techniques and limitations as discount rate...............................................8

QUESTION THREE.......................................................................................................................9

Objectives of the working capital management and central role of working capital in financial

management.................................................................................................................................9

REFERENCES..............................................................................................................................12

QUESTION ONE

a) Calculation of the ratios

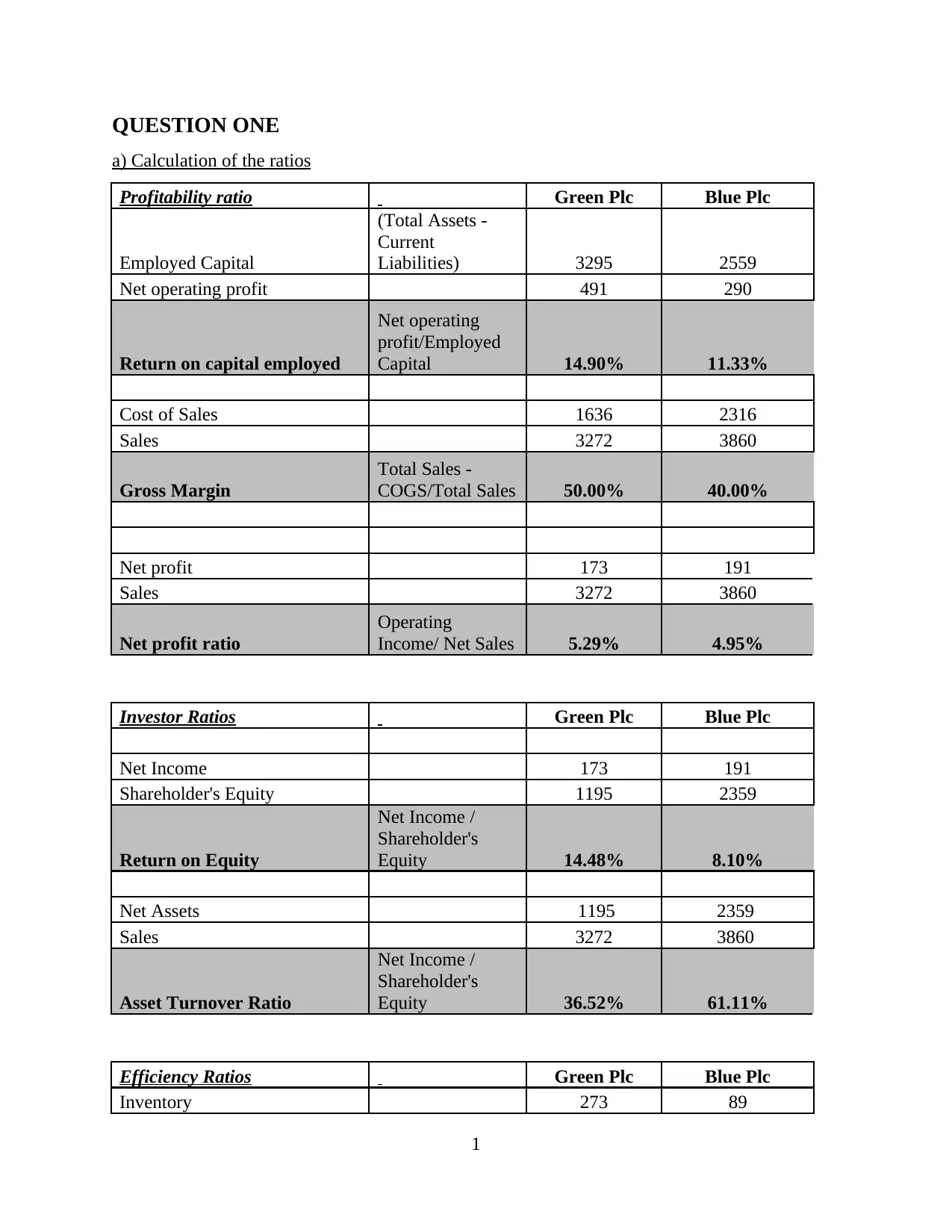

Profitability ratio Green Plc Blue Plc

Employed Capital

(Total Assets -

Current

Liabilities) 3295 2559

Net operating profit 491 290

Return on capital employed

Net operating

profit/Employed

Capital 14.90% 11.33%

Cost of Sales 1636 2316

Sales 3272 3860

Gross Margin

Total Sales -

COGS/Total Sales 50.00% 40.00%

Net profit 173 191

Sales 3272 3860

Net profit ratio

Operating

Income/ Net Sales 5.29% 4.95%

Investor Ratios Green Plc Blue Plc

Net Income 173 191

Shareholder's Equity 1195 2359

Return on Equity

Net Income /

Shareholder's

Equity 14.48% 8.10%

Net Assets 1195 2359

Sales 3272 3860

Asset Turnover Ratio

Net Income /

Shareholder's

Equity 36.52% 61.11%

Efficiency Ratios Green Plc Blue Plc

Inventory 273 89

1

a) Calculation of the ratios

Profitability ratio Green Plc Blue Plc

Employed Capital

(Total Assets -

Current

Liabilities) 3295 2559

Net operating profit 491 290

Return on capital employed

Net operating

profit/Employed

Capital 14.90% 11.33%

Cost of Sales 1636 2316

Sales 3272 3860

Gross Margin

Total Sales -

COGS/Total Sales 50.00% 40.00%

Net profit 173 191

Sales 3272 3860

Net profit ratio

Operating

Income/ Net Sales 5.29% 4.95%

Investor Ratios Green Plc Blue Plc

Net Income 173 191

Shareholder's Equity 1195 2359

Return on Equity

Net Income /

Shareholder's

Equity 14.48% 8.10%

Net Assets 1195 2359

Sales 3272 3860

Asset Turnover Ratio

Net Income /

Shareholder's

Equity 36.52% 61.11%

Efficiency Ratios Green Plc Blue Plc

Inventory 273 89

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

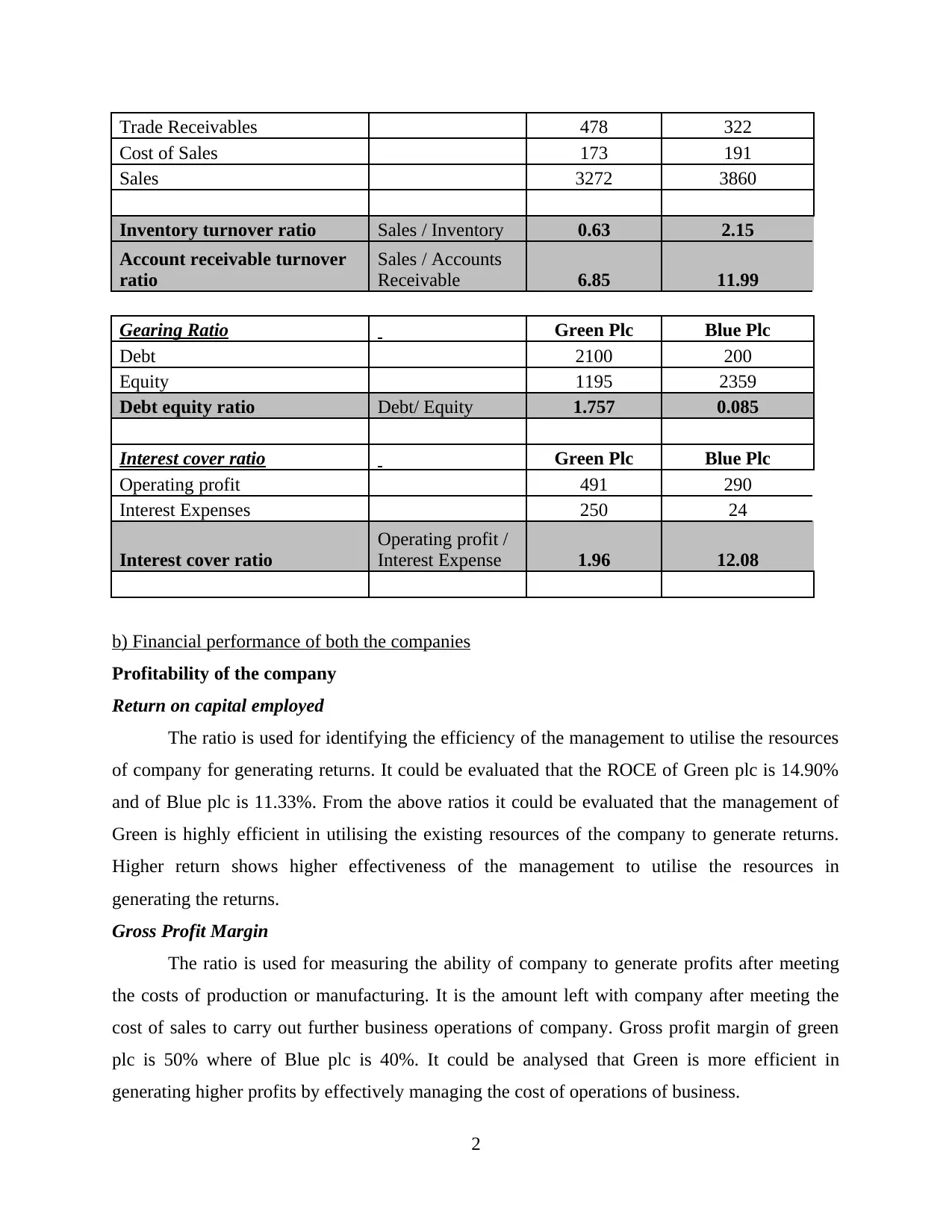

Trade Receivables 478 322

Cost of Sales 173 191

Sales 3272 3860

Inventory turnover ratio Sales / Inventory 0.63 2.15

Account receivable turnover

ratio

Sales / Accounts

Receivable 6.85 11.99

Gearing Ratio Green Plc Blue Plc

Debt 2100 200

Equity 1195 2359

Debt equity ratio Debt/ Equity 1.757 0.085

Interest cover ratio Green Plc Blue Plc

Operating profit 491 290

Interest Expenses 250 24

Interest cover ratio

Operating profit /

Interest Expense 1.96 12.08

b) Financial performance of both the companies

Profitability of the company

Return on capital employed

The ratio is used for identifying the efficiency of the management to utilise the resources

of company for generating returns. It could be evaluated that the ROCE of Green plc is 14.90%

and of Blue plc is 11.33%. From the above ratios it could be evaluated that the management of

Green is highly efficient in utilising the existing resources of the company to generate returns.

Higher return shows higher effectiveness of the management to utilise the resources in

generating the returns.

Gross Profit Margin

The ratio is used for measuring the ability of company to generate profits after meeting

the costs of production or manufacturing. It is the amount left with company after meeting the

cost of sales to carry out further business operations of company. Gross profit margin of green

plc is 50% where of Blue plc is 40%. It could be analysed that Green is more efficient in

generating higher profits by effectively managing the cost of operations of business.

2

Cost of Sales 173 191

Sales 3272 3860

Inventory turnover ratio Sales / Inventory 0.63 2.15

Account receivable turnover

ratio

Sales / Accounts

Receivable 6.85 11.99

Gearing Ratio Green Plc Blue Plc

Debt 2100 200

Equity 1195 2359

Debt equity ratio Debt/ Equity 1.757 0.085

Interest cover ratio Green Plc Blue Plc

Operating profit 491 290

Interest Expenses 250 24

Interest cover ratio

Operating profit /

Interest Expense 1.96 12.08

b) Financial performance of both the companies

Profitability of the company

Return on capital employed

The ratio is used for identifying the efficiency of the management to utilise the resources

of company for generating returns. It could be evaluated that the ROCE of Green plc is 14.90%

and of Blue plc is 11.33%. From the above ratios it could be evaluated that the management of

Green is highly efficient in utilising the existing resources of the company to generate returns.

Higher return shows higher effectiveness of the management to utilise the resources in

generating the returns.

Gross Profit Margin

The ratio is used for measuring the ability of company to generate profits after meeting

the costs of production or manufacturing. It is the amount left with company after meeting the

cost of sales to carry out further business operations of company. Gross profit margin of green

plc is 50% where of Blue plc is 40%. It could be analysed that Green is more efficient in

generating higher profits by effectively managing the cost of operations of business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

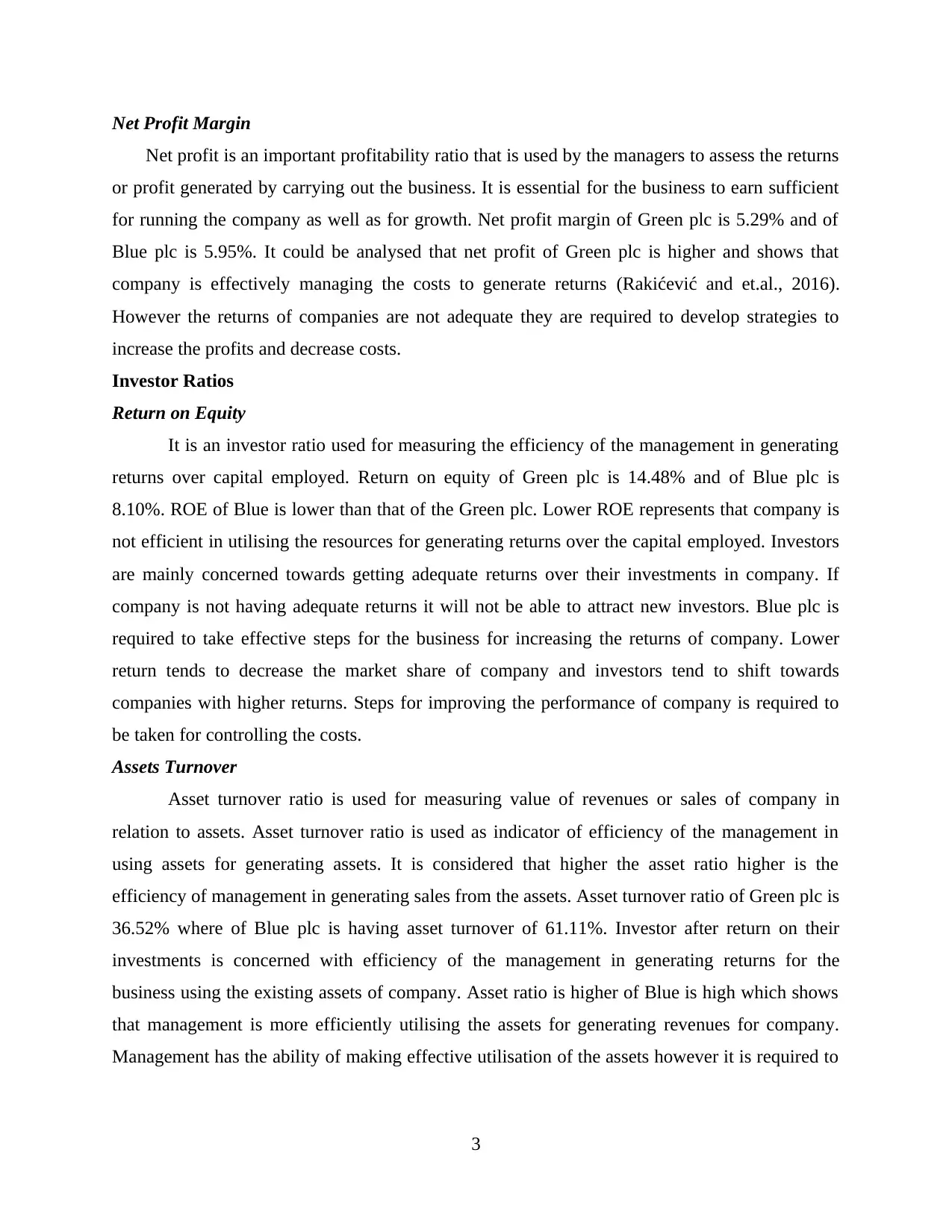

Net Profit Margin

Net profit is an important profitability ratio that is used by the managers to assess the returns

or profit generated by carrying out the business. It is essential for the business to earn sufficient

for running the company as well as for growth. Net profit margin of Green plc is 5.29% and of

Blue plc is 5.95%. It could be analysed that net profit of Green plc is higher and shows that

company is effectively managing the costs to generate returns (Rakićević and et.al., 2016).

However the returns of companies are not adequate they are required to develop strategies to

increase the profits and decrease costs.

Investor Ratios

Return on Equity

It is an investor ratio used for measuring the efficiency of the management in generating

returns over capital employed. Return on equity of Green plc is 14.48% and of Blue plc is

8.10%. ROE of Blue is lower than that of the Green plc. Lower ROE represents that company is

not efficient in utilising the resources for generating returns over the capital employed. Investors

are mainly concerned towards getting adequate returns over their investments in company. If

company is not having adequate returns it will not be able to attract new investors. Blue plc is

required to take effective steps for the business for increasing the returns of company. Lower

return tends to decrease the market share of company and investors tend to shift towards

companies with higher returns. Steps for improving the performance of company is required to

be taken for controlling the costs.

Assets Turnover

Asset turnover ratio is used for measuring value of revenues or sales of company in

relation to assets. Asset turnover ratio is used as indicator of efficiency of the management in

using assets for generating assets. It is considered that higher the asset ratio higher is the

efficiency of management in generating sales from the assets. Asset turnover ratio of Green plc is

36.52% where of Blue plc is having asset turnover of 61.11%. Investor after return on their

investments is concerned with efficiency of the management in generating returns for the

business using the existing assets of company. Asset ratio is higher of Blue is high which shows

that management is more efficiently utilising the assets for generating revenues for company.

Management has the ability of making effective utilisation of the assets however it is required to

3

Net profit is an important profitability ratio that is used by the managers to assess the returns

or profit generated by carrying out the business. It is essential for the business to earn sufficient

for running the company as well as for growth. Net profit margin of Green plc is 5.29% and of

Blue plc is 5.95%. It could be analysed that net profit of Green plc is higher and shows that

company is effectively managing the costs to generate returns (Rakićević and et.al., 2016).

However the returns of companies are not adequate they are required to develop strategies to

increase the profits and decrease costs.

Investor Ratios

Return on Equity

It is an investor ratio used for measuring the efficiency of the management in generating

returns over capital employed. Return on equity of Green plc is 14.48% and of Blue plc is

8.10%. ROE of Blue is lower than that of the Green plc. Lower ROE represents that company is

not efficient in utilising the resources for generating returns over the capital employed. Investors

are mainly concerned towards getting adequate returns over their investments in company. If

company is not having adequate returns it will not be able to attract new investors. Blue plc is

required to take effective steps for the business for increasing the returns of company. Lower

return tends to decrease the market share of company and investors tend to shift towards

companies with higher returns. Steps for improving the performance of company is required to

be taken for controlling the costs.

Assets Turnover

Asset turnover ratio is used for measuring value of revenues or sales of company in

relation to assets. Asset turnover ratio is used as indicator of efficiency of the management in

using assets for generating assets. It is considered that higher the asset ratio higher is the

efficiency of management in generating sales from the assets. Asset turnover ratio of Green plc is

36.52% where of Blue plc is having asset turnover of 61.11%. Investor after return on their

investments is concerned with efficiency of the management in generating returns for the

business using the existing assets of company. Asset ratio is higher of Blue is high which shows

that management is more efficiently utilising the assets for generating revenues for company.

Management has the ability of making effective utilisation of the assets however it is required to

3

be further increased by implementing new measures and strategies. To make effective allocation

of the resources in the company

Efficiency Ratios

Inventory Turnover Ratio

Inventory ratio measures the number of times inventory of company has been sold and

replaced by the company during the given time period. The ratio enables management to make

sound decisions on manufacturing, marketing, pricing and purchase of new inventory. Lower

turnover shows that there are weaker sales and stocks are in excess and higher ratio implies that

the stocks of company are lower and sales are stronger (Kourtis, Kourtis and Curtis, 2019).

Inventory turnover ratio is 0.63 of Green plc and 2.15 of Blue plc. Management of Blue is more

efficient in managing the inventory and generating sales. It could be analysed from the above

ratio that company is company is efficient moving its inventory and with higher frequency. The

strategies of the company are highly effective and enable the company to generate sales for the

business and moving inventories faster. Company is having more growth prospects as it helps in

maintain effective cash cycle.

Accounts Receivable Turnover Ratio

Receivables turnover measures efficiency of the company in collection of the credits

granted to the customers. It also measures the number of times receivables of company are

converted into cash within a year. It could be calculated as per requirement of company that is

quarterly, half yearly or annually. Receivables turnover are 6.85 of Green plc and 12 of the Blue

plc. From the above ratio it could be analysed that the collection of Blue is more frequent and

stronger as compared with Green which is having lower turnover. It shows that Green is not

efficient and strong in the collection of money from the customers for good given on credit. It

gives higher credit to the customers to increase the revenues and sales. It is a strategy used by the

companies for increasing their customer base and to provide the business with increased

revenues and sales. Efficiency in collection of receivables is important for effectively managing

the cash cycle and for meeting the working capital requirements

Gearing Ratio

The ratio is used for measuring the proportion of borrowed capital to equity. Gearing

ratio of companies are 1.757 and 0.085. It could be seen that ratio of Green plc is higher as it

uses more of the debts against its equity and where of Blue plc is only 0.085 which is

4

of the resources in the company

Efficiency Ratios

Inventory Turnover Ratio

Inventory ratio measures the number of times inventory of company has been sold and

replaced by the company during the given time period. The ratio enables management to make

sound decisions on manufacturing, marketing, pricing and purchase of new inventory. Lower

turnover shows that there are weaker sales and stocks are in excess and higher ratio implies that

the stocks of company are lower and sales are stronger (Kourtis, Kourtis and Curtis, 2019).

Inventory turnover ratio is 0.63 of Green plc and 2.15 of Blue plc. Management of Blue is more

efficient in managing the inventory and generating sales. It could be analysed from the above

ratio that company is company is efficient moving its inventory and with higher frequency. The

strategies of the company are highly effective and enable the company to generate sales for the

business and moving inventories faster. Company is having more growth prospects as it helps in

maintain effective cash cycle.

Accounts Receivable Turnover Ratio

Receivables turnover measures efficiency of the company in collection of the credits

granted to the customers. It also measures the number of times receivables of company are

converted into cash within a year. It could be calculated as per requirement of company that is

quarterly, half yearly or annually. Receivables turnover are 6.85 of Green plc and 12 of the Blue

plc. From the above ratio it could be analysed that the collection of Blue is more frequent and

stronger as compared with Green which is having lower turnover. It shows that Green is not

efficient and strong in the collection of money from the customers for good given on credit. It

gives higher credit to the customers to increase the revenues and sales. It is a strategy used by the

companies for increasing their customer base and to provide the business with increased

revenues and sales. Efficiency in collection of receivables is important for effectively managing

the cash cycle and for meeting the working capital requirements

Gearing Ratio

The ratio is used for measuring the proportion of borrowed capital to equity. Gearing

ratio of companies are 1.757 and 0.085. It could be seen that ratio of Green plc is higher as it

uses more of the debts against its equity and where of Blue plc is only 0.085 which is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

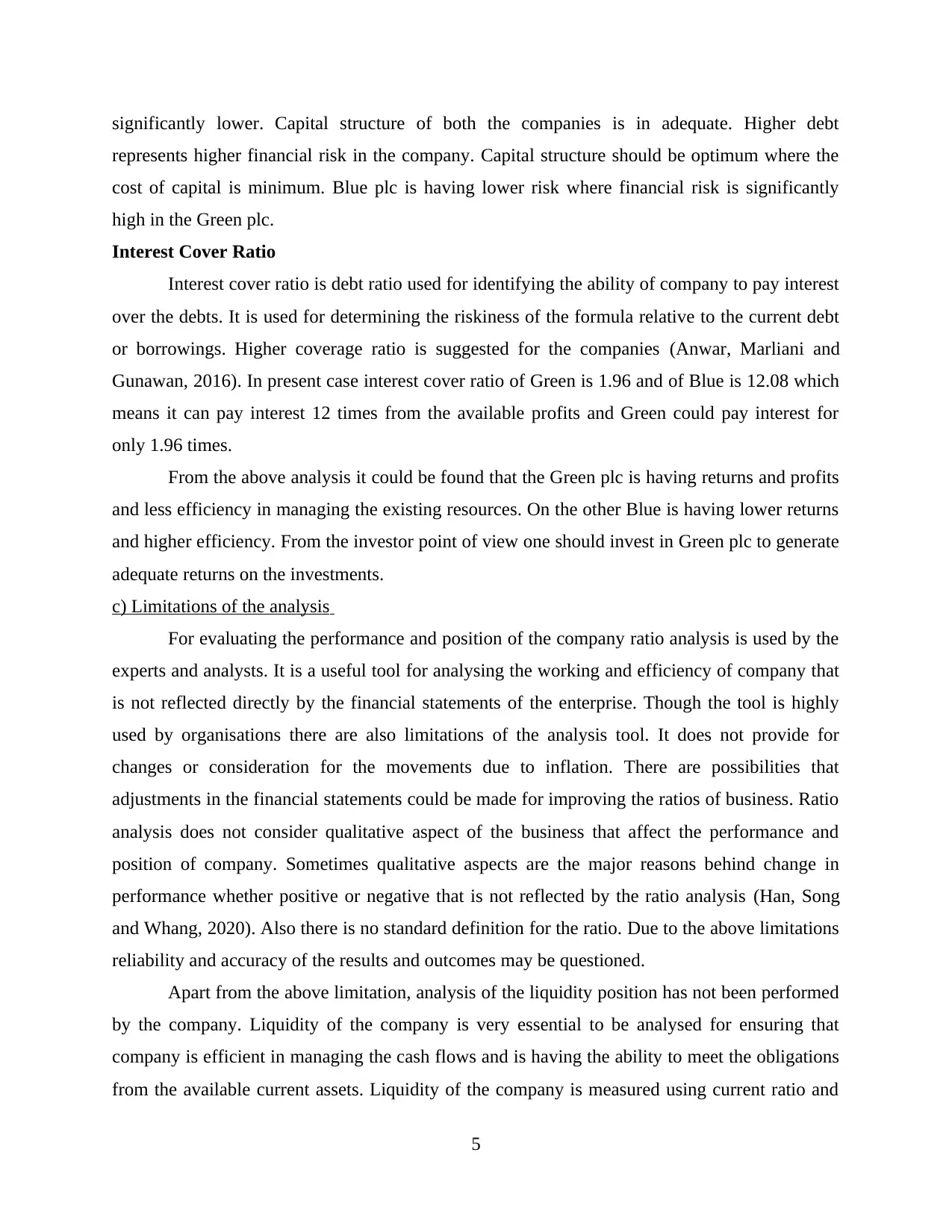

significantly lower. Capital structure of both the companies is in adequate. Higher debt

represents higher financial risk in the company. Capital structure should be optimum where the

cost of capital is minimum. Blue plc is having lower risk where financial risk is significantly

high in the Green plc.

Interest Cover Ratio

Interest cover ratio is debt ratio used for identifying the ability of company to pay interest

over the debts. It is used for determining the riskiness of the formula relative to the current debt

or borrowings. Higher coverage ratio is suggested for the companies (Anwar, Marliani and

Gunawan, 2016). In present case interest cover ratio of Green is 1.96 and of Blue is 12.08 which

means it can pay interest 12 times from the available profits and Green could pay interest for

only 1.96 times.

From the above analysis it could be found that the Green plc is having returns and profits

and less efficiency in managing the existing resources. On the other Blue is having lower returns

and higher efficiency. From the investor point of view one should invest in Green plc to generate

adequate returns on the investments.

c) Limitations of the analysis

For evaluating the performance and position of the company ratio analysis is used by the

experts and analysts. It is a useful tool for analysing the working and efficiency of company that

is not reflected directly by the financial statements of the enterprise. Though the tool is highly

used by organisations there are also limitations of the analysis tool. It does not provide for

changes or consideration for the movements due to inflation. There are possibilities that

adjustments in the financial statements could be made for improving the ratios of business. Ratio

analysis does not consider qualitative aspect of the business that affect the performance and

position of company. Sometimes qualitative aspects are the major reasons behind change in

performance whether positive or negative that is not reflected by the ratio analysis (Han, Song

and Whang, 2020). Also there is no standard definition for the ratio. Due to the above limitations

reliability and accuracy of the results and outcomes may be questioned.

Apart from the above limitation, analysis of the liquidity position has not been performed

by the company. Liquidity of the company is very essential to be analysed for ensuring that

company is efficient in managing the cash flows and is having the ability to meet the obligations

from the available current assets. Liquidity of the company is measured using current ratio and

5

represents higher financial risk in the company. Capital structure should be optimum where the

cost of capital is minimum. Blue plc is having lower risk where financial risk is significantly

high in the Green plc.

Interest Cover Ratio

Interest cover ratio is debt ratio used for identifying the ability of company to pay interest

over the debts. It is used for determining the riskiness of the formula relative to the current debt

or borrowings. Higher coverage ratio is suggested for the companies (Anwar, Marliani and

Gunawan, 2016). In present case interest cover ratio of Green is 1.96 and of Blue is 12.08 which

means it can pay interest 12 times from the available profits and Green could pay interest for

only 1.96 times.

From the above analysis it could be found that the Green plc is having returns and profits

and less efficiency in managing the existing resources. On the other Blue is having lower returns

and higher efficiency. From the investor point of view one should invest in Green plc to generate

adequate returns on the investments.

c) Limitations of the analysis

For evaluating the performance and position of the company ratio analysis is used by the

experts and analysts. It is a useful tool for analysing the working and efficiency of company that

is not reflected directly by the financial statements of the enterprise. Though the tool is highly

used by organisations there are also limitations of the analysis tool. It does not provide for

changes or consideration for the movements due to inflation. There are possibilities that

adjustments in the financial statements could be made for improving the ratios of business. Ratio

analysis does not consider qualitative aspect of the business that affect the performance and

position of company. Sometimes qualitative aspects are the major reasons behind change in

performance whether positive or negative that is not reflected by the ratio analysis (Han, Song

and Whang, 2020). Also there is no standard definition for the ratio. Due to the above limitations

reliability and accuracy of the results and outcomes may be questioned.

Apart from the above limitation, analysis of the liquidity position has not been performed

by the company. Liquidity of the company is very essential to be analysed for ensuring that

company is efficient in managing the cash flows and is having the ability to meet the obligations

from the available current assets. Liquidity of the company is measured using current ratio and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

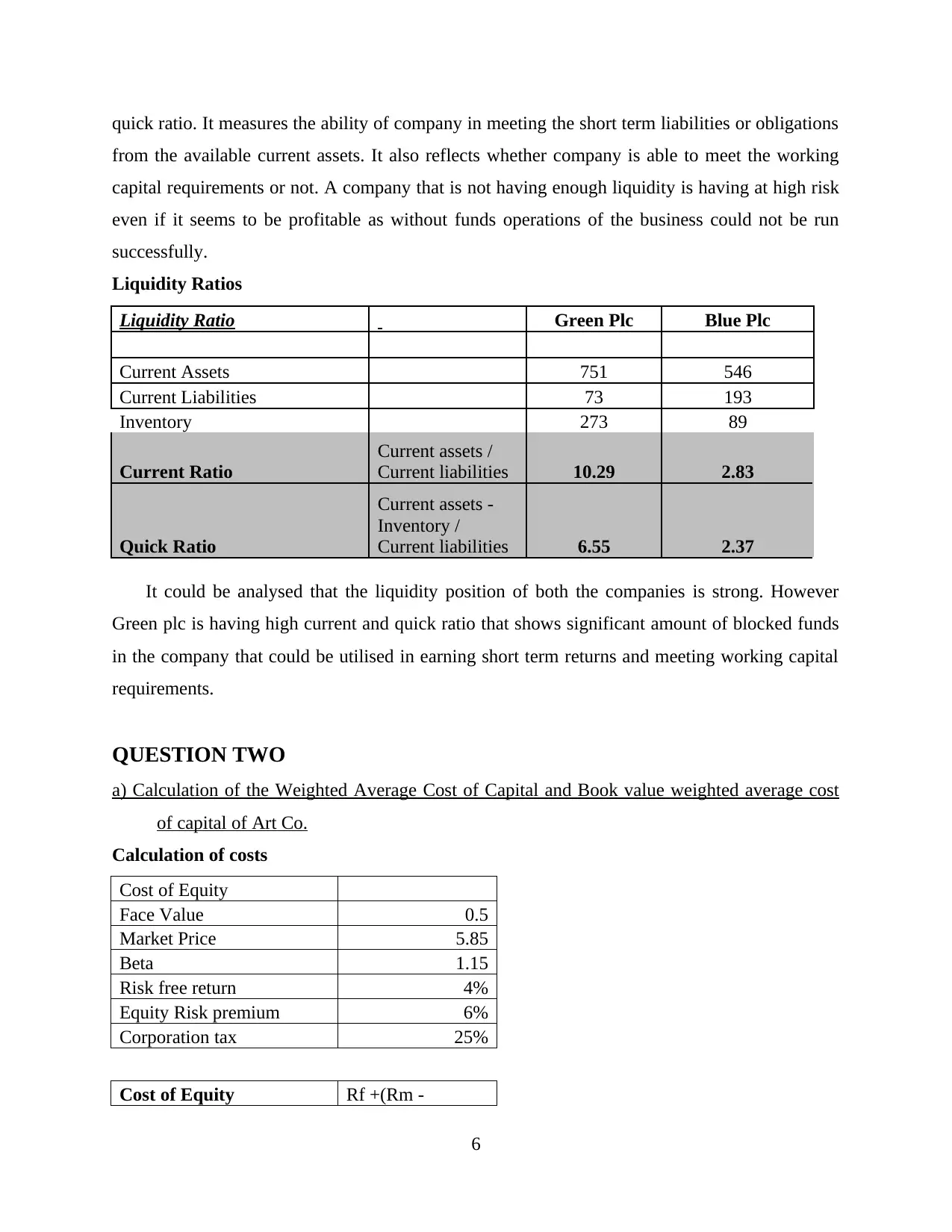

quick ratio. It measures the ability of company in meeting the short term liabilities or obligations

from the available current assets. It also reflects whether company is able to meet the working

capital requirements or not. A company that is not having enough liquidity is having at high risk

even if it seems to be profitable as without funds operations of the business could not be run

successfully.

Liquidity Ratios

Liquidity Ratio Green Plc Blue Plc

Current Assets 751 546

Current Liabilities 73 193

Inventory 273 89

Current Ratio

Current assets /

Current liabilities 10.29 2.83

Quick Ratio

Current assets -

Inventory /

Current liabilities 6.55 2.37

It could be analysed that the liquidity position of both the companies is strong. However

Green plc is having high current and quick ratio that shows significant amount of blocked funds

in the company that could be utilised in earning short term returns and meeting working capital

requirements.

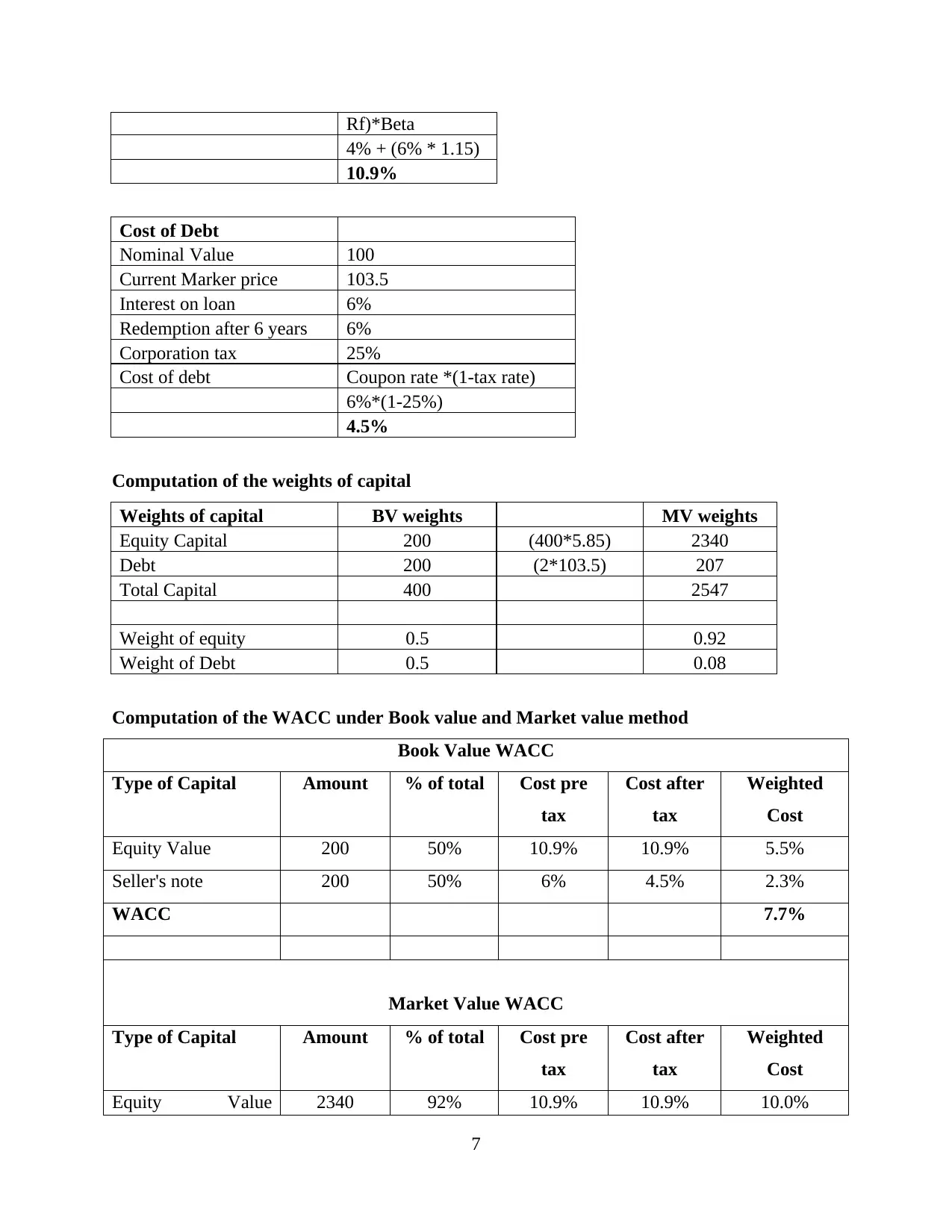

QUESTION TWO

a) Calculation of the Weighted Average Cost of Capital and Book value weighted average cost

of capital of Art Co.

Calculation of costs

Cost of Equity

Face Value 0.5

Market Price 5.85

Beta 1.15

Risk free return 4%

Equity Risk premium 6%

Corporation tax 25%

Cost of Equity Rf +(Rm -

6

from the available current assets. It also reflects whether company is able to meet the working

capital requirements or not. A company that is not having enough liquidity is having at high risk

even if it seems to be profitable as without funds operations of the business could not be run

successfully.

Liquidity Ratios

Liquidity Ratio Green Plc Blue Plc

Current Assets 751 546

Current Liabilities 73 193

Inventory 273 89

Current Ratio

Current assets /

Current liabilities 10.29 2.83

Quick Ratio

Current assets -

Inventory /

Current liabilities 6.55 2.37

It could be analysed that the liquidity position of both the companies is strong. However

Green plc is having high current and quick ratio that shows significant amount of blocked funds

in the company that could be utilised in earning short term returns and meeting working capital

requirements.

QUESTION TWO

a) Calculation of the Weighted Average Cost of Capital and Book value weighted average cost

of capital of Art Co.

Calculation of costs

Cost of Equity

Face Value 0.5

Market Price 5.85

Beta 1.15

Risk free return 4%

Equity Risk premium 6%

Corporation tax 25%

Cost of Equity Rf +(Rm -

6

Rf)*Beta

4% + (6% * 1.15)

10.9%

Cost of Debt

Nominal Value 100

Current Marker price 103.5

Interest on loan 6%

Redemption after 6 years 6%

Corporation tax 25%

Cost of debt Coupon rate *(1-tax rate)

6%*(1-25%)

4.5%

Computation of the weights of capital

Weights of capital BV weights MV weights

Equity Capital 200 (400*5.85) 2340

Debt 200 (2*103.5) 207

Total Capital 400 2547

Weight of equity 0.5 0.92

Weight of Debt 0.5 0.08

Computation of the WACC under Book value and Market value method

Book Value WACC

Type of Capital Amount % of total Cost pre

tax

Cost after

tax

Weighted

Cost

Equity Value 200 50% 10.9% 10.9% 5.5%

Seller's note 200 50% 6% 4.5% 2.3%

WACC 7.7%

Market Value WACC

Type of Capital Amount % of total Cost pre

tax

Cost after

tax

Weighted

Cost

Equity Value 2340 92% 10.9% 10.9% 10.0%

7

4% + (6% * 1.15)

10.9%

Cost of Debt

Nominal Value 100

Current Marker price 103.5

Interest on loan 6%

Redemption after 6 years 6%

Corporation tax 25%

Cost of debt Coupon rate *(1-tax rate)

6%*(1-25%)

4.5%

Computation of the weights of capital

Weights of capital BV weights MV weights

Equity Capital 200 (400*5.85) 2340

Debt 200 (2*103.5) 207

Total Capital 400 2547

Weight of equity 0.5 0.92

Weight of Debt 0.5 0.08

Computation of the WACC under Book value and Market value method

Book Value WACC

Type of Capital Amount % of total Cost pre

tax

Cost after

tax

Weighted

Cost

Equity Value 200 50% 10.9% 10.9% 5.5%

Seller's note 200 50% 6% 4.5% 2.3%

WACC 7.7%

Market Value WACC

Type of Capital Amount % of total Cost pre

tax

Cost after

tax

Weighted

Cost

Equity Value 2340 92% 10.9% 10.9% 10.0%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(400*5.85)

Seller's note

(2*103.5)

207 8% 6.0% 4.5% 0.4%

WACC 10.4%

It could be evaluated that the cost of capital is different in both the methods. Cost of

capital under book value weights is 7.7% and under market value is 10.4%. The difference

between the two is due to the weights of debt and equity under both the approaches. In book

value WACC weights are derived on the basis of nominal value of the equity and debt at which

they are booked in the financial statements of the company. On the other, in market value

WACC it could be seen that the weights are different as the value of equity and debt is

considered on the basis of market value. Market value are generally higher than the book values

that changes the proportion of debt and equity in terms of value thereby changing the whole cost

of capital. WACC of company under market value is considered as more appropriate and reliable

as it reflects the true cost of capital of company (Drobetz and et.al., 2018). Company is having

significant amount of equity capital as against the equity.

A company should have appropriate mix of the capital where cost of capital is least. As

per the book value capital structure is adequate whereas per market value it is having equity

capital.

b) Circumstances where the weighted average cost of capital of company could be used in the

investment appraisal techniques and limitations as discount rate.

Weighted average cost of capital is the weighted average debt, equity and preference

share cost and are weights are percentage of the capital sourced from every component in terms

of market value. WACC is mainly used by investors and management for prompt decision

making. Limitations of the method are its restricted scope of the application and rigid

assumptions to be taken for evaluating the projects.

The WACC could be used as discount rate in the investment appraisal if the risk of

investment project that is evaluated is equivalent or similar to current risk of investing firm.

WACC then will be reflecting and representing average rate of return as compensation for the

risks. It could be used for the investment appraisal if the business risks of proposed investments

8

Seller's note

(2*103.5)

207 8% 6.0% 4.5% 0.4%

WACC 10.4%

It could be evaluated that the cost of capital is different in both the methods. Cost of

capital under book value weights is 7.7% and under market value is 10.4%. The difference

between the two is due to the weights of debt and equity under both the approaches. In book

value WACC weights are derived on the basis of nominal value of the equity and debt at which

they are booked in the financial statements of the company. On the other, in market value

WACC it could be seen that the weights are different as the value of equity and debt is

considered on the basis of market value. Market value are generally higher than the book values

that changes the proportion of debt and equity in terms of value thereby changing the whole cost

of capital. WACC of company under market value is considered as more appropriate and reliable

as it reflects the true cost of capital of company (Drobetz and et.al., 2018). Company is having

significant amount of equity capital as against the equity.

A company should have appropriate mix of the capital where cost of capital is least. As

per the book value capital structure is adequate whereas per market value it is having equity

capital.

b) Circumstances where the weighted average cost of capital of company could be used in the

investment appraisal techniques and limitations as discount rate.

Weighted average cost of capital is the weighted average debt, equity and preference

share cost and are weights are percentage of the capital sourced from every component in terms

of market value. WACC is mainly used by investors and management for prompt decision

making. Limitations of the method are its restricted scope of the application and rigid

assumptions to be taken for evaluating the projects.

The WACC could be used as discount rate in the investment appraisal if the risk of

investment project that is evaluated is equivalent or similar to current risk of investing firm.

WACC then will be reflecting and representing average rate of return as compensation for the

risks. It could be used for the investment appraisal if the business risks of proposed investments

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are similar to business risks of the existing operations (Frank and Shen, 2016). It means that

WACC could be used for evaluating the expansion of the existing business.

If business risk of investment option is different from business risks of the existing

operations than the discount rates that are project specific reflecting business risks of investment

option are to be considered. Capital asset pricing model is also used by the analysts in the

investment appraisals where financial risks of proposed investment are same as financial risk of

the existing operations. It means that the financing for project to be raised in proportion that

could broadly preserve capital structure of investing company. If case is different than this the

investment appraisal technique known as adjusted present value is used. On the other CAPM

computed specific project cost of capital could be adjusted for reflecting financial risks of project

financing.

Third constraint over using the WACC in the investment appraisal is that proposed

investment option should be smaller as compared with size of company. If this was not case,

scale of investment project can cause changes to occur in perceived risk of investing company

making existing WACC inappropriate rate of discount.

Comparison with the other investments is based on time value of money linked to risk of

the future cash flows. WACC reflects risk to future cash flows that will be received by the

organisation from the operations. Company with lower WACC are seen as having lower risks

attached over the cash that will be generated in future. It is used as the discount rate as it is the

cost which company pays for capital that is used for investing in operations. a company is aimed

at achieving at least this much return from the proposed investments so that it could cover the

costs of raising the funds for project (El Ghou and et.al., 2018). If the company is not able to

achieve at least this return then the project is considered to be of high risk where company will

be suffering losses.

QUESTION THREE

Objectives of the working capital management and central role of working capital in financial

management

Working capital management refers to the business strategy which is designed for

ensuring that company is operating effectively by monitoring and by using the current assets and

liabilities in the best possible manner. Primary purpose of the working capital management is of

enabling company to have sufficient cash flows for meeting the short term operational costs and

9

WACC could be used for evaluating the expansion of the existing business.

If business risk of investment option is different from business risks of the existing

operations than the discount rates that are project specific reflecting business risks of investment

option are to be considered. Capital asset pricing model is also used by the analysts in the

investment appraisals where financial risks of proposed investment are same as financial risk of

the existing operations. It means that the financing for project to be raised in proportion that

could broadly preserve capital structure of investing company. If case is different than this the

investment appraisal technique known as adjusted present value is used. On the other CAPM

computed specific project cost of capital could be adjusted for reflecting financial risks of project

financing.

Third constraint over using the WACC in the investment appraisal is that proposed

investment option should be smaller as compared with size of company. If this was not case,

scale of investment project can cause changes to occur in perceived risk of investing company

making existing WACC inappropriate rate of discount.

Comparison with the other investments is based on time value of money linked to risk of

the future cash flows. WACC reflects risk to future cash flows that will be received by the

organisation from the operations. Company with lower WACC are seen as having lower risks

attached over the cash that will be generated in future. It is used as the discount rate as it is the

cost which company pays for capital that is used for investing in operations. a company is aimed

at achieving at least this much return from the proposed investments so that it could cover the

costs of raising the funds for project (El Ghou and et.al., 2018). If the company is not able to

achieve at least this return then the project is considered to be of high risk where company will

be suffering losses.

QUESTION THREE

Objectives of the working capital management and central role of working capital in financial

management

Working capital management refers to the business strategy which is designed for

ensuring that company is operating effectively by monitoring and by using the current assets and

liabilities in the best possible manner. Primary purpose of the working capital management is of

enabling company to have sufficient cash flows for meeting the short term operational costs and

9

the short term obligations (Afrifa and Padachi, 2016). Working capital of the company is derived

by deducting current liabilities from the current assets.

Primary objective of the working capital is to ensure that operating cycle of the business

is smooth. Secondary objective is of optimizing level of the working capital and minimising cost

of the funds. Major objective of the working capital in financial management is to help company

in wealth maximisation and it could be gained by the profit maximisation along with sustainable

development and growth of the business. Objectives of stakeholders should be aligned with

growth of organisation.

Objective of the working capital management is smooth flow of operating cycle. It

implies that operating cycle from acquisition of raw materials to conversion in cash is smooth. It

is a complex process. It requires that raw material is present on demand and does not lead to

interruptions in production. Sale of the finished goods should be made at the earliest.

Lowest working capital which refers current assets minus current liabilities. It aims at

having optimum working capital as higher capital will lead to increased interest cost and where

lower capital will lead to disturbance in the operating cycle.

Another objective if the working capital management is minimising cost of capital or the

interest costs. Costs that are used in the working capital are to be minimised for achieving higher

profitability. Sources where the cost is minimum should be used (Le, 2019). Costs are also

minimised using long term borrowings with proper mix.

Working capital management also involves monitoring the cash flows, current liabilities

and the current assets by ratio analysis. It is very essential for maintain smooth flow of the cash

conversion cycle. It ensures that company takes minimum time to convert the current assets and

liabilities to cash. It enables company to improve the profitability by efficient use of the

resources. It also includes inventory management ensuring that inventory is moving fast and

generating revenues for the business.

Role of working capital in financial management

Working capital is the part of total assets of company. It is difference between the current

assets as well as current liabilities. It is required for meeting day to day operations of the

business and it is essential that company is having enough funds for meeting the working capital

requirements. In financial management working capital refers to process of management of short

10

by deducting current liabilities from the current assets.

Primary objective of the working capital is to ensure that operating cycle of the business

is smooth. Secondary objective is of optimizing level of the working capital and minimising cost

of the funds. Major objective of the working capital in financial management is to help company

in wealth maximisation and it could be gained by the profit maximisation along with sustainable

development and growth of the business. Objectives of stakeholders should be aligned with

growth of organisation.

Objective of the working capital management is smooth flow of operating cycle. It

implies that operating cycle from acquisition of raw materials to conversion in cash is smooth. It

is a complex process. It requires that raw material is present on demand and does not lead to

interruptions in production. Sale of the finished goods should be made at the earliest.

Lowest working capital which refers current assets minus current liabilities. It aims at

having optimum working capital as higher capital will lead to increased interest cost and where

lower capital will lead to disturbance in the operating cycle.

Another objective if the working capital management is minimising cost of capital or the

interest costs. Costs that are used in the working capital are to be minimised for achieving higher

profitability. Sources where the cost is minimum should be used (Le, 2019). Costs are also

minimised using long term borrowings with proper mix.

Working capital management also involves monitoring the cash flows, current liabilities

and the current assets by ratio analysis. It is very essential for maintain smooth flow of the cash

conversion cycle. It ensures that company takes minimum time to convert the current assets and

liabilities to cash. It enables company to improve the profitability by efficient use of the

resources. It also includes inventory management ensuring that inventory is moving fast and

generating revenues for the business.

Role of working capital in financial management

Working capital is the part of total assets of company. It is difference between the current

assets as well as current liabilities. It is required for meeting day to day operations of the

business and it is essential that company is having enough funds for meeting the working capital

requirements. In financial management working capital refers to process of management of short

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.