LCBB6002: International Financial Management - Assessment 2 Analysis

VerifiedAdded on 2022/12/15

|15

|3394

|393

Homework Assignment

AI Summary

This assignment on International Financial Management (IFM) analyzes investment decision-making using Net Present Value (NPV) and Internal Rate of Return (IRR) methods. It includes calculations of NPV, standard deviation, and expected values for various projects under different scenarios. The assignment evaluates the profitability of projects, compares the NPV and IRR techniques, and determines optimal capital allocation to maximize returns. The analysis covers initial investments, cash flow projections, risk assessments, and the probability of achieving specific financial outcomes. The document provides detailed calculations, rankings of projects, and justifications for investment choices, offering a comprehensive understanding of financial management principles and practical applications.

INTERNATIONAL

FINANCIAL

MANAGEMENT

[ASSESSMENT 2]

1

FINANCIAL

MANAGEMENT

[ASSESSMENT 2]

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question: 1.......................................................................................................................................3

Question: 2.......................................................................................................................................5

Question: 3.......................................................................................................................................8

a) Calculation of Net Present Value of four projects...................................................................8

b) Reasons for regarding Net Present Value technique superior to internal rate of Return while

project appraisal...........................................................................................................................9

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value..........................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question: 1.......................................................................................................................................3

Question: 2.......................................................................................................................................5

Question: 3.......................................................................................................................................8

a) Calculation of Net Present Value of four projects...................................................................8

b) Reasons for regarding Net Present Value technique superior to internal rate of Return while

project appraisal...........................................................................................................................9

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value..........................................................................................................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

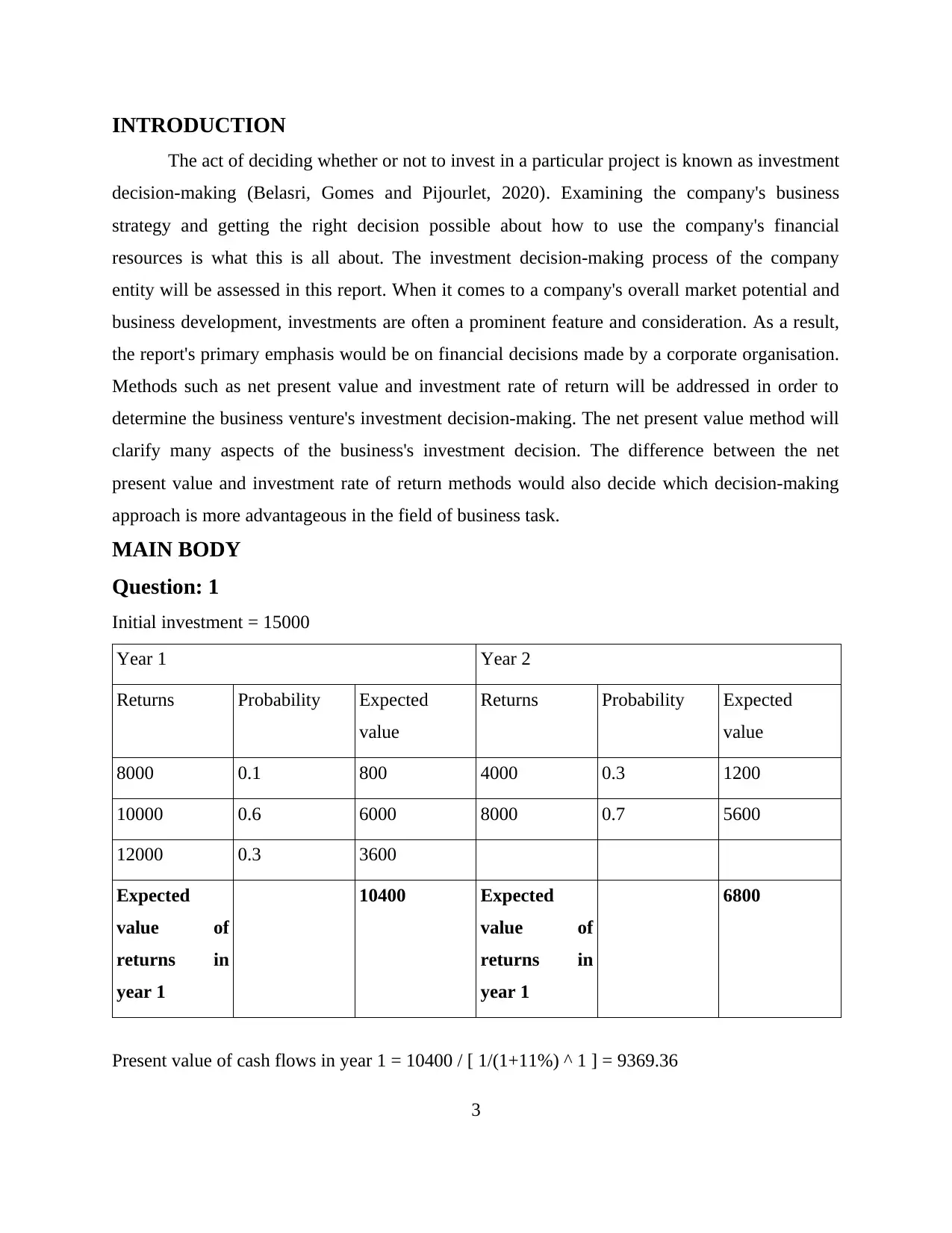

INTRODUCTION

The act of deciding whether or not to invest in a particular project is known as investment

decision-making (Belasri, Gomes and Pijourlet, 2020). Examining the company's business

strategy and getting the right decision possible about how to use the company's financial

resources is what this is all about. The investment decision-making process of the company

entity will be assessed in this report. When it comes to a company's overall market potential and

business development, investments are often a prominent feature and consideration. As a result,

the report's primary emphasis would be on financial decisions made by a corporate organisation.

Methods such as net present value and investment rate of return will be addressed in order to

determine the business venture's investment decision-making. The net present value method will

clarify many aspects of the business's investment decision. The difference between the net

present value and investment rate of return methods would also decide which decision-making

approach is more advantageous in the field of business task.

MAIN BODY

Question: 1

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

3

The act of deciding whether or not to invest in a particular project is known as investment

decision-making (Belasri, Gomes and Pijourlet, 2020). Examining the company's business

strategy and getting the right decision possible about how to use the company's financial

resources is what this is all about. The investment decision-making process of the company

entity will be assessed in this report. When it comes to a company's overall market potential and

business development, investments are often a prominent feature and consideration. As a result,

the report's primary emphasis would be on financial decisions made by a corporate organisation.

Methods such as net present value and investment rate of return will be addressed in order to

determine the business venture's investment decision-making. The net present value method will

clarify many aspects of the business's investment decision. The difference between the net

present value and investment rate of return methods would also decide which decision-making

approach is more advantageous in the field of business task.

MAIN BODY

Question: 1

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Present Value of cash flows in year 2 = 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Present value of cash inflows = 14891

a) Net present value of the project = present value of cash inflows – initial investment = (109).

Thus, if the program's net present value (NPV) is negative, that ensures that the project

will result in a net loss for the company, and the company will not continue the project because it

does not appear to be competitive in today's market, according to the current rules of NPV. A

significant reduction in the expected value of the proposal's returns compared to year 1 may be

the reason for the project's negative net present value. The business company will now gain

capital appreciation by investing in the new project as a result of the current project. It is

important in the sense of each project that the business entity earns a higher return on its initial

investment (De Smet, Mention and Torkkeli, 2016). The net present value strategy's basic

premise is that the project's total future inflow must exceed the project's total expenditure. The

above results clearly demonstrate that at this stage of the project's growth, the business enterprise

is incapable of achieving a positive npv outcome.

The company expects to lose money in the second year due to lower inflow, as seen in

the graph above. Since the first year's inflow was so high, the second year's inflow could be half

as high. All of this suggests that the business would lose money on the project. Negative present

value is a weakness in the project because it basically means that if the company invests in it, it

will lose money when it is finished (Duque-Grisales and Aguilera-Caracuel, 2019).

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

4

Present value of cash inflows = 14891

a) Net present value of the project = present value of cash inflows – initial investment = (109).

Thus, if the program's net present value (NPV) is negative, that ensures that the project

will result in a net loss for the company, and the company will not continue the project because it

does not appear to be competitive in today's market, according to the current rules of NPV. A

significant reduction in the expected value of the proposal's returns compared to year 1 may be

the reason for the project's negative net present value. The business company will now gain

capital appreciation by investing in the new project as a result of the current project. It is

important in the sense of each project that the business entity earns a higher return on its initial

investment (De Smet, Mention and Torkkeli, 2016). The net present value strategy's basic

premise is that the project's total future inflow must exceed the project's total expenditure. The

above results clearly demonstrate that at this stage of the project's growth, the business enterprise

is incapable of achieving a positive npv outcome.

The company expects to lose money in the second year due to lower inflow, as seen in

the graph above. Since the first year's inflow was so high, the second year's inflow could be half

as high. All of this suggests that the business would lose money on the project. Negative present

value is a weakness in the project because it basically means that if the company invests in it, it

will lose money when it is finished (Duque-Grisales and Aguilera-Caracuel, 2019).

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard deviation of returns in year 1 = square root of σ2 = σ = 1200.

The standard deviation of various possible cash flow scenarios from the project in Year 1

is 1200, meaning that different cash flow events deviate by 1200 from the project's expected

return in Year 1.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

The standard deviation of numerous alternate cash flow results from the plan in year 2 is

1833, meaning that different cash flow outcomes in year 2 deviate from the project's expected

return by 1833 (Enomoto, Kimura and Yamaguchi, 2018).

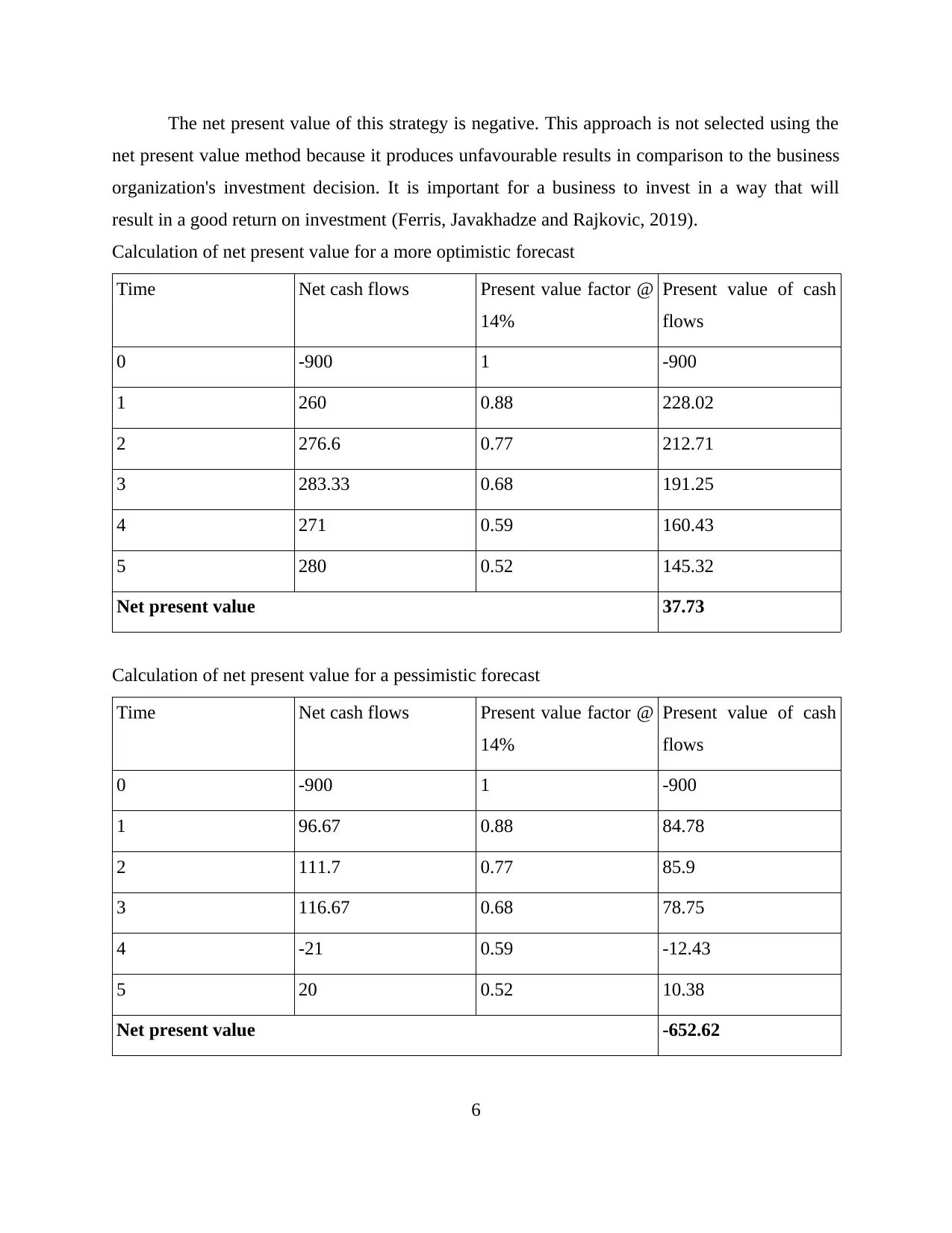

Question: 2

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

5

The standard deviation of various possible cash flow scenarios from the project in Year 1

is 1200, meaning that different cash flow events deviate by 1200 from the project's expected

return in Year 1.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

The standard deviation of numerous alternate cash flow results from the plan in year 2 is

1833, meaning that different cash flow outcomes in year 2 deviate from the project's expected

return by 1833 (Enomoto, Kimura and Yamaguchi, 2018).

Question: 2

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

5

The net present value of this strategy is negative. This approach is not selected using the

net present value method because it produces unfavourable results in comparison to the business

organization's investment decision. It is important for a business to invest in a way that will

result in a good return on investment (Ferris, Javakhadze and Rajkovic, 2019).

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

6

net present value method because it produces unfavourable results in comparison to the business

organization's investment decision. It is important for a business to invest in a way that will

result in a good return on investment (Ferris, Javakhadze and Rajkovic, 2019).

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

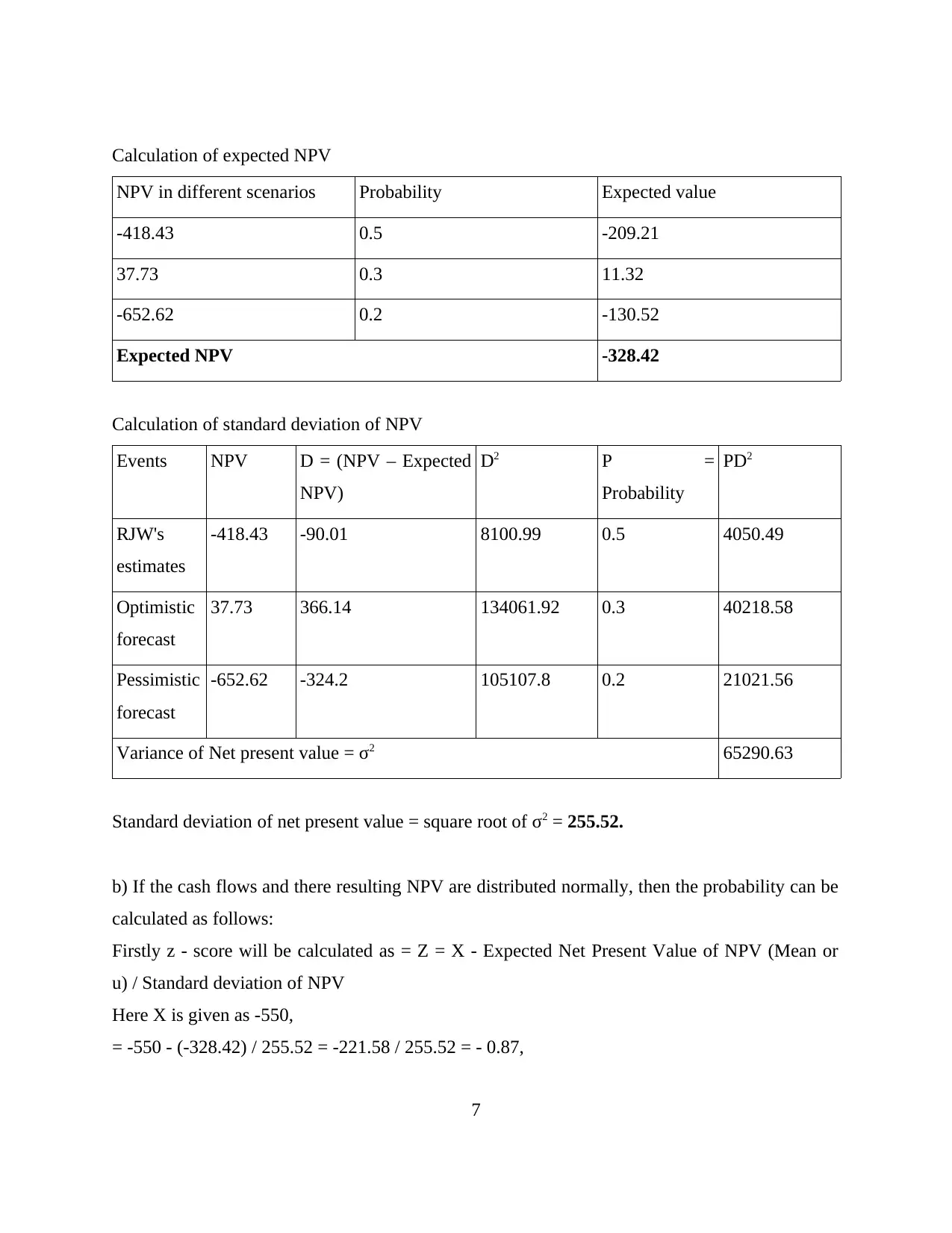

Calculation of expected NPV

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) If the cash flows and there resulting NPV are distributed normally, then the probability can be

calculated as follows:

Firstly z - score will be calculated as = Z = X - Expected Net Present Value of NPV (Mean or

u) / Standard deviation of NPV

Here X is given as -550,

= -550 - (-328.42) / 255.52 = -221.58 / 255.52 = - 0.87,

7

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) If the cash flows and there resulting NPV are distributed normally, then the probability can be

calculated as follows:

Firstly z - score will be calculated as = Z = X - Expected Net Present Value of NPV (Mean or

u) / Standard deviation of NPV

Here X is given as -550,

= -550 - (-328.42) / 255.52 = -221.58 / 255.52 = - 0.87,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

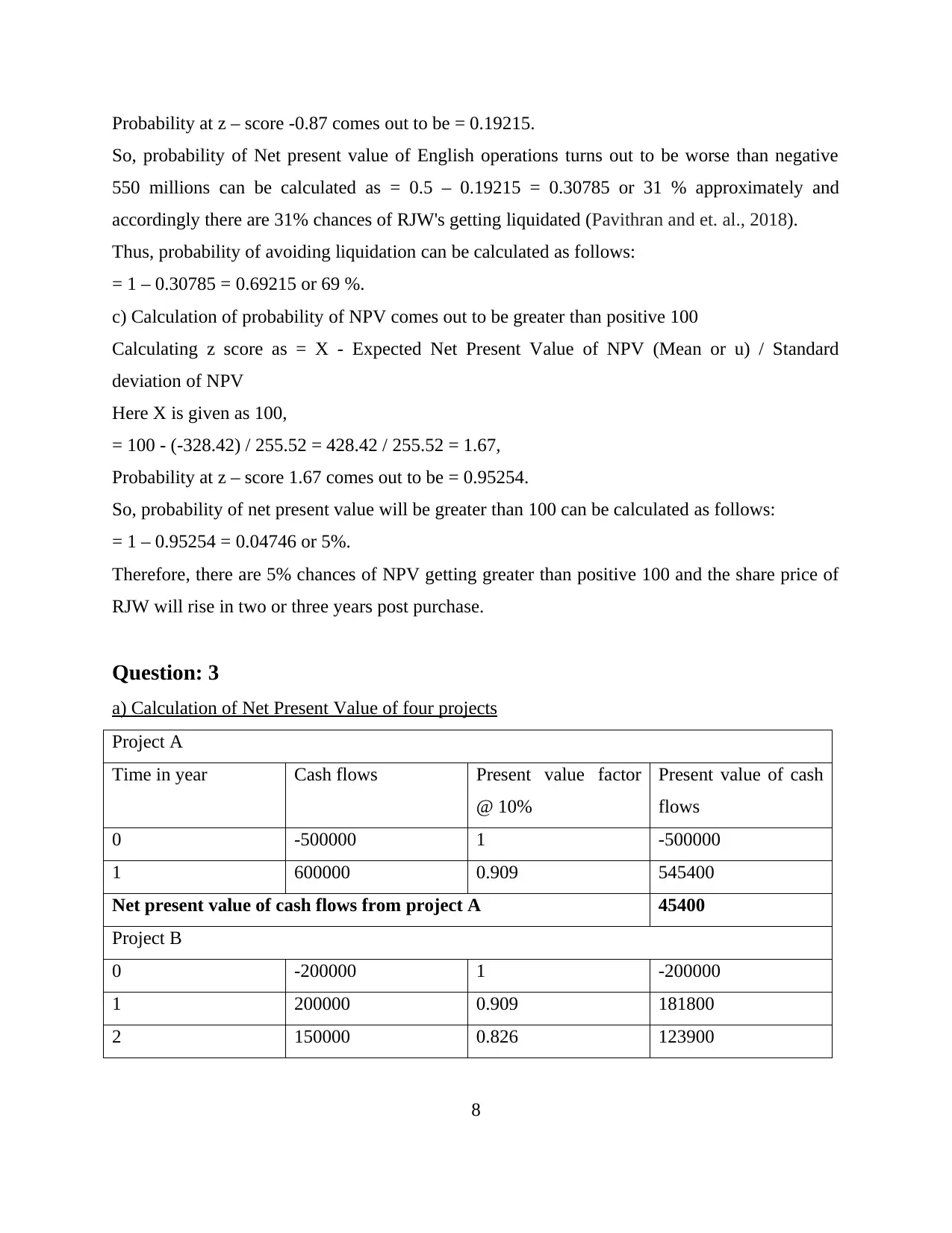

Probability at z – score -0.87 comes out to be = 0.19215.

So, probability of Net present value of English operations turns out to be worse than negative

550 millions can be calculated as = 0.5 – 0.19215 = 0.30785 or 31 % approximately and

accordingly there are 31% chances of RJW's getting liquidated (Pavithran and et. al., 2018).

Thus, probability of avoiding liquidation can be calculated as follows:

= 1 – 0.30785 = 0.69215 or 69 %.

c) Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, there are 5% chances of NPV getting greater than positive 100 and the share price of

RJW will rise in two or three years post purchase.

Question: 3

a) Calculation of Net Present Value of four projects

Project A

Time in year Cash flows Present value factor

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

8

So, probability of Net present value of English operations turns out to be worse than negative

550 millions can be calculated as = 0.5 – 0.19215 = 0.30785 or 31 % approximately and

accordingly there are 31% chances of RJW's getting liquidated (Pavithran and et. al., 2018).

Thus, probability of avoiding liquidation can be calculated as follows:

= 1 – 0.30785 = 0.69215 or 69 %.

c) Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, there are 5% chances of NPV getting greater than positive 100 and the share price of

RJW will rise in two or three years post purchase.

Question: 3

a) Calculation of Net Present Value of four projects

Project A

Time in year Cash flows Present value factor

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

8

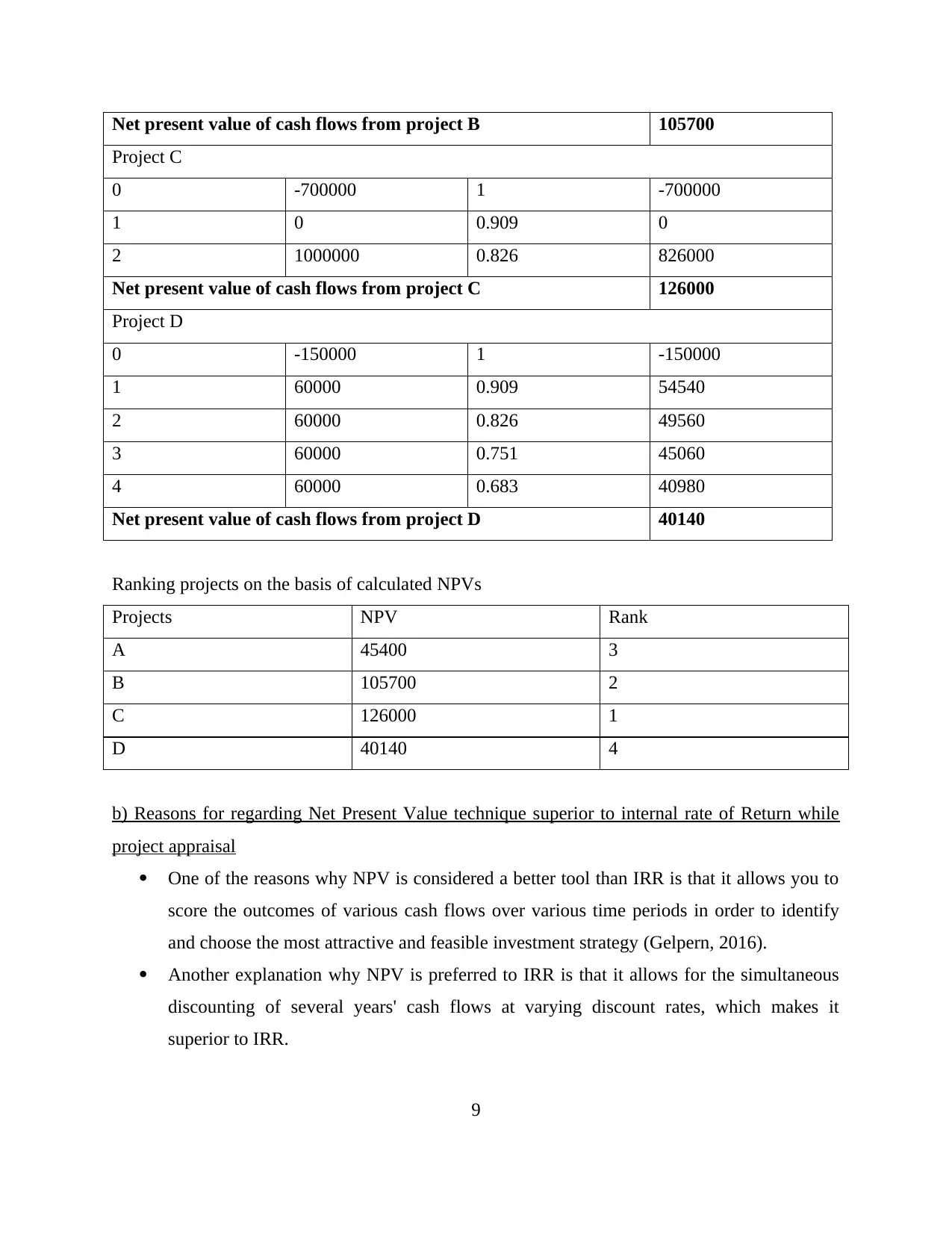

Net present value of cash flows from project B 105700

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

b) Reasons for regarding Net Present Value technique superior to internal rate of Return while

project appraisal

One of the reasons why NPV is considered a better tool than IRR is that it allows you to

score the outcomes of various cash flows over various time periods in order to identify

and choose the most attractive and feasible investment strategy (Gelpern, 2016).

Another explanation why NPV is preferred to IRR is that it allows for the simultaneous

discounting of several years' cash flows at varying discount rates, which makes it

superior to IRR.

9

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

b) Reasons for regarding Net Present Value technique superior to internal rate of Return while

project appraisal

One of the reasons why NPV is considered a better tool than IRR is that it allows you to

score the outcomes of various cash flows over various time periods in order to identify

and choose the most attractive and feasible investment strategy (Gelpern, 2016).

Another explanation why NPV is preferred to IRR is that it allows for the simultaneous

discounting of several years' cash flows at varying discount rates, which makes it

superior to IRR.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

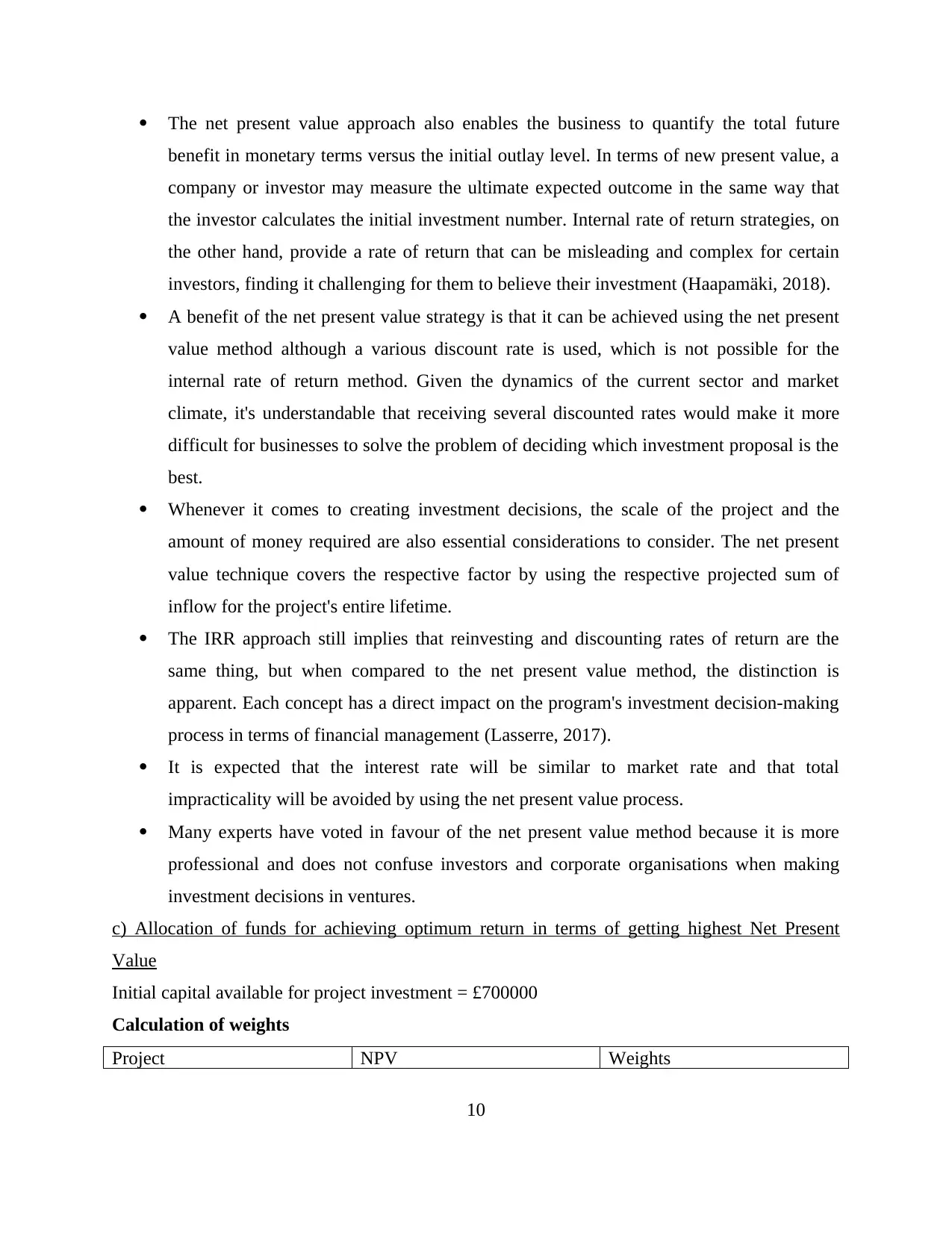

The net present value approach also enables the business to quantify the total future

benefit in monetary terms versus the initial outlay level. In terms of new present value, a

company or investor may measure the ultimate expected outcome in the same way that

the investor calculates the initial investment number. Internal rate of return strategies, on

the other hand, provide a rate of return that can be misleading and complex for certain

investors, finding it challenging for them to believe their investment (Haapamäki, 2018).

A benefit of the net present value strategy is that it can be achieved using the net present

value method although a various discount rate is used, which is not possible for the

internal rate of return method. Given the dynamics of the current sector and market

climate, it's understandable that receiving several discounted rates would make it more

difficult for businesses to solve the problem of deciding which investment proposal is the

best.

Whenever it comes to creating investment decisions, the scale of the project and the

amount of money required are also essential considerations to consider. The net present

value technique covers the respective factor by using the respective projected sum of

inflow for the project's entire lifetime.

The IRR approach still implies that reinvesting and discounting rates of return are the

same thing, but when compared to the net present value method, the distinction is

apparent. Each concept has a direct impact on the program's investment decision-making

process in terms of financial management (Lasserre, 2017).

It is expected that the interest rate will be similar to market rate and that total

impracticality will be avoided by using the net present value process.

Many experts have voted in favour of the net present value method because it is more

professional and does not confuse investors and corporate organisations when making

investment decisions in ventures.

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital available for project investment = £700000

Calculation of weights

Project NPV Weights

10

benefit in monetary terms versus the initial outlay level. In terms of new present value, a

company or investor may measure the ultimate expected outcome in the same way that

the investor calculates the initial investment number. Internal rate of return strategies, on

the other hand, provide a rate of return that can be misleading and complex for certain

investors, finding it challenging for them to believe their investment (Haapamäki, 2018).

A benefit of the net present value strategy is that it can be achieved using the net present

value method although a various discount rate is used, which is not possible for the

internal rate of return method. Given the dynamics of the current sector and market

climate, it's understandable that receiving several discounted rates would make it more

difficult for businesses to solve the problem of deciding which investment proposal is the

best.

Whenever it comes to creating investment decisions, the scale of the project and the

amount of money required are also essential considerations to consider. The net present

value technique covers the respective factor by using the respective projected sum of

inflow for the project's entire lifetime.

The IRR approach still implies that reinvesting and discounting rates of return are the

same thing, but when compared to the net present value method, the distinction is

apparent. Each concept has a direct impact on the program's investment decision-making

process in terms of financial management (Lasserre, 2017).

It is expected that the interest rate will be similar to market rate and that total

impracticality will be avoided by using the net present value process.

Many experts have voted in favour of the net present value method because it is more

professional and does not confuse investors and corporate organisations when making

investment decisions in ventures.

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital available for project investment = £700000

Calculation of weights

Project NPV Weights

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

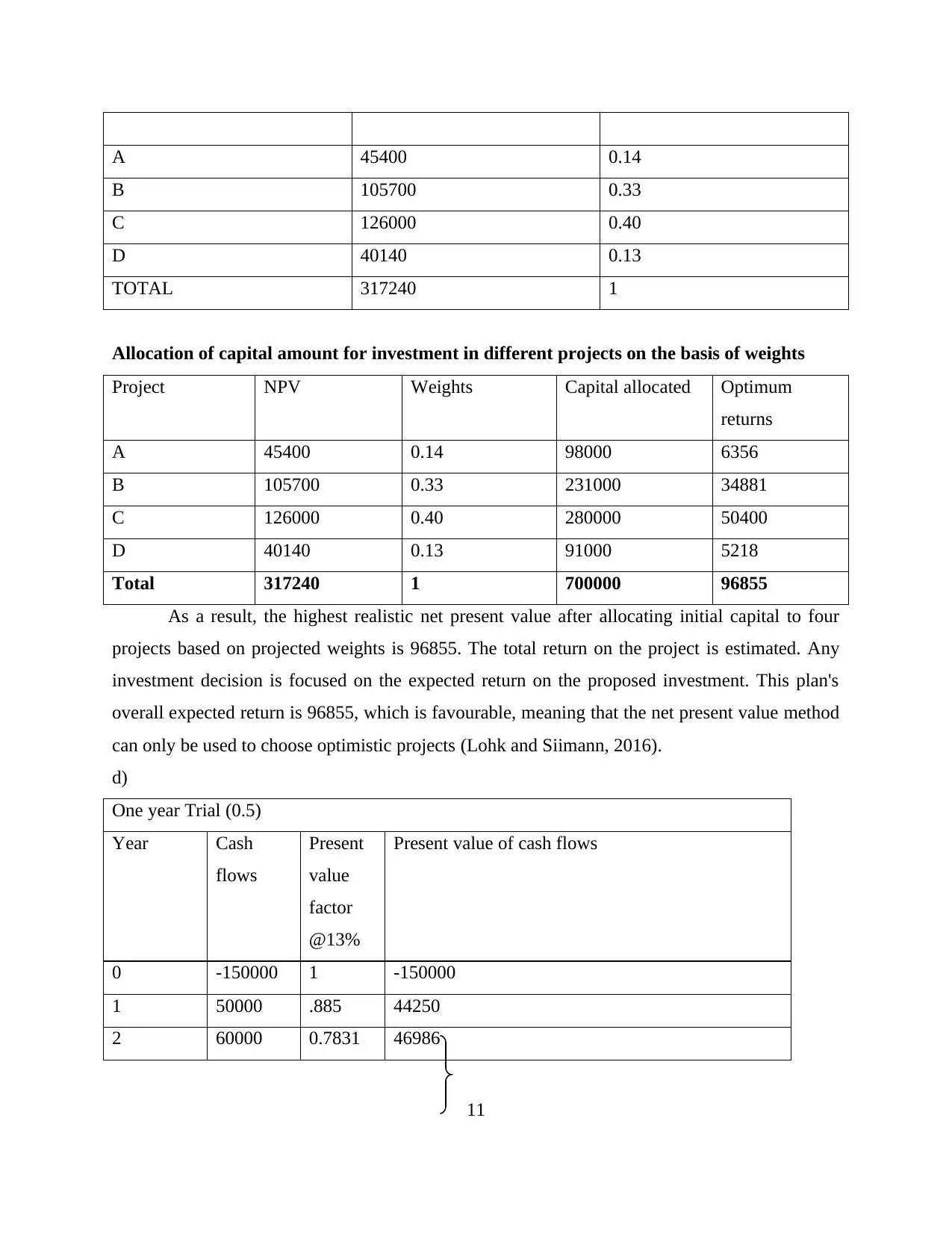

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

As a result, the highest realistic net present value after allocating initial capital to four

projects based on projected weights is 96855. The total return on the project is estimated. Any

investment decision is focused on the expected return on the proposed investment. This plan's

overall expected return is 96855, which is favourable, meaning that the net present value method

can only be used to choose optimistic projects (Lohk and Siimann, 2016).

d)

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

11

B 105700 0.33

C 126000 0.40

D 40140 0.13

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

As a result, the highest realistic net present value after allocating initial capital to four

projects based on projected weights is 96855. The total return on the project is estimated. Any

investment decision is focused on the expected return on the proposed investment. This plan's

overall expected return is 96855, which is favourable, meaning that the net present value method

can only be used to choose optimistic projects (Lohk and Siimann, 2016).

d)

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

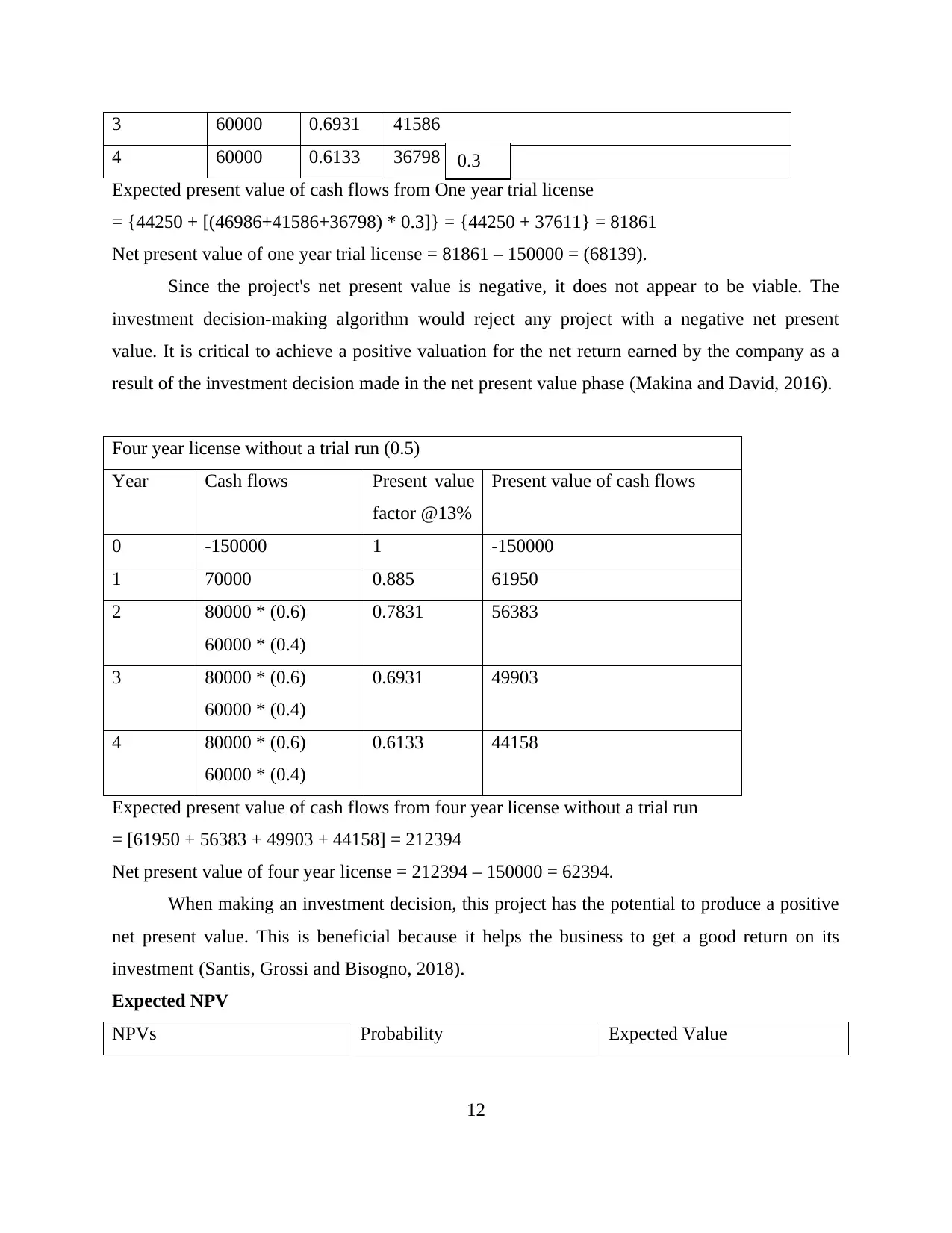

11

3 60000 0.6931 41586

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Net present value of one year trial license = 81861 – 150000 = (68139).

Since the project's net present value is negative, it does not appear to be viable. The

investment decision-making algorithm would reject any project with a negative net present

value. It is critical to achieve a positive valuation for the net return earned by the company as a

result of the investment decision made in the net present value phase (Makina and David, 2016).

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

Expected present value of cash flows from four year license without a trial run

= [61950 + 56383 + 49903 + 44158] = 212394

Net present value of four year license = 212394 – 150000 = 62394.

When making an investment decision, this project has the potential to produce a positive

net present value. This is beneficial because it helps the business to get a good return on its

investment (Santis, Grossi and Bisogno, 2018).

Expected NPV

NPVs Probability Expected Value

12

0.3

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Net present value of one year trial license = 81861 – 150000 = (68139).

Since the project's net present value is negative, it does not appear to be viable. The

investment decision-making algorithm would reject any project with a negative net present

value. It is critical to achieve a positive valuation for the net return earned by the company as a

result of the investment decision made in the net present value phase (Makina and David, 2016).

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

Expected present value of cash flows from four year license without a trial run

= [61950 + 56383 + 49903 + 44158] = 212394

Net present value of four year license = 212394 – 150000 = 62394.

When making an investment decision, this project has the potential to produce a positive

net present value. This is beneficial because it helps the business to get a good return on its

investment (Santis, Grossi and Bisogno, 2018).

Expected NPV

NPVs Probability Expected Value

12

0.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

![International Finance Management Assignment - Finance [Course Code]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Ffd%2F69271dad5c5f4f2c8ab93e7e6daf77ee.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.