International Financial Management (IFM) Assessment 2 Analysis

VerifiedAdded on 2022/12/15

|16

|3646

|434

Report

AI Summary

This report addresses key aspects of international financial management, focusing on investment decision-making processes. It begins by calculating the expected Net Present Value (NPV) and standard deviation of NPV for a project, evaluating potential returns and risks. The report then calculates and interprets NPV under optimistic, pessimistic, and base-case scenarios, incorporating probability analysis to assess the likelihood of different financial outcomes, including the risk of liquidation. Furthermore, the report delves into project appraisal, calculating the NPV for four distinct projects and ranking them based on their NPV. The report then provides a comparative analysis between the Net Present Value (NPV) and Internal Rate of Return (IRR) methods, highlighting the superiority of NPV in investment decision-making. The report concludes by providing a comparative analysis between the Net Present Value (NPV) and Internal Rate of Return (IRR) methods, highlighting the superiority of NPV in investment decision-making, and the allocation of funds for achieving optimum return.

INTERNATIONAL

FINANCIAL

MANAGEMENT(ASSESSM

ENT2)

FINANCIAL

MANAGEMENT(ASSESSM

ENT2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Question: 1.................................................................................................................................3

a) Expected NPV.................................................................................................................3

b) The standard deviation of NPV.........................................................................................4

Question: 2.................................................................................................................................6

Question: 3.................................................................................................................................8

a) Calculation of Net Present Value of four projects.............................................................8

b) Reasons regarding Net Present Value technique superior to internal rate of Return while

project appraisal...................................................................................................................10

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value....................................................................................................................................11

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

Question: 1.................................................................................................................................3

a) Expected NPV.................................................................................................................3

b) The standard deviation of NPV.........................................................................................4

Question: 2.................................................................................................................................6

Question: 3.................................................................................................................................8

a) Calculation of Net Present Value of four projects.............................................................8

b) Reasons regarding Net Present Value technique superior to internal rate of Return while

project appraisal...................................................................................................................10

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value....................................................................................................................................11

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION

International financial management refers to the management of finance of the

business which is operating at an international level. The aim of this branch of financial

management is to maximise shareholder’s wealth by making a wise decision and choice

among the available alternatives for investment. So, that the shareholder’s wealth can be

financially better off than what it was before such decision and its implementation.Investment

decision making for businesses operating at an international level is defined as taking the best

level of decision on the basis of needs and requirements associated with the business entity

operating in different countries. It further involves looking at the business objectives and

takes the most suitable decision that can strengthen the financial efficiency of the business

entity. This report will give emphasis over the investment decision making of the business

entity (Verschuur, 2019). In regards to the growth of the business house investment decision

making technique provide a clear understanding what are the areas organisation should focus

on while taking the investment like decision. Henceforth this project will discuss about the

investment decision making of the organisation. Different Methods like net present value,

investment rate of return will be a part of the decision making process when it comes to

assessing the best suitable decision in regards to the business venture. Net present value

technique would assess the most feasible investment decision making in regards to the

business entity. Key differentiation in between the net present value technique and internal

rate of return technique will also elaborate in this project so that proper understanding about

both the techniques could have been developed as a part of this project.

MAIN BODY

Question: 1

a) Expected NPV

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

International financial management refers to the management of finance of the

business which is operating at an international level. The aim of this branch of financial

management is to maximise shareholder’s wealth by making a wise decision and choice

among the available alternatives for investment. So, that the shareholder’s wealth can be

financially better off than what it was before such decision and its implementation.Investment

decision making for businesses operating at an international level is defined as taking the best

level of decision on the basis of needs and requirements associated with the business entity

operating in different countries. It further involves looking at the business objectives and

takes the most suitable decision that can strengthen the financial efficiency of the business

entity. This report will give emphasis over the investment decision making of the business

entity (Verschuur, 2019). In regards to the growth of the business house investment decision

making technique provide a clear understanding what are the areas organisation should focus

on while taking the investment like decision. Henceforth this project will discuss about the

investment decision making of the organisation. Different Methods like net present value,

investment rate of return will be a part of the decision making process when it comes to

assessing the best suitable decision in regards to the business venture. Net present value

technique would assess the most feasible investment decision making in regards to the

business entity. Key differentiation in between the net present value technique and internal

rate of return technique will also elaborate in this project so that proper understanding about

both the techniques could have been developed as a part of this project.

MAIN BODY

Question: 1

a) Expected NPV

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

Present Value of cash flows in year 2 = 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Present value of cash inflows = 14891

a) Net present value of the project = Present value of future cash inflows – initial cost of

investment = (109).

Therefore, a negative net present value of the project indicates that the adoption of this

project will result in net loss to the company. So, established rules of net present value

technique suggests that the company must avoid or reject such project proposals with

negative net present value or NPV(Luceyand et. al., 2018). The companies must not go for

such projects due to it inability to generate profits for the company in today’s date. The

reason for such negative net present value can be regarded as the considerable reduction in

expected value of the company’s return obtained through the project in year 2 as compared to

year1.

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

Present Value of cash flows in year 2 = 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Present value of cash inflows = 14891

a) Net present value of the project = Present value of future cash inflows – initial cost of

investment = (109).

Therefore, a negative net present value of the project indicates that the adoption of this

project will result in net loss to the company. So, established rules of net present value

technique suggests that the company must avoid or reject such project proposals with

negative net present value or NPV(Luceyand et. al., 2018). The companies must not go for

such projects due to it inability to generate profits for the company in today’s date. The

reason for such negative net present value can be regarded as the considerable reduction in

expected value of the company’s return obtained through the project in year 2 as compared to

year1.

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

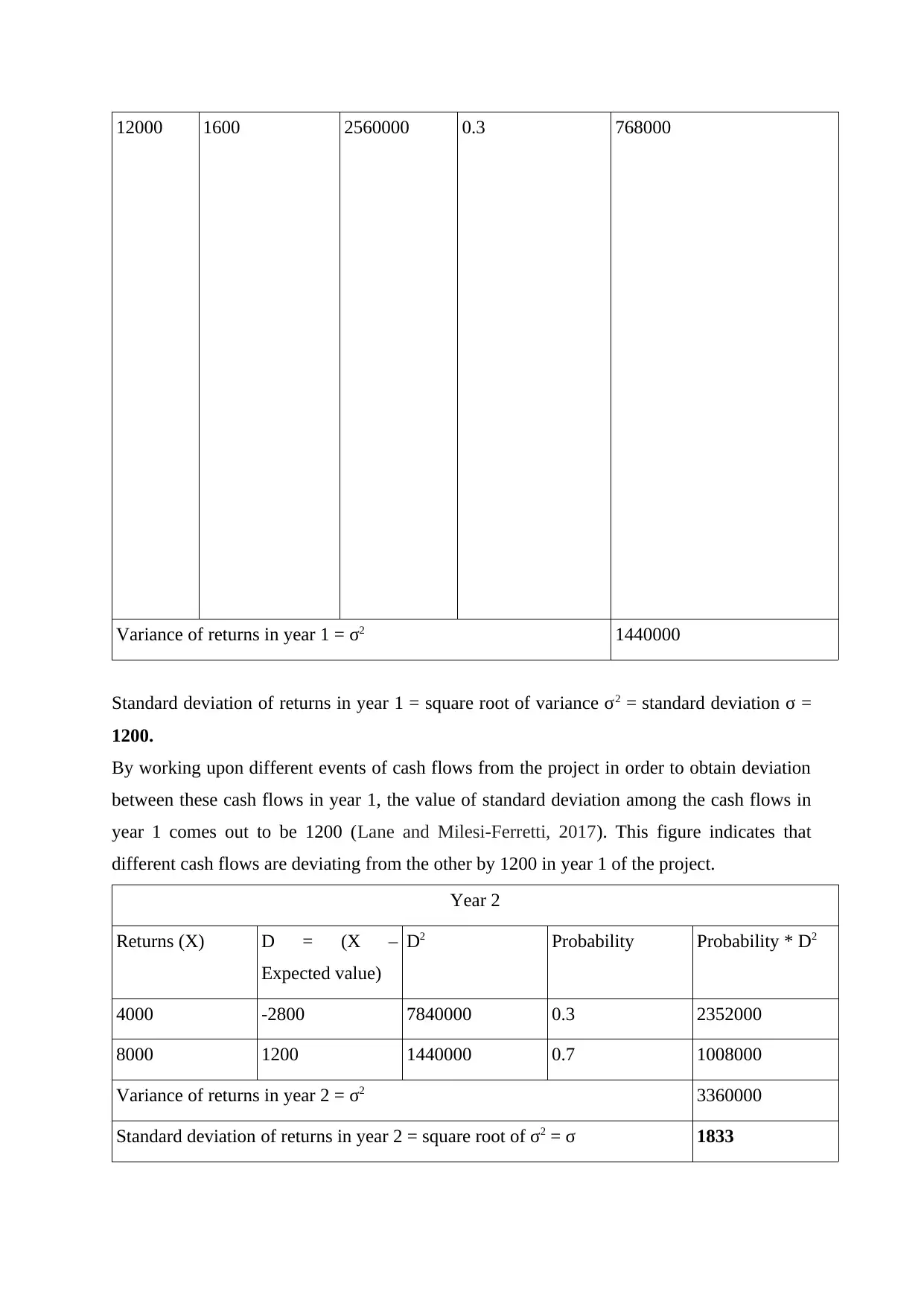

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of variance σ2 = standard deviation σ =

1200.

By working upon different events of cash flows from the project in order to obtain deviation

between these cash flows in year 1, the value of standard deviation among the cash flows in

year 1 comes out to be 1200 (Lane and Milesi-Ferretti, 2017). This figure indicates that

different cash flows are deviating from the other by 1200 in year 1 of the project.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of variance σ2 = standard deviation σ =

1200.

By working upon different events of cash flows from the project in order to obtain deviation

between these cash flows in year 1, the value of standard deviation among the cash flows in

year 1 comes out to be 1200 (Lane and Milesi-Ferretti, 2017). This figure indicates that

different cash flows are deviating from the other by 1200 in year 1 of the project.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

Standard deviation of cash flows year 2 from the project comes out as 1833 which shows that

different scenarios of cash flows expected to be obtained from the project in year 2 are

deviating from each other by 1833.

Question: 2

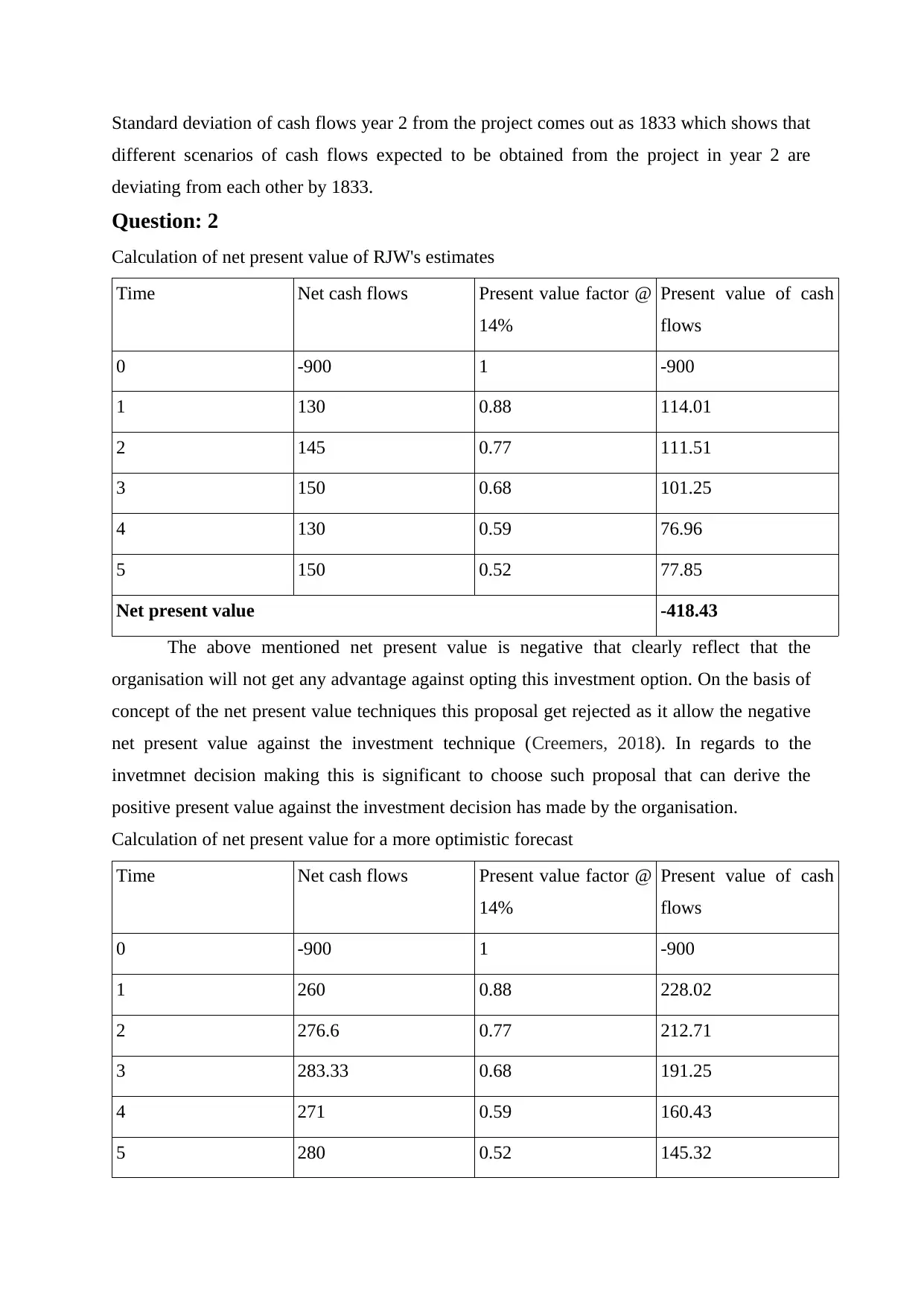

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

The above mentioned net present value is negative that clearly reflect that the

organisation will not get any advantage against opting this investment option. On the basis of

concept of the net present value techniques this proposal get rejected as it allow the negative

net present value against the investment technique (Creemers, 2018). In regards to the

invetmnet decision making this is significant to choose such proposal that can derive the

positive present value against the investment decision has made by the organisation.

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

different scenarios of cash flows expected to be obtained from the project in year 2 are

deviating from each other by 1833.

Question: 2

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

The above mentioned net present value is negative that clearly reflect that the

organisation will not get any advantage against opting this investment option. On the basis of

concept of the net present value techniques this proposal get rejected as it allow the negative

net present value against the investment technique (Creemers, 2018). In regards to the

invetmnet decision making this is significant to choose such proposal that can derive the

positive present value against the investment decision has made by the organisation.

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

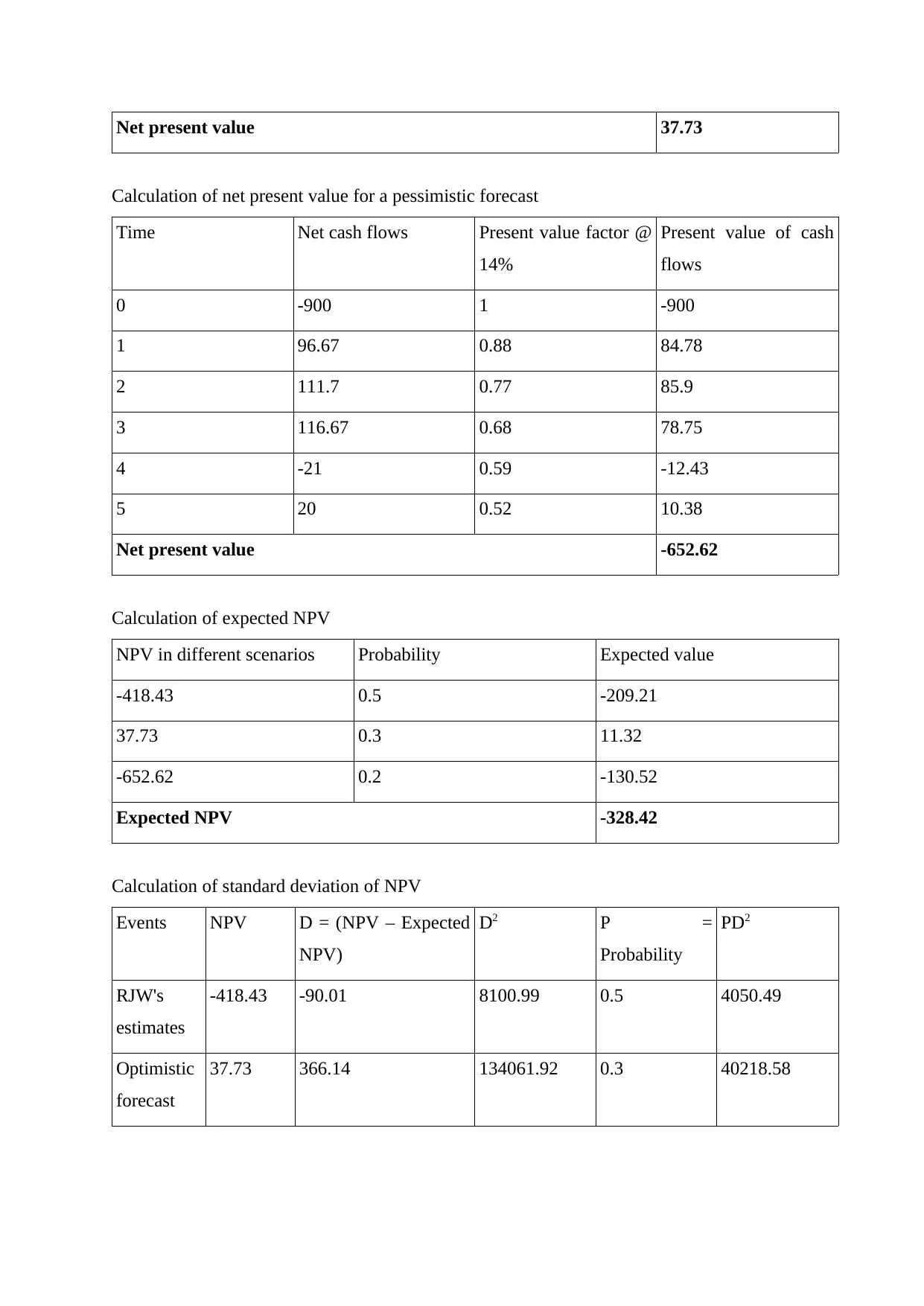

Net present value 37.73

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

Calculation of expected NPV

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

Calculation of expected NPV

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected

NPV)

D2 P =

Probability

PD2

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pessimistic

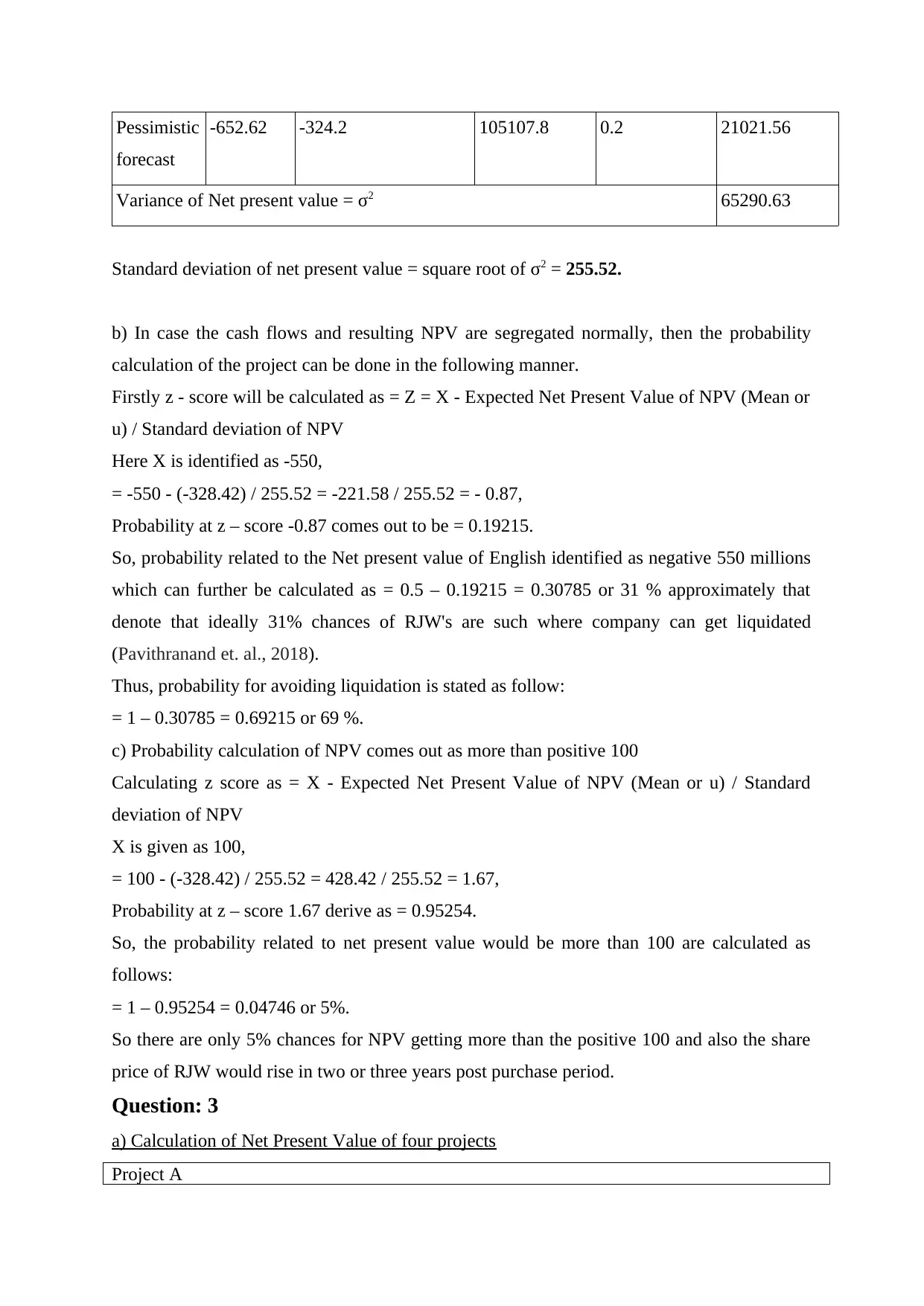

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) In case the cash flows and resulting NPV are segregated normally, then the probability

calculation of the project can be done in the following manner.

Firstly z - score will be calculated as = Z = X - Expected Net Present Value of NPV (Mean or

u) / Standard deviation of NPV

Here X is identified as -550,

= -550 - (-328.42) / 255.52 = -221.58 / 255.52 = - 0.87,

Probability at z – score -0.87 comes out to be = 0.19215.

So, probability related to the Net present value of English identified as negative 550 millions

which can further be calculated as = 0.5 – 0.19215 = 0.30785 or 31 % approximately that

denote that ideally 31% chances of RJW's are such where company can get liquidated

(Pavithranand et. al., 2018).

Thus, probability for avoiding liquidation is stated as follow:

= 1 – 0.30785 = 0.69215 or 69 %.

c) Probability calculation of NPV comes out as more than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 derive as = 0.95254.

So, the probability related to net present value would be more than 100 are calculated as

follows:

= 1 – 0.95254 = 0.04746 or 5%.

So there are only 5% chances for NPV getting more than the positive 100 and also the share

price of RJW would rise in two or three years post purchase period.

Question: 3

a) Calculation of Net Present Value of four projects

Project A

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) In case the cash flows and resulting NPV are segregated normally, then the probability

calculation of the project can be done in the following manner.

Firstly z - score will be calculated as = Z = X - Expected Net Present Value of NPV (Mean or

u) / Standard deviation of NPV

Here X is identified as -550,

= -550 - (-328.42) / 255.52 = -221.58 / 255.52 = - 0.87,

Probability at z – score -0.87 comes out to be = 0.19215.

So, probability related to the Net present value of English identified as negative 550 millions

which can further be calculated as = 0.5 – 0.19215 = 0.30785 or 31 % approximately that

denote that ideally 31% chances of RJW's are such where company can get liquidated

(Pavithranand et. al., 2018).

Thus, probability for avoiding liquidation is stated as follow:

= 1 – 0.30785 = 0.69215 or 69 %.

c) Probability calculation of NPV comes out as more than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 derive as = 0.95254.

So, the probability related to net present value would be more than 100 are calculated as

follows:

= 1 – 0.95254 = 0.04746 or 5%.

So there are only 5% chances for NPV getting more than the positive 100 and also the share

price of RJW would rise in two or three years post purchase period.

Question: 3

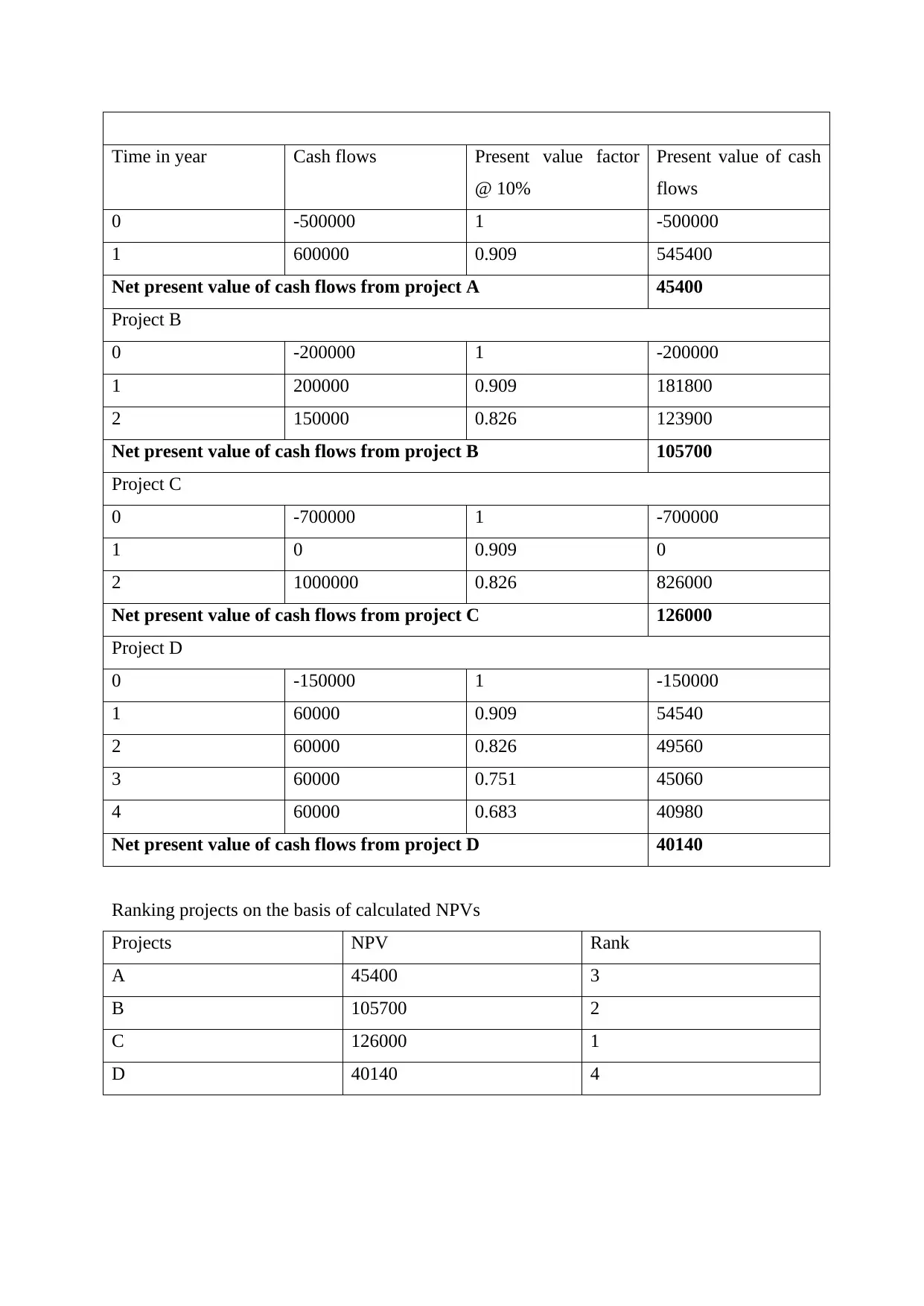

a) Calculation of Net Present Value of four projects

Project A

Time in year Cash flows Present value factor

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

Net present value of cash flows from project B 105700

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

Net present value of cash flows from project B 105700

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Reasons regarding Net Present Value technique superior to internal rate of Return while

project appraisal

Net present value is a technique which allows the business entity to select the

optimum project based on company’s need and requirements that can provide the best

return possible out of multiple choices and project option available.

The key reason behind the NPV is considered as more superior method than IRR is

that it provides the scope to the business entity to give necessary ranking on the basis

of the selection criteria stated under the net present value technique from most

preferred to least prefer proposal (Amrollahi and Bathaee, 2017). Whereas, under the

IRR method there is only rate evaluated of every project against the investment made.

Net present value method allows business entity to discount various years’

cashinflowsat a discounted rate on a yearly based segregation that further is not

available under the IRR technique.

The basic concept of the net present value method is that i allow the business entity to

identify the total expected benefits company will generate in the total spam of life of

every single project (Amin, Zhang and Akhtar, 2017). This method liquidate every

single proposal in such manner that business entity get to know how much the

financial outcomes company will entertain in order to choose or select a certain or

specific project.. Suchproposal gets selected that derive the most positive net outcome

from the project selection. Whereas, under the IRR technique this segregation is not

available over the net inflow basis.

In case of net present value method even if the multiple discount rates is given this

will not confuse management as all could have been handled with support of NET

present value calculation and this is not possible in context to the internal rate of

return technique.

Investment decision making is ery complex in nature that require clear understanding

of the expected benefits business entity can derive out of the selection of specific

proposal which is available only in case of the net present value method whereas in

regards to the IRR technique the calculation is complicated and do not indicate clearly

about which proposal business should select as a part of the investment decision

making.

Practice situation is always differ from the booking knowledge as this is not feasible

that all the options available in front of the organisation will offer the similar life

tenure or duration of every proposal available in front of the business entity and in

project appraisal

Net present value is a technique which allows the business entity to select the

optimum project based on company’s need and requirements that can provide the best

return possible out of multiple choices and project option available.

The key reason behind the NPV is considered as more superior method than IRR is

that it provides the scope to the business entity to give necessary ranking on the basis

of the selection criteria stated under the net present value technique from most

preferred to least prefer proposal (Amrollahi and Bathaee, 2017). Whereas, under the

IRR method there is only rate evaluated of every project against the investment made.

Net present value method allows business entity to discount various years’

cashinflowsat a discounted rate on a yearly based segregation that further is not

available under the IRR technique.

The basic concept of the net present value method is that i allow the business entity to

identify the total expected benefits company will generate in the total spam of life of

every single project (Amin, Zhang and Akhtar, 2017). This method liquidate every

single proposal in such manner that business entity get to know how much the

financial outcomes company will entertain in order to choose or select a certain or

specific project.. Suchproposal gets selected that derive the most positive net outcome

from the project selection. Whereas, under the IRR technique this segregation is not

available over the net inflow basis.

In case of net present value method even if the multiple discount rates is given this

will not confuse management as all could have been handled with support of NET

present value calculation and this is not possible in context to the internal rate of

return technique.

Investment decision making is ery complex in nature that require clear understanding

of the expected benefits business entity can derive out of the selection of specific

proposal which is available only in case of the net present value method whereas in

regards to the IRR technique the calculation is complicated and do not indicate clearly

about which proposal business should select as a part of the investment decision

making.

Practice situation is always differ from the booking knowledge as this is not feasible

that all the options available in front of the organisation will offer the similar life

tenure or duration of every proposal available in front of the business entity and in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

such a situation Net present value method look more feasible to make the investment

decision as compare to the IRR technique (Knoke, Gosling and Paul, 2020).

The preference of majority of investor banker is towards the net present value

technique is appreciated due to the end result of the technique. Net present value

method derive the total expected benefit out of the project selected in the life time of

the project whereas, in context to the IRR method breakeven point in relation to every

proposal is derived as a end result that do not allow the clear understanding in regards

to the profitability of every single proposal available (Egwunatum and Akpokodje,

2019).

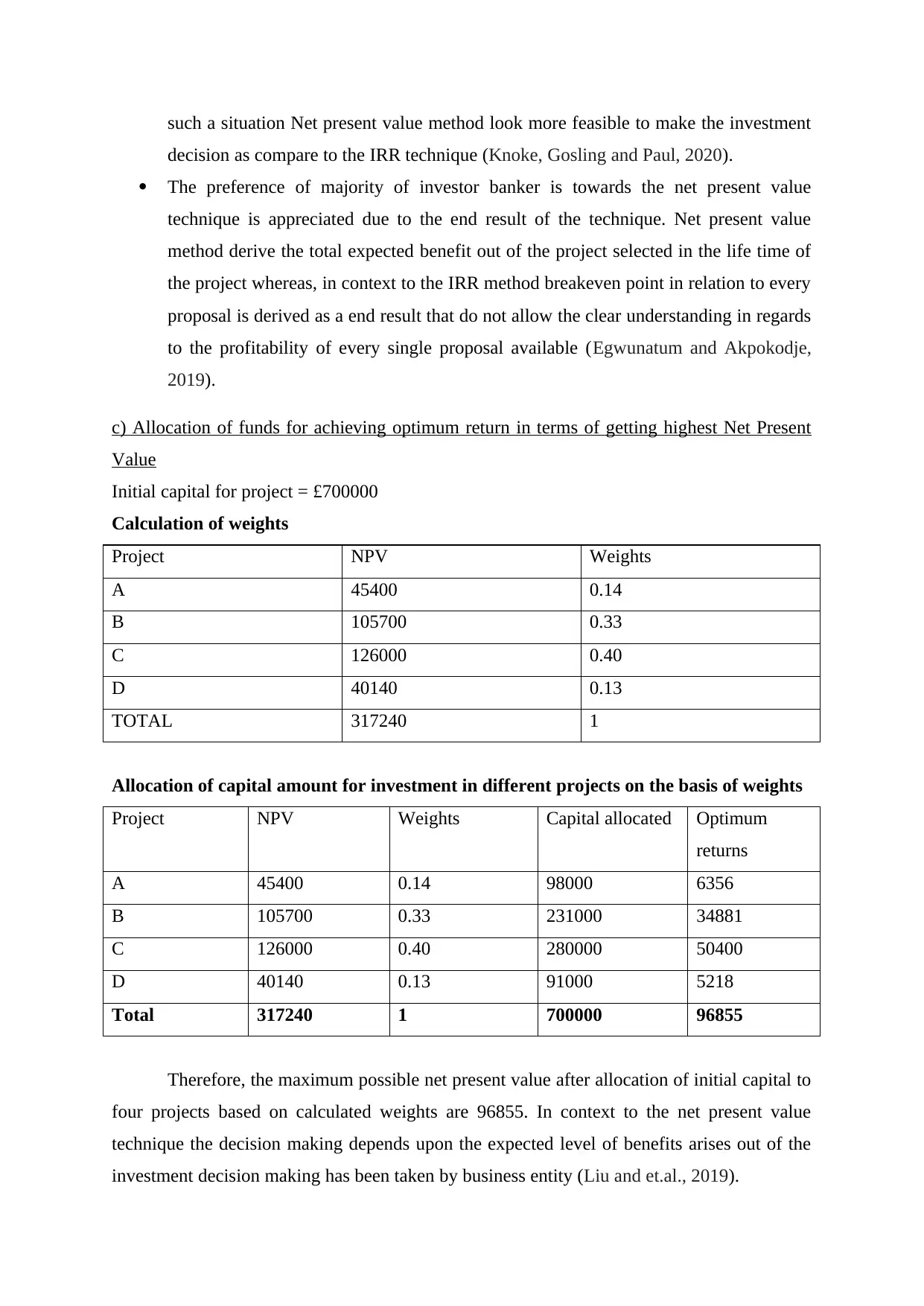

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital for project = £700000

Calculation of weights

Project NPV Weights

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

Therefore, the maximum possible net present value after allocation of initial capital to

four projects based on calculated weights are 96855. In context to the net present value

technique the decision making depends upon the expected level of benefits arises out of the

investment decision making has been taken by business entity (Liu and et.al., 2019).

decision as compare to the IRR technique (Knoke, Gosling and Paul, 2020).

The preference of majority of investor banker is towards the net present value

technique is appreciated due to the end result of the technique. Net present value

method derive the total expected benefit out of the project selected in the life time of

the project whereas, in context to the IRR method breakeven point in relation to every

proposal is derived as a end result that do not allow the clear understanding in regards

to the profitability of every single proposal available (Egwunatum and Akpokodje,

2019).

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital for project = £700000

Calculation of weights

Project NPV Weights

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

Therefore, the maximum possible net present value after allocation of initial capital to

four projects based on calculated weights are 96855. In context to the net present value

technique the decision making depends upon the expected level of benefits arises out of the

investment decision making has been taken by business entity (Liu and et.al., 2019).

d)

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Net present value of one year trial license = 81861 – 150000 = (68139).

This project contains a negative net present value figre which completely reject this

project to get selected against the investment decision making made. Negative net present

value do not offer the confidence to the business entity for getting the project selected

(Caetano and et.al., 2018). On the ground of negative NPV the project does not meet up the

selection criteria.

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

0.3

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Net present value of one year trial license = 81861 – 150000 = (68139).

This project contains a negative net present value figre which completely reject this

project to get selected against the investment decision making made. Negative net present

value do not offer the confidence to the business entity for getting the project selected

(Caetano and et.al., 2018). On the ground of negative NPV the project does not meet up the

selection criteria.

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

0.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

![International Finance Management Assignment - Finance [Course Code]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Ffd%2F69271dad5c5f4f2c8ab93e7e6daf77ee.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.