University: International Financial Management Homework 2 - FIN3IFM

VerifiedAdded on 2022/11/13

|9

|1473

|157

Homework Assignment

AI Summary

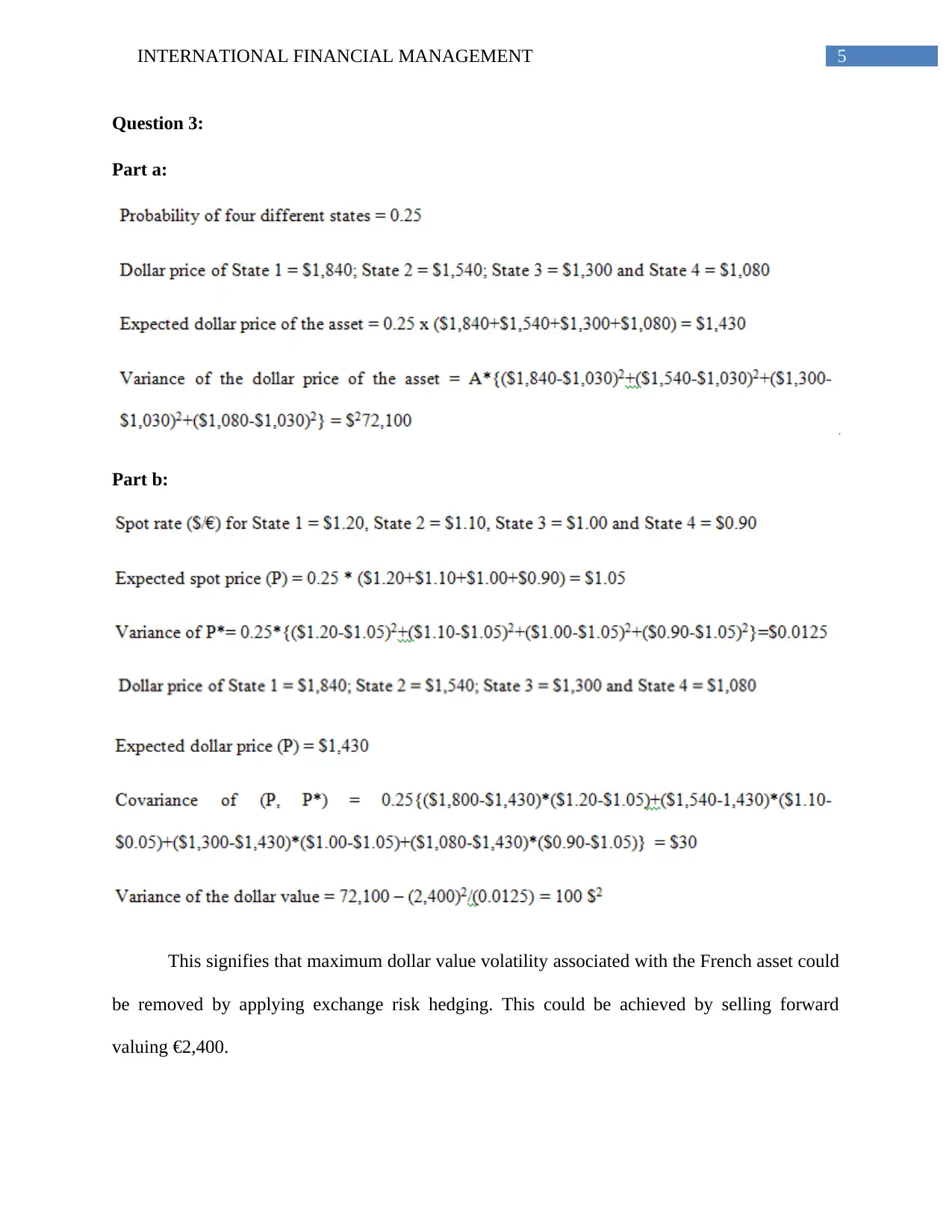

This homework assignment on International Financial Management (FIN3IFM) addresses key concepts in international finance. It begins by defining and differentiating between transaction, economic, and translation exposures, providing examples of each. The assignment then explores the role of hedging in mitigating these exposures, particularly in imperfect capital markets. It delves into the causes and implications of the global financial crisis, focusing on liquidity risks, off-balance sheet market risks, and the actions of financial intermediaries. Furthermore, it examines the role of structured investment vehicles (SIVs) and collateralized debt obligations (CDOs) in the crisis. The assignment provides a comprehensive overview of the core issues in international finance, providing a solid foundation for understanding financial risk and management in a global context.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.