PGBM144: International Financial Markets and Econometrics Report

VerifiedAdded on 2023/01/09

|20

|7009

|74

Report

AI Summary

This report provides a comprehensive analysis of international financial markets, focusing on exchange rate volatility, risks associated with international transactions, and the application of econometrics. The report begins with a critical discussion of the causes of exchange rate volatility, particularly in the context of the Pound/Dollar spot exchange rate, and assesses its impact on international trade. It then explores the nature of risks in international transactions, including commercial, political, and legal risks, and examines how international traders can manage these risks using derivative markets. The report also includes a financial econometrics investigation to assess the informational efficiency of the London Stock Exchange market. Finally, it critically examines the impact of recent interest rate policies and quantitative easing operations on international capital markets and stock prices. The report incorporates relevant financial data, charts, and academic literature to support its findings and conclusions.

Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Critical discussion of the main causes of the exchange rate volatility in the foreign exchange

markets.........................................................................................................................................1

b. Explanation of the nature of potential risks in international transactions and critical

discussion of the way in which international traders might manage the risks in derivative

market..........................................................................................................................................4

QUESTION 2..................................................................................................................................6

Carrying out the financial econometrics investigation to critical examine the level of

informational efficiency of the London Stock Exchange market................................................6

QUESTION 3................................................................................................................................11

Critical examination of the way in which recent interest rate policy and quantitative easing

operations via short term international money markets have impacted international capital

markets and stock prices............................................................................................................11

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Critical discussion of the main causes of the exchange rate volatility in the foreign exchange

markets.........................................................................................................................................1

b. Explanation of the nature of potential risks in international transactions and critical

discussion of the way in which international traders might manage the risks in derivative

market..........................................................................................................................................4

QUESTION 2..................................................................................................................................6

Carrying out the financial econometrics investigation to critical examine the level of

informational efficiency of the London Stock Exchange market................................................6

QUESTION 3................................................................................................................................11

Critical examination of the way in which recent interest rate policy and quantitative easing

operations via short term international money markets have impacted international capital

markets and stock prices............................................................................................................11

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

International financial market could be defined as a place where different buyers and

sellers of financial assets perform trading related activities. Some of the assets that are traded

through this market are stock, currencies, derivatives, bonds and commodities. There are several

types of markets which are used for the purpose of conducting the trading activities. These are

capital, money, derivatives and commodity markets. For smooth operation of capitalist

economies, it is very important to maintain the financial markets in systematic manner. The

international currency market is the largest financial market at global level where the average

trading of five dollar trillion is performed on daily basis. Large banks and brokers from different

countries performed trading related activities in this market. Some of the main function of the

market are fund mobilisation, easy access, risk sharing, capital formation, price determination,

liquidity, reduction of transaction costs etc. International financial markets are beneficial for all

the investors as well as firms because when the cost of the share will be low then it may attract

large number of investors (Ahelegbey, 2016). Apart from this, these markets also offer

opportunities for risk sharing to the investors. Present report is based upon international financial

markets and econometrics. This assignment covers various topics such as exchange rate

volatility, risks in the international transactions, hedging, forward and future contracts,

examination of the level of informational efficiency of the London stock exchange market,

implication of empirical investigation etc. Additionally, critical examination of the way in which

recent interest rate policy and quantitative easing operations via short-term international money

markets have impacted international markets and stock price are also covered in this report.

QUESTION 1

a. Critical discussion of the main causes of the exchange rate volatility in the foreign exchange

markets

Exchange rate volatility could be described as the risk which is associated with

movements in exchange rate which are unexpected. Some of the main economic fundamentals

like interest and inflation rates play major role in it. In other words, it could be defined as the rate

at which currency of one country is converted in to currency of another country. The rapid

changes or fluctuations in the exchange rates are known as their volatility. When the investors

will be planning to invest in a new country or willing to exchange their currency into another one

1

International financial market could be defined as a place where different buyers and

sellers of financial assets perform trading related activities. Some of the assets that are traded

through this market are stock, currencies, derivatives, bonds and commodities. There are several

types of markets which are used for the purpose of conducting the trading activities. These are

capital, money, derivatives and commodity markets. For smooth operation of capitalist

economies, it is very important to maintain the financial markets in systematic manner. The

international currency market is the largest financial market at global level where the average

trading of five dollar trillion is performed on daily basis. Large banks and brokers from different

countries performed trading related activities in this market. Some of the main function of the

market are fund mobilisation, easy access, risk sharing, capital formation, price determination,

liquidity, reduction of transaction costs etc. International financial markets are beneficial for all

the investors as well as firms because when the cost of the share will be low then it may attract

large number of investors (Ahelegbey, 2016). Apart from this, these markets also offer

opportunities for risk sharing to the investors. Present report is based upon international financial

markets and econometrics. This assignment covers various topics such as exchange rate

volatility, risks in the international transactions, hedging, forward and future contracts,

examination of the level of informational efficiency of the London stock exchange market,

implication of empirical investigation etc. Additionally, critical examination of the way in which

recent interest rate policy and quantitative easing operations via short-term international money

markets have impacted international markets and stock price are also covered in this report.

QUESTION 1

a. Critical discussion of the main causes of the exchange rate volatility in the foreign exchange

markets

Exchange rate volatility could be described as the risk which is associated with

movements in exchange rate which are unexpected. Some of the main economic fundamentals

like interest and inflation rates play major role in it. In other words, it could be defined as the rate

at which currency of one country is converted in to currency of another country. The rapid

changes or fluctuations in the exchange rates are known as their volatility. When the investors

will be planning to invest in a new country or willing to exchange their currency into another one

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then it will be very important for them to be aware of volatility in the exchange rate. It can help

them to make appropriate decisions for investment. It may have positive impact on the liquidity

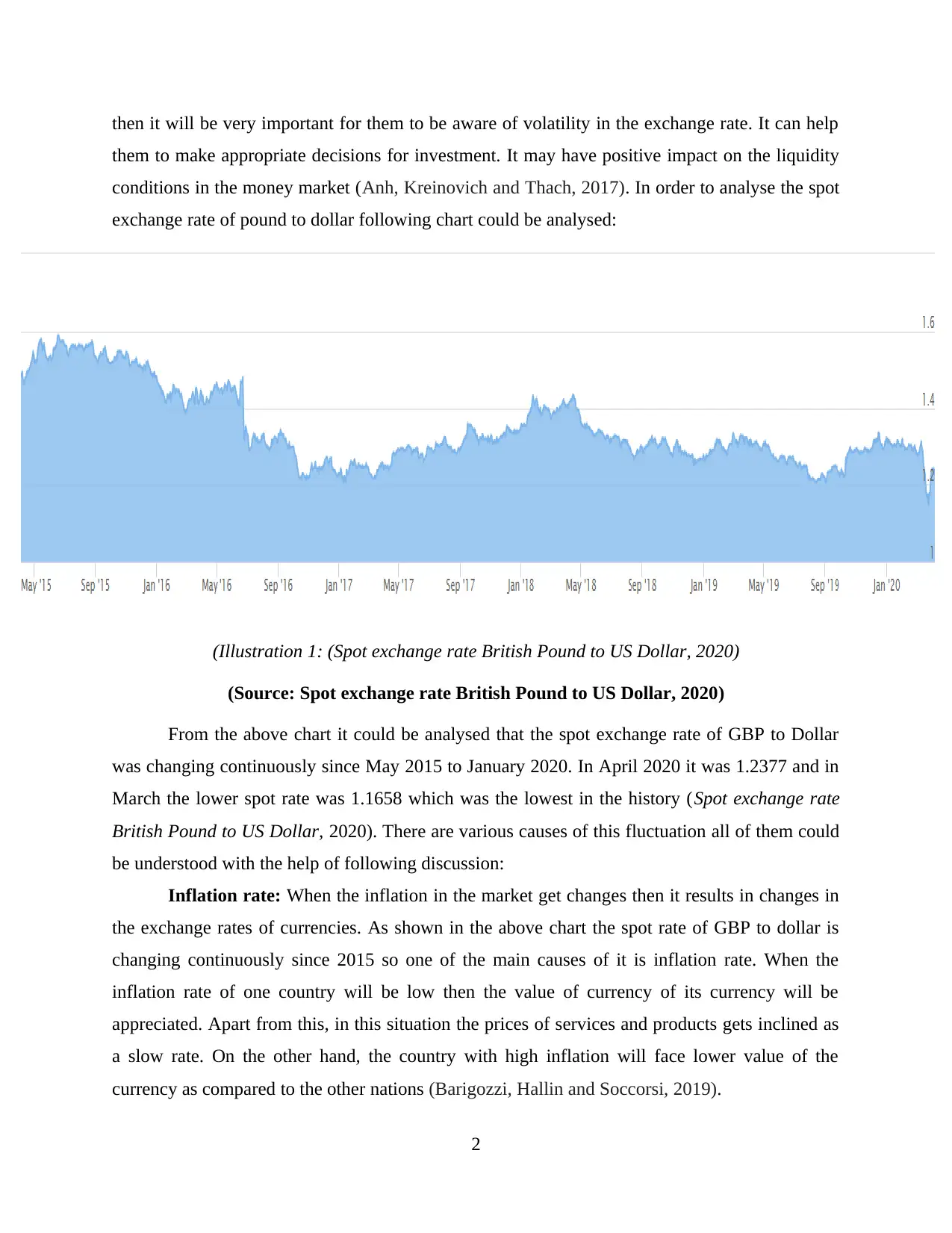

conditions in the money market (Anh, Kreinovich and Thach, 2017). In order to analyse the spot

exchange rate of pound to dollar following chart could be analysed:

(Illustration 1: (Spot exchange rate British Pound to US Dollar, 2020)

(Source: Spot exchange rate British Pound to US Dollar, 2020)

From the above chart it could be analysed that the spot exchange rate of GBP to Dollar

was changing continuously since May 2015 to January 2020. In April 2020 it was 1.2377 and in

March the lower spot rate was 1.1658 which was the lowest in the history (Spot exchange rate

British Pound to US Dollar, 2020). There are various causes of this fluctuation all of them could

be understood with the help of following discussion:

Inflation rate: When the inflation in the market get changes then it results in changes in

the exchange rates of currencies. As shown in the above chart the spot rate of GBP to dollar is

changing continuously since 2015 so one of the main causes of it is inflation rate. When the

inflation rate of one country will be low then the value of currency of its currency will be

appreciated. Apart from this, in this situation the prices of services and products gets inclined as

a slow rate. On the other hand, the country with high inflation will face lower value of the

currency as compared to the other nations (Barigozzi, Hallin and Soccorsi, 2019).

2

them to make appropriate decisions for investment. It may have positive impact on the liquidity

conditions in the money market (Anh, Kreinovich and Thach, 2017). In order to analyse the spot

exchange rate of pound to dollar following chart could be analysed:

(Illustration 1: (Spot exchange rate British Pound to US Dollar, 2020)

(Source: Spot exchange rate British Pound to US Dollar, 2020)

From the above chart it could be analysed that the spot exchange rate of GBP to Dollar

was changing continuously since May 2015 to January 2020. In April 2020 it was 1.2377 and in

March the lower spot rate was 1.1658 which was the lowest in the history (Spot exchange rate

British Pound to US Dollar, 2020). There are various causes of this fluctuation all of them could

be understood with the help of following discussion:

Inflation rate: When the inflation in the market get changes then it results in changes in

the exchange rates of currencies. As shown in the above chart the spot rate of GBP to dollar is

changing continuously since 2015 so one of the main causes of it is inflation rate. When the

inflation rate of one country will be low then the value of currency of its currency will be

appreciated. Apart from this, in this situation the prices of services and products gets inclined as

a slow rate. On the other hand, the country with high inflation will face lower value of the

currency as compared to the other nations (Barigozzi, Hallin and Soccorsi, 2019).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Government debts: It is a type of national or public debt which is owned by the central

government. If a country is having very high government debt then the possibility of acquiring

foreign capital of the same will be low which will lead to inflation. In opposite situation the

foreign investment will be very high and it is the cause of exchange rate volatility of GBP to

dollar because the government debt in UK is very low (Causes of changes in the exchange rate

volatility, 2020).

Interest rates: It is also a cause which has affected the spot exchange rate of pound.

When the interest rate gets changed then it affects the dollar exchange rate as well se the

currency value. There are various rates such as inflation, forex and interest and all of them are

correlated. When the interest rate increases then it enhances the value of currency because it

provides higher rates to the lenders. It also results in attraction of more and more foreign

investors that results in increased exchange rate.

Balance of payment of current account of the nation: Current account of a country is

mainly used for the purpose of reflecting the balance of trade and earnings on the foreign

investment. Due to this, the spot rate of GBP to dollar got changes during the years 2015 to

2020. All the transactions including imports, export and debt are included in it. If there will be

deficit in the current account or balance of payment of the country then it may result in decreased

value of the currency.

Recession: It is one of the major factors which results in exchange rate volatility and it

has also resulted in changes in the spot exchange rate of GBP to dollar. If the country is dealing

with recession then the interest rate will be very low and the change of acquiring the foreign

investment will also get decreased. Therefore, it is the common cause of decreased spot rate of

the currency.

Speculation: When it is expected that the value of currency of a country will rise then the

demand of investors for the same will be increased so that they can make higher profits of it. Due

to this, the value of the currency will also be increased with higher demand and it enhances the

exchange rate which is a cause of changes in spot exchange rate of GBP to dollar as reflected in

the chart (Barnett and Sergi, 2018).

Volatility in exchange rate may result in various impacts upon the trade. When there will

be higher risk with it then it will increase the transaction costs which will reduce the gain from

the international trade activities because the interest of investors will get decreased due to this. It

3

government. If a country is having very high government debt then the possibility of acquiring

foreign capital of the same will be low which will lead to inflation. In opposite situation the

foreign investment will be very high and it is the cause of exchange rate volatility of GBP to

dollar because the government debt in UK is very low (Causes of changes in the exchange rate

volatility, 2020).

Interest rates: It is also a cause which has affected the spot exchange rate of pound.

When the interest rate gets changed then it affects the dollar exchange rate as well se the

currency value. There are various rates such as inflation, forex and interest and all of them are

correlated. When the interest rate increases then it enhances the value of currency because it

provides higher rates to the lenders. It also results in attraction of more and more foreign

investors that results in increased exchange rate.

Balance of payment of current account of the nation: Current account of a country is

mainly used for the purpose of reflecting the balance of trade and earnings on the foreign

investment. Due to this, the spot rate of GBP to dollar got changes during the years 2015 to

2020. All the transactions including imports, export and debt are included in it. If there will be

deficit in the current account or balance of payment of the country then it may result in decreased

value of the currency.

Recession: It is one of the major factors which results in exchange rate volatility and it

has also resulted in changes in the spot exchange rate of GBP to dollar. If the country is dealing

with recession then the interest rate will be very low and the change of acquiring the foreign

investment will also get decreased. Therefore, it is the common cause of decreased spot rate of

the currency.

Speculation: When it is expected that the value of currency of a country will rise then the

demand of investors for the same will be increased so that they can make higher profits of it. Due

to this, the value of the currency will also be increased with higher demand and it enhances the

exchange rate which is a cause of changes in spot exchange rate of GBP to dollar as reflected in

the chart (Barnett and Sergi, 2018).

Volatility in exchange rate may result in various impacts upon the trade. When there will

be higher risk with it then it will increase the transaction costs which will reduce the gain from

the international trade activities because the interest of investors will get decreased due to this. It

3

also leaves impact upon the growth of the country. When the volatility will be low then the

possibility of international trade gains will be low as the exchange rate in this situation will be

very low. On the other hand, if the volatility will be high then it will increase the gain from the

international trade which attracts more and more foreign capital.

b. Explanation of the nature of potential risks in international transactions and critical discussion

of the way in which international traders might manage the risks in derivative market

International transactions could be defined as the purchase or sales of different types of

securities, financial assets etc. that are traded for the purpose of earning higher returns. There are

various types of risks that may affect the international transaction. All of them are as follows:

Commercial risks: One of the common risks is commercial risk that exist in the domestic

as well as international market but the impact of it is very high in the international market as

compared to the domestic. The changes in the trades that are make in the global market place are

difficult to anticipate and hazardous. Acceptability and suitability of the product international

market is very hard to gauge. Apart from this, the changes in supply and demand of the securities

in the market are also unpredictable which also enhances the possibility of commercial risk

(Nature of risk in the international transactions, 2019).

Political risk: When the political situation of the importing or exporting countries will be

changed then this type of risk may take place. The key factors which may result in such risks are

changes in the ruling party, civil wars, rebellions, capture of cargo by the enemies etc.

Legal risks: These are the main risks which may take place due to foreign laws. If the

rules and regulations regarding foreign trade are changed by the legal authorities of importing or

exporting countries then it may result in huge risk for the trade. The investors will take low

interest in such situations because of the expensive nature of the legal proceedings.

For all the international trades it is very important to manage all the above described risks

via derivative markets. For this purpose, exposures arising between the liabilities and assets

could be analysed which could be overlaid using a derivative. These are mainly used to hedge

the unrewarded risks in the interest rates which provides greater flexibility in the asset allocation.

By using derivatives investors, municipalities and investors can transfer the risks and rewards

that are associated with the financial and commercial outcomes of the other parties (Belke,

Dubova and Osowski, 2018).

4

possibility of international trade gains will be low as the exchange rate in this situation will be

very low. On the other hand, if the volatility will be high then it will increase the gain from the

international trade which attracts more and more foreign capital.

b. Explanation of the nature of potential risks in international transactions and critical discussion

of the way in which international traders might manage the risks in derivative market

International transactions could be defined as the purchase or sales of different types of

securities, financial assets etc. that are traded for the purpose of earning higher returns. There are

various types of risks that may affect the international transaction. All of them are as follows:

Commercial risks: One of the common risks is commercial risk that exist in the domestic

as well as international market but the impact of it is very high in the international market as

compared to the domestic. The changes in the trades that are make in the global market place are

difficult to anticipate and hazardous. Acceptability and suitability of the product international

market is very hard to gauge. Apart from this, the changes in supply and demand of the securities

in the market are also unpredictable which also enhances the possibility of commercial risk

(Nature of risk in the international transactions, 2019).

Political risk: When the political situation of the importing or exporting countries will be

changed then this type of risk may take place. The key factors which may result in such risks are

changes in the ruling party, civil wars, rebellions, capture of cargo by the enemies etc.

Legal risks: These are the main risks which may take place due to foreign laws. If the

rules and regulations regarding foreign trade are changed by the legal authorities of importing or

exporting countries then it may result in huge risk for the trade. The investors will take low

interest in such situations because of the expensive nature of the legal proceedings.

For all the international trades it is very important to manage all the above described risks

via derivative markets. For this purpose, exposures arising between the liabilities and assets

could be analysed which could be overlaid using a derivative. These are mainly used to hedge

the unrewarded risks in the interest rates which provides greater flexibility in the asset allocation.

By using derivatives investors, municipalities and investors can transfer the risks and rewards

that are associated with the financial and commercial outcomes of the other parties (Belke,

Dubova and Osowski, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is very important for the firms to use hedging of net payable and receivables rather than

future or forward contracts. Some of the main benefits of it are as follows:

With the help of hedging of net payable and receivable the investor will be able to expose

the money to the risks of fluctuations in different financial prices that are interest rate,

commodity price, forex rate etc. When future and forward contracts will be used by the

hedger the risk with the exchange rate fluctuations could be determined and eliminate the

risk of loss from the unfavourable movements in the market.

If hedging will be used then it will be very easy for the firm to exercise the options upon

observing the realised future exchanger rate. On the other hand, if future or forward

contracts will be used then the hedger may have to suffer (Chen, 2018).

If a firm will use currency option as opposed to the forward contract for the purpose of

hedging then following advantages and disadvantages could be faced:

Advantages: All the benefits of selecting the currency options are as follows:

All the currency options are very cheap to trade so the investor will have to pay very low

cost for hedging while using currency option.

When the investor will select the currency option for hedging then all of them are

available on or off exchange which will be beneficial in long run.

The potential returns in currency options are very high as compared to the risks

associated with them (Advantages and disadvantages of currency options, 2020).

There are various strategies to speculate on volatility and price movements.

Disadvantages: Some of the drawbacks of selecting the currency options for hedging

purpose are as follows:

The investor hedging through currency option may have to face the issues because

currency options could be illiquid.

When the currency option will be adopted by the seller then the risk will be unlimited for

that party as it provides huge returns to the buyers.

Currency options may quickly become worthless which may affect the actual earnings of

the investor.

5

future or forward contracts. Some of the main benefits of it are as follows:

With the help of hedging of net payable and receivable the investor will be able to expose

the money to the risks of fluctuations in different financial prices that are interest rate,

commodity price, forex rate etc. When future and forward contracts will be used by the

hedger the risk with the exchange rate fluctuations could be determined and eliminate the

risk of loss from the unfavourable movements in the market.

If hedging will be used then it will be very easy for the firm to exercise the options upon

observing the realised future exchanger rate. On the other hand, if future or forward

contracts will be used then the hedger may have to suffer (Chen, 2018).

If a firm will use currency option as opposed to the forward contract for the purpose of

hedging then following advantages and disadvantages could be faced:

Advantages: All the benefits of selecting the currency options are as follows:

All the currency options are very cheap to trade so the investor will have to pay very low

cost for hedging while using currency option.

When the investor will select the currency option for hedging then all of them are

available on or off exchange which will be beneficial in long run.

The potential returns in currency options are very high as compared to the risks

associated with them (Advantages and disadvantages of currency options, 2020).

There are various strategies to speculate on volatility and price movements.

Disadvantages: Some of the drawbacks of selecting the currency options for hedging

purpose are as follows:

The investor hedging through currency option may have to face the issues because

currency options could be illiquid.

When the currency option will be adopted by the seller then the risk will be unlimited for

that party as it provides huge returns to the buyers.

Currency options may quickly become worthless which may affect the actual earnings of

the investor.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

Carrying out the financial econometrics investigation to critical examine the level of

informational efficiency of the London Stock Exchange market

Financial econometrics could be defined as the application of various types of statistical

models in the data of financial market. It I a branch of financial economics which includes the

study of capital market, corporate finance and governance, financial institutions etc. It has huge

impact upon the structure and formulation of the global financial markets. With the help of it, the

growth and innovation in an industry could be promoted which is very important for the

optimum allocation of risk and capital. With the help of it, existing hypotheses of the economy

are analysed and then it is used to forecast the historical data and future trends. When the

econometrics are applied to the finance related problems then these are known as financial

econometrics so that solutions for the issues could be figured out. There are various types of

financial econometrics models which could be used for the purpose of conducting the

investigation (Chen and Jin, 2020). Description of all of them is as follows:

Analysis of high frequency price observations: It is one of the main and commonly used

model of financial econometrics investigations. With the help of it, financial analysis of high

frequency trading could be conducted. When the data is high frequency then it provides intraday

observations that could be used to understand the behaviour of the market. Apart from this, it

could also be used to analyse the micro structure and dynamics of the market. It helps to

determine that the stock prices that are provided by LSE are efficient or not because it provides

proper understanding of the changes in the share price index.

Arbitrage pricing theory: It is a model which is used in the asset pricing and it was

developed by Stephen Ross. It holds that the estimated return of an asset could be modelled as

the linear function of different types of theoretical market indices or the factors. It could be used

in case of changes in all the factors which is represented by beta coefficient. When it is used for

the purpose of analysis of prices index it helps to analyse the linear relationship of the factors.

When it is not possible to use capital asset pricing model then it could be used as it is an

alternative for the same theory (Chow, 2018).

Asset price dynamics: This model specifies different types of statements that are having

proper detail to specify the probability distribution of future prices of an asset. When it is used

then such elements are used which are empirically credible and able to explain the historical

6

Carrying out the financial econometrics investigation to critical examine the level of

informational efficiency of the London Stock Exchange market

Financial econometrics could be defined as the application of various types of statistical

models in the data of financial market. It I a branch of financial economics which includes the

study of capital market, corporate finance and governance, financial institutions etc. It has huge

impact upon the structure and formulation of the global financial markets. With the help of it, the

growth and innovation in an industry could be promoted which is very important for the

optimum allocation of risk and capital. With the help of it, existing hypotheses of the economy

are analysed and then it is used to forecast the historical data and future trends. When the

econometrics are applied to the finance related problems then these are known as financial

econometrics so that solutions for the issues could be figured out. There are various types of

financial econometrics models which could be used for the purpose of conducting the

investigation (Chen and Jin, 2020). Description of all of them is as follows:

Analysis of high frequency price observations: It is one of the main and commonly used

model of financial econometrics investigations. With the help of it, financial analysis of high

frequency trading could be conducted. When the data is high frequency then it provides intraday

observations that could be used to understand the behaviour of the market. Apart from this, it

could also be used to analyse the micro structure and dynamics of the market. It helps to

determine that the stock prices that are provided by LSE are efficient or not because it provides

proper understanding of the changes in the share price index.

Arbitrage pricing theory: It is a model which is used in the asset pricing and it was

developed by Stephen Ross. It holds that the estimated return of an asset could be modelled as

the linear function of different types of theoretical market indices or the factors. It could be used

in case of changes in all the factors which is represented by beta coefficient. When it is used for

the purpose of analysis of prices index it helps to analyse the linear relationship of the factors.

When it is not possible to use capital asset pricing model then it could be used as it is an

alternative for the same theory (Chow, 2018).

Asset price dynamics: This model specifies different types of statements that are having

proper detail to specify the probability distribution of future prices of an asset. When it is used

then such elements are used which are empirically credible and able to explain the historical

6

prices that are already analysed by the investors. All the dynamics that are used in this model for

the purpose of conducting the investigation are focused with finance theory and statistical

evidences. When it will be used then it could be analysed that the source which is used to gather

the information of share price index is effectively informative or not.

Optimal price dynamics: It Is a model which is used for the purpose of analysing the

price discrimination so that it could be analysed that the buyer of security is able to pay the

amount for the security which was expected previously. With the help of it, the level at which the

profit could be maximised could be analysed. It can also be used for the purpose of analysing

that the information which is used from a trusted source is able informative enough to make any

type of judgement for future or not (Eleftheriou and Patsoulis, 2020).

Cointegration: It is a financial econometrics method which is used for the purpose of

finding the correlation between the long-term time series processes. It was developed in year

1987 by Clive Granger and Nobel Laureated Robert Engle. Some of the most popular tests of

this method are Johnsen test, Phillips Ouliaris Test and Engle Granger Test. With the help of all

of them, the arbitrager can analyse that the source of data which is used to gather information of

price index is able to meet the expectations and it is informative enough or not. It is also known

as the long-term relationship between the variables that are analysed for the purpose of

investigation.

Event study: It is a type of empirical analysis which is conducted for a security traded in

the financial market. With the help of it, impact of the contingent event or the significant catalyst

occurrence could be analysed. All the event studies that are conducted for analysing the share

price indexes are able to reveal the essential data about the way in which the security will react to

the given event. When it will be used for making sure that the information used from the source

for assessment of financial econometrics investigation is effective or not then it may guide to

formulate the right decision (Ficici, 2018).

Autoregressive conditional heteroskedasticity: It is a non-linear model which is used in

the financial econometric investigation. It is a tie series statistical method applied for the purpose

of analysing the impacts that are left by the unexplained models of econometrics. When it is used

then the users can determine the error term which is the residual result left unexplained by the

model. With the help of it, variance of current error could be determined so that it could be

analysed that the information which is used for gathering the results is accurate or not.

7

the purpose of conducting the investigation are focused with finance theory and statistical

evidences. When it will be used then it could be analysed that the source which is used to gather

the information of share price index is effectively informative or not.

Optimal price dynamics: It Is a model which is used for the purpose of analysing the

price discrimination so that it could be analysed that the buyer of security is able to pay the

amount for the security which was expected previously. With the help of it, the level at which the

profit could be maximised could be analysed. It can also be used for the purpose of analysing

that the information which is used from a trusted source is able informative enough to make any

type of judgement for future or not (Eleftheriou and Patsoulis, 2020).

Cointegration: It is a financial econometrics method which is used for the purpose of

finding the correlation between the long-term time series processes. It was developed in year

1987 by Clive Granger and Nobel Laureated Robert Engle. Some of the most popular tests of

this method are Johnsen test, Phillips Ouliaris Test and Engle Granger Test. With the help of all

of them, the arbitrager can analyse that the source of data which is used to gather information of

price index is able to meet the expectations and it is informative enough or not. It is also known

as the long-term relationship between the variables that are analysed for the purpose of

investigation.

Event study: It is a type of empirical analysis which is conducted for a security traded in

the financial market. With the help of it, impact of the contingent event or the significant catalyst

occurrence could be analysed. All the event studies that are conducted for analysing the share

price indexes are able to reveal the essential data about the way in which the security will react to

the given event. When it will be used for making sure that the information used from the source

for assessment of financial econometrics investigation is effective or not then it may guide to

formulate the right decision (Ficici, 2018).

Autoregressive conditional heteroskedasticity: It is a non-linear model which is used in

the financial econometric investigation. It is a tie series statistical method applied for the purpose

of analysing the impacts that are left by the unexplained models of econometrics. When it is used

then the users can determine the error term which is the residual result left unexplained by the

model. With the help of it, variance of current error could be determined so that it could be

analysed that the information which is used for gathering the results is accurate or not.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From all the above described models of financial econometric investigation the first

model which is Analysis of high frequency price observations will be used to analyse that LSE

(London Stock Exchange) is effectively informative or not. For the purpose of analysis of the

pricing index the three companies that are selected are Fresnillo Plc, Avast Plc and Poly Metal

International Plc. All these companies are listed on London Stock Exchange. In order to conduct

the investigation and apply the model of Analysis of high frequency price observations

following charts are generated for pricing index of all the companies:

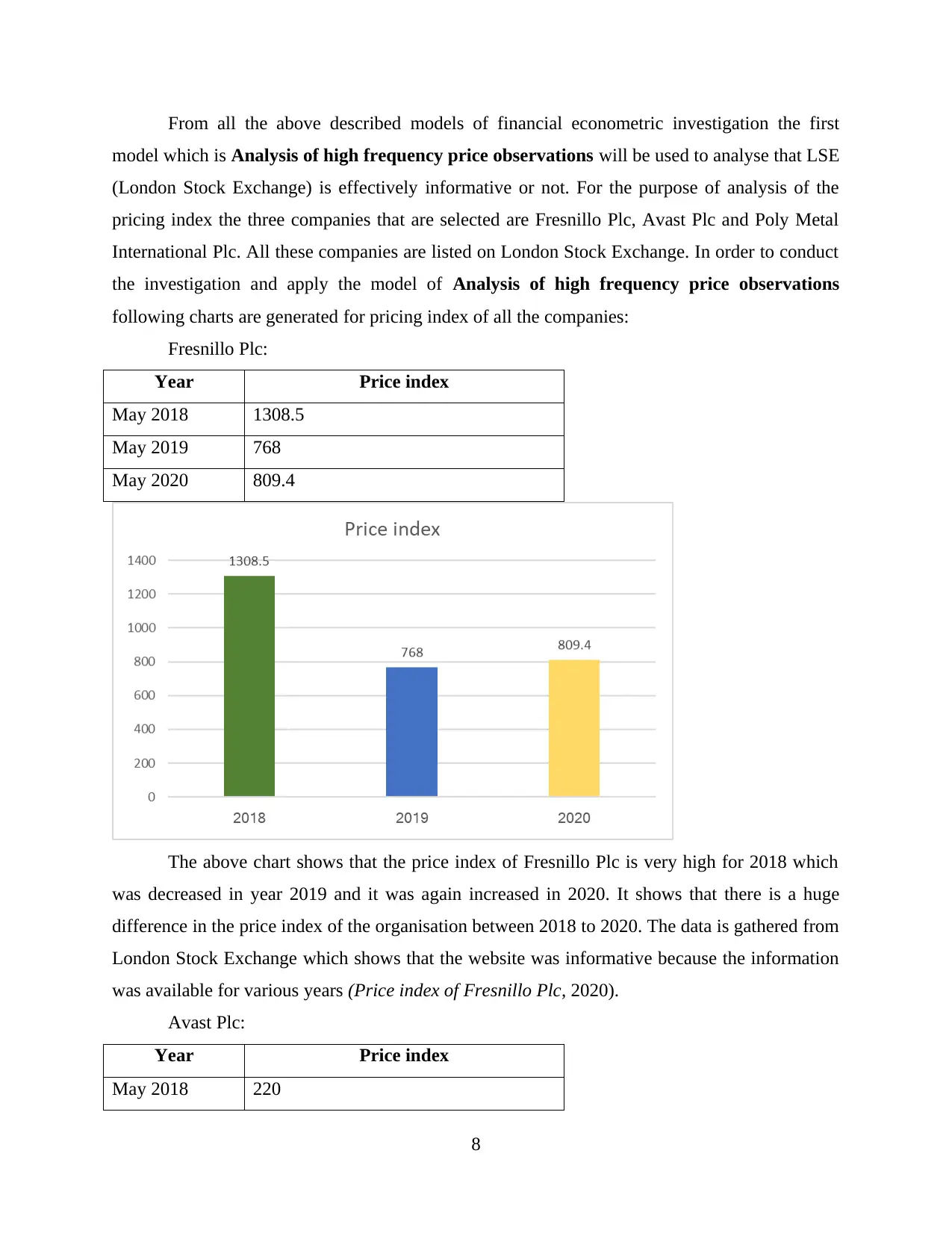

Fresnillo Plc:

Year Price index

May 2018 1308.5

May 2019 768

May 2020 809.4

The above chart shows that the price index of Fresnillo Plc is very high for 2018 which

was decreased in year 2019 and it was again increased in 2020. It shows that there is a huge

difference in the price index of the organisation between 2018 to 2020. The data is gathered from

London Stock Exchange which shows that the website was informative because the information

was available for various years (Price index of Fresnillo Plc, 2020).

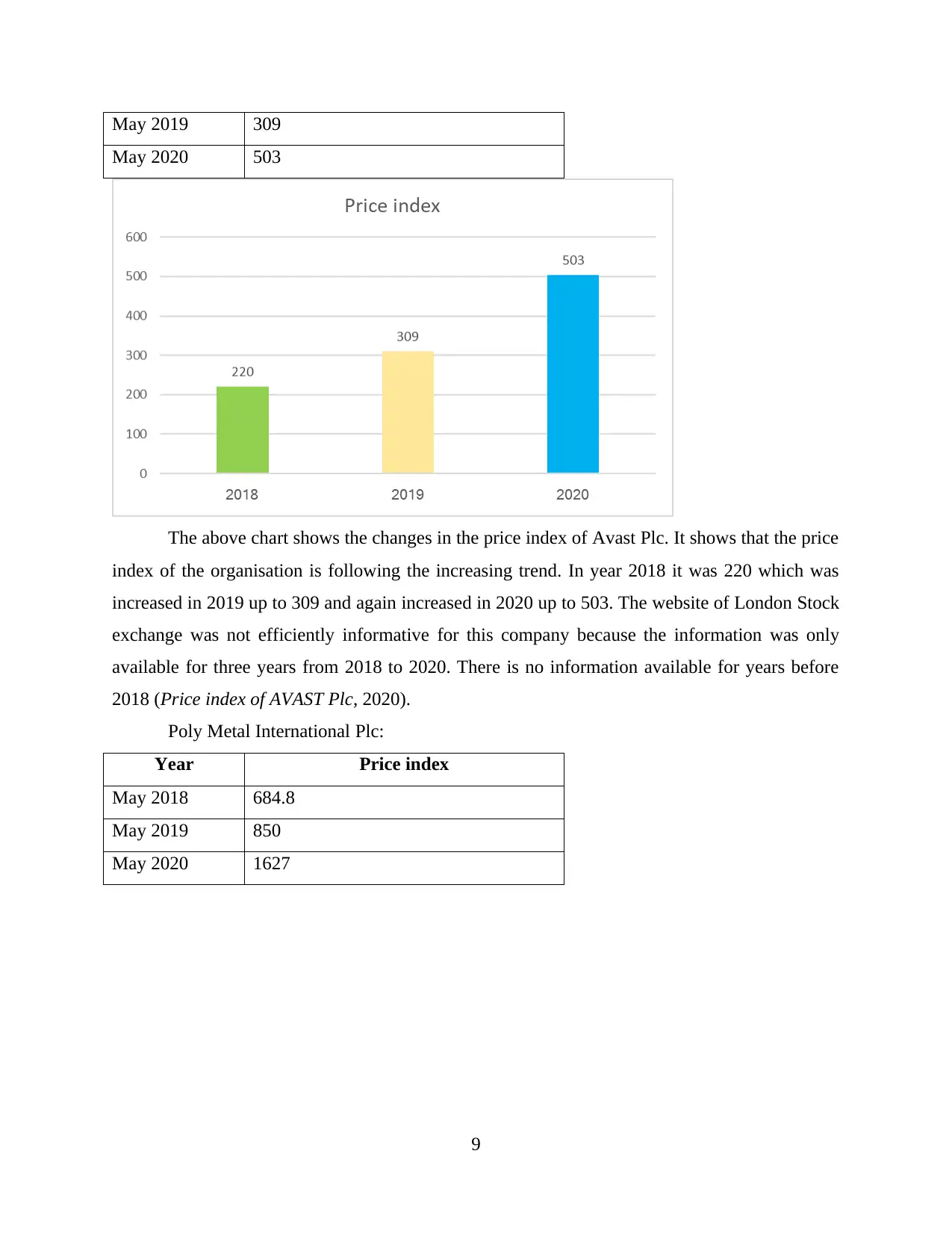

Avast Plc:

Year Price index

May 2018 220

8

model which is Analysis of high frequency price observations will be used to analyse that LSE

(London Stock Exchange) is effectively informative or not. For the purpose of analysis of the

pricing index the three companies that are selected are Fresnillo Plc, Avast Plc and Poly Metal

International Plc. All these companies are listed on London Stock Exchange. In order to conduct

the investigation and apply the model of Analysis of high frequency price observations

following charts are generated for pricing index of all the companies:

Fresnillo Plc:

Year Price index

May 2018 1308.5

May 2019 768

May 2020 809.4

The above chart shows that the price index of Fresnillo Plc is very high for 2018 which

was decreased in year 2019 and it was again increased in 2020. It shows that there is a huge

difference in the price index of the organisation between 2018 to 2020. The data is gathered from

London Stock Exchange which shows that the website was informative because the information

was available for various years (Price index of Fresnillo Plc, 2020).

Avast Plc:

Year Price index

May 2018 220

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

May 2019 309

May 2020 503

The above chart shows the changes in the price index of Avast Plc. It shows that the price

index of the organisation is following the increasing trend. In year 2018 it was 220 which was

increased in 2019 up to 309 and again increased in 2020 up to 503. The website of London Stock

exchange was not efficiently informative for this company because the information was only

available for three years from 2018 to 2020. There is no information available for years before

2018 (Price index of AVAST Plc, 2020).

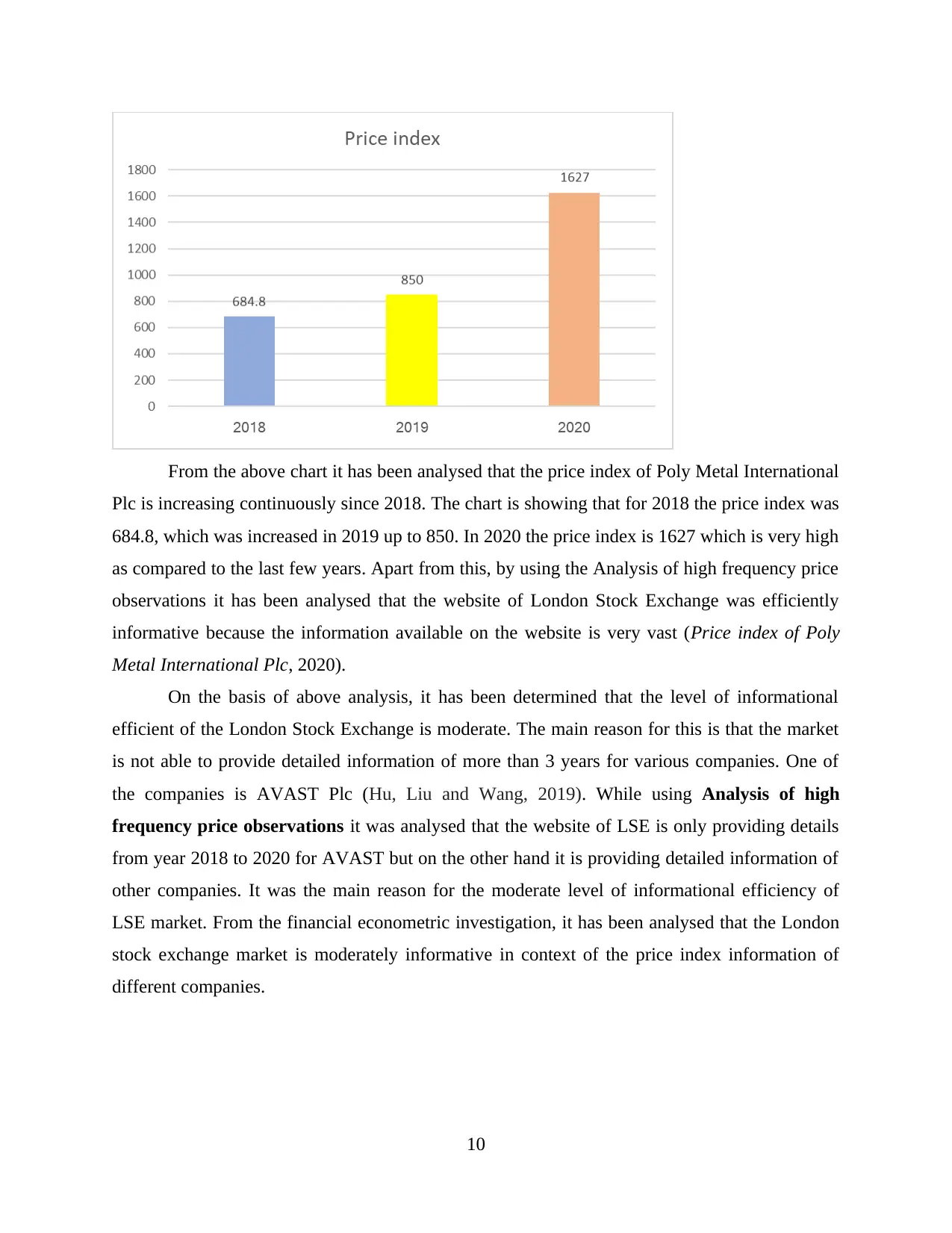

Poly Metal International Plc:

Year Price index

May 2018 684.8

May 2019 850

May 2020 1627

9

May 2020 503

The above chart shows the changes in the price index of Avast Plc. It shows that the price

index of the organisation is following the increasing trend. In year 2018 it was 220 which was

increased in 2019 up to 309 and again increased in 2020 up to 503. The website of London Stock

exchange was not efficiently informative for this company because the information was only

available for three years from 2018 to 2020. There is no information available for years before

2018 (Price index of AVAST Plc, 2020).

Poly Metal International Plc:

Year Price index

May 2018 684.8

May 2019 850

May 2020 1627

9

From the above chart it has been analysed that the price index of Poly Metal International

Plc is increasing continuously since 2018. The chart is showing that for 2018 the price index was

684.8, which was increased in 2019 up to 850. In 2020 the price index is 1627 which is very high

as compared to the last few years. Apart from this, by using the Analysis of high frequency price

observations it has been analysed that the website of London Stock Exchange was efficiently

informative because the information available on the website is very vast (Price index of Poly

Metal International Plc, 2020).

On the basis of above analysis, it has been determined that the level of informational

efficient of the London Stock Exchange is moderate. The main reason for this is that the market

is not able to provide detailed information of more than 3 years for various companies. One of

the companies is AVAST Plc (Hu, Liu and Wang, 2019). While using Analysis of high

frequency price observations it was analysed that the website of LSE is only providing details

from year 2018 to 2020 for AVAST but on the other hand it is providing detailed information of

other companies. It was the main reason for the moderate level of informational efficiency of

LSE market. From the financial econometric investigation, it has been analysed that the London

stock exchange market is moderately informative in context of the price index information of

different companies.

10

Plc is increasing continuously since 2018. The chart is showing that for 2018 the price index was

684.8, which was increased in 2019 up to 850. In 2020 the price index is 1627 which is very high

as compared to the last few years. Apart from this, by using the Analysis of high frequency price

observations it has been analysed that the website of London Stock Exchange was efficiently

informative because the information available on the website is very vast (Price index of Poly

Metal International Plc, 2020).

On the basis of above analysis, it has been determined that the level of informational

efficient of the London Stock Exchange is moderate. The main reason for this is that the market

is not able to provide detailed information of more than 3 years for various companies. One of

the companies is AVAST Plc (Hu, Liu and Wang, 2019). While using Analysis of high

frequency price observations it was analysed that the website of LSE is only providing details

from year 2018 to 2020 for AVAST but on the other hand it is providing detailed information of

other companies. It was the main reason for the moderate level of informational efficiency of

LSE market. From the financial econometric investigation, it has been analysed that the London

stock exchange market is moderately informative in context of the price index information of

different companies.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.