International Financial Reporting: Analysis and Interpretation

VerifiedAdded on 2020/12/29

|15

|4180

|477

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with an introduction to its context and purpose, followed by an examination of the conceptual and regulatory frameworks, including their requirements and objectives. The report identifies key stakeholders and their benefits from financial information, emphasizing the value of financial reporting in organizational growth. It includes an analysis of Goodwin PLC's financial statements prepared according to IAS 1, covering the statement of profit and loss, changes in equity, financial position (balance sheet), and cash flow. The report also interprets the financial performance of Marks & Spencer plc using liquidity, profitability, and solvency ratios, and distinguishes between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS). Furthermore, it evaluates the benefits of IFRS, identifies varying degrees of IFRS compliance across nations, and concludes with a summary of key findings.

INTERNATIONAL FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Discussing the context and purpose of financial reporting.....................................................1

2. Examining the conceptual and regulatory framework with their requirement and purposes..2

3. Identifying the main stakeholder of the organisation and their benefit from financial

information..................................................................................................................................3

4. Examining the value of financial reporting in achieving the organisational growth..............4

5. The financial statements of Goodwin plc as per IAS 1. 150..................................................5

a).Godwin PLC Statement of Profit and Loss for the year ended 31 December 2017...............5

b). statement of equity change....................................................................................................6

c.) financial position or balance sheet of Goodwin plc...............................................................8

d). explaining the information that are provided by cash flow in comparison to other financial

statements....................................................................................................................................8

6. Interpreting the financial performance of Marks & Spencer plc............................................9

7.Explaining the difference between International Accounting Standard and International

Financial reporting Standard.....................................................................................................11

8. Evaluating the benefit of IFRS..............................................................................................12

9. Identifying the various degree of compliance of IFRS across the nation with relevant

example.....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

1. Discussing the context and purpose of financial reporting.....................................................1

2. Examining the conceptual and regulatory framework with their requirement and purposes..2

3. Identifying the main stakeholder of the organisation and their benefit from financial

information..................................................................................................................................3

4. Examining the value of financial reporting in achieving the organisational growth..............4

5. The financial statements of Goodwin plc as per IAS 1. 150..................................................5

a).Godwin PLC Statement of Profit and Loss for the year ended 31 December 2017...............5

b). statement of equity change....................................................................................................6

c.) financial position or balance sheet of Goodwin plc...............................................................8

d). explaining the information that are provided by cash flow in comparison to other financial

statements....................................................................................................................................8

6. Interpreting the financial performance of Marks & Spencer plc............................................9

7.Explaining the difference between International Accounting Standard and International

Financial reporting Standard.....................................................................................................11

8. Evaluating the benefit of IFRS..............................................................................................12

9. Identifying the various degree of compliance of IFRS across the nation with relevant

example.....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial reporting is an important concept for any organisation, it is the process which

helps in disclosure of the financial results and the related financial information to management of

company. It helps the management and external users or stakeholders in evaluating the financial

performance of the company which helps them in making decision regarding investing in

company. As a junior accountant in organisation, present report is prepared which will discussed

about the financial reporting system and different aspects of financial reporting. The present

report will help in outlines different components and purpose of preparing financial reports.

Further, conceptual regulatory framework and its important will be discuss in study. Report will

also help in understanding the importance of financial information to different stakeholder of

organisation and in the organisation's growth. The project will include the financial statement of

Goodwin plc as per IAS 1. Moreover, a comparison will be present on different regulatory board

of accounting with their benefits in financial accounting. Present report will also discuss about

different compliance with IFRS in different nation with a relevant example.

1. Discussing the context and purpose of financial reporting.

It the process which helps in transforming the financial information and financial

performance of the company to the management and stakeholders of the company. It is an

important process for Goodwin plc which helps the management and stakeholder to analyse the

financial information which will help them to decide the financial condition of the organisation.

Financial reporting includes the preparation of the financial statements. It in mandatory for all

company to produce and publish their financial statements.

Financial reports are usually prepared on the quarterly or yearly basis. The components of

the financial reports are as follows:

Balance sheet: This report helps in showing Goodwin plc's assets, liability and owner's

equity at a certain point of time. It can be prepared at the end of quarter or yearly basis (Barth,

2018).

Income statement: It assist in showing Goodwin plc' income, expenses and overall

profit in a year. This reports also includes sales and all other expenses that are incurred in that

year.

1

Financial reporting is an important concept for any organisation, it is the process which

helps in disclosure of the financial results and the related financial information to management of

company. It helps the management and external users or stakeholders in evaluating the financial

performance of the company which helps them in making decision regarding investing in

company. As a junior accountant in organisation, present report is prepared which will discussed

about the financial reporting system and different aspects of financial reporting. The present

report will help in outlines different components and purpose of preparing financial reports.

Further, conceptual regulatory framework and its important will be discuss in study. Report will

also help in understanding the importance of financial information to different stakeholder of

organisation and in the organisation's growth. The project will include the financial statement of

Goodwin plc as per IAS 1. Moreover, a comparison will be present on different regulatory board

of accounting with their benefits in financial accounting. Present report will also discuss about

different compliance with IFRS in different nation with a relevant example.

1. Discussing the context and purpose of financial reporting.

It the process which helps in transforming the financial information and financial

performance of the company to the management and stakeholders of the company. It is an

important process for Goodwin plc which helps the management and stakeholder to analyse the

financial information which will help them to decide the financial condition of the organisation.

Financial reporting includes the preparation of the financial statements. It in mandatory for all

company to produce and publish their financial statements.

Financial reports are usually prepared on the quarterly or yearly basis. The components of

the financial reports are as follows:

Balance sheet: This report helps in showing Goodwin plc's assets, liability and owner's

equity at a certain point of time. It can be prepared at the end of quarter or yearly basis (Barth,

2018).

Income statement: It assist in showing Goodwin plc' income, expenses and overall

profit in a year. This reports also includes sales and all other expenses that are incurred in that

year.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Statement of retain earning: it is the report which help in knowing the stakeholder and

the management on the changes in the equity of the company in a specific period.

Cash Flow Statement: It is the report which shows the company's cash inflow and

outflow activity.

The purpose of the financial reporting are as follows:

To provide accurate information to management of Goodwin plc that are beneficial in

the purpose of planning, analysing, benchmarking and other decision making process.

The main purpose of preparing the financial report is to provide the information to the

company' to investors, promoters, debt provider and other creditors. It will help them in

making decision regarding their investment in Goodwin Plc(Bonsall IV and et.al., 2017).

It also assist in showing the performance of the management.

2. Examining the conceptual and regulatory framework with their requirement and purposes.

In financial reporting, conceptual framework can be defined as the theory according to

which the financial reporting are being prepared. The conceptual framework is helps in dealing

with the issues regarding the preparation of the financial statements of the companies. The

regulatory framework ensures the purpose of preparing the financial statements that are

mandatory as it it is essential for the financial statements users in accomplishing their needs from

this information. The main purpose of the conceptual framework are:

Assisting the development of future IFRS and the checking of the existing standard that

are set up in the process of the underlying the concepts.

In order to promote the accounting regulation and the standard that are help in reducing

the number of alternative accounting treatments (Leuz and Wysocki, 2016).

To assist the preparation of financial statements with the proper application of IFRS, it

also includes the dealing of the accounting transaction which do not have proper

accounting standard.

The key principles of Financial accounting reporting are as follows:

Accounting principles includes both accounting concepts and convections that are as

follows:

2

the management on the changes in the equity of the company in a specific period.

Cash Flow Statement: It is the report which shows the company's cash inflow and

outflow activity.

The purpose of the financial reporting are as follows:

To provide accurate information to management of Goodwin plc that are beneficial in

the purpose of planning, analysing, benchmarking and other decision making process.

The main purpose of preparing the financial report is to provide the information to the

company' to investors, promoters, debt provider and other creditors. It will help them in

making decision regarding their investment in Goodwin Plc(Bonsall IV and et.al., 2017).

It also assist in showing the performance of the management.

2. Examining the conceptual and regulatory framework with their requirement and purposes.

In financial reporting, conceptual framework can be defined as the theory according to

which the financial reporting are being prepared. The conceptual framework is helps in dealing

with the issues regarding the preparation of the financial statements of the companies. The

regulatory framework ensures the purpose of preparing the financial statements that are

mandatory as it it is essential for the financial statements users in accomplishing their needs from

this information. The main purpose of the conceptual framework are:

Assisting the development of future IFRS and the checking of the existing standard that

are set up in the process of the underlying the concepts.

In order to promote the accounting regulation and the standard that are help in reducing

the number of alternative accounting treatments (Leuz and Wysocki, 2016).

To assist the preparation of financial statements with the proper application of IFRS, it

also includes the dealing of the accounting transaction which do not have proper

accounting standard.

The key principles of Financial accounting reporting are as follows:

Accounting principles includes both accounting concepts and convections that are as

follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Money measurement concept: All the business transaction should be expressed in terms

of money which are recorded in the statements.

Business entity concept: a business entity has to treated differently from its owner. All

the transaction will be recorded separately.

Going concern concept: the business is expected to be continue for a long time.

The importance of having qualitative characteristics of financial statements are as follows:

Understandability: it guides the preparation of the financial statements in a away that can

be properly understandable to the external users.

Relevance: it is important for the stakeholders to get the relevant information, it will help

the users in evaluating their decision making process.

Reliability: this characteristics in important for preparing the financial information that

are free from errors, the reporting should be complete and free from any bias.

Comparability: this characteristics helps in making the financial information in a way that

can be easily be compared with the other company's financial information.

3. Identifying the main stakeholder of the organisation and their benefit from financial

information.

These can be refers as the different individual, groups or the organisation that have

concerns of the performance and business activities of Goodwin Plc. Stakeholders are the

important part of the organisation as they can be affected and can influence the business

operations of company. The main stakeholders of Goodwin plc are as follows:

Shareholders: they are the equity investors in the company who are expected to get

better return of their investment from the company (Nobes, 2014). Financial information will

help them in getting the information of current financial position of the company. It helps in

providing the current cash flow information, which are the source of their cash in form of

dividend.

Suppliers: they are the one who provide raw material in the manufacturing of the goods

and services to the organisation. They wants to be assured of getting their amount on time,

financial information will help them in knowing the status of cash flow of GoodWin plc.

3

of money which are recorded in the statements.

Business entity concept: a business entity has to treated differently from its owner. All

the transaction will be recorded separately.

Going concern concept: the business is expected to be continue for a long time.

The importance of having qualitative characteristics of financial statements are as follows:

Understandability: it guides the preparation of the financial statements in a away that can

be properly understandable to the external users.

Relevance: it is important for the stakeholders to get the relevant information, it will help

the users in evaluating their decision making process.

Reliability: this characteristics in important for preparing the financial information that

are free from errors, the reporting should be complete and free from any bias.

Comparability: this characteristics helps in making the financial information in a way that

can be easily be compared with the other company's financial information.

3. Identifying the main stakeholder of the organisation and their benefit from financial

information.

These can be refers as the different individual, groups or the organisation that have

concerns of the performance and business activities of Goodwin Plc. Stakeholders are the

important part of the organisation as they can be affected and can influence the business

operations of company. The main stakeholders of Goodwin plc are as follows:

Shareholders: they are the equity investors in the company who are expected to get

better return of their investment from the company (Nobes, 2014). Financial information will

help them in getting the information of current financial position of the company. It helps in

providing the current cash flow information, which are the source of their cash in form of

dividend.

Suppliers: they are the one who provide raw material in the manufacturing of the goods

and services to the organisation. They wants to be assured of getting their amount on time,

financial information will help them in knowing the status of cash flow of GoodWin plc.

3

Employees: they are the most important resources of the company, they work in order to

lead the growth of the company and improving its financial performance. The financial

information will help the employees in evaluating the stability, profitability and growth of the

company. It helps in ensuring the employees as the growth of the company will give them

opportunity for their personal growth and development in their career.

Customers: They are main source of the company to generate the revenue. Goodwin Plc

is a source of getting the goods and services to the customers. With the help of financial

information, the customer can judge the profitability of the company and ability in providing

them the goods and the services (Francis and et.al., 2015). With the help of the financial

information, customer can evaluate the profitability of the company which is also essential in

creating the goodwill of the company in market.

4. Examining the value of financial reporting in achieving the organisational growth.

Financial reporting plays a vital role in the growth and success of Goodwin plc, it helps

in providing accurate and timely information regarding the company's financial performance and

position in order to make policies and strategies. The importance of the financial reporting in the

growth of Goodwin plc are:

The financial reporting helps the management of company in evaluating the performance

of several business activities in the organisation. The financial statements like cash flow and

income statements will help in determining the income and expenditure of the company.

Management can take better decisions in order to minimize the companies expenses and

increasing revenue of Goodwin plc (Kanapickienė and Grundienė, 2015). With the help of the

company's financial reporting, financial manager can easily monitor the cash inflow and outflow

of the company.. It also helps the manager to control the cash-flow in company. Proper business

reporting will help in ensuring timely recording of company's liability that helps in timely

payment of all the expenses. It will help Goodwin plc in increasing its goodwill in the market.

4

lead the growth of the company and improving its financial performance. The financial

information will help the employees in evaluating the stability, profitability and growth of the

company. It helps in ensuring the employees as the growth of the company will give them

opportunity for their personal growth and development in their career.

Customers: They are main source of the company to generate the revenue. Goodwin Plc

is a source of getting the goods and services to the customers. With the help of financial

information, the customer can judge the profitability of the company and ability in providing

them the goods and the services (Francis and et.al., 2015). With the help of the financial

information, customer can evaluate the profitability of the company which is also essential in

creating the goodwill of the company in market.

4. Examining the value of financial reporting in achieving the organisational growth.

Financial reporting plays a vital role in the growth and success of Goodwin plc, it helps

in providing accurate and timely information regarding the company's financial performance and

position in order to make policies and strategies. The importance of the financial reporting in the

growth of Goodwin plc are:

The financial reporting helps the management of company in evaluating the performance

of several business activities in the organisation. The financial statements like cash flow and

income statements will help in determining the income and expenditure of the company.

Management can take better decisions in order to minimize the companies expenses and

increasing revenue of Goodwin plc (Kanapickienė and Grundienė, 2015). With the help of the

company's financial reporting, financial manager can easily monitor the cash inflow and outflow

of the company.. It also helps the manager to control the cash-flow in company. Proper business

reporting will help in ensuring timely recording of company's liability that helps in timely

payment of all the expenses. It will help Goodwin plc in increasing its goodwill in the market.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

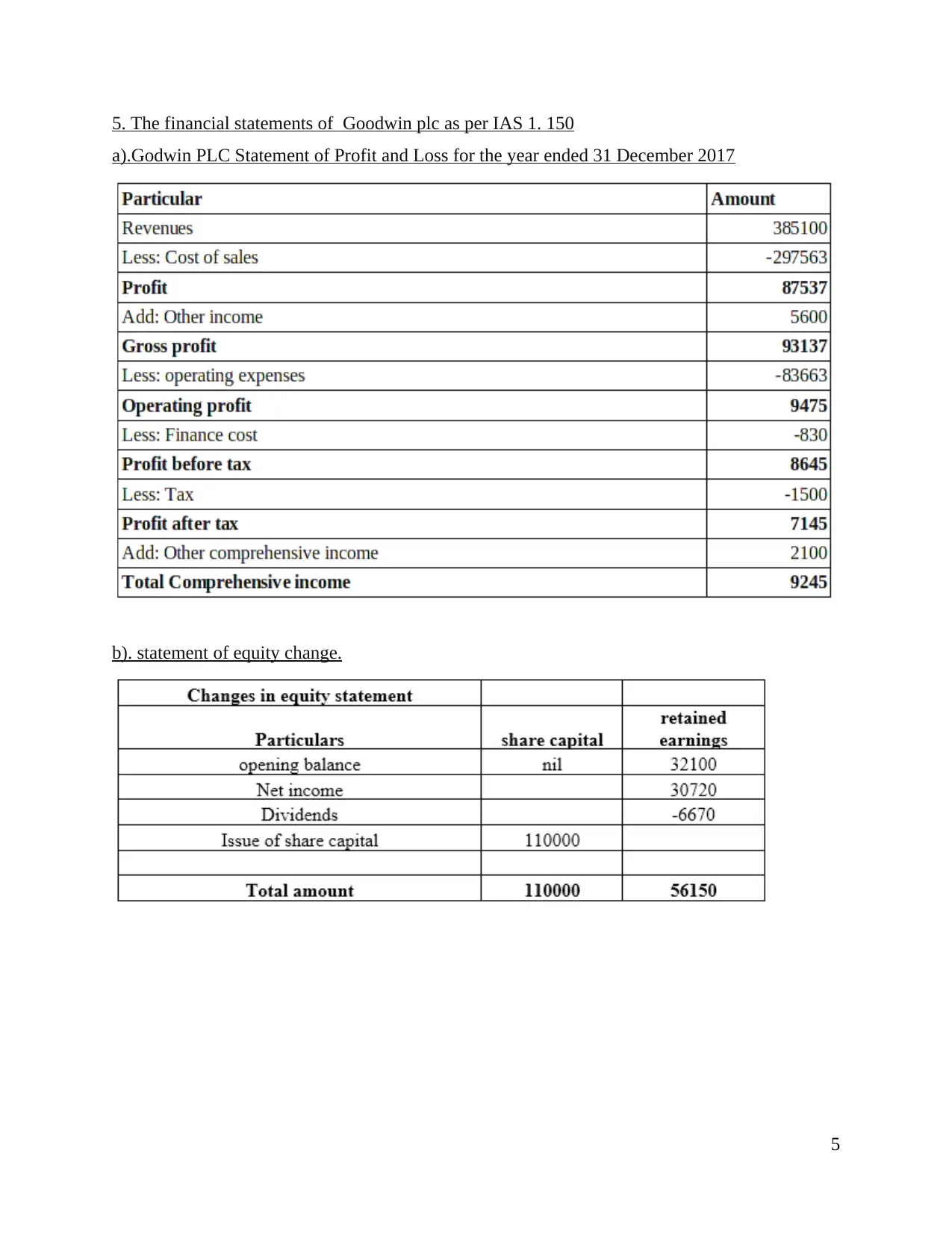

5. The financial statements of Goodwin plc as per IAS 1. 150

a).Godwin PLC Statement of Profit and Loss for the year ended 31 December 2017

b). statement of equity change.

5

a).Godwin PLC Statement of Profit and Loss for the year ended 31 December 2017

b). statement of equity change.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

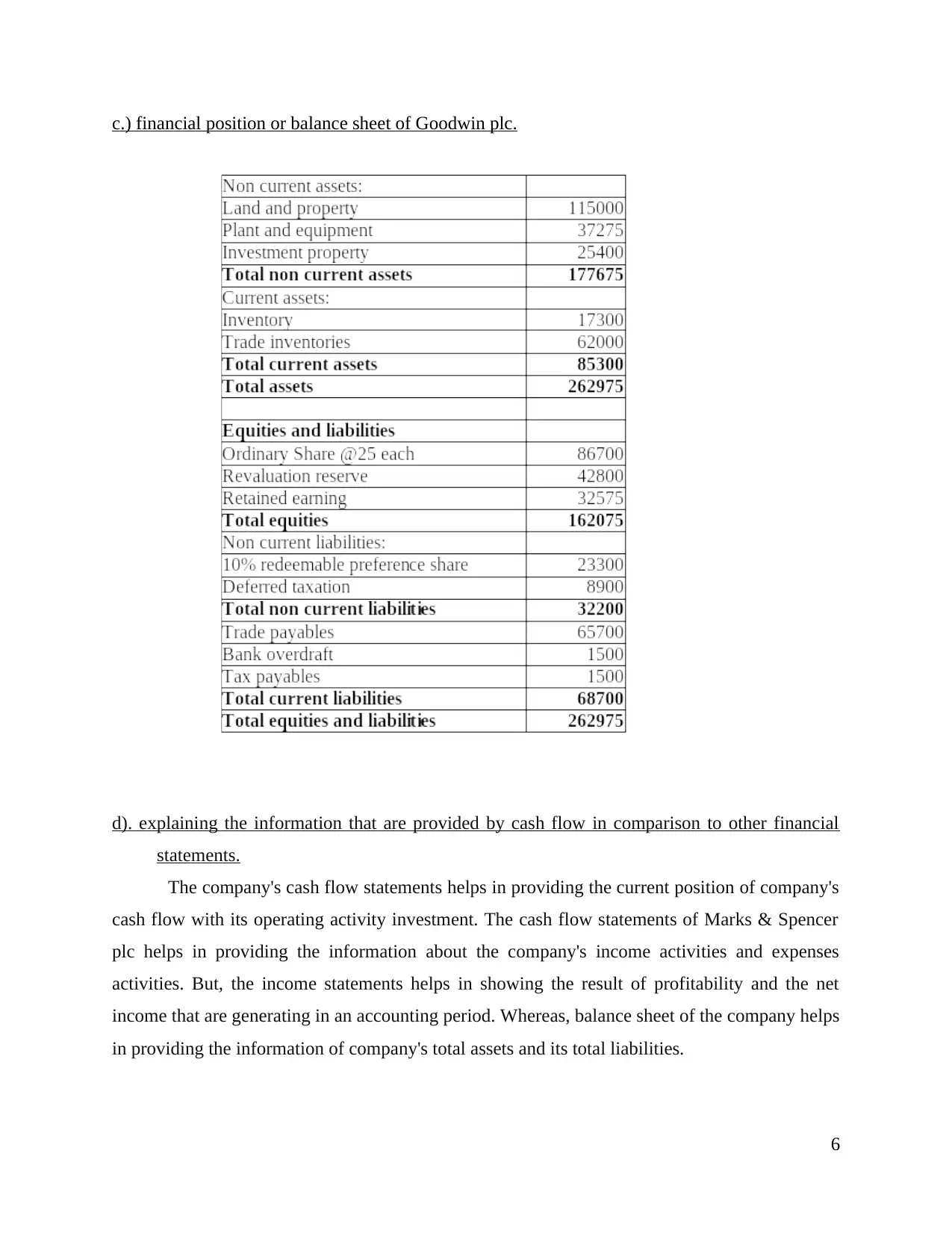

c.) financial position or balance sheet of Goodwin plc.

d). explaining the information that are provided by cash flow in comparison to other financial

statements.

The company's cash flow statements helps in providing the current position of company's

cash flow with its operating activity investment. The cash flow statements of Marks & Spencer

plc helps in providing the information about the company's income activities and expenses

activities. But, the income statements helps in showing the result of profitability and the net

income that are generating in an accounting period. Whereas, balance sheet of the company helps

in providing the information of company's total assets and its total liabilities.

6

d). explaining the information that are provided by cash flow in comparison to other financial

statements.

The company's cash flow statements helps in providing the current position of company's

cash flow with its operating activity investment. The cash flow statements of Marks & Spencer

plc helps in providing the information about the company's income activities and expenses

activities. But, the income statements helps in showing the result of profitability and the net

income that are generating in an accounting period. Whereas, balance sheet of the company helps

in providing the information of company's total assets and its total liabilities.

6

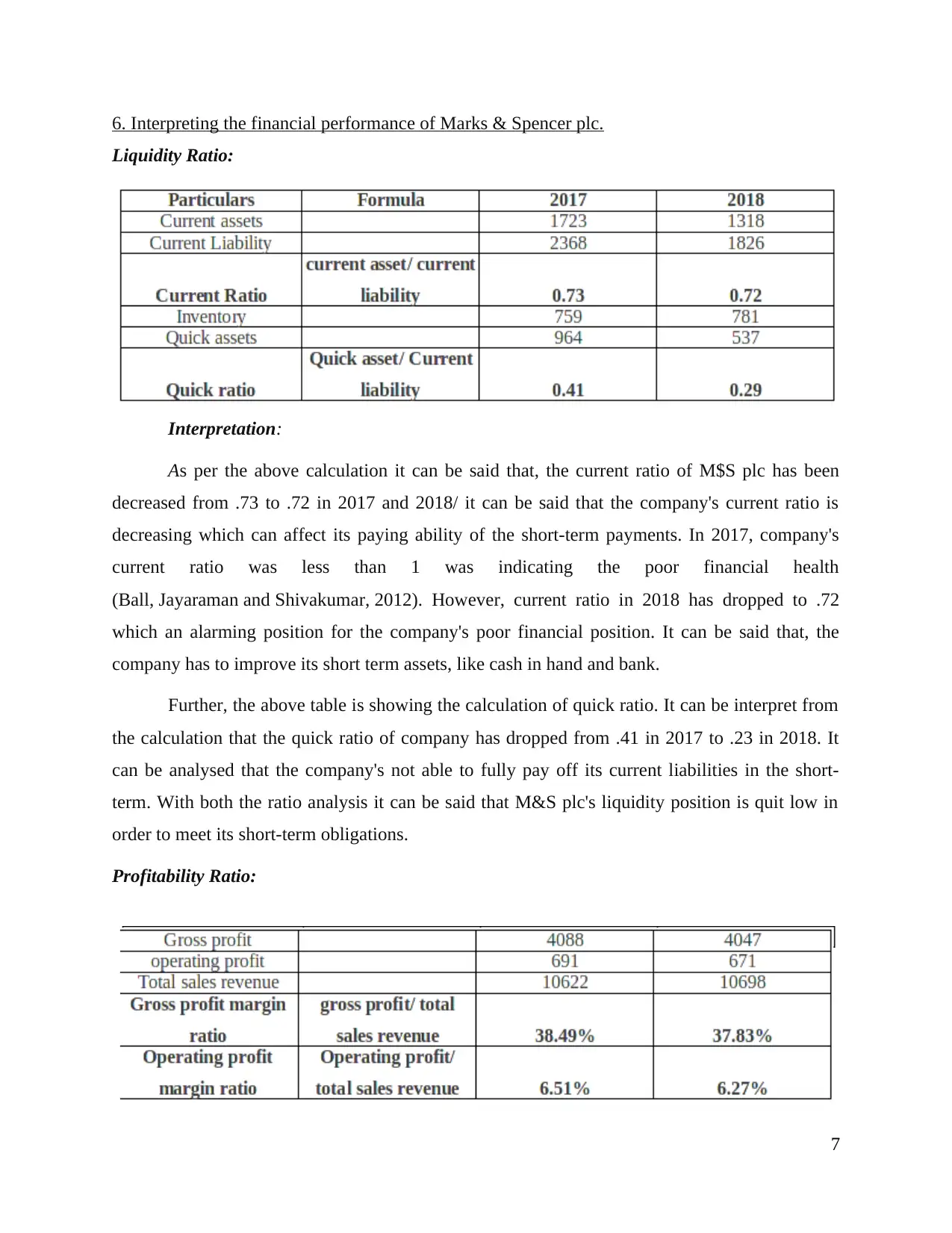

6. Interpreting the financial performance of Marks & Spencer plc.

Liquidity Ratio:

Interpretation:

As per the above calculation it can be said that, the current ratio of M$S plc has been

decreased from .73 to .72 in 2017 and 2018/ it can be said that the company's current ratio is

decreasing which can affect its paying ability of the short-term payments. In 2017, company's

current ratio was less than 1 was indicating the poor financial health

(Ball, Jayaraman and Shivakumar, 2012). However, current ratio in 2018 has dropped to .72

which an alarming position for the company's poor financial position. It can be said that, the

company has to improve its short term assets, like cash in hand and bank.

Further, the above table is showing the calculation of quick ratio. It can be interpret from

the calculation that the quick ratio of company has dropped from .41 in 2017 to .23 in 2018. It

can be analysed that the company's not able to fully pay off its current liabilities in the short-

term. With both the ratio analysis it can be said that M&S plc's liquidity position is quit low in

order to meet its short-term obligations.

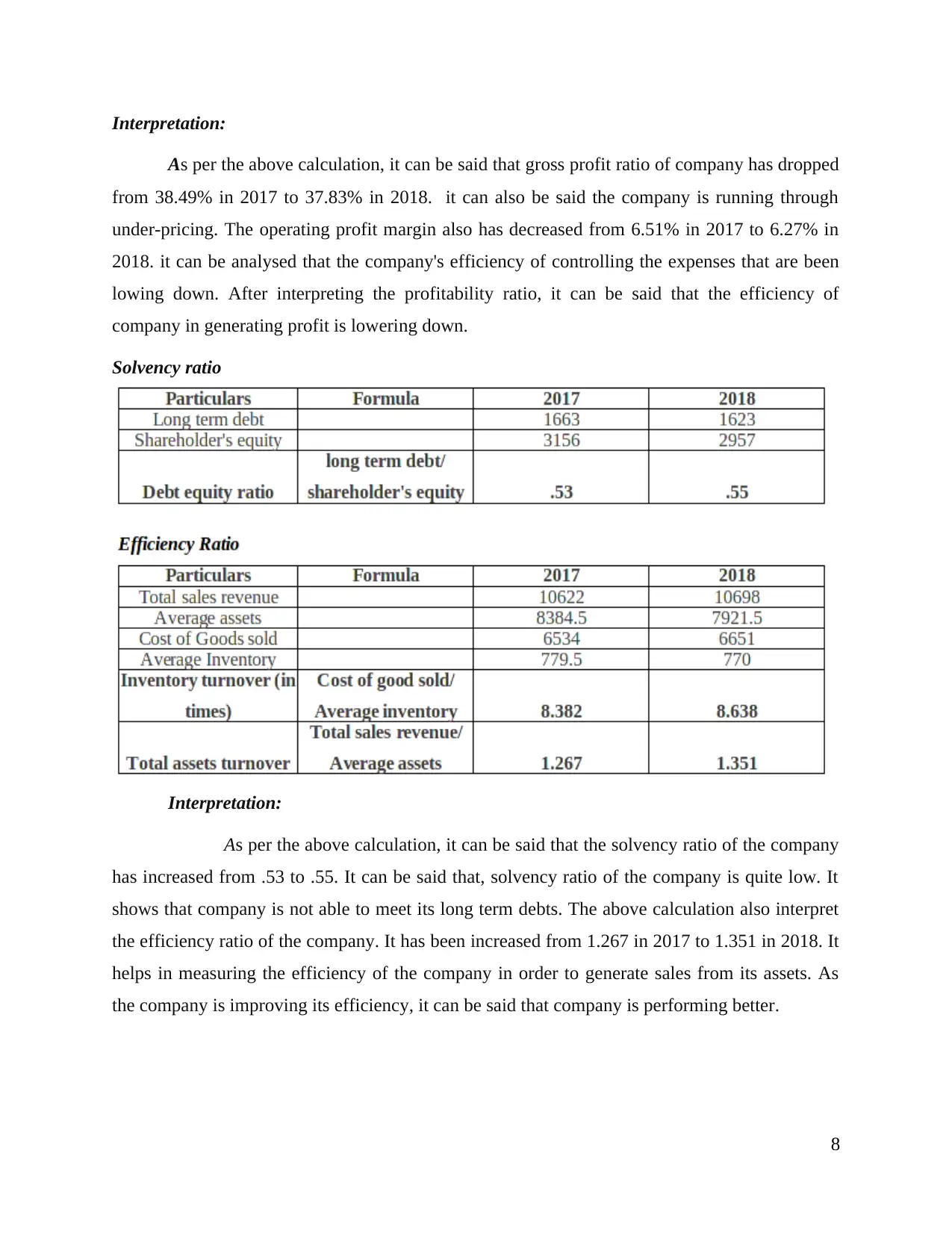

Profitability Ratio:

7

Liquidity Ratio:

Interpretation:

As per the above calculation it can be said that, the current ratio of M$S plc has been

decreased from .73 to .72 in 2017 and 2018/ it can be said that the company's current ratio is

decreasing which can affect its paying ability of the short-term payments. In 2017, company's

current ratio was less than 1 was indicating the poor financial health

(Ball, Jayaraman and Shivakumar, 2012). However, current ratio in 2018 has dropped to .72

which an alarming position for the company's poor financial position. It can be said that, the

company has to improve its short term assets, like cash in hand and bank.

Further, the above table is showing the calculation of quick ratio. It can be interpret from

the calculation that the quick ratio of company has dropped from .41 in 2017 to .23 in 2018. It

can be analysed that the company's not able to fully pay off its current liabilities in the short-

term. With both the ratio analysis it can be said that M&S plc's liquidity position is quit low in

order to meet its short-term obligations.

Profitability Ratio:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation:

As per the above calculation, it can be said that gross profit ratio of company has dropped

from 38.49% in 2017 to 37.83% in 2018. it can also be said the company is running through

under-pricing. The operating profit margin also has decreased from 6.51% in 2017 to 6.27% in

2018. it can be analysed that the company's efficiency of controlling the expenses that are been

lowing down. After interpreting the profitability ratio, it can be said that the efficiency of

company in generating profit is lowering down.

Solvency ratio

Interpretation:

As per the above calculation, it can be said that the solvency ratio of the company

has increased from .53 to .55. It can be said that, solvency ratio of the company is quite low. It

shows that company is not able to meet its long term debts. The above calculation also interpret

the efficiency ratio of the company. It has been increased from 1.267 in 2017 to 1.351 in 2018. It

helps in measuring the efficiency of the company in order to generate sales from its assets. As

the company is improving its efficiency, it can be said that company is performing better.

8

As per the above calculation, it can be said that gross profit ratio of company has dropped

from 38.49% in 2017 to 37.83% in 2018. it can also be said the company is running through

under-pricing. The operating profit margin also has decreased from 6.51% in 2017 to 6.27% in

2018. it can be analysed that the company's efficiency of controlling the expenses that are been

lowing down. After interpreting the profitability ratio, it can be said that the efficiency of

company in generating profit is lowering down.

Solvency ratio

Interpretation:

As per the above calculation, it can be said that the solvency ratio of the company

has increased from .53 to .55. It can be said that, solvency ratio of the company is quite low. It

shows that company is not able to meet its long term debts. The above calculation also interpret

the efficiency ratio of the company. It has been increased from 1.267 in 2017 to 1.351 in 2018. It

helps in measuring the efficiency of the company in order to generate sales from its assets. As

the company is improving its efficiency, it can be said that company is performing better.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

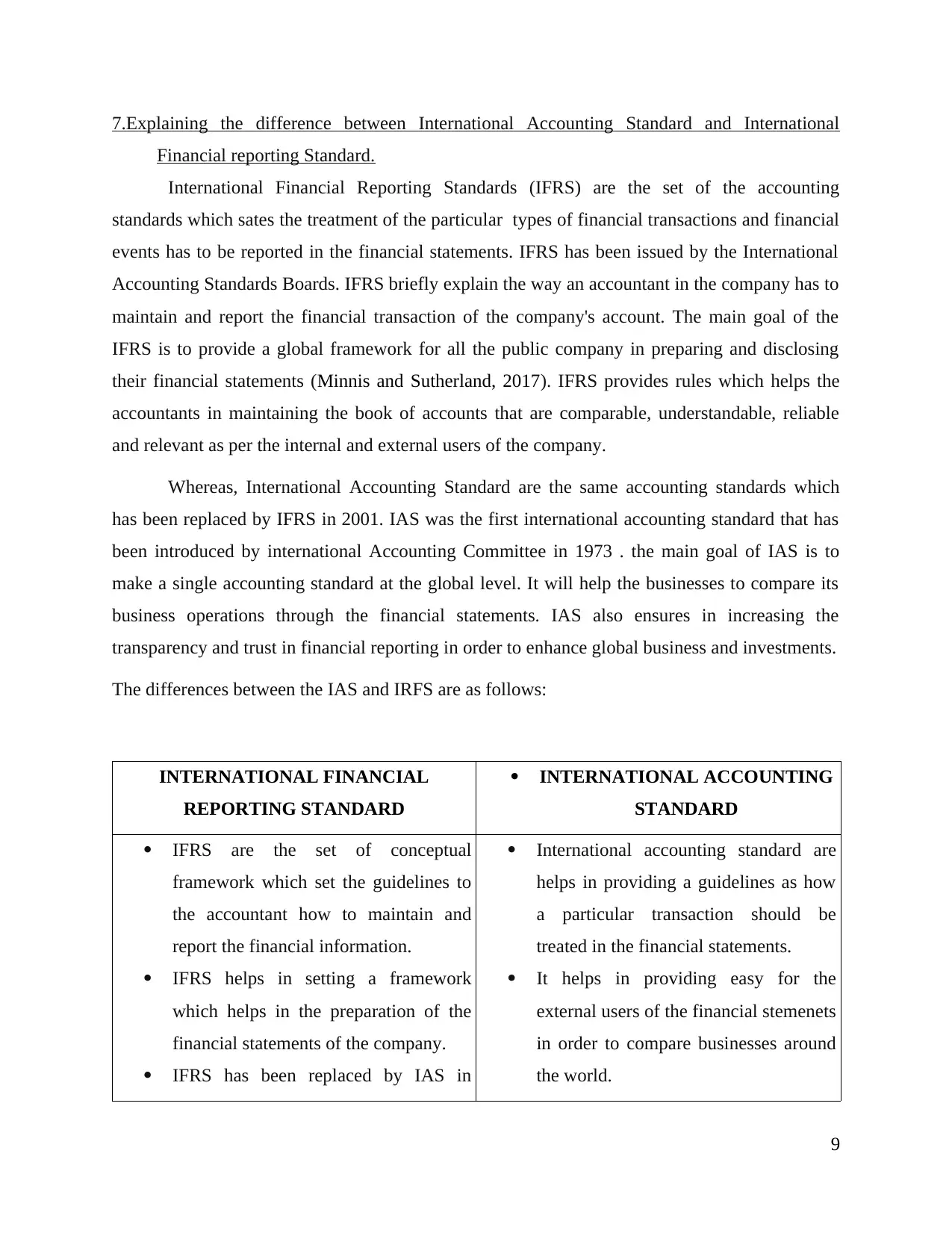

7.Explaining the difference between International Accounting Standard and International

Financial reporting Standard.

International Financial Reporting Standards (IFRS) are the set of the accounting

standards which sates the treatment of the particular types of financial transactions and financial

events has to be reported in the financial statements. IFRS has been issued by the International

Accounting Standards Boards. IFRS briefly explain the way an accountant in the company has to

maintain and report the financial transaction of the company's account. The main goal of the

IFRS is to provide a global framework for all the public company in preparing and disclosing

their financial statements (Minnis and Sutherland, 2017). IFRS provides rules which helps the

accountants in maintaining the book of accounts that are comparable, understandable, reliable

and relevant as per the internal and external users of the company.

Whereas, International Accounting Standard are the same accounting standards which

has been replaced by IFRS in 2001. IAS was the first international accounting standard that has

been introduced by international Accounting Committee in 1973 . the main goal of IAS is to

make a single accounting standard at the global level. It will help the businesses to compare its

business operations through the financial statements. IAS also ensures in increasing the

transparency and trust in financial reporting in order to enhance global business and investments.

The differences between the IAS and IRFS are as follows:

INTERNATIONAL FINANCIAL

REPORTING STANDARD

INTERNATIONAL ACCOUNTING

STANDARD

IFRS are the set of conceptual

framework which set the guidelines to

the accountant how to maintain and

report the financial information.

IFRS helps in setting a framework

which helps in the preparation of the

financial statements of the company.

IFRS has been replaced by IAS in

International accounting standard are

helps in providing a guidelines as how

a particular transaction should be

treated in the financial statements.

It helps in providing easy for the

external users of the financial stemenets

in order to compare businesses around

the world.

9

Financial reporting Standard.

International Financial Reporting Standards (IFRS) are the set of the accounting

standards which sates the treatment of the particular types of financial transactions and financial

events has to be reported in the financial statements. IFRS has been issued by the International

Accounting Standards Boards. IFRS briefly explain the way an accountant in the company has to

maintain and report the financial transaction of the company's account. The main goal of the

IFRS is to provide a global framework for all the public company in preparing and disclosing

their financial statements (Minnis and Sutherland, 2017). IFRS provides rules which helps the

accountants in maintaining the book of accounts that are comparable, understandable, reliable

and relevant as per the internal and external users of the company.

Whereas, International Accounting Standard are the same accounting standards which

has been replaced by IFRS in 2001. IAS was the first international accounting standard that has

been introduced by international Accounting Committee in 1973 . the main goal of IAS is to

make a single accounting standard at the global level. It will help the businesses to compare its

business operations through the financial statements. IAS also ensures in increasing the

transparency and trust in financial reporting in order to enhance global business and investments.

The differences between the IAS and IRFS are as follows:

INTERNATIONAL FINANCIAL

REPORTING STANDARD

INTERNATIONAL ACCOUNTING

STANDARD

IFRS are the set of conceptual

framework which set the guidelines to

the accountant how to maintain and

report the financial information.

IFRS helps in setting a framework

which helps in the preparation of the

financial statements of the company.

IFRS has been replaced by IAS in

International accounting standard are

helps in providing a guidelines as how

a particular transaction should be

treated in the financial statements.

It helps in providing easy for the

external users of the financial stemenets

in order to compare businesses around

the world.

9

2001, which is the newer version of

IAS.

IFRS has been formed in order to form

a common accounting language, so that

the business operations and accounting

can be understand easily of any

company in world.

The standard for the IFRS was

published by the International

Accounting Standard Board(IASB)

from 2001.

IAS were put in order to advice the

companies how to report the financial

events in a financial statements.

IAS is the first accounting standard

which has been introduced by the

International Accounting Standard

Committee in 1973.

The standard in the IAS has been

describes and formed by IASC in 1973.

8. Evaluating the benefit of IFRS.

Having an international standard in accounting is very essential for the companies that

are being operated in more than one country. Having a single set of accounting standard in

worldwide will help in simplifies the same accounting procedures in worldwide. The accounting

standards will help in creating one accounting language in a global level for the business to

operates its function (AICPA, 2017). International Financial Reporting system are being

designed to set a common global language for the business affairs which helps in simplifies the

other companies operations in order to understand and compare. IFRS provides a framework set

of rules to the accountant which helps them to maintain and record the financial information and

transaction in a way that can be comparable, understandable, reliable and relevant. As per the

IFRS, apart from the basic financial report. a company must have to give the summary of its

accounting principles.

IFRS are the single set of accounting that has been adopted in 110 countries as the

regulatory framework in preparing the financial statements of the country. The importance of

IRS has been increased as it helps in providing comparability of the financial information for

investors in order to invest in companies across borders (Importance of Financial Knowledge to

Business Success ,2018). With the adaptation of the IFRS, companies has achieved the lower

cost of capital and and more efficient in allocation of capital. The benefit of IFRS are as follows:

10

IAS.

IFRS has been formed in order to form

a common accounting language, so that

the business operations and accounting

can be understand easily of any

company in world.

The standard for the IFRS was

published by the International

Accounting Standard Board(IASB)

from 2001.

IAS were put in order to advice the

companies how to report the financial

events in a financial statements.

IAS is the first accounting standard

which has been introduced by the

International Accounting Standard

Committee in 1973.

The standard in the IAS has been

describes and formed by IASC in 1973.

8. Evaluating the benefit of IFRS.

Having an international standard in accounting is very essential for the companies that

are being operated in more than one country. Having a single set of accounting standard in

worldwide will help in simplifies the same accounting procedures in worldwide. The accounting

standards will help in creating one accounting language in a global level for the business to

operates its function (AICPA, 2017). International Financial Reporting system are being

designed to set a common global language for the business affairs which helps in simplifies the

other companies operations in order to understand and compare. IFRS provides a framework set

of rules to the accountant which helps them to maintain and record the financial information and

transaction in a way that can be comparable, understandable, reliable and relevant. As per the

IFRS, apart from the basic financial report. a company must have to give the summary of its

accounting principles.

IFRS are the single set of accounting that has been adopted in 110 countries as the

regulatory framework in preparing the financial statements of the country. The importance of

IRS has been increased as it helps in providing comparability of the financial information for

investors in order to invest in companies across borders (Importance of Financial Knowledge to

Business Success ,2018). With the adaptation of the IFRS, companies has achieved the lower

cost of capital and and more efficient in allocation of capital. The benefit of IFRS are as follows:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.