Financial Reporting Analysis: Standards, Stakeholders, and Compliance

VerifiedAdded on 2020/10/04

|17

|4116

|358

Report

AI Summary

This report provides a detailed analysis of financial reporting, encompassing its context, purpose, and the conceptual and regulatory frameworks that govern it. It explores the qualitative characteristics essential for reliable financial information and identifies the main stakeholders of an organization, highlighting the benefits of providing them with financial data. The report delves into the value of financial reporting in meeting organizational objectives and fostering growth, while also examining the key financial statements as per IAS 1. It includes a comparison between IFRS and IAS, discusses the advantages of international financial reporting standards, and considers the varying degrees of compliance with IFRS by organizations, including factors influencing compliance within nations. The content also includes the financial statements of Marks and Spencer to determine the various ratios.

INTERNATIONAL

FINANCIAL REPORTING

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Context and Purpose of Financial reporting ..........................................................................1

2. The conceptual and regulatory framework of an organisation and qualitative characteristics

of financial reporting...................................................................................................................2

3. The main staekholders of an organisation and benfits of providing them fiancial

information..................................................................................................................................3

4. The value of financial reporting for meeting organisational obejtives and growth ...............5

5. Main fiancial statemenst as per IAS 1.....................................................................................5

6. Financial statements of Marks and Spencer ..........................................................................8

7. Difference between IFRS and IAS ......................................................................................10

8. The benefits of international financial reporting standards..................................................10

9. The varying degree of compliance with IFRS by organisations and factors in a nation that

may impact compliance.............................................................................................................11

CONCLUSION .............................................................................................................................12

.......................................................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................15

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Context and Purpose of Financial reporting ..........................................................................1

2. The conceptual and regulatory framework of an organisation and qualitative characteristics

of financial reporting...................................................................................................................2

3. The main staekholders of an organisation and benfits of providing them fiancial

information..................................................................................................................................3

4. The value of financial reporting for meeting organisational obejtives and growth ...............5

5. Main fiancial statemenst as per IAS 1.....................................................................................5

6. Financial statements of Marks and Spencer ..........................................................................8

7. Difference between IFRS and IAS ......................................................................................10

8. The benefits of international financial reporting standards..................................................10

9. The varying degree of compliance with IFRS by organisations and factors in a nation that

may impact compliance.............................................................................................................11

CONCLUSION .............................................................................................................................12

.......................................................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................15

INTRODUCTION

Financial reporting is a method to present the financial information in the reporting

format. Financial reporting helps the firm in identifying the various operations performed b y the

organisation. This information helps in improving the future performance and profitability of the

firm. Financial reporting include profit and loss statements, balance sheet , statements of equity

and cash flow statements. This study will include the context and purpose of financial reporting.

Furthermore , it will include the conceptual and regulatory framework and the qualitative

characteristics required to make the financial information reliable. Moreover, it will include the

main stakeholders of the organisation and the benefit of providing them financial information.

This assignment will provide understanding of the financial statements to determine the various

ratios of marks and Spencer. This assignment will include difference between international

accounting standards and International financial reporting standard. Also, it will provide

understanding of the factors that impact on compliance with IFRS.

MAIN BODY

1. Context and Purpose of Financial reporting

The main purpose of financial reporting is to provide useful and reliable information to

the management of the organisation in order to assist them in making effective decision for the

organisation. Financial reporting is used by organisation and various stakeholders to determiner

the performance and profitability of the firm inn order to compare the performance with its

competitors and identify the trends of performance of the firm (Alexander, Britton and Jorissen,

2014). Also , it helps the firm in determining the cash requirement of the organisation which

helps them in performing the future activities of the organisation. With the helps of financial

reporting the obligation of the company which they have to pay can be determined.

The purpose of preparing financial reporting is to serve the information to the

management and various stakeholders to provide them information about the various activities of

the company (Chen and Li, 2015). It assists management in identifying the deviations due to

which the goals of the organisation are not achieved which helps them in formulating various

strategies and planning to improve the performance. The information contained in the financial

reporting provide understanding about the liquidity position of the firm and also about the

profitability of the firm and factors which impact on the profitability of the organisation. It helps

the firm in reducing its expenses and increasing the sources of incomes.

1

Financial reporting is a method to present the financial information in the reporting

format. Financial reporting helps the firm in identifying the various operations performed b y the

organisation. This information helps in improving the future performance and profitability of the

firm. Financial reporting include profit and loss statements, balance sheet , statements of equity

and cash flow statements. This study will include the context and purpose of financial reporting.

Furthermore , it will include the conceptual and regulatory framework and the qualitative

characteristics required to make the financial information reliable. Moreover, it will include the

main stakeholders of the organisation and the benefit of providing them financial information.

This assignment will provide understanding of the financial statements to determine the various

ratios of marks and Spencer. This assignment will include difference between international

accounting standards and International financial reporting standard. Also, it will provide

understanding of the factors that impact on compliance with IFRS.

MAIN BODY

1. Context and Purpose of Financial reporting

The main purpose of financial reporting is to provide useful and reliable information to

the management of the organisation in order to assist them in making effective decision for the

organisation. Financial reporting is used by organisation and various stakeholders to determiner

the performance and profitability of the firm inn order to compare the performance with its

competitors and identify the trends of performance of the firm (Alexander, Britton and Jorissen,

2014). Also , it helps the firm in determining the cash requirement of the organisation which

helps them in performing the future activities of the organisation. With the helps of financial

reporting the obligation of the company which they have to pay can be determined.

The purpose of preparing financial reporting is to serve the information to the

management and various stakeholders to provide them information about the various activities of

the company (Chen and Li, 2015). It assists management in identifying the deviations due to

which the goals of the organisation are not achieved which helps them in formulating various

strategies and planning to improve the performance. The information contained in the financial

reporting provide understanding about the liquidity position of the firm and also about the

profitability of the firm and factors which impact on the profitability of the organisation. It helps

the firm in reducing its expenses and increasing the sources of incomes.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial information is very useful for the firm in order to determine its growth and

achieve the business objectives. On the basis of financial reporting firm is able to prepare

budgets for future which helps in achieving the performance objective of organisation. Financial

information provide information to investors and lenders about the performance and profitability

of the organisation which helps them in making decision about investing their money in the firm

(Christiaens and et.al., 2015). This reports consist of profit and loss statements, balance sheet ,

and cash flow statements. Profit and loss statements contains the information regarding the

incomes and expenses of the firm. Balance sheet provide information about the assets and

liabilities of organisation. Cash flow contains the information of the cash inflows and outflows

for the period.

2. The conceptual and regulatory framework of an organisation and qualitative characteristics of

financial reporting

The conceptual framework of financial reporting provide the objectives of general

purpose of financial reporting. The conceptual framework helps in formulating accounting

policies when there are no IFRS standards applicable to the particular transaction. It also

provides qualitative characteristics which is required to presenting reliable information.

Conceptual framework of financial reporting include the definition of assets , liabilities, incomes

and expenses (Hadi, Suryanto and Hussain, 2016). Furthermore, it provides measurement bases

and guidance to use them. It also provides concepts band guidance for presentation and

disclosure of financial information. The conceptual framework provide fundamental concepts

which helps the board in developing the IFRS standards.

The regulatory framework which is used to govern the financial reporting includes IFRS

and IAS. IFRS ans IAS are the standards set by the board to present the financial information in

the reporting format. International financial reporting standards are the standards set by the

board which provide rules and regulation on the basis of which financial statements are prepared

by the organisation. International accounting standards are the old standards which were replaced

by international financial reporting standards (Kaya and Koch, 2015). Principles of IFRS

includes various standards such as IFRS 4 provided principles for shadow accounting, IFRS 3

provide principles for business conmninations. IFRS 2 provide principles for shar based

compensation and IAS 2 is related to treasury shares.

The qualitative characterstics of fiancial reporting

2

achieve the business objectives. On the basis of financial reporting firm is able to prepare

budgets for future which helps in achieving the performance objective of organisation. Financial

information provide information to investors and lenders about the performance and profitability

of the organisation which helps them in making decision about investing their money in the firm

(Christiaens and et.al., 2015). This reports consist of profit and loss statements, balance sheet ,

and cash flow statements. Profit and loss statements contains the information regarding the

incomes and expenses of the firm. Balance sheet provide information about the assets and

liabilities of organisation. Cash flow contains the information of the cash inflows and outflows

for the period.

2. The conceptual and regulatory framework of an organisation and qualitative characteristics of

financial reporting

The conceptual framework of financial reporting provide the objectives of general

purpose of financial reporting. The conceptual framework helps in formulating accounting

policies when there are no IFRS standards applicable to the particular transaction. It also

provides qualitative characteristics which is required to presenting reliable information.

Conceptual framework of financial reporting include the definition of assets , liabilities, incomes

and expenses (Hadi, Suryanto and Hussain, 2016). Furthermore, it provides measurement bases

and guidance to use them. It also provides concepts band guidance for presentation and

disclosure of financial information. The conceptual framework provide fundamental concepts

which helps the board in developing the IFRS standards.

The regulatory framework which is used to govern the financial reporting includes IFRS

and IAS. IFRS ans IAS are the standards set by the board to present the financial information in

the reporting format. International financial reporting standards are the standards set by the

board which provide rules and regulation on the basis of which financial statements are prepared

by the organisation. International accounting standards are the old standards which were replaced

by international financial reporting standards (Kaya and Koch, 2015). Principles of IFRS

includes various standards such as IFRS 4 provided principles for shadow accounting, IFRS 3

provide principles for business conmninations. IFRS 2 provide principles for shar based

compensation and IAS 2 is related to treasury shares.

The qualitative characterstics of fiancial reporting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Understandability : The ifnormation presented in the fiancial reporting must be claery

presen5ted inh order to provide understandability to the users of the fiancial

refornmation. The organisation must present the information clearly with the footnots ton

giove clear understanding of the various operations performed by the organisation.

Relevance : The information presented in the statements must be relevant. So that it is

useful for the users while making decisions. Thuisb include providing relevant

information that omission and misstatemnts will impact the economic deicison of the

users.

Reliability : accoridng to this characterstics the informatiopn persented in the fiancial

reporting must be reliable and must be free from material errors.n the informaqtion

propvided in the statemnts must is accurate, so that the users can rely upon that

information (Klychova And et.al., 2015). The organisation must present the faithful

trancation with misleading any transaction.

Comparability : The fiancial information must have the compararble charactertsics

which helps the organisatioon in comapring the fiancial information with the past eyar

statements to identify the perofrmabnce trend and growth of the organisation which helps

the firm in making future decisions effectively (Financial Reporting, 2017).

3. The main staekholders of an organisation and benfits of providing them fiancial information

The stakeholders of the organisation are classifies into internal and external stakeholders.

Internal stakeholders : It consist of people that arewithin the rganisation which use thye

fiancila information. The internal stakeholders consist of owners, managenmnts and employees.

Owners : They use the fioancial informationn inn lorder to identiofy the performance of

company and also helsp in determiningb the risk which there company can face (Nobes, 2014).

Itb helps the opwners inj formulating various policies nad strtategies ton reduce the risk.

Management : the managers of the organisation use the fiancial information in order to

idnetify the performance and profitability ogf the organisatuon lon the basis of which various

decisions are made by the managers whioch helps the organisation in imprioving the

performance of the firm. Managers of thje organisation by usingb the fiancial data of perverious

yeard can identrfy the future profitability and performance of the firm.

Employees : they are provided wioth the fiancial; information which helps them in

determining the fusture profitability and performanc eof the organisatiion in order to determine

3

presen5ted inh order to provide understandability to the users of the fiancial

refornmation. The organisation must present the information clearly with the footnots ton

giove clear understanding of the various operations performed by the organisation.

Relevance : The information presented in the statements must be relevant. So that it is

useful for the users while making decisions. Thuisb include providing relevant

information that omission and misstatemnts will impact the economic deicison of the

users.

Reliability : accoridng to this characterstics the informatiopn persented in the fiancial

reporting must be reliable and must be free from material errors.n the informaqtion

propvided in the statemnts must is accurate, so that the users can rely upon that

information (Klychova And et.al., 2015). The organisation must present the faithful

trancation with misleading any transaction.

Comparability : The fiancial information must have the compararble charactertsics

which helps the organisatioon in comapring the fiancial information with the past eyar

statements to identify the perofrmabnce trend and growth of the organisation which helps

the firm in making future decisions effectively (Financial Reporting, 2017).

3. The main staekholders of an organisation and benfits of providing them fiancial information

The stakeholders of the organisation are classifies into internal and external stakeholders.

Internal stakeholders : It consist of people that arewithin the rganisation which use thye

fiancila information. The internal stakeholders consist of owners, managenmnts and employees.

Owners : They use the fioancial informationn inn lorder to identiofy the performance of

company and also helsp in determiningb the risk which there company can face (Nobes, 2014).

Itb helps the opwners inj formulating various policies nad strtategies ton reduce the risk.

Management : the managers of the organisation use the fiancial information in order to

idnetify the performance and profitability ogf the organisatuon lon the basis of which various

decisions are made by the managers whioch helps the organisation in imprioving the

performance of the firm. Managers of thje organisation by usingb the fiancial data of perverious

yeard can identrfy the future profitability and performance of the firm.

Employees : they are provided wioth the fiancial; information which helps them in

determining the fusture profitability and performanc eof the organisatiion in order to determine

3

their future job prospects and also helps them in comparing the financial perofrmance of the

orgtabnisation with that of other organisation in the industry.

External stakeholders : There are people which are outside the organisation and are

provided with the financial infornmation to help them in making various decisions (Perera and

Chand, 2015). External stakeholders of the organisation consist of suppliers , investors,

customers , governmntes etc.

Investors : the fiancial information is provided to the ivenstors inj order to helps inn

making decisions about investing their monmey in the organisation by indefying the performance

and profitability of the firm with comparision to other organisations. It also helps them in

determinjing the return whchb will be provuided by thye organisation on the amount invested by

them in the firm.

Suppliers and lenders : they are provided with the financial informatiion in order to

provide understanding of the liquidity position of the firm in order to pay the firm 's obligation s

ton the lenders and suppliers. Lenders of the organistion lent money to the firm for performing

their day to day activities. Lenders wioth the helps of financial information can identiofy the

asbility of the firm ton pay its obligations.

Customers : they are provided with the fiancila informatiopn in order to priovide them

understanding about the poerformance and profitability of the firm to retain thyem in business to

provide them various products and services of the organisation.

Government : They use the financial information to identify the tax obligationj of the

firm. Fiancial information also helps the governmnmebnt in determining the performanxce of

the firm in theb economy and its contribution in thyue growthy of economy.

Benfits to stakeholders by providing financial information

financial information helps the firm in identifying the performance and profitbailityb of

the orgfanisation.

Financial information helps the management in majking effective decisions for the firm .

It helsp the lenders and suppliers of the organisation in determining the ability of the firm

to pay its obligations.

Financial information helps the governmnet in idnetifying the tax obligation of the

organisation in order to pay the tax liability properly.

It helps the employees in identifying the future job prosepects for their benefit.

4

orgtabnisation with that of other organisation in the industry.

External stakeholders : There are people which are outside the organisation and are

provided with the financial infornmation to help them in making various decisions (Perera and

Chand, 2015). External stakeholders of the organisation consist of suppliers , investors,

customers , governmntes etc.

Investors : the fiancial information is provided to the ivenstors inj order to helps inn

making decisions about investing their monmey in the organisation by indefying the performance

and profitability of the firm with comparision to other organisations. It also helps them in

determinjing the return whchb will be provuided by thye organisation on the amount invested by

them in the firm.

Suppliers and lenders : they are provided with the financial informatiion in order to

provide understanding of the liquidity position of the firm in order to pay the firm 's obligation s

ton the lenders and suppliers. Lenders of the organistion lent money to the firm for performing

their day to day activities. Lenders wioth the helps of financial information can identiofy the

asbility of the firm ton pay its obligations.

Customers : they are provided with the fiancila informatiopn in order to priovide them

understanding about the poerformance and profitability of the firm to retain thyem in business to

provide them various products and services of the organisation.

Government : They use the financial information to identify the tax obligationj of the

firm. Fiancial information also helps the governmnmebnt in determining the performanxce of

the firm in theb economy and its contribution in thyue growthy of economy.

Benfits to stakeholders by providing financial information

financial information helps the firm in identifying the performance and profitbailityb of

the orgfanisation.

Financial information helps the management in majking effective decisions for the firm .

It helsp the lenders and suppliers of the organisation in determining the ability of the firm

to pay its obligations.

Financial information helps the governmnet in idnetifying the tax obligation of the

organisation in order to pay the tax liability properly.

It helps the employees in identifying the future job prosepects for their benefit.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the owners of the organisation in formulating starategies and policies for future

imporve ment of the performance and profitability of the organisation.

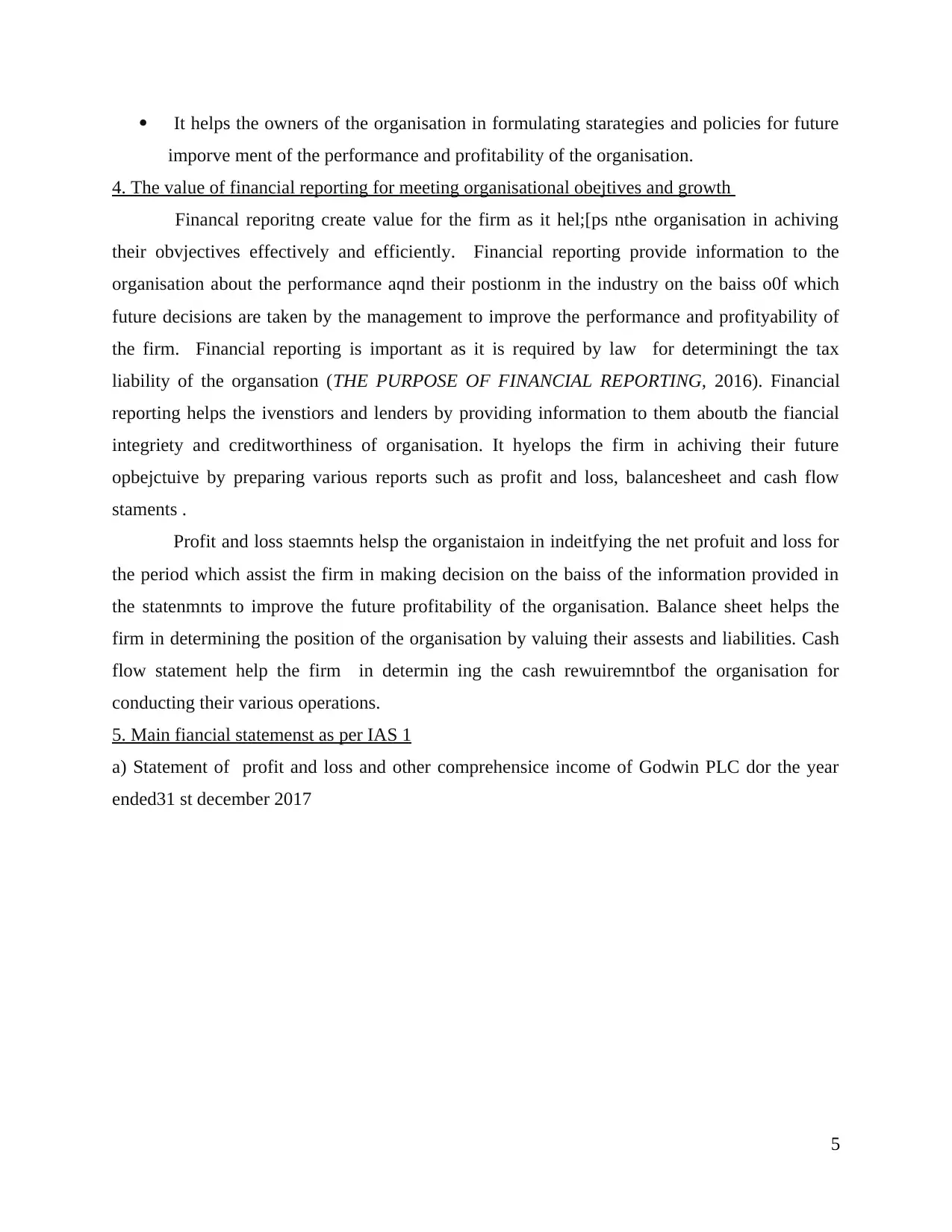

4. The value of financial reporting for meeting organisational obejtives and growth

Financal reporitng create value for the firm as it hel;[ps nthe organisation in achiving

their obvjectives effectively and efficiently. Financial reporting provide information to the

organisation about the performance aqnd their postionm in the industry on the baiss o0f which

future decisions are taken by the management to improve the performance and profityability of

the firm. Financial reporting is important as it is required by law for determiningt the tax

liability of the organsation (THE PURPOSE OF FINANCIAL REPORTING, 2016). Financial

reporting helps the ivenstiors and lenders by providing information to them aboutb the fiancial

integriety and creditworthiness of organisation. It hyelops the firm in achiving their future

opbejctuive by preparing various reports such as profit and loss, balancesheet and cash flow

staments .

Profit and loss staemnts helsp the organistaion in indeitfying the net profuit and loss for

the period which assist the firm in making decision on the baiss of the information provided in

the statenmnts to improve the future profitability of the organisation. Balance sheet helps the

firm in determining the position of the organisation by valuing their assests and liabilities. Cash

flow statement help the firm in determin ing the cash rewuiremntbof the organisation for

conducting their various operations.

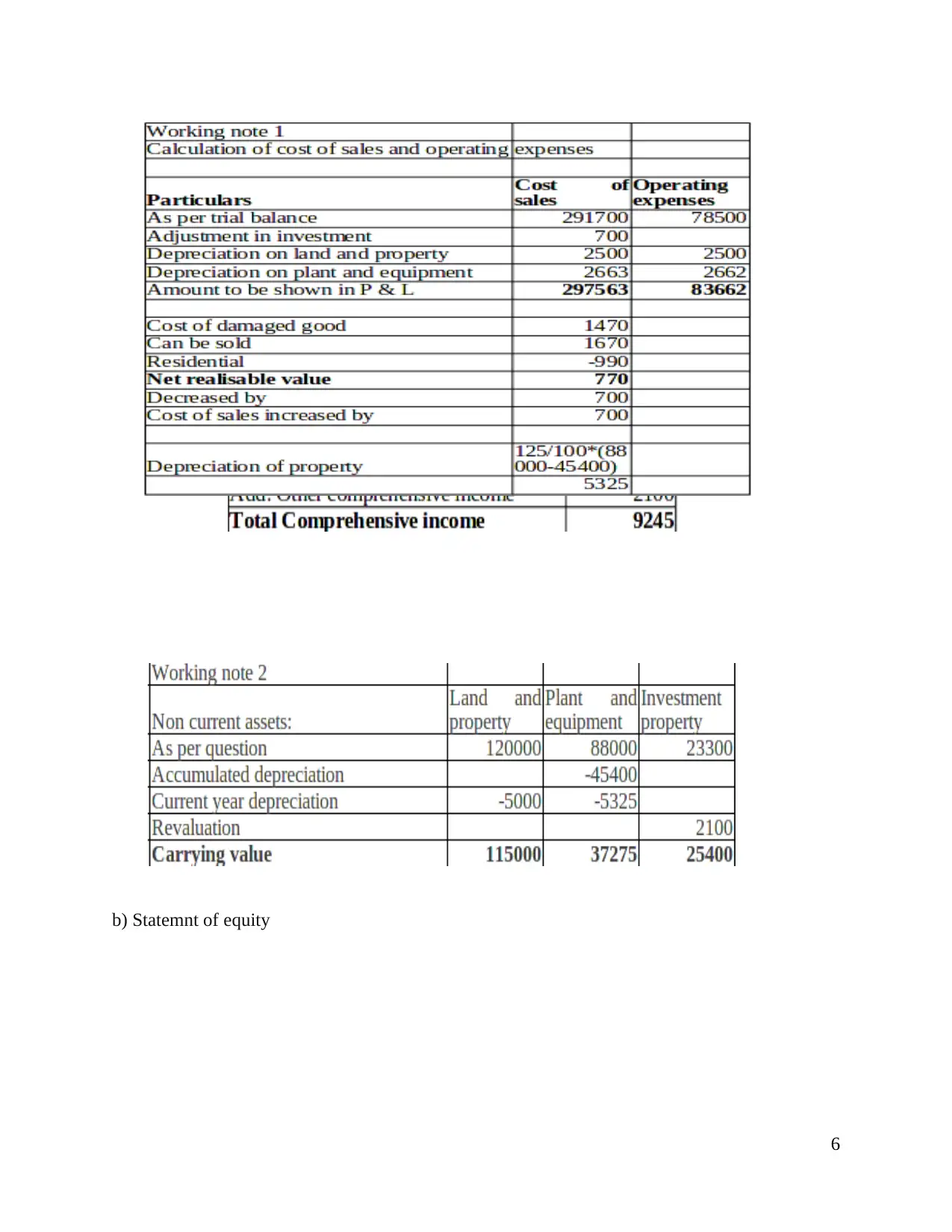

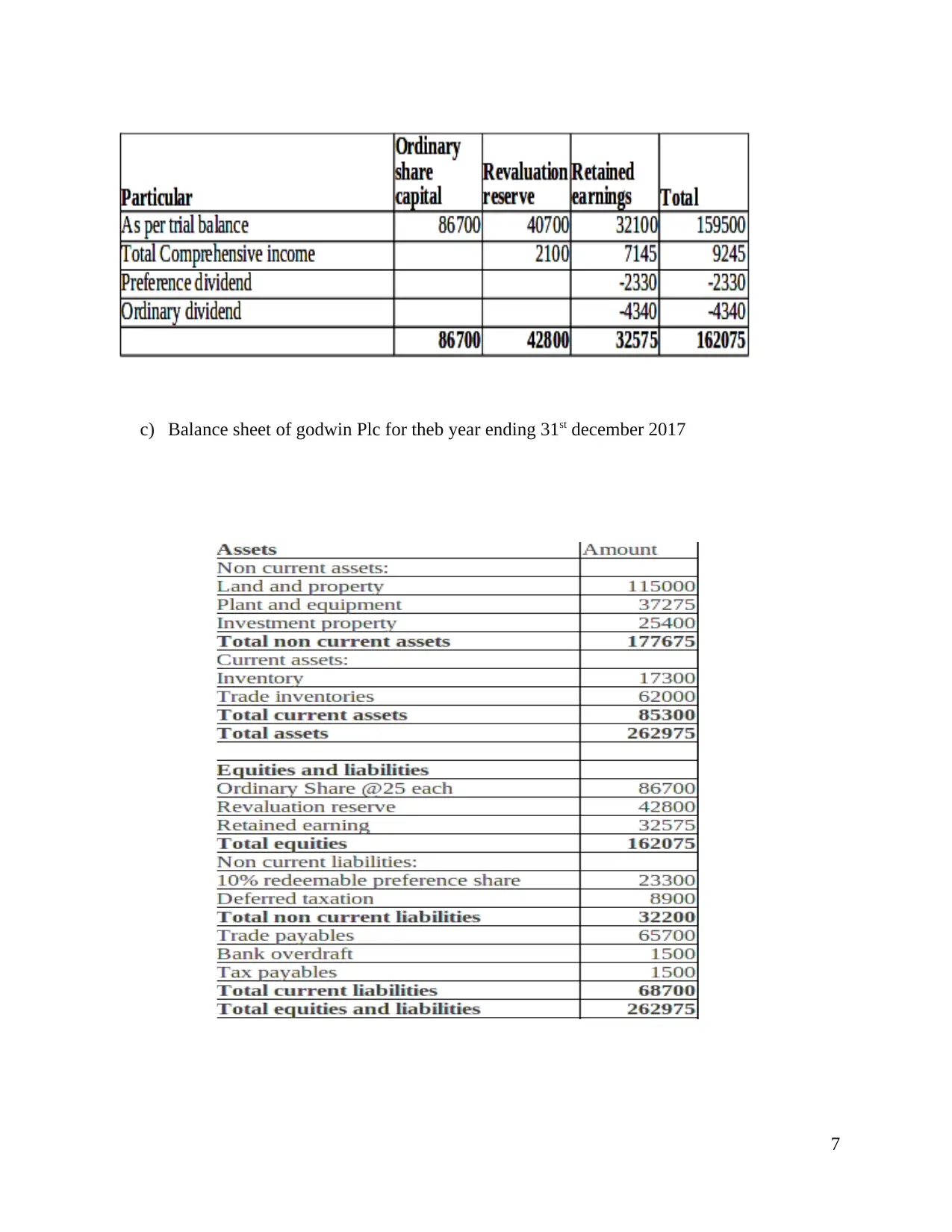

5. Main fiancial statemenst as per IAS 1

a) Statement of profit and loss and other comprehensice income of Godwin PLC dor the year

ended31 st december 2017

5

imporve ment of the performance and profitability of the organisation.

4. The value of financial reporting for meeting organisational obejtives and growth

Financal reporitng create value for the firm as it hel;[ps nthe organisation in achiving

their obvjectives effectively and efficiently. Financial reporting provide information to the

organisation about the performance aqnd their postionm in the industry on the baiss o0f which

future decisions are taken by the management to improve the performance and profityability of

the firm. Financial reporting is important as it is required by law for determiningt the tax

liability of the organsation (THE PURPOSE OF FINANCIAL REPORTING, 2016). Financial

reporting helps the ivenstiors and lenders by providing information to them aboutb the fiancial

integriety and creditworthiness of organisation. It hyelops the firm in achiving their future

opbejctuive by preparing various reports such as profit and loss, balancesheet and cash flow

staments .

Profit and loss staemnts helsp the organistaion in indeitfying the net profuit and loss for

the period which assist the firm in making decision on the baiss of the information provided in

the statenmnts to improve the future profitability of the organisation. Balance sheet helps the

firm in determining the position of the organisation by valuing their assests and liabilities. Cash

flow statement help the firm in determin ing the cash rewuiremntbof the organisation for

conducting their various operations.

5. Main fiancial statemenst as per IAS 1

a) Statement of profit and loss and other comprehensice income of Godwin PLC dor the year

ended31 st december 2017

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Statemnt of equity

6

6

c) Balance sheet of godwin Plc for theb year ending 31st december 2017

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

d) The cash flow statement provide information about the cash inflow and outflow for the period

on the basis of which firm is able to determine the cash requieremnt ofn the oprganisation.l cash

flow staemnts is prepared using the three activities that include4s operating activity , investing

activyt and financial activity. Operating activity incvlude the cash inflow and outflow relating

the operating activties of the firm such as payment made to suppliers of goods and services and

anyb other operatring expenses. Financial activity includes repurchase of debenture loan, issue of

ordianry capital etc. Investing activity includes payments to acquire intabngible fixed assets,

recepits from the sales of fixed assets etc.

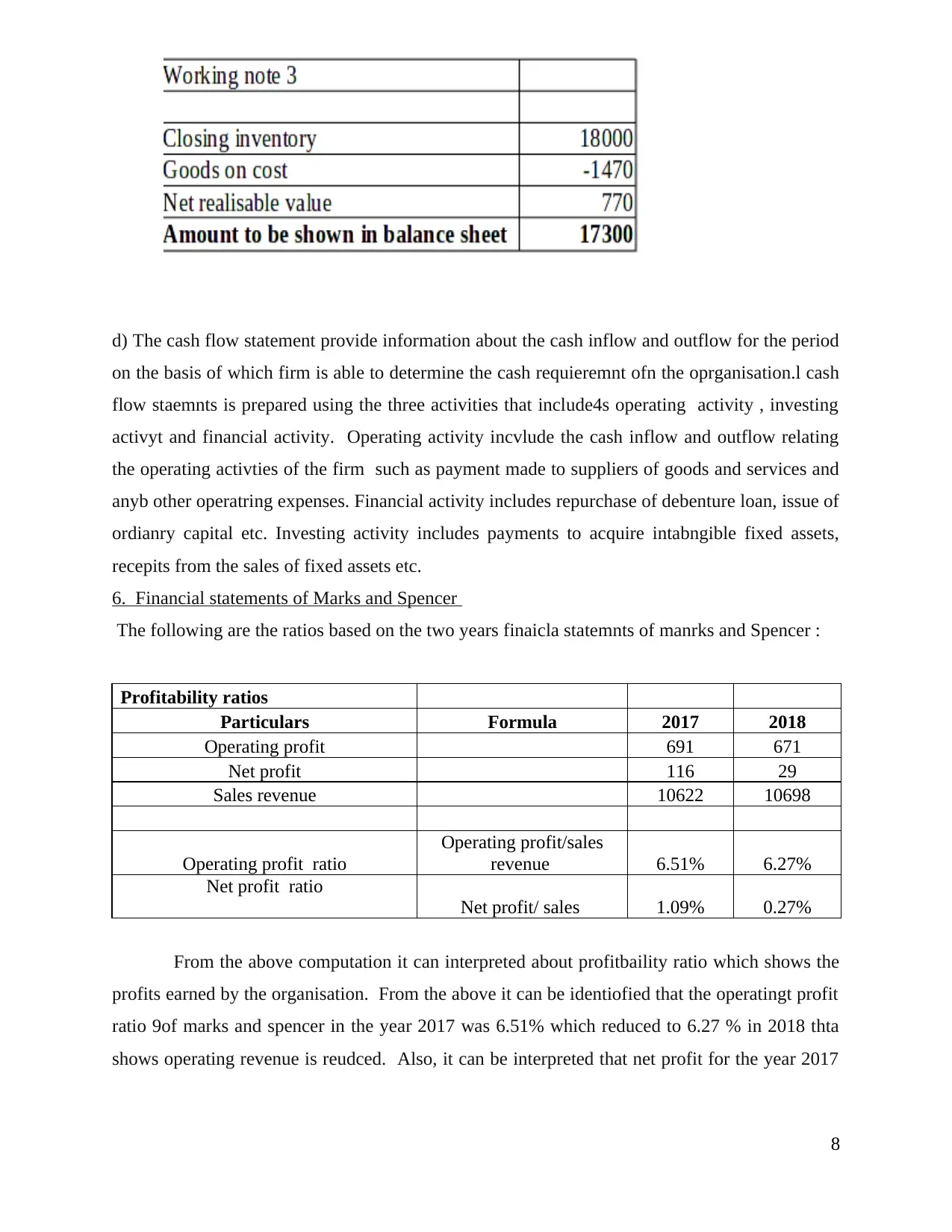

6. Financial statements of Marks and Spencer

The following are the ratios based on the two years finaicla statemnts of manrks and Spencer :

Profitability ratios

Particulars Formula 2017 2018

Operating profit 691 671

Net profit 116 29

Sales revenue 10622 10698

Operating profit ratio

Operating profit/sales

revenue 6.51% 6.27%

Net profit ratio

Net profit/ sales 1.09% 0.27%

From the above computation it can interpreted about profitbaility ratio which shows the

profits earned by the organisation. From the above it can be identiofied that the operatingt profit

ratio 9of marks and spencer in the year 2017 was 6.51% which reduced to 6.27 % in 2018 thta

shows operating revenue is reudced. Also, it can be interpreted that net profit for the year 2017

8

on the basis of which firm is able to determine the cash requieremnt ofn the oprganisation.l cash

flow staemnts is prepared using the three activities that include4s operating activity , investing

activyt and financial activity. Operating activity incvlude the cash inflow and outflow relating

the operating activties of the firm such as payment made to suppliers of goods and services and

anyb other operatring expenses. Financial activity includes repurchase of debenture loan, issue of

ordianry capital etc. Investing activity includes payments to acquire intabngible fixed assets,

recepits from the sales of fixed assets etc.

6. Financial statements of Marks and Spencer

The following are the ratios based on the two years finaicla statemnts of manrks and Spencer :

Profitability ratios

Particulars Formula 2017 2018

Operating profit 691 671

Net profit 116 29

Sales revenue 10622 10698

Operating profit ratio

Operating profit/sales

revenue 6.51% 6.27%

Net profit ratio

Net profit/ sales 1.09% 0.27%

From the above computation it can interpreted about profitbaility ratio which shows the

profits earned by the organisation. From the above it can be identiofied that the operatingt profit

ratio 9of marks and spencer in the year 2017 was 6.51% which reduced to 6.27 % in 2018 thta

shows operating revenue is reudced. Also, it can be interpreted that net profit for the year 2017

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

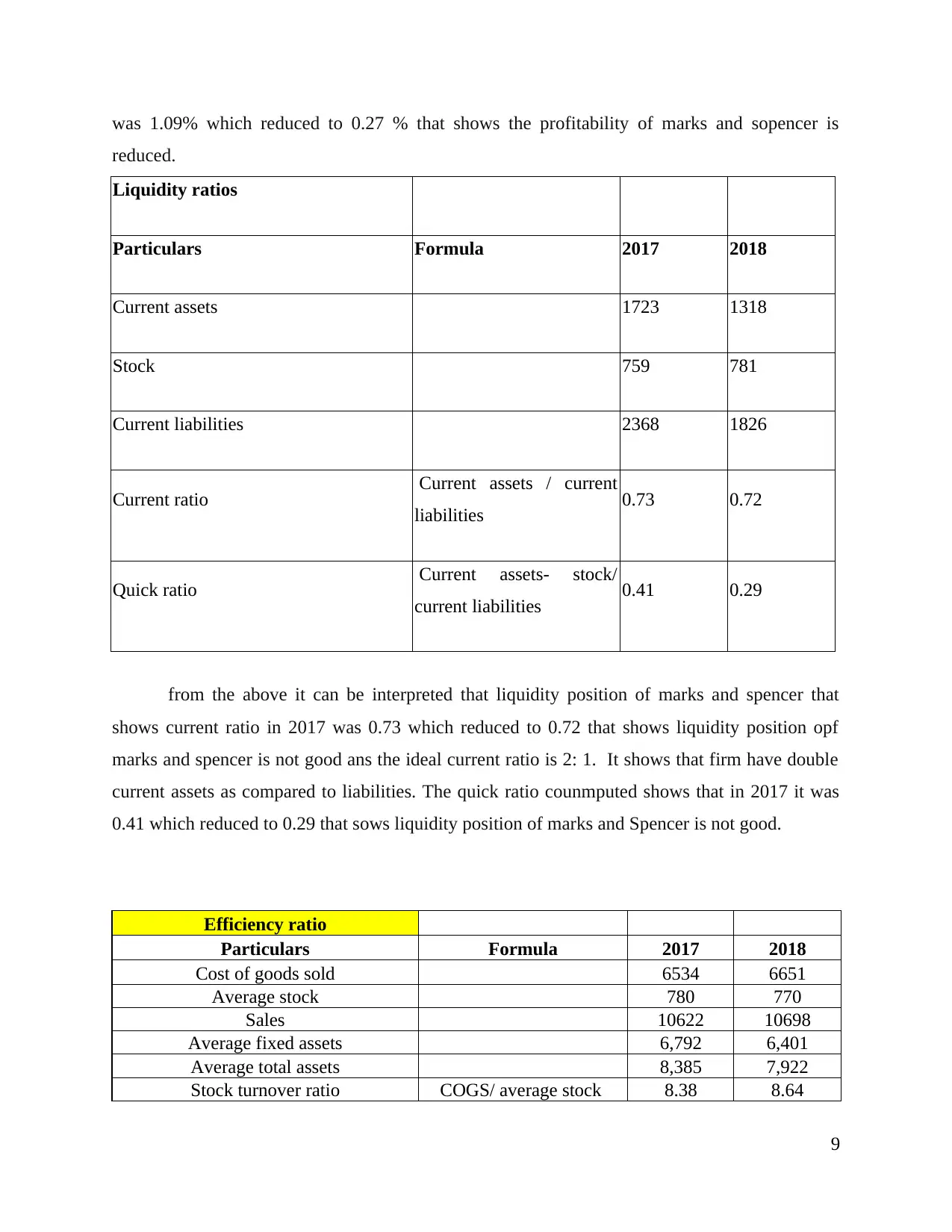

was 1.09% which reduced to 0.27 % that shows the profitability of marks and sopencer is

reduced.

Liquidity ratios

Particulars Formula 2017 2018

Current assets 1723 1318

Stock 759 781

Current liabilities 2368 1826

Current ratio Current assets / current

liabilities 0.73 0.72

Quick ratio Current assets- stock/

current liabilities 0.41 0.29

from the above it can be interpreted that liquidity position of marks and spencer that

shows current ratio in 2017 was 0.73 which reduced to 0.72 that shows liquidity position opf

marks and spencer is not good ans the ideal current ratio is 2: 1. It shows that firm have double

current assets as compared to liabilities. The quick ratio counmputed shows that in 2017 it was

0.41 which reduced to 0.29 that sows liquidity position of marks and Spencer is not good.

Efficiency ratio

Particulars Formula 2017 2018

Cost of goods sold 6534 6651

Average stock 780 770

Sales 10622 10698

Average fixed assets 6,792 6,401

Average total assets 8,385 7,922

Stock turnover ratio COGS/ average stock 8.38 8.64

9

reduced.

Liquidity ratios

Particulars Formula 2017 2018

Current assets 1723 1318

Stock 759 781

Current liabilities 2368 1826

Current ratio Current assets / current

liabilities 0.73 0.72

Quick ratio Current assets- stock/

current liabilities 0.41 0.29

from the above it can be interpreted that liquidity position of marks and spencer that

shows current ratio in 2017 was 0.73 which reduced to 0.72 that shows liquidity position opf

marks and spencer is not good ans the ideal current ratio is 2: 1. It shows that firm have double

current assets as compared to liabilities. The quick ratio counmputed shows that in 2017 it was

0.41 which reduced to 0.29 that sows liquidity position of marks and Spencer is not good.

Efficiency ratio

Particulars Formula 2017 2018

Cost of goods sold 6534 6651

Average stock 780 770

Sales 10622 10698

Average fixed assets 6,792 6,401

Average total assets 8,385 7,922

Stock turnover ratio COGS/ average stock 8.38 8.64

9

Fixed assets turnover ratio Sales/ fixed assets 1.56 1.67

Total assets turnover ratio Sales / total assets 1.27 1.35

From the above it can be interpreted about efficiency ratio that shows the ability of

firnms assets to genreate more revenue. It can be interprerted that in 2017 fixed assets turnover

ration was 1.56 which increses to 1.67 that shows fixed assets are utilised properly. Total assets

turnover ratio is incresed to 1.35 from 1.27 that shows marks and Spencer isn utilising the assets

propely to generate revenue.

Investment ratios

Particulars 2017 2018

EPS 0.14 0.03

DPS 0.35 0.38

From the above computation it can be interpreted that earning per share is reduced to

0.03 for marks and Spencer that shows earning of marks and Spencer is reduced on the share

issued. Also , it shows that Dividend per share is increased to 0.38 from 0.35 for marks and

Spencer that shows company is paying higher dividend in 2018 as compared to 2017.

7. Difference between IFRS and IAS

IFRS stands for in ternational fiancial reporting standards and IAS stans for

International accounting standards . IAS are the standards which were developed by IAS

committe and there standards were published between 1973 and 2001. whereas international

financial reporting standards were published fromm 2001 onwards (Haslam and et.al., 2016).

International fiancial reporting standards are issued by Ingtwernational accounting standards

board. IFRS is the current set of standards which is used by organisation for reportingt the

financial information (IAS vs IFRS ,2018). International accountinmgb standards were used befor

the IFRS standards were nopt published. International accounting standards was a set of

standards used for relecting a particular transaction. IFRS is the current and Updated version of

International accounting standards. It provide information for disclosure of fiancial information

in the financial statement. Also , if there is any contradiction between IOFRS and IAS then the

tyranscation is treaterd as per IFRS and IAS is ignored.

10

Total assets turnover ratio Sales / total assets 1.27 1.35

From the above it can be interpreted about efficiency ratio that shows the ability of

firnms assets to genreate more revenue. It can be interprerted that in 2017 fixed assets turnover

ration was 1.56 which increses to 1.67 that shows fixed assets are utilised properly. Total assets

turnover ratio is incresed to 1.35 from 1.27 that shows marks and Spencer isn utilising the assets

propely to generate revenue.

Investment ratios

Particulars 2017 2018

EPS 0.14 0.03

DPS 0.35 0.38

From the above computation it can be interpreted that earning per share is reduced to

0.03 for marks and Spencer that shows earning of marks and Spencer is reduced on the share

issued. Also , it shows that Dividend per share is increased to 0.38 from 0.35 for marks and

Spencer that shows company is paying higher dividend in 2018 as compared to 2017.

7. Difference between IFRS and IAS

IFRS stands for in ternational fiancial reporting standards and IAS stans for

International accounting standards . IAS are the standards which were developed by IAS

committe and there standards were published between 1973 and 2001. whereas international

financial reporting standards were published fromm 2001 onwards (Haslam and et.al., 2016).

International fiancial reporting standards are issued by Ingtwernational accounting standards

board. IFRS is the current set of standards which is used by organisation for reportingt the

financial information (IAS vs IFRS ,2018). International accountinmgb standards were used befor

the IFRS standards were nopt published. International accounting standards was a set of

standards used for relecting a particular transaction. IFRS is the current and Updated version of

International accounting standards. It provide information for disclosure of fiancial information

in the financial statement. Also , if there is any contradiction between IOFRS and IAS then the

tyranscation is treaterd as per IFRS and IAS is ignored.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.