Analysis of International Financial Reporting Standards and Framework

VerifiedAdded on 2022/12/28

|16

|3969

|86

Report

AI Summary

This report provides a detailed analysis of the International Financial Reporting Standards (IFRS) and the IASB's conceptual framework. It begins with an introduction to international financial reporting and its role in ethical financial statement presentation. Part A delves into the IASB's conceptual framework, explaining its purpose, assumptions, qualitative characteristics, and the concept of materiality. It also examines IFRS 1, outlining its objectives and essential requirements. Part 2 focuses on lease accounting under IFRS 16 and the calculation of interest rates in lease agreements. The report concludes with a demonstration of cash flow statements using both the direct and indirect methods, providing a comprehensive overview of key financial reporting concepts and their practical application. The report covers financial concept, physical concept of capital maintenance and how leases should be accounted in financial statement for lessee.

International Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

QUESTION 1 IASB’s Conceptual Framework ..............................................................................3

a) Brief description regarding main purpose of IASB's conceptual framework document........3

b) Brief explanation regarding assumptions use for preparation of financial statements...........4

Explanation regarding concept of capital maintenance under IASB's framework.....................5

IASB's framework is based on two assumption which is related with financial as well as

physical concept of capital, both are defined below:..................................................................5

d) Brief description regarding 5 qualitative characteristics & attributes of financial statement

use in IASB's conceptual framework. ........................................................................................5

e) Concept of materiality in financial reporting..........................................................................6

QUESTION 2 : IFRS1 ....................................................................................................................6

a) Brief description regarding mention within IFRS 1................................................................6

b) Essential requirement of IFRS 1 which required by Prisca Plc used for preparing financial

statement.....................................................................................................................................7

PART 2............................................................................................................................................8

QUESTION 4...................................................................................................................................8

Brief description regarding how leases should be accounted in financial statement for lessee..8

b) Calculation of interest rate inherent in lease agreement.........................................................9

QUESTION 6...................................................................................................................................9

Cash flow statement of Cross Dale Limited as per indirect method.........................................9

Cash flow statement of Cross Dale Limited as per direct method. ........................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

QUESTION 1 IASB’s Conceptual Framework ..............................................................................3

a) Brief description regarding main purpose of IASB's conceptual framework document........3

b) Brief explanation regarding assumptions use for preparation of financial statements...........4

Explanation regarding concept of capital maintenance under IASB's framework.....................5

IASB's framework is based on two assumption which is related with financial as well as

physical concept of capital, both are defined below:..................................................................5

d) Brief description regarding 5 qualitative characteristics & attributes of financial statement

use in IASB's conceptual framework. ........................................................................................5

e) Concept of materiality in financial reporting..........................................................................6

QUESTION 2 : IFRS1 ....................................................................................................................6

a) Brief description regarding mention within IFRS 1................................................................6

b) Essential requirement of IFRS 1 which required by Prisca Plc used for preparing financial

statement.....................................................................................................................................7

PART 2............................................................................................................................................8

QUESTION 4...................................................................................................................................8

Brief description regarding how leases should be accounted in financial statement for lessee..8

b) Calculation of interest rate inherent in lease agreement.........................................................9

QUESTION 6...................................................................................................................................9

Cash flow statement of Cross Dale Limited as per indirect method.........................................9

Cash flow statement of Cross Dale Limited as per direct method. ........................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

International financial reporting is a framework which define various standard in order to

formulate and represent financial statement in ethical manner. This retort has been formulated to

define the relevance of IASB's conceptual framework by showing purpose, importance of this

standard. It is useful for maintain consistency and transparency during the time of compound of

financial statement. In other part use of IFRS for calculating of lease as well as formulation of

statement of cash flow by applying IAS 7 is define in systematic manner.

PART A

QUESTION 1 IASB’s Conceptual Framework

a) Brief description regarding main purpose of IASB's conceptual framework document.

The term conceptual purpose is used to determine the concept that only those items which

fulfil the criteria of being an assets, or liability or equity are used to recognize as financial

position as well as only those item which fulfill the criteria of expenses and income are treated

consider as showing financial performance (Barker, Lennard Nobes, Trombetta and Walton,

2014).

The main purpose of this conceptual framework is to developed future policies of IFRS

as well as receive the current policy and performance of various department of international

accounting board. This is also focus on formulating those policies and rules m as well as

regulation regarding items which are not consider and tenter during the time of preparation of

financial statement. Following are the purpose of IASB which define below

To formulate those policies which help in developing norms of IFRS.

To focus on cut throat those policies which are not useful during the time of formulation

of financial statements.

Focus on development of national standards.

To focus on assist those standard which help in formulate financial statement in

accordance with following norms of international accounting standard.

To assist, auditor of companies in forming opinion regarding with internation standard

complied whit rules and regulation of audit or not.

To formulate those policies which help users at the time of interpreting financial

statement.

International financial reporting is a framework which define various standard in order to

formulate and represent financial statement in ethical manner. This retort has been formulated to

define the relevance of IASB's conceptual framework by showing purpose, importance of this

standard. It is useful for maintain consistency and transparency during the time of compound of

financial statement. In other part use of IFRS for calculating of lease as well as formulation of

statement of cash flow by applying IAS 7 is define in systematic manner.

PART A

QUESTION 1 IASB’s Conceptual Framework

a) Brief description regarding main purpose of IASB's conceptual framework document.

The term conceptual purpose is used to determine the concept that only those items which

fulfil the criteria of being an assets, or liability or equity are used to recognize as financial

position as well as only those item which fulfill the criteria of expenses and income are treated

consider as showing financial performance (Barker, Lennard Nobes, Trombetta and Walton,

2014).

The main purpose of this conceptual framework is to developed future policies of IFRS

as well as receive the current policy and performance of various department of international

accounting board. This is also focus on formulating those policies and rules m as well as

regulation regarding items which are not consider and tenter during the time of preparation of

financial statement. Following are the purpose of IASB which define below

To formulate those policies which help in developing norms of IFRS.

To focus on cut throat those policies which are not useful during the time of formulation

of financial statements.

Focus on development of national standards.

To focus on assist those standard which help in formulate financial statement in

accordance with following norms of international accounting standard.

To assist, auditor of companies in forming opinion regarding with internation standard

complied whit rules and regulation of audit or not.

To formulate those policies which help users at the time of interpreting financial

statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Focus on amendment of the rules of IFRS International financial reporting in order to

create ethical conceptual framework.

IASB’s Conceptual Framework also focus on formulation of various guideline which

help in interpret useless business transactions.

To assist accountability and creditability business activities.

b) Brief explanation regarding assumptions use for preparation of financial statements.

Financial statements are consider as essential document for every business organization .

As with the use of financial statement investors able to recognize their financial position of

organization for specific or given time period. As per the requirement of conceptual framework

of IASB's following assumption needs to be follow by companies or personal during the time of

formulation of financial statement:

Going concern: Every business organization run their operation by assumption that their

organization run for long term purpose and working for foreseeable future operations

without the fear of liquidation or winding up of business (Bauer'Brien and Saeed, 2014).

This assumption is used by personal at the time of formulation of financials statement as

on the basis of that transaction related with recording and selling of business asset has

been recorded. This assumption is based on the concept that business entity will never

affected from any kind of operation which may lead to reason of failure of project.

Organization is work on continuous basis and it only end up or stop their operation with

the mutual concept of their members or by following systematic legal winding up

process.

Accrual basis: This concept is based on the assumption is that organization needs to

record every business transaction activity which affect running business cycle at the time

of it occurs not on the basis of when cash collected.This type of assumption is basically

suitable for large business organization. It is focus on match the amount of expenses and

income generate for particular financial year. According to this concept credit sale must

be record at the time of transaction incurred not when cash received from debtors. This

assumption beneficial for recording transaction in systematic manner.

Assumption related with time period: In order to fulfil the norms of IASB, every

organization need to follow the assumption of time period. According to this concept

every business entity whether it was small or large or work in national or international

create ethical conceptual framework.

IASB’s Conceptual Framework also focus on formulation of various guideline which

help in interpret useless business transactions.

To assist accountability and creditability business activities.

b) Brief explanation regarding assumptions use for preparation of financial statements.

Financial statements are consider as essential document for every business organization .

As with the use of financial statement investors able to recognize their financial position of

organization for specific or given time period. As per the requirement of conceptual framework

of IASB's following assumption needs to be follow by companies or personal during the time of

formulation of financial statement:

Going concern: Every business organization run their operation by assumption that their

organization run for long term purpose and working for foreseeable future operations

without the fear of liquidation or winding up of business (Bauer'Brien and Saeed, 2014).

This assumption is used by personal at the time of formulation of financials statement as

on the basis of that transaction related with recording and selling of business asset has

been recorded. This assumption is based on the concept that business entity will never

affected from any kind of operation which may lead to reason of failure of project.

Organization is work on continuous basis and it only end up or stop their operation with

the mutual concept of their members or by following systematic legal winding up

process.

Accrual basis: This concept is based on the assumption is that organization needs to

record every business transaction activity which affect running business cycle at the time

of it occurs not on the basis of when cash collected.This type of assumption is basically

suitable for large business organization. It is focus on match the amount of expenses and

income generate for particular financial year. According to this concept credit sale must

be record at the time of transaction incurred not when cash received from debtors. This

assumption beneficial for recording transaction in systematic manner.

Assumption related with time period: In order to fulfil the norms of IASB, every

organization need to follow the assumption of time period. According to this concept

every business entity whether it was small or large or work in national or international

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market , needs to represent and showcase their financial statement, document and records

in between gap of time periods, like, months or years. The main purpose of applying this

concept is that it will beneficial for organization as well as relevant interest parties of

business entity for comparing and analysing financial performance of organization. As

well as find out the real position of company in order to attain future goals.

c) Explanation regarding concept of capital maintenance under IASB's framework.

IASB's framework is based on two assumption which is related with financial as well as physical

concept of capital, both are defined below:

Financial concept: This concept is connected with investment and is synonymous of

equity or net assets which highlighted in the equation of accounts. This concept is based on the

assumption that capital is maintain if the closing value of net assets of organization is higher then

its opening balance of net assets then organization generate profit and maintain their level of

financial capital. This type of concept generally beneficial for evaluate value of nominal

financial units or purchasing power units (Bischof. and Ebert, 2014).

Physical capital maintenance: This concept is related with analysis and evaluating

capital on the basis of recognizing productive or operating business performance. This concept is

based on the assumption that organization able to generate profit only when its ability of

resource or physical , operating capacity opening balance is higher then closing balance.

d) Brief description regarding 5 qualitative characteristics & attributes of financial statement use

in IASB's conceptual framework.

Financial statements are formulated for the purpose of showing real financial position of

organization for specific time period. It is also useful for record transactions in systematic

manner. Following are the attributes which every company;s financial statement need to have

according to the guideline of IASB:

Understandability: This is consider as essential trait, which every manager needs to

apply during the time of preparing financial statement. Theses statement must be prepare

in such manner which easily understood and reliable for user. Manager need to focus on

using essential terms, and formulate short notes regarding all the items which may been

difficult to understand they also need to clearly define description related with typical

in between gap of time periods, like, months or years. The main purpose of applying this

concept is that it will beneficial for organization as well as relevant interest parties of

business entity for comparing and analysing financial performance of organization. As

well as find out the real position of company in order to attain future goals.

c) Explanation regarding concept of capital maintenance under IASB's framework.

IASB's framework is based on two assumption which is related with financial as well as physical

concept of capital, both are defined below:

Financial concept: This concept is connected with investment and is synonymous of

equity or net assets which highlighted in the equation of accounts. This concept is based on the

assumption that capital is maintain if the closing value of net assets of organization is higher then

its opening balance of net assets then organization generate profit and maintain their level of

financial capital. This type of concept generally beneficial for evaluate value of nominal

financial units or purchasing power units (Bischof. and Ebert, 2014).

Physical capital maintenance: This concept is related with analysis and evaluating

capital on the basis of recognizing productive or operating business performance. This concept is

based on the assumption that organization able to generate profit only when its ability of

resource or physical , operating capacity opening balance is higher then closing balance.

d) Brief description regarding 5 qualitative characteristics & attributes of financial statement use

in IASB's conceptual framework.

Financial statements are formulated for the purpose of showing real financial position of

organization for specific time period. It is also useful for record transactions in systematic

manner. Following are the attributes which every company;s financial statement need to have

according to the guideline of IASB:

Understandability: This is consider as essential trait, which every manager needs to

apply during the time of preparing financial statement. Theses statement must be prepare

in such manner which easily understood and reliable for user. Manager need to focus on

using essential terms, and formulate short notes regarding all the items which may been

difficult to understand they also need to clearly define description related with typical

financial terms which users not easily interpret. Thus every financial statement should be

formulated in such a way which help shareholders, as well as external users so that that

each easily understand overall position of organization.

Relevant: Financial statement must be showcase relevant information which useful for

their stockholders. As different types of users have different requirement ad exception

thus manager need to formulate statement information in such a way which beneficial for

all users.

Reliable: It is another attribute which must be present in financial statement that all the

information which present in statements are real and collected from authenticate and legal

source (Koning Mertens and Roosenboom 2018).

Comparable: As per the norms of IASB, manager need to prepared financial statement

in such a manner through which they can compare the financial performance with past

years. As well as it also useful in compare and evaluate the position of company as well

as beneficial for manager to compare it with their rival industry on the basis of that

position of organization within the competitive market has been recognize. And user take

decision regarding investment in companies if financial statement have comparable

attribute.

e) Concept of materiality in financial reporting.

This concept is related with accounting norms which define each and every business

activity that directly affect organization's financial statements. According to this concept ,

personal need to record all the items with the financial reports. Material items is related with the

omission or on the basis of inclusion. Which further affect decision making procedure of

organization. This concept is useful in record essential business data. It is generally based on

providing guideline and relevance regarding information,and business transactions to accountant

during the time of preparing financial statement.

QUESTION 2 : IFRS1

a) Brief description regarding mention within IFRS 1.

It is consider as First-time Adoption of International Financial Reporting Standards,

which is issued by ISAB. This is useful for recognizing the requirement of items or source for

preparing financial statements. It is useful in providing guideline to new organization which set

formulated in such a way which help shareholders, as well as external users so that that

each easily understand overall position of organization.

Relevant: Financial statement must be showcase relevant information which useful for

their stockholders. As different types of users have different requirement ad exception

thus manager need to formulate statement information in such a way which beneficial for

all users.

Reliable: It is another attribute which must be present in financial statement that all the

information which present in statements are real and collected from authenticate and legal

source (Koning Mertens and Roosenboom 2018).

Comparable: As per the norms of IASB, manager need to prepared financial statement

in such a manner through which they can compare the financial performance with past

years. As well as it also useful in compare and evaluate the position of company as well

as beneficial for manager to compare it with their rival industry on the basis of that

position of organization within the competitive market has been recognize. And user take

decision regarding investment in companies if financial statement have comparable

attribute.

e) Concept of materiality in financial reporting.

This concept is related with accounting norms which define each and every business

activity that directly affect organization's financial statements. According to this concept ,

personal need to record all the items with the financial reports. Material items is related with the

omission or on the basis of inclusion. Which further affect decision making procedure of

organization. This concept is useful in record essential business data. It is generally based on

providing guideline and relevance regarding information,and business transactions to accountant

during the time of preparing financial statement.

QUESTION 2 : IFRS1

a) Brief description regarding mention within IFRS 1.

It is consider as First-time Adoption of International Financial Reporting Standards,

which is issued by ISAB. This is useful for recognizing the requirement of items or source for

preparing financial statements. It is useful in providing guideline to new organization which set

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

up their operations in financial market. It is compulsory for Prisca Plc that they need to formulate

those accounting policies through which they can follow norms of GAAP. There will be specific

guideline has been given and showcase regarding the date of transaction by using the

competence and norms of IFRS 1 (Kythreotis, 2014).

The main objective of IFRS is that they organizations when they formulated financial statements

after using IFRS norms it must be transparent, and beneficial for users as well as these statement

must be showcase the real value of cost for preparation and running business organization.

b) Essential requirement of IFRS 1 which required by Prisca Plc used for preparing financial

statement

Business organizations apply this concept for specific period of time in order to present

financial statement on the basis of IFRS statements. If Prisca Plc not work according to norms of

IFRS then they face many issues. IFRS useful in formulate and set deduction by observing

general requirement. Following are essential requirement which needed in order to prepare

financial statement as per requirement of IFRS 1

it is necessary to formulate 3 statement of financial position.

It is compulsory for formulate income statement and comprehensive statement of

income .

2 statement of profit and loss.

It is required for organizations to mention essential reliable and related business

information which useful for the purpose of comparison with other organizations.

It is required to formulate 2 cash flow.

With the use of theses organization able to systematic maintain and record their business

transactions.

those accounting policies through which they can follow norms of GAAP. There will be specific

guideline has been given and showcase regarding the date of transaction by using the

competence and norms of IFRS 1 (Kythreotis, 2014).

The main objective of IFRS is that they organizations when they formulated financial statements

after using IFRS norms it must be transparent, and beneficial for users as well as these statement

must be showcase the real value of cost for preparation and running business organization.

b) Essential requirement of IFRS 1 which required by Prisca Plc used for preparing financial

statement

Business organizations apply this concept for specific period of time in order to present

financial statement on the basis of IFRS statements. If Prisca Plc not work according to norms of

IFRS then they face many issues. IFRS useful in formulate and set deduction by observing

general requirement. Following are essential requirement which needed in order to prepare

financial statement as per requirement of IFRS 1

it is necessary to formulate 3 statement of financial position.

It is compulsory for formulate income statement and comprehensive statement of

income .

2 statement of profit and loss.

It is required for organizations to mention essential reliable and related business

information which useful for the purpose of comparison with other organizations.

It is required to formulate 2 cash flow.

With the use of theses organization able to systematic maintain and record their business

transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

QUESTION 4

Brief description regarding how leases should be accounted in financial statement for lessee.

In order to evaluate the concept of leases, IFRS 16 is formulated which will define all the

essential concept and requirements, norms related with treatment of lease. The main objective of

IFRS 16 is to record the entry of lease transaction in faithful way. And also showcase the real

information regarding with cash flow arise due to the use of lease. With the help of norms which

formulated under IFRS 16 individual able to recognize the assets or liabilities arise due to the

use of lease.

In order to determine the value of lease, single lessee model has been used. It is essential

that lessee need to recognize the value of lessee as their asset or liability of organization. If the

value of underlying assets is lower then lessee needs to classify their value of lease on

continuous basis.

Lessee needs to recognize and have knowledge regarding how to use assets. Which useful

to determine how to use lease. With the use of this statement organization able to determine the

value of lease liability which they need to pay (Merkt, 2014).

The main objective of this standard is to acknowledge demonstration, mensuration, &

revelation of requirements of leases, with the purpose that lease & lessor both needs to present

essential information regarding lease.

IFRS 16 consider as an essential part of agreement which useful in represent the right

and norms which determine how to use and formulate policies and record transaction related

with leases. It is also beneficial in order to determine how to use asset for specific financial year

as well as define systematic manner of exchange of business consideration. It showcase non

cancellable payments of lease. This standard help in determine regulation related with how the

amount of lease will be accepted or rejection of lease.

Organizations needs to formulate their financial statement in order to showing right

balance of lessee. Personal when they prepared financial statements use lease as their underlying

assets. Organizations need to receive their right of incentive in order to use lease as part of their

assets. In order to assign or evaluate cost using for underlying lease as an assets need to as how

QUESTION 4

Brief description regarding how leases should be accounted in financial statement for lessee.

In order to evaluate the concept of leases, IFRS 16 is formulated which will define all the

essential concept and requirements, norms related with treatment of lease. The main objective of

IFRS 16 is to record the entry of lease transaction in faithful way. And also showcase the real

information regarding with cash flow arise due to the use of lease. With the help of norms which

formulated under IFRS 16 individual able to recognize the assets or liabilities arise due to the

use of lease.

In order to determine the value of lease, single lessee model has been used. It is essential

that lessee need to recognize the value of lessee as their asset or liability of organization. If the

value of underlying assets is lower then lessee needs to classify their value of lease on

continuous basis.

Lessee needs to recognize and have knowledge regarding how to use assets. Which useful

to determine how to use lease. With the use of this statement organization able to determine the

value of lease liability which they need to pay (Merkt, 2014).

The main objective of this standard is to acknowledge demonstration, mensuration, &

revelation of requirements of leases, with the purpose that lease & lessor both needs to present

essential information regarding lease.

IFRS 16 consider as an essential part of agreement which useful in represent the right

and norms which determine how to use and formulate policies and record transaction related

with leases. It is also beneficial in order to determine how to use asset for specific financial year

as well as define systematic manner of exchange of business consideration. It showcase non

cancellable payments of lease. This standard help in determine regulation related with how the

amount of lease will be accepted or rejection of lease.

Organizations needs to formulate their financial statement in order to showing right

balance of lessee. Personal when they prepared financial statements use lease as their underlying

assets. Organizations need to receive their right of incentive in order to use lease as part of their

assets. In order to assign or evaluate cost using for underlying lease as an assets need to as how

as part of property, equipment and plant. Lease is calculated on amortization basis. In this

implicit interest as reasonable interest.

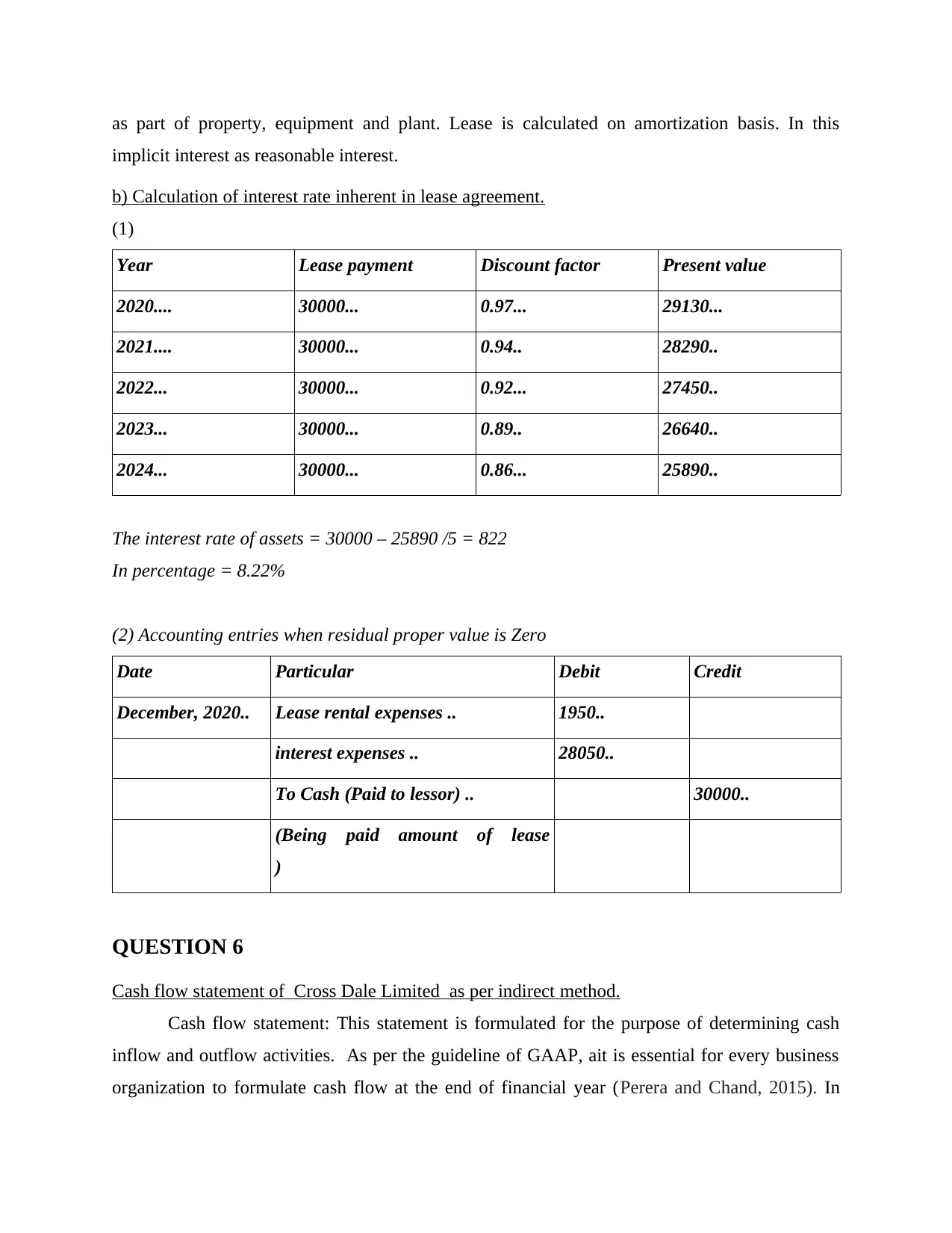

b) Calculation of interest rate inherent in lease agreement.

(1)

Year Lease payment Discount factor Present value

2020.... 30000... 0.97... 29130...

2021.... 30000... 0.94.. 28290..

2022... 30000... 0.92... 27450..

2023... 30000... 0.89.. 26640..

2024... 30000... 0.86... 25890..

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020.. Lease rental expenses .. 1950..

interest expenses .. 28050..

To Cash (Paid to lessor) .. 30000..

(Being paid amount of lease

)

QUESTION 6

Cash flow statement of Cross Dale Limited as per indirect method.

Cash flow statement: This statement is formulated for the purpose of determining cash

inflow and outflow activities. As per the guideline of GAAP, ait is essential for every business

organization to formulate cash flow at the end of financial year (Perera and Chand, 2015). In

implicit interest as reasonable interest.

b) Calculation of interest rate inherent in lease agreement.

(1)

Year Lease payment Discount factor Present value

2020.... 30000... 0.97... 29130...

2021.... 30000... 0.94.. 28290..

2022... 30000... 0.92... 27450..

2023... 30000... 0.89.. 26640..

2024... 30000... 0.86... 25890..

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020.. Lease rental expenses .. 1950..

interest expenses .. 28050..

To Cash (Paid to lessor) .. 30000..

(Being paid amount of lease

)

QUESTION 6

Cash flow statement of Cross Dale Limited as per indirect method.

Cash flow statement: This statement is formulated for the purpose of determining cash

inflow and outflow activities. As per the guideline of GAAP, ait is essential for every business

organization to formulate cash flow at the end of financial year (Perera and Chand, 2015). In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order to determine financial position of organization at the end of financial year. There are two

types of method which define under a the IFRS, indirect as well as direct method of formulation

of cash flow statement. However as per the norms of IFRS 7 every organization need to use

indirect method as it is consider as universally accepted and useful a s well as reliable method in

order to prepare cash flow statement.

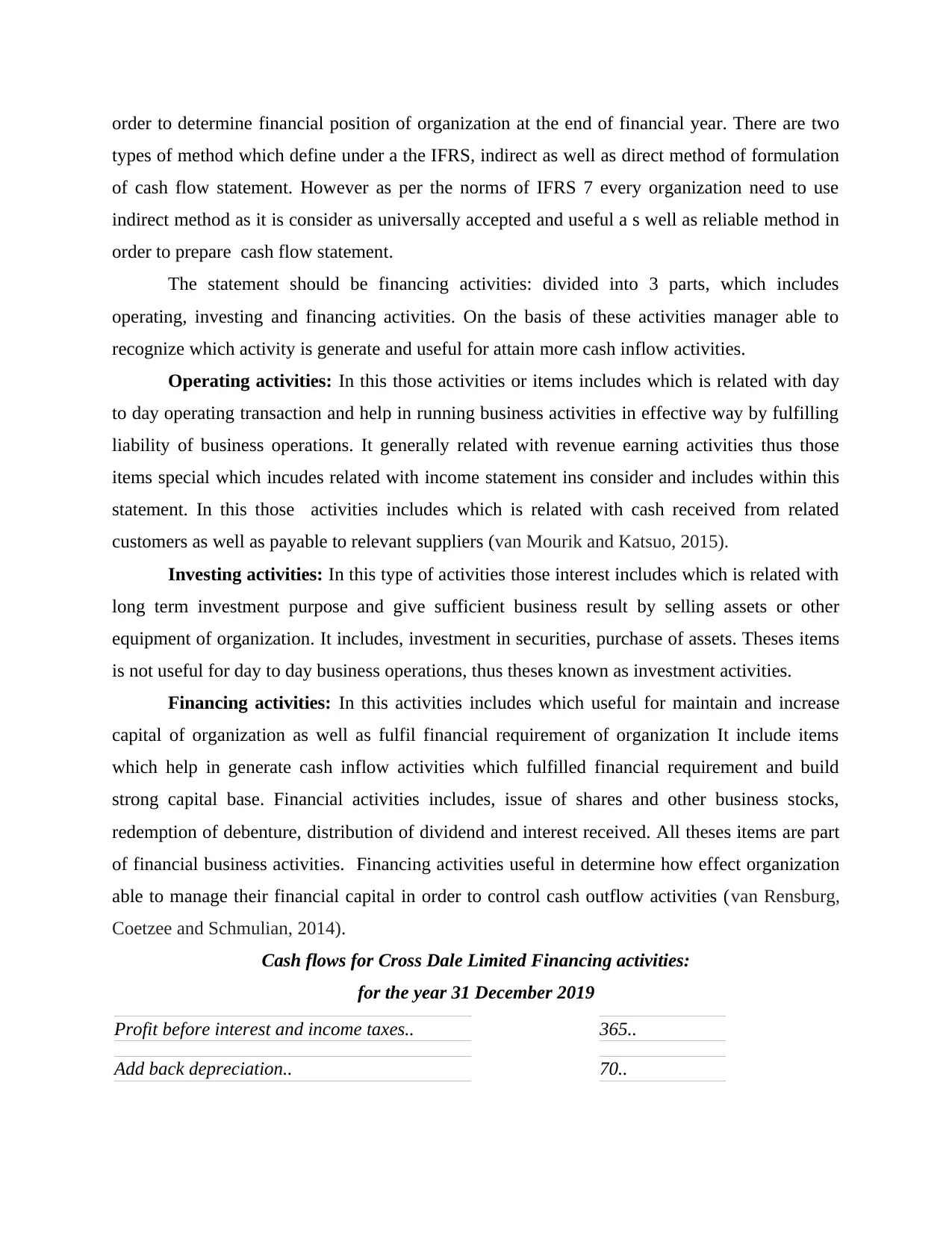

The statement should be financing activities: divided into 3 parts, which includes

operating, investing and financing activities. On the basis of these activities manager able to

recognize which activity is generate and useful for attain more cash inflow activities.

Operating activities: In this those activities or items includes which is related with day

to day operating transaction and help in running business activities in effective way by fulfilling

liability of business operations. It generally related with revenue earning activities thus those

items special which incudes related with income statement ins consider and includes within this

statement. In this those activities includes which is related with cash received from related

customers as well as payable to relevant suppliers (van Mourik and Katsuo, 2015).

Investing activities: In this type of activities those interest includes which is related with

long term investment purpose and give sufficient business result by selling assets or other

equipment of organization. It includes, investment in securities, purchase of assets. Theses items

is not useful for day to day business operations, thus theses known as investment activities.

Financing activities: In this activities includes which useful for maintain and increase

capital of organization as well as fulfil financial requirement of organization It include items

which help in generate cash inflow activities which fulfilled financial requirement and build

strong capital base. Financial activities includes, issue of shares and other business stocks,

redemption of debenture, distribution of dividend and interest received. All theses items are part

of financial business activities. Financing activities useful in determine how effect organization

able to manage their financial capital in order to control cash outflow activities (van Rensburg,

Coetzee and Schmulian, 2014).

Cash flows for Cross Dale Limited Financing activities:

for the year 31 December 2019

Profit before interest and income taxes.. 365..

Add back depreciation.. 70..

types of method which define under a the IFRS, indirect as well as direct method of formulation

of cash flow statement. However as per the norms of IFRS 7 every organization need to use

indirect method as it is consider as universally accepted and useful a s well as reliable method in

order to prepare cash flow statement.

The statement should be financing activities: divided into 3 parts, which includes

operating, investing and financing activities. On the basis of these activities manager able to

recognize which activity is generate and useful for attain more cash inflow activities.

Operating activities: In this those activities or items includes which is related with day

to day operating transaction and help in running business activities in effective way by fulfilling

liability of business operations. It generally related with revenue earning activities thus those

items special which incudes related with income statement ins consider and includes within this

statement. In this those activities includes which is related with cash received from related

customers as well as payable to relevant suppliers (van Mourik and Katsuo, 2015).

Investing activities: In this type of activities those interest includes which is related with

long term investment purpose and give sufficient business result by selling assets or other

equipment of organization. It includes, investment in securities, purchase of assets. Theses items

is not useful for day to day business operations, thus theses known as investment activities.

Financing activities: In this activities includes which useful for maintain and increase

capital of organization as well as fulfil financial requirement of organization It include items

which help in generate cash inflow activities which fulfilled financial requirement and build

strong capital base. Financial activities includes, issue of shares and other business stocks,

redemption of debenture, distribution of dividend and interest received. All theses items are part

of financial business activities. Financing activities useful in determine how effect organization

able to manage their financial capital in order to control cash outflow activities (van Rensburg,

Coetzee and Schmulian, 2014).

Cash flows for Cross Dale Limited Financing activities:

for the year 31 December 2019

Profit before interest and income taxes.. 365..

Add back depreciation.. 70..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add back impairment of assets... Nil..

Increase in receivables... 17..

Decrease in inventories... 19..

Increase in trade payables.. 6..

Interest expense... Nil..

Less Interest accrued but not yet paid.. 3..

Interest paid... 18..

Income taxes paid... 33..

Net cash from operating activities.. 475..

Cash flow statement of Cross Dale Limited as per direct method.

As per the norms of IFRS there will be two types methods which help in formulation of

cash flow statement. Direct method is part of this. It is different form indirect method as during

the time of formulation of cash flow through direct method manager need not to categories

activities in single frame of document. Rather then they calculate cash flow from different

categorised by formulating separate document. In this all cash inflow as well as outflow

activities directly add or deducted by formulation of cash flow from operating activities.

Investment as well as financial activities is also determine or calculated in same manner.

However during the time of formulation of direct method it is not essential to calculate value of

financial or investment activities.

In this cash flow statement of Cross Dale Limited is formulated for the purpose of operating

activities.

Cash received from customers: In order to evaluate the amount of operating cash inflow

activities, it is assumed that all the sales is generate on cash basis (Zhang and Andrew 2014).

Cash paid to suppliers: For calculation of cash from operating business activities, it is

also consider that all the goods are purchase on the basis of cash.

Cash paid to employees: For calculation of actual amount of cash generate from

operating cash activities it has been analysis that salaries are paid on cash basis.

Cash flows for Cross Dale Limited

Increase in receivables... 17..

Decrease in inventories... 19..

Increase in trade payables.. 6..

Interest expense... Nil..

Less Interest accrued but not yet paid.. 3..

Interest paid... 18..

Income taxes paid... 33..

Net cash from operating activities.. 475..

Cash flow statement of Cross Dale Limited as per direct method.

As per the norms of IFRS there will be two types methods which help in formulation of

cash flow statement. Direct method is part of this. It is different form indirect method as during

the time of formulation of cash flow through direct method manager need not to categories

activities in single frame of document. Rather then they calculate cash flow from different

categorised by formulating separate document. In this all cash inflow as well as outflow

activities directly add or deducted by formulation of cash flow from operating activities.

Investment as well as financial activities is also determine or calculated in same manner.

However during the time of formulation of direct method it is not essential to calculate value of

financial or investment activities.

In this cash flow statement of Cross Dale Limited is formulated for the purpose of operating

activities.

Cash received from customers: In order to evaluate the amount of operating cash inflow

activities, it is assumed that all the sales is generate on cash basis (Zhang and Andrew 2014).

Cash paid to suppliers: For calculation of cash from operating business activities, it is

also consider that all the goods are purchase on the basis of cash.

Cash paid to employees: For calculation of actual amount of cash generate from

operating cash activities it has been analysis that salaries are paid on cash basis.

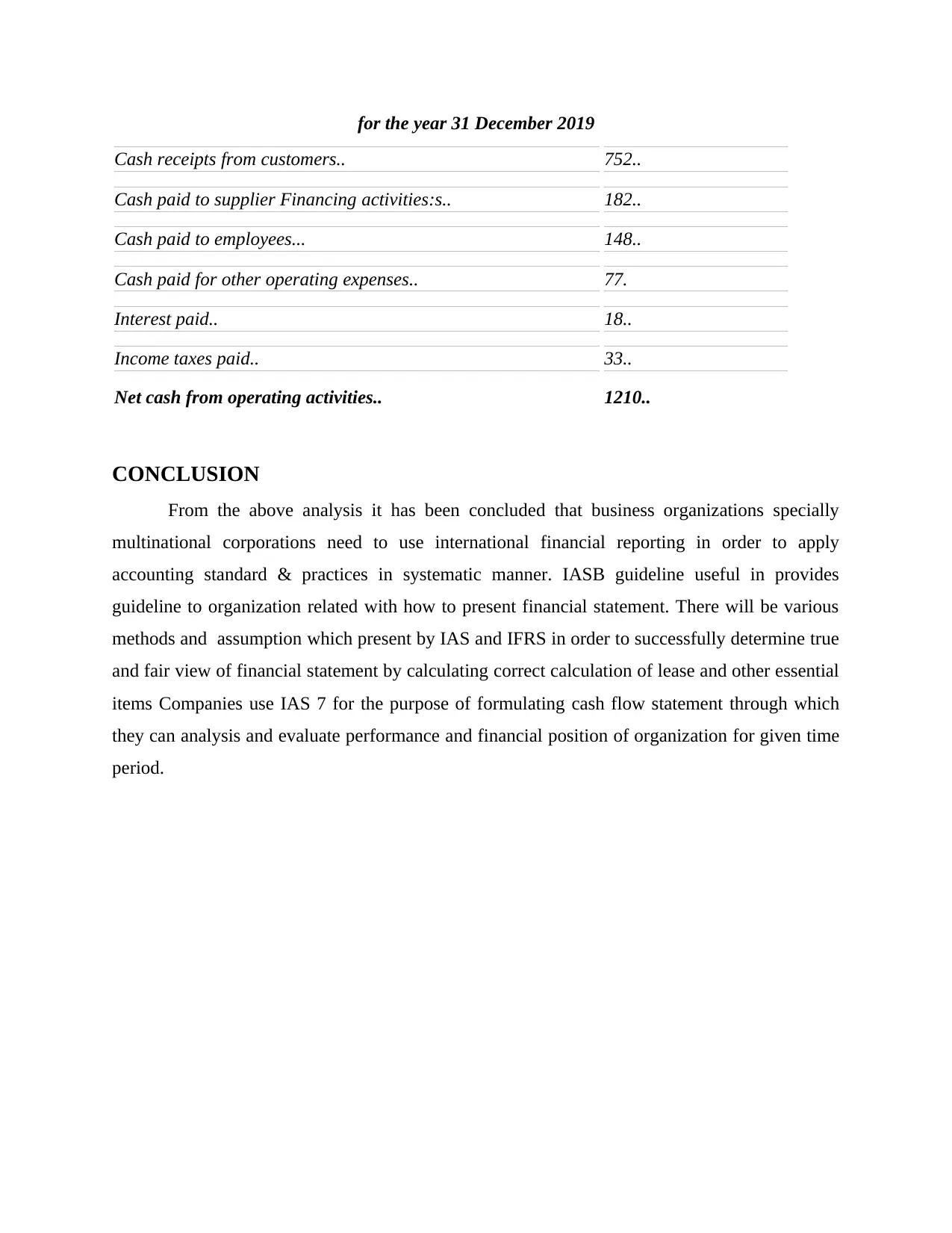

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers.. 752..

Cash paid to supplier Financing activities:s.. 182..

Cash paid to employees... 148..

Cash paid for other operating expenses.. 77.

Interest paid.. 18..

Income taxes paid.. 33..

Net cash from operating activities.. 1210..

CONCLUSION

From the above analysis it has been concluded that business organizations specially

multinational corporations need to use international financial reporting in order to apply

accounting standard & practices in systematic manner. IASB guideline useful in provides

guideline to organization related with how to present financial statement. There will be various

methods and assumption which present by IAS and IFRS in order to successfully determine true

and fair view of financial statement by calculating correct calculation of lease and other essential

items Companies use IAS 7 for the purpose of formulating cash flow statement through which

they can analysis and evaluate performance and financial position of organization for given time

period.

Cash receipts from customers.. 752..

Cash paid to supplier Financing activities:s.. 182..

Cash paid to employees... 148..

Cash paid for other operating expenses.. 77.

Interest paid.. 18..

Income taxes paid.. 33..

Net cash from operating activities.. 1210..

CONCLUSION

From the above analysis it has been concluded that business organizations specially

multinational corporations need to use international financial reporting in order to apply

accounting standard & practices in systematic manner. IASB guideline useful in provides

guideline to organization related with how to present financial statement. There will be various

methods and assumption which present by IAS and IFRS in order to successfully determine true

and fair view of financial statement by calculating correct calculation of lease and other essential

items Companies use IAS 7 for the purpose of formulating cash flow statement through which

they can analysis and evaluate performance and financial position of organization for given time

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.