International Financial Reporting Standards: A Comprehensive Report

VerifiedAdded on 2022/12/30

|13

|3727

|50

Report

AI Summary

This report provides a comprehensive overview of International Financial Reporting Standards (IFRS). It begins with an introduction to IFRS and its role in financial reporting, emphasizing the importance of consistent, transparent, and comparable financial statements. The report is divided into two parts. Part A focuses on the IASB's conceptual framework, including its purpose, assumptions for financial statement preparation, capital maintenance concepts, qualitative characteristics, and the concept of materiality. Part B addresses practical applications, specifically IFRS 16 (Leases) and IAS 7 (Statement of Cash Flows). The report explains the terms 'first IFRS reporting period' and 'date of transition' as defined by IFRS 1, along with its requirements. The report also covers the single lessee accounting model from IFRS 16 and the requirements of the cash flow statement. Overall, the report aims to provide a detailed analysis of IFRS and its practical implications for financial reporting.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Question 1 IASB's conceptual framework.......................................................................................1

(a) Main purpose of the IASB's conceptual framework document.............................................1

(b) Assumptions of preparation of financial statements.............................................................2

(c) Main concepts of capital maintenance, make references to the IASB's conceptual

framework...................................................................................................................................2

(d) Five qualitative characteristics and attributes of financial statements in the IASB's

conceptual framework.................................................................................................................3

(e) Concept of materiality...........................................................................................................4

Question 2 IFRS1 - First-time Adoption of International Financial Reporting Standard................4

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1..4

Requirements of IFRS1...............................................................................................................5

PART B............................................................................................................................................6

Question 4 IFRS16 - Lease.........................................................................................................6

Question 6 : IAS7 - Statement of Cash Flows............................................................................7

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Question 1 IASB's conceptual framework.......................................................................................1

(a) Main purpose of the IASB's conceptual framework document.............................................1

(b) Assumptions of preparation of financial statements.............................................................2

(c) Main concepts of capital maintenance, make references to the IASB's conceptual

framework...................................................................................................................................2

(d) Five qualitative characteristics and attributes of financial statements in the IASB's

conceptual framework.................................................................................................................3

(e) Concept of materiality...........................................................................................................4

Question 2 IFRS1 - First-time Adoption of International Financial Reporting Standard................4

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1..4

Requirements of IFRS1...............................................................................................................5

PART B............................................................................................................................................6

Question 4 IFRS16 - Lease.........................................................................................................6

Question 6 : IAS7 - Statement of Cash Flows............................................................................7

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

International financial reporting standard (IFRS) is accounting framework which is used

by the organisation to proper organize financial report. This framework uses to make financial

statement in consistent, transparent and comparable manner. IFRS use by businesses to carry out

all the financial outcomes and actual worth of company with same rules. On the basis of IFRS

framework public and non public organisations prepare their financial statements and present

their actual financial position (Lakew and Musa, 2019). It is also providing common guidelines

for the preparation of financial statements instead of set out rules for particular industry. This

report categorised into two parts Part A and Part B. In Part A, define the purpose of IASB's

conceptual framework, assumptions to prepare financial statements. Along with explain

qualitative characteristics and attributes of financial statements and critically define materiality

concept to financial reporting. In Part B, sort out the practicals of lease, cash flow statement to

analysis the actual position of business.

PART A

Question 1 IASB's conceptual framework

(a) Main purpose of the IASB's conceptual framework document

Conceptual framework is use to analysis the IASB in developing and revising IFRSs.

This concept mainly used for preparation of accounting policies and focus on those areas that are

not covered as per accounting policy and assistance of all users to know the IFRS. There are

mentioned different purpose of conceptual framework such as:

The main purpose of IASB conceptual framework to analysis the development of future

IFRS and determine of existing IFRSs.

The conceptual framework uses to preparation of financial statements in set up

accounting guidelines for different transactions or event not included into existing

standards (Lisowsky and Minnis, 2020).

In some cases, the IASB might require to amended IFRS that create issue with other

activities of the conceptual framework. Thus, IASB require to define and explain the

departure from the framework as the basis for conclusions.

1

International financial reporting standard (IFRS) is accounting framework which is used

by the organisation to proper organize financial report. This framework uses to make financial

statement in consistent, transparent and comparable manner. IFRS use by businesses to carry out

all the financial outcomes and actual worth of company with same rules. On the basis of IFRS

framework public and non public organisations prepare their financial statements and present

their actual financial position (Lakew and Musa, 2019). It is also providing common guidelines

for the preparation of financial statements instead of set out rules for particular industry. This

report categorised into two parts Part A and Part B. In Part A, define the purpose of IASB's

conceptual framework, assumptions to prepare financial statements. Along with explain

qualitative characteristics and attributes of financial statements and critically define materiality

concept to financial reporting. In Part B, sort out the practicals of lease, cash flow statement to

analysis the actual position of business.

PART A

Question 1 IASB's conceptual framework

(a) Main purpose of the IASB's conceptual framework document

Conceptual framework is use to analysis the IASB in developing and revising IFRSs.

This concept mainly used for preparation of accounting policies and focus on those areas that are

not covered as per accounting policy and assistance of all users to know the IFRS. There are

mentioned different purpose of conceptual framework such as:

The main purpose of IASB conceptual framework to analysis the development of future

IFRS and determine of existing IFRSs.

The conceptual framework uses to preparation of financial statements in set up

accounting guidelines for different transactions or event not included into existing

standards (Lisowsky and Minnis, 2020).

In some cases, the IASB might require to amended IFRS that create issue with other

activities of the conceptual framework. Thus, IASB require to define and explain the

departure from the framework as the basis for conclusions.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The another purpose of conceptual framework is it carry out different guidelines to

interpret unusual transactions. Along with it improve the credibility and accounting

activities on overall basis.

(b) Assumptions of preparation of financial statements

To prepare of the financial statements requires to follow IASB assumptions that guide

how to prepare authentic and effective financial statements that present actual financial position

of business. These assumptions are mention below such as:

Going concern: This assumption use by the organisation to prepare financial statements

and present all operation for the foreseeable future. It is most essential assumption

because it is using at the end of financial year, that time all the assets have to be sold and

sales value recorded at book value (Mnif Sellami and Gafsi, 2019).

Accrual basis: This is another assumption which is using by the business entity to match

the all income and expenditure in particular financial year. There is earned or incurred

not in the particular time in which payment was accepted or made.

Time period assumption: It refers that company presents all the necessary financial

information in brief time of period like months, quarter and years. On the basis of these

information compare and analysis activity easily. These information will be timely and

and help to present actual picture of business entity.

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework

Capital maintenance: It is most important concept that use for only income generation

in excess manner and manage capital in regard of profit. The particular IASB conceptual

framework define the concept of capital maintenance such as:

Financial capital maintenance: In this concept profit is generated by business when

financial amount of net assets increase at the end of financial year as compare of stating

net assets amount after excludes any distributions to contribution from owners at

financial year. Financial capital maintenance used for nominal monetary units and for

purchasing power units (Mohammadi and et.al, 2020).

Physical capital maintenance: As per the concept a profit is generated by the business

when physical productive capacity use at the end of financial year because it increases the

physical productive capacity at the starting of financial year. In this excludes all the

distribution and contribution as per owner.

2

interpret unusual transactions. Along with it improve the credibility and accounting

activities on overall basis.

(b) Assumptions of preparation of financial statements

To prepare of the financial statements requires to follow IASB assumptions that guide

how to prepare authentic and effective financial statements that present actual financial position

of business. These assumptions are mention below such as:

Going concern: This assumption use by the organisation to prepare financial statements

and present all operation for the foreseeable future. It is most essential assumption

because it is using at the end of financial year, that time all the assets have to be sold and

sales value recorded at book value (Mnif Sellami and Gafsi, 2019).

Accrual basis: This is another assumption which is using by the business entity to match

the all income and expenditure in particular financial year. There is earned or incurred

not in the particular time in which payment was accepted or made.

Time period assumption: It refers that company presents all the necessary financial

information in brief time of period like months, quarter and years. On the basis of these

information compare and analysis activity easily. These information will be timely and

and help to present actual picture of business entity.

(c) Main concepts of capital maintenance, make references to the IASB's conceptual framework

Capital maintenance: It is most important concept that use for only income generation

in excess manner and manage capital in regard of profit. The particular IASB conceptual

framework define the concept of capital maintenance such as:

Financial capital maintenance: In this concept profit is generated by business when

financial amount of net assets increase at the end of financial year as compare of stating

net assets amount after excludes any distributions to contribution from owners at

financial year. Financial capital maintenance used for nominal monetary units and for

purchasing power units (Mohammadi and et.al, 2020).

Physical capital maintenance: As per the concept a profit is generated by the business

when physical productive capacity use at the end of financial year because it increases the

physical productive capacity at the starting of financial year. In this excludes all the

distribution and contribution as per owner.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d) Five qualitative characteristics and attributes of financial statements in the IASB's conceptual

framework

Qualitative characteristics of financial statements: The main aim of the financial

statements to record all the transactions that occur in particular financial year because it helps to

calculate actual profit of the business and present a clear picture to shareholders. Following are

the main qualitative characteristics of financial statement as per IASB:

Understandability: It is most important characteristic of financial statement that all the

information that provide should be understood easily by users and interest by the

shareholders. All the financial information must be clear and readable. In case on

understandability, the management focus on statutory data and also on the specific

information to make financial statements properly (G Tayo and O Olayeye, 2019).

Relevant: It is another characteristic must have in financial statement that all the

information provide in the report is relevant to the need of users. On the basis of these

information use take financial decision in regard of investment. Along with these

information analysis, past, present and potential events. For example, dividend paid up

information is valuable last year for future investors.

Reliable: The information provided in the financial reports must be reliable and authentic.

All the information collects from authentic sources because the financial reports presents

actual picture of company affairs. All the transactions shown on basis of concept of

prudence and present all the transactions as well as operations.

Comparable: The financial statements must be prepared in comparison manner. It means

financial report compare with prior year financial statements. It is essential to maintain

and assure about the performance of the organisations that could be analysed and

compared. To manage this characteristics require to adopt accounting policies as well as

standards in effective way from period to period in between various dominion (Akther

and Xu, 2020). The requirement of comparability to present ability of business and their

accounts is effective way. Whenever relevance and reliability is not authentic manner so

require to continue with the same policies, they should be changed.

Timeliness: It is last characteristic that presents that all the financial information presents

to company in particular period of time. All the income of expenses of a financial year

present in same year financial reports not in next year financial statements. Thus, it will

3

framework

Qualitative characteristics of financial statements: The main aim of the financial

statements to record all the transactions that occur in particular financial year because it helps to

calculate actual profit of the business and present a clear picture to shareholders. Following are

the main qualitative characteristics of financial statement as per IASB:

Understandability: It is most important characteristic of financial statement that all the

information that provide should be understood easily by users and interest by the

shareholders. All the financial information must be clear and readable. In case on

understandability, the management focus on statutory data and also on the specific

information to make financial statements properly (G Tayo and O Olayeye, 2019).

Relevant: It is another characteristic must have in financial statement that all the

information provide in the report is relevant to the need of users. On the basis of these

information use take financial decision in regard of investment. Along with these

information analysis, past, present and potential events. For example, dividend paid up

information is valuable last year for future investors.

Reliable: The information provided in the financial reports must be reliable and authentic.

All the information collects from authentic sources because the financial reports presents

actual picture of company affairs. All the transactions shown on basis of concept of

prudence and present all the transactions as well as operations.

Comparable: The financial statements must be prepared in comparison manner. It means

financial report compare with prior year financial statements. It is essential to maintain

and assure about the performance of the organisations that could be analysed and

compared. To manage this characteristics require to adopt accounting policies as well as

standards in effective way from period to period in between various dominion (Akther

and Xu, 2020). The requirement of comparability to present ability of business and their

accounts is effective way. Whenever relevance and reliability is not authentic manner so

require to continue with the same policies, they should be changed.

Timeliness: It is last characteristic that presents that all the financial information presents

to company in particular period of time. All the income of expenses of a financial year

present in same year financial reports not in next year financial statements. Thus, it will

3

help to make right economic decision and possess all related and up to date knowledge.

Therefore this characteristics require more resources and as delayed information make

any bad decision that time.

(e) Concept of materiality

The concept of materiality is type of accounting rules that use by the organisations to

dictates any activity and item which directly affect on the financial statements. This concept

refers that all materials items should be recorded into financial reports. These material items

consider on basis of its inclusion or omission that affect on the decision making procedure of

financial accountant (Bushee, Goodman and Sunder, 2019). Materiality in accounting is

subjective and important for financial statement in order to present all important material

information. Most of the aspects of materiality are remarkable during the comparison of large as

well as small size organisation. The main aim of the concept in accounting to analysis the all

financial information that directly affect on the mindset of financial statement users. Materiality

implies to importance of particular items in case of other items that based on the financial

statements and size of the business entity. As per the IASB guideline there is not set particular

guideline for the calculation of materiality amount.

Pros: The main advantage of this concept that it provides all the information of the

material and help to in decision making procedure.

Cons: Many time deductions and omissions create problem to calculate materiality

amount in financial statement.

Question 2 IFRS1 - First-time Adoption of International Financial Reporting

Standard

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1

IFRS 1 use by business when first time apply IFRS standards in business to set their

financial statements in which consist of its first IFRS reporting period and the preceding year.

The organisation uses these accounting policies and standards in particular financial year to

present IFRS financial statements. These accounting policies related with every standard in

effective at the end of its first IFRS reporting period. IFRS 1 consist of limited exemptions as per

the requirement to restate prior periods in particular areas with the cost and likely to increase the

advantage of users of financial statements (Shepardson, 2019).

4

Therefore this characteristics require more resources and as delayed information make

any bad decision that time.

(e) Concept of materiality

The concept of materiality is type of accounting rules that use by the organisations to

dictates any activity and item which directly affect on the financial statements. This concept

refers that all materials items should be recorded into financial reports. These material items

consider on basis of its inclusion or omission that affect on the decision making procedure of

financial accountant (Bushee, Goodman and Sunder, 2019). Materiality in accounting is

subjective and important for financial statement in order to present all important material

information. Most of the aspects of materiality are remarkable during the comparison of large as

well as small size organisation. The main aim of the concept in accounting to analysis the all

financial information that directly affect on the mindset of financial statement users. Materiality

implies to importance of particular items in case of other items that based on the financial

statements and size of the business entity. As per the IASB guideline there is not set particular

guideline for the calculation of materiality amount.

Pros: The main advantage of this concept that it provides all the information of the

material and help to in decision making procedure.

Cons: Many time deductions and omissions create problem to calculate materiality

amount in financial statement.

Question 2 IFRS1 - First-time Adoption of International Financial Reporting

Standard

Explain the terms "first IFRS reporting period" and "date of transition" as defined by IFRS1

IFRS 1 use by business when first time apply IFRS standards in business to set their

financial statements in which consist of its first IFRS reporting period and the preceding year.

The organisation uses these accounting policies and standards in particular financial year to

present IFRS financial statements. These accounting policies related with every standard in

effective at the end of its first IFRS reporting period. IFRS 1 consist of limited exemptions as per

the requirement to restate prior periods in particular areas with the cost and likely to increase the

advantage of users of financial statements (Shepardson, 2019).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main objective of this IFRS is to assure that an entity first IFRS financial statements

and its temporary financial statements for the portion of period covered by those financial

statements consist of high quality information.

Date of transition: As per the IFRS 1, date of transition defined as at the starting of the

earliest time in which business presents full comparative knowledge under IFRSs in its first IFRS

financial reports. At the starting of when company first time adopt IFRS that time prepare

opening balance sheet at the date of transition and this opening balance sheet is prepared as per

the IFRS1 where consist of common principle of retrospective application and alternative

exemption. This balance sheet is not necessary to present in financial statements whether is is

utilised on basis for preparation of such financial reports.

Requirements of IFRS1

IFRS refers how businesses require to manage and report their accounts. It is used by the

business entity to set accounting language and help to achieve goal of international financial

reporting standards to make effective financial decision that agreeable and conformable with

various nations and industries. The main requirements of IFRS 1 is set financial statements in

which consist of explicit and unpractised statement of cooperation with IFRS (Hope, Yue and

Zhong, 2020). When the Prisca plc do not apply IFRS so face many problems like need to

modification in accounting policies in IAS 8 and require particular transitional requirements in

other IFRs.

IFRS 1 first time adoption of IFRS sets out a process in which a business follow when

agree to apply accounting rules and policies of IFRS 1 on time basis for preparation its general

reason of financial reports. It is setting limited deductions on basis of general requirements to

related with beginning and ending period of IFRS. There are mentioned mainly requirements of

IFRS 1 to prepare financial statements such as:

Three statements of financial position

2 statements prepare for profit and loss account and other comprehensive income

Prepare two different statements of profit or loss (if presented)

Two statements of cash flows

Mention all related notes in which consist of comparative information

Two reports of cash flow

5

and its temporary financial statements for the portion of period covered by those financial

statements consist of high quality information.

Date of transition: As per the IFRS 1, date of transition defined as at the starting of the

earliest time in which business presents full comparative knowledge under IFRSs in its first IFRS

financial reports. At the starting of when company first time adopt IFRS that time prepare

opening balance sheet at the date of transition and this opening balance sheet is prepared as per

the IFRS1 where consist of common principle of retrospective application and alternative

exemption. This balance sheet is not necessary to present in financial statements whether is is

utilised on basis for preparation of such financial reports.

Requirements of IFRS1

IFRS refers how businesses require to manage and report their accounts. It is used by the

business entity to set accounting language and help to achieve goal of international financial

reporting standards to make effective financial decision that agreeable and conformable with

various nations and industries. The main requirements of IFRS 1 is set financial statements in

which consist of explicit and unpractised statement of cooperation with IFRS (Hope, Yue and

Zhong, 2020). When the Prisca plc do not apply IFRS so face many problems like need to

modification in accounting policies in IAS 8 and require particular transitional requirements in

other IFRs.

IFRS 1 first time adoption of IFRS sets out a process in which a business follow when

agree to apply accounting rules and policies of IFRS 1 on time basis for preparation its general

reason of financial reports. It is setting limited deductions on basis of general requirements to

related with beginning and ending period of IFRS. There are mentioned mainly requirements of

IFRS 1 to prepare financial statements such as:

Three statements of financial position

2 statements prepare for profit and loss account and other comprehensive income

Prepare two different statements of profit or loss (if presented)

Two statements of cash flows

Mention all related notes in which consist of comparative information

Two reports of cash flow

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Question 4 IFRS16 - Lease

IFRS 16 is defined about the IFRS reporter will identify, analysis, present and reveal

leases. This standard define about the single lessee accounting model which is used by the

organisation to identify assets and liabilities for all leases unless the leases term set 12 months.

From the amount less low value of underlying assets and the lessors continue with the

classification of leases (Bratten, Causholli and Omer, 2019). The main aim of this principle that

IFRS 16 set up for the acknowledgement, mensuration, demonstration and revelation of leases

with the objective of that assure about the leases and lessor present all related information that

use faithfully to present all the transactions.

(a) IFRS 16 refers as an agreement or a part of agreement that use to present right use of assets in

particular financial period and in manner of exchange of consideration. Assets and liabilities that

related with the lease are mainly analysed on the basis of present value. In this measurement

consist of non cancellable lease payments and also consist of alternative periods when the lessee

is effectively definite to exercise an option to increase the lease or not to exercise in order to

rejected the lease.

At the time of preparation of financial statements lease assets is using in the statements as

underlying assets and shown at the side of plant, property and equipment. The right of use assets

in which consisting of particular amounts that related with lease incentives received. There are

considering of starting direct cost and analysis the cost by lessee in dismasting and ignoring the

underlying assets or restoring the site that based on the location to produce inventories. For the

liabilities lease is effectively identified that is measured on the basis of amortised cost and use

the rate of interest implicit in case of lease as the reasonable interest rate (Shahzad and et.al,

2019).

(b)

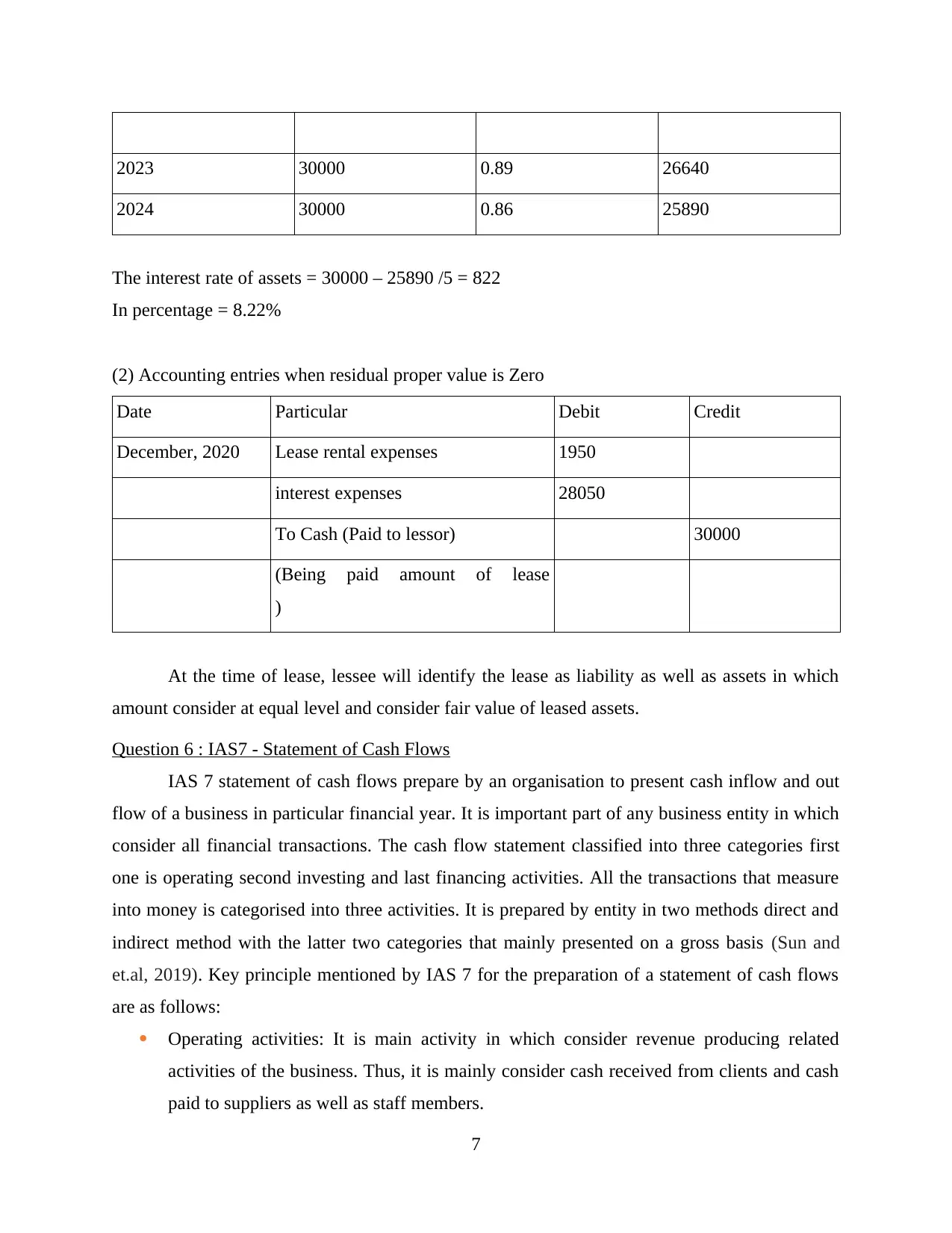

(1)

Year Lease payment Discount factor Present value

2020 30000 0.97 29130

2021 30000 0.94 28290

2022 30000 0.92 27450

6

Question 4 IFRS16 - Lease

IFRS 16 is defined about the IFRS reporter will identify, analysis, present and reveal

leases. This standard define about the single lessee accounting model which is used by the

organisation to identify assets and liabilities for all leases unless the leases term set 12 months.

From the amount less low value of underlying assets and the lessors continue with the

classification of leases (Bratten, Causholli and Omer, 2019). The main aim of this principle that

IFRS 16 set up for the acknowledgement, mensuration, demonstration and revelation of leases

with the objective of that assure about the leases and lessor present all related information that

use faithfully to present all the transactions.

(a) IFRS 16 refers as an agreement or a part of agreement that use to present right use of assets in

particular financial period and in manner of exchange of consideration. Assets and liabilities that

related with the lease are mainly analysed on the basis of present value. In this measurement

consist of non cancellable lease payments and also consist of alternative periods when the lessee

is effectively definite to exercise an option to increase the lease or not to exercise in order to

rejected the lease.

At the time of preparation of financial statements lease assets is using in the statements as

underlying assets and shown at the side of plant, property and equipment. The right of use assets

in which consisting of particular amounts that related with lease incentives received. There are

considering of starting direct cost and analysis the cost by lessee in dismasting and ignoring the

underlying assets or restoring the site that based on the location to produce inventories. For the

liabilities lease is effectively identified that is measured on the basis of amortised cost and use

the rate of interest implicit in case of lease as the reasonable interest rate (Shahzad and et.al,

2019).

(b)

(1)

Year Lease payment Discount factor Present value

2020 30000 0.97 29130

2021 30000 0.94 28290

2022 30000 0.92 27450

6

2023 30000 0.89 26640

2024 30000 0.86 25890

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

interest expenses 28050

To Cash (Paid to lessor) 30000

(Being paid amount of lease

)

At the time of lease, lessee will identify the lease as liability as well as assets in which

amount consider at equal level and consider fair value of leased assets.

Question 6 : IAS7 - Statement of Cash Flows

IAS 7 statement of cash flows prepare by an organisation to present cash inflow and out

flow of a business in particular financial year. It is important part of any business entity in which

consider all financial transactions. The cash flow statement classified into three categories first

one is operating second investing and last financing activities. All the transactions that measure

into money is categorised into three activities. It is prepared by entity in two methods direct and

indirect method with the latter two categories that mainly presented on a gross basis (Sun and

et.al, 2019). Key principle mentioned by IAS 7 for the preparation of a statement of cash flows

are as follows:

Operating activities: It is main activity in which consider revenue producing related

activities of the business. Thus, it is mainly consider cash received from clients and cash

paid to suppliers as well as staff members.

7

2024 30000 0.86 25890

The interest rate of assets = 30000 – 25890 /5 = 822

In percentage = 8.22%

(2) Accounting entries when residual proper value is Zero

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

interest expenses 28050

To Cash (Paid to lessor) 30000

(Being paid amount of lease

)

At the time of lease, lessee will identify the lease as liability as well as assets in which

amount consider at equal level and consider fair value of leased assets.

Question 6 : IAS7 - Statement of Cash Flows

IAS 7 statement of cash flows prepare by an organisation to present cash inflow and out

flow of a business in particular financial year. It is important part of any business entity in which

consider all financial transactions. The cash flow statement classified into three categories first

one is operating second investing and last financing activities. All the transactions that measure

into money is categorised into three activities. It is prepared by entity in two methods direct and

indirect method with the latter two categories that mainly presented on a gross basis (Sun and

et.al, 2019). Key principle mentioned by IAS 7 for the preparation of a statement of cash flows

are as follows:

Operating activities: It is main activity in which consider revenue producing related

activities of the business. Thus, it is mainly consider cash received from clients and cash

paid to suppliers as well as staff members.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investing activities: There are considering all those activities which is related to

acquisition and disposal of lengthy term assets and investments which is not cash

equivalents.

Financing activities: These activities are modifying with the equity capital and borrowing

structure of the business.

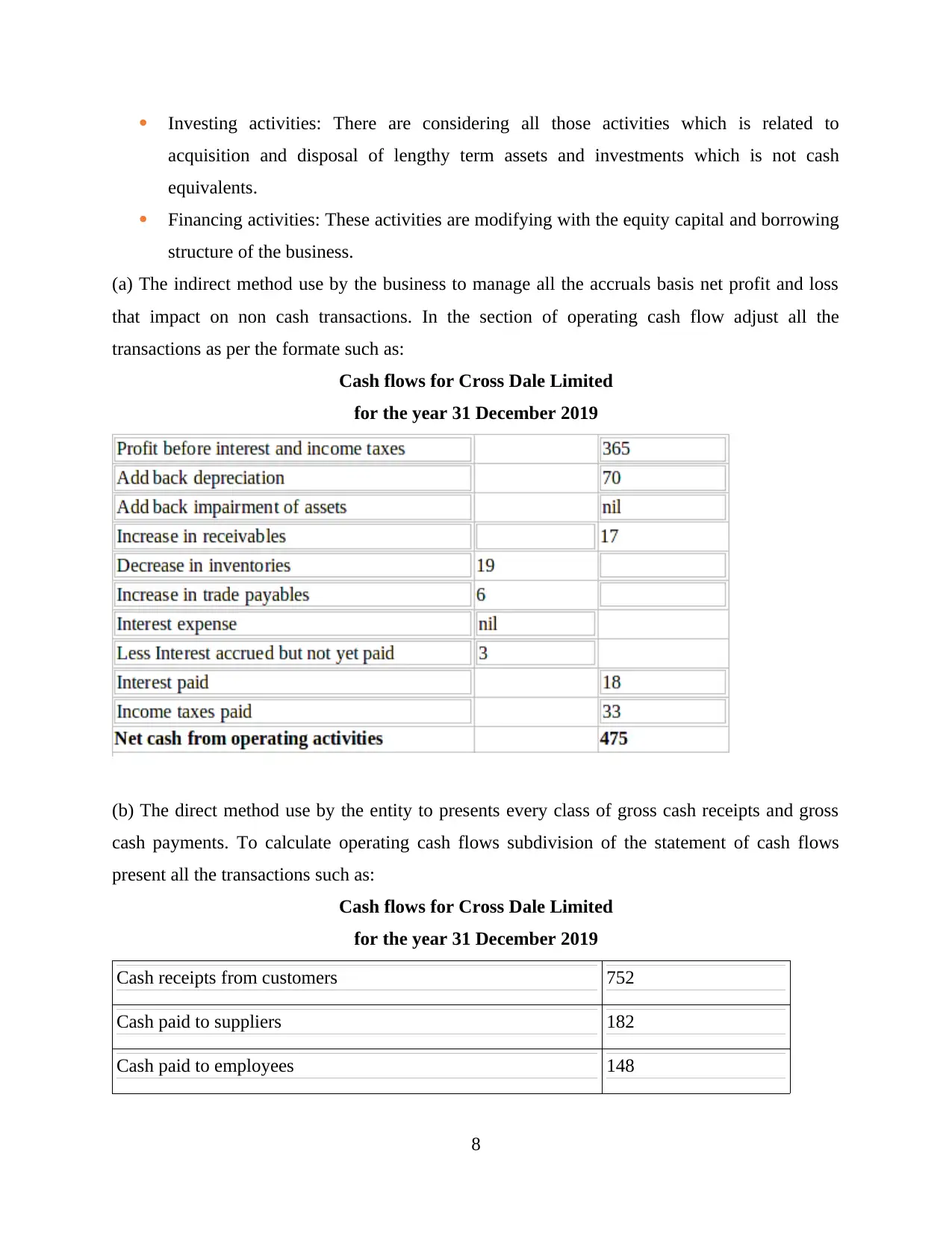

(a) The indirect method use by the business to manage all the accruals basis net profit and loss

that impact on non cash transactions. In the section of operating cash flow adjust all the

transactions as per the formate such as:

Cash flows for Cross Dale Limited

for the year 31 December 2019

(b) The direct method use by the entity to presents every class of gross cash receipts and gross

cash payments. To calculate operating cash flows subdivision of the statement of cash flows

present all the transactions such as:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

8

acquisition and disposal of lengthy term assets and investments which is not cash

equivalents.

Financing activities: These activities are modifying with the equity capital and borrowing

structure of the business.

(a) The indirect method use by the business to manage all the accruals basis net profit and loss

that impact on non cash transactions. In the section of operating cash flow adjust all the

transactions as per the formate such as:

Cash flows for Cross Dale Limited

for the year 31 December 2019

(b) The direct method use by the entity to presents every class of gross cash receipts and gross

cash payments. To calculate operating cash flows subdivision of the statement of cash flows

present all the transactions such as:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash paid for other operating expenses 77

Interest paid 18

Income taxes paid 33

Net cash from operating activities 1210

Note:

Cash received from customers: It has been assumed that all the sales are transacted on

cash basis.

Cash paid to suppliers: In this section consider all the trade payables which is paid by

the owner to their suppliers.

Cash paid to employees: There are consisting of salaries which is paid by the owner to

their employees.

Interpretation: As per the above calculation it has been analysed that to prepare cash

flow apply direct and indirect method. After the application different answers from both method

from the indirect method get answer 475 and after application direct method get results 1210.

Thus both results are different and cash generated by operating activities (Sharma, Bhattacharya

and Thukral, 2019).

CONCLUSION

As per the above report it has been concluded that international financial reporting

mainly require for the big organisation which have subsidiaries in various nations. IFRS use by

the business to carry out consistency in accounting standards and practices. There are different

usage of IFRS and IAS to calculate the lease and carry out interest rate. Mostly companies using

IFRS for first time so it is required to apply changes in their accounting policies and standards. It

helps to set out the financial statements and helps businesses to presents the actual position of the

business effectively. There are making cash flow statement in direct and indirect method as per

the guidelines of IAS 7 and get that both amounts are different from both methods

9

Interest paid 18

Income taxes paid 33

Net cash from operating activities 1210

Note:

Cash received from customers: It has been assumed that all the sales are transacted on

cash basis.

Cash paid to suppliers: In this section consider all the trade payables which is paid by

the owner to their suppliers.

Cash paid to employees: There are consisting of salaries which is paid by the owner to

their employees.

Interpretation: As per the above calculation it has been analysed that to prepare cash

flow apply direct and indirect method. After the application different answers from both method

from the indirect method get answer 475 and after application direct method get results 1210.

Thus both results are different and cash generated by operating activities (Sharma, Bhattacharya

and Thukral, 2019).

CONCLUSION

As per the above report it has been concluded that international financial reporting

mainly require for the big organisation which have subsidiaries in various nations. IFRS use by

the business to carry out consistency in accounting standards and practices. There are different

usage of IFRS and IAS to calculate the lease and carry out interest rate. Mostly companies using

IFRS for first time so it is required to apply changes in their accounting policies and standards. It

helps to set out the financial statements and helps businesses to presents the actual position of the

business effectively. There are making cash flow statement in direct and indirect method as per

the guidelines of IAS 7 and get that both amounts are different from both methods

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.