International Financial Reporting Report - Finance Module, Semester 1

VerifiedAdded on 2022/12/28

|16

|3852

|28

Report

AI Summary

This report provides a comprehensive overview of international financial reporting. It begins with an introduction to international finance and its relevance to companies managing finances globally. Part A delves into the IASB's Conceptual Framework, explaining its purposes, underlying assumptions, and the concepts of capital maintenance. It also examines qualitative characteristics of financial statements and the concept of materiality. Question 2 addresses the first-time adoption of International Financial Reporting Standards (IFRS), including definitions of key terms and requirements of IFRS 1. Part B focuses on specific accounting topics, including lease accounting under IFRS 16, calculation of implicit interest rates, and accounting entries for residual values. It also includes the preparation of a cash flow statement in accordance with IAS 7. The report concludes with a discussion of the key concepts and principles of international financial reporting.

International

Financial

Reporting

Financial

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

QUESTION 1...................................................................................................................................4

IASB's Conceptual framework:...................................................................................................4

Explain the main purposes of the IASB’s Conceptual Framework document:...........................5

Discuss the assumption which (according to the IASB’s Conceptual Framework) underlies the

preparation of financial statements:.............................................................................................5

Explain the main concepts of capital maintenance, making references to the IASB’s

Conceptual Framework:...............................................................................................................6

Identify and explain the meanings of five qualitative characteristics and attributes of financial

statements including how they respectively make financial information useful as entrenched in

the IASB’s Conceptual Framework:............................................................................................6

Critically discuss how concept of materiality is fundamental to financial reporting:.................7

QUESTION 2...................................................................................................................................8

First time adoption for international financial reporting standard:..............................................8

explain the terms "first IFRS reporting period" and "date of transition":....................................8

what are the requirements of IFRS1 which must be satisfied by Prisca Plc when preparing

these financial statements:...........................................................................................................8

PART B............................................................................................................................................9

QUESTION 4...................................................................................................................................9

A. Lease:......................................................................................................................................9

B. Calculation for interest rate implicit for the lease:..................................................................9

B. Accounting entries when residual proper value is Zero:.......................................................10

QUESTION 6.................................................................................................................................10

Cash flow statements:................................................................................................................10

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

QUESTION 1...................................................................................................................................4

IASB's Conceptual framework:...................................................................................................4

Explain the main purposes of the IASB’s Conceptual Framework document:...........................5

Discuss the assumption which (according to the IASB’s Conceptual Framework) underlies the

preparation of financial statements:.............................................................................................5

Explain the main concepts of capital maintenance, making references to the IASB’s

Conceptual Framework:...............................................................................................................6

Identify and explain the meanings of five qualitative characteristics and attributes of financial

statements including how they respectively make financial information useful as entrenched in

the IASB’s Conceptual Framework:............................................................................................6

Critically discuss how concept of materiality is fundamental to financial reporting:.................7

QUESTION 2...................................................................................................................................8

First time adoption for international financial reporting standard:..............................................8

explain the terms "first IFRS reporting period" and "date of transition":....................................8

what are the requirements of IFRS1 which must be satisfied by Prisca Plc when preparing

these financial statements:...........................................................................................................8

PART B............................................................................................................................................9

QUESTION 4...................................................................................................................................9

A. Lease:......................................................................................................................................9

B. Calculation for interest rate implicit for the lease:..................................................................9

B. Accounting entries when residual proper value is Zero:.......................................................10

QUESTION 6.................................................................................................................................10

Cash flow statements:................................................................................................................10

A. The Statement of Cash Flows for Cross Dale Limited for the year to 31 December 2019 in

accordance with the requirements of IAS 7:..............................................................................10

B. the use of the direct method would give the same figure for ‘Cash generated from

operations’:................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

accordance with the requirements of IAS 7:..............................................................................10

B. the use of the direct method would give the same figure for ‘Cash generated from

operations’:................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

International finance is the study for monetary transactions for international countries.

International finance focuses for areas which includes foreign direct investment, currency

exchange rates. Globalisation makes international finance for the companies who are managing

financing in various countries. International finance is the branch for financial economics which

concerned with monetary, macroeconomics interrelations. It is the process for making relations

with various countries for the monetary terms. It helps companies for the business transactions

for expanding business. Finance is the process for managing funds for the company which gives

higher profitability for the businesses (Ajibade, Okeke, and Olurin, 2019). It defines as the

management for money which includes borrowing, lending, investing activities for the

businesses. This report is based for international finance for companies. This report includes

topics which are IASB's conceptual framework, first time adoption for international financial

reporting standard, inventories etc. Apart from this it includes lease, cash flow statements etc.

PART A

QUESTION 1

IASB's Conceptual framework:

The IASB's conceptual framework basis for its financial reporting standards for the

conceptual framework which founded for 2010. The conceptual framework develops for the

IASB which includes basic concepts which are act as the foundation for preparing financial

statements. The framework are also uses for guides in order to develop standards for itself which

are not use for the alternative for the financial reporting standards which are applicable for the

country. The IFRS framework which includes objectives for the financial statements,

assumptions for the financial statements, qualitative characteristics for the financial statements,

elements for financial statements, recognition for the elements for the financial statements,

measurement for the elements for the financial statements etc. the objectives for financial

statements are providing financial information. The useful views as the needs for the financial

statements for providing higher quality information for the users. The information should which

financial statements are provides which includes balance sheet, cash flow statements, income

statements etc. The users which includes for financial statements are lenders, investors,

employees, vendors, customers etc.

International finance is the study for monetary transactions for international countries.

International finance focuses for areas which includes foreign direct investment, currency

exchange rates. Globalisation makes international finance for the companies who are managing

financing in various countries. International finance is the branch for financial economics which

concerned with monetary, macroeconomics interrelations. It is the process for making relations

with various countries for the monetary terms. It helps companies for the business transactions

for expanding business. Finance is the process for managing funds for the company which gives

higher profitability for the businesses (Ajibade, Okeke, and Olurin, 2019). It defines as the

management for money which includes borrowing, lending, investing activities for the

businesses. This report is based for international finance for companies. This report includes

topics which are IASB's conceptual framework, first time adoption for international financial

reporting standard, inventories etc. Apart from this it includes lease, cash flow statements etc.

PART A

QUESTION 1

IASB's Conceptual framework:

The IASB's conceptual framework basis for its financial reporting standards for the

conceptual framework which founded for 2010. The conceptual framework develops for the

IASB which includes basic concepts which are act as the foundation for preparing financial

statements. The framework are also uses for guides in order to develop standards for itself which

are not use for the alternative for the financial reporting standards which are applicable for the

country. The IFRS framework which includes objectives for the financial statements,

assumptions for the financial statements, qualitative characteristics for the financial statements,

elements for financial statements, recognition for the elements for the financial statements,

measurement for the elements for the financial statements etc. the objectives for financial

statements are providing financial information. The useful views as the needs for the financial

statements for providing higher quality information for the users. The information should which

financial statements are provides which includes balance sheet, cash flow statements, income

statements etc. The users which includes for financial statements are lenders, investors,

employees, vendors, customers etc.

Explain the main purposes of the IASB’s Conceptual Framework document:

The purpose for the conceptual framework for assist the IASB for the development for

future IFRS's. The conceptual framework assists the preparing for financial statements for

developing accounting policies for transactions which not includes for the existing standards.

The IFRS framework which includes objectives for the financial statements, assumptions for the

financial statements, qualitative characteristics for the financial statements, elements for financial

statements, recognition for the elements for the financial statements, measurement for the

elements for the financial statements etc. the objectives for financial statements are providing

financial information. The conceptual framework IASB develops for the future accounting

standards. It includes accounting standards which related for presenting financial statements. It

includes preparing financial standards which are dealing for subject for accounting standards

(Cordery and Simpkins, 2016). It includes assist the users for interpreting the financial

statements which information includes for the financial statements which are prepare for the

compliance for the international financial reporting standards. It includes auditors for informing

the opinion for financial statements which are comply for international accounting standards. In

includes providing information about the approach for the approaches for formulating accounting

standards.

Discuss the assumption which (according to the IASB’s Conceptual Framework) underlies the

preparation of financial statements:

The financial frameworks are basis for the accrual basis. Accrual basis accounting it

shows that the effects for transactions, other events are recognise when the transactions are

happens, it is not for when the cash receives it includes when the transactions happens. Going

concern basis the financial statements are preparing for this accounting standard. It is the process

for business which includes the business will continue its activity. Financial statements are

prepare for the accounting standards. Financial statements includes cash flow statement, balance

sheet, income statements etc. These statements makes for the viewing company's financial

position. Cash flow statements which includes the transactions which are happens for the cash &

its equivalents. Balance sheet views as the liabilities, assets for the businesses (Stubbs and

Higgins, 2018). Income statements views as the profits for the expenses & income for the

businesses. These statements are prepares for the business transactions which shows financial

position for the business. It helps managers for making finance decisions. The elements for the

The purpose for the conceptual framework for assist the IASB for the development for

future IFRS's. The conceptual framework assists the preparing for financial statements for

developing accounting policies for transactions which not includes for the existing standards.

The IFRS framework which includes objectives for the financial statements, assumptions for the

financial statements, qualitative characteristics for the financial statements, elements for financial

statements, recognition for the elements for the financial statements, measurement for the

elements for the financial statements etc. the objectives for financial statements are providing

financial information. The conceptual framework IASB develops for the future accounting

standards. It includes accounting standards which related for presenting financial statements. It

includes preparing financial standards which are dealing for subject for accounting standards

(Cordery and Simpkins, 2016). It includes assist the users for interpreting the financial

statements which information includes for the financial statements which are prepare for the

compliance for the international financial reporting standards. It includes auditors for informing

the opinion for financial statements which are comply for international accounting standards. In

includes providing information about the approach for the approaches for formulating accounting

standards.

Discuss the assumption which (according to the IASB’s Conceptual Framework) underlies the

preparation of financial statements:

The financial frameworks are basis for the accrual basis. Accrual basis accounting it

shows that the effects for transactions, other events are recognise when the transactions are

happens, it is not for when the cash receives it includes when the transactions happens. Going

concern basis the financial statements are preparing for this accounting standard. It is the process

for business which includes the business will continue its activity. Financial statements are

prepare for the accounting standards. Financial statements includes cash flow statement, balance

sheet, income statements etc. These statements makes for the viewing company's financial

position. Cash flow statements which includes the transactions which are happens for the cash &

its equivalents. Balance sheet views as the liabilities, assets for the businesses (Stubbs and

Higgins, 2018). Income statements views as the profits for the expenses & income for the

businesses. These statements are prepares for the business transactions which shows financial

position for the business. It helps managers for making finance decisions. The elements for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statements includes equity, liabilities, assets, expenses, income etc. The equity are the

interest which happens for the assets for the company. The liability are obligations for the

company which company takes for running its activities. The assets are the resources which

manages by the company for activities which are happens in the business for the higher

profitability. The expenses are those which company pays for purchasing goods which gives

benefits for the company. The income are those which company receives for its activities which

it runs for the business (Dewi and Dewi, 2019). Equity, liabilities, assets are views for the

balance sheet financial statements. Expenses, income views for the income statement for the

financial statements.

Explain the main concepts of capital maintenance, making references to the IASB’s Conceptual

Framework:

The capital maintenance the company receives profits when the business receives its

costs associated for the business activities. The capital maintenance, when the inflation are

higher business needs for its assets valuations for adjustment in order to knows the achieved

capital maintenance. Capital maintenance helps business for running its activities. Capital

maintenance are the process which helps business for its transactions which helps business for

higher profitability. It has various concepts which includes physical capital concept, financial

capital concept etc. physical capital concept which includes profits which earns for the physical

productive capacity for the businesses (Tee and Kew, 2018). Financial capital concept which

includes profits earns for the financial value. The concept for capital maintenance are the

accounting model which uses for preparing financial statements. The conceptual framework

views the various accounting models which helps for preparing financial statements.

Identify and explain the meanings of five qualitative characteristics and attributes of financial

statements including how they respectively make financial information useful as

entrenched in the IASB’s Conceptual Framework:

Equity: Equity views for the financial statements, which is balance sheet. It shows

company's shares which it is liable for paying dividends. It has various terms which includes

shareholders, dividends etc. shareholders are who purchases company's shares for the receiving

interest. Dividends are which company are pays for its shareholders for the amount which

interest which happens for the assets for the company. The liability are obligations for the

company which company takes for running its activities. The assets are the resources which

manages by the company for activities which are happens in the business for the higher

profitability. The expenses are those which company pays for purchasing goods which gives

benefits for the company. The income are those which company receives for its activities which

it runs for the business (Dewi and Dewi, 2019). Equity, liabilities, assets are views for the

balance sheet financial statements. Expenses, income views for the income statement for the

financial statements.

Explain the main concepts of capital maintenance, making references to the IASB’s Conceptual

Framework:

The capital maintenance the company receives profits when the business receives its

costs associated for the business activities. The capital maintenance, when the inflation are

higher business needs for its assets valuations for adjustment in order to knows the achieved

capital maintenance. Capital maintenance helps business for running its activities. Capital

maintenance are the process which helps business for its transactions which helps business for

higher profitability. It has various concepts which includes physical capital concept, financial

capital concept etc. physical capital concept which includes profits which earns for the physical

productive capacity for the businesses (Tee and Kew, 2018). Financial capital concept which

includes profits earns for the financial value. The concept for capital maintenance are the

accounting model which uses for preparing financial statements. The conceptual framework

views the various accounting models which helps for preparing financial statements.

Identify and explain the meanings of five qualitative characteristics and attributes of financial

statements including how they respectively make financial information useful as

entrenched in the IASB’s Conceptual Framework:

Equity: Equity views for the financial statements, which is balance sheet. It shows

company's shares which it is liable for paying dividends. It has various terms which includes

shareholders, dividends etc. shareholders are who purchases company's shares for the receiving

interest. Dividends are which company are pays for its shareholders for the amount which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company receives for its shareholders for paying dividends to them for the company's

profitability.

Liabilities: Liabilities are the element which includes for the balance sheet. It describes

for the company which it has to pay for its debts.

Assets: Assets are the financial element which includes for the balance sheet. It includes

company's capital which it has for maintaining business activities. Assets includes various terms

as cash, banks, stock, furniture, building which company uses for achieving higher profitability.

Expenses: Expenses are those which company pays for running its activities for

purchasing material for its activities which helps it for achieving higher profitability .(Perkins,

2016).

Income: Income are those which company earns for its activities, it runs activities for

achieving higher profitability which gives higher benefits for the businesses (Erin and Oduwole,

2018).

Critically discuss how concept of materiality is fundamental to financial reporting:

Materiality concept is the process which views accounting standard which views the

data's for the decisions which are taken for the users. It views as when information is misleading

which impacts the decisions which the users use when preparing financial statements. It is the

concept for financial reporting which needs for the company for the financial statements. In

finance, materiality concept is the situation where the financial information for the company

consider for the material for the point of view in order to preparing financial statements.

Materiality concept is the principle for accounting which views transactions, items which makes

impacts for the financial statements should accounting for using GAAP exclusive. The

materiality concept for accounting views that items are properly recorded for the financial

statements. This concept for accounting helps businesses for ignoring another accounting

principle those which principles has not impact for the financial statements for the company.

Materiality principle for accounting which is about relevance for information which are record

for the financial information. This concept uses for the accountant as they are preparing financial

statements (Kalashyan, 2017). The concept for materiality works for filter through which

management shifts information. The objectives for makes suers that financial information which

influence investors decisions which includes financial statements.

profitability.

Liabilities: Liabilities are the element which includes for the balance sheet. It describes

for the company which it has to pay for its debts.

Assets: Assets are the financial element which includes for the balance sheet. It includes

company's capital which it has for maintaining business activities. Assets includes various terms

as cash, banks, stock, furniture, building which company uses for achieving higher profitability.

Expenses: Expenses are those which company pays for running its activities for

purchasing material for its activities which helps it for achieving higher profitability .(Perkins,

2016).

Income: Income are those which company earns for its activities, it runs activities for

achieving higher profitability which gives higher benefits for the businesses (Erin and Oduwole,

2018).

Critically discuss how concept of materiality is fundamental to financial reporting:

Materiality concept is the process which views accounting standard which views the

data's for the decisions which are taken for the users. It views as when information is misleading

which impacts the decisions which the users use when preparing financial statements. It is the

concept for financial reporting which needs for the company for the financial statements. In

finance, materiality concept is the situation where the financial information for the company

consider for the material for the point of view in order to preparing financial statements.

Materiality concept is the principle for accounting which views transactions, items which makes

impacts for the financial statements should accounting for using GAAP exclusive. The

materiality concept for accounting views that items are properly recorded for the financial

statements. This concept for accounting helps businesses for ignoring another accounting

principle those which principles has not impact for the financial statements for the company.

Materiality principle for accounting which is about relevance for information which are record

for the financial information. This concept uses for the accountant as they are preparing financial

statements (Kalashyan, 2017). The concept for materiality works for filter through which

management shifts information. The objectives for makes suers that financial information which

influence investors decisions which includes financial statements.

QUESTION 2

First time adoption for international financial reporting standard:

explain the terms "first IFRS reporting period" and "date of transition":

First time adoption for international financial reporting standards is the international

financial reporting standard which are issue for the international accounting standards board. It

sets needs for the preparation for financial statements in order to ensure that they contains high

quality information. The date for transition for IFRS is April 1 2015. first time adoption for

international financial reporting standards needs the company which adopts IFRD for the first

time in order to apply IFRS retrospectively. The objectives for IFRS which ensure that the

company's first IFRS financial statements has higher quality information which is transparent for

users, provides suitable starting point for accounting for international financial reporting

standards, manages for the costs which does not exceed the benefits (Nobesand and Stadler,

2018). First time adoption for international financial reporting standard sets procedure which the

company follows when it accepts IFRSs for the first time for basis for preparing financial

statements.

what are the requirements of IFRS1 which must be satisfied by Prisca Plc when preparing these

financial statements:

International financial reporting standard makes common rules for financial statements

which are consistent, transparent, comparable for the various countries. IFRS are issues for the

international accounting standards board. They specify for company's maintenance their account

s. IFRS establishes for creating accounting language for businesses, their financial statements are

consistent for the company for company. It sets standards for accounting which helps company's

for making financial statements for the businesses (Loghin, 2016).

First time adoption for international financial reporting standard:

explain the terms "first IFRS reporting period" and "date of transition":

First time adoption for international financial reporting standards is the international

financial reporting standard which are issue for the international accounting standards board. It

sets needs for the preparation for financial statements in order to ensure that they contains high

quality information. The date for transition for IFRS is April 1 2015. first time adoption for

international financial reporting standards needs the company which adopts IFRD for the first

time in order to apply IFRS retrospectively. The objectives for IFRS which ensure that the

company's first IFRS financial statements has higher quality information which is transparent for

users, provides suitable starting point for accounting for international financial reporting

standards, manages for the costs which does not exceed the benefits (Nobesand and Stadler,

2018). First time adoption for international financial reporting standard sets procedure which the

company follows when it accepts IFRSs for the first time for basis for preparing financial

statements.

what are the requirements of IFRS1 which must be satisfied by Prisca Plc when preparing these

financial statements:

International financial reporting standard makes common rules for financial statements

which are consistent, transparent, comparable for the various countries. IFRS are issues for the

international accounting standards board. They specify for company's maintenance their account

s. IFRS establishes for creating accounting language for businesses, their financial statements are

consistent for the company for company. It sets standards for accounting which helps company's

for making financial statements for the businesses (Loghin, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

QUESTION 4

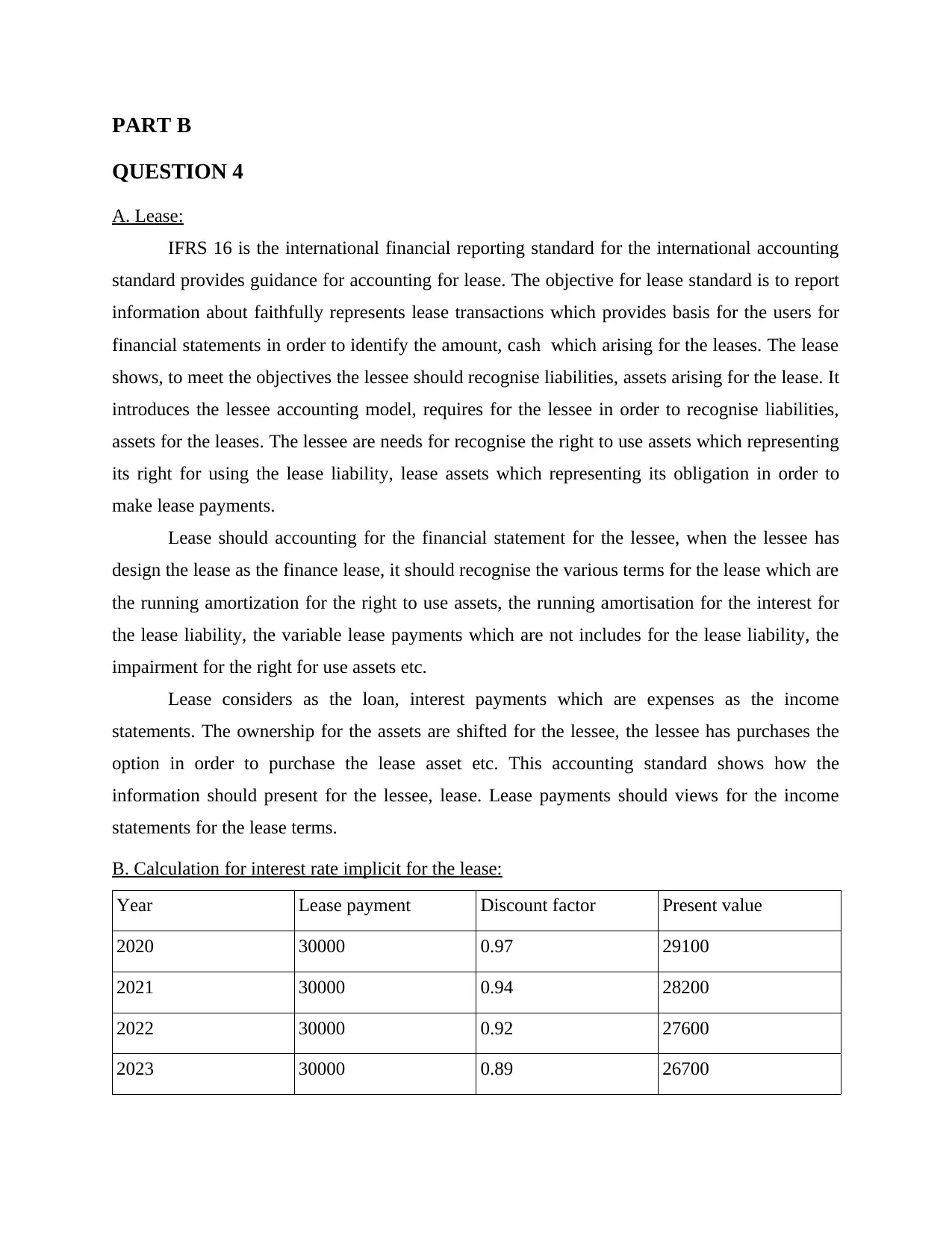

A. Lease:

IFRS 16 is the international financial reporting standard for the international accounting

standard provides guidance for accounting for lease. The objective for lease standard is to report

information about faithfully represents lease transactions which provides basis for the users for

financial statements in order to identify the amount, cash which arising for the leases. The lease

shows, to meet the objectives the lessee should recognise liabilities, assets arising for the lease. It

introduces the lessee accounting model, requires for the lessee in order to recognise liabilities,

assets for the leases. The lessee are needs for recognise the right to use assets which representing

its right for using the lease liability, lease assets which representing its obligation in order to

make lease payments.

Lease should accounting for the financial statement for the lessee, when the lessee has

design the lease as the finance lease, it should recognise the various terms for the lease which are

the running amortization for the right to use assets, the running amortisation for the interest for

the lease liability, the variable lease payments which are not includes for the lease liability, the

impairment for the right for use assets etc.

Lease considers as the loan, interest payments which are expenses as the income

statements. The ownership for the assets are shifted for the lessee, the lessee has purchases the

option in order to purchase the lease asset etc. This accounting standard shows how the

information should present for the lessee, lease. Lease payments should views for the income

statements for the lease terms.

B. Calculation for interest rate implicit for the lease:

Year Lease payment Discount factor Present value

2020 30000 0.97 29100

2021 30000 0.94 28200

2022 30000 0.92 27600

2023 30000 0.89 26700

QUESTION 4

A. Lease:

IFRS 16 is the international financial reporting standard for the international accounting

standard provides guidance for accounting for lease. The objective for lease standard is to report

information about faithfully represents lease transactions which provides basis for the users for

financial statements in order to identify the amount, cash which arising for the leases. The lease

shows, to meet the objectives the lessee should recognise liabilities, assets arising for the lease. It

introduces the lessee accounting model, requires for the lessee in order to recognise liabilities,

assets for the leases. The lessee are needs for recognise the right to use assets which representing

its right for using the lease liability, lease assets which representing its obligation in order to

make lease payments.

Lease should accounting for the financial statement for the lessee, when the lessee has

design the lease as the finance lease, it should recognise the various terms for the lease which are

the running amortization for the right to use assets, the running amortisation for the interest for

the lease liability, the variable lease payments which are not includes for the lease liability, the

impairment for the right for use assets etc.

Lease considers as the loan, interest payments which are expenses as the income

statements. The ownership for the assets are shifted for the lessee, the lessee has purchases the

option in order to purchase the lease asset etc. This accounting standard shows how the

information should present for the lessee, lease. Lease payments should views for the income

statements for the lease terms.

B. Calculation for interest rate implicit for the lease:

Year Lease payment Discount factor Present value

2020 30000 0.97 29100

2021 30000 0.94 28200

2022 30000 0.92 27600

2023 30000 0.89 26700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

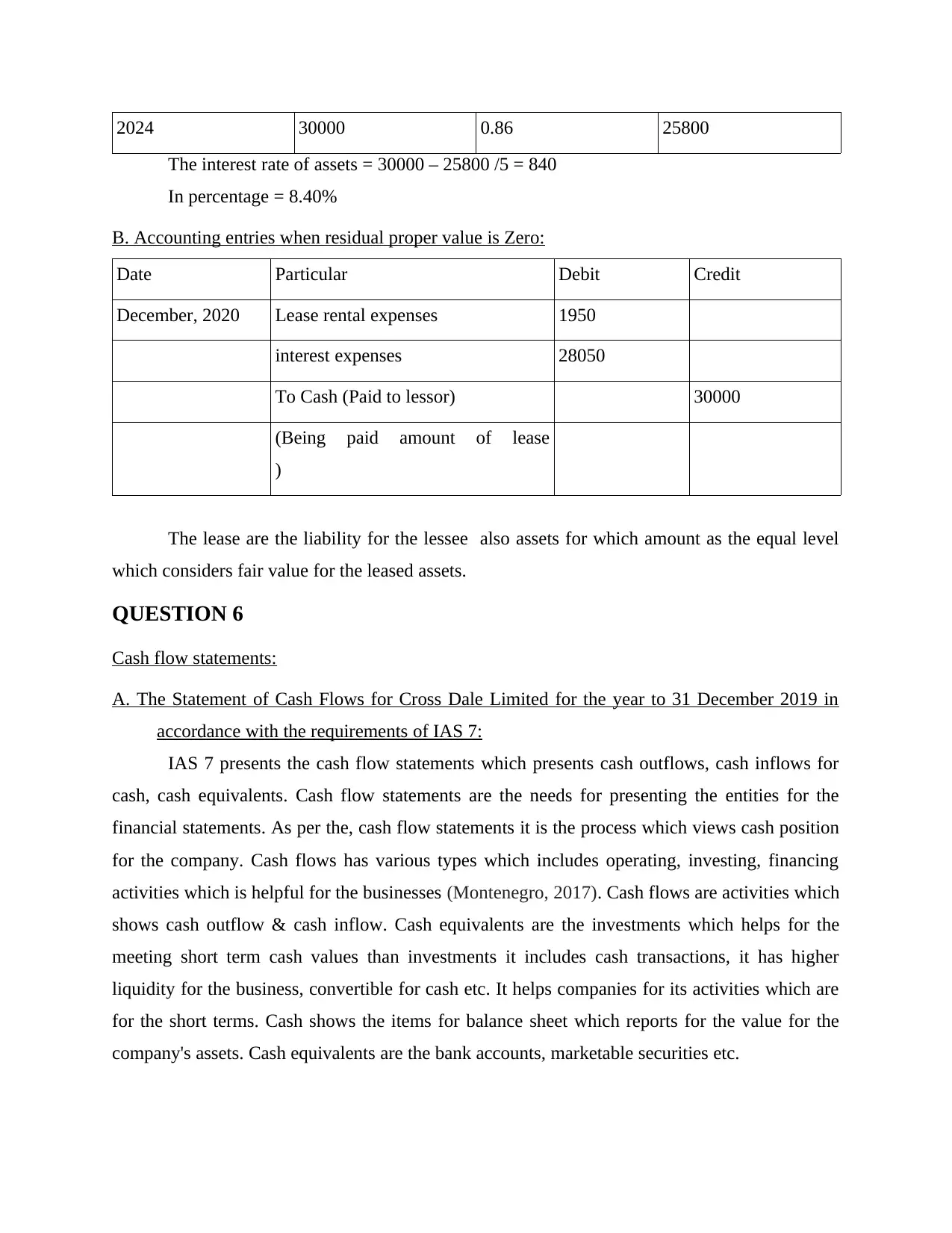

2024 30000 0.86 25800

The interest rate of assets = 30000 – 25800 /5 = 840

In percentage = 8.40%

B. Accounting entries when residual proper value is Zero:

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

interest expenses 28050

To Cash (Paid to lessor) 30000

(Being paid amount of lease

)

The lease are the liability for the lessee also assets for which amount as the equal level

which considers fair value for the leased assets.

QUESTION 6

Cash flow statements:

A. The Statement of Cash Flows for Cross Dale Limited for the year to 31 December 2019 in

accordance with the requirements of IAS 7:

IAS 7 presents the cash flow statements which presents cash outflows, cash inflows for

cash, cash equivalents. Cash flow statements are the needs for presenting the entities for the

financial statements. As per the, cash flow statements it is the process which views cash position

for the company. Cash flows has various types which includes operating, investing, financing

activities which is helpful for the businesses (Montenegro, 2017). Cash flows are activities which

shows cash outflow & cash inflow. Cash equivalents are the investments which helps for the

meeting short term cash values than investments it includes cash transactions, it has higher

liquidity for the business, convertible for cash etc. It helps companies for its activities which are

for the short terms. Cash shows the items for balance sheet which reports for the value for the

company's assets. Cash equivalents are the bank accounts, marketable securities etc.

The interest rate of assets = 30000 – 25800 /5 = 840

In percentage = 8.40%

B. Accounting entries when residual proper value is Zero:

Date Particular Debit Credit

December, 2020 Lease rental expenses 1950

interest expenses 28050

To Cash (Paid to lessor) 30000

(Being paid amount of lease

)

The lease are the liability for the lessee also assets for which amount as the equal level

which considers fair value for the leased assets.

QUESTION 6

Cash flow statements:

A. The Statement of Cash Flows for Cross Dale Limited for the year to 31 December 2019 in

accordance with the requirements of IAS 7:

IAS 7 presents the cash flow statements which presents cash outflows, cash inflows for

cash, cash equivalents. Cash flow statements are the needs for presenting the entities for the

financial statements. As per the, cash flow statements it is the process which views cash position

for the company. Cash flows has various types which includes operating, investing, financing

activities which is helpful for the businesses (Montenegro, 2017). Cash flows are activities which

shows cash outflow & cash inflow. Cash equivalents are the investments which helps for the

meeting short term cash values than investments it includes cash transactions, it has higher

liquidity for the business, convertible for cash etc. It helps companies for its activities which are

for the short terms. Cash shows the items for balance sheet which reports for the value for the

company's assets. Cash equivalents are the bank accounts, marketable securities etc.

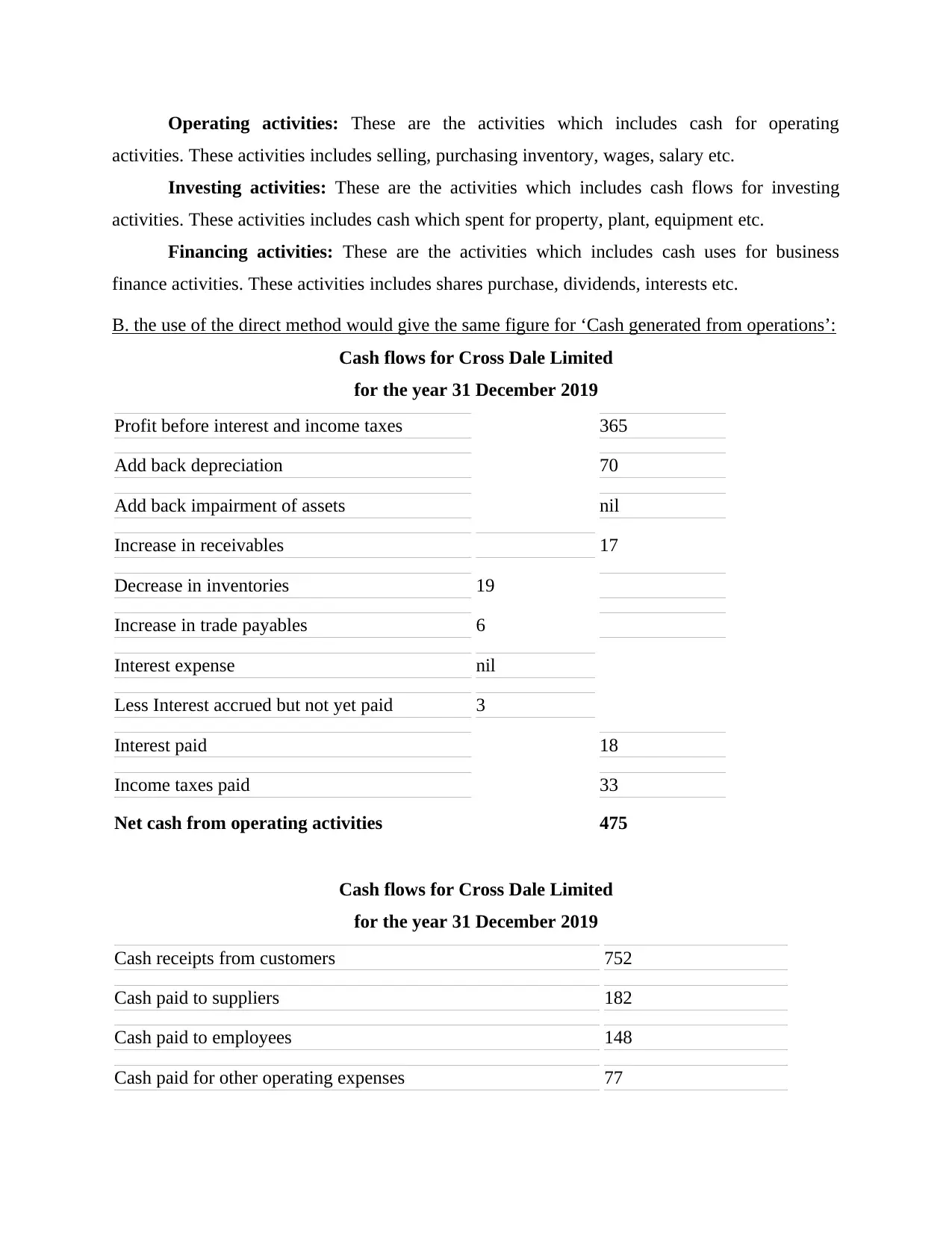

Operating activities: These are the activities which includes cash for operating

activities. These activities includes selling, purchasing inventory, wages, salary etc.

Investing activities: These are the activities which includes cash flows for investing

activities. These activities includes cash which spent for property, plant, equipment etc.

Financing activities: These are the activities which includes cash uses for business

finance activities. These activities includes shares purchase, dividends, interests etc.

B. the use of the direct method would give the same figure for ‘Cash generated from operations’:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Profit before interest and income taxes 365

Add back depreciation 70

Add back impairment of assets nil

Increase in receivables 17

Decrease in inventories 19

Increase in trade payables 6

Interest expense nil

Less Interest accrued but not yet paid 3

Interest paid 18

Income taxes paid 33

Net cash from operating activities 475

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

Cash paid for other operating expenses 77

activities. These activities includes selling, purchasing inventory, wages, salary etc.

Investing activities: These are the activities which includes cash flows for investing

activities. These activities includes cash which spent for property, plant, equipment etc.

Financing activities: These are the activities which includes cash uses for business

finance activities. These activities includes shares purchase, dividends, interests etc.

B. the use of the direct method would give the same figure for ‘Cash generated from operations’:

Cash flows for Cross Dale Limited

for the year 31 December 2019

Profit before interest and income taxes 365

Add back depreciation 70

Add back impairment of assets nil

Increase in receivables 17

Decrease in inventories 19

Increase in trade payables 6

Interest expense nil

Less Interest accrued but not yet paid 3

Interest paid 18

Income taxes paid 33

Net cash from operating activities 475

Cash flows for Cross Dale Limited

for the year 31 December 2019

Cash receipts from customers 752

Cash paid to suppliers 182

Cash paid to employees 148

Cash paid for other operating expenses 77

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.