International Financial Reporting: Standards, Compliance & Analysis

VerifiedAdded on 2023/06/13

|24

|5079

|421

Report

AI Summary

This report provides a comprehensive overview of international financial reporting, focusing on its context, purpose, and key principles as defined by conceptual and regulatory frameworks. It identifies the main stakeholders of an organization and analyzes how they benefit from financial information. The report explains the difference between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), critically evaluating the benefits of IFRS. It also identifies the varying degrees of compliance with IFRS by organizations across the world and the factors in a nation which may impact compliance. The financial information of Morrisons is analyzed and interpreted in the appendix. The report highlights the auditing models used by businesses, emphasizing the value of financial reporting for meeting organizational objectives and growth. Desklib offers a platform to access this and similar solved assignments for students.

Unit Number and

Title

Unit 13 Financial Reporting

Project Title International Financial

Reporting

Title

Unit 13 Financial Reporting

Project Title International Financial

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial reporting helps the business in the utilisation of the business assets and the

different funds which are present with the business. This reporting helps the business to

communicate the various information to the diversified stakeholders. The following

report provides information related to the financial reporting and how the different

organisations use it to provide the information related to the business. It gives

information about the different stakeholders that are there for a business. It also identifies

the various degrees of compliance which impacts the different nations and the reporting

done in these nations.

Financial reporting helps the business in the utilisation of the business assets and the

different funds which are present with the business. This reporting helps the business to

communicate the various information to the diversified stakeholders. The following

report provides information related to the financial reporting and how the different

organisations use it to provide the information related to the business. It gives

information about the different stakeholders that are there for a business. It also identifies

the various degrees of compliance which impacts the different nations and the reporting

done in these nations.

Table of Content

1.0 Introduction 3

2.0 An outline of the context and purpose of financial reporting 3

3.0 A critical examination of the key principles of conceptual and regulatory

frameworks, their purpose and why they are required 5

4.0 Identification of the main stakeholders of an organisation and analysis of how

they benefit from financial information 7

5.0 An analysis of the value of financial reporting for meeting organisational

objectives and growth 8

6.0 An explanation of the difference between International Accounting Standards

(IAS) and International Financial Reporting Standards (IFRS) and a critical

evaluation of the benefits of IFRS 8

6. Identification of the varying degrees of compliance with IFRS by organisations

across the world and the factors in a nation which may impact compliance

9

7.0 Conclusions 11

References 12

Appendix 1.0 14

Appendix 2.0 15

1.0 Introduction 3

2.0 An outline of the context and purpose of financial reporting 3

3.0 A critical examination of the key principles of conceptual and regulatory

frameworks, their purpose and why they are required 5

4.0 Identification of the main stakeholders of an organisation and analysis of how

they benefit from financial information 7

5.0 An analysis of the value of financial reporting for meeting organisational

objectives and growth 8

6.0 An explanation of the difference between International Accounting Standards

(IAS) and International Financial Reporting Standards (IFRS) and a critical

evaluation of the benefits of IFRS 8

6. Identification of the varying degrees of compliance with IFRS by organisations

across the world and the factors in a nation which may impact compliance

9

7.0 Conclusions 11

References 12

Appendix 1.0 14

Appendix 2.0 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.0 Introduction

Financial Reporting includes the exposure of monetary data to the different partners

about the monetary execution and monetary place of the association for a predetermined

timeframe. Monetary announcing contains solid and significant data which are involved

by numerous partners for different purposes. The financial reporting needs to be done in

accordance with legislation and regulation of the company. Financial reporting helps the

business in the utilisation of the business assets and the different funds which are present

with the business. This reporting helps the business to communicate the various

information to the diversified stakeholders (Bajra, and Čadež, 2018). The international

financial reporting standards are general guidelines which are followed by the businesses

in and around the world. These principles provides insights to the business as how they

can use the accounting in their day-to-day business operations and how they can report

the financial results obtained by the businesses to its different stakeholders. The report

highlights the company selected for this report is Morrisons. The financial information of

the business is analysed and interpreted in the attached appendix. The report highlights

the detailed concept related to the international reporting standards. The key principles

and the their purpose is also examined in report the last part of the report highlights the

auditing models used by the businesses.

2.0 An outline of the context and purpose of financial

reporting

It is the accounting standard practice that disclose the financial information by using

financial statements of a company. International financial reporting evaluates the

performance over a particular period. This report helps the management in making good

business decisions by considering the facts based on company's financial health.

Investors and banks also use these financial reports in order to decide whether they want

to make investment or grant loan to the company or not, they are easily comparable

around the world (Baral, and Ali, 2018). These reports are also audited by the

governments, firms and Chartered Accountants to check the accuracy. International

Financial Reporting includes the exposure of monetary data to the different partners

about the monetary execution and monetary place of the association for a predetermined

timeframe. Monetary announcing contains solid and significant data which are involved

by numerous partners for different purposes. The financial reporting needs to be done in

accordance with legislation and regulation of the company. Financial reporting helps the

business in the utilisation of the business assets and the different funds which are present

with the business. This reporting helps the business to communicate the various

information to the diversified stakeholders (Bajra, and Čadež, 2018). The international

financial reporting standards are general guidelines which are followed by the businesses

in and around the world. These principles provides insights to the business as how they

can use the accounting in their day-to-day business operations and how they can report

the financial results obtained by the businesses to its different stakeholders. The report

highlights the company selected for this report is Morrisons. The financial information of

the business is analysed and interpreted in the attached appendix. The report highlights

the detailed concept related to the international reporting standards. The key principles

and the their purpose is also examined in report the last part of the report highlights the

auditing models used by the businesses.

2.0 An outline of the context and purpose of financial

reporting

It is the accounting standard practice that disclose the financial information by using

financial statements of a company. International financial reporting evaluates the

performance over a particular period. This report helps the management in making good

business decisions by considering the facts based on company's financial health.

Investors and banks also use these financial reports in order to decide whether they want

to make investment or grant loan to the company or not, they are easily comparable

around the world (Baral, and Ali, 2018). These reports are also audited by the

governments, firms and Chartered Accountants to check the accuracy. International

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Reports Standards are the set of rules, so that the financial statements prepared

brings consistency, transparency and can be comparable all around the globe. These were

created so that the financial statements can have common accounting language and can

serve with the reliable and consistent information from company to company and country

to country (Brukhanskyi, and Spilnyk, 2019). There is a advantage to multinational

companies as its access to international finance will become easier and there will be more

efficiency in accounts department. Better comparisons between the different business

entities are required because decisions of investors will be based on the worldwide

availability of investments. It will bring consistency and reliability between entities and

different regions. Tax liabilities can be easier to calculate. It had certain disadvantages as

well, like there are different legal, political, social systems so it was difficult to introduce.

Purpose of International Financial Reporting-

To bring uniformity – The purpose is to create a common flow between the

different countries so that the entities can prepare their financial statements on

same platform. IFRS ensures that entities follow same guidelines and adopt the

universal way of preparing the financial reports.

To prepare reliable financial records- By following the IFRS, there will be the

uniformity between the nations. The quality of accuracy, reliability will make

easy for the investors to rely on the financial statements of different entities as

they will work under the same guidelines.

To ensure transparency, consistency and flexibility- The transparency in

reporting the accounting practices helps in easy comparison of financial

statements of different entities across the nations (Bu, Tang, and Wu, 2019). This

comparison helps the investors and creditors to identify the risks before investing

and granting loan to the entity.

To ensure easy foreign trade and investment- The consistency, accuracy will lead

to the better understanding of the financial statements of different companies

across the globe. Foreign trade and investment requires full disclosure of relevant

brings consistency, transparency and can be comparable all around the globe. These were

created so that the financial statements can have common accounting language and can

serve with the reliable and consistent information from company to company and country

to country (Brukhanskyi, and Spilnyk, 2019). There is a advantage to multinational

companies as its access to international finance will become easier and there will be more

efficiency in accounts department. Better comparisons between the different business

entities are required because decisions of investors will be based on the worldwide

availability of investments. It will bring consistency and reliability between entities and

different regions. Tax liabilities can be easier to calculate. It had certain disadvantages as

well, like there are different legal, political, social systems so it was difficult to introduce.

Purpose of International Financial Reporting-

To bring uniformity – The purpose is to create a common flow between the

different countries so that the entities can prepare their financial statements on

same platform. IFRS ensures that entities follow same guidelines and adopt the

universal way of preparing the financial reports.

To prepare reliable financial records- By following the IFRS, there will be the

uniformity between the nations. The quality of accuracy, reliability will make

easy for the investors to rely on the financial statements of different entities as

they will work under the same guidelines.

To ensure transparency, consistency and flexibility- The transparency in

reporting the accounting practices helps in easy comparison of financial

statements of different entities across the nations (Bu, Tang, and Wu, 2019). This

comparison helps the investors and creditors to identify the risks before investing

and granting loan to the entity.

To ensure easy foreign trade and investment- The consistency, accuracy will lead

to the better understanding of the financial statements of different companies

across the globe. Foreign trade and investment requires full disclosure of relevant

information to the investors. Hence investors will be able to take effective

decision regarding the foreign investments.

To ensure the improvement in the economy- Again, because of the transparency

and accuracy factors, investors are open to invest globally in the companies

because of the IFRS implementation (Dawood. and AL-Massoodi, 2019). This

creditability welcomes the foreign investments and thus there is way for economic

improvement.

In short, the purpose of International Financial Reporting Standards is to bring the

efficiency, effectiveness, and accuracy in the reporting of financial statements across the

globe.

3.0 A critical examination of the key principles of conceptual

and regulatory frameworks, their purpose and why they

are required

Accounting, in a broad sense, is the process of recording transactions and occurrences in

an operational business with the aim of gathering and disseminating financial information

necessary for the entity's operations to run smoothly. It is the most common way of

recording, breaking down, ordering, summing up, conveying, and deciphering monetary

data about business in total and exhaustively, mirroring all exchanges including the

receipt, move, and demeanor of business assets and property, as indicated by Oshisami

and senior member refered to in Oshisami (1992). The goals are to show that transitions

are proper and follow set norms, to demonstrate accountability for government resource

stewardship, and to offer relevant information for excellent control and efficient

administration of government activities (DWIKATRESNA, 2018).

The point of broadly useful monetary detailing is to give monetary data about the

revealing organization that is helpful to current and planned financial backers, loan

specialists, and different leasers while settling on asset related choices.

These choices include: (a) purchasing, selling, or holding offers and obligation

instruments; (b) allowing or settling advances and different types of credit; and (c)

practicing casting a ballot rights or in any case impacting the board's activities

decision regarding the foreign investments.

To ensure the improvement in the economy- Again, because of the transparency

and accuracy factors, investors are open to invest globally in the companies

because of the IFRS implementation (Dawood. and AL-Massoodi, 2019). This

creditability welcomes the foreign investments and thus there is way for economic

improvement.

In short, the purpose of International Financial Reporting Standards is to bring the

efficiency, effectiveness, and accuracy in the reporting of financial statements across the

globe.

3.0 A critical examination of the key principles of conceptual

and regulatory frameworks, their purpose and why they

are required

Accounting, in a broad sense, is the process of recording transactions and occurrences in

an operational business with the aim of gathering and disseminating financial information

necessary for the entity's operations to run smoothly. It is the most common way of

recording, breaking down, ordering, summing up, conveying, and deciphering monetary

data about business in total and exhaustively, mirroring all exchanges including the

receipt, move, and demeanor of business assets and property, as indicated by Oshisami

and senior member refered to in Oshisami (1992). The goals are to show that transitions

are proper and follow set norms, to demonstrate accountability for government resource

stewardship, and to offer relevant information for excellent control and efficient

administration of government activities (DWIKATRESNA, 2018).

The point of broadly useful monetary detailing is to give monetary data about the

revealing organization that is helpful to current and planned financial backers, loan

specialists, and different leasers while settling on asset related choices.

These choices include: (a) purchasing, selling, or holding offers and obligation

instruments; (b) allowing or settling advances and different types of credit; and (c)

practicing casting a ballot rights or in any case impacting the board's activities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

influencing the substance's financial assets. General purpose monetary reports give data

on an announcing substance's monetary status, which incorporates data about the

element's financial assets and cases against it. Monetary reports additionally give

subtleties on the effect of exchanges and different occasions on an announcing element's

financial assets and cases. The two kinds of information are valuable while making

decisions concerning how to designate assets to a substance. Rather than reasonable

portrayals, monetary reports depend principally on evaluations, decisions, and models.

The ideas that help the appraisals, decisions, and models are laid forward in the

Conceptual Framework (FADILLAH, 2018). The Board's and monetary report preparers'

definitive objective is to accomplish the standards.

The Conceptual Framework's notion of flawless monetary revealing is probably not going

to be acknowledged completely, essentially not sooner rather than later, on the grounds

that it requires some investment to ingest, adjust, and apply better approaches for

examining exchanges and different events. Monetary announcing, then again, should

have an objective as a main priority assuming it is to improve and turn out to be more

significant. Following are some of the accounting principles that are used in the

framework which aids the businesses to prepare their financial statements:

Historical Cost Principle: It requires businesses to keep track of the amount they

paid for wares, administrations, and capital resources. Resources are consequently

left on the asset report at their verifiable worth, unadjusted for market varieties.

Revenue Recognition Principle: Organizations should report pay when it is

procured rather than when it is gotten. The accumulation underpinning of

bookkeeping gives a more exact image of the period's monetary occasions.

Full Disclosure Principle: orders that any data that could seriously affect a budget

summary client's judgment with respect to the firm be remembered for the fiscal

report references (Golden, 2019). This wipes out the chance of future enterprises

hiding significant data with respect to bookkeeping strategies or known

possibilities.

Objectivity Principle: Financial statements, accounting records, and financial data

in general should be unbiased and impartial. The purpose of financial statements

is to explain the company's financial status, not to compel end users to take

on an announcing substance's monetary status, which incorporates data about the

element's financial assets and cases against it. Monetary reports additionally give

subtleties on the effect of exchanges and different occasions on an announcing element's

financial assets and cases. The two kinds of information are valuable while making

decisions concerning how to designate assets to a substance. Rather than reasonable

portrayals, monetary reports depend principally on evaluations, decisions, and models.

The ideas that help the appraisals, decisions, and models are laid forward in the

Conceptual Framework (FADILLAH, 2018). The Board's and monetary report preparers'

definitive objective is to accomplish the standards.

The Conceptual Framework's notion of flawless monetary revealing is probably not going

to be acknowledged completely, essentially not sooner rather than later, on the grounds

that it requires some investment to ingest, adjust, and apply better approaches for

examining exchanges and different events. Monetary announcing, then again, should

have an objective as a main priority assuming it is to improve and turn out to be more

significant. Following are some of the accounting principles that are used in the

framework which aids the businesses to prepare their financial statements:

Historical Cost Principle: It requires businesses to keep track of the amount they

paid for wares, administrations, and capital resources. Resources are consequently

left on the asset report at their verifiable worth, unadjusted for market varieties.

Revenue Recognition Principle: Organizations should report pay when it is

procured rather than when it is gotten. The accumulation underpinning of

bookkeeping gives a more exact image of the period's monetary occasions.

Full Disclosure Principle: orders that any data that could seriously affect a budget

summary client's judgment with respect to the firm be remembered for the fiscal

report references (Golden, 2019). This wipes out the chance of future enterprises

hiding significant data with respect to bookkeeping strategies or known

possibilities.

Objectivity Principle: Financial statements, accounting records, and financial data

in general should be unbiased and impartial. The purpose of financial statements

is to explain the company's financial status, not to compel end users to take

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

certain actions.

4.0 Identification of the main stakeholders of an organisation

and analysis of how they benefit from financial

information

Any stakeholder, including entrepreneurs, exchange banks, loan specialists, financial

backers, trade guilds, laborers, experts, and anybody with a premium in the organization,

can direct a budget summary assessment, This is Because investigators' inclinations

differs, the kind of examination will shift contingent upon the point of the investigation.

A technique often utilized by one analyst may not fulfil the objective of other analysts

(Hadiyanto, Puspitasari, and Ghani, 2018). Following is a detailed list about same:

Board of directors: They would utilize financial statements to evaluate

management's performance and the company's overall success. Financial reports

are also required for the proper running of the organization by managers and

owners in order to make critical business choices. The present debt-to-equity, is

basic in deciding how much long-haul capital that will be expected to settle on

specific business choices. Shareholders: The interest of the shareholders will be

on how the firm is using the money they have invested, as well as whether it is

profitable or not (Hu, Song, and Guo, 2019). If it's lucrative, they'll want a return

in the form of dividends, therefore they'll be worried about the amount of

dividends paid out year after year, as well as the possibility for future profits and

dividends.

Creditors: The monetary reports of a firm, for example, the monetary record and

pay explanation, will plainly bear some significance with its exchange leasers and

providers. Such partners will be stressed over whether the firm can pay for its

buys from them consistently, subsequently they will watch out for the

organization's money position - its liquidity.

Competitors: Contenders will be keen on a contender's monetary execution in a

similar modern area to see whether they are preferable or more regrettable over

their own, assuming they have acquainted new things with the market, and how

4.0 Identification of the main stakeholders of an organisation

and analysis of how they benefit from financial

information

Any stakeholder, including entrepreneurs, exchange banks, loan specialists, financial

backers, trade guilds, laborers, experts, and anybody with a premium in the organization,

can direct a budget summary assessment, This is Because investigators' inclinations

differs, the kind of examination will shift contingent upon the point of the investigation.

A technique often utilized by one analyst may not fulfil the objective of other analysts

(Hadiyanto, Puspitasari, and Ghani, 2018). Following is a detailed list about same:

Board of directors: They would utilize financial statements to evaluate

management's performance and the company's overall success. Financial reports

are also required for the proper running of the organization by managers and

owners in order to make critical business choices. The present debt-to-equity, is

basic in deciding how much long-haul capital that will be expected to settle on

specific business choices. Shareholders: The interest of the shareholders will be

on how the firm is using the money they have invested, as well as whether it is

profitable or not (Hu, Song, and Guo, 2019). If it's lucrative, they'll want a return

in the form of dividends, therefore they'll be worried about the amount of

dividends paid out year after year, as well as the possibility for future profits and

dividends.

Creditors: The monetary reports of a firm, for example, the monetary record and

pay explanation, will plainly bear some significance with its exchange leasers and

providers. Such partners will be stressed over whether the firm can pay for its

buys from them consistently, subsequently they will watch out for the

organization's money position - its liquidity.

Competitors: Contenders will be keen on a contender's monetary execution in a

similar modern area to see whether they are preferable or more regrettable over

their own, assuming they have acquainted new things with the market, and how

well they have performed (Jaber, 2021).

Customers: These individuals would be interested in the company's ability to

continue as a reliable source of supplies in the future, and would look for any

factors that may hinder this, such as production issues, sales price rises, and so on.

5.0 An analysis of the value of financial reporting for meeting

organisational objectives and growth

Financial analysis and reporting are solid, steady, and by and large open strategies

for scattering essential monetary information across the organization. Things could

quickly go to pieces assuming your monetary bits of knowledge or information are

disconnected. Basically, this by itself explains what monetary detailing and investigation

are. Financial analysis and reporting can help you answer a slew of important questions

about your company's finances, providing both internal and external stakeholders with an

accurate, complete picture of the strategic and operational metrics they need to make

choices and take action (Kuběnka, Honková, Sejkora, and Jedlička, 2018).

Financial reports should be as accurate as possible; in any event, any

administration reports (and subsequent choices) based on them would be on shaky

footing. This is where businesses may run into troubles if they rely on antiquated

practises (such as a single large bookkeeping page with a few clients) rather than

embracing financial dashboards to reap the benefits of financial reporting.

Financial reporting is important because it allows consumers of financial data to

follow trends in the firm and act in such a way that they may reap the maximum rewards.

Management can better manage the company's debts if they have complete understanding

of the company's liquidity. Financial data reporting assists in risk mitigation by predicting

changes in market circumstances.

6.0 An explanation of the difference between International

Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) and a critical evaluation of

the benefits of IFRS

International accounting standard (IAS)

Customers: These individuals would be interested in the company's ability to

continue as a reliable source of supplies in the future, and would look for any

factors that may hinder this, such as production issues, sales price rises, and so on.

5.0 An analysis of the value of financial reporting for meeting

organisational objectives and growth

Financial analysis and reporting are solid, steady, and by and large open strategies

for scattering essential monetary information across the organization. Things could

quickly go to pieces assuming your monetary bits of knowledge or information are

disconnected. Basically, this by itself explains what monetary detailing and investigation

are. Financial analysis and reporting can help you answer a slew of important questions

about your company's finances, providing both internal and external stakeholders with an

accurate, complete picture of the strategic and operational metrics they need to make

choices and take action (Kuběnka, Honková, Sejkora, and Jedlička, 2018).

Financial reports should be as accurate as possible; in any event, any

administration reports (and subsequent choices) based on them would be on shaky

footing. This is where businesses may run into troubles if they rely on antiquated

practises (such as a single large bookkeeping page with a few clients) rather than

embracing financial dashboards to reap the benefits of financial reporting.

Financial reporting is important because it allows consumers of financial data to

follow trends in the firm and act in such a way that they may reap the maximum rewards.

Management can better manage the company's debts if they have complete understanding

of the company's liquidity. Financial data reporting assists in risk mitigation by predicting

changes in market circumstances.

6.0 An explanation of the difference between International

Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) and a critical evaluation of

the benefits of IFRS

International accounting standard (IAS)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

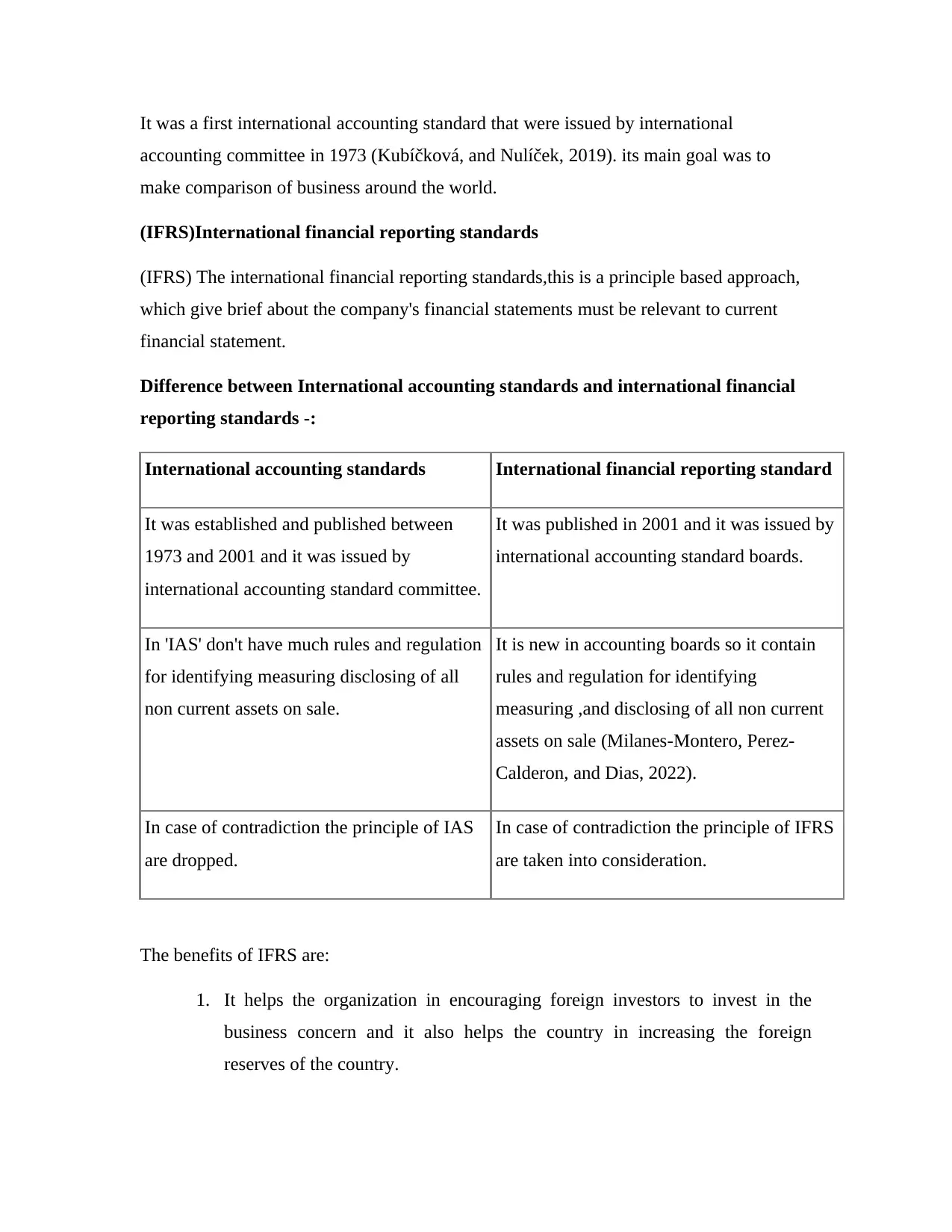

It was a first international accounting standard that were issued by international

accounting committee in 1973 (Kubíčková, and Nulíček, 2019). its main goal was to

make comparison of business around the world.

(IFRS)International financial reporting standards

(IFRS) The international financial reporting standards,this is a principle based approach,

which give brief about the company's financial statements must be relevant to current

financial statement.

Difference between International accounting standards and international financial

reporting standards -:

International accounting standards International financial reporting standard

It was established and published between

1973 and 2001 and it was issued by

international accounting standard committee.

It was published in 2001 and it was issued by

international accounting standard boards.

In 'IAS' don't have much rules and regulation

for identifying measuring disclosing of all

non current assets on sale.

It is new in accounting boards so it contain

rules and regulation for identifying

measuring ,and disclosing of all non current

assets on sale (Milanes-Montero, Perez-

Calderon, and Dias, 2022).

In case of contradiction the principle of IAS

are dropped.

In case of contradiction the principle of IFRS

are taken into consideration.

The benefits of IFRS are:

1. It helps the organization in encouraging foreign investors to invest in the

business concern and it also helps the country in increasing the foreign

reserves of the country.

accounting committee in 1973 (Kubíčková, and Nulíček, 2019). its main goal was to

make comparison of business around the world.

(IFRS)International financial reporting standards

(IFRS) The international financial reporting standards,this is a principle based approach,

which give brief about the company's financial statements must be relevant to current

financial statement.

Difference between International accounting standards and international financial

reporting standards -:

International accounting standards International financial reporting standard

It was established and published between

1973 and 2001 and it was issued by

international accounting standard committee.

It was published in 2001 and it was issued by

international accounting standard boards.

In 'IAS' don't have much rules and regulation

for identifying measuring disclosing of all

non current assets on sale.

It is new in accounting boards so it contain

rules and regulation for identifying

measuring ,and disclosing of all non current

assets on sale (Milanes-Montero, Perez-

Calderon, and Dias, 2022).

In case of contradiction the principle of IAS

are dropped.

In case of contradiction the principle of IFRS

are taken into consideration.

The benefits of IFRS are:

1. It helps the organization in encouraging foreign investors to invest in the

business concern and it also helps the country in increasing the foreign

reserves of the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. By using common set of accounting standards helps in interpreting the books

of accounts more easily and conveniently. This helps in understanding those

financial books more number of individual (Siladjaja, and Anwar, 2021).

3. Company’s helps in raising the funds needed by organization from the foreign

markets as they have been able attract the foreign investors by using this

globally accepted accounting principle.

4. Easy Comparison – IFRS helps in comparing the financial data of company

with the other as the procedure of maintain books of accounts in both the

companies is same then it would be easy to compare both the companies.

These helps in evaluating and comparing the financial books.

5. Encourages global acceptability of the books of accounts as it is same

worldwide and prepared in similar manner.

6. It encourage over the border transactions as well as investments in the

countries by providing them proper financial insights of a business concern.

7. These rules also help in international mergers and acquisitions with bigger

brands (Tian, 2018). IFRS also helps to know the risk involved in the business

that provides a clear picture of risk involved in the business.

8. These rules benefit the company in expanding their international business as

well as the economy as whole.

6. Identification of the varying degrees of compliance with

IFRS by organisations across the world and the factors in a

nation which may impact compliance

Financial reporting models are a variety of models that address a real-world financial

situation and are designed to help the administration better understand the need for

financial reporting and evaluation, as well as to help the administration estimate the costs

and benefits of a proposed project (Muhamad Sori, 2018).

of accounts more easily and conveniently. This helps in understanding those

financial books more number of individual (Siladjaja, and Anwar, 2021).

3. Company’s helps in raising the funds needed by organization from the foreign

markets as they have been able attract the foreign investors by using this

globally accepted accounting principle.

4. Easy Comparison – IFRS helps in comparing the financial data of company

with the other as the procedure of maintain books of accounts in both the

companies is same then it would be easy to compare both the companies.

These helps in evaluating and comparing the financial books.

5. Encourages global acceptability of the books of accounts as it is same

worldwide and prepared in similar manner.

6. It encourage over the border transactions as well as investments in the

countries by providing them proper financial insights of a business concern.

7. These rules also help in international mergers and acquisitions with bigger

brands (Tian, 2018). IFRS also helps to know the risk involved in the business

that provides a clear picture of risk involved in the business.

8. These rules benefit the company in expanding their international business as

well as the economy as whole.

6. Identification of the varying degrees of compliance with

IFRS by organisations across the world and the factors in a

nation which may impact compliance

Financial reporting models are a variety of models that address a real-world financial

situation and are designed to help the administration better understand the need for

financial reporting and evaluation, as well as to help the administration estimate the costs

and benefits of a proposed project (Muhamad Sori, 2018).

The varying degree of compliance with IFRS present withing different nations is due to

the following reasons:

Legislative system: If organisations in a country are specifically asked to present

monetary data in a certain format by legal experts in that country, they must

follow these instructions, which creates a different foundation for reporting all

over the world (Maradona and Chand, 2018).

Tax assessment: While disseminated monetary records form the basis of

expenditure computation in certain countries, financial reports are modified to tax

reasons in others due to government regulations (RAMELAN, 2019).

Political and Economic Ties: It allows regulations and guidelines to be

communicated from one country to the next, allowing for greater analysis and a

more efficient interchange of professionals to work and promote the other.

Inflation: If a country's inflation rate is high, or if it is expected that the country

will confront inflation in the future, the accounting bodies should consider

changing the historical cost numbers (Shadrina, 2018) In addition, adjusting

salary for inflation has a substantial impact on tax computation.

7.0 Conclusions

According to the aforementioned research, the International Financial Reporting

Standards (IFRS) are an important viewpoint in the field of bookkeeping. The

International Financial Reporting Standards (IFRS) are a collection of principles and

rules that an organisation must follow when preparing and disclosing budget reports to

various clients. The administrative structure aids the specialists in having a better

knowledge of what exactly has to be done in order to achieve the goals. The foundation

for preparing and exposing budget reports and data to recognised partners is bookkeeping

standards and administrative systems. Each user of financial data interacts with it in their

own unique way, and as a result, it is critical for bookkeepers to put up the records in

such a way that no one has difficulty accessing them and can fully benefit from

something comparable. While using Morrisons as the basic organisation for this research,

this paper explained how IFRS is important for many reasons, the concept of accounting

the following reasons:

Legislative system: If organisations in a country are specifically asked to present

monetary data in a certain format by legal experts in that country, they must

follow these instructions, which creates a different foundation for reporting all

over the world (Maradona and Chand, 2018).

Tax assessment: While disseminated monetary records form the basis of

expenditure computation in certain countries, financial reports are modified to tax

reasons in others due to government regulations (RAMELAN, 2019).

Political and Economic Ties: It allows regulations and guidelines to be

communicated from one country to the next, allowing for greater analysis and a

more efficient interchange of professionals to work and promote the other.

Inflation: If a country's inflation rate is high, or if it is expected that the country

will confront inflation in the future, the accounting bodies should consider

changing the historical cost numbers (Shadrina, 2018) In addition, adjusting

salary for inflation has a substantial impact on tax computation.

7.0 Conclusions

According to the aforementioned research, the International Financial Reporting

Standards (IFRS) are an important viewpoint in the field of bookkeeping. The

International Financial Reporting Standards (IFRS) are a collection of principles and

rules that an organisation must follow when preparing and disclosing budget reports to

various clients. The administrative structure aids the specialists in having a better

knowledge of what exactly has to be done in order to achieve the goals. The foundation

for preparing and exposing budget reports and data to recognised partners is bookkeeping

standards and administrative systems. Each user of financial data interacts with it in their

own unique way, and as a result, it is critical for bookkeepers to put up the records in

such a way that no one has difficulty accessing them and can fully benefit from

something comparable. While using Morrisons as the basic organisation for this research,

this paper explained how IFRS is important for many reasons, the concept of accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.