Analysis of International Financial Reporting for Able Plc (2017)

VerifiedAdded on 2020/06/04

|13

|4055

|42

Report

AI Summary

This report examines the application of International Financial Reporting Standards (IFRS) to the financial statements of Able Plc for the year 2017. It begins with an introduction to IFRS and its role in preparing financial statements, emphasizing its importance for stakeholders. The report then presents and analyzes Able Plc's income statement, calculating net income and discussing key components like revenue, cost of sales, and operating expenses. It highlights the critical aspects of regulatory discussions and relevant accounting standards. Furthermore, the report delves into identifying and valuing intangible assets, specifically focusing on the capitalization of research and development (R&D) costs according to IAS 38. Finally, it explains the valuation of inventories at the lower of cost and net realizable value. The report concludes by summarizing the key findings and implications of IFRS on Able Plc's financial reporting and performance.

International Financial

Report

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Q1 International Financial Reporting standards and Income statement of Able Plc for the year

2017.............................................................................................................................................1

Q2 Critical revelation over the regulator discussion and relevant international accounting

standards......................................................................................................................................3

Identifying the intangible assets looking at the specific area of capitalising R&D costs...........5

Q3 Explanation of the statement Inventories should be valued at “ Lower of cost and net

realisable value” .........................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Q1 International Financial Reporting standards and Income statement of Able Plc for the year

2017.............................................................................................................................................1

Q2 Critical revelation over the regulator discussion and relevant international accounting

standards......................................................................................................................................3

Identifying the intangible assets looking at the specific area of capitalising R&D costs...........5

Q3 Explanation of the statement Inventories should be valued at “ Lower of cost and net

realisable value” .........................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

The preparation of financial statements, reports and data set which brings the informative

details relevant with firm's growth, liquidity and ability to meet the debts. However, to prepare

the suitable informative data base there will be requirement of implicating the authenticated

framework to perform these activities. Similarly, in the present report there will be preparation of

income statements which will present the revenue and expenses of Able Plc in the proposed

period. Moreover, there will be determination of the facts and usefulness of the financial

statements in relation with a regulatory framework of international accounting standards. The

importance of such techniques in funneling the accounting professionals to prepare the financials

as per the requirements.

Q1 International Financial Reporting standards and Income statement of Able Plc for the year

2017

Generally accepted accounting principles is been represented by International financial

reporting standards and these are used by the organisations for the preparation of financial

statements which has been published annually which is useful to stakeholders such as debtors,

clients, shareholders, government and employees for the understanding of financial position and

stability of the organizations. IFRS has been developed by International Accounting Standards

Board, set of accounting rules adopted by more than 100 countries. The whole members of

European Union should mandatory use IFRS. The increase of globalisation of financial markets

and companies has increased the use of single set of financial reporting standards across all

countries and it has made the comparison of financial statements easy across the borders. Due to

this the cost of preparing financial statements has been reduced which has been prepared by

group of companies which conducts business in the world. Generally these standards are

developed by not for profit organisations and independent organizations (Cascino and Gassen,

2015).

The main objective of IFRS standard is to disclose the financial statement's preparation or

in the same guidance has been provided for the procedure. The companies who have subsidiaries

in many other countries have a vital and important role of IFRS standards. Statement of

comprehensive income represents the financial performance of company. Sub parts of profit and

loss statements such as revenue and expenses, enhancement of assets and inflows helps in raising

economic benefit and if in case liabilities are decreased then there is increase in equity. Equity

1

The preparation of financial statements, reports and data set which brings the informative

details relevant with firm's growth, liquidity and ability to meet the debts. However, to prepare

the suitable informative data base there will be requirement of implicating the authenticated

framework to perform these activities. Similarly, in the present report there will be preparation of

income statements which will present the revenue and expenses of Able Plc in the proposed

period. Moreover, there will be determination of the facts and usefulness of the financial

statements in relation with a regulatory framework of international accounting standards. The

importance of such techniques in funneling the accounting professionals to prepare the financials

as per the requirements.

Q1 International Financial Reporting standards and Income statement of Able Plc for the year

2017

Generally accepted accounting principles is been represented by International financial

reporting standards and these are used by the organisations for the preparation of financial

statements which has been published annually which is useful to stakeholders such as debtors,

clients, shareholders, government and employees for the understanding of financial position and

stability of the organizations. IFRS has been developed by International Accounting Standards

Board, set of accounting rules adopted by more than 100 countries. The whole members of

European Union should mandatory use IFRS. The increase of globalisation of financial markets

and companies has increased the use of single set of financial reporting standards across all

countries and it has made the comparison of financial statements easy across the borders. Due to

this the cost of preparing financial statements has been reduced which has been prepared by

group of companies which conducts business in the world. Generally these standards are

developed by not for profit organisations and independent organizations (Cascino and Gassen,

2015).

The main objective of IFRS standard is to disclose the financial statement's preparation or

in the same guidance has been provided for the procedure. The companies who have subsidiaries

in many other countries have a vital and important role of IFRS standards. Statement of

comprehensive income represents the financial performance of company. Sub parts of profit and

loss statements such as revenue and expenses, enhancement of assets and inflows helps in raising

economic benefit and if in case liabilities are decreased then there is increase in equity. Equity

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

contributions like partners, owners and shareholders are not considered as revenue. And if there

is outflow then there is decrease in economic benefit and because of increase in liabilities there is

decrement in equity. Equity participants does not consist of distribution. There are major

circumstances which are reflection of comprehensive income such as, remeasurement of assets

and liabilities, fair value of financial asset might decrease or increase and can be modified as

availability for sale and even revaluation of some assets such as plant, property and intangible

asset may rise or fall.

Offsetting has been forbidden by IFRS standards. If some specific condition is mentioned

then offsetting should be used. There is a basic need for fair representation for effect of all the

conditions which are set according to IFRS framework and criteria should be recognised for

income, assets, liabilities and expenses (Kieso, Weygandt and Warfield, 2010). Narrative and

descriptive information is given by comparative information related to current year's financial

statement and the alternative to know the financial position is the balance sheet statement of

International accounting standard 1 and the items are been classified for financial statements.

The income statement of Able plc. For the year ending 31 December 2017 is as follows:

Income statement of the year ending 31 December 2017

Particulars Details Amount (in £)

Net sales 205000

Return Inwards -10000

Net Revenue 195000

Cost of sales

Opening inventory 20000

Purchases 130000

Return outwards -1000

Adjusted purchase 129000

Goods available for sale 150000

Closing inventory -26000

Cost of sales 124000

Gross Margin 397000

Operating Expenses

Carriage inwards 1000

2

is outflow then there is decrease in economic benefit and because of increase in liabilities there is

decrement in equity. Equity participants does not consist of distribution. There are major

circumstances which are reflection of comprehensive income such as, remeasurement of assets

and liabilities, fair value of financial asset might decrease or increase and can be modified as

availability for sale and even revaluation of some assets such as plant, property and intangible

asset may rise or fall.

Offsetting has been forbidden by IFRS standards. If some specific condition is mentioned

then offsetting should be used. There is a basic need for fair representation for effect of all the

conditions which are set according to IFRS framework and criteria should be recognised for

income, assets, liabilities and expenses (Kieso, Weygandt and Warfield, 2010). Narrative and

descriptive information is given by comparative information related to current year's financial

statement and the alternative to know the financial position is the balance sheet statement of

International accounting standard 1 and the items are been classified for financial statements.

The income statement of Able plc. For the year ending 31 December 2017 is as follows:

Income statement of the year ending 31 December 2017

Particulars Details Amount (in £)

Net sales 205000

Return Inwards -10000

Net Revenue 195000

Cost of sales

Opening inventory 20000

Purchases 130000

Return outwards -1000

Adjusted purchase 129000

Goods available for sale 150000

Closing inventory -26000

Cost of sales 124000

Gross Margin 397000

Operating Expenses

Carriage inwards 1000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

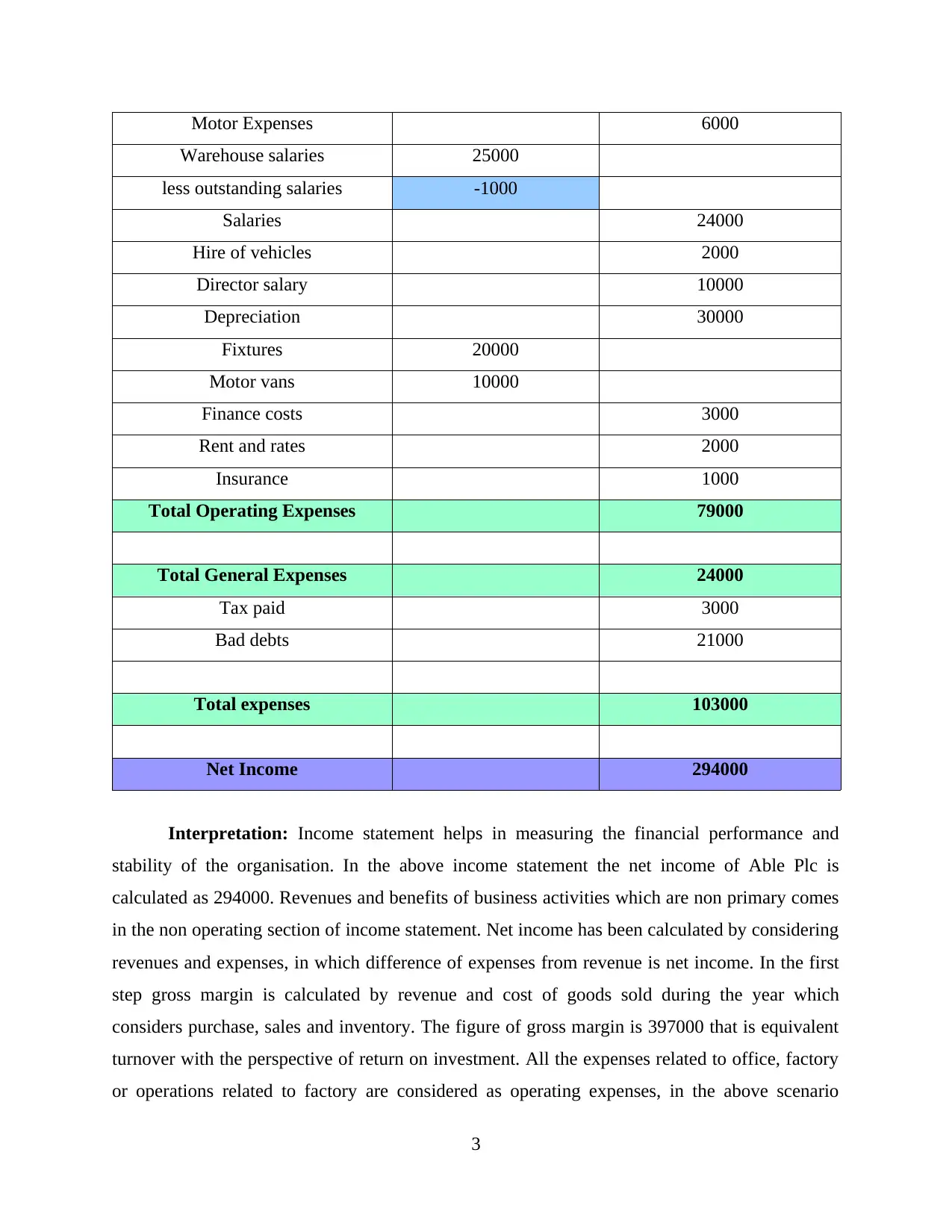

Motor Expenses 6000

Warehouse salaries 25000

less outstanding salaries -1000

Salaries 24000

Hire of vehicles 2000

Director salary 10000

Depreciation 30000

Fixtures 20000

Motor vans 10000

Finance costs 3000

Rent and rates 2000

Insurance 1000

Total Operating Expenses 79000

Total General Expenses 24000

Tax paid 3000

Bad debts 21000

Total expenses 103000

Net Income 294000

Interpretation: Income statement helps in measuring the financial performance and

stability of the organisation. In the above income statement the net income of Able Plc is

calculated as 294000. Revenues and benefits of business activities which are non primary comes

in the non operating section of income statement. Net income has been calculated by considering

revenues and expenses, in which difference of expenses from revenue is net income. In the first

step gross margin is calculated by revenue and cost of goods sold during the year which

considers purchase, sales and inventory. The figure of gross margin is 397000 that is equivalent

turnover with the perspective of return on investment. All the expenses related to office, factory

or operations related to factory are considered as operating expenses, in the above scenario

3

Warehouse salaries 25000

less outstanding salaries -1000

Salaries 24000

Hire of vehicles 2000

Director salary 10000

Depreciation 30000

Fixtures 20000

Motor vans 10000

Finance costs 3000

Rent and rates 2000

Insurance 1000

Total Operating Expenses 79000

Total General Expenses 24000

Tax paid 3000

Bad debts 21000

Total expenses 103000

Net Income 294000

Interpretation: Income statement helps in measuring the financial performance and

stability of the organisation. In the above income statement the net income of Able Plc is

calculated as 294000. Revenues and benefits of business activities which are non primary comes

in the non operating section of income statement. Net income has been calculated by considering

revenues and expenses, in which difference of expenses from revenue is net income. In the first

step gross margin is calculated by revenue and cost of goods sold during the year which

considers purchase, sales and inventory. The figure of gross margin is 397000 that is equivalent

turnover with the perspective of return on investment. All the expenses related to office, factory

or operations related to factory are considered as operating expenses, in the above scenario

3

operating expenses are carriage inward, motor expenses, salaries, hire of vehicle, depreciation on

assets, finance costs, rents and rate and insurance whose sum is 79000. The general expenses of

24000 like tax and interest so the combination of all expenses is 10300. The last step is to find

net income by subtracting total expenses from gross margin which is net income as 294000. the

suggestion for the company in the perspective of increasing net income, then it should try to

reduce the expenses so this will directly reflect on the net income of the organization.

Q2 Critical revelation over the regulator discussion and relevant international accounting

standards

To manage an operational framework within organisational premises as well as preparing

various reports which will be helpful to establish the appropriate accounting framework in the

business. Moreover, the regulation incorporated by these accounting standards is to provide the

relevant information funnel the managers to have appropriate operational activities. The

guidance is based on recording of all the financial transactions held in during the period which in

turn will be effective and beneficial as to have preparation of the statement on the basis of such

financials (Volberding, 2017). The main purpose of developing the accounting standard is that

the preparation of financial will be based on a universal framework as well as universal

operations which in turn will easily be understandable and recognizable to all the accounting

professionals, investors, financial authorities as well as government.

Universally accepted standard and the framework of the accounting techniques which

will be indicative and helpful as to have appropriate rise in the level of reporting systems.

Therefore, it will be helpful and adequate sources for the shareholders in relation with attaining

all the infotainments which are listed in the financial statements. They can easily recognise that

revenue, expense and the profits tare listed in the income statement of the firm while liabilities

and assets are in balance sheet. This makes them able to analyse the growth and profitability of

the industry in the coming time as well as also analyse the dividend payable by them (IAS 38 —

Intangible Assets, 2018). It will be much effective to the organisation as they will have large

numbers of investors in the firm as well as it supports the good financial governance in business

activities. Thus, the capital structure and costs incurred in each business activities which will be

recognised and ascertained by business professionals. It helps in balancing the expenditure,

revenue and costs incurred in each business operations which will be managed and have proper

recording of all the informations.

4

assets, finance costs, rents and rate and insurance whose sum is 79000. The general expenses of

24000 like tax and interest so the combination of all expenses is 10300. The last step is to find

net income by subtracting total expenses from gross margin which is net income as 294000. the

suggestion for the company in the perspective of increasing net income, then it should try to

reduce the expenses so this will directly reflect on the net income of the organization.

Q2 Critical revelation over the regulator discussion and relevant international accounting

standards

To manage an operational framework within organisational premises as well as preparing

various reports which will be helpful to establish the appropriate accounting framework in the

business. Moreover, the regulation incorporated by these accounting standards is to provide the

relevant information funnel the managers to have appropriate operational activities. The

guidance is based on recording of all the financial transactions held in during the period which in

turn will be effective and beneficial as to have preparation of the statement on the basis of such

financials (Volberding, 2017). The main purpose of developing the accounting standard is that

the preparation of financial will be based on a universal framework as well as universal

operations which in turn will easily be understandable and recognizable to all the accounting

professionals, investors, financial authorities as well as government.

Universally accepted standard and the framework of the accounting techniques which

will be indicative and helpful as to have appropriate rise in the level of reporting systems.

Therefore, it will be helpful and adequate sources for the shareholders in relation with attaining

all the infotainments which are listed in the financial statements. They can easily recognise that

revenue, expense and the profits tare listed in the income statement of the firm while liabilities

and assets are in balance sheet. This makes them able to analyse the growth and profitability of

the industry in the coming time as well as also analyse the dividend payable by them (IAS 38 —

Intangible Assets, 2018). It will be much effective to the organisation as they will have large

numbers of investors in the firm as well as it supports the good financial governance in business

activities. Thus, the capital structure and costs incurred in each business activities which will be

recognised and ascertained by business professionals. It helps in balancing the expenditure,

revenue and costs incurred in each business operations which will be managed and have proper

recording of all the informations.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It comprises with the high quality of accounting standards with the neutral principles that

will be comparable, reliable, consistent and relevant. The information stated in the financial

accounts are needed to have concrete evidence behind them which in turn will be effective and

helpful for proper records. The collected data than will be analysed by the accounting

professionals or auditors to redetermine the growth of business (Dos Reis and et.al., 2017).

Thereafter, it will be used in decision making, planing and forecasting the budgets for the

favourable operational development of the organisation. It guides th accounting professionals in

terms of allocating the capital funds in each business activities such as manufacturing,

purchasing, promoting etc. it brings the balance between level of spending and the revenue

gathered by the firm. On the other side, the implication of various techniques which in context

with bringing the appropriate control over financial operations in the economy.

It also enhances the knowledge of investors as to analyse the market with ascertain the

risks and opportunities stated in the environment. Therefore, this will prevail in the market as to

have satisfactory outcomes and capital allocations with proper efficiency and ascertainment. The

motive of implicating the international standards is for developing the standards and global

market for a proper platform which will be helpful to the shareholders, investors etc. that will

reduce international reporting costs as well as removes the territorial barriers (Carvalho and

et.al., 2017). Moreover, a firm will have investments from the foreign investors which will be

beneficial in rising the market value of organisation. Apart from managing the capital allocation

in the international business it will be suitable as to have proper management of the work and

workforce force for the operations. It brings the proper control over the costs of capital as well as

review the financial performance of the organisation in the periodical basis. Hence, the

preparation of the financial accounts which in turn will have informative gains and operational

activities. The informations which are to be considered by investors in the financial reports of an

entity which are mainly the profits, turnover as well as the dividend paid by them. Thus, it will

bring them knowledge regrading the profitability of the firm as well as the ability to meet the

financial gains.

Identifying the intangible assets looking at the specific area of capitalising R&D costs

In relation with measuring the intangible assets of the business there will be various

operational treatment and accounting entries which in turn will have effective control over the

operations of the business. However, valuation of these assets is very complex and needs efforts

5

will be comparable, reliable, consistent and relevant. The information stated in the financial

accounts are needed to have concrete evidence behind them which in turn will be effective and

helpful for proper records. The collected data than will be analysed by the accounting

professionals or auditors to redetermine the growth of business (Dos Reis and et.al., 2017).

Thereafter, it will be used in decision making, planing and forecasting the budgets for the

favourable operational development of the organisation. It guides th accounting professionals in

terms of allocating the capital funds in each business activities such as manufacturing,

purchasing, promoting etc. it brings the balance between level of spending and the revenue

gathered by the firm. On the other side, the implication of various techniques which in context

with bringing the appropriate control over financial operations in the economy.

It also enhances the knowledge of investors as to analyse the market with ascertain the

risks and opportunities stated in the environment. Therefore, this will prevail in the market as to

have satisfactory outcomes and capital allocations with proper efficiency and ascertainment. The

motive of implicating the international standards is for developing the standards and global

market for a proper platform which will be helpful to the shareholders, investors etc. that will

reduce international reporting costs as well as removes the territorial barriers (Carvalho and

et.al., 2017). Moreover, a firm will have investments from the foreign investors which will be

beneficial in rising the market value of organisation. Apart from managing the capital allocation

in the international business it will be suitable as to have proper management of the work and

workforce force for the operations. It brings the proper control over the costs of capital as well as

review the financial performance of the organisation in the periodical basis. Hence, the

preparation of the financial accounts which in turn will have informative gains and operational

activities. The informations which are to be considered by investors in the financial reports of an

entity which are mainly the profits, turnover as well as the dividend paid by them. Thus, it will

bring them knowledge regrading the profitability of the firm as well as the ability to meet the

financial gains.

Identifying the intangible assets looking at the specific area of capitalising R&D costs

In relation with measuring the intangible assets of the business there will be various

operational treatment and accounting entries which in turn will have effective control over the

operations of the business. However, valuation of these assets is very complex and needs efforts

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the counteraction managers in performing such tasks. There will be requirement of appropriate

and authenticate information that will bring the proper justification over the operations of entity.

It mainly includes patents, copy rights, goodwill and brand image. Thus, implication of various

factors which in turn will be indicative and helpful to the professionals as to have proper

management as well as valuation of these assets. In relation with the internal intangible assets

which are mainly comprises with research and development made in the premises (Saucier and

et.al., 2017). In accordance with IAS 38, the valuation of intangible assets will be necessary to a

business and there will be taxable assumptions mainly over the patents, copyrights etc. Thus, to

improve the intangible assets will eventually rise the ability of firm in balancing the capital

structure as well as making the effective planning and development which in turn helps in

managing operational activities of the entity. The main characteristics of these assets are they are

capable of being separate from other assets which will be sold, purchases, transferred, licensed,

rented as well as exchanged with other entities. It also incorporated with the various legal rights

in relation with transferring the rights to another corporation of person.

The valuation of these assets will be helpful in bringing the suitable and satisfactory

knowledge relevant with the capital structure of the firm. It includes patent technology, database

and trade secrets, software, trademarks, internet domains, details of stakeholder, consumers or

investors etc. therefore, the confidentiality of such details as well as valuation will have positive

impacts over the growth of firm for the long term gains. To measure the reliable value of the

intangible assets the accounting treatment will be measured in the presumption of their fair

value. On context with the research and development which will be projected as to have

appropriate assets at costs that comprises with the favourable results (Khan and et.al., 2018).

Moreover, it can be said that to retain the rights for the longer period there will be requirements

of having the proper innovative changes in the operations. Moreover, the large discovered and

development of products and services which will be unique in the market as well as attractive to

consumer that will create the brand value, goodwill of the business. Thus, such techniques will

be efficiency for making the growth in the operational activities. To secure the individual rights

which in turn will be effective for determining the fruitful revenue gains.

In accordance to IAS 38 which states that intangible assets will be recognised as if the

probable future financial gains will flow to the entity as well as costs of assets which will

reliability measured by the professionals. The valuation of assets will bring the strength to capital

6

and authenticate information that will bring the proper justification over the operations of entity.

It mainly includes patents, copy rights, goodwill and brand image. Thus, implication of various

factors which in turn will be indicative and helpful to the professionals as to have proper

management as well as valuation of these assets. In relation with the internal intangible assets

which are mainly comprises with research and development made in the premises (Saucier and

et.al., 2017). In accordance with IAS 38, the valuation of intangible assets will be necessary to a

business and there will be taxable assumptions mainly over the patents, copyrights etc. Thus, to

improve the intangible assets will eventually rise the ability of firm in balancing the capital

structure as well as making the effective planning and development which in turn helps in

managing operational activities of the entity. The main characteristics of these assets are they are

capable of being separate from other assets which will be sold, purchases, transferred, licensed,

rented as well as exchanged with other entities. It also incorporated with the various legal rights

in relation with transferring the rights to another corporation of person.

The valuation of these assets will be helpful in bringing the suitable and satisfactory

knowledge relevant with the capital structure of the firm. It includes patent technology, database

and trade secrets, software, trademarks, internet domains, details of stakeholder, consumers or

investors etc. therefore, the confidentiality of such details as well as valuation will have positive

impacts over the growth of firm for the long term gains. To measure the reliable value of the

intangible assets the accounting treatment will be measured in the presumption of their fair

value. On context with the research and development which will be projected as to have

appropriate assets at costs that comprises with the favourable results (Khan and et.al., 2018).

Moreover, it can be said that to retain the rights for the longer period there will be requirements

of having the proper innovative changes in the operations. Moreover, the large discovered and

development of products and services which will be unique in the market as well as attractive to

consumer that will create the brand value, goodwill of the business. Thus, such techniques will

be efficiency for making the growth in the operational activities. To secure the individual rights

which in turn will be effective for determining the fruitful revenue gains.

In accordance to IAS 38 which states that intangible assets will be recognised as if the

probable future financial gains will flow to the entity as well as costs of assets which will

reliability measured by the professionals. The valuation of assets will bring the strength to capital

6

structure of firm (Volberding, 2017). It enhances liquidity and current ability in the firm which in

turn will be effective as to meet the short term as well as long term debts. On the basis of their

treatment in the accounting statements which comprises with the amortisation, commercial

production as well as proper managements of the operations.

Conclusion:

On the basis of above discussion there will be proper judgements which were based on

the operational framework of IAS in the financial reporting. Therefore, the main motive of

implicating such rule is to provide the appropriate guidance and funnelling to accounting

professionals as to have prepared the reports as per the requirements. Moreover, the valuation

and transactional entities of intangible assets in reliable manner neds the proper administration as

well as control of the professionals for better operations. Thus, the main motive is to prepare the

financial reports which in turn will be helpful and indicative to the professionals as to have

appropriate gains and development of facts. Therefore, such accounting operations will be held

at the end of each period as well as management of the operations which in turn will be

indicative as well as beneficial to have appropriate recognition of any loopholes.

Q3 Explanation of the statement Inventories should be valued at “ Lower of cost and net

realisable value”

According to the international accounting standard 2 inventories should be valued at

lower of cost and net realisable value. The direction has been provided by IAS 2 for determining

the inventory's cost and recognition of cost which signifies as expense. For assigning cost to

inventories cost formula is implied (Ahmed, Neel and Wang, 2013). Cost formula indicates the

inventory's cost which cannot be interchangeable and the particular goods and services are

differentiated and produced for projects which are more specific and specific identification is

been referred to individual costs. Attributed items of inventory is been identified at cost whose

significance is of particular cost. Example in the same series can be, different operating segment

uses some specific inventories of the different segment of the entity, so the location of that

inventories is not sufficient for justifying the specific application of the cost formula. In case the

inventories become obsolete or damaged then that cost is not recoverable whether they are partial

of fully damaged even there is fall in prices of selling price. Net realisable value is accurate

measure for reducing cost of inventories with the perspective of assets whose excess amount

must not be carried.

7

turn will be effective as to meet the short term as well as long term debts. On the basis of their

treatment in the accounting statements which comprises with the amortisation, commercial

production as well as proper managements of the operations.

Conclusion:

On the basis of above discussion there will be proper judgements which were based on

the operational framework of IAS in the financial reporting. Therefore, the main motive of

implicating such rule is to provide the appropriate guidance and funnelling to accounting

professionals as to have prepared the reports as per the requirements. Moreover, the valuation

and transactional entities of intangible assets in reliable manner neds the proper administration as

well as control of the professionals for better operations. Thus, the main motive is to prepare the

financial reports which in turn will be helpful and indicative to the professionals as to have

appropriate gains and development of facts. Therefore, such accounting operations will be held

at the end of each period as well as management of the operations which in turn will be

indicative as well as beneficial to have appropriate recognition of any loopholes.

Q3 Explanation of the statement Inventories should be valued at “ Lower of cost and net

realisable value”

According to the international accounting standard 2 inventories should be valued at

lower of cost and net realisable value. The direction has been provided by IAS 2 for determining

the inventory's cost and recognition of cost which signifies as expense. For assigning cost to

inventories cost formula is implied (Ahmed, Neel and Wang, 2013). Cost formula indicates the

inventory's cost which cannot be interchangeable and the particular goods and services are

differentiated and produced for projects which are more specific and specific identification is

been referred to individual costs. Attributed items of inventory is been identified at cost whose

significance is of particular cost. Example in the same series can be, different operating segment

uses some specific inventories of the different segment of the entity, so the location of that

inventories is not sufficient for justifying the specific application of the cost formula. In case the

inventories become obsolete or damaged then that cost is not recoverable whether they are partial

of fully damaged even there is fall in prices of selling price. Net realisable value is accurate

measure for reducing cost of inventories with the perspective of assets whose excess amount

must not be carried.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Though, net realisable value helps in reducing inventories such as in many cases they can

be perfect for related or similar terms. The inventories which are used for same purpose,

application, product line even traded or marketed for same location or geographical area that

cannot be evaluated practically in different ways. On the perspective of classification, inventories

cannot be write off such as inventories of specific operating segment and specific finished goods.

The most essential and reliable indication is of net realisable value whose availability during the

preparation of estimates and price fluctuations that is directly linked to the situation which occurs

at end of the period and there is also consideration of application of inventories. It can be

justified by the example that, the organisation's service or the sales contract has satisfied the net

realisable value which is directly linked to the contract's price. If the quantity of inventory is

more than sales contract then the excess net realisable value is purely based on selling price. The

inventory's cost consists of conversion cost like production overhead and direct labour. To bring

all the inventories in present condition and location is been occurred by purchase cost and other

cost. So the inventories cost is been assigned by FIFO method i.e. First in first out or WACC that

is weighted average cost of capital for exchangeable objects and identifying the specific items in

inventory which can not be exchangeable (Cascino and Gassen, 2015). When the inventories are

sold and the expense where revenue is recognised then the carrying amount is considered in the

inventories.

The accounting treatment of inventories is referred by international accounting standard

which also determines the inventory's cost and all the expenses which are related to inventory.

As cost formula is been assigned to give cost to the inventory. According to IAS 2 cost of

purchase, net of trade discounts received, conversion cost and all related cost which is sued for

bringing the inventory in present geographical location is been used for measuring the

inventories. The basic fundamental principle of IAS 2 says that inventories are required for

stating lower of cost and net realisable value. Abnormal waste, storage cost, selling cost and

interest cost which is linked from the acquisition of inventory that is invoiced in foreign currency

is never included in inventory cost.

Conclusion:

From the above question it has been clear that required level of inventories in the

company then IAS 2 will be a mode which will be adequate and effective for the analysis of

inventory's cost. The basis of analysing the holding cost by considering the EOQ measurments

8

be perfect for related or similar terms. The inventories which are used for same purpose,

application, product line even traded or marketed for same location or geographical area that

cannot be evaluated practically in different ways. On the perspective of classification, inventories

cannot be write off such as inventories of specific operating segment and specific finished goods.

The most essential and reliable indication is of net realisable value whose availability during the

preparation of estimates and price fluctuations that is directly linked to the situation which occurs

at end of the period and there is also consideration of application of inventories. It can be

justified by the example that, the organisation's service or the sales contract has satisfied the net

realisable value which is directly linked to the contract's price. If the quantity of inventory is

more than sales contract then the excess net realisable value is purely based on selling price. The

inventory's cost consists of conversion cost like production overhead and direct labour. To bring

all the inventories in present condition and location is been occurred by purchase cost and other

cost. So the inventories cost is been assigned by FIFO method i.e. First in first out or WACC that

is weighted average cost of capital for exchangeable objects and identifying the specific items in

inventory which can not be exchangeable (Cascino and Gassen, 2015). When the inventories are

sold and the expense where revenue is recognised then the carrying amount is considered in the

inventories.

The accounting treatment of inventories is referred by international accounting standard

which also determines the inventory's cost and all the expenses which are related to inventory.

As cost formula is been assigned to give cost to the inventory. According to IAS 2 cost of

purchase, net of trade discounts received, conversion cost and all related cost which is sued for

bringing the inventory in present geographical location is been used for measuring the

inventories. The basic fundamental principle of IAS 2 says that inventories are required for

stating lower of cost and net realisable value. Abnormal waste, storage cost, selling cost and

interest cost which is linked from the acquisition of inventory that is invoiced in foreign currency

is never included in inventory cost.

Conclusion:

From the above question it has been clear that required level of inventories in the

company then IAS 2 will be a mode which will be adequate and effective for the analysis of

inventory's cost. The basis of analysing the holding cost by considering the EOQ measurments

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and organisation's reorder level of inventory. The main motive of IAS 2 is to engaging the

business ongoing purpose which will be increasing the level of efficiency of the business. All the

information will help accounting professionals in the context of analysing the holding cost of

inventory along with this all manufacturing expenses. The business policies will be reframed by

effective and accurate decision. Even the guidance will impact in effective business efficiency

and growth on the long term perspective. It also gives the basic guidance and framework for

analysing various cost like purchase cost, conversion cost even fixed and variable cost. The main

objective of implementing such techniques in operations of the business which will be managing

all abnormal waste, selling cost, administration cost etc. So this will lead for generating more

revenue and control over the organisation's cost.

CONCLUSION

By considering the above study it will be concluded that the need of preparing the

financial accounts which in turn will be helpful to the business as to disclose the fruitful

information to the investors. Moreover, it will be attractive to the investors as to make their

profitable investments in the firm. They fetch informations which are mainly relevant with the

profits, annual turnover as well as dividend payable by the firm in the recent years. That will be

indicative to them as to analyse the profitability of the firm. On the other side, the report is also

comprises with income statement of Able plc and discussion based on various standard of

international accounting standard.

9

business ongoing purpose which will be increasing the level of efficiency of the business. All the

information will help accounting professionals in the context of analysing the holding cost of

inventory along with this all manufacturing expenses. The business policies will be reframed by

effective and accurate decision. Even the guidance will impact in effective business efficiency

and growth on the long term perspective. It also gives the basic guidance and framework for

analysing various cost like purchase cost, conversion cost even fixed and variable cost. The main

objective of implementing such techniques in operations of the business which will be managing

all abnormal waste, selling cost, administration cost etc. So this will lead for generating more

revenue and control over the organisation's cost.

CONCLUSION

By considering the above study it will be concluded that the need of preparing the

financial accounts which in turn will be helpful to the business as to disclose the fruitful

information to the investors. Moreover, it will be attractive to the investors as to make their

profitable investments in the firm. They fetch informations which are mainly relevant with the

profits, annual turnover as well as dividend payable by the firm in the recent years. That will be

indicative to them as to analyse the profitability of the firm. On the other side, the report is also

comprises with income statement of Able plc and discussion based on various standard of

international accounting standard.

9

REFERENCES

Books and Journals

Ahmed, A. S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

pp.1344-1372.

Carvalho, Y.M. and et.al., 2017. Inclusion complex between β-cyclodextrin and hecogenin

acetate produces superior analgesic effect in animal models for orofacial pain. Biomedicine

& Pharmacotherapy. 93. pp.754-762.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Dos Reis, G. S. and et.al., 2017. Removal of phenolic compounds from aqueous solutions using

sludge-based activated carbons prepared by conventional heating and microwave-assisted

pyrolysis. Water, Air, & Soil Pollution. 228(1). p.33.

Khan, G. and et.al., 2018. Weak population structure and no genetic erosion in Pilosocereus

aureispinus: A microendemic and threatened cactus species from eastern Brazil. PloS

one. 13(4). p.e0195475.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2010. Intermediate accounting: IFRS

edition (Vol. 2). John Wiley & Sons.

Saucier, C. and et.al., 2017. Efficient removal of amoxicillin and paracetamol from aqueous

solutions using magnetic activated carbon. Environmental Science and Pollution

Research. 24(6). pp.5918-5932.

Volberding, P. A., 2017. HIV Treatment and Prevention: An Overview of Recommendations

From the 2016 IAS–USA Antiretroviral Guidelines Panel. Topics in antiviral

medicine. 25(1). p.17.

Online

List of IFRS standards, 2018.[Online]. Available through <https://www.ifrs.org/issued-

standards/list-of-standards/>

IAS 1 Presentation of Financial statements .[Online]. Available through

<https://www.ifrs.org/issued-standards/list-of-standards/ias-1-presentation-of-financial-

statements/>

10

Books and Journals

Ahmed, A. S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research. 30(4).

pp.1344-1372.

Carvalho, Y.M. and et.al., 2017. Inclusion complex between β-cyclodextrin and hecogenin

acetate produces superior analgesic effect in animal models for orofacial pain. Biomedicine

& Pharmacotherapy. 93. pp.754-762.

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies. 20(1). pp.242-282.

Dos Reis, G. S. and et.al., 2017. Removal of phenolic compounds from aqueous solutions using

sludge-based activated carbons prepared by conventional heating and microwave-assisted

pyrolysis. Water, Air, & Soil Pollution. 228(1). p.33.

Khan, G. and et.al., 2018. Weak population structure and no genetic erosion in Pilosocereus

aureispinus: A microendemic and threatened cactus species from eastern Brazil. PloS

one. 13(4). p.e0195475.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2010. Intermediate accounting: IFRS

edition (Vol. 2). John Wiley & Sons.

Saucier, C. and et.al., 2017. Efficient removal of amoxicillin and paracetamol from aqueous

solutions using magnetic activated carbon. Environmental Science and Pollution

Research. 24(6). pp.5918-5932.

Volberding, P. A., 2017. HIV Treatment and Prevention: An Overview of Recommendations

From the 2016 IAS–USA Antiretroviral Guidelines Panel. Topics in antiviral

medicine. 25(1). p.17.

Online

List of IFRS standards, 2018.[Online]. Available through <https://www.ifrs.org/issued-

standards/list-of-standards/>

IAS 1 Presentation of Financial statements .[Online]. Available through

<https://www.ifrs.org/issued-standards/list-of-standards/ias-1-presentation-of-financial-

statements/>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

![Managerial Accounting Assignment Solution - [University] [Semester]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fnr%2Feb6ffb76356e457ab3cc2da237f03df4.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.