Financial Reporting: IFRS, IAS, and Stakeholder Analysis

VerifiedAdded on 2021/02/21

|15

|3926

|324

Report

AI Summary

This report provides a comprehensive overview of International Financial Reporting Standards (IFRS). It begins by explaining the context and purpose of financial reporting, including its role in transforming raw data into relevant information for stakeholders and management. The report then delves into the conceptual and regulatory frameworks underpinning financial reporting, emphasizing key principles and qualitative characteristics like timeliness, relevance, and faithful representation. It identifies the main stakeholders, differentiating between internal (equity holders, employees) and external (investors, creditors, government) groups, and explores how financial information benefits each group. The report further examines the value of financial reporting in achieving business objectives and fostering growth, including its role in managerial decision-making and organizational development. It presents and analyzes the main financial statements, including the Profit and Loss Account, Statement of Changes in Equity, and Statement of Financial Position. The report also covers the interpretation and communication of financial performance using profitability ratios, and highlights the differences between IAS and IFRS. It concludes by discussing the advantages of the international financial reporting system and the degree of compliance with IFRS.

International Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

1. Context and purpose of financial reporting........................................................................2

2. Conceptual, regulatory framework, key principle and qualitative characteristics.............3

3. Main Stakeholder and benefit to financial information......................................................4

4. Value of financial reporting to meet objective and growth................................................6

5. Main Financial Statements:................................................................................................7

6. Interpretation and communication of financial performance.............................................9

7. Differences between IAS and IFRS.................................................................................10

8. Advantages of International financial reporting system...................................................11

9. Degree of compliance with IFRS:....................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................14

1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

1. Context and purpose of financial reporting........................................................................2

2. Conceptual, regulatory framework, key principle and qualitative characteristics.............3

3. Main Stakeholder and benefit to financial information......................................................4

4. Value of financial reporting to meet objective and growth................................................6

5. Main Financial Statements:................................................................................................7

6. Interpretation and communication of financial performance.............................................9

7. Differences between IAS and IFRS.................................................................................10

8. Advantages of International financial reporting system...................................................11

9. Degree of compliance with IFRS:....................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................14

1

INTRODUCTION

Globally, different kind and sort of business corporates reports its consolidated and

merged accounts to shareholders. While preparing consolidated annual accounts various kind of

methods, assumptions, policies etc. are used by accounting officials. Making uniform accounts of

organizations throughout the globe internation financial reporting play a crucial role. It includes

conman set of standard, effective policies and reliable guidelines for formulation and

consolidation of accounts of subsidiaries, holding and different venture. IFRS, Ind AS and IAS,

are major example of international financial reporting standards (Adams, 2017). Effective

adoption of these global standards creates similarities in accounting practices and leads to

enhancement in creditability of business entity' books of accounts. The study report discuss

about the motive of financial reporting, its frameworks used to enhance reliability of data and

explanation to what extent financial information is beneficial for stakeholders. Study also

evaluates role of financial reporting in achieving business and trade goals, differentiation in IASs

and IFRSs and numerical sum of preparation of annual accounts.

TASK 1

1. Context and purpose of financial reporting

Financial reporting relates to transforming raw information into relevant information and

report and present information for managerial use or for stakeholders. It is essential annual task

for corporates as compliance of its is required by different statutes across world. It begins with

recognising, recording and classifying fiscal events, and ends with communicating in formal way

this information to various interested parties and shareholders. Financial reporting information

are used by a large so relevance, creditability, reliability is essentially required. It acts as

complete and full assessment of entity's performance and result (Stubbs and et.al., 2014).

Management play crucial duty in adoption and accomplishment of financial reporting process.

However accountants prepares final accounts. Different stakeholders apply information reported

in financial accounting for different context so it is notable for accountant personnels and

managers to maintain the relevance of accounts while considering various stakeholders.

Following points explains about key purposes related to financial reporting, as follows:

Under process of Financial reporting, management's primary goal or aim relates to

developing efficient strategies as well as in decision-making.

2

Globally, different kind and sort of business corporates reports its consolidated and

merged accounts to shareholders. While preparing consolidated annual accounts various kind of

methods, assumptions, policies etc. are used by accounting officials. Making uniform accounts of

organizations throughout the globe internation financial reporting play a crucial role. It includes

conman set of standard, effective policies and reliable guidelines for formulation and

consolidation of accounts of subsidiaries, holding and different venture. IFRS, Ind AS and IAS,

are major example of international financial reporting standards (Adams, 2017). Effective

adoption of these global standards creates similarities in accounting practices and leads to

enhancement in creditability of business entity' books of accounts. The study report discuss

about the motive of financial reporting, its frameworks used to enhance reliability of data and

explanation to what extent financial information is beneficial for stakeholders. Study also

evaluates role of financial reporting in achieving business and trade goals, differentiation in IASs

and IFRSs and numerical sum of preparation of annual accounts.

TASK 1

1. Context and purpose of financial reporting

Financial reporting relates to transforming raw information into relevant information and

report and present information for managerial use or for stakeholders. It is essential annual task

for corporates as compliance of its is required by different statutes across world. It begins with

recognising, recording and classifying fiscal events, and ends with communicating in formal way

this information to various interested parties and shareholders. Financial reporting information

are used by a large so relevance, creditability, reliability is essentially required. It acts as

complete and full assessment of entity's performance and result (Stubbs and et.al., 2014).

Management play crucial duty in adoption and accomplishment of financial reporting process.

However accountants prepares final accounts. Different stakeholders apply information reported

in financial accounting for different context so it is notable for accountant personnels and

managers to maintain the relevance of accounts while considering various stakeholders.

Following points explains about key purposes related to financial reporting, as follows:

Under process of Financial reporting, management's primary goal or aim relates to

developing efficient strategies as well as in decision-making.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It facilities enhancement in accuracy, quality and reliability of information reported

though annual final accounts

It assisting stakeholders understand the each financial aspect of company for efficient

investment decisions.

It supports corporate organisation to motivate new interested investors and companies to

make investments in company (Botzem, 2012).

It provides information for suppliers to decide credit terms to be given by them to

corporate.

It facilitates auditors to make fair and true comment on company's results and particular

period's performance.

It determines liquidity, operational efficiency, solvency and profitability to provide alert

to company and concerned parties.

It provides a basis for making strategies and formulate strategies for effectively

operating.

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Framework of financial reporting relates to fundamental structure which supports

different kind of financial accounting tasks within company. It is applied by all business entities

to provide smoothness in process of financial reporting. It is essential to cover different aspects

of organisation. Financial accounting's framework covers all qualitative, fiscal and quantitative

aspects to provide effectiveness in overall accounting's processes (Cavusgil and et.al., 2014).

Such Framework of financial reporting is determined by relevant statuaries in different countries.

International accounting standard board is internationally bears the duty of tracking compliance

and for making improvement in financial reporting 's framework. It contains basic ideas to be

applied by accountants to face accounting complexities and issues. It is majorly classified as

regulatory and conceptual framework.

Conceptual and Regulatory framework:

A conceptual framework of financial reporting emphasises on building a logical structure

of accounting whereas regulatory framework is part of compliances of rules and guidelines

imposed by governing authorities. Both frameworks supports an effective reporting and

acceptable by stakeholders across the globe. Conceptual framework is not compulsory for

business organisations but application of this framework makes financial statements more

3

though annual final accounts

It assisting stakeholders understand the each financial aspect of company for efficient

investment decisions.

It supports corporate organisation to motivate new interested investors and companies to

make investments in company (Botzem, 2012).

It provides information for suppliers to decide credit terms to be given by them to

corporate.

It facilitates auditors to make fair and true comment on company's results and particular

period's performance.

It determines liquidity, operational efficiency, solvency and profitability to provide alert

to company and concerned parties.

It provides a basis for making strategies and formulate strategies for effectively

operating.

2. Conceptual, regulatory framework, key principle and qualitative characteristics

Framework of financial reporting relates to fundamental structure which supports

different kind of financial accounting tasks within company. It is applied by all business entities

to provide smoothness in process of financial reporting. It is essential to cover different aspects

of organisation. Financial accounting's framework covers all qualitative, fiscal and quantitative

aspects to provide effectiveness in overall accounting's processes (Cavusgil and et.al., 2014).

Such Framework of financial reporting is determined by relevant statuaries in different countries.

International accounting standard board is internationally bears the duty of tracking compliance

and for making improvement in financial reporting 's framework. It contains basic ideas to be

applied by accountants to face accounting complexities and issues. It is majorly classified as

regulatory and conceptual framework.

Conceptual and Regulatory framework:

A conceptual framework of financial reporting emphasises on building a logical structure

of accounting whereas regulatory framework is part of compliances of rules and guidelines

imposed by governing authorities. Both frameworks supports an effective reporting and

acceptable by stakeholders across the globe. Conceptual framework is not compulsory for

business organisations but application of this framework makes financial statements more

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reliable. Where as regulatory framework make ensures that all necessary guidelines and

procedures are followed by business entity. These frameworks provide completeness in reporting

processes (Valentinetti and Rea, 2012). Main objectives of these frameworks is to increase the

confidence of public and stakeholder in financial statements and other reports prepared by

different sectors' companies. IFRS, IASs etc. are key standards which provides effectiveness in

these frameworks. Financial statements prepared considering frameworks are primarily used by

stakeholders to compute the viability of funds invested. Conceptual frameworks give easiness in

operating financial reporting tasks by providing typical guidance to enter fiscal events and

summaries effectively.

Qualitative Characteristics of financial reporting

Understanding of qualitative characteristics of financial reporting is significant to resolve

any complexity in routine accounting tasks. Following points explains characteristics of

financial accounting, as follows:

Timeliness – It ensures that right information is available at right time in a business

entity with aim to timely reporting of financial information. Corporates reports or files

its financial statement annually and in special exceptional cases reporting may be done on

quarterly basis (Cohen, J.R. and et.al., 2013). A delay in reporting may leads to legal

punishment and miss-understanding in stakeholders.

Relevance – It assures that relevant and reliable sources are used to access information

for preparing financial statements, to maintain relevance of information presented for

shareholders.

Faithful Representation – Building trust and faith in main aim of financial reporting so

financial statements emphasises on faithful representation of fiscal data.

Understandability – It facilities providing information in financial accounts which is

easily understandable all kind of people belongs to financial and non financial sectors.

3. Main Stakeholder and benefit to financial information

In corporate terms, stakeholders are key personnels, corporates and other trade entities

which can influence the business of entity and can be influenced by decisions and operations of

company. Every organisation prepare strategies while considering benefits of its various

stakeholders. Steps taken by different stakeholder can alter or influence company's decisions.

4

procedures are followed by business entity. These frameworks provide completeness in reporting

processes (Valentinetti and Rea, 2012). Main objectives of these frameworks is to increase the

confidence of public and stakeholder in financial statements and other reports prepared by

different sectors' companies. IFRS, IASs etc. are key standards which provides effectiveness in

these frameworks. Financial statements prepared considering frameworks are primarily used by

stakeholders to compute the viability of funds invested. Conceptual frameworks give easiness in

operating financial reporting tasks by providing typical guidance to enter fiscal events and

summaries effectively.

Qualitative Characteristics of financial reporting

Understanding of qualitative characteristics of financial reporting is significant to resolve

any complexity in routine accounting tasks. Following points explains characteristics of

financial accounting, as follows:

Timeliness – It ensures that right information is available at right time in a business

entity with aim to timely reporting of financial information. Corporates reports or files

its financial statement annually and in special exceptional cases reporting may be done on

quarterly basis (Cohen, J.R. and et.al., 2013). A delay in reporting may leads to legal

punishment and miss-understanding in stakeholders.

Relevance – It assures that relevant and reliable sources are used to access information

for preparing financial statements, to maintain relevance of information presented for

shareholders.

Faithful Representation – Building trust and faith in main aim of financial reporting so

financial statements emphasises on faithful representation of fiscal data.

Understandability – It facilities providing information in financial accounts which is

easily understandable all kind of people belongs to financial and non financial sectors.

3. Main Stakeholder and benefit to financial information

In corporate terms, stakeholders are key personnels, corporates and other trade entities

which can influence the business of entity and can be influenced by decisions and operations of

company. Every organisation prepare strategies while considering benefits of its various

stakeholders. Steps taken by different stakeholder can alter or influence company's decisions.

4

There are differentiated as internal and external stakeholders as per their influence power and

place.

Internal stakeholders

These are internal part of a business enterprise and having more effective influential

power upon entity. Company's actions also affects them positively or negatively. So analysis of

these stakeholders can provide more efficiency in organisation's decisions. Below discussed are

crucial internal stakeholder: Equity Holders: They holds ownership in company through investing money in

company's securities. Mostly in large organisation equity holders are person or entity who

are also company's promoters, managing directors and part of higher management

(Fernández-Feijóo-Souto, Romero and Ruiz-Blanco, 2012). They are benefited by getting

part in incomes or profits of company.

Employees – They are get benefited by company's performance as they want to get job

security, promotions, retirement benefits.

External stakeholders

These kinds of stakeholders are not officially interested in the day-to-day tasks and

operations of the company, but are duly affected by the operation of an organization. Below

discussed are vital external stakeholder:

Investors- Investors are fundamental stakeholders of a business entity, which receive

percentage part in net profit on investment made by them in company. Investor decisions

have direct impact on organisation's course of actions and strategies.

Creditors: They provides credits and short term loans to company, having direct impact

on company's working capital funds. They are benefited by company as they receive

timely payments from company. They use financial reporting information of company to

decide the term of credit.

Government: They are regulators of industry, decisions of company is made by

considering steps and policies of company. Government receives, taxes on net profit

earned by companies, so it is beneficial for regulatory authority or government to

analyses financial statement of company.

5

place.

Internal stakeholders

These are internal part of a business enterprise and having more effective influential

power upon entity. Company's actions also affects them positively or negatively. So analysis of

these stakeholders can provide more efficiency in organisation's decisions. Below discussed are

crucial internal stakeholder: Equity Holders: They holds ownership in company through investing money in

company's securities. Mostly in large organisation equity holders are person or entity who

are also company's promoters, managing directors and part of higher management

(Fernández-Feijóo-Souto, Romero and Ruiz-Blanco, 2012). They are benefited by getting

part in incomes or profits of company.

Employees – They are get benefited by company's performance as they want to get job

security, promotions, retirement benefits.

External stakeholders

These kinds of stakeholders are not officially interested in the day-to-day tasks and

operations of the company, but are duly affected by the operation of an organization. Below

discussed are vital external stakeholder:

Investors- Investors are fundamental stakeholders of a business entity, which receive

percentage part in net profit on investment made by them in company. Investor decisions

have direct impact on organisation's course of actions and strategies.

Creditors: They provides credits and short term loans to company, having direct impact

on company's working capital funds. They are benefited by company as they receive

timely payments from company. They use financial reporting information of company to

decide the term of credit.

Government: They are regulators of industry, decisions of company is made by

considering steps and policies of company. Government receives, taxes on net profit

earned by companies, so it is beneficial for regulatory authority or government to

analyses financial statement of company.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Value of financial reporting to meet objective and growth

Adoption of financial reporting is essential for making effective and credible financial

statements. Financial statements provides at least two year's results which makes easy for

company to make effective comparison. Managerial planning and decision-making is also

depends on results provided under reporting. Company's growth structure is determined by

managers by analysing company's annual reports.

Financial Reporting and development of organisation

Financial reporting provide a core basis for effective development of organisational

structure. At first it help to make improvement in accounting processes as it contains specific

guidance for recording, posting and formulating yearly accounts (Jhunjhunwala, 2014). It also

help to track the flow of funds and resources to develop a effective funding and management

structure.

Financial reporting and growth of business

A compete and comparative analysis of financial data reporting by corporate entities,

provides help in making momentary and instantaneous decisions. Which ultimately leads to

growth of entity in all sectors. Financial reporting defines the objectives and performance of

company to ensure its future growth. Any growth oriented strategy is also developed by business

entity on the basis of company's reported figures.

6

Adoption of financial reporting is essential for making effective and credible financial

statements. Financial statements provides at least two year's results which makes easy for

company to make effective comparison. Managerial planning and decision-making is also

depends on results provided under reporting. Company's growth structure is determined by

managers by analysing company's annual reports.

Financial Reporting and development of organisation

Financial reporting provide a core basis for effective development of organisational

structure. At first it help to make improvement in accounting processes as it contains specific

guidance for recording, posting and formulating yearly accounts (Jhunjhunwala, 2014). It also

help to track the flow of funds and resources to develop a effective funding and management

structure.

Financial reporting and growth of business

A compete and comparative analysis of financial data reporting by corporate entities,

provides help in making momentary and instantaneous decisions. Which ultimately leads to

growth of entity in all sectors. Financial reporting defines the objectives and performance of

company to ensure its future growth. Any growth oriented strategy is also developed by business

entity on the basis of company's reported figures.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

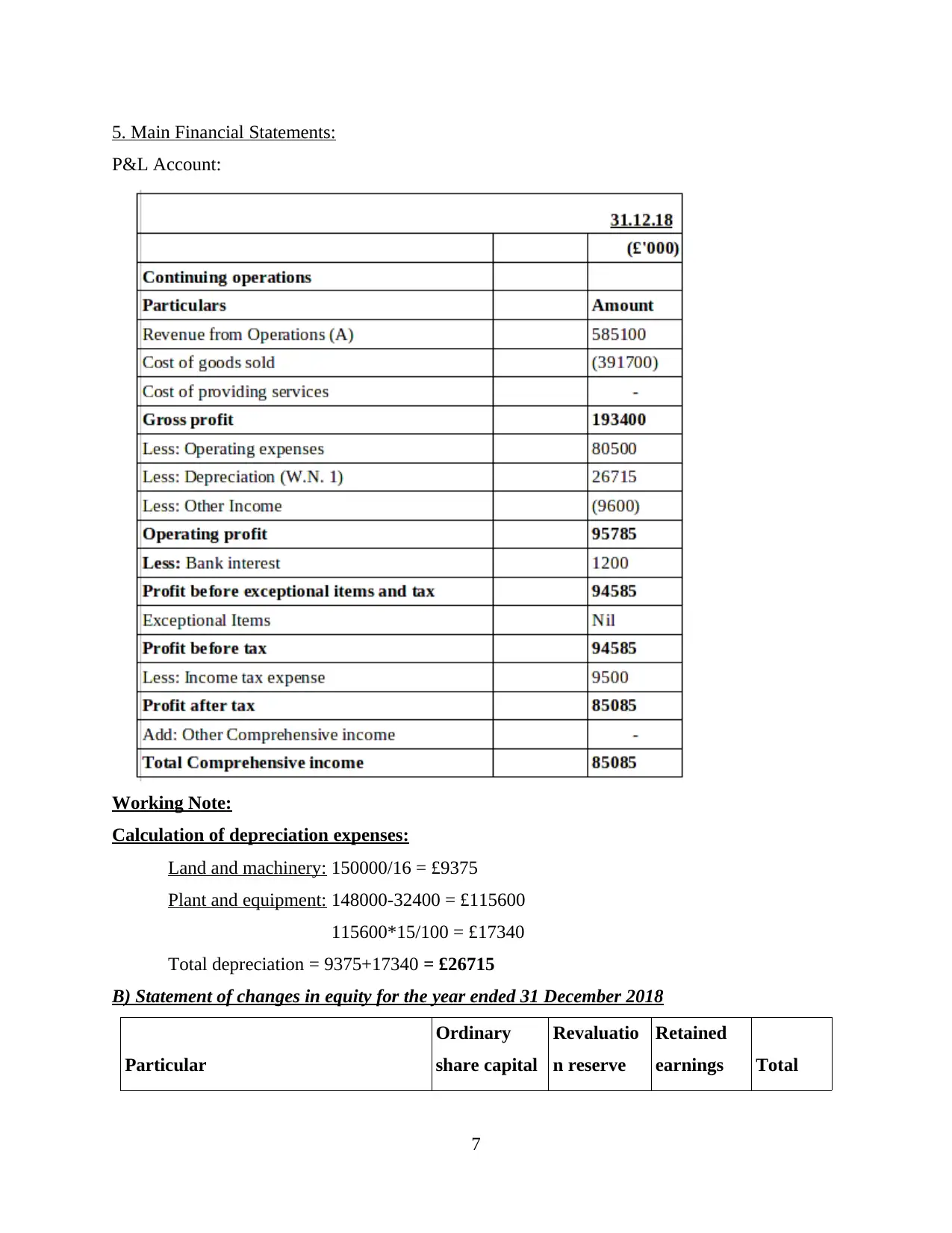

5. Main Financial Statements:

P&L Account:

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

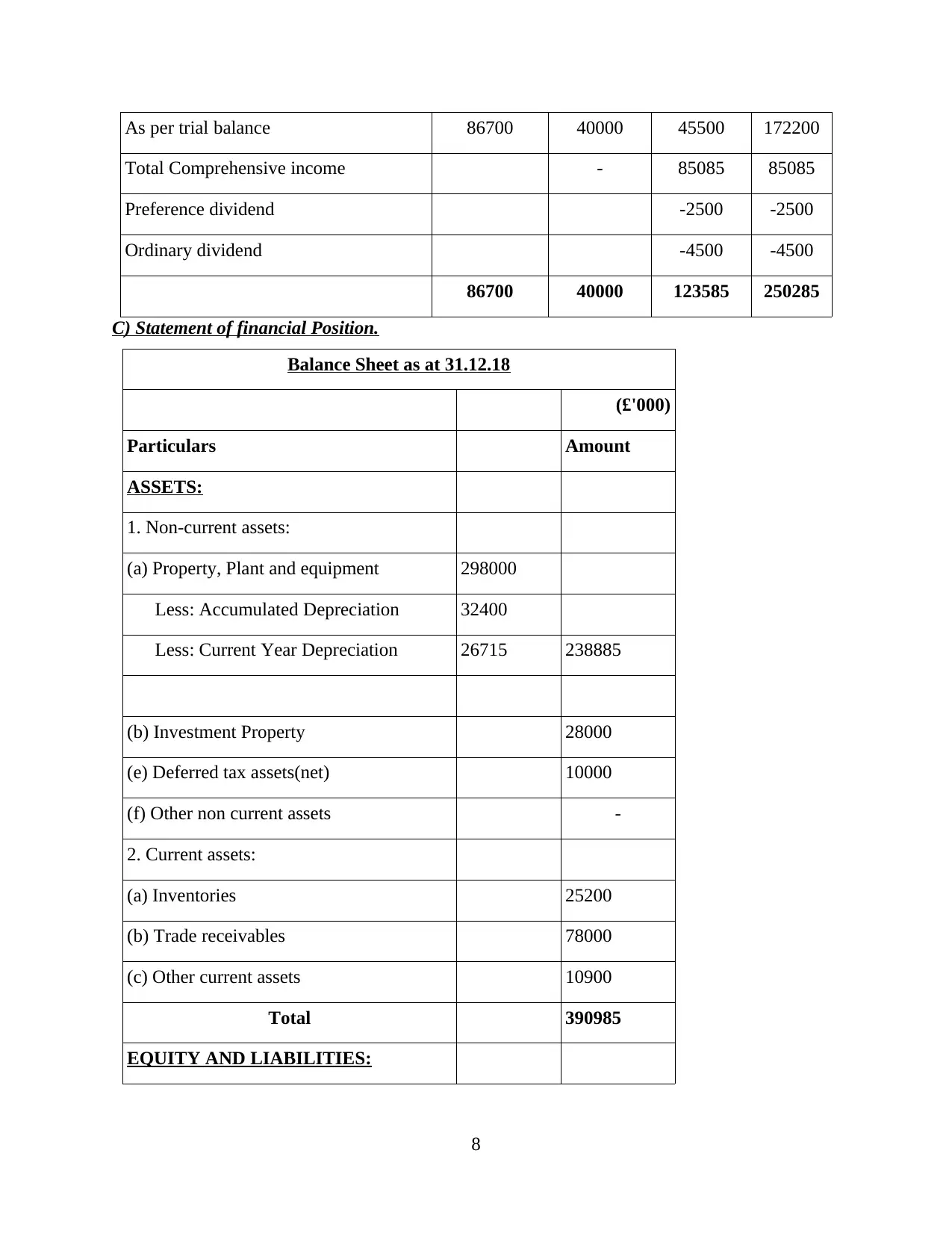

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

7

P&L Account:

Working Note:

Calculation of depreciation expenses:

Land and machinery: 150000/16 = £9375

Plant and equipment: 148000-32400 = £115600

115600*15/100 = £17340

Total depreciation = 9375+17340 = £26715

B) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluatio

n reserve

Retained

earnings Total

7

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

C) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

8

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

C) Statement of financial Position.

Balance Sheet as at 31.12.18

(£'000)

Particulars Amount

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

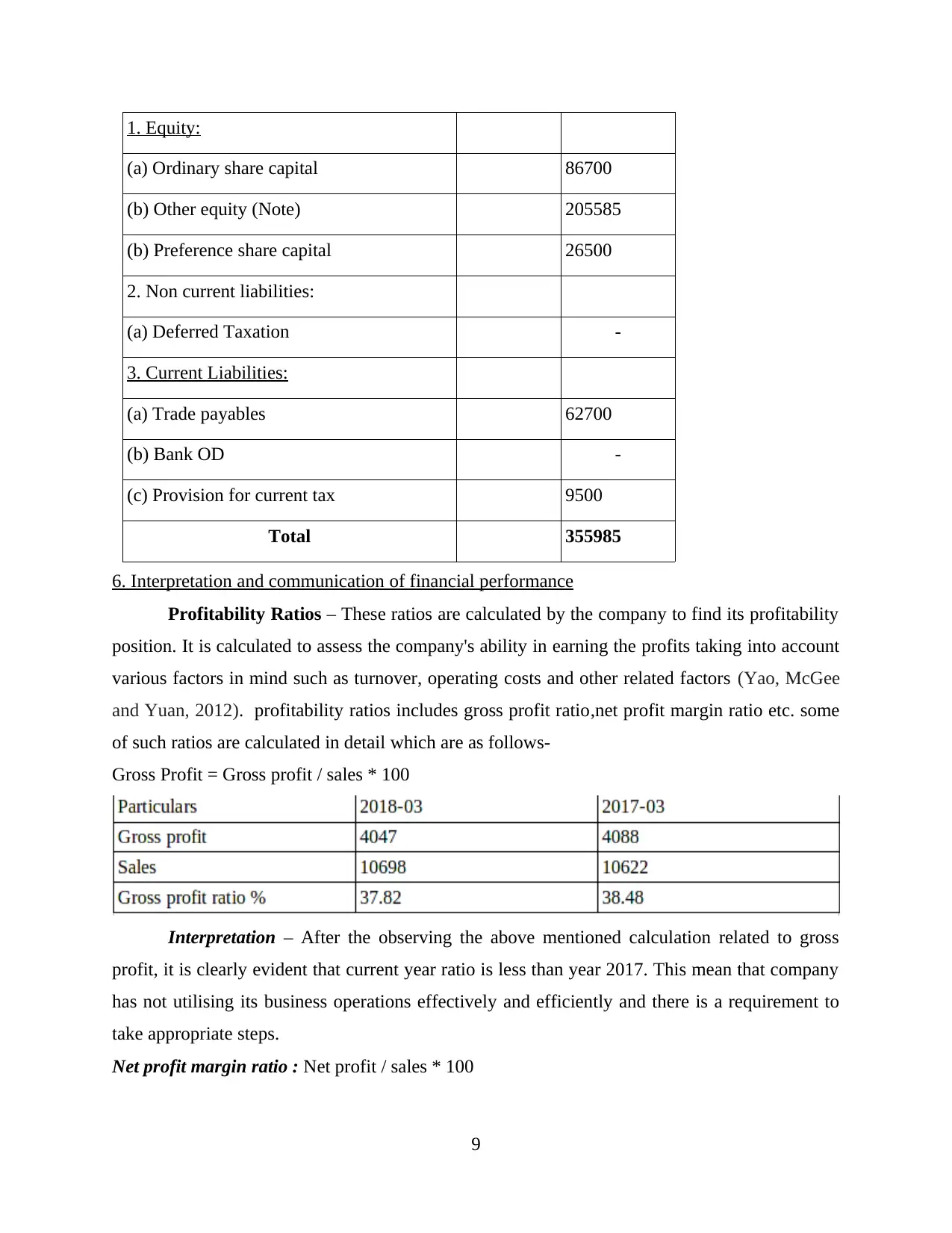

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

6. Interpretation and communication of financial performance

Profitability Ratios – These ratios are calculated by the company to find its profitability

position. It is calculated to assess the company's ability in earning the profits taking into account

various factors in mind such as turnover, operating costs and other related factors (Yao, McGee

and Yuan, 2012). profitability ratios includes gross profit ratio,net profit margin ratio etc. some

of such ratios are calculated in detail which are as follows-

Gross Profit = Gross profit / sales * 100

Interpretation – After the observing the above mentioned calculation related to gross

profit, it is clearly evident that current year ratio is less than year 2017. This mean that company

has not utilising its business operations effectively and efficiently and there is a requirement to

take appropriate steps.

Net profit margin ratio : Net profit / sales * 100

9

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

6. Interpretation and communication of financial performance

Profitability Ratios – These ratios are calculated by the company to find its profitability

position. It is calculated to assess the company's ability in earning the profits taking into account

various factors in mind such as turnover, operating costs and other related factors (Yao, McGee

and Yuan, 2012). profitability ratios includes gross profit ratio,net profit margin ratio etc. some

of such ratios are calculated in detail which are as follows-

Gross Profit = Gross profit / sales * 100

Interpretation – After the observing the above mentioned calculation related to gross

profit, it is clearly evident that current year ratio is less than year 2017. This mean that company

has not utilising its business operations effectively and efficiently and there is a requirement to

take appropriate steps.

Net profit margin ratio : Net profit / sales * 100

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

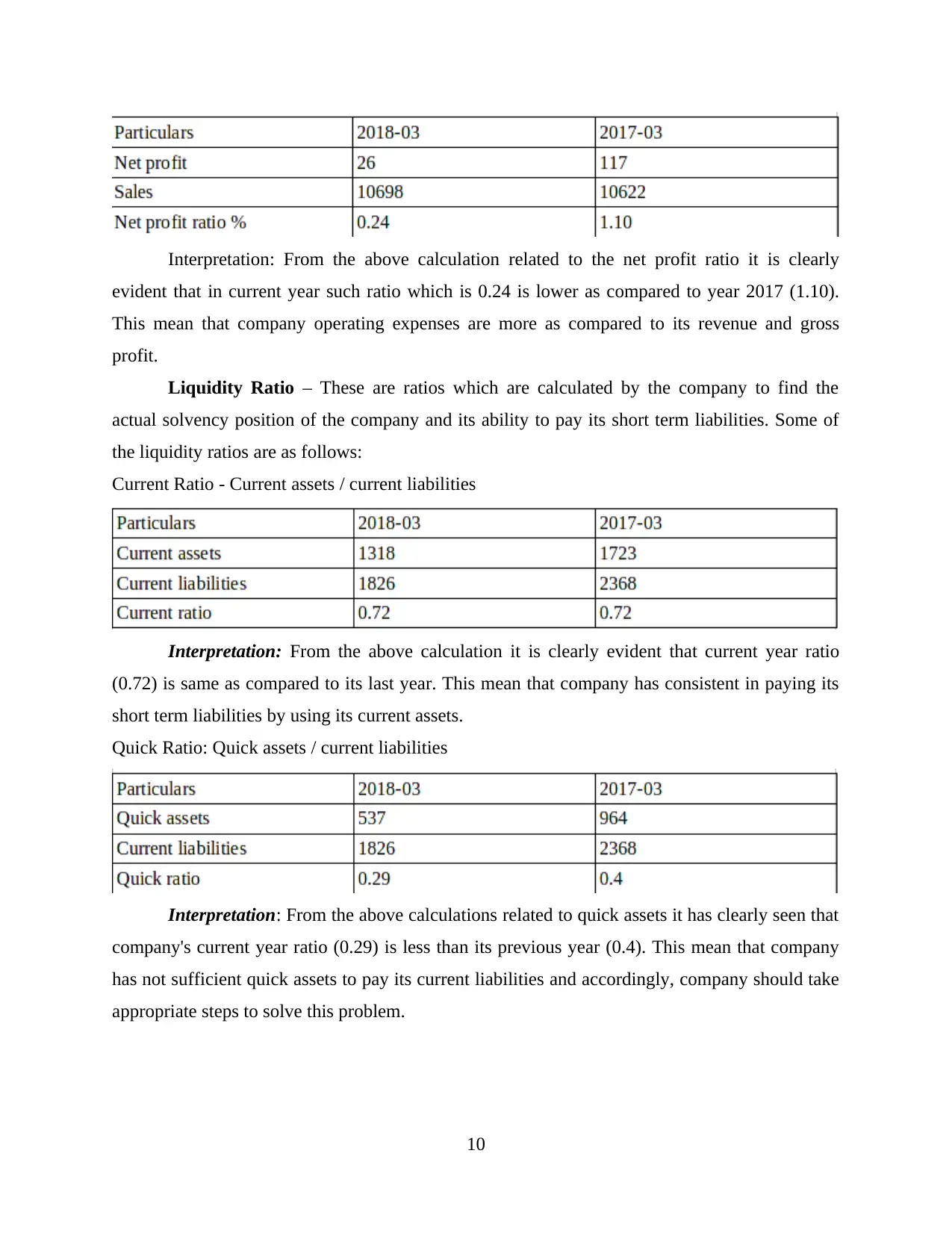

Interpretation: From the above calculation related to the net profit ratio it is clearly

evident that in current year such ratio which is 0.24 is lower as compared to year 2017 (1.10).

This mean that company operating expenses are more as compared to its revenue and gross

profit.

Liquidity Ratio – These are ratios which are calculated by the company to find the

actual solvency position of the company and its ability to pay its short term liabilities. Some of

the liquidity ratios are as follows:

Current Ratio - Current assets / current liabilities

Interpretation: From the above calculation it is clearly evident that current year ratio

(0.72) is same as compared to its last year. This mean that company has consistent in paying its

short term liabilities by using its current assets.

Quick Ratio: Quick assets / current liabilities

Interpretation: From the above calculations related to quick assets it has clearly seen that

company's current year ratio (0.29) is less than its previous year (0.4). This mean that company

has not sufficient quick assets to pay its current liabilities and accordingly, company should take

appropriate steps to solve this problem.

10

evident that in current year such ratio which is 0.24 is lower as compared to year 2017 (1.10).

This mean that company operating expenses are more as compared to its revenue and gross

profit.

Liquidity Ratio – These are ratios which are calculated by the company to find the

actual solvency position of the company and its ability to pay its short term liabilities. Some of

the liquidity ratios are as follows:

Current Ratio - Current assets / current liabilities

Interpretation: From the above calculation it is clearly evident that current year ratio

(0.72) is same as compared to its last year. This mean that company has consistent in paying its

short term liabilities by using its current assets.

Quick Ratio: Quick assets / current liabilities

Interpretation: From the above calculations related to quick assets it has clearly seen that

company's current year ratio (0.29) is less than its previous year (0.4). This mean that company

has not sufficient quick assets to pay its current liabilities and accordingly, company should take

appropriate steps to solve this problem.

10

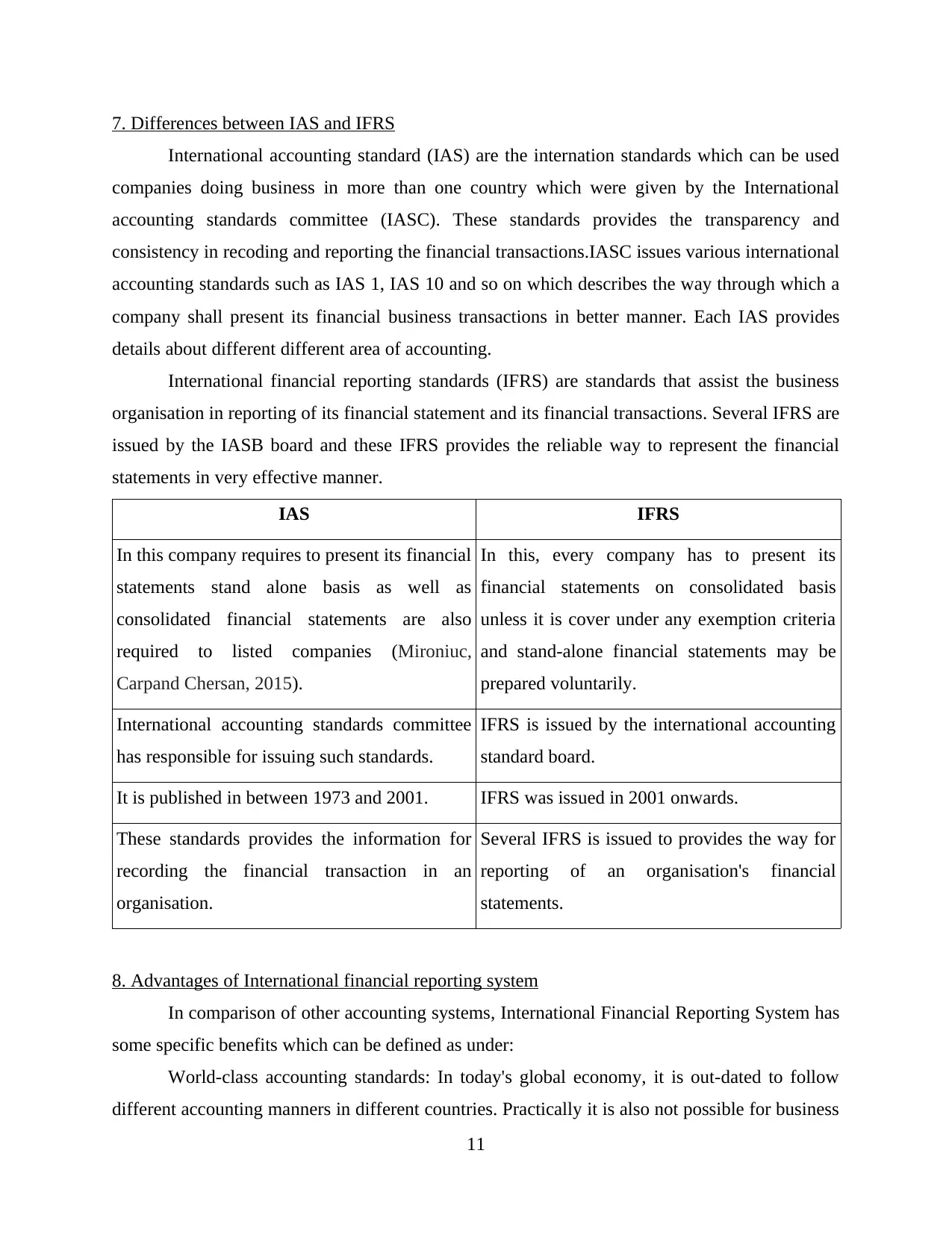

7. Differences between IAS and IFRS

International accounting standard (IAS) are the internation standards which can be used

companies doing business in more than one country which were given by the International

accounting standards committee (IASC). These standards provides the transparency and

consistency in recoding and reporting the financial transactions.IASC issues various international

accounting standards such as IAS 1, IAS 10 and so on which describes the way through which a

company shall present its financial business transactions in better manner. Each IAS provides

details about different different area of accounting.

International financial reporting standards (IFRS) are standards that assist the business

organisation in reporting of its financial statement and its financial transactions. Several IFRS are

issued by the IASB board and these IFRS provides the reliable way to represent the financial

statements in very effective manner.

IAS IFRS

In this company requires to present its financial

statements stand alone basis as well as

consolidated financial statements are also

required to listed companies (Mironiuc,

Carpand Chersan, 2015).

In this, every company has to present its

financial statements on consolidated basis

unless it is cover under any exemption criteria

and stand-alone financial statements may be

prepared voluntarily.

International accounting standards committee

has responsible for issuing such standards.

IFRS is issued by the international accounting

standard board.

It is published in between 1973 and 2001. IFRS was issued in 2001 onwards.

These standards provides the information for

recording the financial transaction in an

organisation.

Several IFRS is issued to provides the way for

reporting of an organisation's financial

statements.

8. Advantages of International financial reporting system

In comparison of other accounting systems, International Financial Reporting System has

some specific benefits which can be defined as under:

World-class accounting standards: In today's global economy, it is out-dated to follow

different accounting manners in different countries. Practically it is also not possible for business

11

International accounting standard (IAS) are the internation standards which can be used

companies doing business in more than one country which were given by the International

accounting standards committee (IASC). These standards provides the transparency and

consistency in recoding and reporting the financial transactions.IASC issues various international

accounting standards such as IAS 1, IAS 10 and so on which describes the way through which a

company shall present its financial business transactions in better manner. Each IAS provides

details about different different area of accounting.

International financial reporting standards (IFRS) are standards that assist the business

organisation in reporting of its financial statement and its financial transactions. Several IFRS are

issued by the IASB board and these IFRS provides the reliable way to represent the financial

statements in very effective manner.

IAS IFRS

In this company requires to present its financial

statements stand alone basis as well as

consolidated financial statements are also

required to listed companies (Mironiuc,

Carpand Chersan, 2015).

In this, every company has to present its

financial statements on consolidated basis

unless it is cover under any exemption criteria

and stand-alone financial statements may be

prepared voluntarily.

International accounting standards committee

has responsible for issuing such standards.

IFRS is issued by the international accounting

standard board.

It is published in between 1973 and 2001. IFRS was issued in 2001 onwards.

These standards provides the information for

recording the financial transaction in an

organisation.

Several IFRS is issued to provides the way for

reporting of an organisation's financial

statements.

8. Advantages of International financial reporting system

In comparison of other accounting systems, International Financial Reporting System has

some specific benefits which can be defined as under:

World-class accounting standards: In today's global economy, it is out-dated to follow

different accounting manners in different countries. Practically it is also not possible for business

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.