International Financial Reporting Standards (IFRS) Impact on Investors

VerifiedAdded on 2021/05/31

|8

|1088

|50

Report

AI Summary

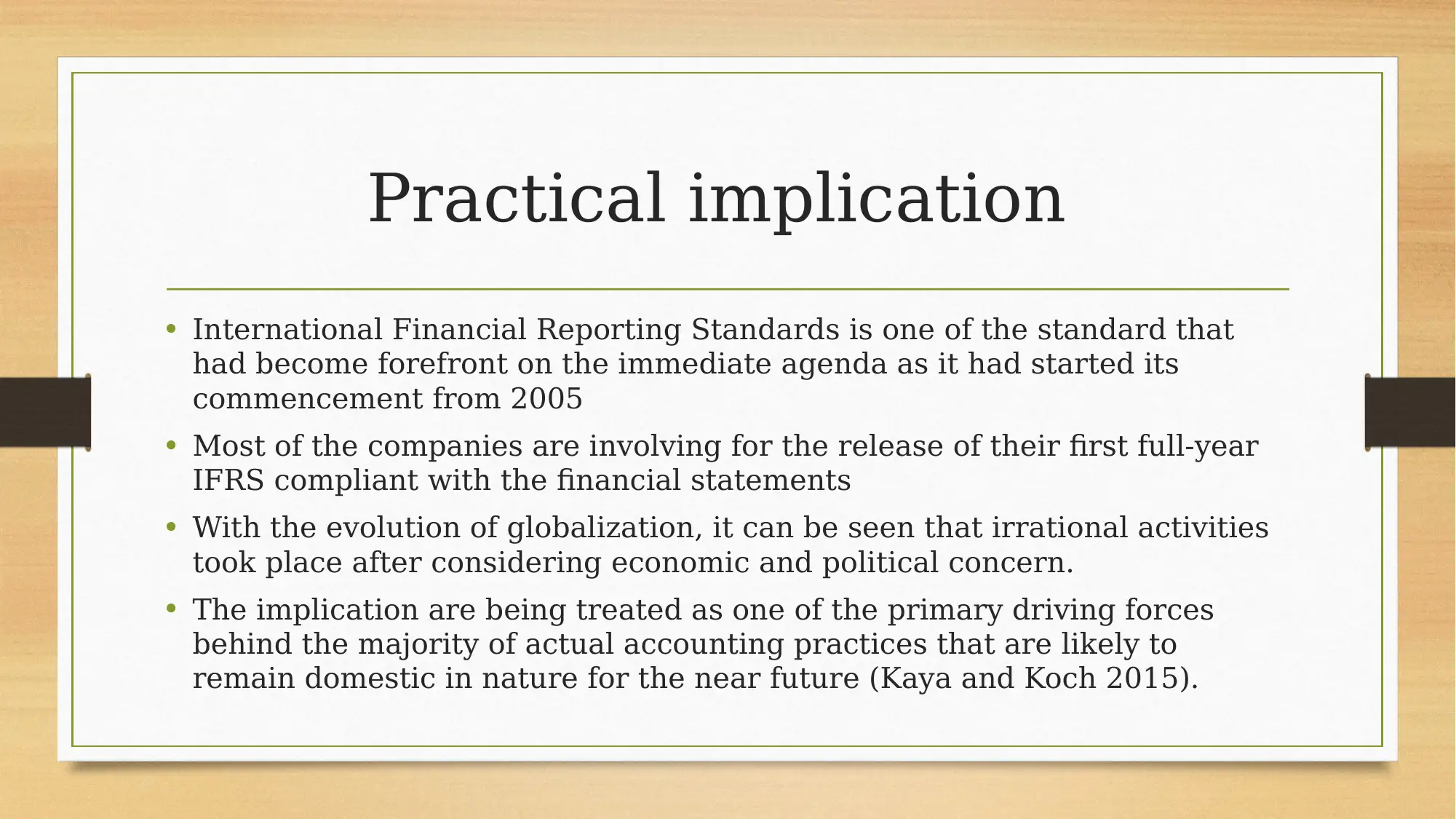

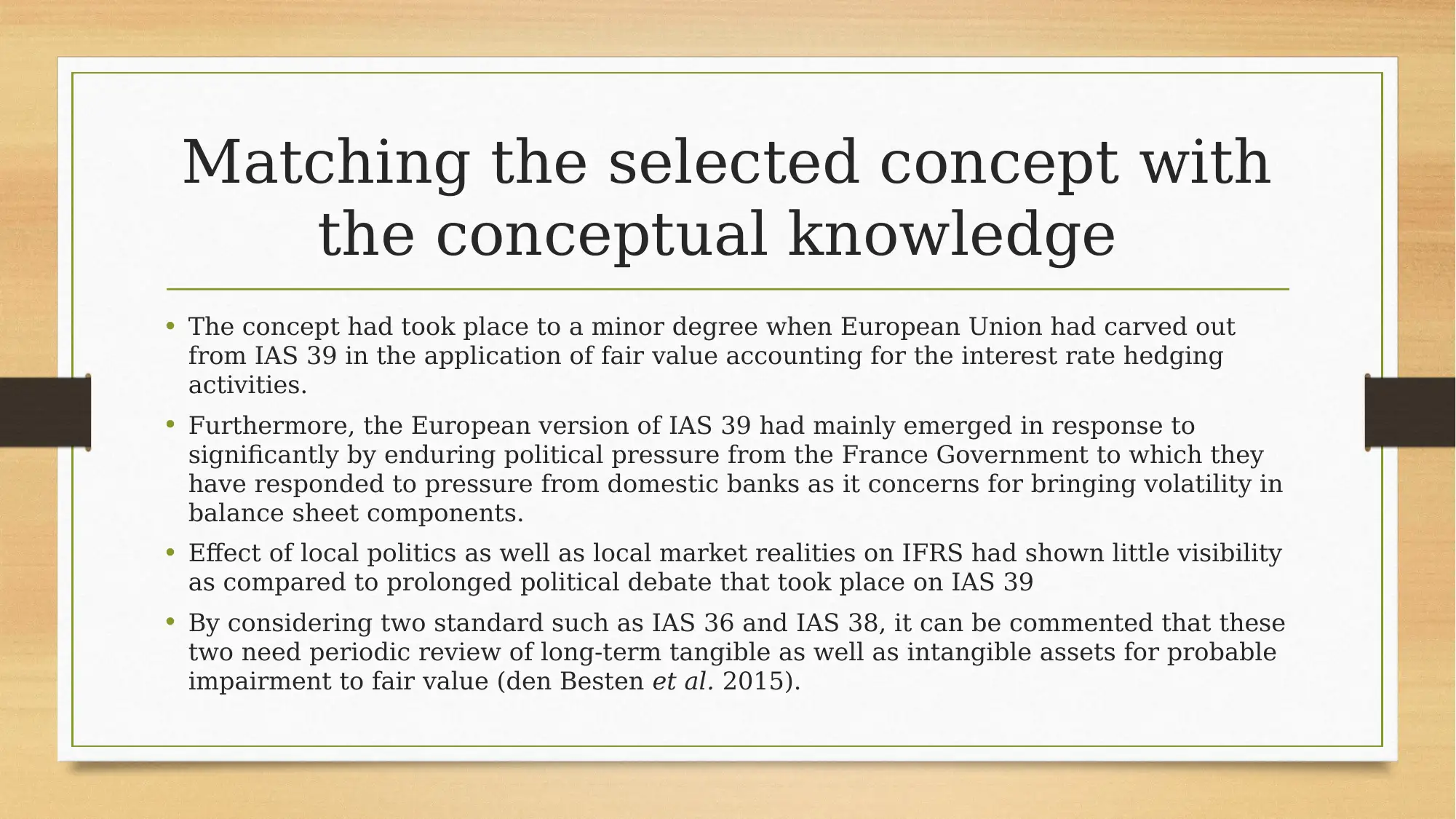

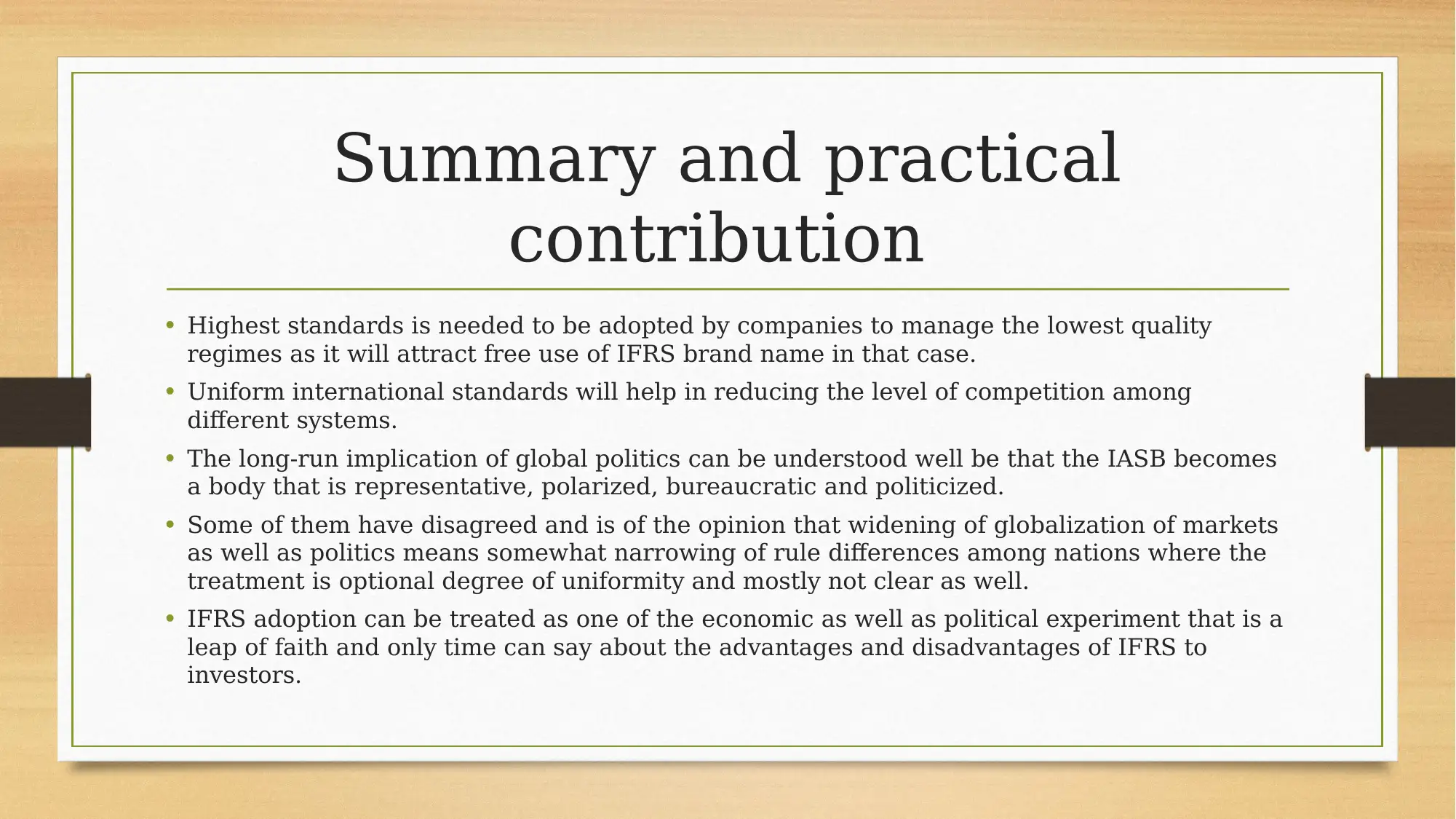

This report examines the International Financial Reporting Standards (IFRS) and its implications for investors. It discusses the advantages, such as the development of high-quality international standards and uniform financial reporting, and disadvantages, including issues with fair value accounting and the influence of local politics. The report highlights the practical implications of IFRS adoption, the impact of local market realities, and the need for periodic reviews of assets. It emphasizes the importance of adopting high standards to maintain the integrity of the IFRS brand and the potential long-term effects of globalization on accounting practices. The document references various studies and provides insights into the ongoing debate surrounding IFRS adoption, treating it as an economic and political experiment. The report concludes that only time will reveal the true benefits and drawbacks of IFRS for investors, making it a valuable resource for understanding the complexities of global financial reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.