International Financial Reporting Standards: Lease Accounting

VerifiedAdded on 2021/02/20

|21

|5143

|128

Report

AI Summary

This report delves into the realm of International Financial Reporting Standards (IFRS), specifically focusing on lease accounting. The report begins with an introduction to IFRS and then details the accounting treatments for both lessees and lessors under IAS 16 and IAS 17. It differentiates between finance and operating leases, outlining the specific conditions and rules associated with each type. The report also explores how leases are accounted for in financial statements. Furthermore, the report includes a detailed case study of Royjoy Limited, calculating the implicit interest rate and providing an amortization schedule to illustrate the application of IFRS in practice. The analysis covers the impact of lease accounting on financial statements, providing a comprehensive understanding of the subject.

INTERNATIONAL

FINANCIAL

REPORTING

FINANCIAL

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY..................................................................................................................................................3

Part (1) ....................................................................................................................................................3

Part (2)...................................................................................................................................................11

Part (3)...................................................................................................................................................14

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION...........................................................................................................................................3

MAIN BODY..................................................................................................................................................3

Part (1) ....................................................................................................................................................3

Part (2)...................................................................................................................................................11

Part (3)...................................................................................................................................................14

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION

The international financial reporting can be defined as a process of producing the

financial statements on the basis of international accounting standards (Alali and Foote, 2012).

Eventually, it is necessary for the organizations who perform at a global level to implement

various kind of accounting concept and standards. Generally, the accounting standards are issued

by the international accounting standard board. Herein, the project report various kind of

accounting standards are mentioned that helps to the companies to take crucial decision making.

The project report covers about the various accounting treatments in an individual accounting

standard as well as defines about way to apply accounting treatment on the financial treatments.

Apart from it, report is categorized into three parts that consist knowledge about IAS 17, 16 and

2.

MAIN BODY

Part (1)

(a) Description about international accounting standard 16 for lease treatment.

Lease can be defined as an agreement that is related to conveying the one party the right

to use property.

Lease contract- It is a kind of contract between two parties wherein, one party gives right

to another party to use of an assets for a particular time period.

Characteristics of a lease contract:

The term lease includes non cancellable time period of a lease with both to the time

covered by an option to extend the lease. As well as time period covered by an option to

limits the lease contract.

In IFRS 16, those leases are covered which are of 12 months.

There are certain conditions and rules of lease agreement.

According to the international accounting standard 16, the accounting policies and

principles are applicable for both to the lessees, lessors (About accounting standard,2018).

Eventually, the leases are categorized as finance lease and operating lease. Eventually, the IAS

16, was evolved for lessors and lessees as well as for accurate accounting policies and principles

The international financial reporting can be defined as a process of producing the

financial statements on the basis of international accounting standards (Alali and Foote, 2012).

Eventually, it is necessary for the organizations who perform at a global level to implement

various kind of accounting concept and standards. Generally, the accounting standards are issued

by the international accounting standard board. Herein, the project report various kind of

accounting standards are mentioned that helps to the companies to take crucial decision making.

The project report covers about the various accounting treatments in an individual accounting

standard as well as defines about way to apply accounting treatment on the financial treatments.

Apart from it, report is categorized into three parts that consist knowledge about IAS 17, 16 and

2.

MAIN BODY

Part (1)

(a) Description about international accounting standard 16 for lease treatment.

Lease can be defined as an agreement that is related to conveying the one party the right

to use property.

Lease contract- It is a kind of contract between two parties wherein, one party gives right

to another party to use of an assets for a particular time period.

Characteristics of a lease contract:

The term lease includes non cancellable time period of a lease with both to the time

covered by an option to extend the lease. As well as time period covered by an option to

limits the lease contract.

In IFRS 16, those leases are covered which are of 12 months.

There are certain conditions and rules of lease agreement.

According to the international accounting standard 16, the accounting policies and

principles are applicable for both to the lessees, lessors (About accounting standard,2018).

Eventually, the leases are categorized as finance lease and operating lease. Eventually, the IAS

16, was evolved for lessors and lessees as well as for accurate accounting policies and principles

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which are needed to be applied in relation to finance and operating lease. Herein, below some

principles are mentioned below which should be implemented in the financial statements of

lessees for finance lease:

During the commencement of lease, the finance lease must be considered as an assets and

also recorded as assets. As well as should be taken as liability at the lower value of the

assets and present value of the total payment of the lease.

Apart from it, the depreciation policy for any particular assets that covers under the

finance lease must be consistent (Cotter, 2012). As well as if it is not clear that lessee will

get the ownership in the end of lease then the assets should be depreciated during the

short time period of lease term.

Additionally, the payment of finance lease should be divided between the finance charge

and minimized outstanding liability. Herein, it is important to know that finance charge

should be assigned such as to produce the equal rate of interest on balance of liability.

So this is all about the finance lease that must be treated in above mentioned manner. Apart from

it, herein, below way to treat operating lease is mentioned below such as:

Eventually as the finance lease, the operating lease does not treated as recognition of an

assets or liability in the balance sheets of lessee. The income and expenditure of operating lease

is considered in the books of lessor or lessee at a uniform base. As per the international

accounting standard 16, in the operating lease accounting, it is being assumed that the lessor has

the leased assets and the lessee takes the assets for a particular fixed time period. So basically on

the basis of this kind of ownership and way to use the assets, the accounting treatment of an

operating lease by the lessee and lessor.

Operating lease accounting by lessee- If an operating lease consists fixed rental increasing

during the lease. In such condition, there are two ways to account for the altered payment which

are follows:

Scheduled increase- If there is scheduled increase in the rent on a straight line basis then

some recognition systems can present the usage of operating assets (Shan, and Taylor,

2015).

principles are mentioned below which should be implemented in the financial statements of

lessees for finance lease:

During the commencement of lease, the finance lease must be considered as an assets and

also recorded as assets. As well as should be taken as liability at the lower value of the

assets and present value of the total payment of the lease.

Apart from it, the depreciation policy for any particular assets that covers under the

finance lease must be consistent (Cotter, 2012). As well as if it is not clear that lessee will

get the ownership in the end of lease then the assets should be depreciated during the

short time period of lease term.

Additionally, the payment of finance lease should be divided between the finance charge

and minimized outstanding liability. Herein, it is important to know that finance charge

should be assigned such as to produce the equal rate of interest on balance of liability.

So this is all about the finance lease that must be treated in above mentioned manner. Apart from

it, herein, below way to treat operating lease is mentioned below such as:

Eventually as the finance lease, the operating lease does not treated as recognition of an

assets or liability in the balance sheets of lessee. The income and expenditure of operating lease

is considered in the books of lessor or lessee at a uniform base. As per the international

accounting standard 16, in the operating lease accounting, it is being assumed that the lessor has

the leased assets and the lessee takes the assets for a particular fixed time period. So basically on

the basis of this kind of ownership and way to use the assets, the accounting treatment of an

operating lease by the lessee and lessor.

Operating lease accounting by lessee- If an operating lease consists fixed rental increasing

during the lease. In such condition, there are two ways to account for the altered payment which

are follows:

Scheduled increase- If there is scheduled increase in the rent on a straight line basis then

some recognition systems can present the usage of operating assets (Shan, and Taylor,

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contingent rentals- If there is change in the lease payment which are based future events.

(inflation, tax occurred etc.)

Operating lease accounting by lessor- This must be account for lease in below mentioned way

which is as follows:

The leased property must be depreciate during its life.

The direct cost of the lease should be deferred.

(b) Explanation of ways in which leases should be accounted for financial statements of

lessee.

As accordance to the international accounting standard 16, herein some conditions in that

leases must be accounted for financial statements of lessee which are as follows:

- If lease contract allows to lessee to buy the same leased assets on a price that is below in

compare to fair value of assets in further.

-As well as in a condition in which term of lease is equal to 75% or more then to the 75% of the

total life of the leased assets.

-If present value of total payment of lease is more then the 90% of fair value of assets.

Lease accounting by lessee and lessor:

In general terms there are two kind of lease one is finance lease and second is operating

lease (Flower, 2018). The finance lease can be defined as to buy an assets by external finance.

As well as the operating lease is related to get an assets on rent.

Accounting for finance lease by lessee- The finance lease is presented by lessee such as in

various financial statements like:

Balance sheet- In this both the leased assets and lease liability is recorded.

Income statement- Under this the interest expenditure on the lease payable is recorded.

As well as it is being calculated on the basis of lease payment at starting applying the

interest rate in the lease. Cash flow statement- Interest of the payment of lease is being recorded as an operating

cash out flow in the cash flow statement. Along with, the repayment is recorded as a

(inflation, tax occurred etc.)

Operating lease accounting by lessor- This must be account for lease in below mentioned way

which is as follows:

The leased property must be depreciate during its life.

The direct cost of the lease should be deferred.

(b) Explanation of ways in which leases should be accounted for financial statements of

lessee.

As accordance to the international accounting standard 16, herein some conditions in that

leases must be accounted for financial statements of lessee which are as follows:

- If lease contract allows to lessee to buy the same leased assets on a price that is below in

compare to fair value of assets in further.

-As well as in a condition in which term of lease is equal to 75% or more then to the 75% of the

total life of the leased assets.

-If present value of total payment of lease is more then the 90% of fair value of assets.

Lease accounting by lessee and lessor:

In general terms there are two kind of lease one is finance lease and second is operating

lease (Flower, 2018). The finance lease can be defined as to buy an assets by external finance.

As well as the operating lease is related to get an assets on rent.

Accounting for finance lease by lessee- The finance lease is presented by lessee such as in

various financial statements like:

Balance sheet- In this both the leased assets and lease liability is recorded.

Income statement- Under this the interest expenditure on the lease payable is recorded.

As well as it is being calculated on the basis of lease payment at starting applying the

interest rate in the lease. Cash flow statement- Interest of the payment of lease is being recorded as an operating

cash out flow in the cash flow statement. Along with, the repayment is recorded as a

financing cash outflow. As well as the expenses of interest may be recorded as an

operating or financing cash outflow.

Accounting for operating lease by lessee- The operating lease is presented by lessee such as in

various financial statements like:

Balance sheet- The operating lease is not reported in the balance sheet.

Income statement- It includes the rent of assets that is similar to the lease payment.

Cash flow statement- Under it, the total payment of lease or rent is considered as

operating cash outflow (Walton, 2012).

Impact of lease accounting on the lessee’s financial statements- The variation of finance and

operating lease effects the different types of elements of financial statements such as:

Total income and cash flow remain equal in both leases.

Assets, liabilities, earning before income and tax of various operations are more in the

finance lease in compare to the operating lease.

Accounting for finance lease by the lessor-

Balance sheet- In this lease receivable is recorded. As well as value of the assets is

minimized on the basis of book value of the leased assets.

Income statement- In this the revenue from the interest is recorded. This is computed on

the basis of received lease in the starting of the interest rate in the lease. Cash flow statement- The interest of the revenue of lease is included in the cash flow

statement in the form of cash inflow. As well as the principle of the total payable amount

is recorded as an investing cash inflow.

Accounting for operating lease by the lessor-

Balance sheet- In this the leased assets is recorded.

Income statement- Under it, the interest revenue is recorded along with the depreciation

.Cash flow statement- Total payment is considered as an operating cash inflow in the

cash flow statement.

Impact of the lease accounting on the lessor’s financial statements: The difference of finance and

operating lease effects the different types of elements of financial statements such as:

operating or financing cash outflow.

Accounting for operating lease by lessee- The operating lease is presented by lessee such as in

various financial statements like:

Balance sheet- The operating lease is not reported in the balance sheet.

Income statement- It includes the rent of assets that is similar to the lease payment.

Cash flow statement- Under it, the total payment of lease or rent is considered as

operating cash outflow (Walton, 2012).

Impact of lease accounting on the lessee’s financial statements- The variation of finance and

operating lease effects the different types of elements of financial statements such as:

Total income and cash flow remain equal in both leases.

Assets, liabilities, earning before income and tax of various operations are more in the

finance lease in compare to the operating lease.

Accounting for finance lease by the lessor-

Balance sheet- In this lease receivable is recorded. As well as value of the assets is

minimized on the basis of book value of the leased assets.

Income statement- In this the revenue from the interest is recorded. This is computed on

the basis of received lease in the starting of the interest rate in the lease. Cash flow statement- The interest of the revenue of lease is included in the cash flow

statement in the form of cash inflow. As well as the principle of the total payable amount

is recorded as an investing cash inflow.

Accounting for operating lease by the lessor-

Balance sheet- In this the leased assets is recorded.

Income statement- Under it, the interest revenue is recorded along with the depreciation

.Cash flow statement- Total payment is considered as an operating cash inflow in the

cash flow statement.

Impact of the lease accounting on the lessor’s financial statements: The difference of finance and

operating lease effects the different types of elements of financial statements such as:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income of the early year is more then the finance lease.

Income of the later year is less then the finance lease.

The total amount of tax in the initial year is more in the finance lease in compare to the

operating lease. The operating cash flow is more of the operating lease in compare to the finance lease

(Erb and Pelger, 2015).

So these are the ways in which the leases should be accounted for financial statements of lessee.

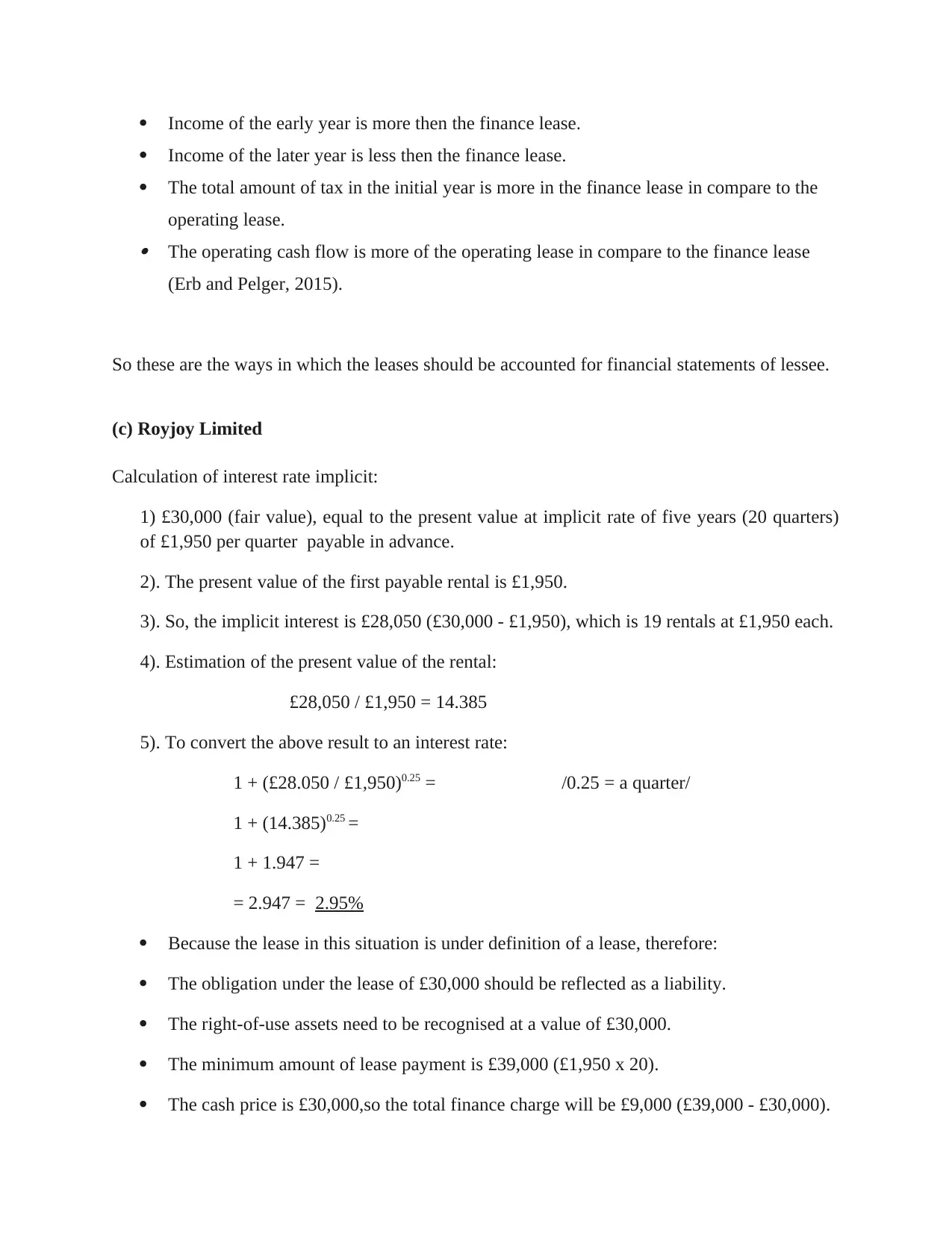

(c) Royjoy Limited

Calculation of interest rate implicit:

1) £30,000 (fair value), equal to the present value at implicit rate of five years (20 quarters)

of £1,950 per quarter payable in advance.

2). The present value of the first payable rental is £1,950.

3). So, the implicit interest is £28,050 (£30,000 - £1,950), which is 19 rentals at £1,950 each.

4). Estimation of the present value of the rental:

£28,050 / £1,950 = 14.385

5). To convert the above result to an interest rate:

1 + (£28.050 / £1,950)0.25 = /0.25 = a quarter/

1 + (14.385)0.25 =

1 + 1.947 =

= 2.947 = 2.95%

Because the lease in this situation is under definition of a lease, therefore:

The obligation under the lease of £30,000 should be reflected as a liability.

The right-of-use assets need to be recognised at a value of £30,000.

The minimum amount of lease payment is £39,000 (£1,950 x 20).

The cash price is £30,000,so the total finance charge will be £9,000 (£39,000 - £30,000).

Income of the later year is less then the finance lease.

The total amount of tax in the initial year is more in the finance lease in compare to the

operating lease. The operating cash flow is more of the operating lease in compare to the finance lease

(Erb and Pelger, 2015).

So these are the ways in which the leases should be accounted for financial statements of lessee.

(c) Royjoy Limited

Calculation of interest rate implicit:

1) £30,000 (fair value), equal to the present value at implicit rate of five years (20 quarters)

of £1,950 per quarter payable in advance.

2). The present value of the first payable rental is £1,950.

3). So, the implicit interest is £28,050 (£30,000 - £1,950), which is 19 rentals at £1,950 each.

4). Estimation of the present value of the rental:

£28,050 / £1,950 = 14.385

5). To convert the above result to an interest rate:

1 + (£28.050 / £1,950)0.25 = /0.25 = a quarter/

1 + (14.385)0.25 =

1 + 1.947 =

= 2.947 = 2.95%

Because the lease in this situation is under definition of a lease, therefore:

The obligation under the lease of £30,000 should be reflected as a liability.

The right-of-use assets need to be recognised at a value of £30,000.

The minimum amount of lease payment is £39,000 (£1,950 x 20).

The cash price is £30,000,so the total finance charge will be £9,000 (£39,000 - £30,000).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On 1 January 2019:

Debit right-of-use asset account - £30,000

Credit lessor - £30,000

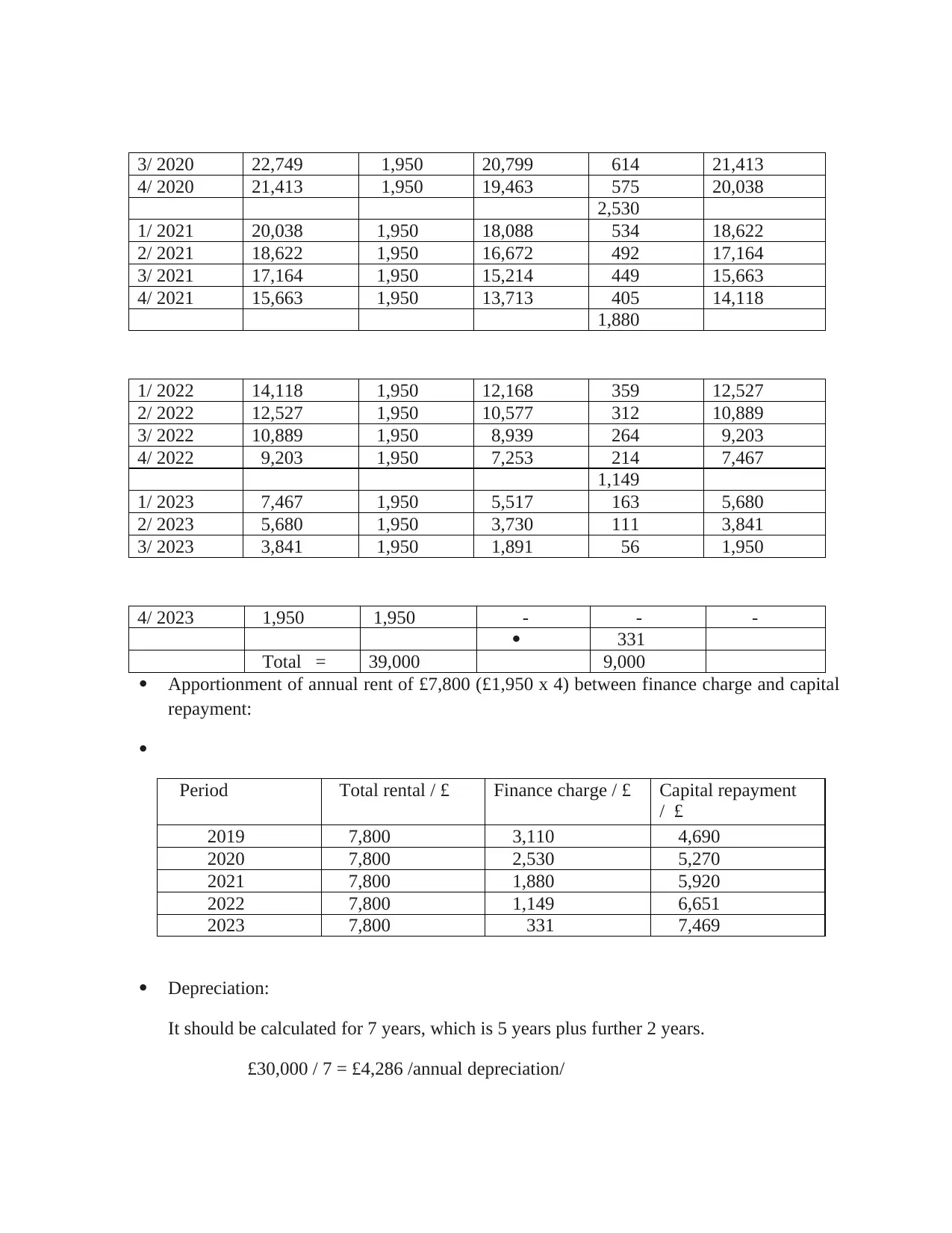

Period in

quarters

Capital sum

at start of

period / £

Rentals

Paid / £

Capital sum

during

period / £

Finance

charge

(2.95%) / £

Capital sum

at end of

period / £

1/ 2019 30,000 1,950 28,050 828 28,878

2/ 2019 28,878 1,950 26,928 795 27,723

3/ 2019 27,723 1,950 25,772 761 26,533

4/ 2019 26,533 1,950 24,582 726 25,308

3, 110

1/ 2020 25,308 1,950 23,358 689 24,047

2/ 2020 24,047 1,950 22,097 652 22,749

Debit right-of-use asset account - £30,000

Credit lessor - £30,000

Period in

quarters

Capital sum

at start of

period / £

Rentals

Paid / £

Capital sum

during

period / £

Finance

charge

(2.95%) / £

Capital sum

at end of

period / £

1/ 2019 30,000 1,950 28,050 828 28,878

2/ 2019 28,878 1,950 26,928 795 27,723

3/ 2019 27,723 1,950 25,772 761 26,533

4/ 2019 26,533 1,950 24,582 726 25,308

3, 110

1/ 2020 25,308 1,950 23,358 689 24,047

2/ 2020 24,047 1,950 22,097 652 22,749

3/ 2020 22,749 1,950 20,799 614 21,413

4/ 2020 21,413 1,950 19,463 575 20,038

2,530

1/ 2021 20,038 1,950 18,088 534 18,622

2/ 2021 18,622 1,950 16,672 492 17,164

3/ 2021 17,164 1,950 15,214 449 15,663

4/ 2021 15,663 1,950 13,713 405 14,118

1,880

1/ 2022 14,118 1,950 12,168 359 12,527

2/ 2022 12,527 1,950 10,577 312 10,889

3/ 2022 10,889 1,950 8,939 264 9,203

4/ 2022 9,203 1,950 7,253 214 7,467

1,149

1/ 2023 7,467 1,950 5,517 163 5,680

2/ 2023 5,680 1,950 3,730 111 3,841

3/ 2023 3,841 1,950 1,891 56 1,950

4/ 2023 1,950 1,950 - - -

331

Total = 39,000 9,000

Apportionment of annual rent of £7,800 (£1,950 x 4) between finance charge and capital

repayment:

Period Total rental / £ Finance charge / £ Capital repayment

/ £

2019 7,800 3,110 4,690

2020 7,800 2,530 5,270

2021 7,800 1,880 5,920

2022 7,800 1,149 6,651

2023 7,800 331 7,469

Depreciation:

It should be calculated for 7 years, which is 5 years plus further 2 years.

£30,000 / 7 = £4,286 /annual depreciation/

4/ 2020 21,413 1,950 19,463 575 20,038

2,530

1/ 2021 20,038 1,950 18,088 534 18,622

2/ 2021 18,622 1,950 16,672 492 17,164

3/ 2021 17,164 1,950 15,214 449 15,663

4/ 2021 15,663 1,950 13,713 405 14,118

1,880

1/ 2022 14,118 1,950 12,168 359 12,527

2/ 2022 12,527 1,950 10,577 312 10,889

3/ 2022 10,889 1,950 8,939 264 9,203

4/ 2022 9,203 1,950 7,253 214 7,467

1,149

1/ 2023 7,467 1,950 5,517 163 5,680

2/ 2023 5,680 1,950 3,730 111 3,841

3/ 2023 3,841 1,950 1,891 56 1,950

4/ 2023 1,950 1,950 - - -

331

Total = 39,000 9,000

Apportionment of annual rent of £7,800 (£1,950 x 4) between finance charge and capital

repayment:

Period Total rental / £ Finance charge / £ Capital repayment

/ £

2019 7,800 3,110 4,690

2020 7,800 2,530 5,270

2021 7,800 1,880 5,920

2022 7,800 1,149 6,651

2023 7,800 331 7,469

Depreciation:

It should be calculated for 7 years, which is 5 years plus further 2 years.

£30,000 / 7 = £4,286 /annual depreciation/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

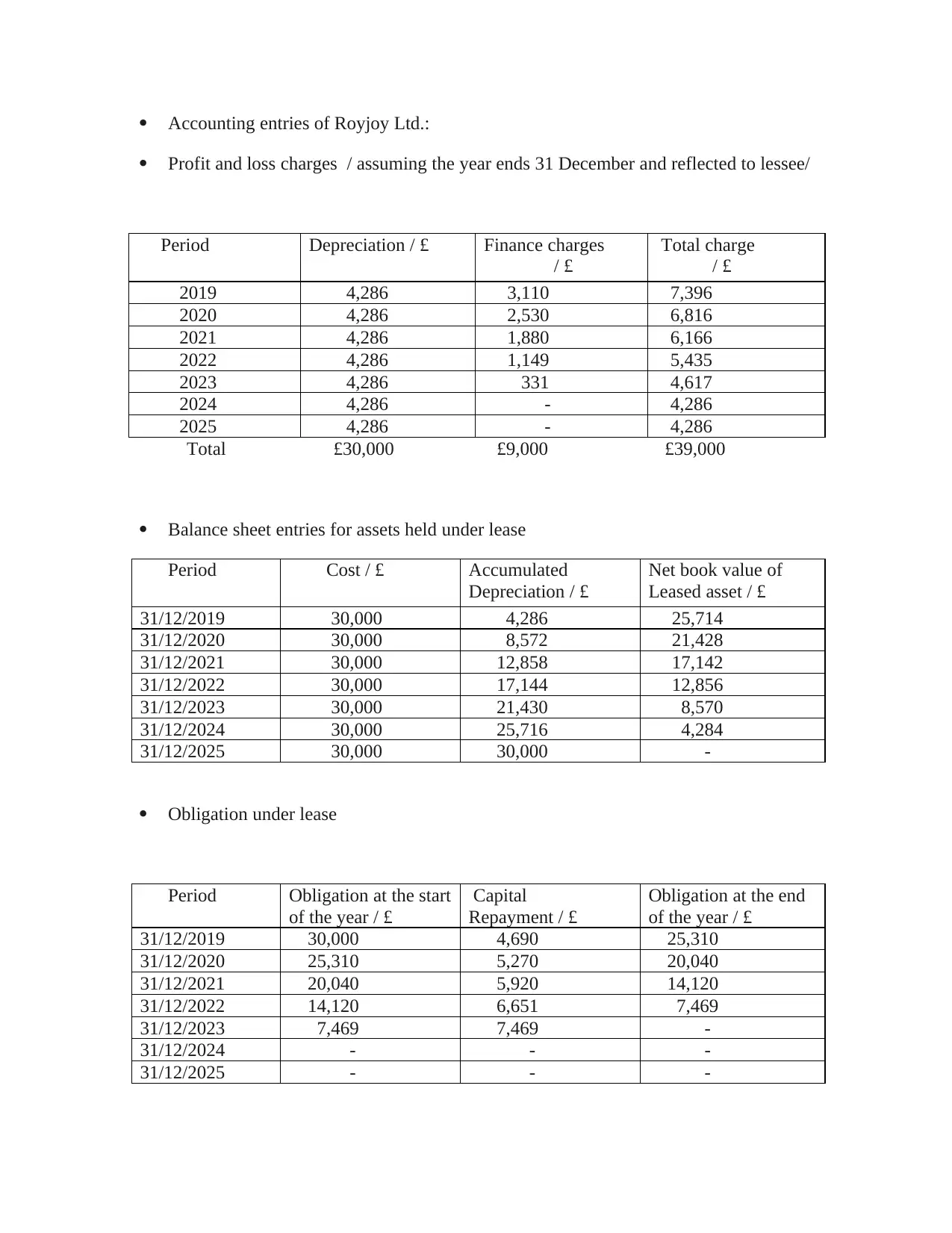

Accounting entries of Royjoy Ltd.:

Profit and loss charges / assuming the year ends 31 December and reflected to lessee/

Period Depreciation / £ Finance charges

/ £

Total charge

/ £

2019 4,286 3,110 7,396

2020 4,286 2,530 6,816

2021 4,286 1,880 6,166

2022 4,286 1,149 5,435

2023 4,286 331 4,617

2024 4,286 - 4,286

2025 4,286 - 4,286

Total £30,000 £9,000 £39,000

Balance sheet entries for assets held under lease

Period Cost / £ Accumulated

Depreciation / £

Net book value of

Leased asset / £

31/12/2019 30,000 4,286 25,714

31/12/2020 30,000 8,572 21,428

31/12/2021 30,000 12,858 17,142

31/12/2022 30,000 17,144 12,856

31/12/2023 30,000 21,430 8,570

31/12/2024 30,000 25,716 4,284

31/12/2025 30,000 30,000 -

Obligation under lease

Period Obligation at the start

of the year / £

Capital

Repayment / £

Obligation at the end

of the year / £

31/12/2019 30,000 4,690 25,310

31/12/2020 25,310 5,270 20,040

31/12/2021 20,040 5,920 14,120

31/12/2022 14,120 6,651 7,469

31/12/2023 7,469 7,469 -

31/12/2024 - - -

31/12/2025 - - -

Profit and loss charges / assuming the year ends 31 December and reflected to lessee/

Period Depreciation / £ Finance charges

/ £

Total charge

/ £

2019 4,286 3,110 7,396

2020 4,286 2,530 6,816

2021 4,286 1,880 6,166

2022 4,286 1,149 5,435

2023 4,286 331 4,617

2024 4,286 - 4,286

2025 4,286 - 4,286

Total £30,000 £9,000 £39,000

Balance sheet entries for assets held under lease

Period Cost / £ Accumulated

Depreciation / £

Net book value of

Leased asset / £

31/12/2019 30,000 4,286 25,714

31/12/2020 30,000 8,572 21,428

31/12/2021 30,000 12,858 17,142

31/12/2022 30,000 17,144 12,856

31/12/2023 30,000 21,430 8,570

31/12/2024 30,000 25,716 4,284

31/12/2025 30,000 30,000 -

Obligation under lease

Period Obligation at the start

of the year / £

Capital

Repayment / £

Obligation at the end

of the year / £

31/12/2019 30,000 4,690 25,310

31/12/2020 25,310 5,270 20,040

31/12/2021 20,040 5,920 14,120

31/12/2022 14,120 6,651 7,469

31/12/2023 7,469 7,469 -

31/12/2024 - - -

31/12/2025 - - -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part (2)

(a) Difference between the capital expenditure and revenue expenditure and impact on the

accounts of company if capital and revenue expenditures are being considered wrongly.

Herein, below the difference between the capital expenditure and revenue expenditure:

Basis of

difference

Capital expenditure Revenue expenditure

Mean The capital expenditure can be defined

as a kind of expenses which is being

done by the businesses for long time

period on valuable assets (Habib and

Jiang, 2015). For example expenses on

building.

On the other hand, it is a kind of

expenditure that is spend on those

goods and services which are used for

short time period. For example rent,

salaries, insurance, free samples etc.

Time

duration

Eventually, this kind of expenditure

consists the time duration of more then

one year. Like the buildings, machinery

are being used for more then one year.

While the revenue expenditure includes

the time duration of less one year.

Need This is needed for the purpose of

enhancing the working capacity and

growing the business. For example

expenses on furniture, buildings help to

the companies in growth.

These expenses are required for

running or operating the business

effectively. Like payment of wages to

employees is necessary to run day to

day operations or tasks.

Sub

categories

The capital expenditures do not include

any category.

While it consists two sub- categories

such as:

Direct expenses (rent, payment of

salary etc.)

Indirect expenses(insurance charges,

utilities etc.)

Financial

reports

These kind of expenses are being

recorded in the balance sheet.

This type of expenditure is recorded in

the Profit & Loss account as well as in

the Trading account.

(a) Difference between the capital expenditure and revenue expenditure and impact on the

accounts of company if capital and revenue expenditures are being considered wrongly.

Herein, below the difference between the capital expenditure and revenue expenditure:

Basis of

difference

Capital expenditure Revenue expenditure

Mean The capital expenditure can be defined

as a kind of expenses which is being

done by the businesses for long time

period on valuable assets (Habib and

Jiang, 2015). For example expenses on

building.

On the other hand, it is a kind of

expenditure that is spend on those

goods and services which are used for

short time period. For example rent,

salaries, insurance, free samples etc.

Time

duration

Eventually, this kind of expenditure

consists the time duration of more then

one year. Like the buildings, machinery

are being used for more then one year.

While the revenue expenditure includes

the time duration of less one year.

Need This is needed for the purpose of

enhancing the working capacity and

growing the business. For example

expenses on furniture, buildings help to

the companies in growth.

These expenses are required for

running or operating the business

effectively. Like payment of wages to

employees is necessary to run day to

day operations or tasks.

Sub

categories

The capital expenditures do not include

any category.

While it consists two sub- categories

such as:

Direct expenses (rent, payment of

salary etc.)

Indirect expenses(insurance charges,

utilities etc.)

Financial

reports

These kind of expenses are being

recorded in the balance sheet.

This type of expenditure is recorded in

the Profit & Loss account as well as in

the Trading account.

Nature The capital expenditures are non

recurring. This is so because these

expenditures do not occur again in

future. For example if a business

expends on the buildings and machinery

then it will not incur again till one year.

These kind of expenses are recurring in

the nature. This is why because these

expenditures occur again in regular

interval. For example a business

requires to pay the wages, salary to the

employees in each month as well as

rent is also being paid on monthly

basis.

Effect on company’s financial statements if any item of capital expenditure is taken as revenue

expenditures:

This is essential for the companies to considered the items of capital and revenue

expenditures separately without making an error (Jeanjean, Stolowy, Erkens and Yohn, 2015).

Otherwise it may impact to company’s accounts. Eventually, it can effect to the assets and

depreciation accounts. It can be understand by an example like journal entry of purchasing of a

capital assets, is debited in the assets account and credited in the cash account. By mistake if

revenue expenditure’s journal entry debits the expenses and credits the cash then capital assets

will be depreciated on the regular basis. So overall the consideration of an asset in a wrong

manner effect to the depreciation during a time period. Additionally, due to this total balance of

income statement is considered in the current year but the net income of the income statement

will be overstated. Eventually, in other words if item of capital expenditure is classified as

revenue expenditure wrongly then it will minimize the recorded profit of organization for year in

that expenditure is occurred. Along with it will reduce non current assets which is shown in

statement of financial position.

(b)

(i)

Tom Limited Factory

Machine's Initial Cost Break-

recurring. This is so because these

expenditures do not occur again in

future. For example if a business

expends on the buildings and machinery

then it will not incur again till one year.

These kind of expenses are recurring in

the nature. This is why because these

expenditures occur again in regular

interval. For example a business

requires to pay the wages, salary to the

employees in each month as well as

rent is also being paid on monthly

basis.

Effect on company’s financial statements if any item of capital expenditure is taken as revenue

expenditures:

This is essential for the companies to considered the items of capital and revenue

expenditures separately without making an error (Jeanjean, Stolowy, Erkens and Yohn, 2015).

Otherwise it may impact to company’s accounts. Eventually, it can effect to the assets and

depreciation accounts. It can be understand by an example like journal entry of purchasing of a

capital assets, is debited in the assets account and credited in the cash account. By mistake if

revenue expenditure’s journal entry debits the expenses and credits the cash then capital assets

will be depreciated on the regular basis. So overall the consideration of an asset in a wrong

manner effect to the depreciation during a time period. Additionally, due to this total balance of

income statement is considered in the current year but the net income of the income statement

will be overstated. Eventually, in other words if item of capital expenditure is classified as

revenue expenditure wrongly then it will minimize the recorded profit of organization for year in

that expenditure is occurred. Along with it will reduce non current assets which is shown in

statement of financial position.

(b)

(i)

Tom Limited Factory

Machine's Initial Cost Break-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.