An Analysis of Management Accounting in International Hospitality

VerifiedAdded on 2023/01/06

|14

|3149

|52

Report

AI Summary

This report provides a detailed overview of management accounting applications within the international hospitality industry. It begins by examining menu engineering and costing, explaining the process and its importance in increasing profitability. The report then delves into customer profitability analysis, exploring how businesses can shift their focus from product line profitability to individual customer profitability, including calculations and criticisms of the method. Furthermore, it addresses event and function management accounting, highlighting the differences between continuous operations like hotels and discrete events, and discusses management accounting tools for event planning. Finally, the report concludes by identifying critical success factors for the hospitality industry, such as customer service and effective advertising strategies. The report is a valuable resource for understanding how management accounting principles can be applied to improve decision-making and financial performance in the hospitality sector.

Running head: INTERNATIONAL HOSPITALITY

International Hospitality

5/5/2019

International Hospitality

5/5/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL HOSPITALITY 1

Table of Contents

Introduction................................................................................................................................2

1. Menu Engineering and Costing..........................................................................................2

Process of Menu-Engineering............................................................................................3

2. Costing and Customer Profitability....................................................................................5

Calculation of Customer Profitability................................................................................5

Application of the analysis of customer profitability.........................................................6

Criticism of Customer Profitability Analysis.....................................................................7

3. Event and Function Management Accounting...................................................................7

Event planning phase management accounting tools.........................................................8

4. Critical Success Factors of the Hospitality Industry..........................................................9

Conclusion................................................................................................................................10

References................................................................................................................................12

Table of Contents

Introduction................................................................................................................................2

1. Menu Engineering and Costing..........................................................................................2

Process of Menu-Engineering............................................................................................3

2. Costing and Customer Profitability....................................................................................5

Calculation of Customer Profitability................................................................................5

Application of the analysis of customer profitability.........................................................6

Criticism of Customer Profitability Analysis.....................................................................7

3. Event and Function Management Accounting...................................................................7

Event planning phase management accounting tools.........................................................8

4. Critical Success Factors of the Hospitality Industry..........................................................9

Conclusion................................................................................................................................10

References................................................................................................................................12

INTERNATIONAL HOSPITALITY 2

Introduction

Hospitality management is said to be the study of the industry of hospitality. It is the wide

fields incorporated in the industry of service which comprises drink, lodging, food services,

theme parks, cruise line, and event planning. The hospitality industry is continuously a

growing sector across the world (Kang, Lee and Huh, 2010). An effective system of

accounting is one of the key requirements for every business and hospitality industry. Every

successful business requires effective financial management for growth. Management

accounting is used by the managers in order to get better information before taking any

decision (Ward, 2012). The intent of this paper is to discuss the use of management

accounting in the hospitality industry with the help of key topics that is Menu Engineering

and costing, costing and customer profitability, event and function accounting, and critical

success factors.

1. Menu Engineering and Costing

Menu engineering is said to be the examination of the popularity and profitability of the

stuffs of the menu and how these features influence the place of the stuff, dish, or item on the

menu. The main objective is to increase per guest profitability. The menu engineering

concept is not a random concept; it is based on work done in the year 1970 by the BCG group

that is Boston Consulting Group in order to support organizations of groups in dividing their

dishes in a manner such that it can facilitate exploration and support in decision making. This

idea was offered to the industry of restaurant roughly by the Michigan State University

Professor “Coach” Donald Smith (Raab, Mayer and Shoemaker, 2010).

According to the analysis of the professor, the well-planned menu-engineering effort can

result in increasing the profits of the restaurant by 10 to 15% on a regular basis. This method

Introduction

Hospitality management is said to be the study of the industry of hospitality. It is the wide

fields incorporated in the industry of service which comprises drink, lodging, food services,

theme parks, cruise line, and event planning. The hospitality industry is continuously a

growing sector across the world (Kang, Lee and Huh, 2010). An effective system of

accounting is one of the key requirements for every business and hospitality industry. Every

successful business requires effective financial management for growth. Management

accounting is used by the managers in order to get better information before taking any

decision (Ward, 2012). The intent of this paper is to discuss the use of management

accounting in the hospitality industry with the help of key topics that is Menu Engineering

and costing, costing and customer profitability, event and function accounting, and critical

success factors.

1. Menu Engineering and Costing

Menu engineering is said to be the examination of the popularity and profitability of the

stuffs of the menu and how these features influence the place of the stuff, dish, or item on the

menu. The main objective is to increase per guest profitability. The menu engineering

concept is not a random concept; it is based on work done in the year 1970 by the BCG group

that is Boston Consulting Group in order to support organizations of groups in dividing their

dishes in a manner such that it can facilitate exploration and support in decision making. This

idea was offered to the industry of restaurant roughly by the Michigan State University

Professor “Coach” Donald Smith (Raab, Mayer and Shoemaker, 2010).

According to the analysis of the professor, the well-planned menu-engineering effort can

result in increasing the profits of the restaurant by 10 to 15% on a regular basis. This method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL HOSPITALITY 3

was first tried on a restaurant the profit of the restaurant increased by 10-15%, after some

time the management of the same restaurant called the professor to help in bringing more

profits on the same menu (Menu Cover Depot, 2019).

Process of Menu-Engineering

Menu Costing

Classifying the products of the menu as per the popularity and profit level

Designing of menu

Testing of the designed menu (Feldman, Mahadevan and Ruzsilla, 2011)

Costing of Menu

Costing of the menu is the procedure of breakdown of each menu item to its individual

ingredients and defining precisely the cost that is used to create each item. Establishments

categorically should cost their products on the menu as per the price of the food because the

procedure of engineering is based majorly in the level of profitability of each of the menu

item (Menu Cover Depot, 2019).

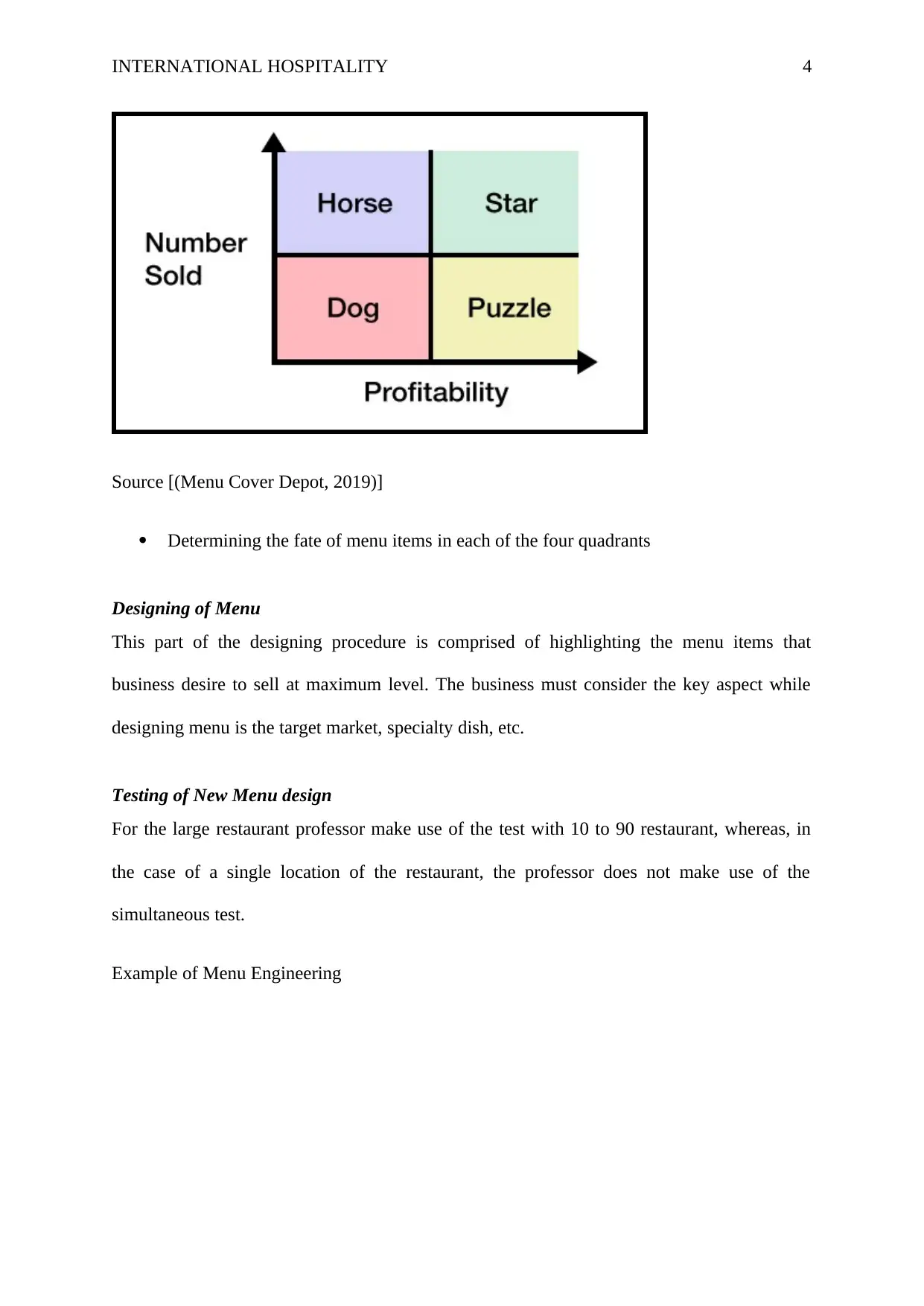

Classifying the products of the menu as per the popularity and profit level

This step is divided into three main steps i.e.

Splitting of the menu into different classes

Placing every item in one of the four quadrants

Dog – Low popularity and low profitability

Puzzle – Low popularity and high profitability

Plow-horses – High popularity and low profitability

Stars – High popularity and high profitability

was first tried on a restaurant the profit of the restaurant increased by 10-15%, after some

time the management of the same restaurant called the professor to help in bringing more

profits on the same menu (Menu Cover Depot, 2019).

Process of Menu-Engineering

Menu Costing

Classifying the products of the menu as per the popularity and profit level

Designing of menu

Testing of the designed menu (Feldman, Mahadevan and Ruzsilla, 2011)

Costing of Menu

Costing of the menu is the procedure of breakdown of each menu item to its individual

ingredients and defining precisely the cost that is used to create each item. Establishments

categorically should cost their products on the menu as per the price of the food because the

procedure of engineering is based majorly in the level of profitability of each of the menu

item (Menu Cover Depot, 2019).

Classifying the products of the menu as per the popularity and profit level

This step is divided into three main steps i.e.

Splitting of the menu into different classes

Placing every item in one of the four quadrants

Dog – Low popularity and low profitability

Puzzle – Low popularity and high profitability

Plow-horses – High popularity and low profitability

Stars – High popularity and high profitability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL HOSPITALITY 4

Source [(Menu Cover Depot, 2019)]

Determining the fate of menu items in each of the four quadrants

Designing of Menu

This part of the designing procedure is comprised of highlighting the menu items that

business desire to sell at maximum level. The business must consider the key aspect while

designing menu is the target market, specialty dish, etc.

Testing of New Menu design

For the large restaurant professor make use of the test with 10 to 90 restaurant, whereas, in

the case of a single location of the restaurant, the professor does not make use of the

simultaneous test.

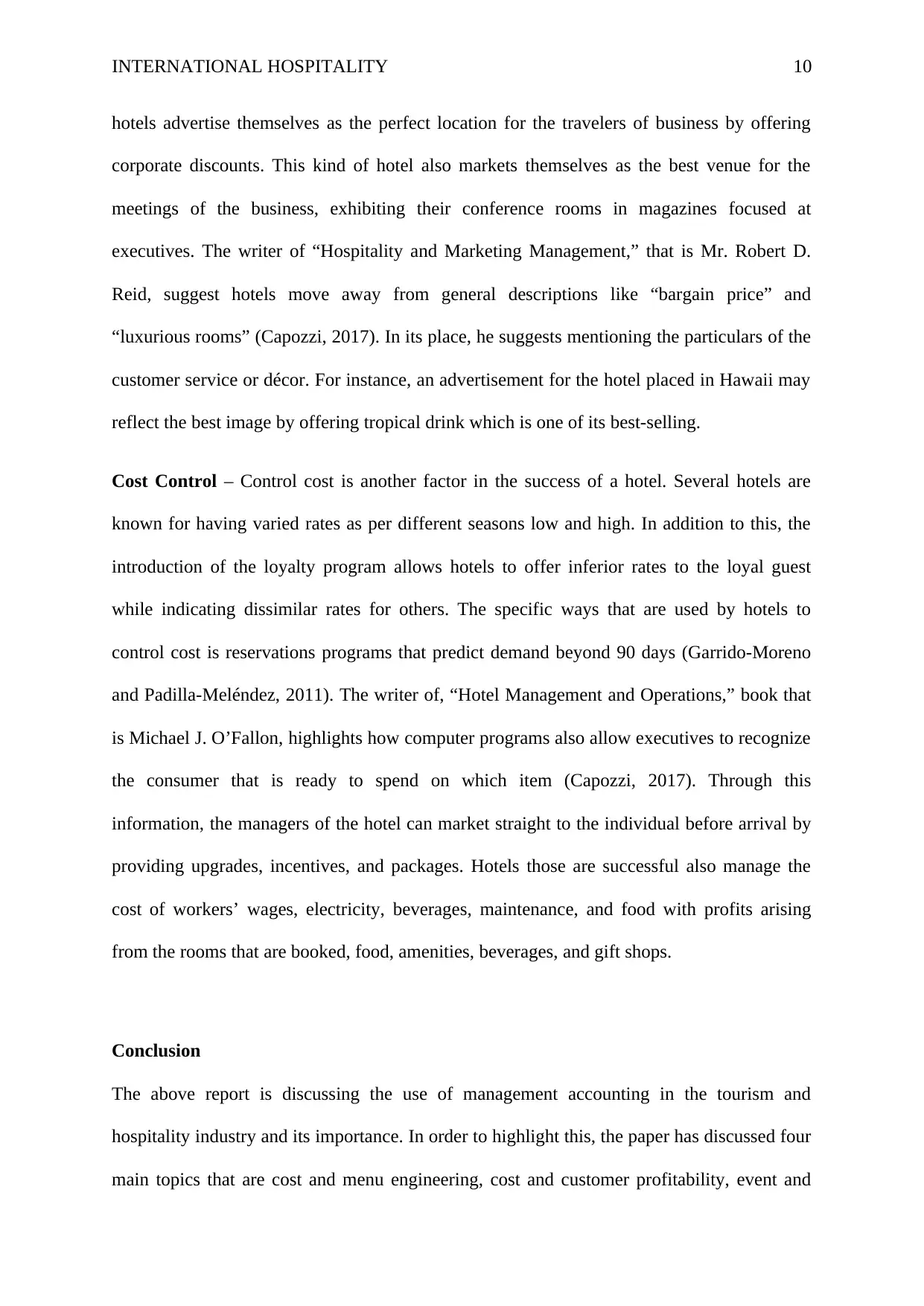

Example of Menu Engineering

Source [(Menu Cover Depot, 2019)]

Determining the fate of menu items in each of the four quadrants

Designing of Menu

This part of the designing procedure is comprised of highlighting the menu items that

business desire to sell at maximum level. The business must consider the key aspect while

designing menu is the target market, specialty dish, etc.

Testing of New Menu design

For the large restaurant professor make use of the test with 10 to 90 restaurant, whereas, in

the case of a single location of the restaurant, the professor does not make use of the

simultaneous test.

Example of Menu Engineering

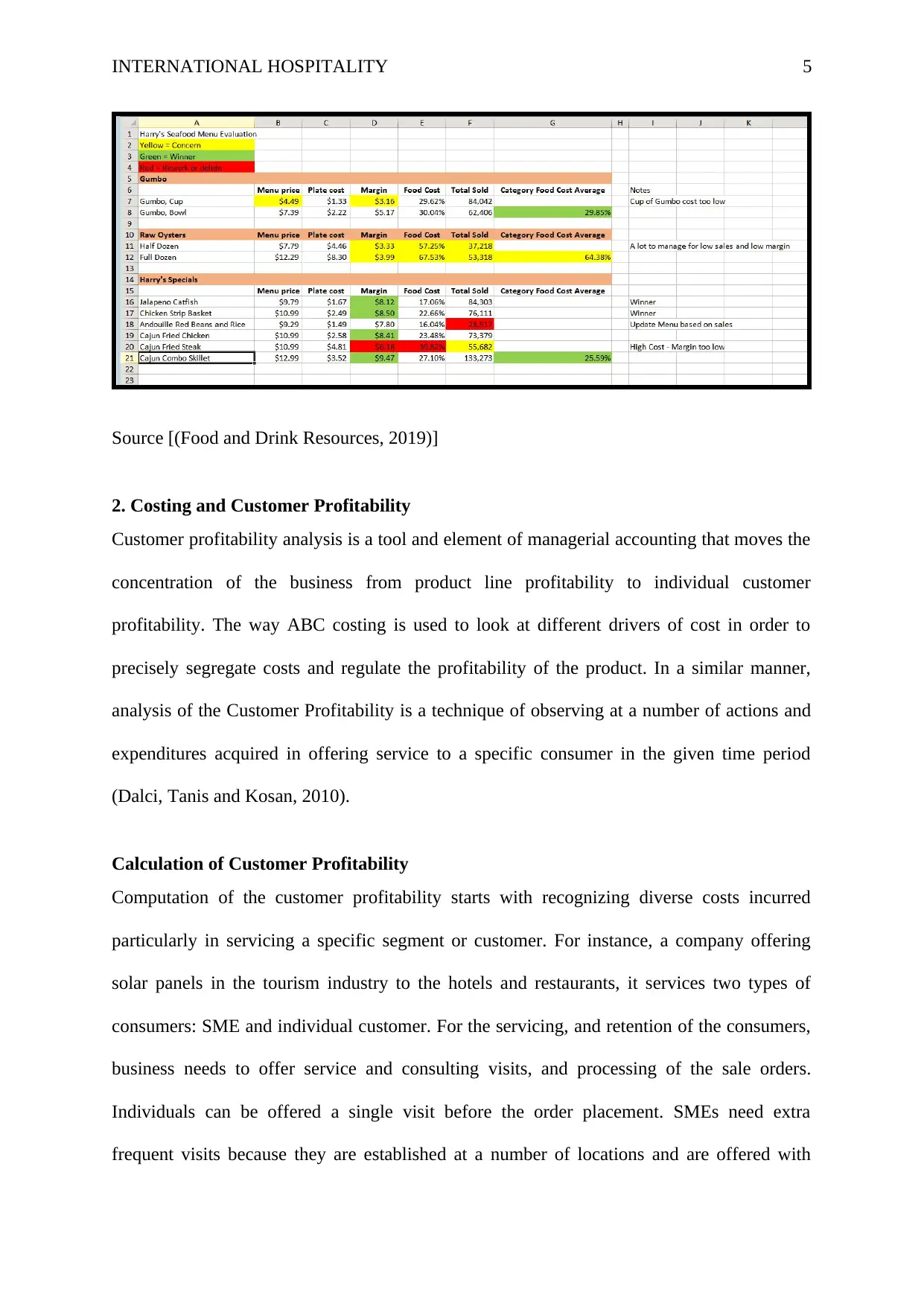

INTERNATIONAL HOSPITALITY 5

Source [(Food and Drink Resources, 2019)]

2. Costing and Customer Profitability

Customer profitability analysis is a tool and element of managerial accounting that moves the

concentration of the business from product line profitability to individual customer

profitability. The way ABC costing is used to look at different drivers of cost in order to

precisely segregate costs and regulate the profitability of the product. In a similar manner,

analysis of the Customer Profitability is a technique of observing at a number of actions and

expenditures acquired in offering service to a specific consumer in the given time period

(Dalci, Tanis and Kosan, 2010).

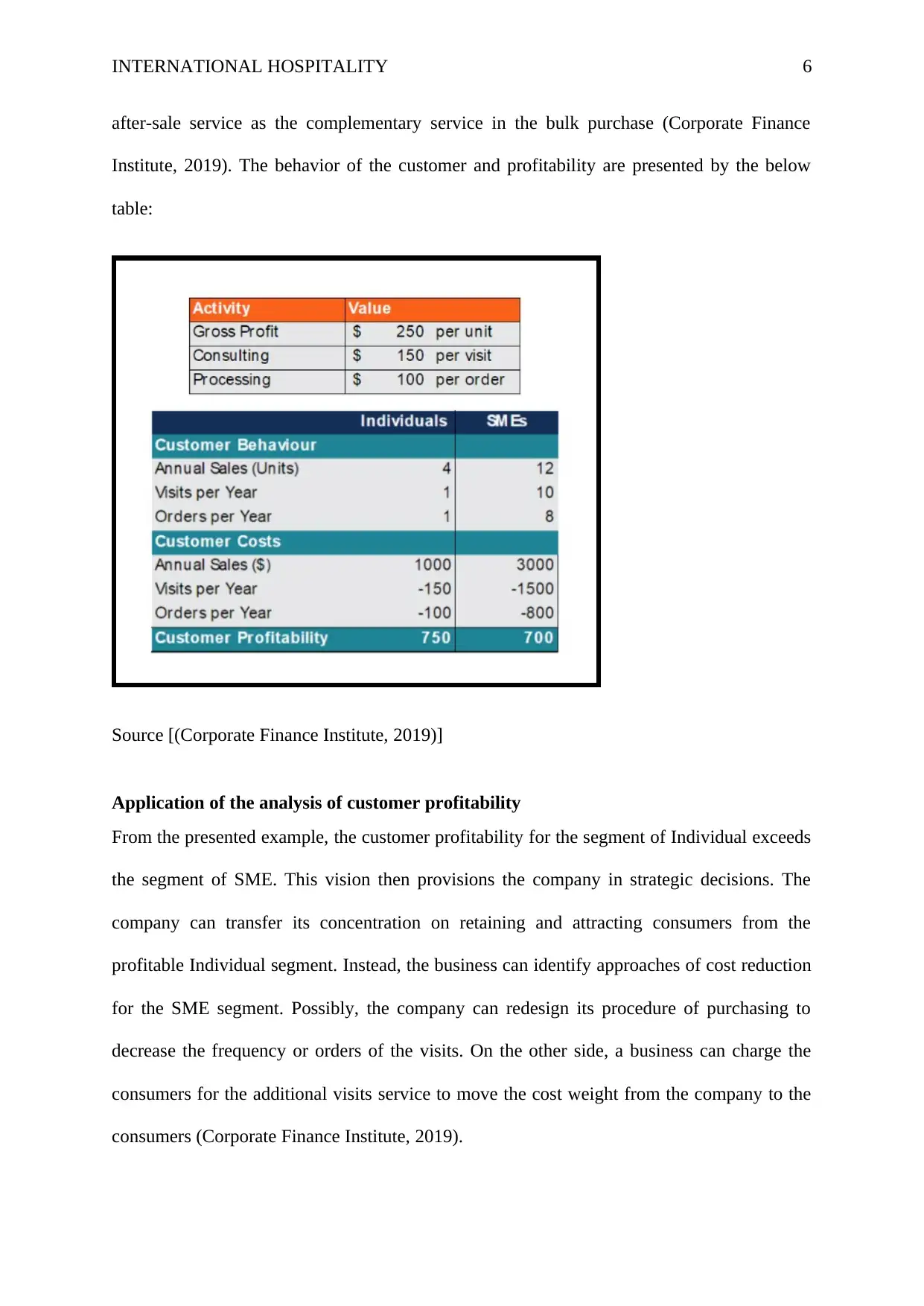

Calculation of Customer Profitability

Computation of the customer profitability starts with recognizing diverse costs incurred

particularly in servicing a specific segment or customer. For instance, a company offering

solar panels in the tourism industry to the hotels and restaurants, it services two types of

consumers: SME and individual customer. For the servicing, and retention of the consumers,

business needs to offer service and consulting visits, and processing of the sale orders.

Individuals can be offered a single visit before the order placement. SMEs need extra

frequent visits because they are established at a number of locations and are offered with

Source [(Food and Drink Resources, 2019)]

2. Costing and Customer Profitability

Customer profitability analysis is a tool and element of managerial accounting that moves the

concentration of the business from product line profitability to individual customer

profitability. The way ABC costing is used to look at different drivers of cost in order to

precisely segregate costs and regulate the profitability of the product. In a similar manner,

analysis of the Customer Profitability is a technique of observing at a number of actions and

expenditures acquired in offering service to a specific consumer in the given time period

(Dalci, Tanis and Kosan, 2010).

Calculation of Customer Profitability

Computation of the customer profitability starts with recognizing diverse costs incurred

particularly in servicing a specific segment or customer. For instance, a company offering

solar panels in the tourism industry to the hotels and restaurants, it services two types of

consumers: SME and individual customer. For the servicing, and retention of the consumers,

business needs to offer service and consulting visits, and processing of the sale orders.

Individuals can be offered a single visit before the order placement. SMEs need extra

frequent visits because they are established at a number of locations and are offered with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL HOSPITALITY 6

after-sale service as the complementary service in the bulk purchase (Corporate Finance

Institute, 2019). The behavior of the customer and profitability are presented by the below

table:

Source [(Corporate Finance Institute, 2019)]

Application of the analysis of customer profitability

From the presented example, the customer profitability for the segment of Individual exceeds

the segment of SME. This vision then provisions the company in strategic decisions. The

company can transfer its concentration on retaining and attracting consumers from the

profitable Individual segment. Instead, the business can identify approaches of cost reduction

for the SME segment. Possibly, the company can redesign its procedure of purchasing to

decrease the frequency or orders of the visits. On the other side, a business can charge the

consumers for the additional visits service to move the cost weight from the company to the

consumers (Corporate Finance Institute, 2019).

after-sale service as the complementary service in the bulk purchase (Corporate Finance

Institute, 2019). The behavior of the customer and profitability are presented by the below

table:

Source [(Corporate Finance Institute, 2019)]

Application of the analysis of customer profitability

From the presented example, the customer profitability for the segment of Individual exceeds

the segment of SME. This vision then provisions the company in strategic decisions. The

company can transfer its concentration on retaining and attracting consumers from the

profitable Individual segment. Instead, the business can identify approaches of cost reduction

for the SME segment. Possibly, the company can redesign its procedure of purchasing to

decrease the frequency or orders of the visits. On the other side, a business can charge the

consumers for the additional visits service to move the cost weight from the company to the

consumers (Corporate Finance Institute, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL HOSPITALITY 7

Criticism of Customer Profitability Analysis

The major criticism received by the customer profitability analysis is the adoption of

segmentation criteria and limited timeframe. With the development of the Big Data, customer

profitability could be computed with new approaches that can define the lifetime value for the

customer in place of just the sales in the restricted timeframe (Hajiha and Alishah, 2011). In

other words, the concept of customer profitability is restrictive in the manner it works on the

customer value segment in a prescribed time period in place of their value during their entire

lifetime involvement with the business (Corporate Finance Institute, 2019). In addition to

this, in terms of segmentation, predictive analytics can be used to predict the individual

customer value by recognizing the drivers in behavioral outlines in place of average customer

value in its particular segment.

3. Event and Function Management Accounting

Whether it is about managing a wedding in the hotel, music festival, charity fun run, annual

conference, international sporting event, vintage steam fair, an air show, corporate event,

literature festival, concert or product launch, every event has same thing common that is they

are not continuous (Jones, Atkinson, Lorenz and Harris, 2012). An ‘event’ is the occurrence,

or activity or a series event every event is usually discrete. If it is compared with the hotel

which is being run 24/7, and 365 days they are different at large level. It has insinuations for

management accounting, which is one of the best methods to be used and the ‘unit’ of

analysis (Good Fellow Publisher, 2010).

In the hotel, the arrival and departure of the customer never stop. There is not a single time

when there is not a single customer in the hotel, some with be departing and some will be

arriving and some will be available in the middle of the stay. On the other side, in the event, it

is the possibility that individuals might not every time reach on time, by nature, an event has

a starting time, has a middle point, and the prearranged endpoint. For instance, for the local

Criticism of Customer Profitability Analysis

The major criticism received by the customer profitability analysis is the adoption of

segmentation criteria and limited timeframe. With the development of the Big Data, customer

profitability could be computed with new approaches that can define the lifetime value for the

customer in place of just the sales in the restricted timeframe (Hajiha and Alishah, 2011). In

other words, the concept of customer profitability is restrictive in the manner it works on the

customer value segment in a prescribed time period in place of their value during their entire

lifetime involvement with the business (Corporate Finance Institute, 2019). In addition to

this, in terms of segmentation, predictive analytics can be used to predict the individual

customer value by recognizing the drivers in behavioral outlines in place of average customer

value in its particular segment.

3. Event and Function Management Accounting

Whether it is about managing a wedding in the hotel, music festival, charity fun run, annual

conference, international sporting event, vintage steam fair, an air show, corporate event,

literature festival, concert or product launch, every event has same thing common that is they

are not continuous (Jones, Atkinson, Lorenz and Harris, 2012). An ‘event’ is the occurrence,

or activity or a series event every event is usually discrete. If it is compared with the hotel

which is being run 24/7, and 365 days they are different at large level. It has insinuations for

management accounting, which is one of the best methods to be used and the ‘unit’ of

analysis (Good Fellow Publisher, 2010).

In the hotel, the arrival and departure of the customer never stop. There is not a single time

when there is not a single customer in the hotel, some with be departing and some will be

arriving and some will be available in the middle of the stay. On the other side, in the event, it

is the possibility that individuals might not every time reach on time, by nature, an event has

a starting time, has a middle point, and the prearranged endpoint. For instance, for the local

INTERNATIONAL HOSPITALITY 8

drink and food festival, the holders or managers of the event may set Thursday as its opening

day and set the timing for the public and Sunday can be set as the end day of the same event.

The insinuations of this offer specific aids, but comprise high financial risks if the evidence

gathered through management accounting is not utilized properly by the directors of the

event.

This risk is linked with the comparative number of ‘events’ organized. If the company of

event planning only work on 2-3 international or national event yearly, then the financial

failure of a single event can result in a third of the year's trading opportunity. On the other

side, in a hotel, if one day has resulted in financial problem the hotel yet has another 364 days

for the trading in a year to depend on. With the outside events in summer, external

uncontainable forces like weather can result in a major influence on the event. It is hence

important that the managers of the event consider every potential situation and are capable

enough to financially model the worst situations and anticipated scenarios.

The opportunity of management accounting is accessible to an event is connected to its

inconspicuous nature. Financial planning and control are based on the level of the event.

Under unceasing operation, like a hotel, control and planning are best at the individual

customer level, or over a period of the time period (Bar and Lillard, 2012). Management

accounting at the event level is corresponding to utilizing ‘job costing’ in manufacturing. A

distinct financial plan could be arranged for the event and can be controlled at the level all

over the operation, planning, and evaluation procedure.

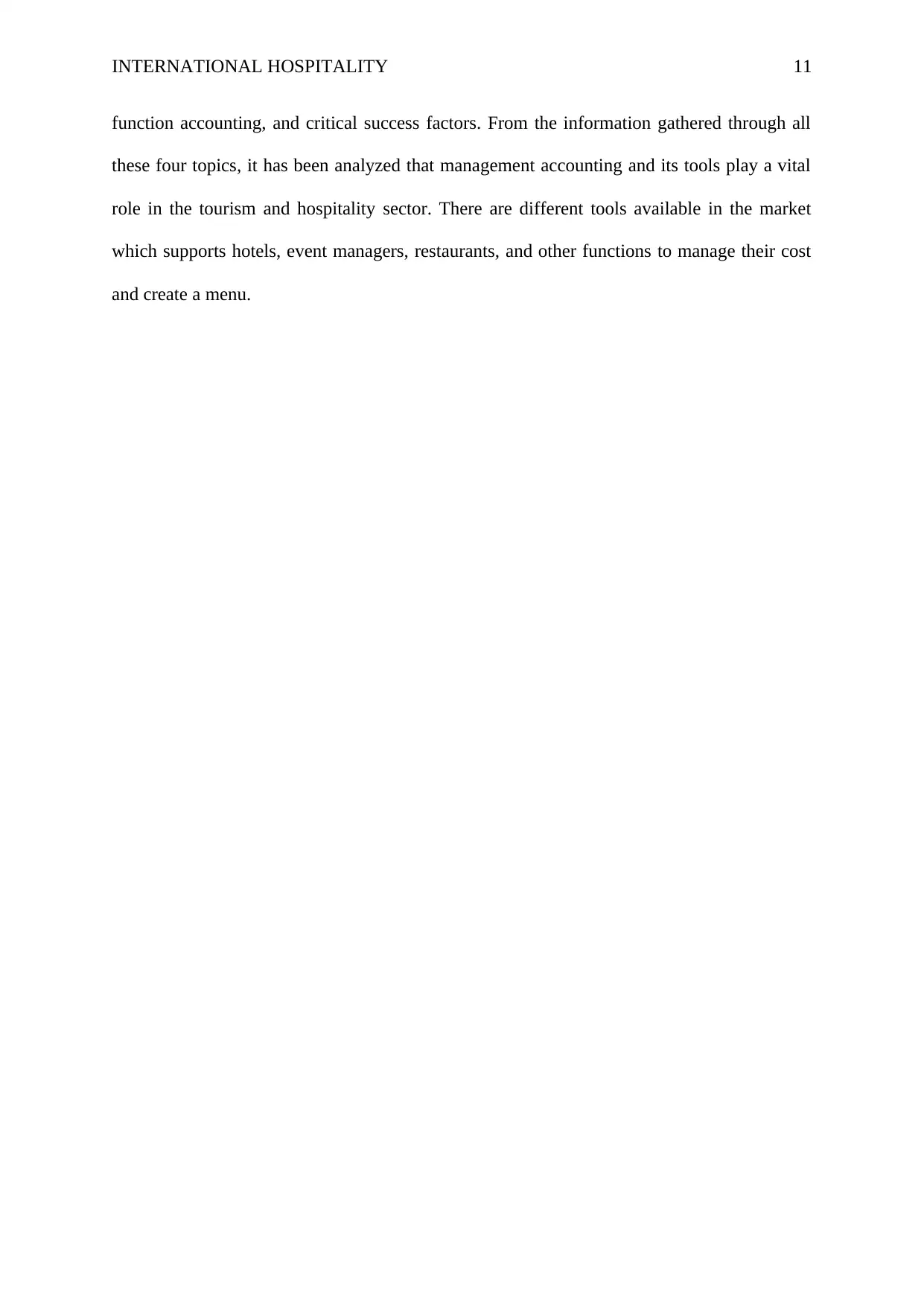

Event planning phase management accounting tools

There is a number of the practical and strategic task of event planning that could be assisted

through management accounting. The below image highlights a few of the financial

drink and food festival, the holders or managers of the event may set Thursday as its opening

day and set the timing for the public and Sunday can be set as the end day of the same event.

The insinuations of this offer specific aids, but comprise high financial risks if the evidence

gathered through management accounting is not utilized properly by the directors of the

event.

This risk is linked with the comparative number of ‘events’ organized. If the company of

event planning only work on 2-3 international or national event yearly, then the financial

failure of a single event can result in a third of the year's trading opportunity. On the other

side, in a hotel, if one day has resulted in financial problem the hotel yet has another 364 days

for the trading in a year to depend on. With the outside events in summer, external

uncontainable forces like weather can result in a major influence on the event. It is hence

important that the managers of the event consider every potential situation and are capable

enough to financially model the worst situations and anticipated scenarios.

The opportunity of management accounting is accessible to an event is connected to its

inconspicuous nature. Financial planning and control are based on the level of the event.

Under unceasing operation, like a hotel, control and planning are best at the individual

customer level, or over a period of the time period (Bar and Lillard, 2012). Management

accounting at the event level is corresponding to utilizing ‘job costing’ in manufacturing. A

distinct financial plan could be arranged for the event and can be controlled at the level all

over the operation, planning, and evaluation procedure.

Event planning phase management accounting tools

There is a number of the practical and strategic task of event planning that could be assisted

through management accounting. The below image highlights a few of the financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL HOSPITALITY 9

considerations in terms of how the tools of management accounting could support managers

of a different event.

Source [(Good Fellow Publisher, 2010)]

4. Critical Success Factors of the Hospitality Industry

Customer Service - It is said to be the key portion of the experience of the hotel. Clayton

Barrows, the writer of “Introduction to Management in the Hospitality Industry,” clarifies the

concept of how the worker at the front-desk aids as the doorkeeper of the hotel. These

workers are the one who leave the initial and last impression to the customers. Thus, hotels

attain a critical success factor by confirming the staffs is well-informed, polite and

accomplished of solving any type of struggles that rise in the hotel. Offering quality of

service is also involves recalling the names and preferences of recurrence guests and offering

instruction regarding the surrounding environment and attractions (Capozzi, 2017).

Advertisement - Successful hotels or hotel groups have a specific target market and frame

their advertisement strategies, pricing, and amenities according to the demand for that

specific customer group (Chittithaworn, Islam and Yusuf, 2011). For instance, few of the

considerations in terms of how the tools of management accounting could support managers

of a different event.

Source [(Good Fellow Publisher, 2010)]

4. Critical Success Factors of the Hospitality Industry

Customer Service - It is said to be the key portion of the experience of the hotel. Clayton

Barrows, the writer of “Introduction to Management in the Hospitality Industry,” clarifies the

concept of how the worker at the front-desk aids as the doorkeeper of the hotel. These

workers are the one who leave the initial and last impression to the customers. Thus, hotels

attain a critical success factor by confirming the staffs is well-informed, polite and

accomplished of solving any type of struggles that rise in the hotel. Offering quality of

service is also involves recalling the names and preferences of recurrence guests and offering

instruction regarding the surrounding environment and attractions (Capozzi, 2017).

Advertisement - Successful hotels or hotel groups have a specific target market and frame

their advertisement strategies, pricing, and amenities according to the demand for that

specific customer group (Chittithaworn, Islam and Yusuf, 2011). For instance, few of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL HOSPITALITY 10

hotels advertise themselves as the perfect location for the travelers of business by offering

corporate discounts. This kind of hotel also markets themselves as the best venue for the

meetings of the business, exhibiting their conference rooms in magazines focused at

executives. The writer of “Hospitality and Marketing Management,” that is Mr. Robert D.

Reid, suggest hotels move away from general descriptions like “bargain price” and

“luxurious rooms” (Capozzi, 2017). In its place, he suggests mentioning the particulars of the

customer service or décor. For instance, an advertisement for the hotel placed in Hawaii may

reflect the best image by offering tropical drink which is one of its best-selling.

Cost Control – Control cost is another factor in the success of a hotel. Several hotels are

known for having varied rates as per different seasons low and high. In addition to this, the

introduction of the loyalty program allows hotels to offer inferior rates to the loyal guest

while indicating dissimilar rates for others. The specific ways that are used by hotels to

control cost is reservations programs that predict demand beyond 90 days (Garrido-Moreno

and Padilla-Meléndez, 2011). The writer of, “Hotel Management and Operations,” book that

is Michael J. O’Fallon, highlights how computer programs also allow executives to recognize

the consumer that is ready to spend on which item (Capozzi, 2017). Through this

information, the managers of the hotel can market straight to the individual before arrival by

providing upgrades, incentives, and packages. Hotels those are successful also manage the

cost of workers’ wages, electricity, beverages, maintenance, and food with profits arising

from the rooms that are booked, food, amenities, beverages, and gift shops.

Conclusion

The above report is discussing the use of management accounting in the tourism and

hospitality industry and its importance. In order to highlight this, the paper has discussed four

main topics that are cost and menu engineering, cost and customer profitability, event and

hotels advertise themselves as the perfect location for the travelers of business by offering

corporate discounts. This kind of hotel also markets themselves as the best venue for the

meetings of the business, exhibiting their conference rooms in magazines focused at

executives. The writer of “Hospitality and Marketing Management,” that is Mr. Robert D.

Reid, suggest hotels move away from general descriptions like “bargain price” and

“luxurious rooms” (Capozzi, 2017). In its place, he suggests mentioning the particulars of the

customer service or décor. For instance, an advertisement for the hotel placed in Hawaii may

reflect the best image by offering tropical drink which is one of its best-selling.

Cost Control – Control cost is another factor in the success of a hotel. Several hotels are

known for having varied rates as per different seasons low and high. In addition to this, the

introduction of the loyalty program allows hotels to offer inferior rates to the loyal guest

while indicating dissimilar rates for others. The specific ways that are used by hotels to

control cost is reservations programs that predict demand beyond 90 days (Garrido-Moreno

and Padilla-Meléndez, 2011). The writer of, “Hotel Management and Operations,” book that

is Michael J. O’Fallon, highlights how computer programs also allow executives to recognize

the consumer that is ready to spend on which item (Capozzi, 2017). Through this

information, the managers of the hotel can market straight to the individual before arrival by

providing upgrades, incentives, and packages. Hotels those are successful also manage the

cost of workers’ wages, electricity, beverages, maintenance, and food with profits arising

from the rooms that are booked, food, amenities, beverages, and gift shops.

Conclusion

The above report is discussing the use of management accounting in the tourism and

hospitality industry and its importance. In order to highlight this, the paper has discussed four

main topics that are cost and menu engineering, cost and customer profitability, event and

INTERNATIONAL HOSPITALITY 11

function accounting, and critical success factors. From the information gathered through all

these four topics, it has been analyzed that management accounting and its tools play a vital

role in the tourism and hospitality sector. There are different tools available in the market

which supports hotels, event managers, restaurants, and other functions to manage their cost

and create a menu.

function accounting, and critical success factors. From the information gathered through all

these four topics, it has been analyzed that management accounting and its tools play a vital

role in the tourism and hospitality sector. There are different tools available in the market

which supports hotels, event managers, restaurants, and other functions to manage their cost

and create a menu.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.