University of Wales: IFM Assignment - Investment Appraisal Techniques

VerifiedAdded on 2023/01/09

|9

|1808

|71

Report

AI Summary

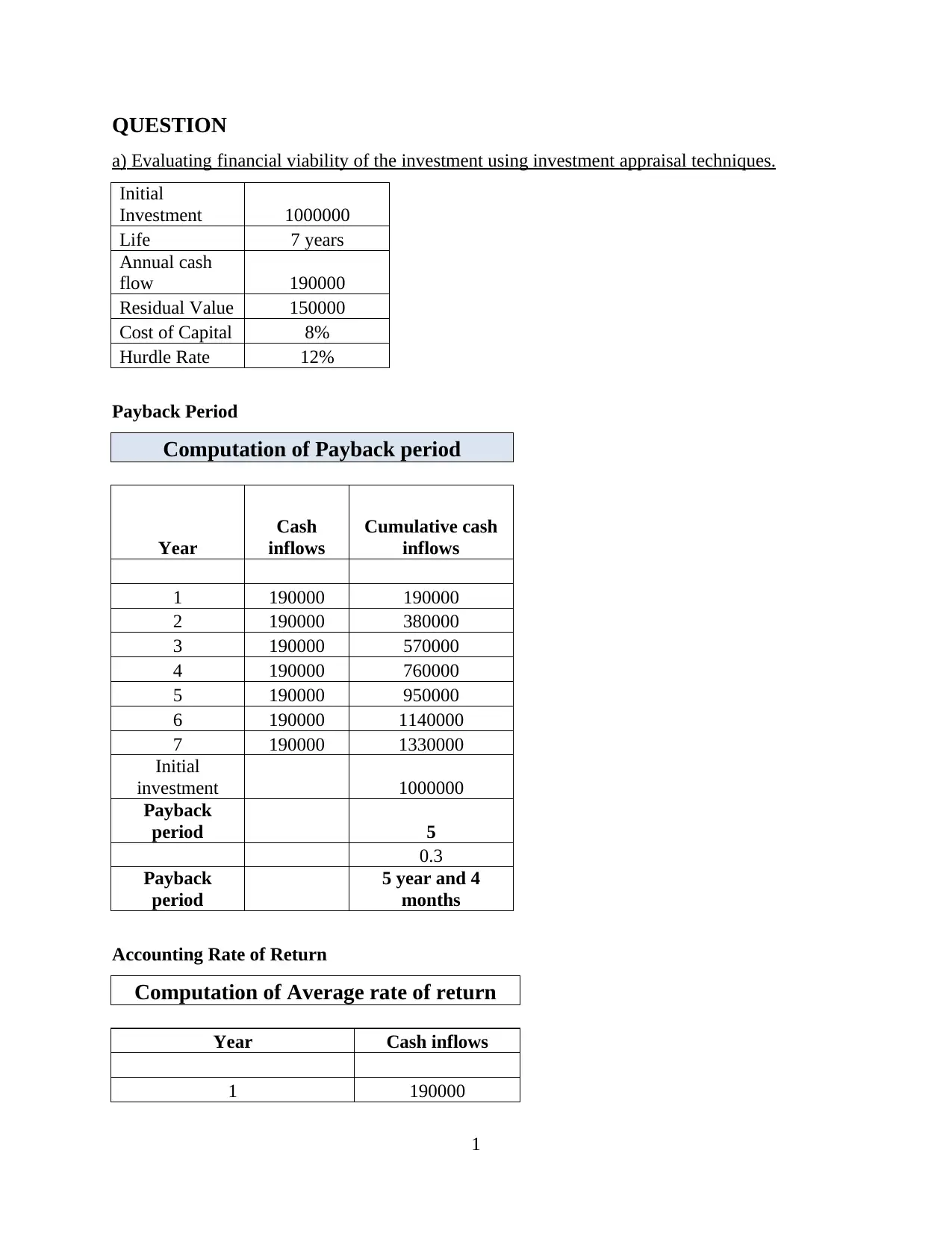

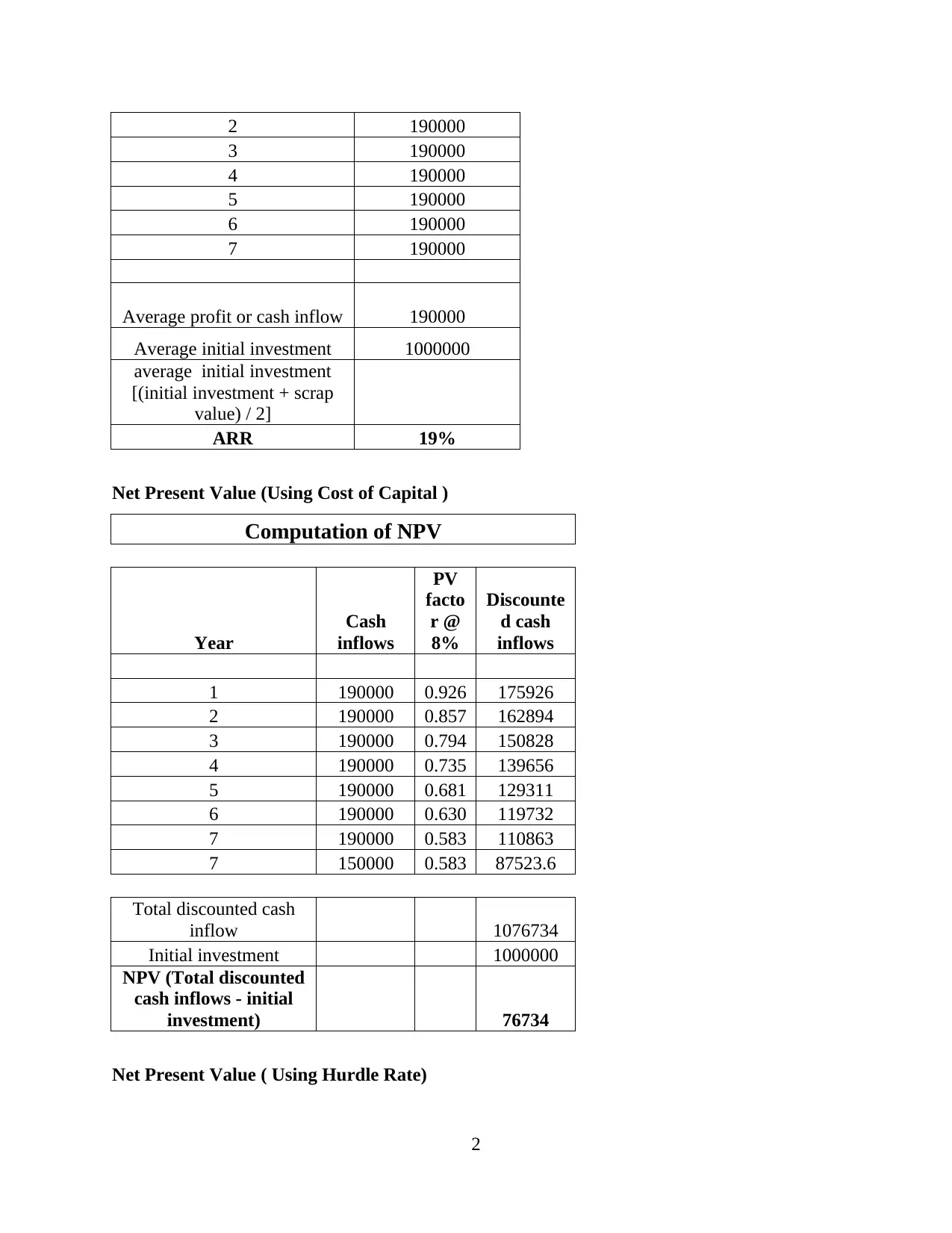

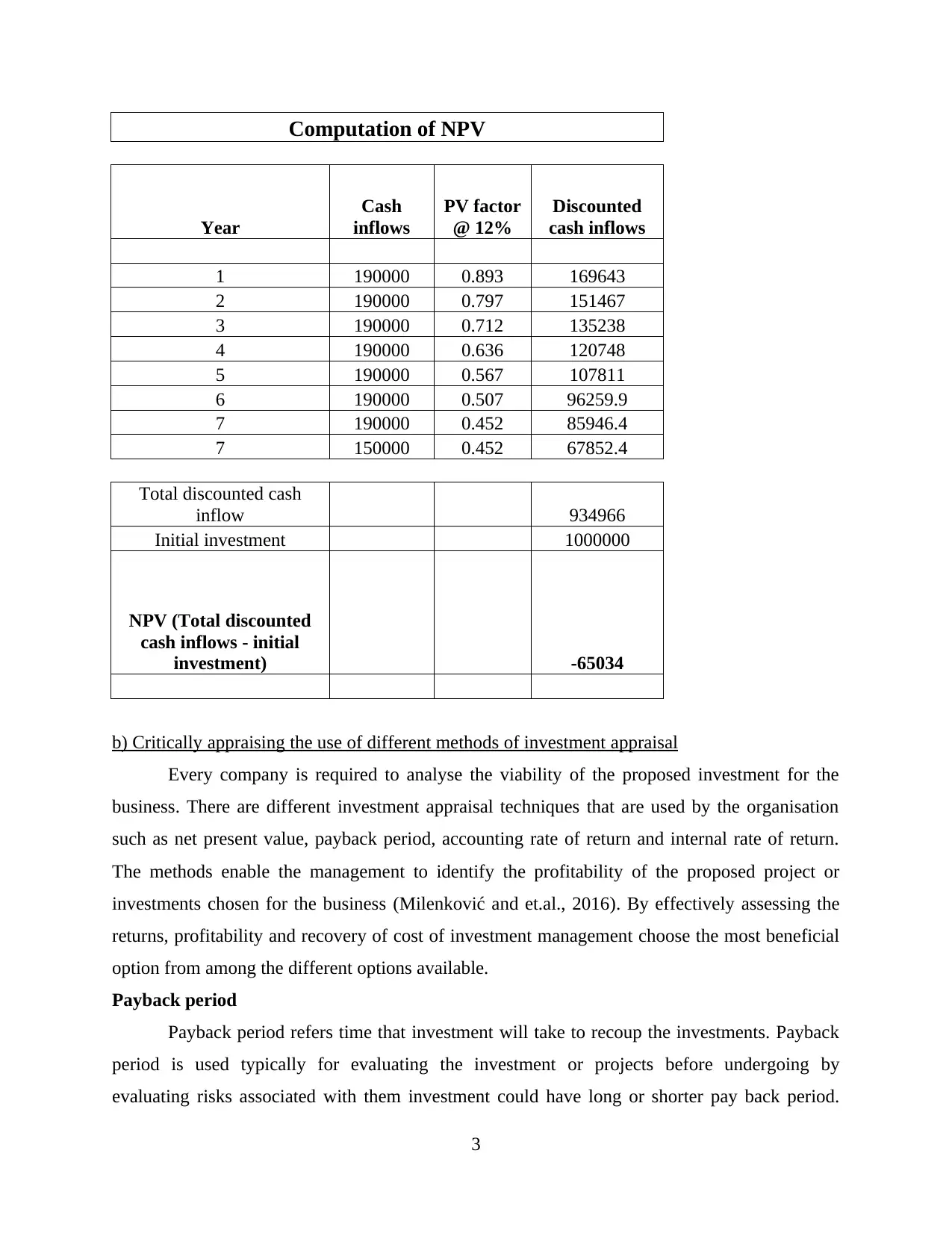

This report, prepared for an International Financial Management course, evaluates the financial viability of an investment using various investment appraisal techniques, including Payback Period, Accounting Rate of Return (ARR), and Net Present Value (NPV), considering both Cost of Capital and Hurdle Rate scenarios. The report then critically appraises the use of these different methods, discussing their strengths and weaknesses in assessing the profitability and risk associated with the investment. Furthermore, it delves into the non-financial factors, such as legal compliance, project capacity, industry standards, maintenance requirements, human and social factors, and the importance of training, that must be considered alongside financial metrics to make informed investment decisions. The analysis provides a comprehensive overview of the investment appraisal process, combining quantitative financial analysis with qualitative considerations for a holistic evaluation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.