International Accounting Report: Nestle's Financial Statements

VerifiedAdded on 2020/02/05

|11

|2634

|175

Report

AI Summary

This report provides a comprehensive analysis of international accounting principles, focusing on the application of International Financial Reporting Standards (IFRS) to Nestle's financial statements. It begins with an explanation of the need for international financial reporting, emphasizing the importance of stock exchanges, market regulations, and user needs. The report then defines the roles and importance of the International Accounting Standards Board (IASB) and the Malaysian Accounting Standards Board (MASB), including how they set and enforce accounting standards globally. Furthermore, the report evaluates Nestle's adherence to IASB standards, defining key concepts such as the going concern principle and the accruals basis of accounting. It also examines the items affecting the going concern concept and transactions influenced by the accrual basis. The analysis includes a discussion of the qualitative characteristics of financial information and concludes with an overview of the limitations of published financial statements.

INTERNATIONAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................................3

1. EXPLAIN THE NEED OF INTERNATIONAL FINANCIAL REPORTING.........................3

CRITERION 1- Stock Exchange importance............................................................................3

CRITERION 2- Need for regulation of stock markets.............................................................3

CRITERION 3- What are User Needs Framework....................................................................3

CRITERION 4 Regulation of accounting methods..................................................................4

CRITERION 5- Define the use of published financial statements ...........................................4

CRITERION 6- Limitations of published financial statements ................................................4

2. DEFINE IASB WITH ITS ROLES AND IMPORTANCE.......................................................5

CRITERION 7- Define roles of IASB.......................................................................................5

CRITERION 8- ways IASB sets accounting standards globally..............................................5

CRITERION 9- How IASB enforces accounting standards globally........................................6

3. DISCUSSION OF THE ROLE AND PURPOSE OF MASB....................................................6

CRITERION 10- Define roles of MASB...................................................................................6

CRITERION 11- The Setting of Malaysian accounting standards............................................6

CRITERION 12- How the MASB enforces accounting standards globally.............................6

4. EVALUATION OF THE ADHEREANCE TO IASB OF THE COMPANY'S FINANCIAL

STATEMENTS...............................................................................................................................7

CRITERION 13- Define going concern concept.......................................................................7

CRITERION 14- Items affecting the going concern concept form the company's financial

statements...................................................................................................................................7

CRITERION 15- Explain accruals basis of accounting ............................................................9

CRITERION 16- List of transactions which are affected by accrual basis. ............................9

CRITERION 17- Define the Qualitative characteristics of Financial information...................9

CRITERION 18- The financial information which are affected by qualitative characteristics.

....................................................................................................................................................9

CONCLUSION...............................................................................................................................9

REFERENCES.............................................................................................................................11

INTRODUCTION..........................................................................................................................3

1. EXPLAIN THE NEED OF INTERNATIONAL FINANCIAL REPORTING.........................3

CRITERION 1- Stock Exchange importance............................................................................3

CRITERION 2- Need for regulation of stock markets.............................................................3

CRITERION 3- What are User Needs Framework....................................................................3

CRITERION 4 Regulation of accounting methods..................................................................4

CRITERION 5- Define the use of published financial statements ...........................................4

CRITERION 6- Limitations of published financial statements ................................................4

2. DEFINE IASB WITH ITS ROLES AND IMPORTANCE.......................................................5

CRITERION 7- Define roles of IASB.......................................................................................5

CRITERION 8- ways IASB sets accounting standards globally..............................................5

CRITERION 9- How IASB enforces accounting standards globally........................................6

3. DISCUSSION OF THE ROLE AND PURPOSE OF MASB....................................................6

CRITERION 10- Define roles of MASB...................................................................................6

CRITERION 11- The Setting of Malaysian accounting standards............................................6

CRITERION 12- How the MASB enforces accounting standards globally.............................6

4. EVALUATION OF THE ADHEREANCE TO IASB OF THE COMPANY'S FINANCIAL

STATEMENTS...............................................................................................................................7

CRITERION 13- Define going concern concept.......................................................................7

CRITERION 14- Items affecting the going concern concept form the company's financial

statements...................................................................................................................................7

CRITERION 15- Explain accruals basis of accounting ............................................................9

CRITERION 16- List of transactions which are affected by accrual basis. ............................9

CRITERION 17- Define the Qualitative characteristics of Financial information...................9

CRITERION 18- The financial information which are affected by qualitative characteristics.

....................................................................................................................................................9

CONCLUSION...............................................................................................................................9

REFERENCES.............................................................................................................................11

INTRODUCTION

International Accounting means the accounting done on the basis of specific accounting

standards which are framed and the same as to be followed Nestle is a growing going concern

company whose financial performance was reduced in the year 2015 due the noodles issue.

1. EXPLAIN THE NEED OF INTERNATIONAL FINANCIAL REPORTING

CRITERION 1- Stock Exchange importance.

Stock Exchange is a platform where securities are bought and sold. For Nestle, Stock

Exchange plays a huge role when it comes to raising capital from the public for the business. It

helps in facilitating company's growth (Marriott, 2014). For any company to be listed stock

exchange impose some stringent rules hence Nestle being a public company have better

management records. The main purpose of stock exchange are that it is a tool form ensuring the

economic growth for the entire country as any change is reflected in the price. As the company,

Nestle is a growing company the prices are based on the demand and supply function and thus

the price of the company is high.

CRITERION 2- Need for regulation of stock markets.

For the smooth functioning, the regulation of stock market has to be done. As every

company listed in the stock exchange has to follow the stringent rules by the stock exchange to

get itself listed. The regulation of stock markets is governed by the government body Securities

and Exchange Commission (SEC) and the regulation helps in ensuring the Fairness and

Transparency. The fairness ensures that all the dealings done in stock exchange is done in fairly

manner without any bias. The transparency is required to be sure about that the investors have

the access to the financial information of the company. The transparency of Nestle also helps in

increasing the stock's performance.

CRITERION 3- What are User Needs Framework.

The IFRS stands for the International Financial Reporting Standards stands for the fact

that is describes the basic concepts and draws the standards about the preparation of the

financial statements. These statements serves as a important tool to gauge the performance of

the company for the external users. As the users need information for making the purchase

decision in the company and not only the buyers but the information is reviewed by the lenders,

government. The users need information for various purposes other than buying and also to

International Accounting means the accounting done on the basis of specific accounting

standards which are framed and the same as to be followed Nestle is a growing going concern

company whose financial performance was reduced in the year 2015 due the noodles issue.

1. EXPLAIN THE NEED OF INTERNATIONAL FINANCIAL REPORTING

CRITERION 1- Stock Exchange importance.

Stock Exchange is a platform where securities are bought and sold. For Nestle, Stock

Exchange plays a huge role when it comes to raising capital from the public for the business. It

helps in facilitating company's growth (Marriott, 2014). For any company to be listed stock

exchange impose some stringent rules hence Nestle being a public company have better

management records. The main purpose of stock exchange are that it is a tool form ensuring the

economic growth for the entire country as any change is reflected in the price. As the company,

Nestle is a growing company the prices are based on the demand and supply function and thus

the price of the company is high.

CRITERION 2- Need for regulation of stock markets.

For the smooth functioning, the regulation of stock market has to be done. As every

company listed in the stock exchange has to follow the stringent rules by the stock exchange to

get itself listed. The regulation of stock markets is governed by the government body Securities

and Exchange Commission (SEC) and the regulation helps in ensuring the Fairness and

Transparency. The fairness ensures that all the dealings done in stock exchange is done in fairly

manner without any bias. The transparency is required to be sure about that the investors have

the access to the financial information of the company. The transparency of Nestle also helps in

increasing the stock's performance.

CRITERION 3- What are User Needs Framework.

The IFRS stands for the International Financial Reporting Standards stands for the fact

that is describes the basic concepts and draws the standards about the preparation of the

financial statements. These statements serves as a important tool to gauge the performance of

the company for the external users. As the users need information for making the purchase

decision in the company and not only the buyers but the information is reviewed by the lenders,

government. The users need information for various purposes other than buying and also to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assess that in future the company will be able to meet its resources or not and also the efficiency

of the company in discharging its responsibilities.

CRITERION 4 Regulation of accounting methods.

As there are variety of companies in the world and follow different accounting methods

to represent their data and perform the accounting accordingly. In order to ensure the uniformity

in the accounting, there are some set standards which are to be met and the entire accounting

information has to be presented accordingly. This helps in the uniformity of the information all

over the world which in turn helps in the comparison of the data and thus helps in the decision

of opting one company over the another (Zeff, 2014). It the systems would have been different

then the comparison between the companies would have been different and this would have

given rise to the confusion.

CRITERION 5- Define the use of published financial statements .

Financial statements helps in depicting the financial position and the performance of the

company and on the basis of that the decisions are made for the future. Financial statements are

the documents which helps in depicting the details of the business about the utilization of the

funds. The financial statements of Nestle which includes Balance sheet, Income statements ,

cash flow statements and helps the users to know the information regrading the revenue of the

company, as this is important for the investors to get the information regarding the dividends of

the company. It also helps the investors to know the future plans of Nestle and know the

direction in which it is heading.

CRITERION 6- Limitations of published financial statements .

The financial statements serves as a tool for measuring the financial performance of the

company but with that it has some limitations which are- the information which is given by the

financial statements may not always stand true in all respects as the human element is involved

in the preparation of the accounts,hence the chances of errors may be there. Sometimes just to

enhance the goodwill of the company window dressing is done in the financial statements

(GAAP, 2000). The financial statements is based on mainly the qualitative information hence

the major qualitative information is ignored which may be essential for the externals users to

know as that can influence their decision to great extent.

of the company in discharging its responsibilities.

CRITERION 4 Regulation of accounting methods.

As there are variety of companies in the world and follow different accounting methods

to represent their data and perform the accounting accordingly. In order to ensure the uniformity

in the accounting, there are some set standards which are to be met and the entire accounting

information has to be presented accordingly. This helps in the uniformity of the information all

over the world which in turn helps in the comparison of the data and thus helps in the decision

of opting one company over the another (Zeff, 2014). It the systems would have been different

then the comparison between the companies would have been different and this would have

given rise to the confusion.

CRITERION 5- Define the use of published financial statements .

Financial statements helps in depicting the financial position and the performance of the

company and on the basis of that the decisions are made for the future. Financial statements are

the documents which helps in depicting the details of the business about the utilization of the

funds. The financial statements of Nestle which includes Balance sheet, Income statements ,

cash flow statements and helps the users to know the information regrading the revenue of the

company, as this is important for the investors to get the information regarding the dividends of

the company. It also helps the investors to know the future plans of Nestle and know the

direction in which it is heading.

CRITERION 6- Limitations of published financial statements .

The financial statements serves as a tool for measuring the financial performance of the

company but with that it has some limitations which are- the information which is given by the

financial statements may not always stand true in all respects as the human element is involved

in the preparation of the accounts,hence the chances of errors may be there. Sometimes just to

enhance the goodwill of the company window dressing is done in the financial statements

(GAAP, 2000). The financial statements is based on mainly the qualitative information hence

the major qualitative information is ignored which may be essential for the externals users to

know as that can influence their decision to great extent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. DEFINE IASB WITH ITS ROLES AND IMPORTANCE..

CRITERION 7- Define roles of IASB

IASB stands for the International Accounting Standards Board which is an independent

private sector body which helps in developing and approving the International Financial

Reporting Standards (IFRS). Any changes or amendments in the IFRS is done by IASB and also

helps in the application of the said standards. In order to ensure the uniformity in the accounting

standards in the entire country thus helps in eradicating the ambiguity in understanding.

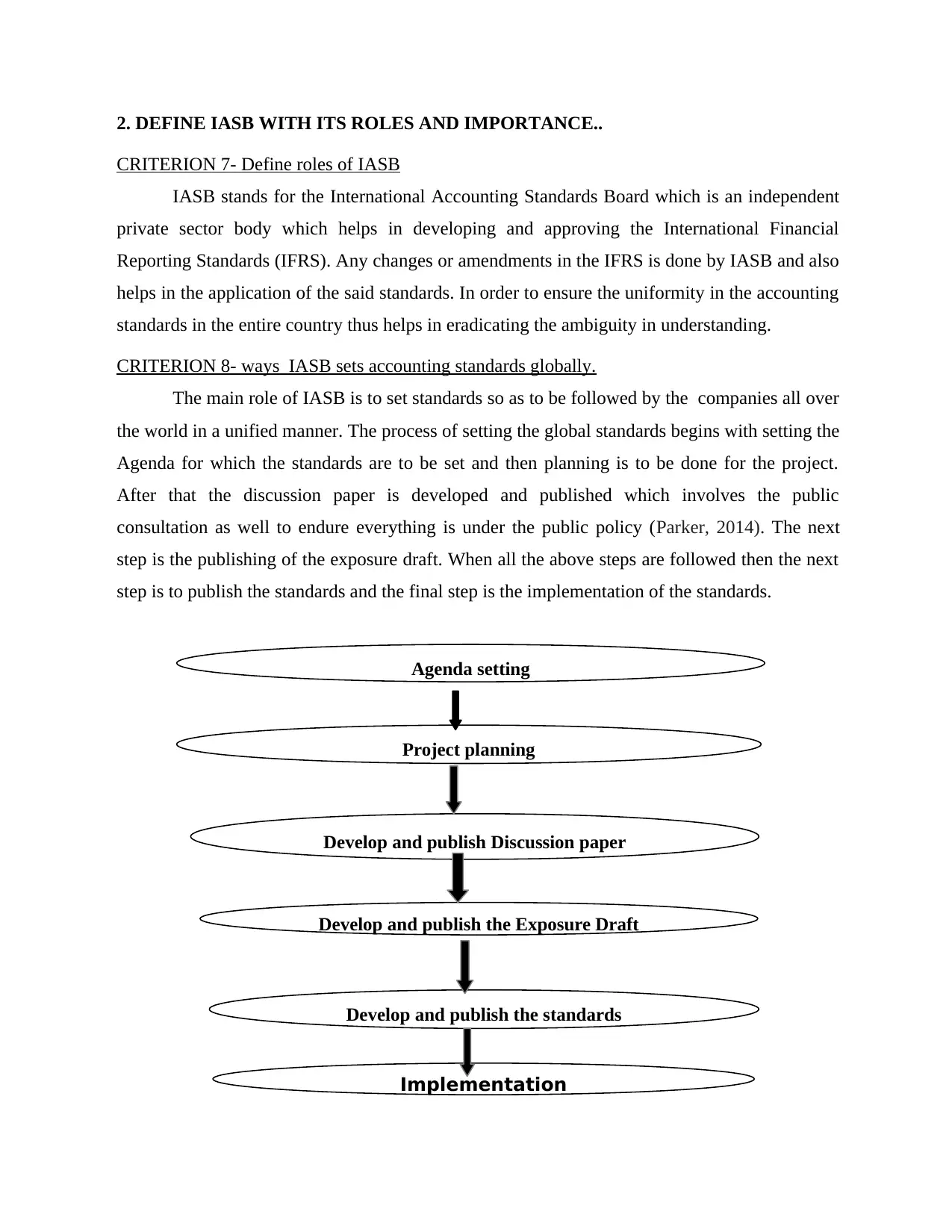

CRITERION 8- ways IASB sets accounting standards globally.

The main role of IASB is to set standards so as to be followed by the companies all over

the world in a unified manner. The process of setting the global standards begins with setting the

Agenda for which the standards are to be set and then planning is to be done for the project.

After that the discussion paper is developed and published which involves the public

consultation as well to endure everything is under the public policy (Parker, 2014). The next

step is the publishing of the exposure draft. When all the above steps are followed then the next

step is to publish the standards and the final step is the implementation of the standards.

Agenda setting

Project planning

Develop and publish Discussion paper

Develop and publish the Exposure Draft

Develop and publish the standards

Implementation

CRITERION 7- Define roles of IASB

IASB stands for the International Accounting Standards Board which is an independent

private sector body which helps in developing and approving the International Financial

Reporting Standards (IFRS). Any changes or amendments in the IFRS is done by IASB and also

helps in the application of the said standards. In order to ensure the uniformity in the accounting

standards in the entire country thus helps in eradicating the ambiguity in understanding.

CRITERION 8- ways IASB sets accounting standards globally.

The main role of IASB is to set standards so as to be followed by the companies all over

the world in a unified manner. The process of setting the global standards begins with setting the

Agenda for which the standards are to be set and then planning is to be done for the project.

After that the discussion paper is developed and published which involves the public

consultation as well to endure everything is under the public policy (Parker, 2014). The next

step is the publishing of the exposure draft. When all the above steps are followed then the next

step is to publish the standards and the final step is the implementation of the standards.

Agenda setting

Project planning

Develop and publish Discussion paper

Develop and publish the Exposure Draft

Develop and publish the standards

Implementation

CRITERION 9- How IASB enforces accounting standards globally.

The role of International Accounting Standards Board is to formulate and approve the

International Accounting Standards as per the needs and requirements of the particular

environment or as per the changes in the government regulations and so thus the changes has to

be incorporated in the standards as well for that a board meeting has to be convened and there

the discussions takes place and accordingly the standards which are set id enforced globally.

3. DISCUSSION OF THE ROLE AND PURPOSE OF MASB

CRITERION 10- Define roles of MASB.

MASB stands for Malaysian Accounting Standards Board was established under the

Financial Reporting Act 1997. it is ans independent body to develop and issue the standards and

the financial reporting in Malaysia. The functions and powers are: to issues new standards, to

review , revise and adopt the existing standards. It is also responsible for determining the scope

and application of the accounting standards according to which the systems are restricted. It has

to restrict its scope and perform the functions as specified by the Ministry of finance. The set

accounting standards are always open for the changes or modifications which are required to be

implemented as per the need and requirements.

CRITERION 11- The Setting of Malaysian accounting standards.

The setting of the accounting standards begins with the identifying the emerging issues

and then the discussion is done with the Working group analyze the issues. The Draft

Discussion paper is prepared by MASB which is submitted to Financial Reporting Foundation

(FRF) for review within the period of 14 days. Then the further discussion is issued for the

comments then the Draft Statement of Principles is Considered by MASB and further any

changes which are specified is to be done and the comments and the development has to be

addressed. Finally the approved standard goes for the publication.

CRITERION 12- How the MASB enforces accounting standards globally.

The enforcement of the global accounting standards which are done by the Malaysian

Accounting Standards Board is done in uniformity only and only after getting the approvals

form all the board members and before that the modifications which are stated has to be

complied with as per the needs and only then the accounting standards are updated and

approved.

The role of International Accounting Standards Board is to formulate and approve the

International Accounting Standards as per the needs and requirements of the particular

environment or as per the changes in the government regulations and so thus the changes has to

be incorporated in the standards as well for that a board meeting has to be convened and there

the discussions takes place and accordingly the standards which are set id enforced globally.

3. DISCUSSION OF THE ROLE AND PURPOSE OF MASB

CRITERION 10- Define roles of MASB.

MASB stands for Malaysian Accounting Standards Board was established under the

Financial Reporting Act 1997. it is ans independent body to develop and issue the standards and

the financial reporting in Malaysia. The functions and powers are: to issues new standards, to

review , revise and adopt the existing standards. It is also responsible for determining the scope

and application of the accounting standards according to which the systems are restricted. It has

to restrict its scope and perform the functions as specified by the Ministry of finance. The set

accounting standards are always open for the changes or modifications which are required to be

implemented as per the need and requirements.

CRITERION 11- The Setting of Malaysian accounting standards.

The setting of the accounting standards begins with the identifying the emerging issues

and then the discussion is done with the Working group analyze the issues. The Draft

Discussion paper is prepared by MASB which is submitted to Financial Reporting Foundation

(FRF) for review within the period of 14 days. Then the further discussion is issued for the

comments then the Draft Statement of Principles is Considered by MASB and further any

changes which are specified is to be done and the comments and the development has to be

addressed. Finally the approved standard goes for the publication.

CRITERION 12- How the MASB enforces accounting standards globally.

The enforcement of the global accounting standards which are done by the Malaysian

Accounting Standards Board is done in uniformity only and only after getting the approvals

form all the board members and before that the modifications which are stated has to be

complied with as per the needs and only then the accounting standards are updated and

approved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. EVALUATION OF THE ADHEREANCE TO IASB OF THE COMPANY'S

FINANCIAL STATEMENTS.

CRITERION 13- Define going concern concept.

In context of the financial frameworks, going concern being a simple but is very

important financial accounting principle which is created on the basis of financial statements

which are stated on the concept of that the organizations will continue for the unlimited period

of time. This principle believes that the organization will continue for unlimited period of time

and there is no intention of close down of the business. The going concern principles affects the

recording of the financial transactions. This principle is applicable for the entire organization as

a whole. Another reason is that the going concern organization has to follow the principles as

well such as IFRS.

CRITERION 14- Items affecting the going concern concept form the company's financial

statements.

Nestle being engaged in the business of food. Being a going concern firm the financial

statements which reveal this are the impact on the sales. If the sales of the organizations

continues to rise for the previous years one can say it is a going concern and even the loyalty of

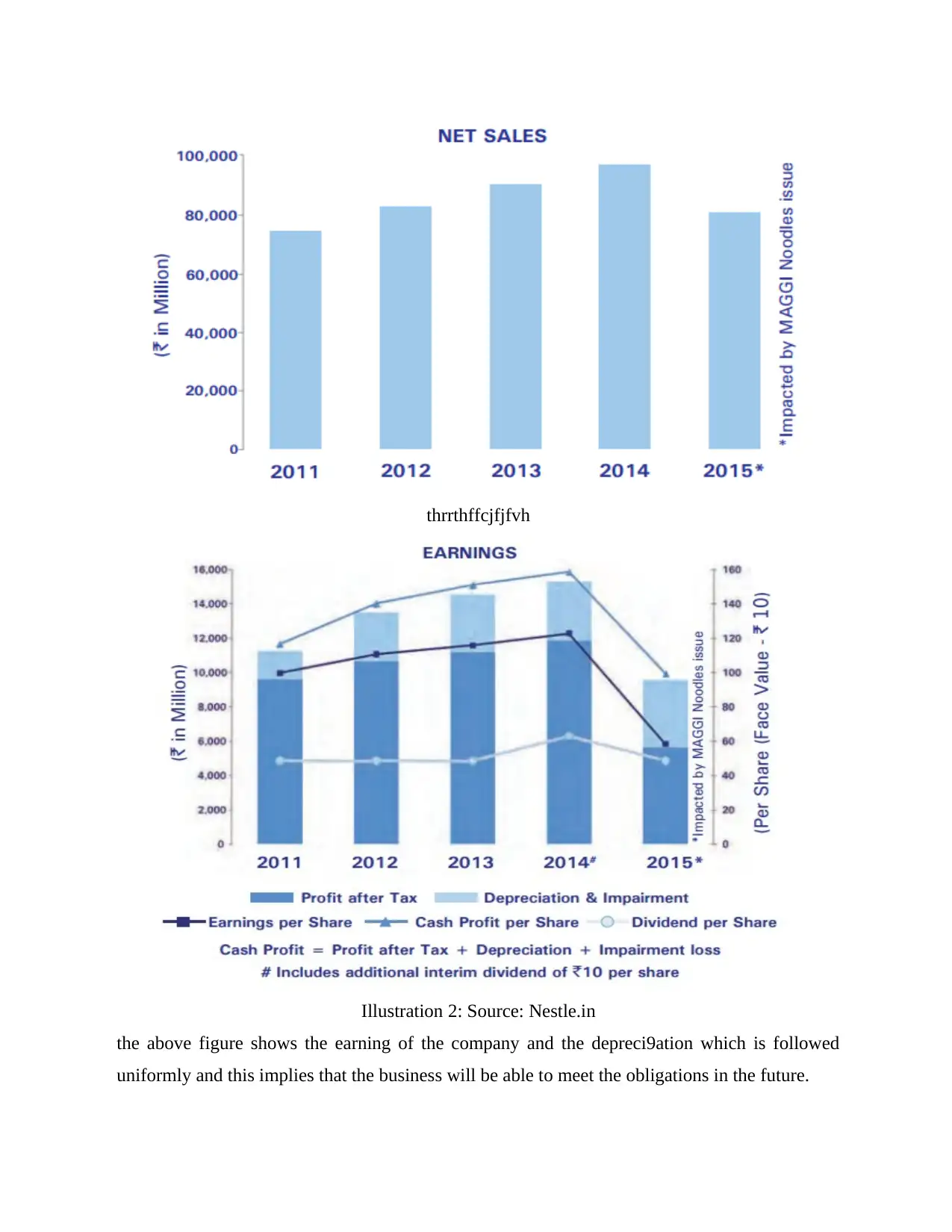

the people can be seen. From the below we can see that the sales continues to increase and only

due to the issue in 2015 it reduces due to the Maggi noodles issue.

FINANCIAL STATEMENTS.

CRITERION 13- Define going concern concept.

In context of the financial frameworks, going concern being a simple but is very

important financial accounting principle which is created on the basis of financial statements

which are stated on the concept of that the organizations will continue for the unlimited period

of time. This principle believes that the organization will continue for unlimited period of time

and there is no intention of close down of the business. The going concern principles affects the

recording of the financial transactions. This principle is applicable for the entire organization as

a whole. Another reason is that the going concern organization has to follow the principles as

well such as IFRS.

CRITERION 14- Items affecting the going concern concept form the company's financial

statements.

Nestle being engaged in the business of food. Being a going concern firm the financial

statements which reveal this are the impact on the sales. If the sales of the organizations

continues to rise for the previous years one can say it is a going concern and even the loyalty of

the people can be seen. From the below we can see that the sales continues to increase and only

due to the issue in 2015 it reduces due to the Maggi noodles issue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

thrrthffcjfjfvh

the above figure shows the earning of the company and the depreci9ation which is followed

uniformly and this implies that the business will be able to meet the obligations in the future.

Illustration 2: Source: Nestle.in

the above figure shows the earning of the company and the depreci9ation which is followed

uniformly and this implies that the business will be able to meet the obligations in the future.

Illustration 2: Source: Nestle.in

CRITERION 15- Explain accruals basis of accounting .

The specified company follows the accrual basis of accounting (Zeff, 2014). In this, the

recording is done whenever they are earned and not at the time when they are received. But in

the cash basis of accounting, the revenues are recorded only when they are received and not on

the date when they are earned. In the accrual basis of accounting the incomes are matched with

their revenues and is recorded until when the cash remains unpaid.

CRITERION 16- List of transactions which are affected by accrual basis.

In accrual basis of accounting , the transactions are recorded at the time when sales took

place. Here sales takes place when the ownership of the products is transferred from one person

to another. Not when the person actually pays for the product as sometimes the payment gets

delayed. These days as the number of credit card transactions has increased therefore the

companies have large amount of accounts receivable and thus this increases the accrued revenue

as well.

CRITERION 17- Define the Qualitative characteristics of Financial information.

The financial information presented by Nestle consist of only the quantitative part but

with that it also included the qualitative aspects as well (Parker, 2014). These aspects are

Relevance means that the financial statements are useful for decision making. Understand

ability implies that the users understand the information.

CRITERION 18- The financial information which are affected by qualitative characteristics.

The financial statements of Nestle reveals that the information which is presented has the

Comparable nature which shows that the financial information is available for many years so

that it can improve thew comparison over the years. The information which is obtained is

Faithful as they are free form the misstatement as that are reviewed by the auditors. As the

financial information is presented it ensures the information is available and is not delayed. This

ensures Timeliness of the information.

CONCLUSION

The entire report concludes that the various accounting standards are implemented by the

appropriate authorities and it discussed the importance of stock markers and the stock changes

for the company.

The specified company follows the accrual basis of accounting (Zeff, 2014). In this, the

recording is done whenever they are earned and not at the time when they are received. But in

the cash basis of accounting, the revenues are recorded only when they are received and not on

the date when they are earned. In the accrual basis of accounting the incomes are matched with

their revenues and is recorded until when the cash remains unpaid.

CRITERION 16- List of transactions which are affected by accrual basis.

In accrual basis of accounting , the transactions are recorded at the time when sales took

place. Here sales takes place when the ownership of the products is transferred from one person

to another. Not when the person actually pays for the product as sometimes the payment gets

delayed. These days as the number of credit card transactions has increased therefore the

companies have large amount of accounts receivable and thus this increases the accrued revenue

as well.

CRITERION 17- Define the Qualitative characteristics of Financial information.

The financial information presented by Nestle consist of only the quantitative part but

with that it also included the qualitative aspects as well (Parker, 2014). These aspects are

Relevance means that the financial statements are useful for decision making. Understand

ability implies that the users understand the information.

CRITERION 18- The financial information which are affected by qualitative characteristics.

The financial statements of Nestle reveals that the information which is presented has the

Comparable nature which shows that the financial information is available for many years so

that it can improve thew comparison over the years. The information which is obtained is

Faithful as they are free form the misstatement as that are reviewed by the auditors. As the

financial information is presented it ensures the information is available and is not delayed. This

ensures Timeliness of the information.

CONCLUSION

The entire report concludes that the various accounting standards are implemented by the

appropriate authorities and it discussed the importance of stock markers and the stock changes

for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research. 47(1). pp.1-29.

Marriott, N., Stoner, G., Fogarty, T. and Sangster, A., 2014. Publishing characteristics,

geographic dispersion and research traditions of recent international accounting

education research. The British Accounting Review. 46(3). pp.264-280.

Zeff, S.A., 2002. “Political” lobbying on proposed standards: A challenge to the

IASB. Accounting Horizons, 16(1), pp.43-54.

GAAP, U., 2000. International accounting standards

Morais, A.I. and Curto, J.D., 2008. Accounting quality and the adoption of IASB standards:

portuguese evidence. Revista Contabilidade & Finanças, 19(48), pp.103-111.

Parker, R.H., 2014. Some international aspects of accounting. International Accounting and

Transnational Decisions. 9.

Online

International accounting system, 2017. [Online]. Available through :< https://www.nestle.in/>.

[Accessed on 29th May 2017].

Books and Journals

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research. 47(1). pp.1-29.

Marriott, N., Stoner, G., Fogarty, T. and Sangster, A., 2014. Publishing characteristics,

geographic dispersion and research traditions of recent international accounting

education research. The British Accounting Review. 46(3). pp.264-280.

Zeff, S.A., 2002. “Political” lobbying on proposed standards: A challenge to the

IASB. Accounting Horizons, 16(1), pp.43-54.

GAAP, U., 2000. International accounting standards

Morais, A.I. and Curto, J.D., 2008. Accounting quality and the adoption of IASB standards:

portuguese evidence. Revista Contabilidade & Finanças, 19(48), pp.103-111.

Parker, R.H., 2014. Some international aspects of accounting. International Accounting and

Transnational Decisions. 9.

Online

International accounting system, 2017. [Online]. Available through :< https://www.nestle.in/>.

[Accessed on 29th May 2017].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.