Corporate Tax Report: Analysis of Temporary and Permanent Differences

VerifiedAdded on 2023/01/16

|6

|937

|88

Report

AI Summary

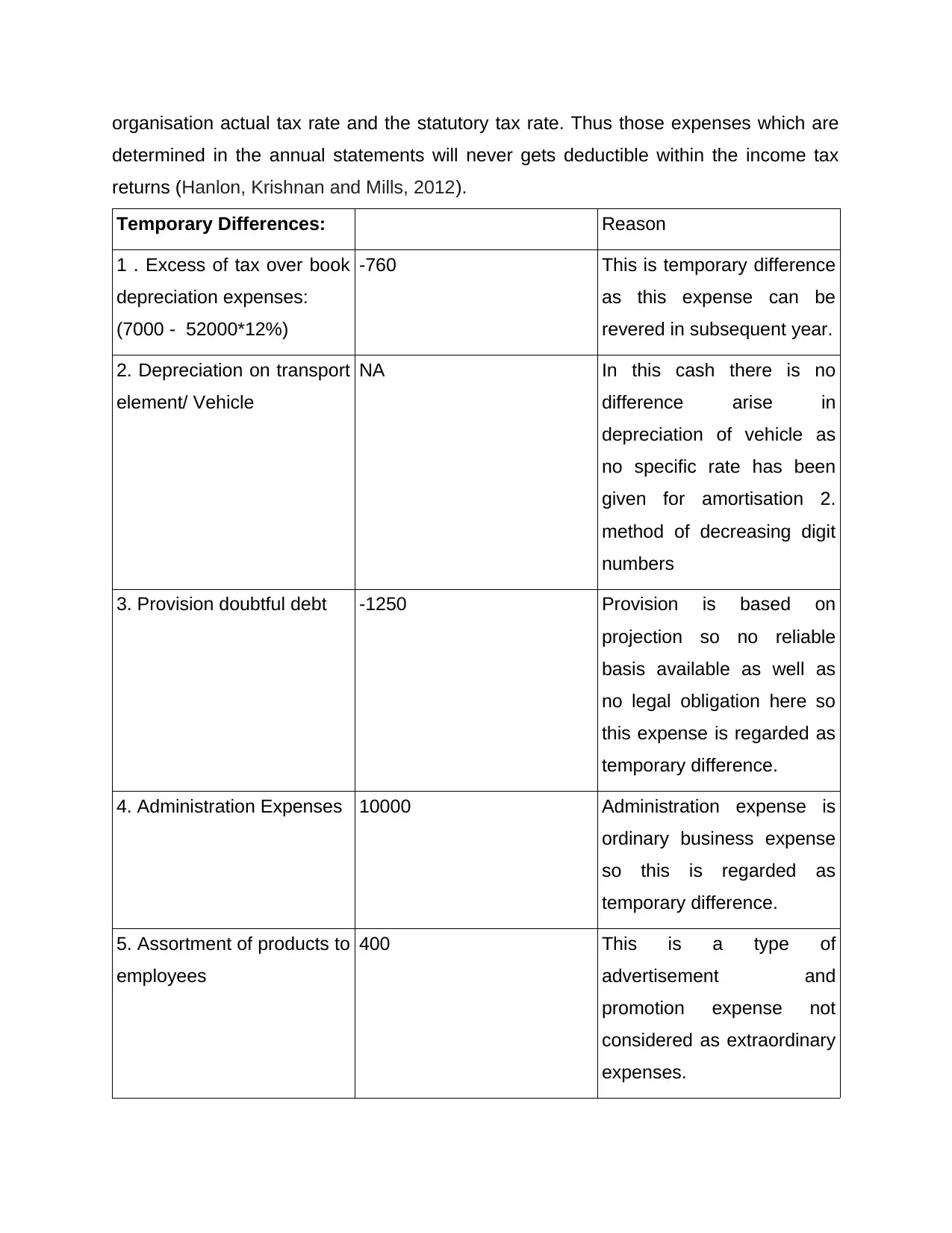

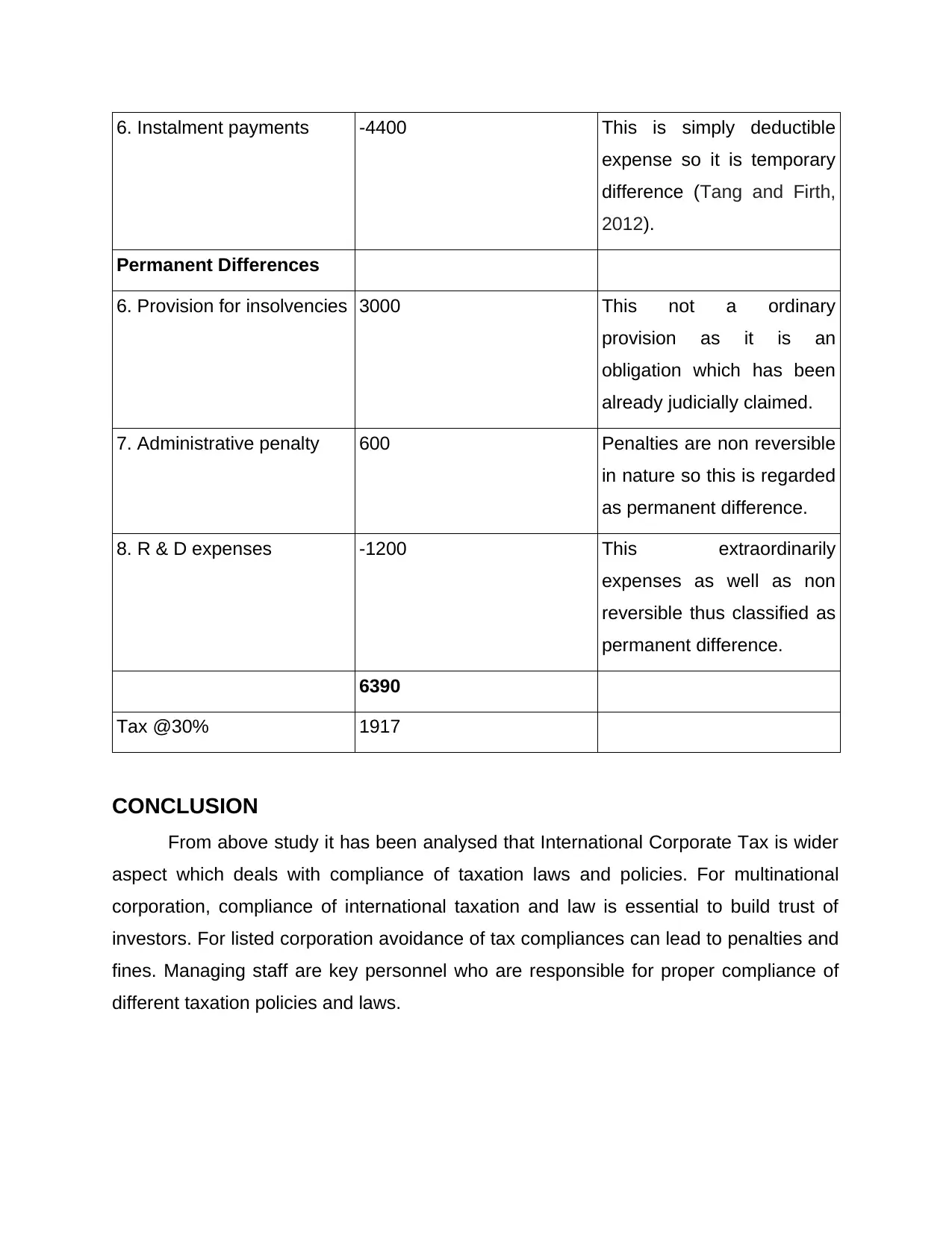

This report offers a detailed analysis of international corporate tax, focusing on the distinction between temporary and permanent differences. It begins with an introduction to corporate tax, also known as corporation tax, and its application at both global and local levels. The core of the report involves a task-based breakdown, calculating corporate tax liabilities based on given data. It thoroughly examines temporary differences, which include depreciation expenses, provisions for doubtful debts, and administrative expenses, explaining how these differences create deferred tax liabilities or assets that reverse over time. The report also investigates permanent differences, such as administrative penalties and research and development expenses, which do not result in deferred tax savings or debts. The conclusion summarizes the importance of compliance with international taxation laws, particularly for multinational corporations, and the role of managing staff in ensuring proper compliance. The report references several academic sources to support its analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.