TAXA3000 Assignment 2: International Tax Systems Comparison

VerifiedAdded on 2023/03/17

|14

|3810

|76

Report

AI Summary

This report provides a comprehensive comparison of the tax systems of the United States of America and Australia, focusing on key aspects such as income tax, company tax, and consumption tax. It delves into the specifics of each tax type, detailing tax rates, brackets, and relevant regulations in both countries. The report also examines the role and significance of Double Tax Agreements (DTAs) and assesses the comprehensiveness of the USA's treaty network. Furthermore, it evaluates the tax systems of both countries based on criteria like simplicity, equity, certainty, and efficiency. The analysis includes a discussion of recent taxation issues and concerns that have been prominent in the USA's government, media, and business communities. The report aims to provide a clear understanding of the similarities and differences in the tax structures of the two nations, offering insights into their respective strengths and weaknesses.

Running head: REPORT 0

FOUNDATION OF INTERNATIONAL TAXATION

MAY 10, 2019

STUDENT DETAILS:

FOUNDATION OF INTERNATIONAL TAXATION

MAY 10, 2019

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Introduction............................................................................................................................ 1

America tax system................................................................................................................ 2

Income Tax......................................................................................................................... 2

Company Tax..................................................................................................................... 4

Consumption Tax................................................................................................................ 5

Double tax agreements.......................................................................................................6

Function and importance Double tax agreements...........................................................6

Ranking of American tax system regarding simplicity, equity, certainty and efficiency...........7

Conclusion............................................................................................................................. 7

Bibliography........................................................................................................................... 9

Appendix.............................................................................................................................. 10

Contents

Introduction............................................................................................................................ 1

America tax system................................................................................................................ 2

Income Tax......................................................................................................................... 2

Company Tax..................................................................................................................... 4

Consumption Tax................................................................................................................ 5

Double tax agreements.......................................................................................................6

Function and importance Double tax agreements...........................................................6

Ranking of American tax system regarding simplicity, equity, certainty and efficiency...........7

Conclusion............................................................................................................................. 7

Bibliography........................................................................................................................... 9

Appendix.............................................................................................................................. 10

REPORT 2

Introduction

Taxation is a significant economic issue like the political issue. Tax policies are

useful in promoting the agenda by adopting numerous taxation reforms such as

reducing tax rates or increasing tax rates, making changes in the meaning of taxable

income, making new tax over the particular products. No person mostly desires to

make payment of tax. Specific groups, such as farmers, owners of small business,

retired people, utilized important political efforts to decrease the shares of the

taxation burden. Tax policies have significant financial consequences for a central

economy as well as for the specific people within economy.

Tax policies are often made with intentions of motivating financial development even

though economists vary significantly regarding the policies, which are most real at

development or progress. Taxmay make incentives encouraging necessary

behaviour and discouragements for undesirable actions. Taxes provide the

resources to reallocate financial resources to those with lower income or specific

requirements (Lawrence, Bernstein, and Schmitt 2016). Tax provides the revenues

required for serious public services like social protection, healthcare services, state

defence, and learning. The policies related to tax markedly show the expression of

powers in United States of America. In the following parts, America tax system

including income tax, consumption tax, company tax, and Double Tax Agreements,

which USA has with other countries. This report also compares these elements of

that tax system of America to the tax system of Australia. The below mentioned parts

also evaluate the tax system of USA as per ranking in respect of easiness, equity,

inevitability and effectiveness.

America tax system

The USA has separate federal government, local government and state

government with tax imposed at all the stages. Taxes are levied on income,

properties, sales, payroll, import, capital gains, dividend, estate and gift, and

numerous fees. The residents or citizens of country are taxed on worldwide income

and permitted the credit for the international taxes (Nora and Pereira 2016). The tax

system of America can be explained below-

Income Tax

Income tax is possibly one of the most well-known methods of tax. In a case where

the people earn income in USA, they would see the deduction on the paycheck. All

the people who earn income in the USA is expected to make payment of income tax

on federal level as well as state level. The federal tax includes FICA as well as social

protection. Every state has its individual method of income tax, which managers also

withhold from thePay check. In a case where individuals earn above the specific

amount 6,750$, then they should file federal tax as well as state tax before 15 April

of every year.

Introduction

Taxation is a significant economic issue like the political issue. Tax policies are

useful in promoting the agenda by adopting numerous taxation reforms such as

reducing tax rates or increasing tax rates, making changes in the meaning of taxable

income, making new tax over the particular products. No person mostly desires to

make payment of tax. Specific groups, such as farmers, owners of small business,

retired people, utilized important political efforts to decrease the shares of the

taxation burden. Tax policies have significant financial consequences for a central

economy as well as for the specific people within economy.

Tax policies are often made with intentions of motivating financial development even

though economists vary significantly regarding the policies, which are most real at

development or progress. Taxmay make incentives encouraging necessary

behaviour and discouragements for undesirable actions. Taxes provide the

resources to reallocate financial resources to those with lower income or specific

requirements (Lawrence, Bernstein, and Schmitt 2016). Tax provides the revenues

required for serious public services like social protection, healthcare services, state

defence, and learning. The policies related to tax markedly show the expression of

powers in United States of America. In the following parts, America tax system

including income tax, consumption tax, company tax, and Double Tax Agreements,

which USA has with other countries. This report also compares these elements of

that tax system of America to the tax system of Australia. The below mentioned parts

also evaluate the tax system of USA as per ranking in respect of easiness, equity,

inevitability and effectiveness.

America tax system

The USA has separate federal government, local government and state

government with tax imposed at all the stages. Taxes are levied on income,

properties, sales, payroll, import, capital gains, dividend, estate and gift, and

numerous fees. The residents or citizens of country are taxed on worldwide income

and permitted the credit for the international taxes (Nora and Pereira 2016). The tax

system of America can be explained below-

Income Tax

Income tax is possibly one of the most well-known methods of tax. In a case where

the people earn income in USA, they would see the deduction on the paycheck. All

the people who earn income in the USA is expected to make payment of income tax

on federal level as well as state level. The federal tax includes FICA as well as social

protection. Every state has its individual method of income tax, which managers also

withhold from thePay check. In a case where individuals earn above the specific

amount 6,750$, then they should file federal tax as well as state tax before 15 April

of every year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Further, taxes are levied on net income of corporation and individual by the federal

state, most state, as well as certain local governments. The tax systems in each

jurisdiction can describe the taxable income distinctly. Various states refer to certain

scope to federal concept for defining the taxable income. The income tax is

calculated by implementing the tax rate that can rise as income rise, to taxable

income that is total income less permissible deduction from income. The income is

largely described. The companies as well as companies are taxable in direct way,

and estate and trust can be taxable over unallocated incomes. In addition, the

partnerships are not taxed; however, the partners are taxed upon the share of

income related to partnership. Residents of United States of America are taxed on

international incomes, when taxes are levied on the income of non-residents within

the jurisdiction. Various kinds of credits decrease the taxes. On the other hand,

certain kinds of credits cango beyond tax prior to credit. A substitute tax relates to

the federal level and certain state levels (Vito 2018).

Most business expenses are deductible. The individual may also deduct the personal

allowances or exemptions and meet individual expenditures, involving interest on

home mortgage, state tax, contribution to donations, and certain more items.

Additionally, there are certain somedeductions are subject to limit.Capital gain is

taxable. The capital loss reduces taxable income to a level of gains (plus, in some

cases, 3,000 $ or 1,500 $ of normal incomes). Individual recently pays the tax with

low rate on capital gain and some corporate dividend (Andrew 2017, 199-219).

Furthermore, the taxpayer usually must self-assess income tax by tax return’s filling.

Tax’s advance payment is essential in respect of projected tax paymentor

withholding tax. Taxes are subject to separate jurisdiction levying taxes. Due date

and other administrative processes differ by jurisdictions. Tax as calculated by the

taxpayer can be adjusted by taxation jurisdiction (Allison, Schoen, and Shay, 2018).

The tax in Australia covers under inspection for being specifically higher. To state

whether these claims are correct, the tax rates in Australia are compared with

America below.

Australia Individual Tax Rate

Resident tax rates 2018–19

Taxable income Tax on this income

0 – $18,200 Nil

Further, taxes are levied on net income of corporation and individual by the federal

state, most state, as well as certain local governments. The tax systems in each

jurisdiction can describe the taxable income distinctly. Various states refer to certain

scope to federal concept for defining the taxable income. The income tax is

calculated by implementing the tax rate that can rise as income rise, to taxable

income that is total income less permissible deduction from income. The income is

largely described. The companies as well as companies are taxable in direct way,

and estate and trust can be taxable over unallocated incomes. In addition, the

partnerships are not taxed; however, the partners are taxed upon the share of

income related to partnership. Residents of United States of America are taxed on

international incomes, when taxes are levied on the income of non-residents within

the jurisdiction. Various kinds of credits decrease the taxes. On the other hand,

certain kinds of credits cango beyond tax prior to credit. A substitute tax relates to

the federal level and certain state levels (Vito 2018).

Most business expenses are deductible. The individual may also deduct the personal

allowances or exemptions and meet individual expenditures, involving interest on

home mortgage, state tax, contribution to donations, and certain more items.

Additionally, there are certain somedeductions are subject to limit.Capital gain is

taxable. The capital loss reduces taxable income to a level of gains (plus, in some

cases, 3,000 $ or 1,500 $ of normal incomes). Individual recently pays the tax with

low rate on capital gain and some corporate dividend (Andrew 2017, 199-219).

Furthermore, the taxpayer usually must self-assess income tax by tax return’s filling.

Tax’s advance payment is essential in respect of projected tax paymentor

withholding tax. Taxes are subject to separate jurisdiction levying taxes. Due date

and other administrative processes differ by jurisdictions. Tax as calculated by the

taxpayer can be adjusted by taxation jurisdiction (Allison, Schoen, and Shay, 2018).

The tax in Australia covers under inspection for being specifically higher. To state

whether these claims are correct, the tax rates in Australia are compared with

America below.

Australia Individual Tax Rate

Resident tax rates 2018–19

Taxable income Tax on this income

0 – $18,200 Nil

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

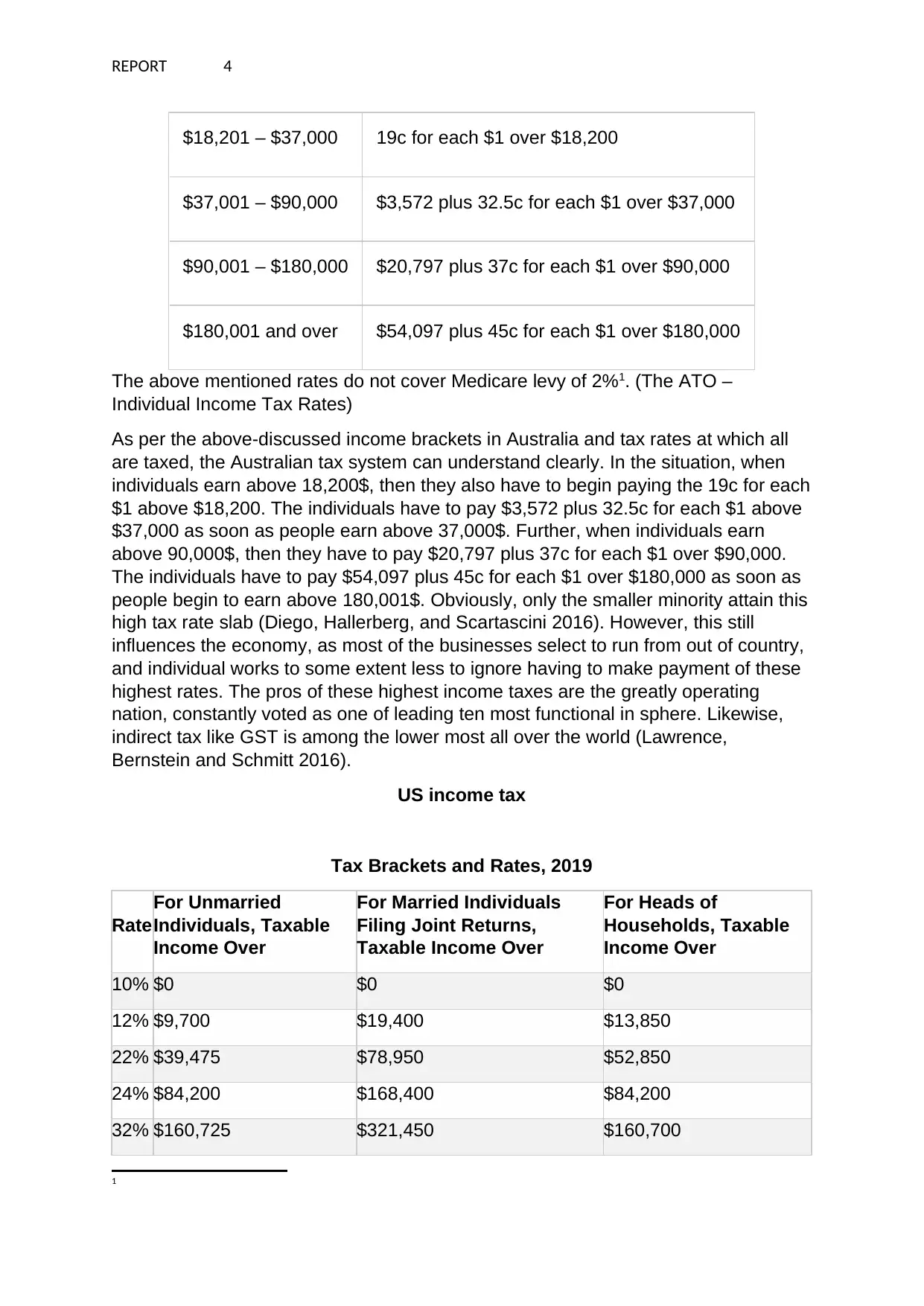

$18,201 – $37,000 19c for each $1 over $18,200

$37,001 – $90,000 $3,572 plus 32.5c for each $1 over $37,000

$90,001 – $180,000 $20,797 plus 37c for each $1 over $90,000

$180,001 and over $54,097 plus 45c for each $1 over $180,000

The above mentioned rates do not cover Medicare levy of 2%1. (The ATO –

Individual Income Tax Rates)

As per the above-discussed income brackets in Australia and tax rates at which all

are taxed, the Australian tax system can understand clearly. In the situation, when

individuals earn above 18,200$, then they also have to begin paying the 19c for each

$1 above $18,200. The individuals have to pay $3,572 plus 32.5c for each $1 above

$37,000 as soon as people earn above 37,000$. Further, when individuals earn

above 90,000$, then they have to pay $20,797 plus 37c for each $1 over $90,000.

The individuals have to pay $54,097 plus 45c for each $1 over $180,000 as soon as

people begin to earn above 180,001$. Obviously, only the smaller minority attain this

high tax rate slab (Diego, Hallerberg, and Scartascini 2016). However, this still

influences the economy, as most of the businesses select to run from out of country,

and individual works to some extent less to ignore having to make payment of these

highest rates. The pros of these highest income taxes are the greatly operating

nation, constantly voted as one of leading ten most functional in sphere. Likewise,

indirect tax like GST is among the lower most all over the world (Lawrence,

Bernstein and Schmitt 2016).

US income tax

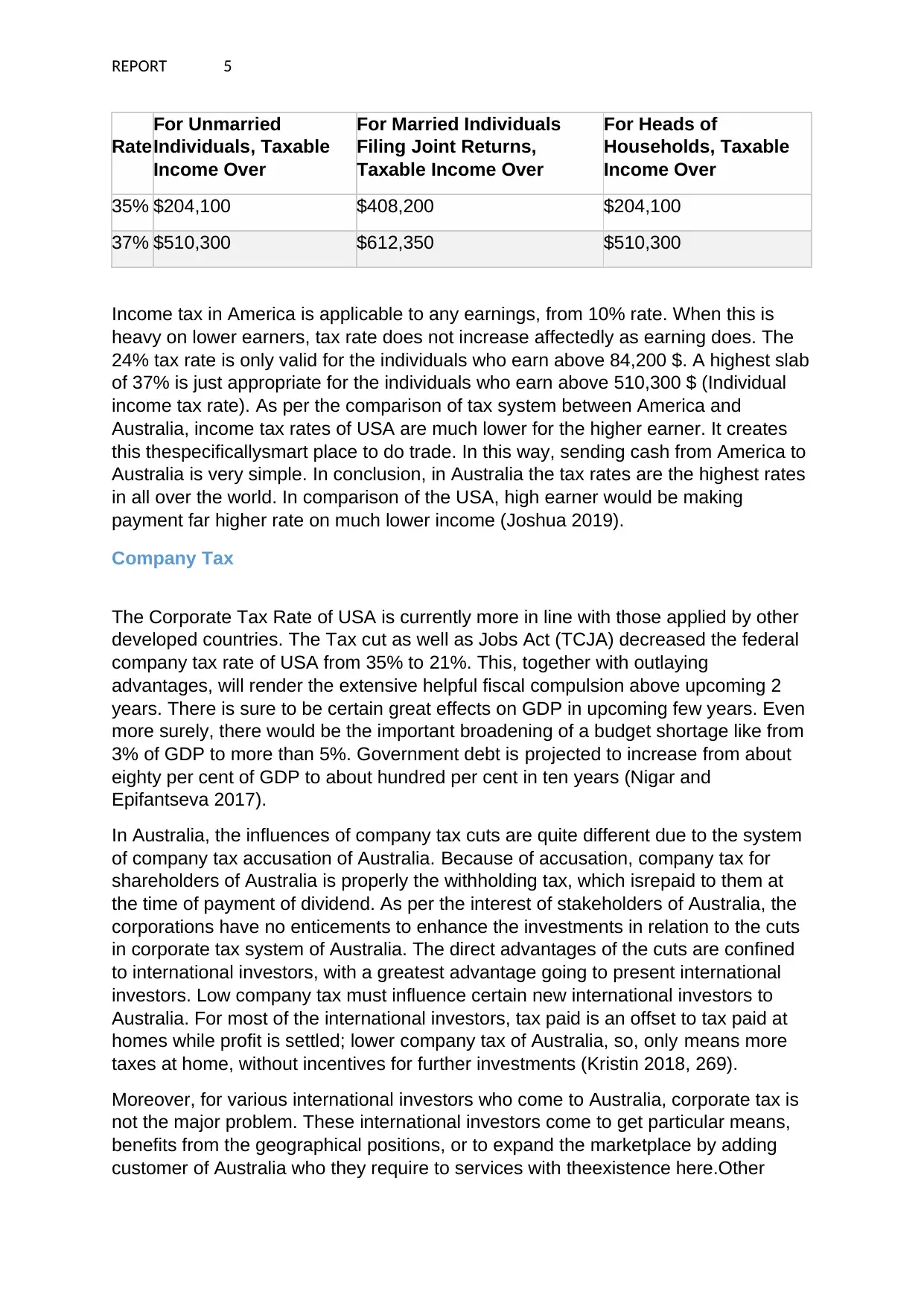

Tax Brackets and Rates, 2019

Rate

For Unmarried

Individuals, Taxable

Income Over

For Married Individuals

Filing Joint Returns,

Taxable Income Over

For Heads of

Households, Taxable

Income Over

10% $0 $0 $0

12% $9,700 $19,400 $13,850

22% $39,475 $78,950 $52,850

24% $84,200 $168,400 $84,200

32% $160,725 $321,450 $160,700

1

$18,201 – $37,000 19c for each $1 over $18,200

$37,001 – $90,000 $3,572 plus 32.5c for each $1 over $37,000

$90,001 – $180,000 $20,797 plus 37c for each $1 over $90,000

$180,001 and over $54,097 plus 45c for each $1 over $180,000

The above mentioned rates do not cover Medicare levy of 2%1. (The ATO –

Individual Income Tax Rates)

As per the above-discussed income brackets in Australia and tax rates at which all

are taxed, the Australian tax system can understand clearly. In the situation, when

individuals earn above 18,200$, then they also have to begin paying the 19c for each

$1 above $18,200. The individuals have to pay $3,572 plus 32.5c for each $1 above

$37,000 as soon as people earn above 37,000$. Further, when individuals earn

above 90,000$, then they have to pay $20,797 plus 37c for each $1 over $90,000.

The individuals have to pay $54,097 plus 45c for each $1 over $180,000 as soon as

people begin to earn above 180,001$. Obviously, only the smaller minority attain this

high tax rate slab (Diego, Hallerberg, and Scartascini 2016). However, this still

influences the economy, as most of the businesses select to run from out of country,

and individual works to some extent less to ignore having to make payment of these

highest rates. The pros of these highest income taxes are the greatly operating

nation, constantly voted as one of leading ten most functional in sphere. Likewise,

indirect tax like GST is among the lower most all over the world (Lawrence,

Bernstein and Schmitt 2016).

US income tax

Tax Brackets and Rates, 2019

Rate

For Unmarried

Individuals, Taxable

Income Over

For Married Individuals

Filing Joint Returns,

Taxable Income Over

For Heads of

Households, Taxable

Income Over

10% $0 $0 $0

12% $9,700 $19,400 $13,850

22% $39,475 $78,950 $52,850

24% $84,200 $168,400 $84,200

32% $160,725 $321,450 $160,700

1

REPORT 5

Rate

For Unmarried

Individuals, Taxable

Income Over

For Married Individuals

Filing Joint Returns,

Taxable Income Over

For Heads of

Households, Taxable

Income Over

35% $204,100 $408,200 $204,100

37% $510,300 $612,350 $510,300

Income tax in America is applicable to any earnings, from 10% rate. When this is

heavy on lower earners, tax rate does not increase affectedly as earning does. The

24% tax rate is only valid for the individuals who earn above 84,200 $. A highest slab

of 37% is just appropriate for the individuals who earn above 510,300 $ (Individual

income tax rate). As per the comparison of tax system between America and

Australia, income tax rates of USA are much lower for the higher earner. It creates

this thespecificallysmart place to do trade. In this way, sending cash from America to

Australia is very simple. In conclusion, in Australia the tax rates are the highest rates

in all over the world. In comparison of the USA, high earner would be making

payment far higher rate on much lower income (Joshua 2019).

Company Tax

The Corporate Tax Rate of USA is currently more in line with those applied by other

developed countries. The Tax cut as well as Jobs Act (TCJA) decreased the federal

company tax rate of USA from 35% to 21%. This, together with outlaying

advantages, will render the extensive helpful fiscal compulsion above upcoming 2

years. There is sure to be certain great effects on GDP in upcoming few years. Even

more surely, there would be the important broadening of a budget shortage like from

3% of GDP to more than 5%. Government debt is projected to increase from about

eighty per cent of GDP to about hundred per cent in ten years (Nigar and

Epifantseva 2017).

In Australia, the influences of company tax cuts are quite different due to the system

of company tax accusation of Australia. Because of accusation, company tax for

shareholders of Australia is properly the withholding tax, which isrepaid to them at

the time of payment of dividend. As per the interest of stakeholders of Australia, the

corporations have no enticements to enhance the investments in relation to the cuts

in corporate tax system of Australia. The direct advantages of the cuts are confined

to international investors, with a greatest advantage going to present international

investors. Low company tax must influence certain new international investors to

Australia. For most of the international investors, tax paid is an offset to tax paid at

homes while profit is settled; lower company tax of Australia, so, only means more

taxes at home, without incentives for further investments (Kristin 2018, 269).

Moreover, for various international investors who come to Australia, corporate tax is

not the major problem. These international investors come to get particular means,

benefits from the geographical positions, or to expand the marketplace by adding

customer of Australia who they require to services with theexistence here.Other

Rate

For Unmarried

Individuals, Taxable

Income Over

For Married Individuals

Filing Joint Returns,

Taxable Income Over

For Heads of

Households, Taxable

Income Over

35% $204,100 $408,200 $204,100

37% $510,300 $612,350 $510,300

Income tax in America is applicable to any earnings, from 10% rate. When this is

heavy on lower earners, tax rate does not increase affectedly as earning does. The

24% tax rate is only valid for the individuals who earn above 84,200 $. A highest slab

of 37% is just appropriate for the individuals who earn above 510,300 $ (Individual

income tax rate). As per the comparison of tax system between America and

Australia, income tax rates of USA are much lower for the higher earner. It creates

this thespecificallysmart place to do trade. In this way, sending cash from America to

Australia is very simple. In conclusion, in Australia the tax rates are the highest rates

in all over the world. In comparison of the USA, high earner would be making

payment far higher rate on much lower income (Joshua 2019).

Company Tax

The Corporate Tax Rate of USA is currently more in line with those applied by other

developed countries. The Tax cut as well as Jobs Act (TCJA) decreased the federal

company tax rate of USA from 35% to 21%. This, together with outlaying

advantages, will render the extensive helpful fiscal compulsion above upcoming 2

years. There is sure to be certain great effects on GDP in upcoming few years. Even

more surely, there would be the important broadening of a budget shortage like from

3% of GDP to more than 5%. Government debt is projected to increase from about

eighty per cent of GDP to about hundred per cent in ten years (Nigar and

Epifantseva 2017).

In Australia, the influences of company tax cuts are quite different due to the system

of company tax accusation of Australia. Because of accusation, company tax for

shareholders of Australia is properly the withholding tax, which isrepaid to them at

the time of payment of dividend. As per the interest of stakeholders of Australia, the

corporations have no enticements to enhance the investments in relation to the cuts

in corporate tax system of Australia. The direct advantages of the cuts are confined

to international investors, with a greatest advantage going to present international

investors. Low company tax must influence certain new international investors to

Australia. For most of the international investors, tax paid is an offset to tax paid at

homes while profit is settled; lower company tax of Australia, so, only means more

taxes at home, without incentives for further investments (Kristin 2018, 269).

Moreover, for various international investors who come to Australia, corporate tax is

not the major problem. These international investors come to get particular means,

benefits from the geographical positions, or to expand the marketplace by adding

customer of Australia who they require to services with theexistence here.Other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

international investors organise the affairs to not to make payment or less payment

of tax in Australia: decreasing the legal rate here has nil impacts over them. It is

specifically correct for huge technical corporations like Amazon, Google, as well as

Facebook, wherever intellectual properties create this simple to shift the profit to

lower-taxationdominions. For any corporation encouraged greatly through corporate

tax, the 25% rate would not induce it away from the very lower rate over offers in

Singapore and Ireland. In conclusion, rather than continue the race-to-a-bottom over

corporatetax, the foreign communities requires to agree on the sensible international

regime that apportions corporate tax revenues amongst the numerous nations

included in producing the revenues.

Consumption Tax

Various nations covering members of the OECD raise revenues with the

consumption tax applied over incremental increases in the product’s value as well as

service’s value as they move by a supply chain. The VAT for short generates

substantial income and are relatively proficient to administer. USA is the only

Organization for Economic Cooperation and Development nation, which applies the

retail sales tax in place of VAT as a main consumption tax (Judith 2016, 328-339).

Further, in Australia, GST covers in the category of consumption tax. Other nations

have various variations of consumption tax normally labelling theirs as VAT. With

approaching the tax reforms, the comparison with consumption tax of different

nations can establish enlightening. America utilises the retail sales tax in place of

VAT. This tax, though, is not the central tax, in its place, state government as well as

local government is liable for the management. Currently, 45 American states apply

the tax involving thousands of local government levies that are as same as the retail

sales taxes. Since the Organization for Economic Cooperation and Development

categorizes retail sales tax and Value added Tax under the similar title of

consumption tax, this guesses that consumption tax shows just eight per cent of the

American total tax revenues, creating this the lowest in Organization for Economic

Cooperation and Development (Christopher, and Garnaut 2017)

Double Tax Agreements (DTAs)

There are various countries, which have entered in Double Tax Agreements or tax

treaties with different nations to avoid or mitigate double taxation. Under Double Tax

Agreements, residents of outside nations are taxed at the decreased rate, or are

exempt from American tax on various income items they get from means in USA.

These reduced rates and exemptions vary amongst nations and particular income

related items (Olivier, Jara, and Rodriguez 2017, 369-392).

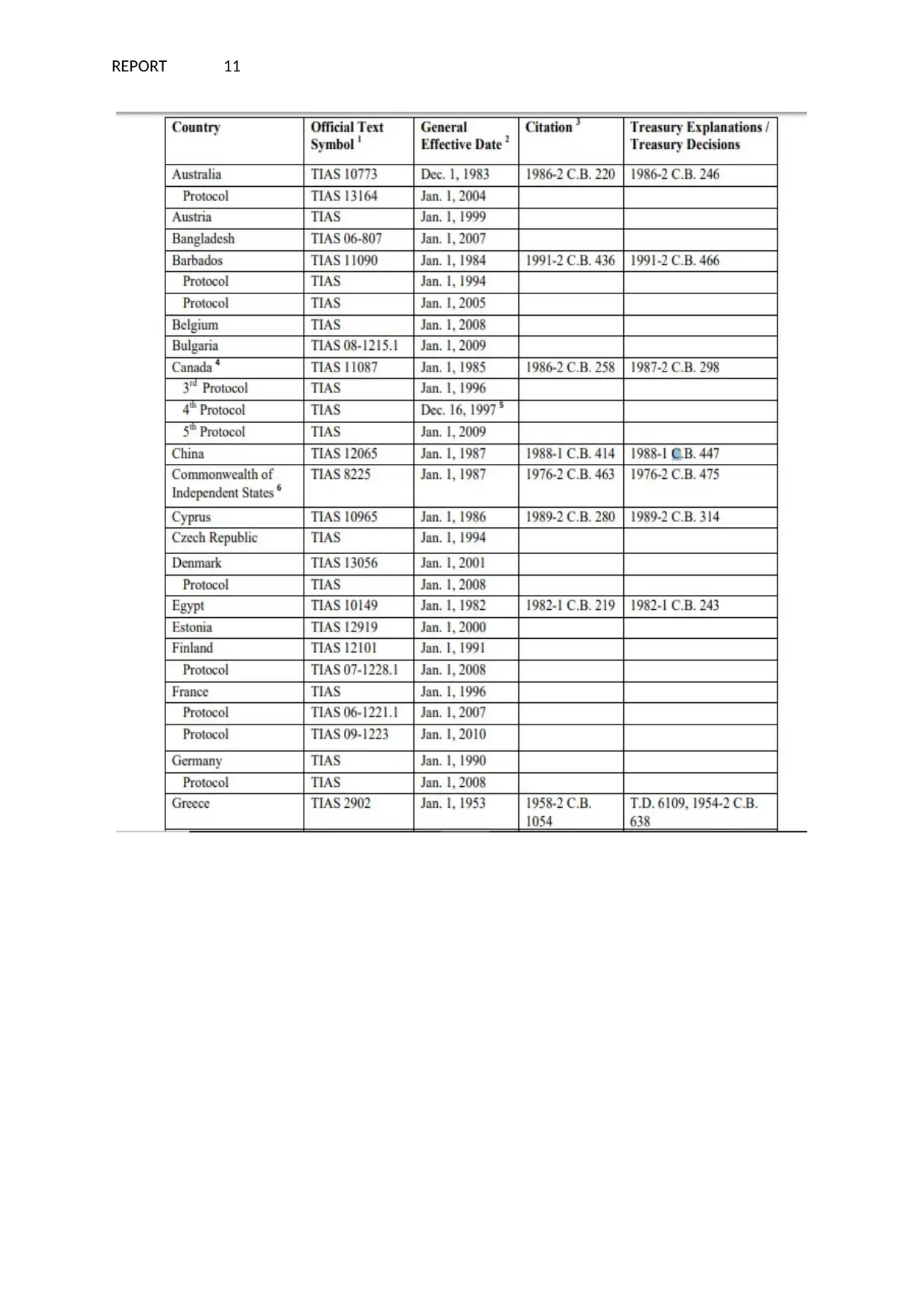

USA made double tax agreements with various countries (Refer Appendix). Under

the double tax agreements, American residents are taxed at the decreased rate, or

international investors organise the affairs to not to make payment or less payment

of tax in Australia: decreasing the legal rate here has nil impacts over them. It is

specifically correct for huge technical corporations like Amazon, Google, as well as

Facebook, wherever intellectual properties create this simple to shift the profit to

lower-taxationdominions. For any corporation encouraged greatly through corporate

tax, the 25% rate would not induce it away from the very lower rate over offers in

Singapore and Ireland. In conclusion, rather than continue the race-to-a-bottom over

corporatetax, the foreign communities requires to agree on the sensible international

regime that apportions corporate tax revenues amongst the numerous nations

included in producing the revenues.

Consumption Tax

Various nations covering members of the OECD raise revenues with the

consumption tax applied over incremental increases in the product’s value as well as

service’s value as they move by a supply chain. The VAT for short generates

substantial income and are relatively proficient to administer. USA is the only

Organization for Economic Cooperation and Development nation, which applies the

retail sales tax in place of VAT as a main consumption tax (Judith 2016, 328-339).

Further, in Australia, GST covers in the category of consumption tax. Other nations

have various variations of consumption tax normally labelling theirs as VAT. With

approaching the tax reforms, the comparison with consumption tax of different

nations can establish enlightening. America utilises the retail sales tax in place of

VAT. This tax, though, is not the central tax, in its place, state government as well as

local government is liable for the management. Currently, 45 American states apply

the tax involving thousands of local government levies that are as same as the retail

sales taxes. Since the Organization for Economic Cooperation and Development

categorizes retail sales tax and Value added Tax under the similar title of

consumption tax, this guesses that consumption tax shows just eight per cent of the

American total tax revenues, creating this the lowest in Organization for Economic

Cooperation and Development (Christopher, and Garnaut 2017)

Double Tax Agreements (DTAs)

There are various countries, which have entered in Double Tax Agreements or tax

treaties with different nations to avoid or mitigate double taxation. Under Double Tax

Agreements, residents of outside nations are taxed at the decreased rate, or are

exempt from American tax on various income items they get from means in USA.

These reduced rates and exemptions vary amongst nations and particular income

related items (Olivier, Jara, and Rodriguez 2017, 369-392).

USA made double tax agreements with various countries (Refer Appendix). Under

the double tax agreements, American residents are taxed at the decreased rate, or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

are exempt from the international tax, on some income related items they get from

mean in international nations. Most tax treaties cover what is known as the saving

clause that stops the citizens and residents of USA from utilising the DTA provisions

to ignore tax of USA income sources. Various individual American states tax income

that is sourced in the states. For that reason, it is required to consult the state tax

authorities from that individual derive income to search whether the state taxes levy

to any income. Certain income states do not honour the tax treaties provisions

(Richard and Zolt 2015, 323-335).

Function and importance Double Tax Agreements (DTAs)

The main function of Double Taxation Agreements is to eradicate double tax in a

matter of cross-nationwide income flow. The more significant characteristics of

double tax avoidance agreements is that they render final principles in comparison of

domestic tax laws in relation to tax of foreign incomes. These agreements are very

significant because these agreements can cover the variety of tax such as VAT,

income tax, inheritance tax, or other tax (Nicholas et. al, 2018).

Furthermore, double tax avoidance agreements are very important because avoid

double tax by considering particular tax law of 2 nations. Besides, double tax

avoidance agreements as foreign tax treaties frequently render taxation data

exchange. These taxation exchange data lower the managerial cost of tax. Another

benefit is that there are legal certainties in double tax avoidance agreements, as

there are particular rules for taxation global incomes. It motivates international

investment to establishing nations where are tax certainties. Moreover, these

agreements also incorporate anti-abusive provisions to make sure that the

advantages of these agreements are attained by the real residents of 2 nations. With

these agreements, investor needs not depend on conflicting country tax rule; rather

tax of foreign income covers under the double taxation agreement rules

(Hermione 2018).

In addition, USA makes its own rules on who are the residents for the purpose of

taxation; someone can be subject to a claim by 2 states on the incomes. There are

certain matters, where one state would provide the credit for tax paid to different

state, however not all time. Therefore, USA has a comprehensive treaty network

(Rifat, et.al, 2015, 1230-1247).

Ranking of American tax system regarding simplicity, equity, certainty and

efficiency

There are various people who want to have the tax system, which is simple to

understand. In USA, campaigner for the more basic tax code frequently campaign for

the flat tax where the flat percentage will be charged on income. With American tax

system, millions are spent each year for filing tax (Ciaran 2017).

Further, the campaigners also point to the equity of tax system. It will not be more

just or reasonable if everybody paid similar percentage. American tax system allows

are exempt from the international tax, on some income related items they get from

mean in international nations. Most tax treaties cover what is known as the saving

clause that stops the citizens and residents of USA from utilising the DTA provisions

to ignore tax of USA income sources. Various individual American states tax income

that is sourced in the states. For that reason, it is required to consult the state tax

authorities from that individual derive income to search whether the state taxes levy

to any income. Certain income states do not honour the tax treaties provisions

(Richard and Zolt 2015, 323-335).

Function and importance Double Tax Agreements (DTAs)

The main function of Double Taxation Agreements is to eradicate double tax in a

matter of cross-nationwide income flow. The more significant characteristics of

double tax avoidance agreements is that they render final principles in comparison of

domestic tax laws in relation to tax of foreign incomes. These agreements are very

significant because these agreements can cover the variety of tax such as VAT,

income tax, inheritance tax, or other tax (Nicholas et. al, 2018).

Furthermore, double tax avoidance agreements are very important because avoid

double tax by considering particular tax law of 2 nations. Besides, double tax

avoidance agreements as foreign tax treaties frequently render taxation data

exchange. These taxation exchange data lower the managerial cost of tax. Another

benefit is that there are legal certainties in double tax avoidance agreements, as

there are particular rules for taxation global incomes. It motivates international

investment to establishing nations where are tax certainties. Moreover, these

agreements also incorporate anti-abusive provisions to make sure that the

advantages of these agreements are attained by the real residents of 2 nations. With

these agreements, investor needs not depend on conflicting country tax rule; rather

tax of foreign income covers under the double taxation agreement rules

(Hermione 2018).

In addition, USA makes its own rules on who are the residents for the purpose of

taxation; someone can be subject to a claim by 2 states on the incomes. There are

certain matters, where one state would provide the credit for tax paid to different

state, however not all time. Therefore, USA has a comprehensive treaty network

(Rifat, et.al, 2015, 1230-1247).

Ranking of American tax system regarding simplicity, equity, certainty and

efficiency

There are various people who want to have the tax system, which is simple to

understand. In USA, campaigner for the more basic tax code frequently campaign for

the flat tax where the flat percentage will be charged on income. With American tax

system, millions are spent each year for filing tax (Ciaran 2017).

Further, the campaigners also point to the equity of tax system. It will not be more

just or reasonable if everybody paid similar percentage. American tax system allows

REPORT 8

paying tax according to the income. Furthermore, the American tax system clearly

specifies at what percentage tax is to be paid, and how an amount to be paid is to be

decided. Consequently, in America, the administrative costs as well as compliance

costs to collect the tax kept to the minimum for government as well as taxpayers. In

this way, American tax system is effective in terms of above discussed criteria

(Richard 2015, 181-205).

Conclusion

As per the above analysis, it can be concluded that Australia ranks amongst

the highest in Organization for Economic Cooperation and Development nation for a

percentage of complete tax revenues, which are taken from individual income tax.

From the above discussion, it is also found that Australian pay more taxes in

comparison of America. However, relative to other high taxes and low taxes nations

in the OCED, not by much. The actual differences are in how the revenues are

spent.

paying tax according to the income. Furthermore, the American tax system clearly

specifies at what percentage tax is to be paid, and how an amount to be paid is to be

decided. Consequently, in America, the administrative costs as well as compliance

costs to collect the tax kept to the minimum for government as well as taxpayers. In

this way, American tax system is effective in terms of above discussed criteria

(Richard 2015, 181-205).

Conclusion

As per the above analysis, it can be concluded that Australia ranks amongst

the highest in Organization for Economic Cooperation and Development nation for a

percentage of complete tax revenues, which are taken from individual income tax.

From the above discussion, it is also found that Australian pay more taxes in

comparison of America. However, relative to other high taxes and low taxes nations

in the OCED, not by much. The actual differences are in how the revenues are

spent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

References

Atun, Rifat, Luiz Odorico Monteiro De Andrade, Gisele Almeida, Daniel Cotlear,

Tania Dmytraczenko, Patricia Frenz, Patrícia Garcia et al. 2015. "Health-system

reform and universal health coverage in Latin America." The Lancet 385, no. 9974,

1230-1247.

Bargain, Olivier, H. Xavier Jara, and David Rodriguez. 2017. "Learning from your

neighbor: tax-benefit systems swaps in Latin America." The Journal of Economic

Inequality 15, no. 4, 369-392.

Barr, Nicholas, Bruce Chapman, Lorraine Dearden, and Susan Dynarski. 2018. "The

US college loans system: Lessons from Australia and England." Economics of

Education Review.

Bird, Richard M., and Eric M. Zolt. 2015. "Fiscal Contracting in Latin America." World

Development 67, 323-335.

Braithwaite, Valerie. 2017. Taxing democracy: Understanding tax avoidance and

evasion. Routledge.

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. 2015. "Measuring top

incomes using tax record data: A cautionary tale from Australia." The Journal of

Economic Inequality 13, no. 2.181-205.

Christians, Allison, Wolfgang Schoen, and Stephen E. Shay. 2018. Foreword:

International Tax Policy in a Disruptive Environment. Edward Elgar Publishing.

Findlay, Christopher, and Ross Garnaut. 2017. The political economy of

manufacturing protection: Experiences of ASEAN and Australia. Routledge.

Focanti, Diego, Mark Hallerberg, and Carlos Scartascini. 2016. "Tax reforms in Latin

America in an era of democracy." Latin American Research Review 51, no. 1, 132-

158.

Hashimzade, Nigar, and Yuliya Epifantseva. 2017. The Routledge Companion to Tax

Avoidance Research. Routledge.

Hickman, Kristin. 2018. "From capital gains to tax administration, and everything in

between: in honour of Professor Chris Evans." eJTR 16, 269.

Individual income tax rate’. The ATO. https://www.ato.gov.au/Rates/Individual-

income-tax-rates/

Kahrl, Andrew W. 2017. "Investing in distress: Tax delinquency and predatory tax

buying in urban America." Critical Sociology 43, no. 2,199-219.

Lustig, Nora, and Claudiney Pereira. 2016. "The Impact of the Tax System and

Social Spending in Income Redistribution and Poverty Reduction in Latin

America." Hacienda Pública Española 219,121.

References

Atun, Rifat, Luiz Odorico Monteiro De Andrade, Gisele Almeida, Daniel Cotlear,

Tania Dmytraczenko, Patricia Frenz, Patrícia Garcia et al. 2015. "Health-system

reform and universal health coverage in Latin America." The Lancet 385, no. 9974,

1230-1247.

Bargain, Olivier, H. Xavier Jara, and David Rodriguez. 2017. "Learning from your

neighbor: tax-benefit systems swaps in Latin America." The Journal of Economic

Inequality 15, no. 4, 369-392.

Barr, Nicholas, Bruce Chapman, Lorraine Dearden, and Susan Dynarski. 2018. "The

US college loans system: Lessons from Australia and England." Economics of

Education Review.

Bird, Richard M., and Eric M. Zolt. 2015. "Fiscal Contracting in Latin America." World

Development 67, 323-335.

Braithwaite, Valerie. 2017. Taxing democracy: Understanding tax avoidance and

evasion. Routledge.

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. 2015. "Measuring top

incomes using tax record data: A cautionary tale from Australia." The Journal of

Economic Inequality 13, no. 2.181-205.

Christians, Allison, Wolfgang Schoen, and Stephen E. Shay. 2018. Foreword:

International Tax Policy in a Disruptive Environment. Edward Elgar Publishing.

Findlay, Christopher, and Ross Garnaut. 2017. The political economy of

manufacturing protection: Experiences of ASEAN and Australia. Routledge.

Focanti, Diego, Mark Hallerberg, and Carlos Scartascini. 2016. "Tax reforms in Latin

America in an era of democracy." Latin American Research Review 51, no. 1, 132-

158.

Hashimzade, Nigar, and Yuliya Epifantseva. 2017. The Routledge Companion to Tax

Avoidance Research. Routledge.

Hickman, Kristin. 2018. "From capital gains to tax administration, and everything in

between: in honour of Professor Chris Evans." eJTR 16, 269.

Individual income tax rate’. The ATO. https://www.ato.gov.au/Rates/Individual-

income-tax-rates/

Kahrl, Andrew W. 2017. "Investing in distress: Tax delinquency and predatory tax

buying in urban America." Critical Sociology 43, no. 2,199-219.

Lustig, Nora, and Claudiney Pereira. 2016. "The Impact of the Tax System and

Social Spending in Income Redistribution and Poverty Reduction in Latin

America." Hacienda Pública Española 219,121.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

Mishel, Lawrence, Jared Bernstein, and John Schmitt. 2016. The state of working

America: 1992-93. Routledge.

Mishel, Lawrence, Jared Bernstein, and John Schmitt. 2016. The state of working

America: 1996-97. Routledge.

O'faircheallaigh, Ciaran. 2017. Mining and development: foreign-financed mines in

Australia, Ireland, Papua New Guinea and Zambia. Routledge.

Parker, Hermione. 2018. Instead of the Dole: an enquiry into integration of the tax

and benefit systems. Routledge.

Tanzi, Vito. 2018. "Tax reform in Latin America: a long-term assessment: Factors

that. Shape the Demand and Supply of Taxes." In The Ecology of Tax Systems.

Edward Elgar Publishing.

Thornton, Joshua. 2019. American Automation Tax Policy. Routledge.

Yates, Judith. 2016. "Why does Australia have an affordable housing problem and

what can be done about it?." Australian Economic Review 49, no. 3. 328-339.

Appendix

Mishel, Lawrence, Jared Bernstein, and John Schmitt. 2016. The state of working

America: 1992-93. Routledge.

Mishel, Lawrence, Jared Bernstein, and John Schmitt. 2016. The state of working

America: 1996-97. Routledge.

O'faircheallaigh, Ciaran. 2017. Mining and development: foreign-financed mines in

Australia, Ireland, Papua New Guinea and Zambia. Routledge.

Parker, Hermione. 2018. Instead of the Dole: an enquiry into integration of the tax

and benefit systems. Routledge.

Tanzi, Vito. 2018. "Tax reform in Latin America: a long-term assessment: Factors

that. Shape the Demand and Supply of Taxes." In The Ecology of Tax Systems.

Edward Elgar Publishing.

Thornton, Joshua. 2019. American Automation Tax Policy. Routledge.

Yates, Judith. 2016. "Why does Australia have an affordable housing problem and

what can be done about it?." Australian Economic Review 49, no. 3. 328-339.

Appendix

REPORT 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.