International Tax Fundamentals: Residency, Income & Superannuation

VerifiedAdded on 2020/07/23

|9

|1614

|31

Report

AI Summary

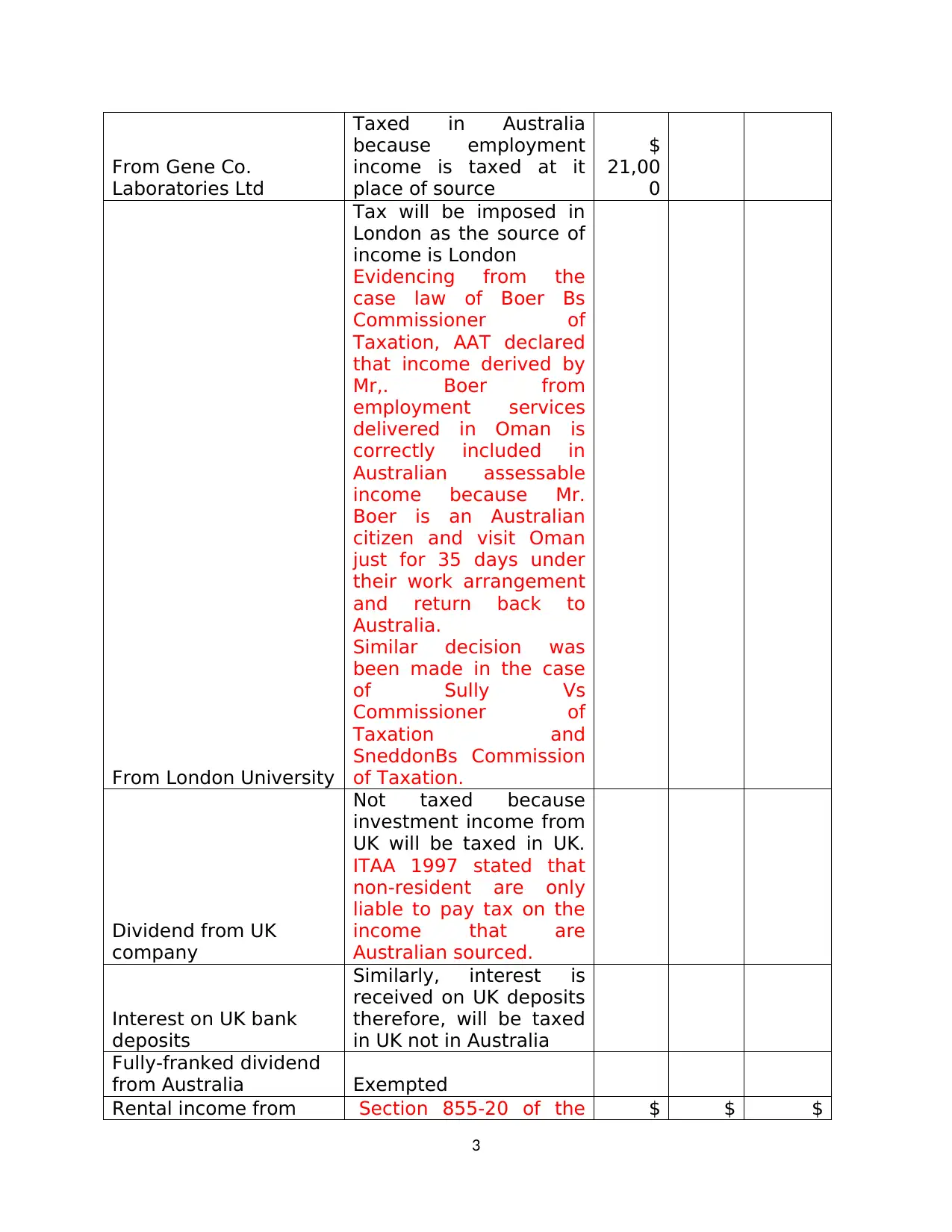

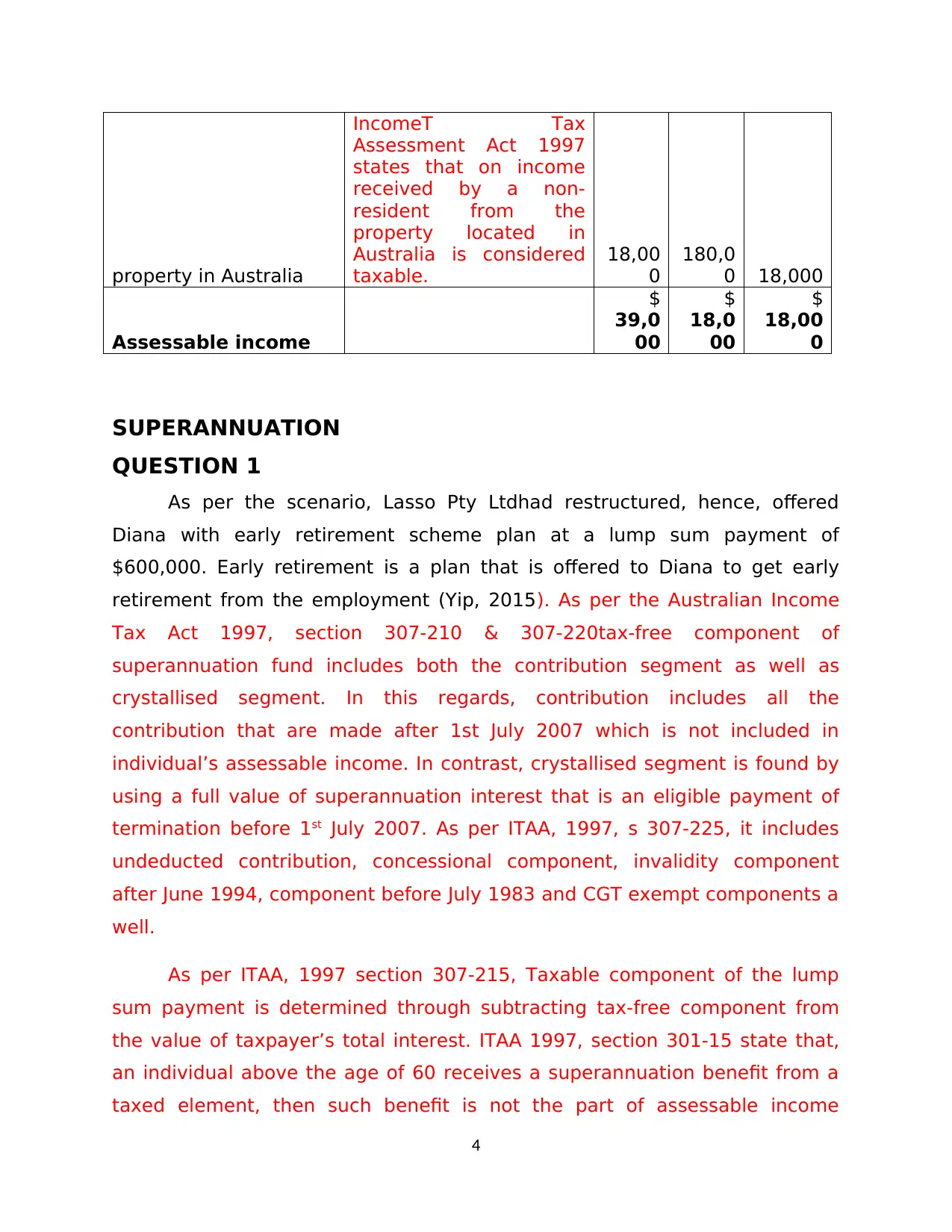

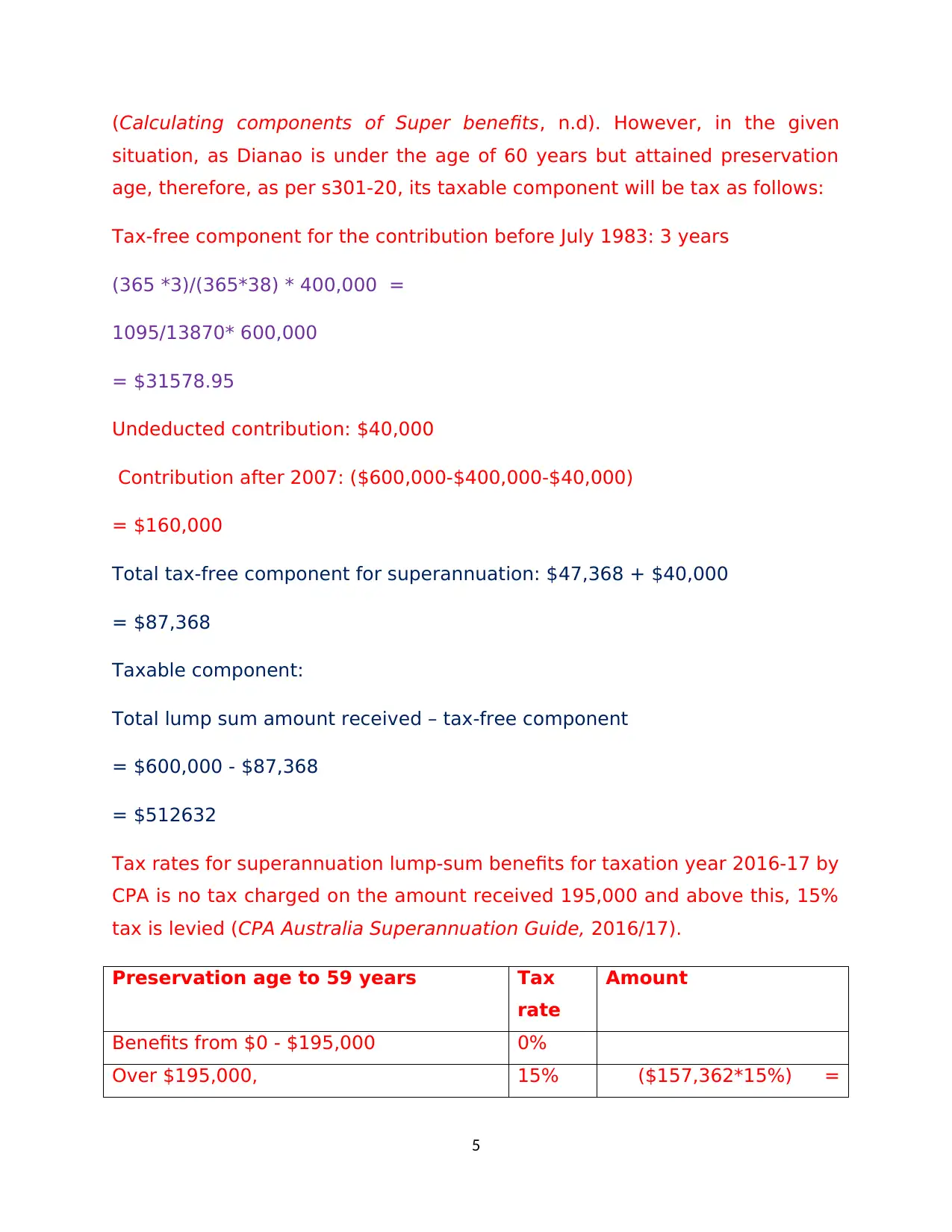

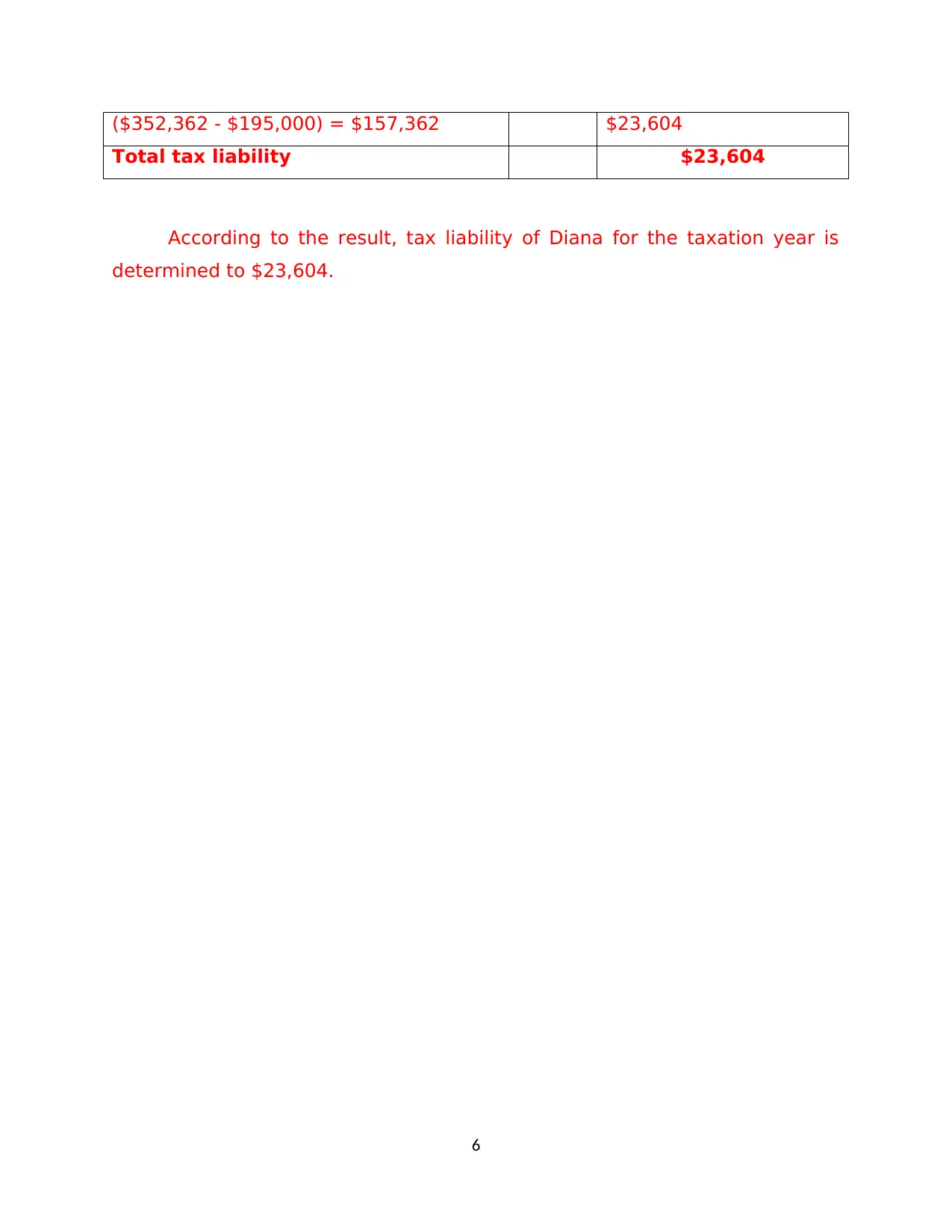

This report provides a comprehensive analysis of international tax fundamentals. It begins by examining the residential status of Dr. Jones, applying the Australian Income Tax Act's residency tests, including the resides test, domicile test, 183-day test, and superannuation test, to determine her non-resident status. The report then calculates Dr. Jones's assessable income for the years 2015/16, 2016/17, and 2017/18, considering employment income, dividends, and rental income, and determining which are taxable in Australia. Finally, the report addresses a superannuation question, calculating the tax liability of Diana, who received a lump-sum payment from an early retirement scheme. It details the tax-free and taxable components of the payment, and the applicable tax rates. The report references relevant Australian tax legislation, rulings, and case laws throughout its analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.