Microeconomics Assignment: Intertemporal Choice and Expected Utility

VerifiedAdded on 2020/06/05

|8

|1224

|50

Homework Assignment

AI Summary

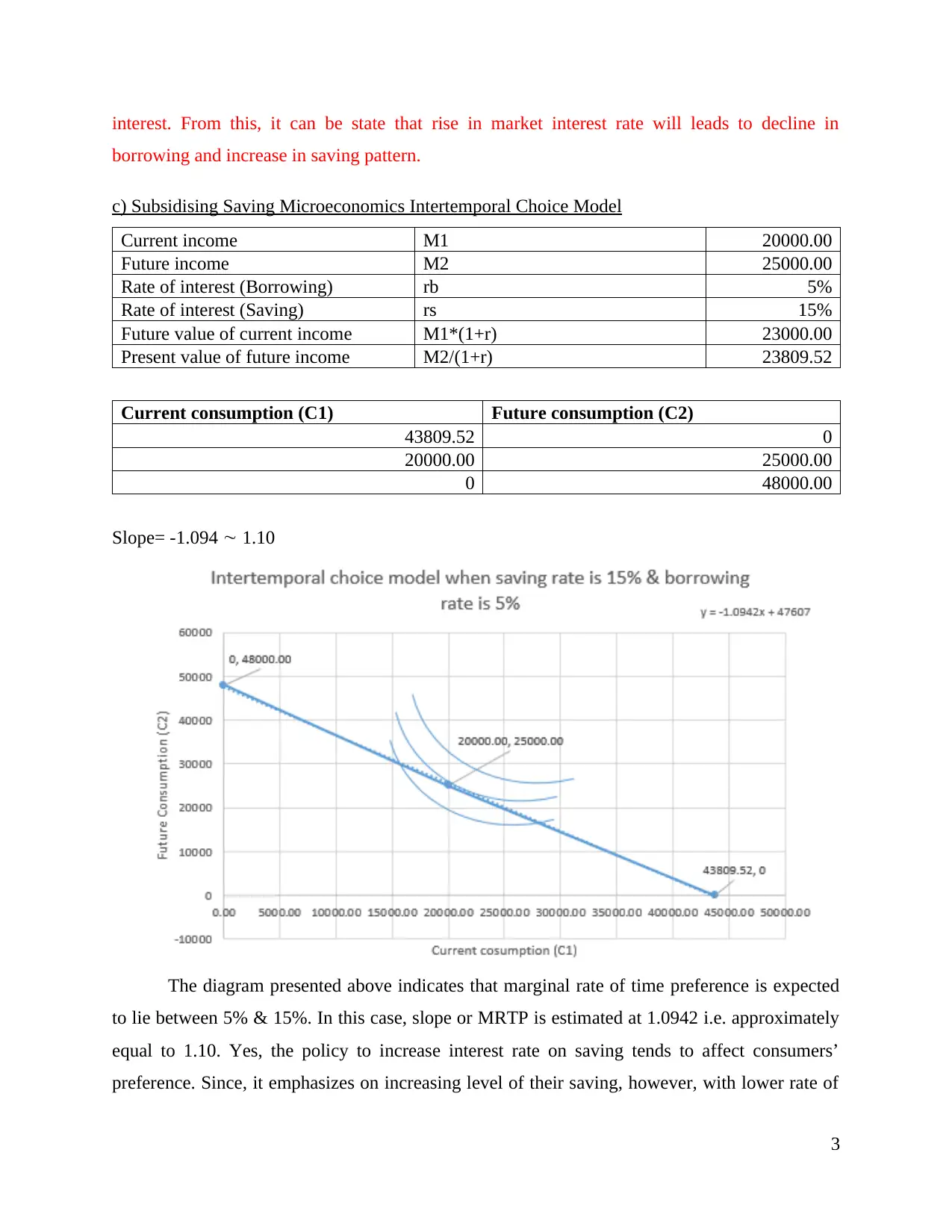

This assignment solution delves into the microeconomic concept of intertemporal choice, examining how individuals make consumption and saving decisions across different time periods. The solution analyzes the impact of interest rate changes on borrowing and saving behavior, illustrating these effects with diagrams and calculations. It further explores the expected utility framework, using a house insurance example to demonstrate how individuals make decisions under uncertainty based on their risk aversion. The assignment also discusses factors beyond the intertemporal choice model, such as population structure and social security, that influence household saving patterns. References to relevant academic literature are included to support the analysis.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.