ACCM4300 - Financial Accounting: Consolidation of Foreign Subsidiaries

VerifiedAdded on 2023/06/07

|9

|1323

|314

Report

AI Summary

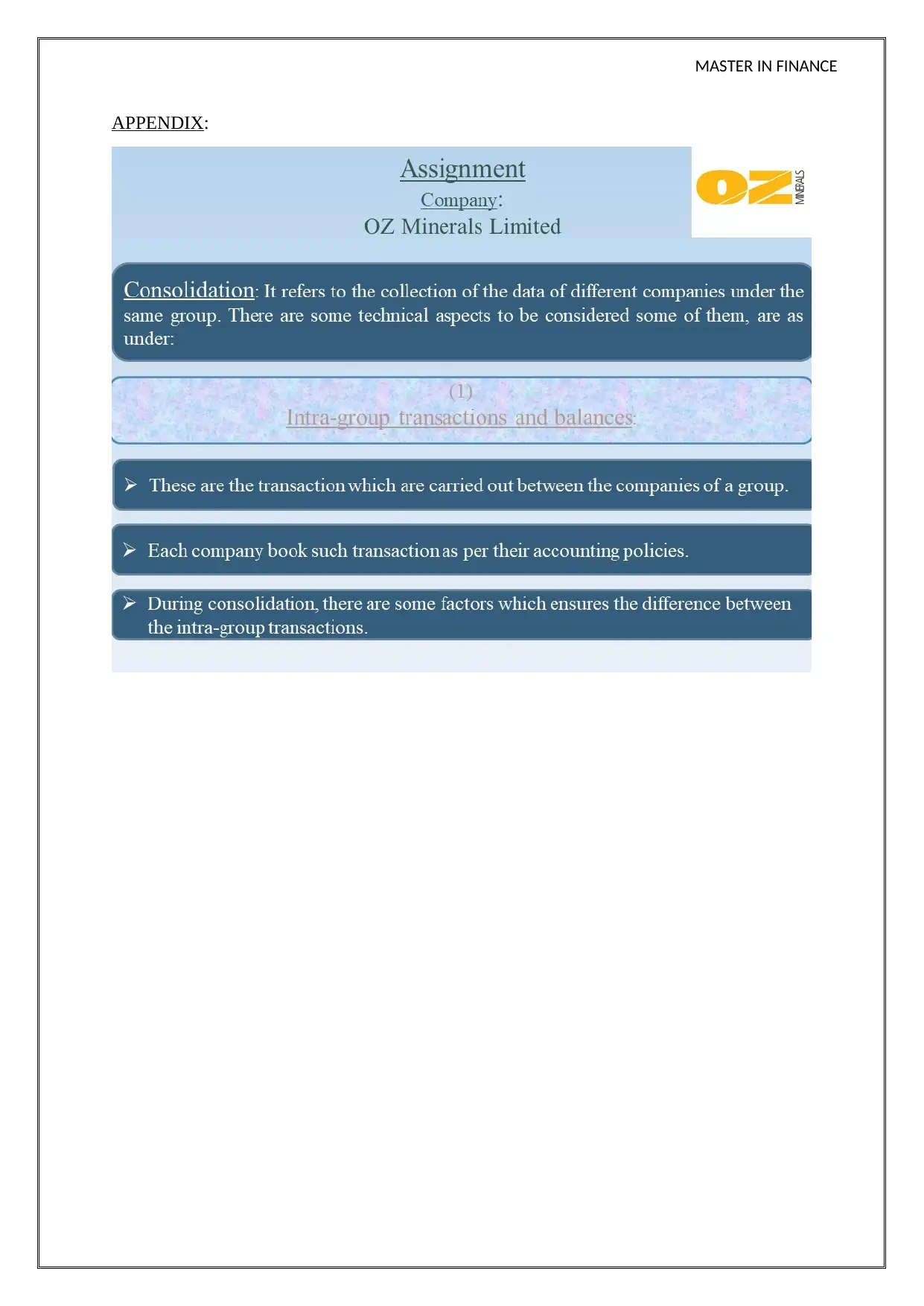

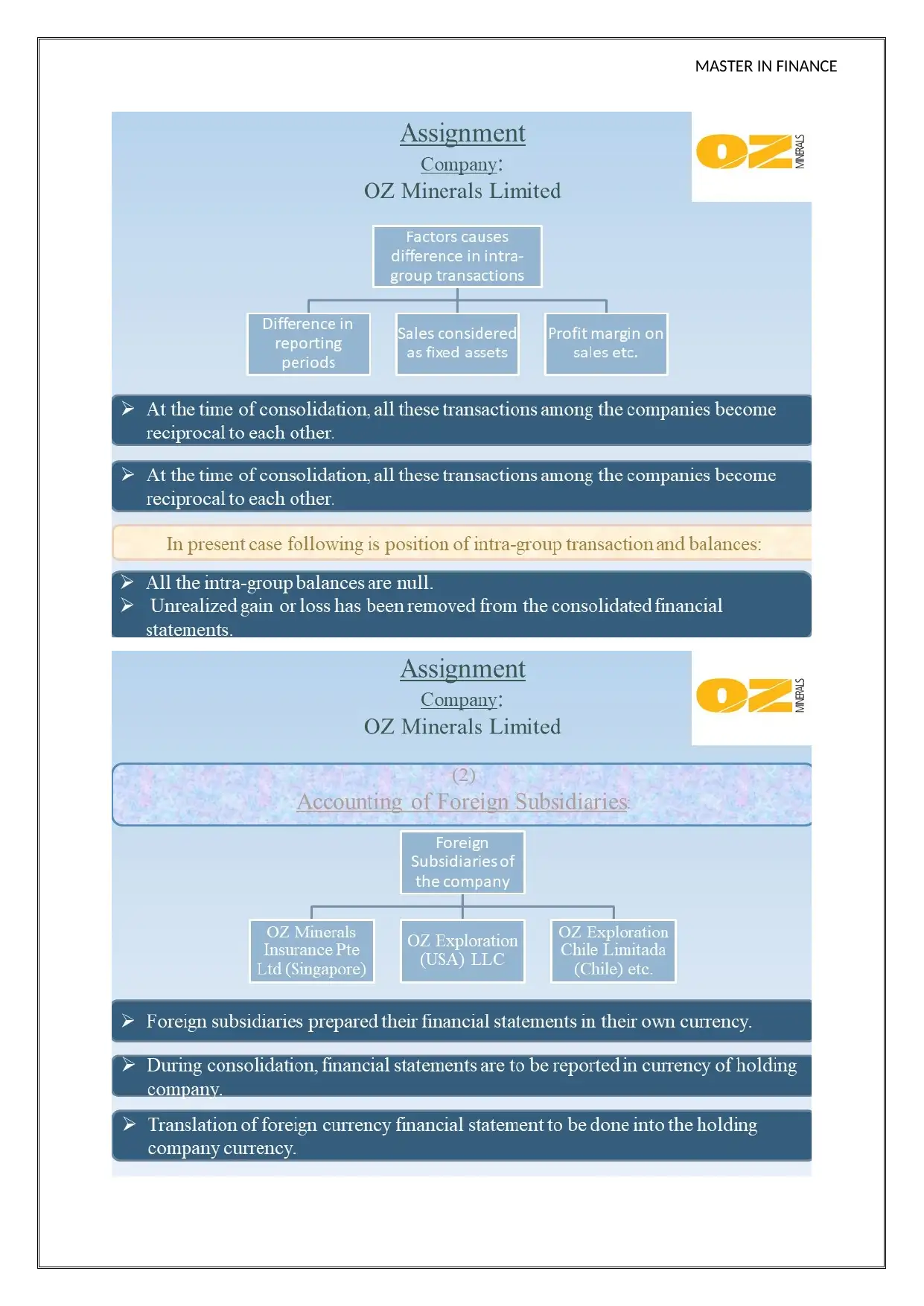

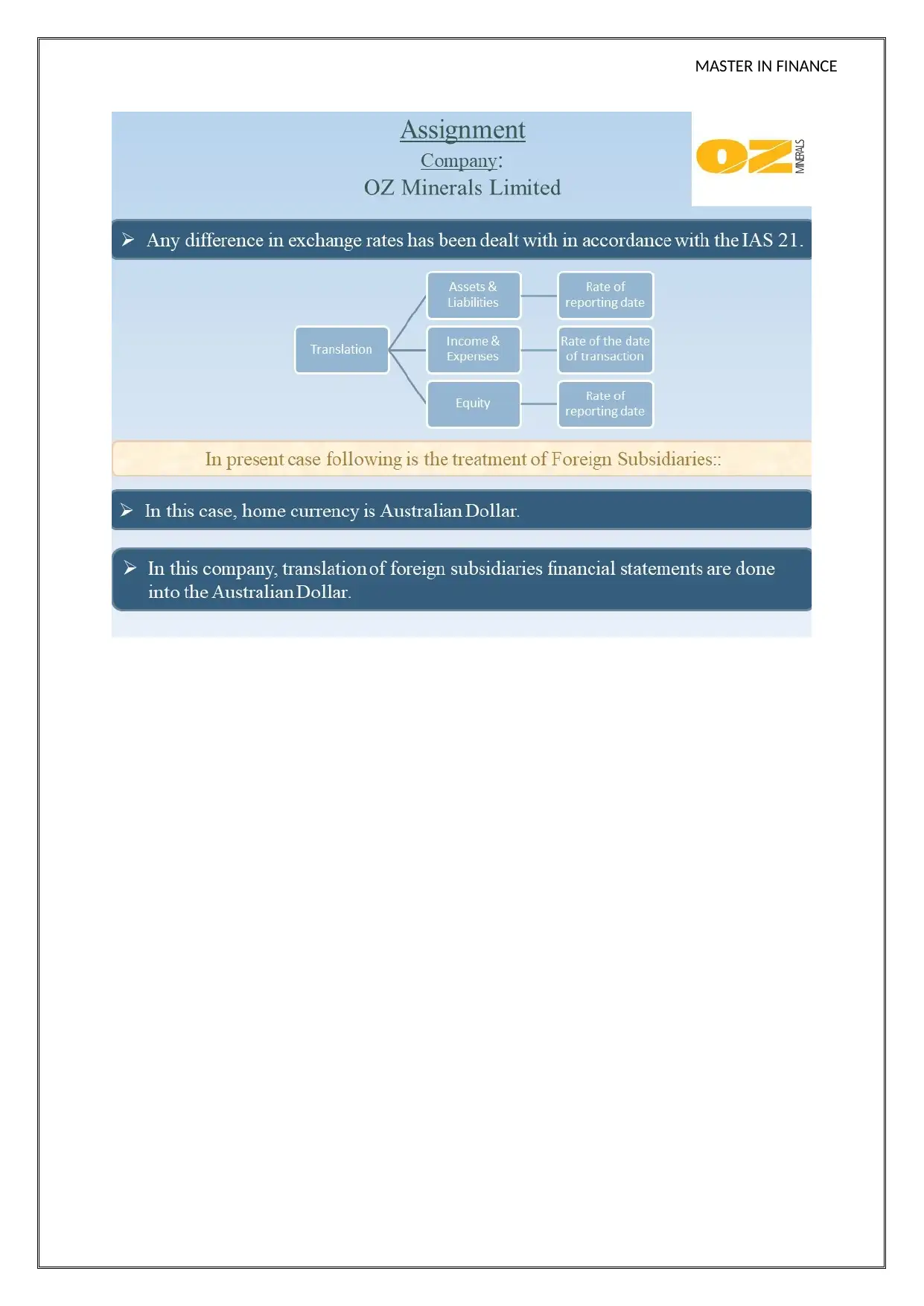

This report discusses the technical aspects of consolidating financial statements, focusing on intra-group transactions and the accounting of foreign subsidiaries, particularly in the context of OZ Minerals. It highlights the importance of properly accounting for intra-group transactions to avoid overstatement or understatement of financial reports, emphasizing the need to eliminate unrealized gains or losses. The report also addresses the translation of foreign subsidiaries' financial statements into the reporting currency, adhering to IAS 21 guidelines for exchange rate conversions and recognizing gains or losses from exchange rate changes. The presentation section summarizes the key topics discussed, including intra-group transactions, balances, and the accounting of foreign subsidiaries, with a conclusion that emphasizes the need for careful treatment of these elements for fair financial statement presentation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.