King's Own Institute ECO100 Introduction to Economics Assignment

VerifiedAdded on 2022/12/23

|13

|3088

|83

Homework Assignment

AI Summary

This document presents a comprehensive solution to an ECO100 Introduction to Economics assignment. The assignment addresses several key economic concepts, beginning with the calculation of equilibrium price and quantity using supply and demand equations, along with graphical representations. It then explores the concepts of consumer and producer surplus, and price elasticity of demand and supply, providing detailed calculations and interpretations. The assignment further delves into the production possibility frontier (PPF), analyzing China's PPF for clothing and rice, including explanations for its concave shape and the assumptions underlying its construction. The solution also discusses production and allocative efficiency within the PPF framework, along with the impact of technological advancements on the PPF. Finally, the assignment examines the Australian espresso coffee market, determining whether firms are price takers or makers, and explaining the market's growth using demand and supply models, including factors like quality, changing culture, and international competition.

Running head: ECO 100 INTRODUCTION TO ECONOMICS

ECO 100 Introduction to Economics

Name

University

ECO 100 Introduction to Economics

Name

University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECO 100 INTRODUCTION TO ECONOMICS 2

Question One

a) Equilibrium quantity

The quantity demand and quantity supply are equal at equilibrium.

P = 200 – 0.4QD (1)

P = 20 + 0.5QS (2)

Demand = 200 - 0.4Q

Supply = 20 + 0.5Q

200 - 0.4Q = 20 + 0.5Q

200 – 20 = 0.5Q + 0.4Q

180 = 0.9Q

Quantity (Q) = 180/ 0.9

= 200 Kilograms

Since, Supply = Demand at equilibrium;

The price equation is P = 200 – 0.4Q

P = 200 – 0.4(200)

P= 200-80

P= 120

Therefore, the Equilibrium price = $120.

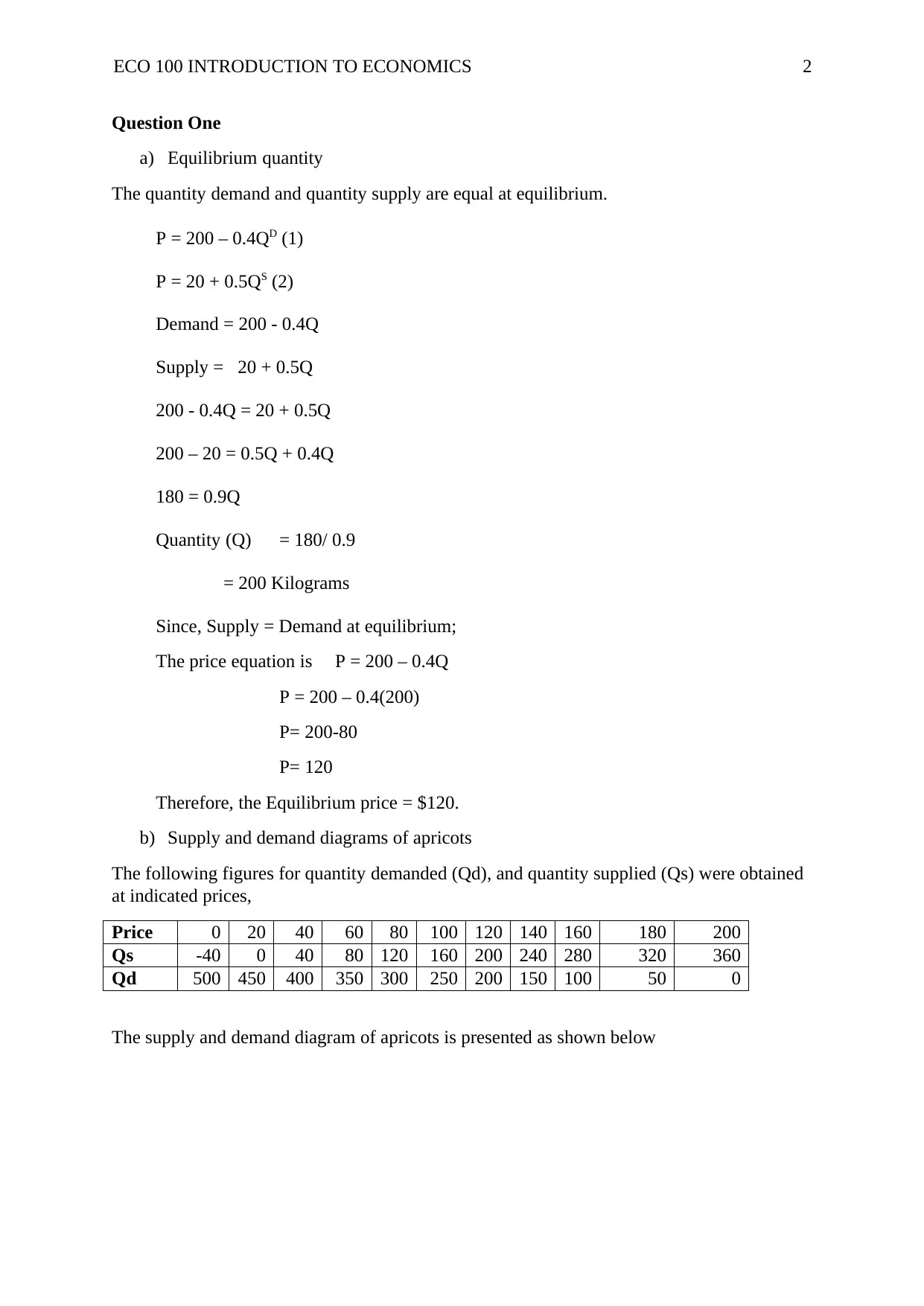

b) Supply and demand diagrams of apricots

The following figures for quantity demanded (Qd), and quantity supplied (Qs) were obtained

at indicated prices,

Price 0 20 40 60 80 100 120 140 160 180 200

Qs -40 0 40 80 120 160 200 240 280 320 360

Qd 500 450 400 350 300 250 200 150 100 50 0

The supply and demand diagram of apricots is presented as shown below

Question One

a) Equilibrium quantity

The quantity demand and quantity supply are equal at equilibrium.

P = 200 – 0.4QD (1)

P = 20 + 0.5QS (2)

Demand = 200 - 0.4Q

Supply = 20 + 0.5Q

200 - 0.4Q = 20 + 0.5Q

200 – 20 = 0.5Q + 0.4Q

180 = 0.9Q

Quantity (Q) = 180/ 0.9

= 200 Kilograms

Since, Supply = Demand at equilibrium;

The price equation is P = 200 – 0.4Q

P = 200 – 0.4(200)

P= 200-80

P= 120

Therefore, the Equilibrium price = $120.

b) Supply and demand diagrams of apricots

The following figures for quantity demanded (Qd), and quantity supplied (Qs) were obtained

at indicated prices,

Price 0 20 40 60 80 100 120 140 160 180 200

Qs -40 0 40 80 120 160 200 240 280 320 360

Qd 500 450 400 350 300 250 200 150 100 50 0

The supply and demand diagram of apricots is presented as shown below

ECO 100 INTRODUCTION TO ECONOMICS 3

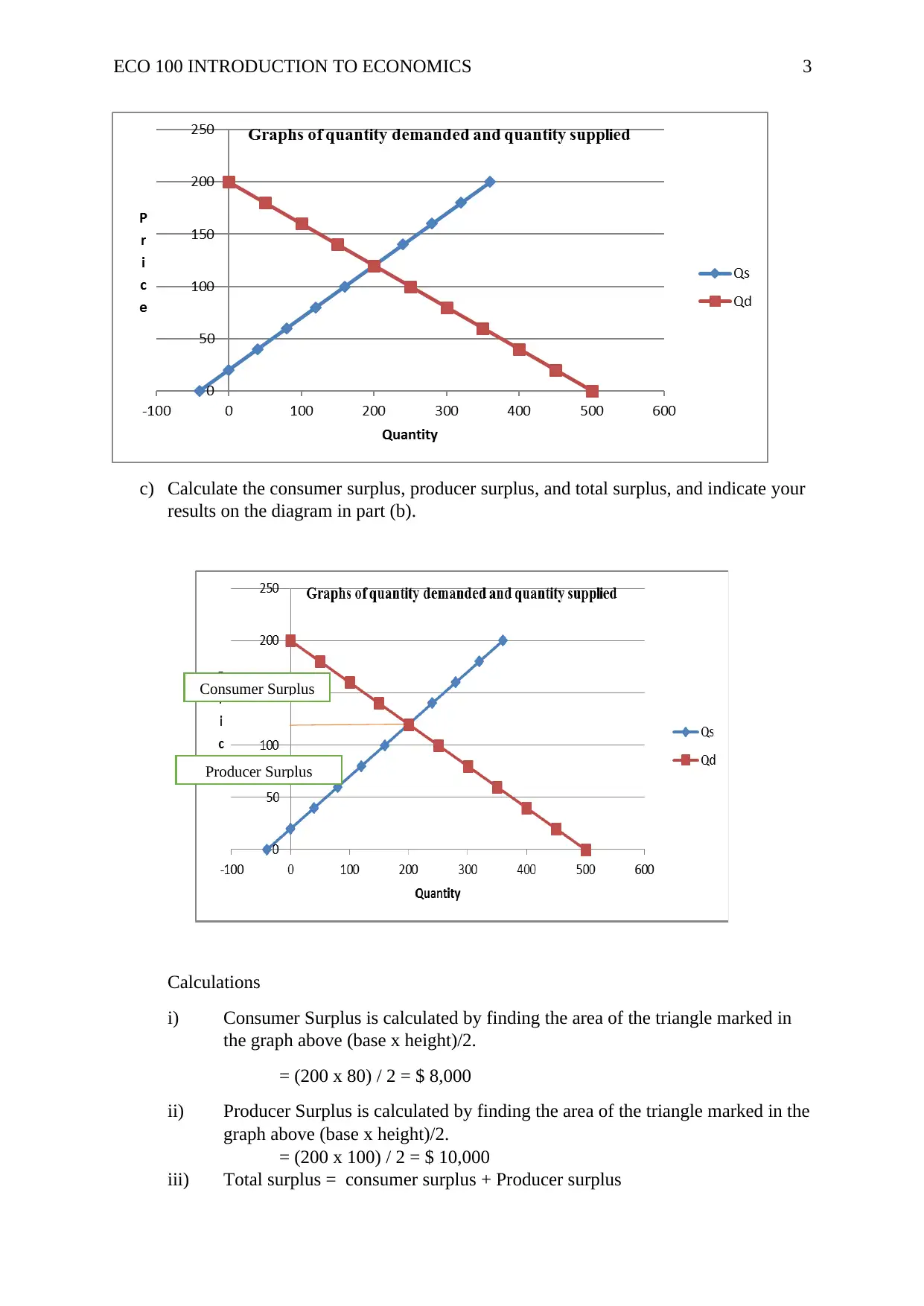

c) Calculate the consumer surplus, producer surplus, and total surplus, and indicate your

results on the diagram in part (b).

Calculations

i) Consumer Surplus is calculated by finding the area of the triangle marked in

the graph above (base x height)/2.

= (200 x 80) / 2 = $ 8,000

ii) Producer Surplus is calculated by finding the area of the triangle marked in the

graph above (base x height)/2.

= (200 x 100) / 2 = $ 10,000

iii) Total surplus = consumer surplus + Producer surplus

Consumer Surplus

Producer Surplus

c) Calculate the consumer surplus, producer surplus, and total surplus, and indicate your

results on the diagram in part (b).

Calculations

i) Consumer Surplus is calculated by finding the area of the triangle marked in

the graph above (base x height)/2.

= (200 x 80) / 2 = $ 8,000

ii) Producer Surplus is calculated by finding the area of the triangle marked in the

graph above (base x height)/2.

= (200 x 100) / 2 = $ 10,000

iii) Total surplus = consumer surplus + Producer surplus

Consumer Surplus

Producer Surplus

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECO 100 INTRODUCTION TO ECONOMICS 4

= $ 8,000 + $ 10,000

= $ 18,000.

d) The price elasticity of demand at the equilibrium price and quantity

Equilibrium quantity (Q) = 200.

Equilibrium Price (P) = $120.

Therefore equilibrium point (Q, P) = (200, 120)

Price elasticity of Demand = change in price/ change in quantity.

Initial point (Q, P) = (200,120)

New point (Q, P) = (150, 140)

=

= 0.1667/ -0.25

Price elasticity of demand = - 0.668

If the price increase by 1%, the quantity demanded will decrease by 0.668%.

Point elasticity of Supply = % change in price% change in quantity

Initial point (Q, P) = (200,120)

New point (Q, P) = (240, 140)

=

= 0.1667 / 0.2

= 0. 8335

If the price increase by 1%, the quantity supplied will increase by 0.8335%.

e) i) Increase of price by 10%

A rise in price by 1% leads to a decrease in quantity demanded by 0.668%. Therefore, an

increase in price by 10% leads to a reduction of quantity demanded by 6.68%.

At equilibrium, Q= 200 and P = 120

10% increase in price = = 132

6.68% decrease in quantity demanded = = 186.8 or 187

= $ 8,000 + $ 10,000

= $ 18,000.

d) The price elasticity of demand at the equilibrium price and quantity

Equilibrium quantity (Q) = 200.

Equilibrium Price (P) = $120.

Therefore equilibrium point (Q, P) = (200, 120)

Price elasticity of Demand = change in price/ change in quantity.

Initial point (Q, P) = (200,120)

New point (Q, P) = (150, 140)

=

= 0.1667/ -0.25

Price elasticity of demand = - 0.668

If the price increase by 1%, the quantity demanded will decrease by 0.668%.

Point elasticity of Supply = % change in price% change in quantity

Initial point (Q, P) = (200,120)

New point (Q, P) = (240, 140)

=

= 0.1667 / 0.2

= 0. 8335

If the price increase by 1%, the quantity supplied will increase by 0.8335%.

e) i) Increase of price by 10%

A rise in price by 1% leads to a decrease in quantity demanded by 0.668%. Therefore, an

increase in price by 10% leads to a reduction of quantity demanded by 6.68%.

At equilibrium, Q= 200 and P = 120

10% increase in price = = 132

6.68% decrease in quantity demanded = = 186.8 or 187

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECO 100 INTRODUCTION TO ECONOMICS 5

Therefore, at a new price of $ 132, the quantity demanded will be 187 apricots.

ii) Effect on the total revenue (TR)

Revenue is defined as the total good sold multiplied by the price of one unit.

At equilibrium point (Q, P = 200,120), Total revenue = 200 x 120 = $24,200

At the new point (Q, P = 187, 132), Total revenue = 187 x 132 = 24,684.

Therefore, a decrease in price by 10% will lead to an increase in total revenue by $484

($24,684 - $ 24,200).

Question Two

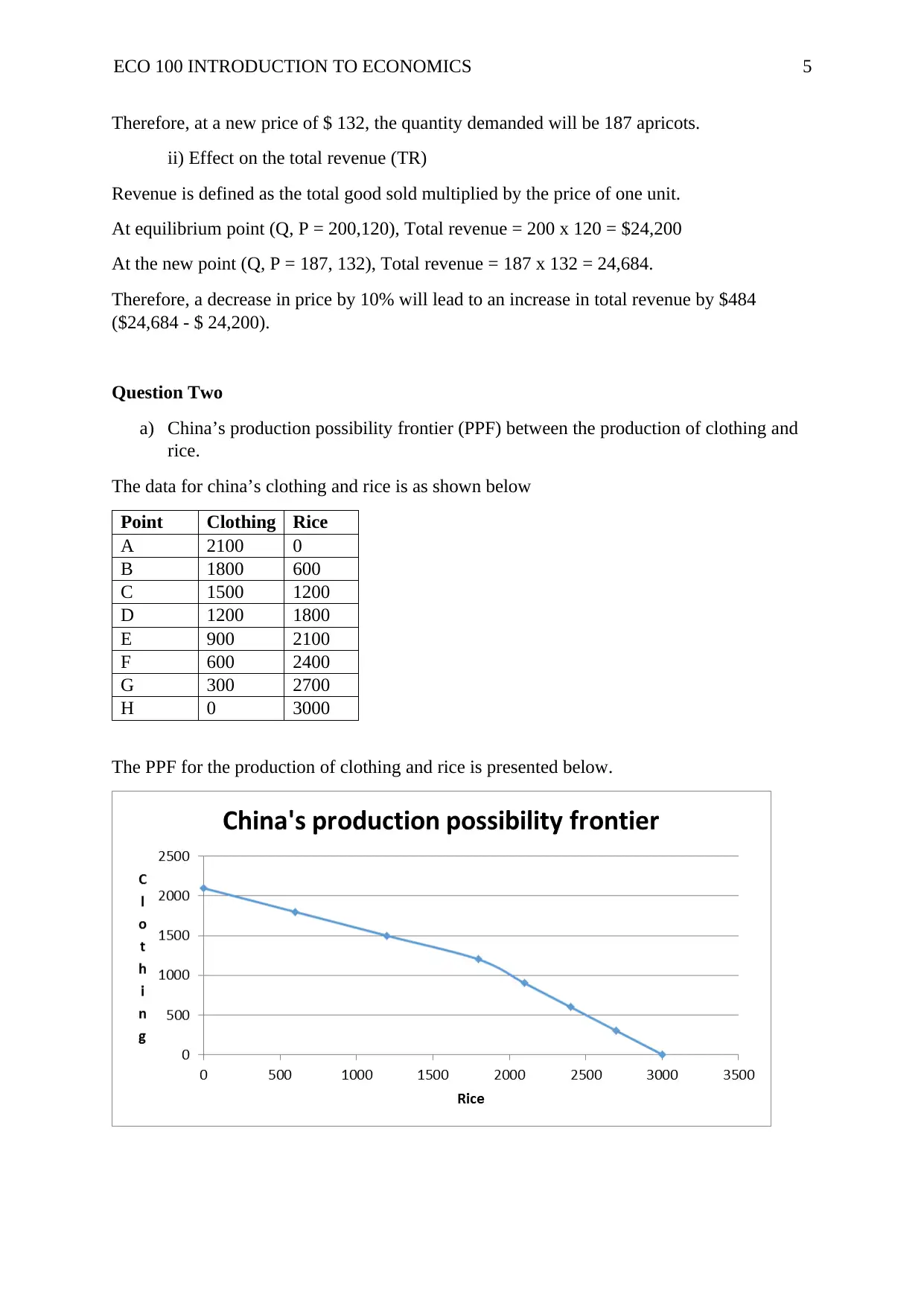

a) China’s production possibility frontier (PPF) between the production of clothing and

rice.

The data for china’s clothing and rice is as shown below

Point Clothing Rice

A 2100 0

B 1800 600

C 1500 1200

D 1200 1800

E 900 2100

F 600 2400

G 300 2700

H 0 3000

The PPF for the production of clothing and rice is presented below.

Therefore, at a new price of $ 132, the quantity demanded will be 187 apricots.

ii) Effect on the total revenue (TR)

Revenue is defined as the total good sold multiplied by the price of one unit.

At equilibrium point (Q, P = 200,120), Total revenue = 200 x 120 = $24,200

At the new point (Q, P = 187, 132), Total revenue = 187 x 132 = 24,684.

Therefore, a decrease in price by 10% will lead to an increase in total revenue by $484

($24,684 - $ 24,200).

Question Two

a) China’s production possibility frontier (PPF) between the production of clothing and

rice.

The data for china’s clothing and rice is as shown below

Point Clothing Rice

A 2100 0

B 1800 600

C 1500 1200

D 1200 1800

E 900 2100

F 600 2400

G 300 2700

H 0 3000

The PPF for the production of clothing and rice is presented below.

ECO 100 INTRODUCTION TO ECONOMICS 6

b) Why is the PPF curve concave?

China’s economy is faced with limited resources for production. The economy cannot

produce clothing and rice products concurrently. In other words, the production of rice must

be forgone to produce the maximum quantity of clothing and vice versa. Likewise, for China

to produce more rice it has to give up on the production of a given quantity of clothing.

Therefore, the PPF curve is concave because of the increasing marginal/ opportunity cost

associated with producing more of the clothing while reducing rice or providing more of rice

and reducing the production of clothing (Banerjee & Warrier, 2018).

c) Assumptions for constructing a PPF

There are four critical assumptions for the construction of a PPF curve. First, it is

assumed that the available resources are only used to produce one or both goods. Second, the

quantity of available resources remains the same. Third, applied production techniques and

technology remain the same. And fourth, the available resources for the production are used

efficiently (Sloman, Norris, & Garett, 2014).

d) Production Efficiency and Allocative Efficiency

In a democratic economy, decisions making process involves different stakeholders

who are guided by several factors. Some of the factors which help stakeholder in making

production decisions are production cost, availability of resources, time, and market

demands. Production decisions are based on the need to maximize the output from the

available inputs (resources). Maximization of output is based on the concept of efficiency

which is explained as a lack of waste from the production process. There are two types of

efficiency under production possibilities frontier (PPF), that is, the allocative efficiency and

productive efficiency (Jones, 2014).

b) Why is the PPF curve concave?

China’s economy is faced with limited resources for production. The economy cannot

produce clothing and rice products concurrently. In other words, the production of rice must

be forgone to produce the maximum quantity of clothing and vice versa. Likewise, for China

to produce more rice it has to give up on the production of a given quantity of clothing.

Therefore, the PPF curve is concave because of the increasing marginal/ opportunity cost

associated with producing more of the clothing while reducing rice or providing more of rice

and reducing the production of clothing (Banerjee & Warrier, 2018).

c) Assumptions for constructing a PPF

There are four critical assumptions for the construction of a PPF curve. First, it is

assumed that the available resources are only used to produce one or both goods. Second, the

quantity of available resources remains the same. Third, applied production techniques and

technology remain the same. And fourth, the available resources for the production are used

efficiently (Sloman, Norris, & Garett, 2014).

d) Production Efficiency and Allocative Efficiency

In a democratic economy, decisions making process involves different stakeholders

who are guided by several factors. Some of the factors which help stakeholder in making

production decisions are production cost, availability of resources, time, and market

demands. Production decisions are based on the need to maximize the output from the

available inputs (resources). Maximization of output is based on the concept of efficiency

which is explained as a lack of waste from the production process. There are two types of

efficiency under production possibilities frontier (PPF), that is, the allocative efficiency and

productive efficiency (Jones, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECO 100 INTRODUCTION TO ECONOMICS 7

Economics explains production efficiency as the impossibility of producing more of

one item without reducing the quantity produced of another item using the available

resources. For instance, in China’s PPF, the economy can only use the available resources to

produce 1800 clothing and 600 rice at point B. In order to produce a quantity of 1200 rice, the

quantity of clothing must be reduced to 1500 items. Production efficiency for China’s PPF

can only be illustrated along the PPF curve. The production below or above the PPF curve is

considered to be production inefficiency because resources would be wasted. In other words,

China can only experience production efficiency by choosing a production combination

which falls along the PPF curve (Bishop, Parrott, Martie, & Miller, 2014).

On the other hand, allocative efficiency is explained as the production-based on the

consumers' desire. For example, a low-income society would prefer food over cars.

Therefore, producers will use the available resources to produce more food items and fewer

cars. Likewise, consider a society with both young and older population faced with the

making a choice between education and health. The producers will produce more educational

resources for the young population and health products for the older population. Allocative

efficiency is achieved at a given point along the PPF curve. For instance, China’s society

prefers 2100 clothing and 0 rice at point A and 900 clothing and 2100 rice at point E

(Krugman & Wells, 2015).

e) Suppose the adoption of a new technology for growing rice lowers the cost of

producing rice, allowing yields to increase by 100%. Show and explain the impact of

this technological change on the initial production possibility frontier in part (a).

Adoption of new technology would reduce the cost associated with the production of

rice because it leads to production efficiency. Subsequently, the initial yield would increase

Economics explains production efficiency as the impossibility of producing more of

one item without reducing the quantity produced of another item using the available

resources. For instance, in China’s PPF, the economy can only use the available resources to

produce 1800 clothing and 600 rice at point B. In order to produce a quantity of 1200 rice, the

quantity of clothing must be reduced to 1500 items. Production efficiency for China’s PPF

can only be illustrated along the PPF curve. The production below or above the PPF curve is

considered to be production inefficiency because resources would be wasted. In other words,

China can only experience production efficiency by choosing a production combination

which falls along the PPF curve (Bishop, Parrott, Martie, & Miller, 2014).

On the other hand, allocative efficiency is explained as the production-based on the

consumers' desire. For example, a low-income society would prefer food over cars.

Therefore, producers will use the available resources to produce more food items and fewer

cars. Likewise, consider a society with both young and older population faced with the

making a choice between education and health. The producers will produce more educational

resources for the young population and health products for the older population. Allocative

efficiency is achieved at a given point along the PPF curve. For instance, China’s society

prefers 2100 clothing and 0 rice at point A and 900 clothing and 2100 rice at point E

(Krugman & Wells, 2015).

e) Suppose the adoption of a new technology for growing rice lowers the cost of

producing rice, allowing yields to increase by 100%. Show and explain the impact of

this technological change on the initial production possibility frontier in part (a).

Adoption of new technology would reduce the cost associated with the production of

rice because it leads to production efficiency. Subsequently, the initial yield would increase

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECO 100 INTRODUCTION TO ECONOMICS 8

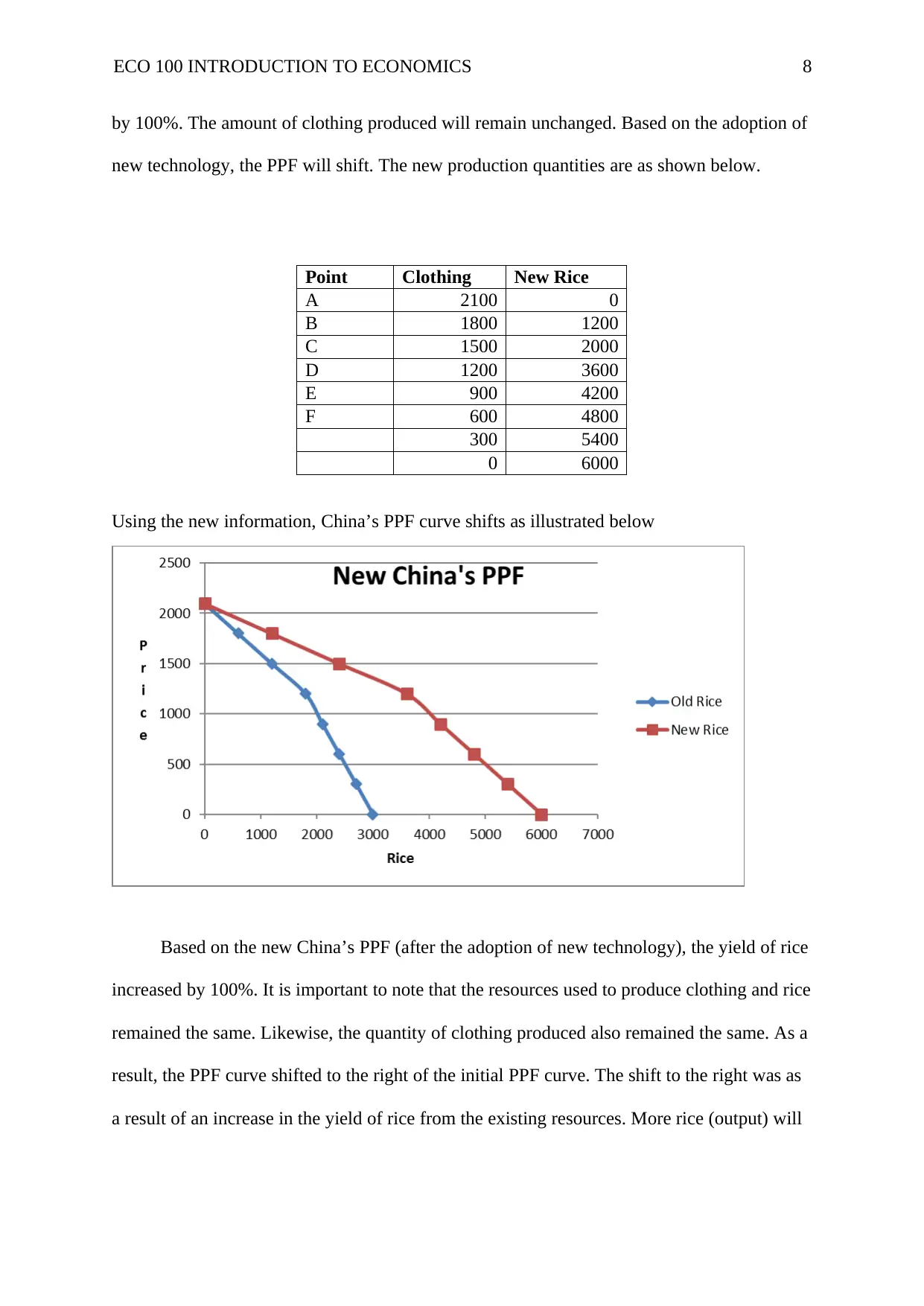

by 100%. The amount of clothing produced will remain unchanged. Based on the adoption of

new technology, the PPF will shift. The new production quantities are as shown below.

Point Clothing New Rice

A 2100 0

B 1800 1200

C 1500 2000

D 1200 3600

E 900 4200

F 600 4800

300 5400

0 6000

Using the new information, China’s PPF curve shifts as illustrated below

Based on the new China’s PPF (after the adoption of new technology), the yield of rice

increased by 100%. It is important to note that the resources used to produce clothing and rice

remained the same. Likewise, the quantity of clothing produced also remained the same. As a

result, the PPF curve shifted to the right of the initial PPF curve. The shift to the right was as

a result of an increase in the yield of rice from the existing resources. More rice (output) will

by 100%. The amount of clothing produced will remain unchanged. Based on the adoption of

new technology, the PPF will shift. The new production quantities are as shown below.

Point Clothing New Rice

A 2100 0

B 1800 1200

C 1500 2000

D 1200 3600

E 900 4200

F 600 4800

300 5400

0 6000

Using the new information, China’s PPF curve shifts as illustrated below

Based on the new China’s PPF (after the adoption of new technology), the yield of rice

increased by 100%. It is important to note that the resources used to produce clothing and rice

remained the same. Likewise, the quantity of clothing produced also remained the same. As a

result, the PPF curve shifted to the right of the initial PPF curve. The shift to the right was as

a result of an increase in the yield of rice from the existing resources. More rice (output) will

ECO 100 INTRODUCTION TO ECONOMICS 9

be produced using the same amount of resources (input). The improvement in technology

causes an outward shift in the production possibility frontier curve (Gillespie, 2014).

Question Three

a) Is the espresso coffee market, are firms price takers or price makers? Explain.

Economics defines price takers has participants in the market who cannot dictate the

price of their products in the market. Price takers have to accept the existing price in the

market. Price takers operate in a market where;

a) There are many sellers and many buyers,

b) The products are identical,

c) And, buyers have easy access to information on product prices.

On the other hand, price makers enjoy the power to dictate the price of their products in

the market. The power to become a price maker is influenced by factors such as;

a) High barrier to market entry or exit,

b) Existence of monopoly and oligopoly firms in the market,

c) And, buyers hold imperfect information on the price of products.

The Australian espresso coffee market has a few large players. Some of the companies

operating in the market include Starbucks, Nestle, McCafe, and Gloria Jeans. The companies

enjoy the ability to differentiate their coffees products according to consumers taste and

preferences. Large espresso coffee companies engage in mergers and acquisitions of smaller

companies to increase or maintain their market shares (Bishop, Parrott, Martie, & Miller,

2014). Second, a few large companies enjoy economies of scale, which is not available for

smaller companies. As a result, entrants by new companies is limited. Likewise, small

companies cannot survive in the market for long; they are forced to either shut down or a

be produced using the same amount of resources (input). The improvement in technology

causes an outward shift in the production possibility frontier curve (Gillespie, 2014).

Question Three

a) Is the espresso coffee market, are firms price takers or price makers? Explain.

Economics defines price takers has participants in the market who cannot dictate the

price of their products in the market. Price takers have to accept the existing price in the

market. Price takers operate in a market where;

a) There are many sellers and many buyers,

b) The products are identical,

c) And, buyers have easy access to information on product prices.

On the other hand, price makers enjoy the power to dictate the price of their products in

the market. The power to become a price maker is influenced by factors such as;

a) High barrier to market entry or exit,

b) Existence of monopoly and oligopoly firms in the market,

c) And, buyers hold imperfect information on the price of products.

The Australian espresso coffee market has a few large players. Some of the companies

operating in the market include Starbucks, Nestle, McCafe, and Gloria Jeans. The companies

enjoy the ability to differentiate their coffees products according to consumers taste and

preferences. Large espresso coffee companies engage in mergers and acquisitions of smaller

companies to increase or maintain their market shares (Bishop, Parrott, Martie, & Miller,

2014). Second, a few large companies enjoy economies of scale, which is not available for

smaller companies. As a result, entrants by new companies is limited. Likewise, small

companies cannot survive in the market for long; they are forced to either shut down or a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECO 100 INTRODUCTION TO ECONOMICS

10

merger with more substantial companies (Krugman & Wells, 2015). Lastly, consumers are

ready to pay any prices as far as the quality of coffee is guaranteed. Based on this market

features, the Australian espresso coffee market has a price maker structure. One, there is an

existence of oligopoly. Second, companies use taste and quality to differentiate their

products. And third, consumers hold imperfect information about the market; they are

interested more with the quality of the coffee (Hubbard, 2014).

b) With the aid of an appropriate economic model, explain why there has been such an

explosion in the number of coffee chains in Australia over the past ten years.

The growth of the Australian coffee market can be explained using the demand and

supply economic model. Demand refers to the ability and willingness to buy a given quantity

of a product at a given price. On the other hand, supply refers the quantity of a product that

producers are willing to sell at a given price. Change in demand and supply is influenced

factors such as quality, taste and preference and technology and innovation, among others

(Gillespie, 2014).

An explosion in the number of coffee chains in Australia has been witnessed over the

past 10 years. The significant growth has been influenced by; a) availability of quality

coffees, b) well-trained baristas, c) changing culture, and d) diversification of consumers

expectation. Moreover, international coffee chains have joined the Australian market bring in

their global expertise and experience.

Apart from the factors that have been mentioned above, Australians have developed a

culture of consuming quality foods in a welcoming and relaxed atmosphere. Many people are

moving away from the culture of heading home after a busy day to joining their friends and

family for a cup of coffee. Consumers have also acquired adequate information in the

10

merger with more substantial companies (Krugman & Wells, 2015). Lastly, consumers are

ready to pay any prices as far as the quality of coffee is guaranteed. Based on this market

features, the Australian espresso coffee market has a price maker structure. One, there is an

existence of oligopoly. Second, companies use taste and quality to differentiate their

products. And third, consumers hold imperfect information about the market; they are

interested more with the quality of the coffee (Hubbard, 2014).

b) With the aid of an appropriate economic model, explain why there has been such an

explosion in the number of coffee chains in Australia over the past ten years.

The growth of the Australian coffee market can be explained using the demand and

supply economic model. Demand refers to the ability and willingness to buy a given quantity

of a product at a given price. On the other hand, supply refers the quantity of a product that

producers are willing to sell at a given price. Change in demand and supply is influenced

factors such as quality, taste and preference and technology and innovation, among others

(Gillespie, 2014).

An explosion in the number of coffee chains in Australia has been witnessed over the

past 10 years. The significant growth has been influenced by; a) availability of quality

coffees, b) well-trained baristas, c) changing culture, and d) diversification of consumers

expectation. Moreover, international coffee chains have joined the Australian market bring in

their global expertise and experience.

Apart from the factors that have been mentioned above, Australians have developed a

culture of consuming quality foods in a welcoming and relaxed atmosphere. Many people are

moving away from the culture of heading home after a busy day to joining their friends and

family for a cup of coffee. Consumers have also acquired adequate information in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECO 100 INTRODUCTION TO ECONOMICS

11

availability of quality coffee within their environment. For example, there are plenty of

webpages and blog posts that inform consumers about the location of coffee shops, the price,

and quality of coffee being offered by each café (Banerjee & Warrier, 2018).

Considering the competitive nature of the Australian coffee industry, coffee shop

owners have turned their attention to operational efficiency. Australian Baristas have become

more efficient with resources, time and productivity. Lack of operation efficiency leads to

poor quality and high cost of production. Subsequently, the final price of coffee becomes

expenses lowering the demand and revenue realized. On the other hand, operational

efficiency results in high productivity, high quality and low cost of production. Operational

efficiency also increases the economies of scale enjoyed by coffee shops (Jones, 2014).

c) Do you foresee firms in the market making positive economic profit in the long run?

Explain.

Positive economic profit refers to the profit realized when the total revenue is higher

than total cost in the long run. In the long run, the total cost declines first before increases

beyond a desirable point. On the other hand, the total revenue increases first before

decreasing beyond a desirable point. The total cost and total revenue start to increase and fall

respectively beyond the economies of scale. The Australian coffee market is considered to be

monopolistically competitive. Unlike perfectly competitive market which can make economic

profits in the long run, monopolistically competitive market cannot. Therefore, firms

operating in the Australian coffee market cannot realize positive economic market in the long

run (Bishop, Parrott, Martie, & Miller, 2014).

d) Would the impact of government subsidy to each existing firm change your answer in

part (c) in the short run? Explain

11

availability of quality coffee within their environment. For example, there are plenty of

webpages and blog posts that inform consumers about the location of coffee shops, the price,

and quality of coffee being offered by each café (Banerjee & Warrier, 2018).

Considering the competitive nature of the Australian coffee industry, coffee shop

owners have turned their attention to operational efficiency. Australian Baristas have become

more efficient with resources, time and productivity. Lack of operation efficiency leads to

poor quality and high cost of production. Subsequently, the final price of coffee becomes

expenses lowering the demand and revenue realized. On the other hand, operational

efficiency results in high productivity, high quality and low cost of production. Operational

efficiency also increases the economies of scale enjoyed by coffee shops (Jones, 2014).

c) Do you foresee firms in the market making positive economic profit in the long run?

Explain.

Positive economic profit refers to the profit realized when the total revenue is higher

than total cost in the long run. In the long run, the total cost declines first before increases

beyond a desirable point. On the other hand, the total revenue increases first before

decreasing beyond a desirable point. The total cost and total revenue start to increase and fall

respectively beyond the economies of scale. The Australian coffee market is considered to be

monopolistically competitive. Unlike perfectly competitive market which can make economic

profits in the long run, monopolistically competitive market cannot. Therefore, firms

operating in the Australian coffee market cannot realize positive economic market in the long

run (Bishop, Parrott, Martie, & Miller, 2014).

d) Would the impact of government subsidy to each existing firm change your answer in

part (c) in the short run? Explain

ECO 100 INTRODUCTION TO ECONOMICS

12

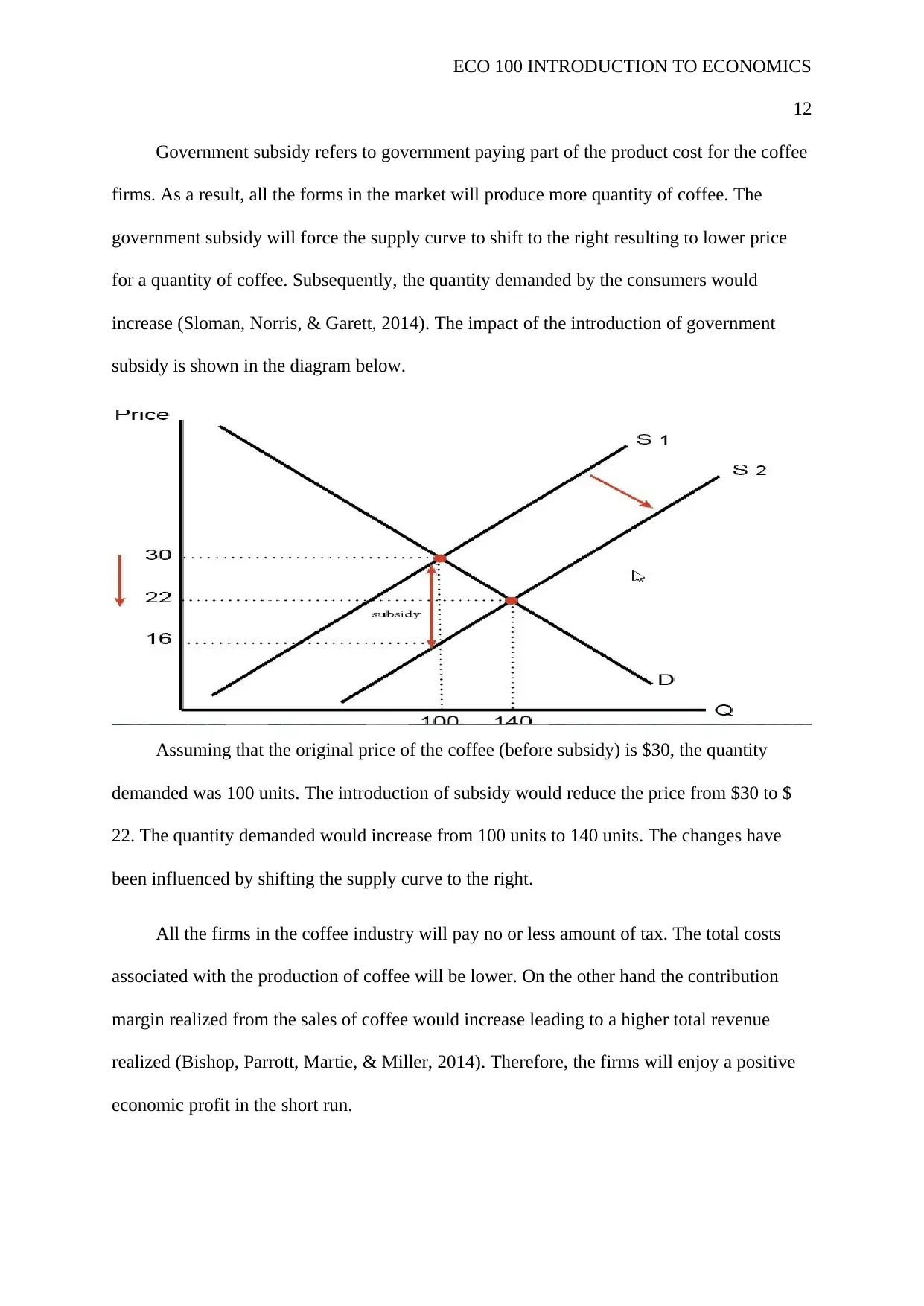

Government subsidy refers to government paying part of the product cost for the coffee

firms. As a result, all the forms in the market will produce more quantity of coffee. The

government subsidy will force the supply curve to shift to the right resulting to lower price

for a quantity of coffee. Subsequently, the quantity demanded by the consumers would

increase (Sloman, Norris, & Garett, 2014). The impact of the introduction of government

subsidy is shown in the diagram below.

Assuming that the original price of the coffee (before subsidy) is $30, the quantity

demanded was 100 units. The introduction of subsidy would reduce the price from $30 to $

22. The quantity demanded would increase from 100 units to 140 units. The changes have

been influenced by shifting the supply curve to the right.

All the firms in the coffee industry will pay no or less amount of tax. The total costs

associated with the production of coffee will be lower. On the other hand the contribution

margin realized from the sales of coffee would increase leading to a higher total revenue

realized (Bishop, Parrott, Martie, & Miller, 2014). Therefore, the firms will enjoy a positive

economic profit in the short run.

12

Government subsidy refers to government paying part of the product cost for the coffee

firms. As a result, all the forms in the market will produce more quantity of coffee. The

government subsidy will force the supply curve to shift to the right resulting to lower price

for a quantity of coffee. Subsequently, the quantity demanded by the consumers would

increase (Sloman, Norris, & Garett, 2014). The impact of the introduction of government

subsidy is shown in the diagram below.

Assuming that the original price of the coffee (before subsidy) is $30, the quantity

demanded was 100 units. The introduction of subsidy would reduce the price from $30 to $

22. The quantity demanded would increase from 100 units to 140 units. The changes have

been influenced by shifting the supply curve to the right.

All the firms in the coffee industry will pay no or less amount of tax. The total costs

associated with the production of coffee will be lower. On the other hand the contribution

margin realized from the sales of coffee would increase leading to a higher total revenue

realized (Bishop, Parrott, Martie, & Miller, 2014). Therefore, the firms will enjoy a positive

economic profit in the short run.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.