Arden University FIN4001: Financial Analysis Assignment

VerifiedAdded on 2023/06/03

|15

|3209

|236

Homework Assignment

AI Summary

This assignment solution provides a comprehensive financial analysis, addressing key concepts in corporate governance, financial ratios, and capital budgeting. The analysis begins with an exploration of corporate accountability and good governance principles, including transparency, fairness, responsibility, and accountability, with examples from companies like Cadbury, Coca-Cola Amatil, and Wesfarmers Group. The solution then delves into financial ratios, comparing profitability and liquidity between two companies, using charts to illustrate the analysis. The assignment further examines sources of finance, including bank loans, angel investors, and venture capital, and contrasts different budgeting methods such as zero-based and incremental budgeting. Finally, the solution covers capital budgeting techniques, including calculating net present value (NPV) and payback periods for investment projects, providing a detailed assessment of each project's financial viability.

Running head: FINANCIAL ANALYSIS

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ANALYSIS

Table of Contents

Question 1........................................................................................................................................2

Part a............................................................................................................................................2

Part b............................................................................................................................................4

Question 2........................................................................................................................................5

Question 3........................................................................................................................................7

Part a............................................................................................................................................7

Part b............................................................................................................................................8

Question 4......................................................................................................................................10

Part a..........................................................................................................................................10

Part b..........................................................................................................................................11

Reference.......................................................................................................................................12

FINANCIAL ANALYSIS

Table of Contents

Question 1........................................................................................................................................2

Part a............................................................................................................................................2

Part b............................................................................................................................................4

Question 2........................................................................................................................................5

Question 3........................................................................................................................................7

Part a............................................................................................................................................7

Part b............................................................................................................................................8

Question 4......................................................................................................................................10

Part a..........................................................................................................................................10

Part b..........................................................................................................................................11

Reference.......................................................................................................................................12

2

FINANCIAL ANALYSIS

Question 1

Part a

In general, the corporate accountability is considered with responsibilities and the obligations

which provides an explanation and reasons for the conduct and actions of the company. In short

sound corporate principles needs to be depicted in form of the understandable and balanced

assessment of the financial position of the company along with the prospects. The board is

further responsible for assessment of the relevant activities which relates to business risks and

internal control systems. A good corporate reporting assumes that board is depicted to maintain

and establish transparent and arrangements along with assigning appropriate relationship with

the auditor of the company. The board needs to also communicate with the stakeholders for fair

and balanced assessment of the purpose which are necessary from the business perspective

(Tricker and Tricker 2015).

In the corporate report published by Cadbury in he UK in 1991 has been able to outline

that the company has followed a good CG system through which business activities controlled

and directed in an appropriate manner. A good CG practice needs to be identified as per the key

factors underpinning the integrity and efficiency of a particular company. In case of depiction of

poor CG practice, the company’s potential may be greatly reduced which can lead to significant

nature of difficulty. Some of the other examples from the company’s potential can lead to

difficulties in financial activities which may have long term impact and damage the reputation of

the organization. A company applying the core principles needs to consider the CG, fairness,

responsibility, transparency and accountability which will lead to attract more number of

investors and support the financial growth (Barkemeyer et al. 2015).

FINANCIAL ANALYSIS

Question 1

Part a

In general, the corporate accountability is considered with responsibilities and the obligations

which provides an explanation and reasons for the conduct and actions of the company. In short

sound corporate principles needs to be depicted in form of the understandable and balanced

assessment of the financial position of the company along with the prospects. The board is

further responsible for assessment of the relevant activities which relates to business risks and

internal control systems. A good corporate reporting assumes that board is depicted to maintain

and establish transparent and arrangements along with assigning appropriate relationship with

the auditor of the company. The board needs to also communicate with the stakeholders for fair

and balanced assessment of the purpose which are necessary from the business perspective

(Tricker and Tricker 2015).

In the corporate report published by Cadbury in he UK in 1991 has been able to outline

that the company has followed a good CG system through which business activities controlled

and directed in an appropriate manner. A good CG practice needs to be identified as per the key

factors underpinning the integrity and efficiency of a particular company. In case of depiction of

poor CG practice, the company’s potential may be greatly reduced which can lead to significant

nature of difficulty. Some of the other examples from the company’s potential can lead to

difficulties in financial activities which may have long term impact and damage the reputation of

the organization. A company applying the core principles needs to consider the CG, fairness,

responsibility, transparency and accountability which will lead to attract more number of

investors and support the financial growth (Barkemeyer et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ANALYSIS

It needs to be therefore seen that, companies applying the core principles as CG, fairness,

responsibility, transparency and accountability are seen with organizations such as Coca Cola

Amatil, Shell and British Petroleum. These organizations are seen with articulating the strategy

to reinforce the company’s agency model. Moreover, these organizations have also considered

the development of the robust planning framework, driven by relevant data and scope-of-work

(Beekes, Brown and Zhang 2015). Some of the other reasons for these companies to follow a

good CG strategy has been further depicted in terms of the different types of the other actions

taken by the companies needs to be depicted as per the continuous effort to scout the agency

industry for top talent (Flower 2015). These organizations have not only identify the right agency

partner but also maintain the best talent pertaining to the agencies in the business which will led

to attract more number of investors and support for the financial growth (Joseph et al. 2016).

These agencies are also seen with the relevant actions required delivering the competitive edge

needed to deliver the goals. Some of the other organizations such as Wesfarmers Group has been

also able to excel in terms of core principles like engaging workers in a more enthusiastic and

productive manner and taking responsibility for attracting fresh talent in the company. There is

also seen to be relevant for rewarding the trainees in having a positive impact and appreciation.

The companies need to be vulnerable for management to be anonymously figuring out the junior

employees and getting to know about the ways the management engages their employees. In this

manner the team members are also depicted to be avoid any instance of conflicts rather than

providing actual opinion (Ni and Van Wart 2015).

FINANCIAL ANALYSIS

It needs to be therefore seen that, companies applying the core principles as CG, fairness,

responsibility, transparency and accountability are seen with organizations such as Coca Cola

Amatil, Shell and British Petroleum. These organizations are seen with articulating the strategy

to reinforce the company’s agency model. Moreover, these organizations have also considered

the development of the robust planning framework, driven by relevant data and scope-of-work

(Beekes, Brown and Zhang 2015). Some of the other reasons for these companies to follow a

good CG strategy has been further depicted in terms of the different types of the other actions

taken by the companies needs to be depicted as per the continuous effort to scout the agency

industry for top talent (Flower 2015). These organizations have not only identify the right agency

partner but also maintain the best talent pertaining to the agencies in the business which will led

to attract more number of investors and support for the financial growth (Joseph et al. 2016).

These agencies are also seen with the relevant actions required delivering the competitive edge

needed to deliver the goals. Some of the other organizations such as Wesfarmers Group has been

also able to excel in terms of core principles like engaging workers in a more enthusiastic and

productive manner and taking responsibility for attracting fresh talent in the company. There is

also seen to be relevant for rewarding the trainees in having a positive impact and appreciation.

The companies need to be vulnerable for management to be anonymously figuring out the junior

employees and getting to know about the ways the management engages their employees. In this

manner the team members are also depicted to be avoid any instance of conflicts rather than

providing actual opinion (Ni and Van Wart 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ANALYSIS

Part b

The principle of the good governance considers that the stakeholders should be informed

on the various activities of the company along with the plans which it intend to execute in the

future. Transparency factor is referred with the openness and readiness for providing clear

information to the stakeholders and other shareholders. For instance, transparency is associated

to the openness and readiness for disclosure of financial performance to be accurate and true in

nature. Moreover, the disclosure of information in the matters related to the performance of the

organization needs to timely and accurately ensure the inventors has access to the information on

the clear, factual, financial, social and environmental position of the organization. The

companies need to confirm responsibilities and roles of the board and management for providing

the shareholders relevant level of accountability. The transparency factor ensures that there is full

confidence among the stakeholders for making the appropriate decision making and management

process associated to the company (Leipziger 2017).

A strong CG ensures that the investors are able to maintain sufficient confidence for

supporting further growth in the financial performance. The organizations involved in the

implementation of sound corporate success and economic growth. The fairness concept is

referred with the equal treatment of the stakeholders. For instance, all the shareholders needs to

obtain equal consideration for any shareholding in their belonging. In different countries the

fairness aspect of the corporate reporting is protected by the relevant laws. However, it needs to

be also seen that the companies also desire to opt for the appropriate shareholder agreement

which is directly associated with including extensive and effective minority protection.

Moreover, the shareholders should be done in a fairness based on the treatment of the

stakeholders by considering the opinions of the employees, communities and public officials. It

FINANCIAL ANALYSIS

Part b

The principle of the good governance considers that the stakeholders should be informed

on the various activities of the company along with the plans which it intend to execute in the

future. Transparency factor is referred with the openness and readiness for providing clear

information to the stakeholders and other shareholders. For instance, transparency is associated

to the openness and readiness for disclosure of financial performance to be accurate and true in

nature. Moreover, the disclosure of information in the matters related to the performance of the

organization needs to timely and accurately ensure the inventors has access to the information on

the clear, factual, financial, social and environmental position of the organization. The

companies need to confirm responsibilities and roles of the board and management for providing

the shareholders relevant level of accountability. The transparency factor ensures that there is full

confidence among the stakeholders for making the appropriate decision making and management

process associated to the company (Leipziger 2017).

A strong CG ensures that the investors are able to maintain sufficient confidence for

supporting further growth in the financial performance. The organizations involved in the

implementation of sound corporate success and economic growth. The fairness concept is

referred with the equal treatment of the stakeholders. For instance, all the shareholders needs to

obtain equal consideration for any shareholding in their belonging. In different countries the

fairness aspect of the corporate reporting is protected by the relevant laws. However, it needs to

be also seen that the companies also desire to opt for the appropriate shareholder agreement

which is directly associated with including extensive and effective minority protection.

Moreover, the shareholders should be done in a fairness based on the treatment of the

stakeholders by considering the opinions of the employees, communities and public officials. It

5

FINANCIAL ANALYSIS

needs to be seen that more fairer is the entity for the stakeholders, the more likely it will survive

the pressure of the interested parties (Ioannou and Serafeim 2017).

The board of directors are also depicted to provide the relevant opportunity which is seen

to be depicted as per the different types of the concepts associated to act on behalf of the

company. The companies need to therefore accept the various types of the propositions for

ensuring that the directors are responsible for monitoring the performance of the company.

Moreover, accountability needs to be considered as per the hand in hand with the responsibility

factor. In addition to this, the board of directors are also seen to be responsibility of

accountability pertaining to the way company carries out the responsibilities (De Villiers, Rouse

and Kerr 2016).

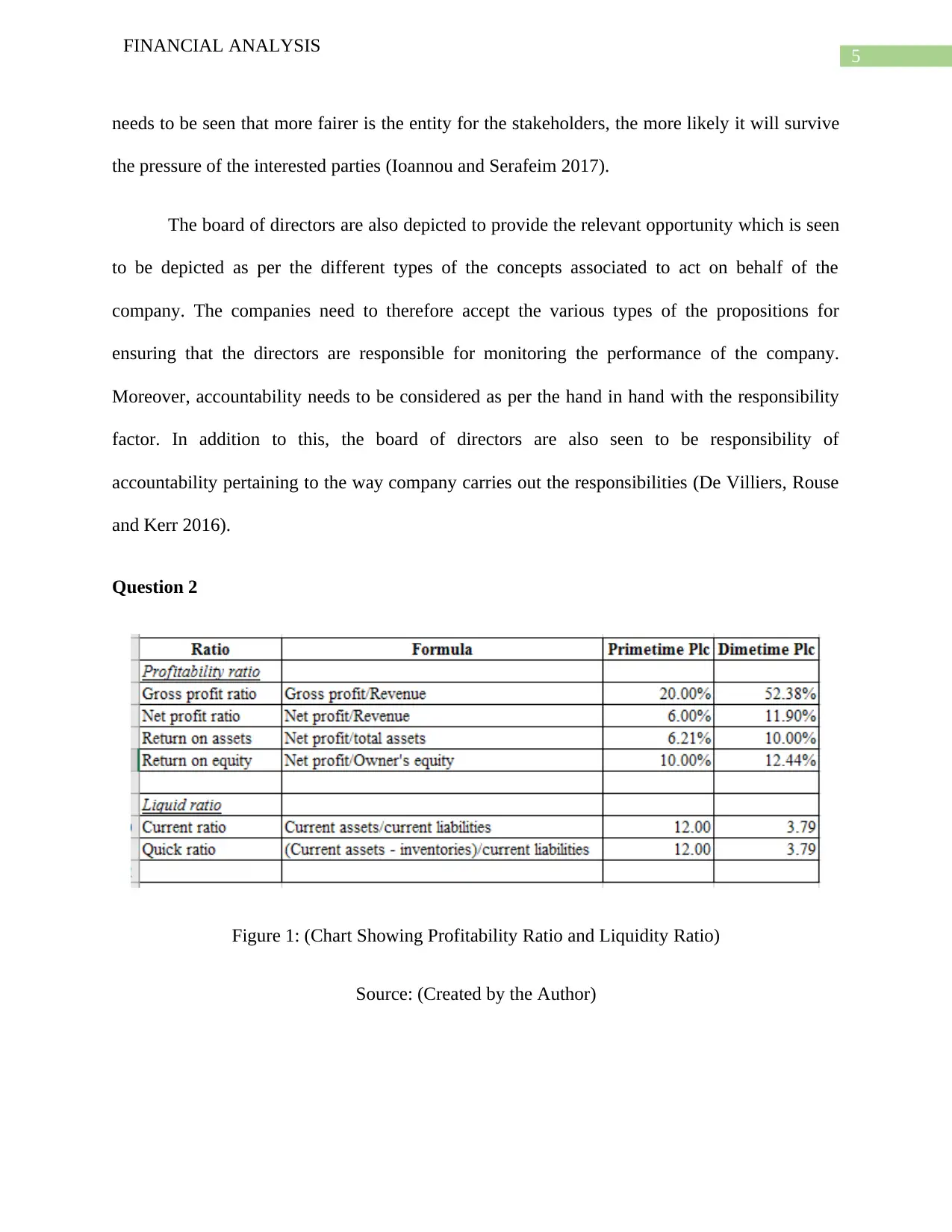

Question 2

Figure 1: (Chart Showing Profitability Ratio and Liquidity Ratio)

Source: (Created by the Author)

FINANCIAL ANALYSIS

needs to be seen that more fairer is the entity for the stakeholders, the more likely it will survive

the pressure of the interested parties (Ioannou and Serafeim 2017).

The board of directors are also depicted to provide the relevant opportunity which is seen

to be depicted as per the different types of the concepts associated to act on behalf of the

company. The companies need to therefore accept the various types of the propositions for

ensuring that the directors are responsible for monitoring the performance of the company.

Moreover, accountability needs to be considered as per the hand in hand with the responsibility

factor. In addition to this, the board of directors are also seen to be responsibility of

accountability pertaining to the way company carries out the responsibilities (De Villiers, Rouse

and Kerr 2016).

Question 2

Figure 1: (Chart Showing Profitability Ratio and Liquidity Ratio)

Source: (Created by the Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ANALYSIS

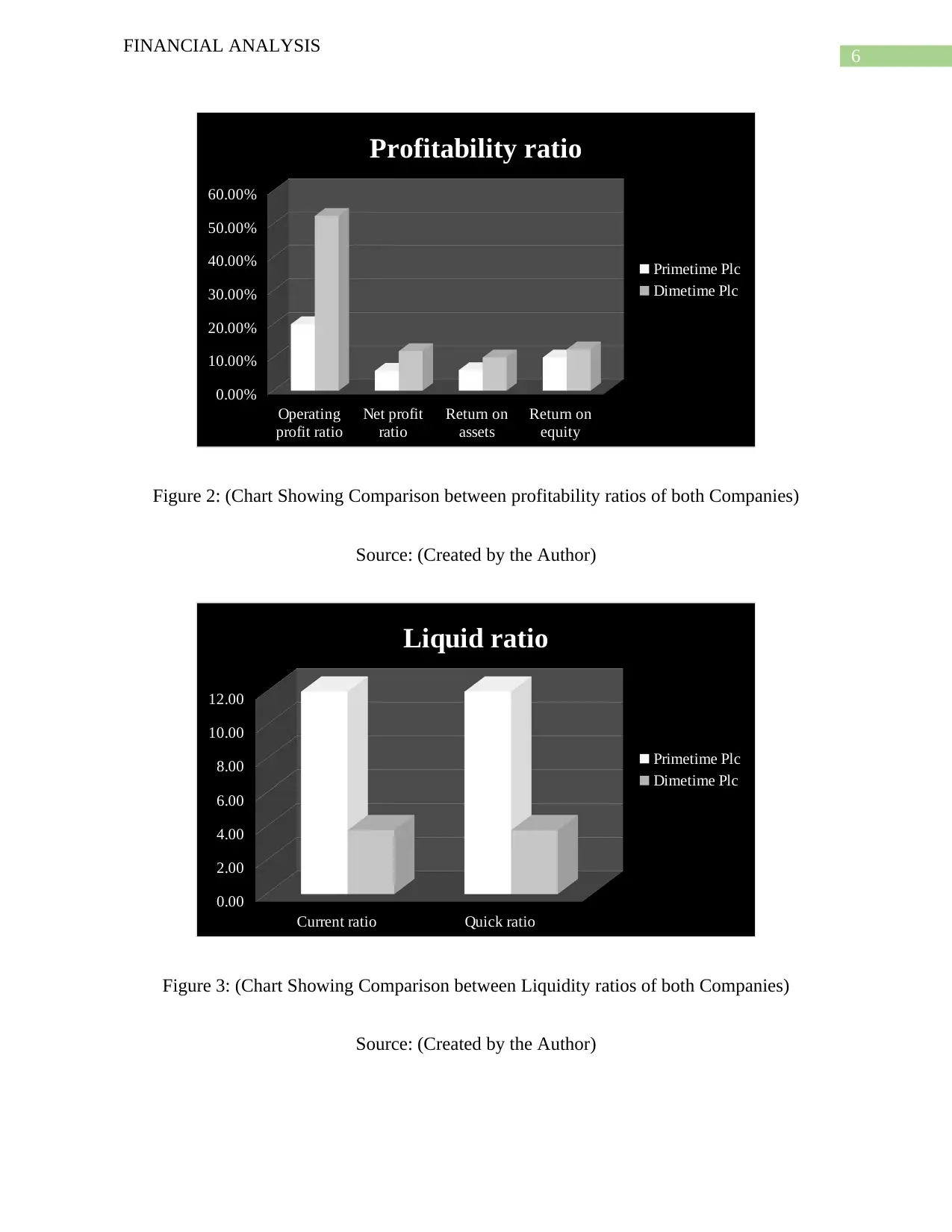

Operating

profit ratio

Net profit

ratio

Return on

assets

Return on

equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Profitability ratio

Primetime Plc

Dimetime Plc

Figure 2: (Chart Showing Comparison between profitability ratios of both Companies)

Source: (Created by the Author)

Current ratio Quick ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Liquid ratio

Primetime Plc

Dimetime Plc

Figure 3: (Chart Showing Comparison between Liquidity ratios of both Companies)

Source: (Created by the Author)

FINANCIAL ANALYSIS

Operating

profit ratio

Net profit

ratio

Return on

assets

Return on

equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Profitability ratio

Primetime Plc

Dimetime Plc

Figure 2: (Chart Showing Comparison between profitability ratios of both Companies)

Source: (Created by the Author)

Current ratio Quick ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Liquid ratio

Primetime Plc

Dimetime Plc

Figure 3: (Chart Showing Comparison between Liquidity ratios of both Companies)

Source: (Created by the Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ANALYSIS

The above table shows that the profitability ratios of the business which are operating

profit ratio, net profit ratio, return on assets and return on equity. The gross profit margin of

Dimetime Plc which is 52.38% is shown to be more than Primetime Plc which is shown to be

20%. The net profit margin of Dimetime Plc is shown to be better than Primetime Plc which

suggest that the financial structure Dimetime Plc is better (Lartey, Antwi and Boadi 2013). The

return on assets and equity of the business are considered to be financial indicators for the overall

success of the business. Both the estimates are shown to be more for Dimetime Plc in

comparison to Primetime Plc.

The liquidity ratios of the business show the ability of the business to meet the current

obligation of the business (Bolek 2013). The current ratio and quick ratio for Primetime Plc is

shown to be 12 which is shown to be more than the estimates shown for Dimetime Plc.

Question 3

Part a

The business of Xporters can select the following sources of finance for the purpose of

funding the activities of the business:

Bank Loan: The business of Xporters can take a loan for the purpose of financing the

planned expansion of the business. The business can avail for loans from banks in

exchange for some collateral securities. As per the anticipation of the business, the

amount of external finance which the company needs to raise is shown to be $ 1 million.

The bank loan is a smart solution towards financing of a business and the same has the

option of being either short term or loan in nature (Lee, Sameen and Cowling 2015). In

addition to this, Loan is considered to a be cheap source of finance and the source also

FINANCIAL ANALYSIS

The above table shows that the profitability ratios of the business which are operating

profit ratio, net profit ratio, return on assets and return on equity. The gross profit margin of

Dimetime Plc which is 52.38% is shown to be more than Primetime Plc which is shown to be

20%. The net profit margin of Dimetime Plc is shown to be better than Primetime Plc which

suggest that the financial structure Dimetime Plc is better (Lartey, Antwi and Boadi 2013). The

return on assets and equity of the business are considered to be financial indicators for the overall

success of the business. Both the estimates are shown to be more for Dimetime Plc in

comparison to Primetime Plc.

The liquidity ratios of the business show the ability of the business to meet the current

obligation of the business (Bolek 2013). The current ratio and quick ratio for Primetime Plc is

shown to be 12 which is shown to be more than the estimates shown for Dimetime Plc.

Question 3

Part a

The business of Xporters can select the following sources of finance for the purpose of

funding the activities of the business:

Bank Loan: The business of Xporters can take a loan for the purpose of financing the

planned expansion of the business. The business can avail for loans from banks in

exchange for some collateral securities. As per the anticipation of the business, the

amount of external finance which the company needs to raise is shown to be $ 1 million.

The bank loan is a smart solution towards financing of a business and the same has the

option of being either short term or loan in nature (Lee, Sameen and Cowling 2015). In

addition to this, Loan is considered to a be cheap source of finance and the source also

8

FINANCIAL ANALYSIS

has tax benefits as the business can get deductions for interest payments which are made

towards the loan.

Friends: The members of Xporters can also raise funds from friends which can also be

considered as loans (Khan 2015). The management can accumulate loans from the

friends and other relatives even though they do not play an active role in day to day

management of the business.

Angel Investors: This reflects a high-profile investor who can invest significant amount

of funds in the business in return for a stake holding in the business. The Angel investors

basically wants a partnership claim in the business (Ding, Sun and Au 2014). These types

of practices are often followed by businesses for the purpose of meeting the financing

requirement of the business.

Venture Capital: This is one of the popular sources of financing and is quite similar to

Angel Investors option. In this option, a group of individuals provides finances for the

business and manages the assets of the company (Maula and Murray 2017). Venture

Capitalists of the business invests in companies which has a strong financial record or

background.

Part b

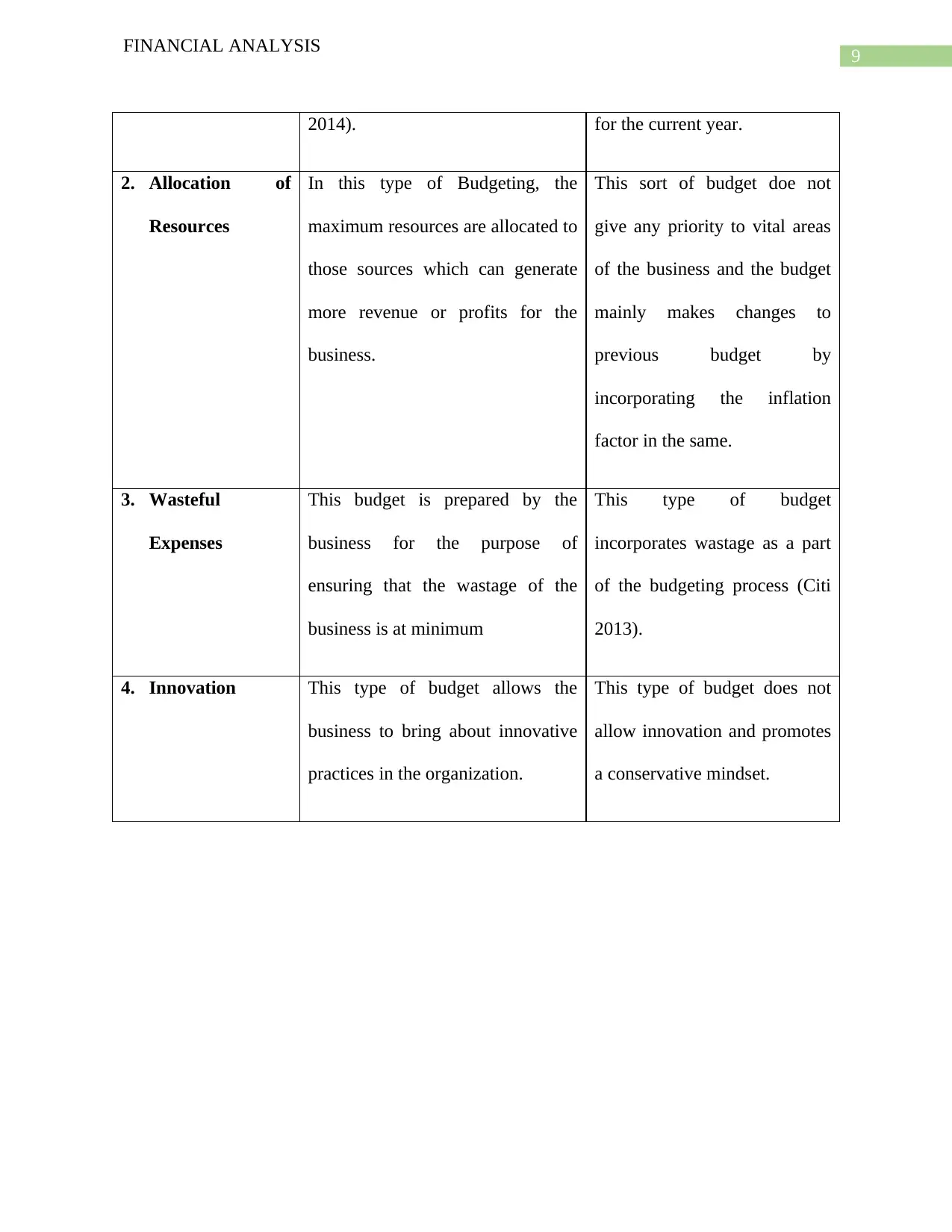

Point of Distinction Zero Based Budgeting Incremental Based Budgeting

1. Base for

Budgeting

This type of budgeting is done by

considering the base to be zero and

the budget is prepared without

considering the budgets which is

prepared for previous year (Ekanem

In this type of Budget, the

changes are made to the

budgets which was prepared in

previous and the same is used

FINANCIAL ANALYSIS

has tax benefits as the business can get deductions for interest payments which are made

towards the loan.

Friends: The members of Xporters can also raise funds from friends which can also be

considered as loans (Khan 2015). The management can accumulate loans from the

friends and other relatives even though they do not play an active role in day to day

management of the business.

Angel Investors: This reflects a high-profile investor who can invest significant amount

of funds in the business in return for a stake holding in the business. The Angel investors

basically wants a partnership claim in the business (Ding, Sun and Au 2014). These types

of practices are often followed by businesses for the purpose of meeting the financing

requirement of the business.

Venture Capital: This is one of the popular sources of financing and is quite similar to

Angel Investors option. In this option, a group of individuals provides finances for the

business and manages the assets of the company (Maula and Murray 2017). Venture

Capitalists of the business invests in companies which has a strong financial record or

background.

Part b

Point of Distinction Zero Based Budgeting Incremental Based Budgeting

1. Base for

Budgeting

This type of budgeting is done by

considering the base to be zero and

the budget is prepared without

considering the budgets which is

prepared for previous year (Ekanem

In this type of Budget, the

changes are made to the

budgets which was prepared in

previous and the same is used

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ANALYSIS

2014). for the current year.

2. Allocation of

Resources

In this type of Budgeting, the

maximum resources are allocated to

those sources which can generate

more revenue or profits for the

business.

This sort of budget doe not

give any priority to vital areas

of the business and the budget

mainly makes changes to

previous budget by

incorporating the inflation

factor in the same.

3. Wasteful

Expenses

This budget is prepared by the

business for the purpose of

ensuring that the wastage of the

business is at minimum

This type of budget

incorporates wastage as a part

of the budgeting process (Citi

2013).

4. Innovation This type of budget allows the

business to bring about innovative

practices in the organization.

This type of budget does not

allow innovation and promotes

a conservative mindset.

FINANCIAL ANALYSIS

2014). for the current year.

2. Allocation of

Resources

In this type of Budgeting, the

maximum resources are allocated to

those sources which can generate

more revenue or profits for the

business.

This sort of budget doe not

give any priority to vital areas

of the business and the budget

mainly makes changes to

previous budget by

incorporating the inflation

factor in the same.

3. Wasteful

Expenses

This budget is prepared by the

business for the purpose of

ensuring that the wastage of the

business is at minimum

This type of budget

incorporates wastage as a part

of the budgeting process (Citi

2013).

4. Innovation This type of budget allows the

business to bring about innovative

practices in the organization.

This type of budget does not

allow innovation and promotes

a conservative mindset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL ANALYSIS

Question 4

Part a

Year Project A Project B Discount rate @ 9% Project A-disc cash flow Project B-disc cash flow

0 -45000 -45000 1 -45000 -45000

1 21250 28750 0.9174 19494.75 26375.25

2 24100 29050 0.8417 20284.97 24451.385

3 24100 27250 0.7722 18610.02 21042.45

4 41250 27500 0.7084 29221.5 19481

42611.24 46350.085NPV

Non-discounted payback period

Year Cash inflows Cumulative cash inflows Cash inflows Cumulative cash inflows

0 -45000 -45000

1 21250 21250 28750 28750

2 24100 45350 29050 57800

3 24100 69450 27250 85050

4 41250 110700 27500 112550

Non-discounted payback period 1.99 1.56

Project A Project B

Payback period

Year Cash inflows Cumulative cash inflows Cash inflows Cumulative cash inflows

0 -45000 -45000

1 19494.75 21250 26375.25 26375.25

2 20284.97 39779.72 24451.385 50826.635

3 18610.02 58389.74 21042.45 71869.085

4 29221.5 87611.24 19481 91350.085

Payback period 2.28 1.76

Project A Project B

Accounting rate of return Project A Project B

Annual depreciation 11250 11250

Average accounting income 10652.81 11587.52

Accounting rate of return 23.67% 25.75%

The above table shows the various investment appraisal techniques which are applied for

the purpose of establishing the viability of a project. The NPV analysis which shows whether a

FINANCIAL ANALYSIS

Question 4

Part a

Year Project A Project B Discount rate @ 9% Project A-disc cash flow Project B-disc cash flow

0 -45000 -45000 1 -45000 -45000

1 21250 28750 0.9174 19494.75 26375.25

2 24100 29050 0.8417 20284.97 24451.385

3 24100 27250 0.7722 18610.02 21042.45

4 41250 27500 0.7084 29221.5 19481

42611.24 46350.085NPV

Non-discounted payback period

Year Cash inflows Cumulative cash inflows Cash inflows Cumulative cash inflows

0 -45000 -45000

1 21250 21250 28750 28750

2 24100 45350 29050 57800

3 24100 69450 27250 85050

4 41250 110700 27500 112550

Non-discounted payback period 1.99 1.56

Project A Project B

Payback period

Year Cash inflows Cumulative cash inflows Cash inflows Cumulative cash inflows

0 -45000 -45000

1 19494.75 21250 26375.25 26375.25

2 20284.97 39779.72 24451.385 50826.635

3 18610.02 58389.74 21042.45 71869.085

4 29221.5 87611.24 19481 91350.085

Payback period 2.28 1.76

Project A Project B

Accounting rate of return Project A Project B

Annual depreciation 11250 11250

Average accounting income 10652.81 11587.52

Accounting rate of return 23.67% 25.75%

The above table shows the various investment appraisal techniques which are applied for

the purpose of establishing the viability of a project. The NPV analysis which shows whether a

11

FINANCIAL ANALYSIS

project will be generating profits or loss for the business is shown to be favorable for Project B

as the NPV of the same is computed to be higher than Project A. The accounting rate of return

and payback period which is shown for the project is shown to be higher for Project B in

comparison to Project A which is shown to be a favorable sign for the business (Almarri and

Blackwell 2014). In addition to this, the discounted Payback period is also shown to be favorable

for Project B. This clearly indicates that the business should select Project B as the same is

shown to be more profitable than Project A.

Part b

The main difference between the discounted and non-discounted investment appraisal

techniques is the application of the concept of time value of money. In discounted appraisal

techniques the concept of time value of money is considered and therefore the techniques are

known to reflect accurate results (Hoesli and MacGregor 2014). In case of Non-Discounted

Appraisal techniques, the concept of time value of money is not considered and therefore the

same is not reflecting the accurate results.

The discounted payback period is not used very often as the investment appraisal

techniques and the same does not reflect accurate results. The payback period also does not show

accurate result even in case of discount rate is considered.

FINANCIAL ANALYSIS

project will be generating profits or loss for the business is shown to be favorable for Project B

as the NPV of the same is computed to be higher than Project A. The accounting rate of return

and payback period which is shown for the project is shown to be higher for Project B in

comparison to Project A which is shown to be a favorable sign for the business (Almarri and

Blackwell 2014). In addition to this, the discounted Payback period is also shown to be favorable

for Project B. This clearly indicates that the business should select Project B as the same is

shown to be more profitable than Project A.

Part b

The main difference between the discounted and non-discounted investment appraisal

techniques is the application of the concept of time value of money. In discounted appraisal

techniques the concept of time value of money is considered and therefore the techniques are

known to reflect accurate results (Hoesli and MacGregor 2014). In case of Non-Discounted

Appraisal techniques, the concept of time value of money is not considered and therefore the

same is not reflecting the accurate results.

The discounted payback period is not used very often as the investment appraisal

techniques and the same does not reflect accurate results. The payback period also does not show

accurate result even in case of discount rate is considered.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.