Introduction to Financial Accounting: March 2021 Transactions Analysis

VerifiedAdded on 2022/12/23

|23

|3246

|57

Homework Assignment

AI Summary

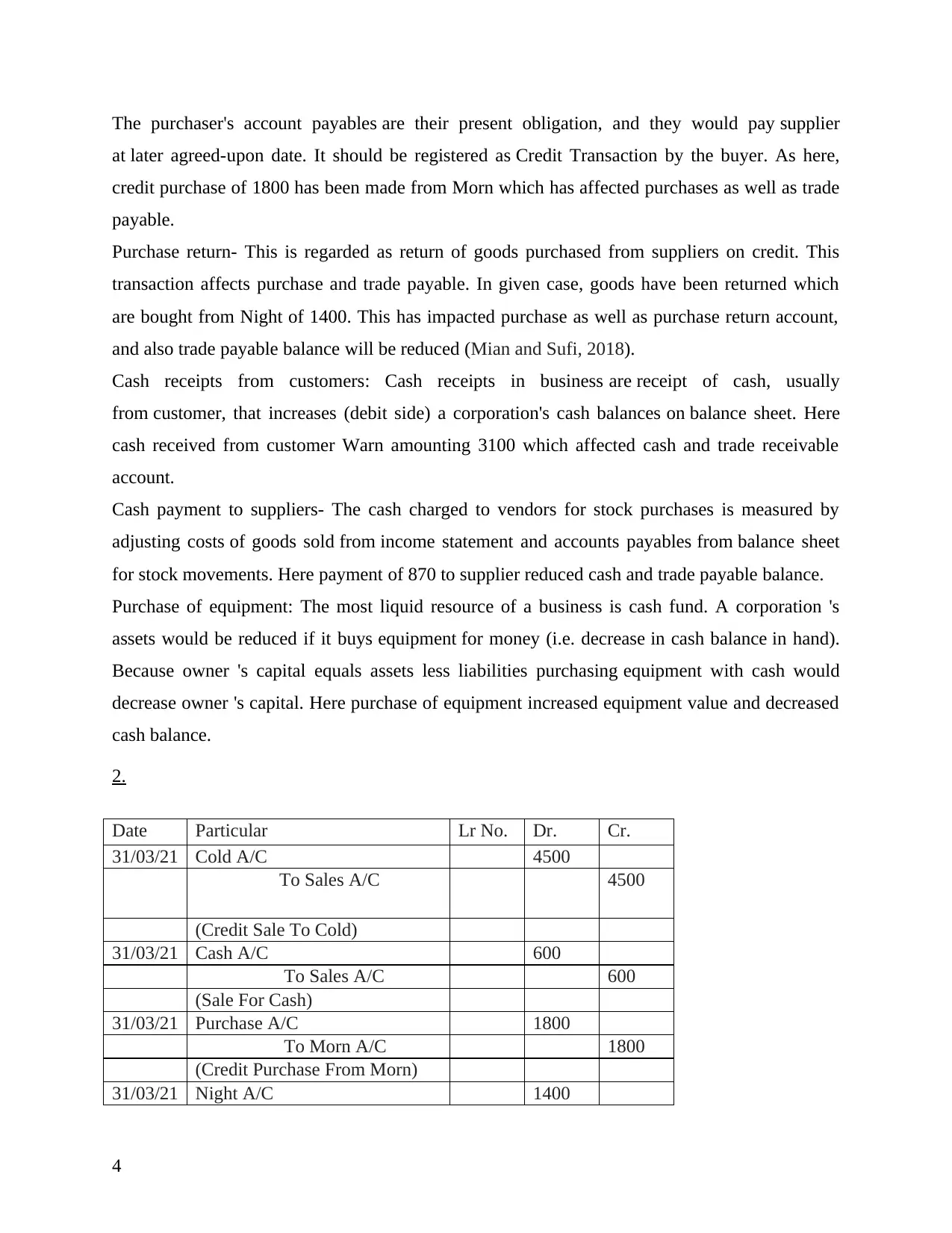

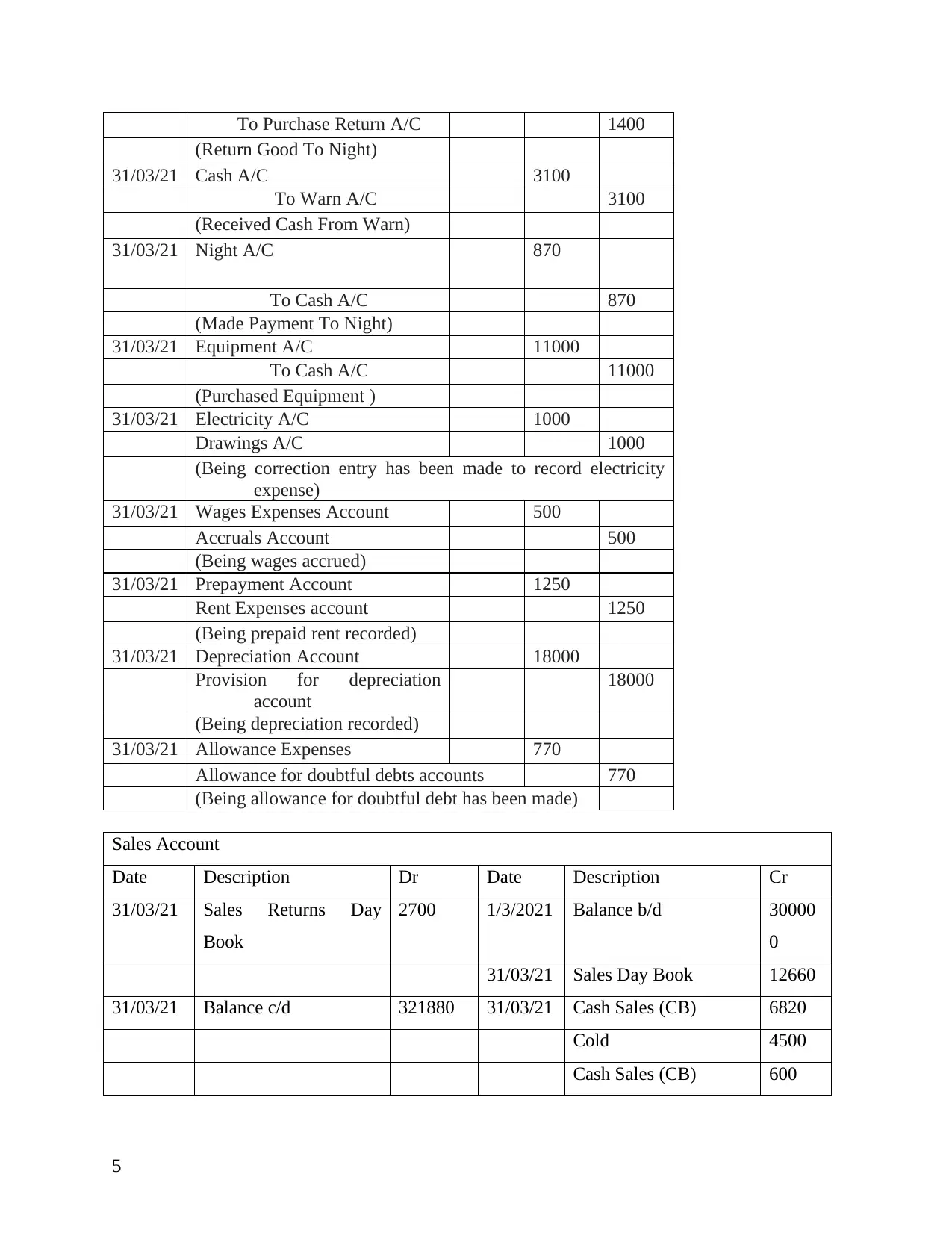

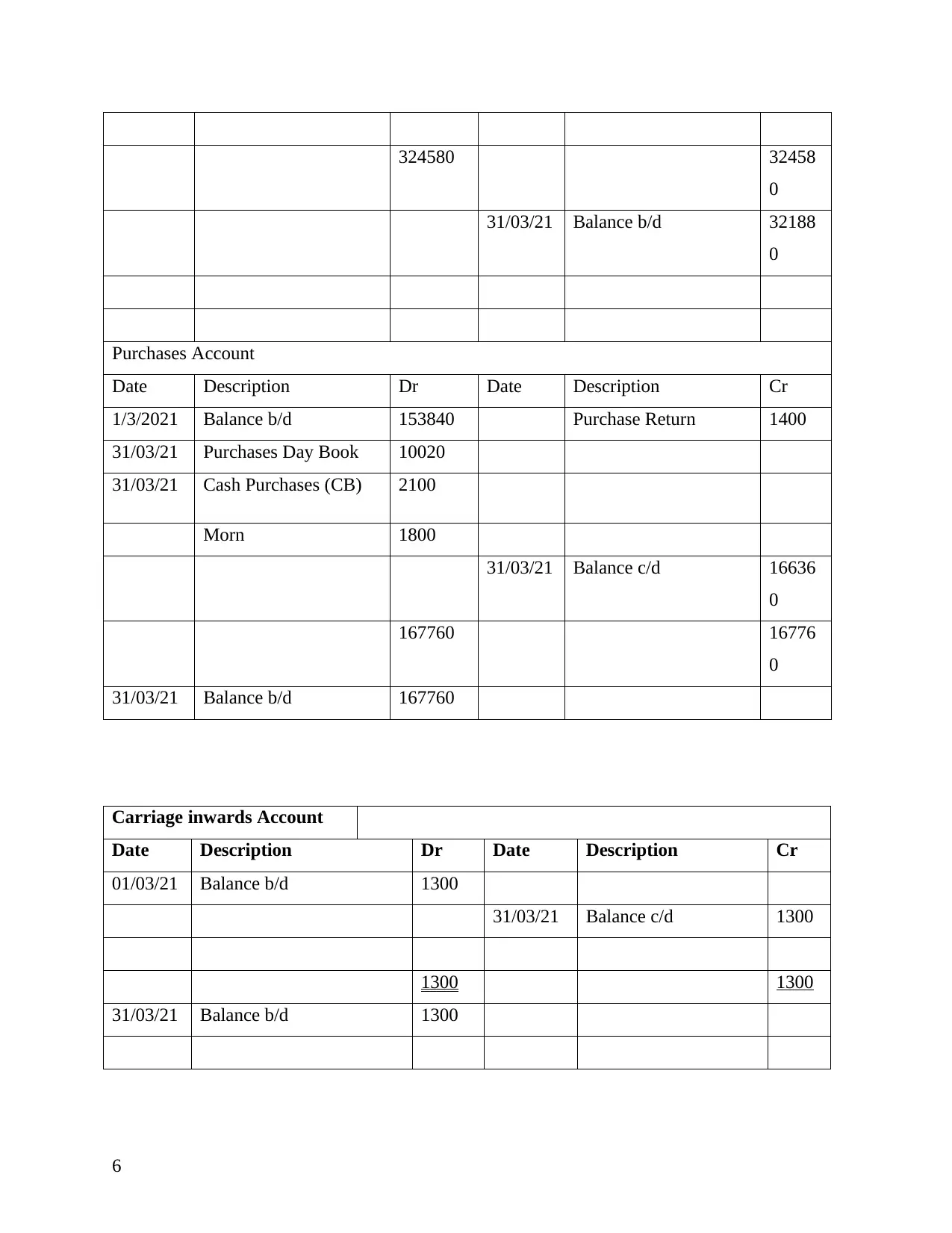

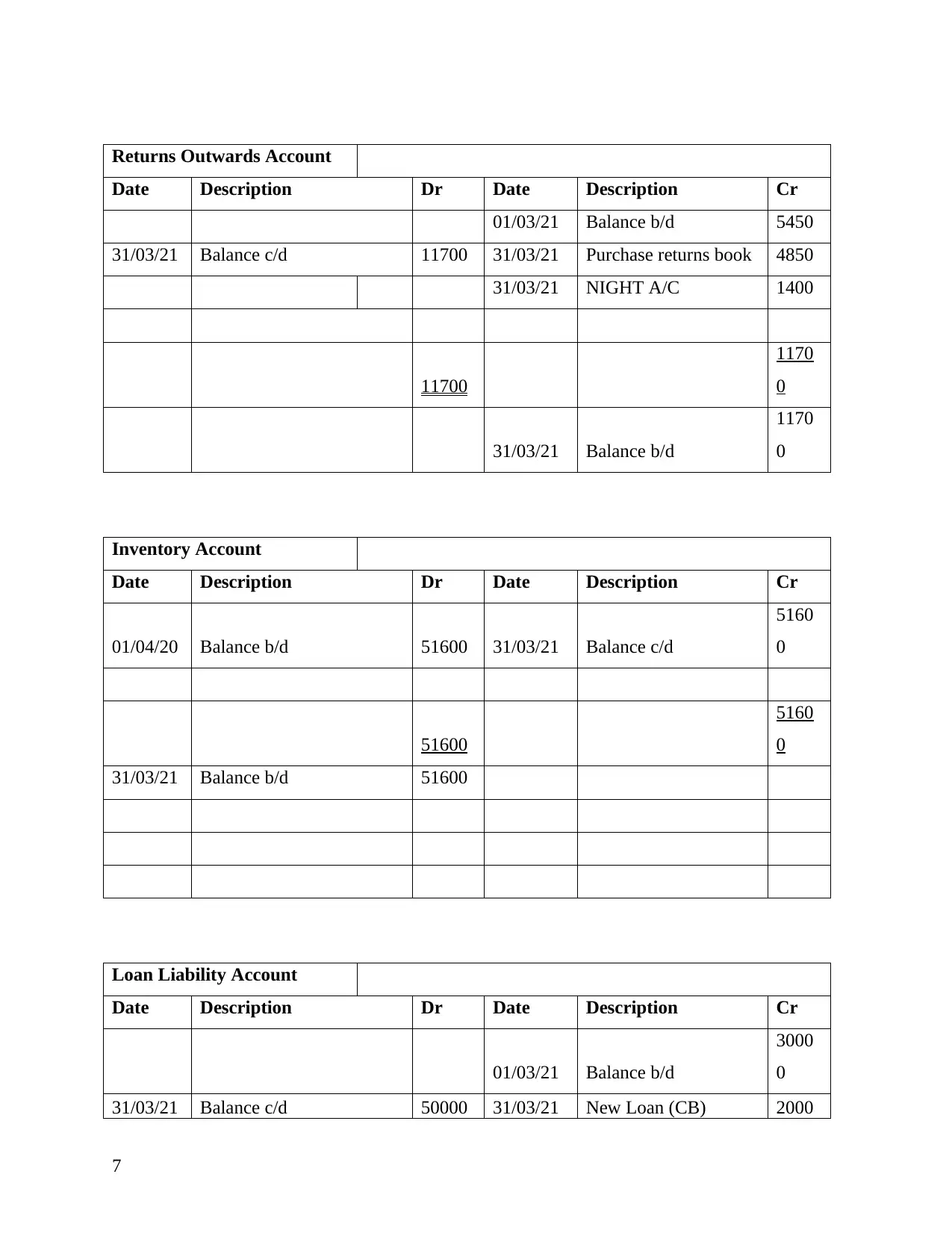

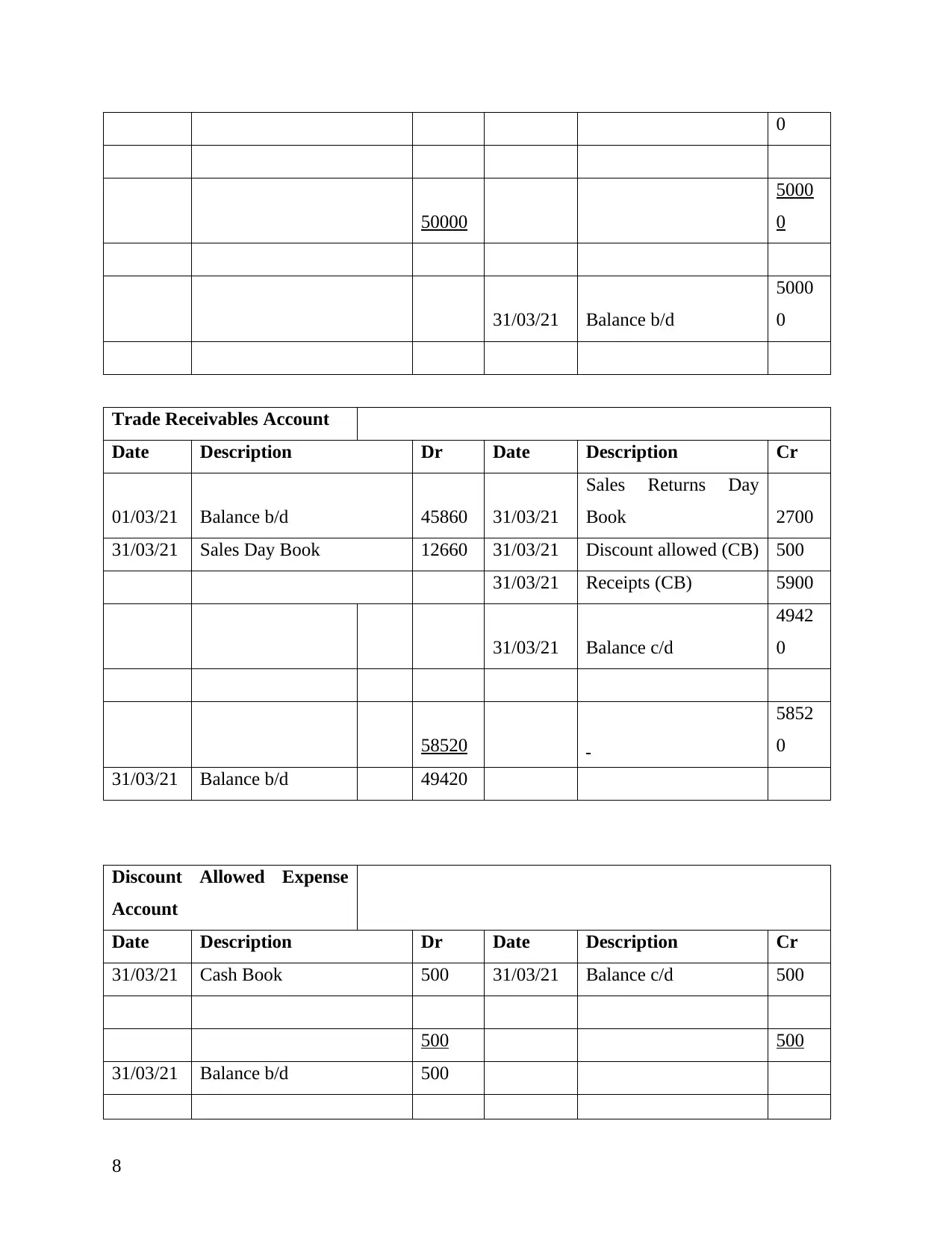

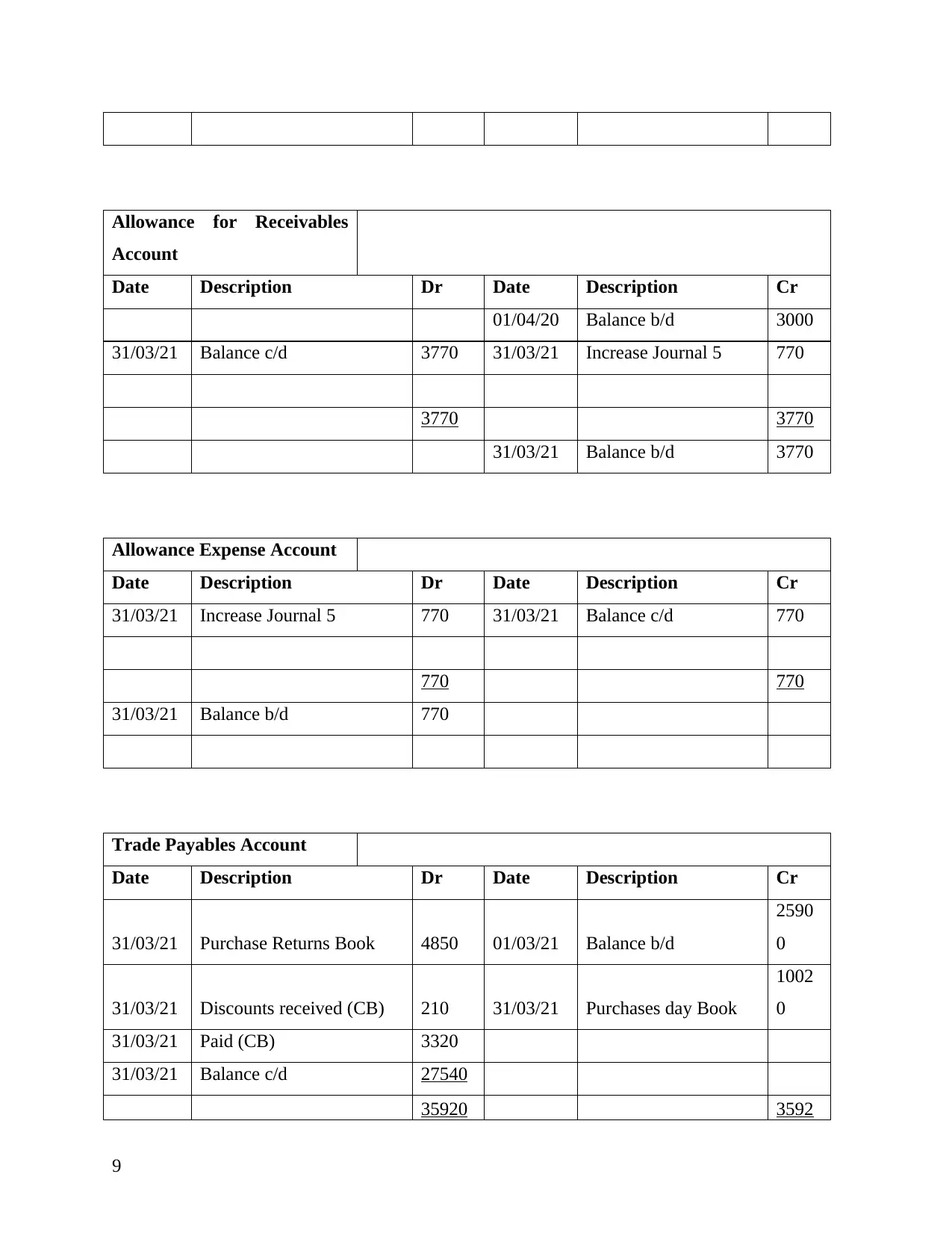

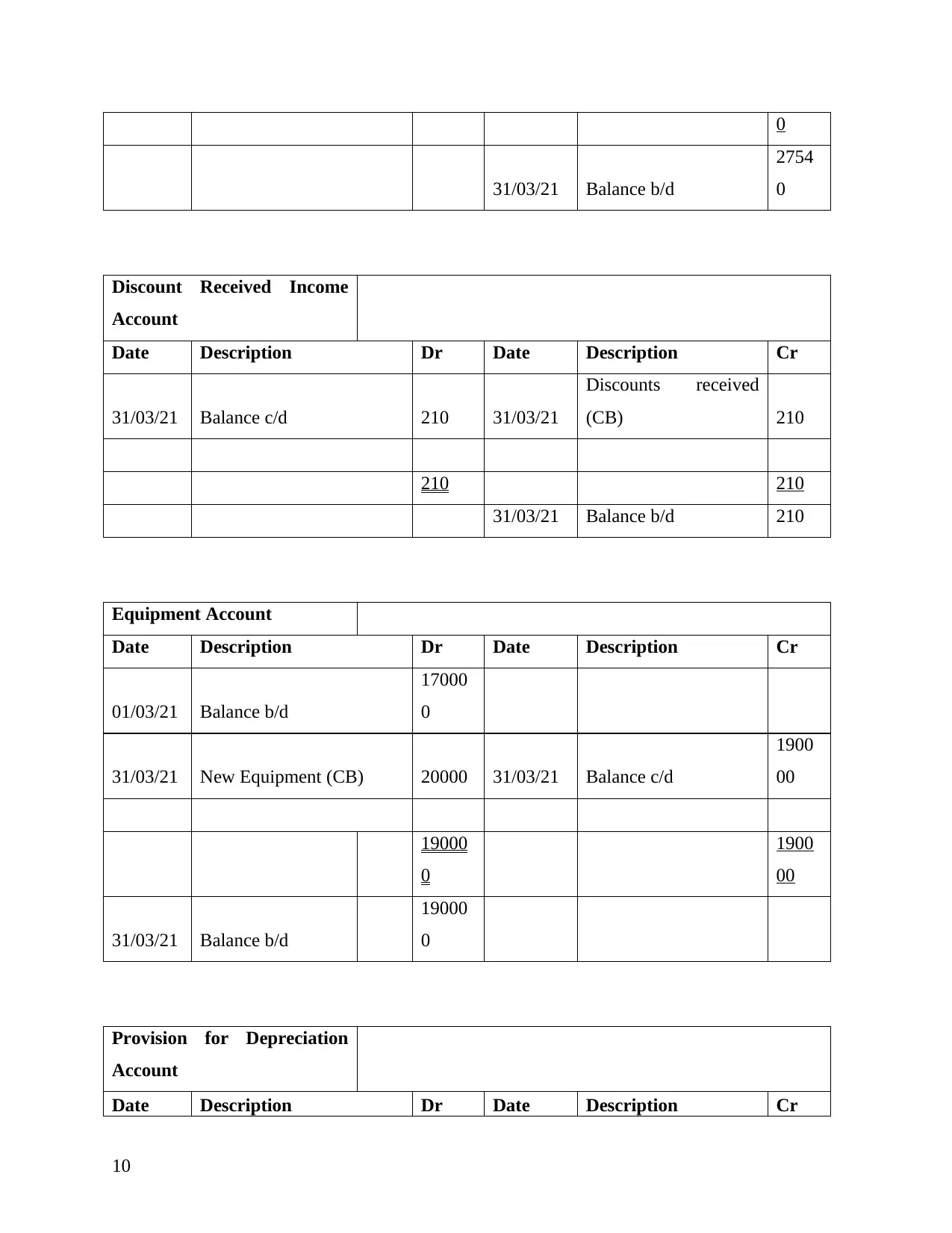

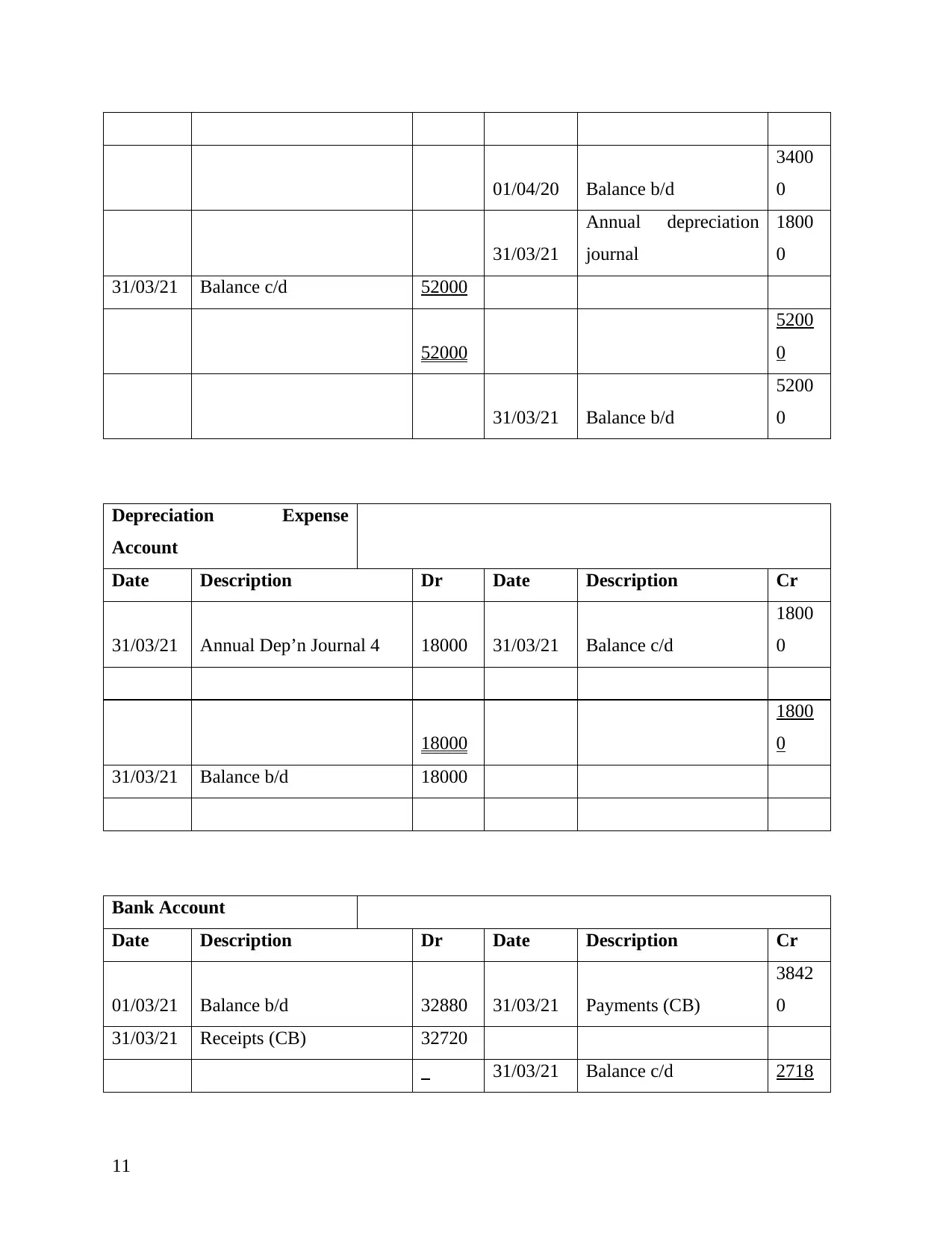

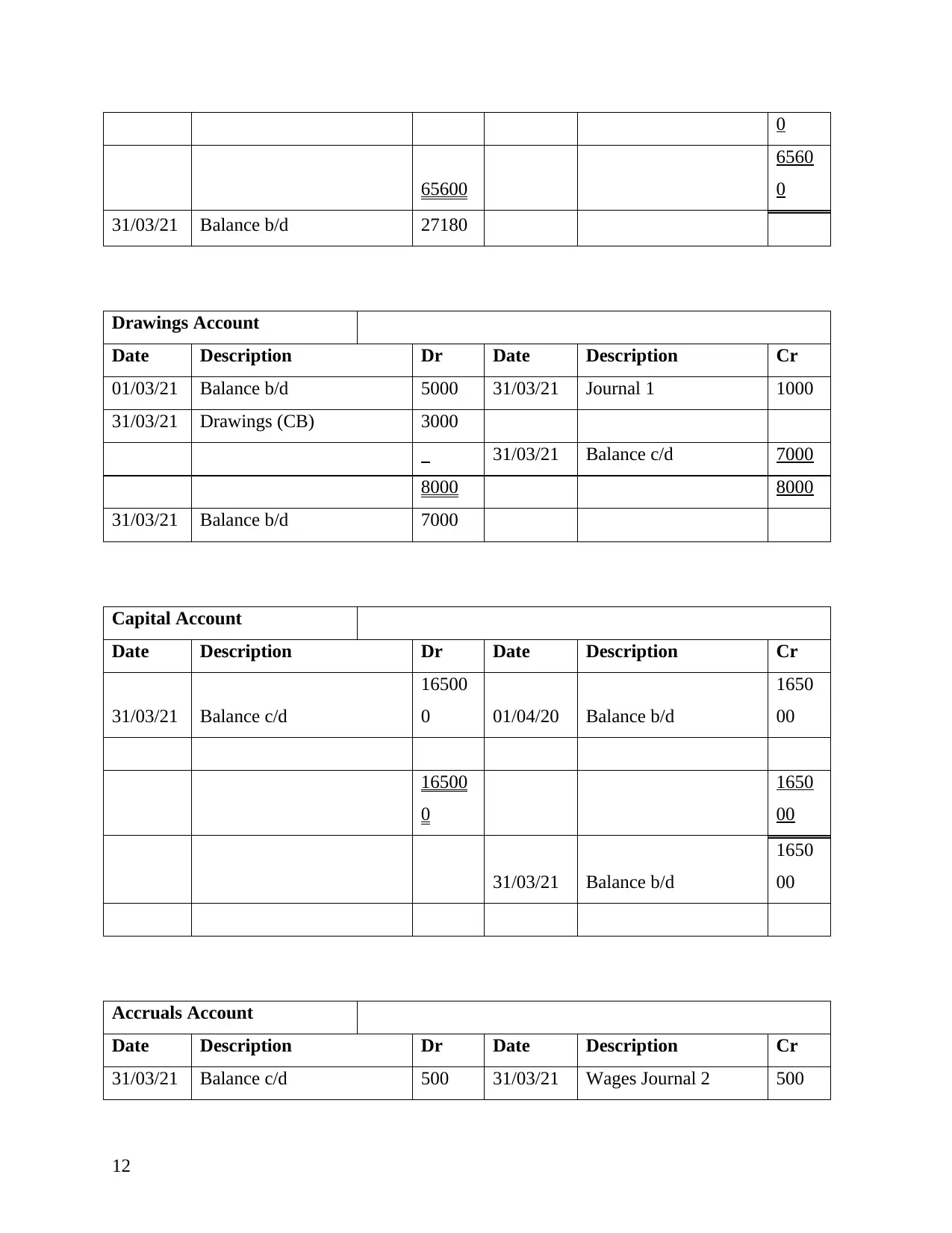

This financial accounting assignment analyzes various transactions that occurred in March 2021. It begins with an introduction to financial accounting, focusing on the summarization, evaluation, and reporting of a company's financial activities, including the use of Generally Accepted Accounting Principles (GAAP) and the importance of the prudence concept. The main body details various transactions such as credit and cash sales, credit purchases, purchase returns, cash receipts and payments, and equipment purchases. The assignment includes journal entries for all transactions, along with sales, purchases, and cash books. It presents trial balances, an income statement, and a statement of changes in financial position. The document also explains the prudence principle and its application in business. The analysis covers a comprehensive range of accounting activities, providing a detailed overview of financial statement preparation and analysis.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.