Preparing Financial Statements: Sole Trader Toy Retailer Business

VerifiedAdded on 2021/01/02

|18

|4919

|256

Homework Assignment

AI Summary

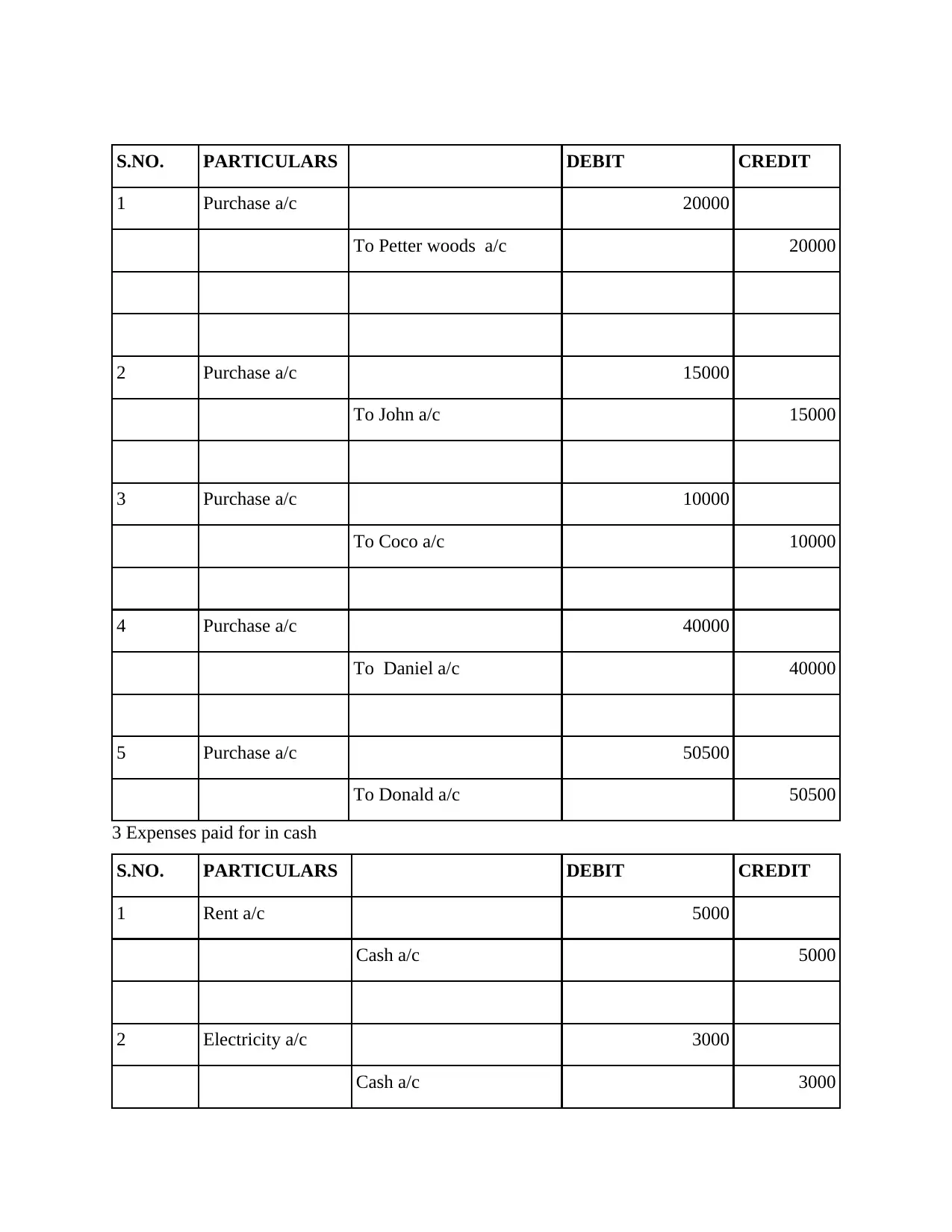

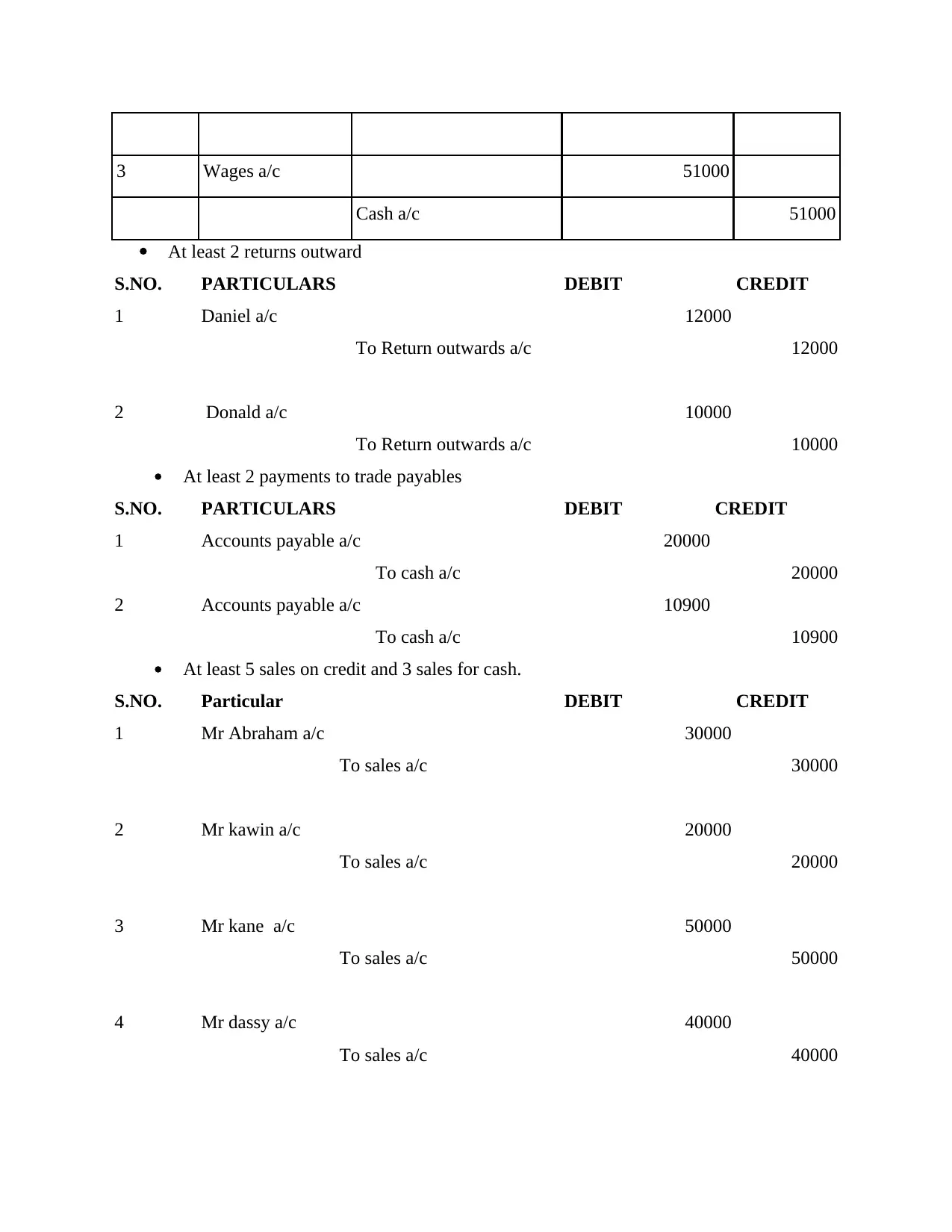

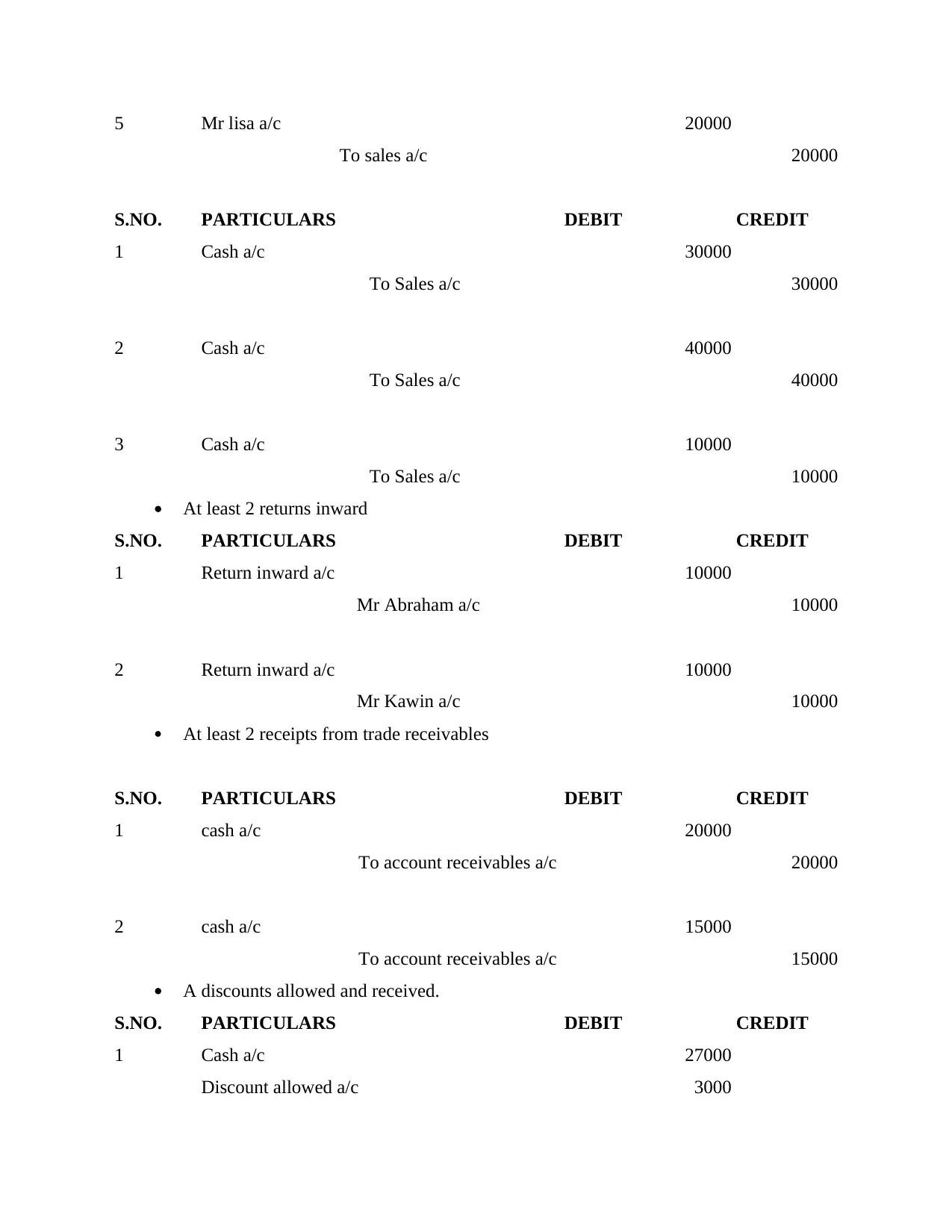

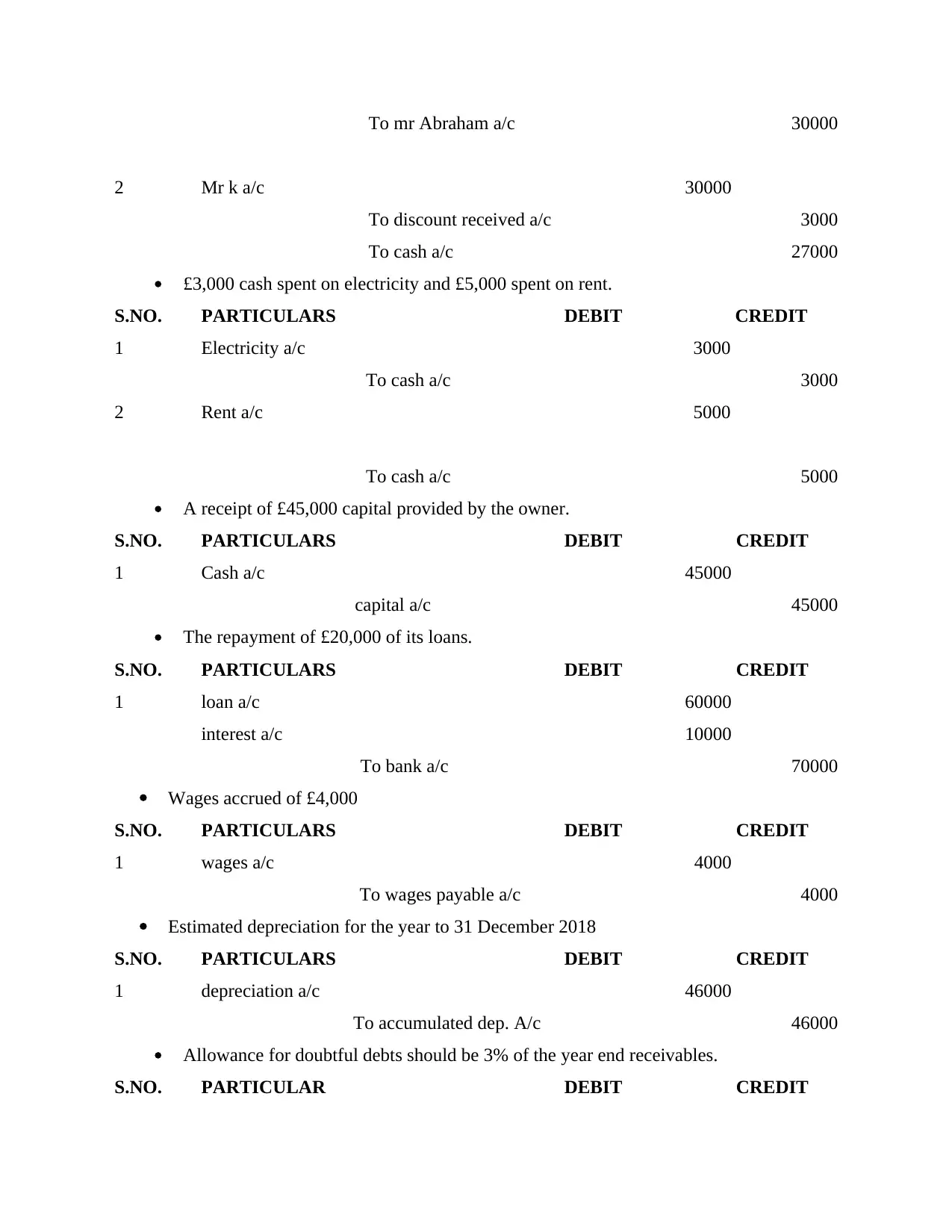

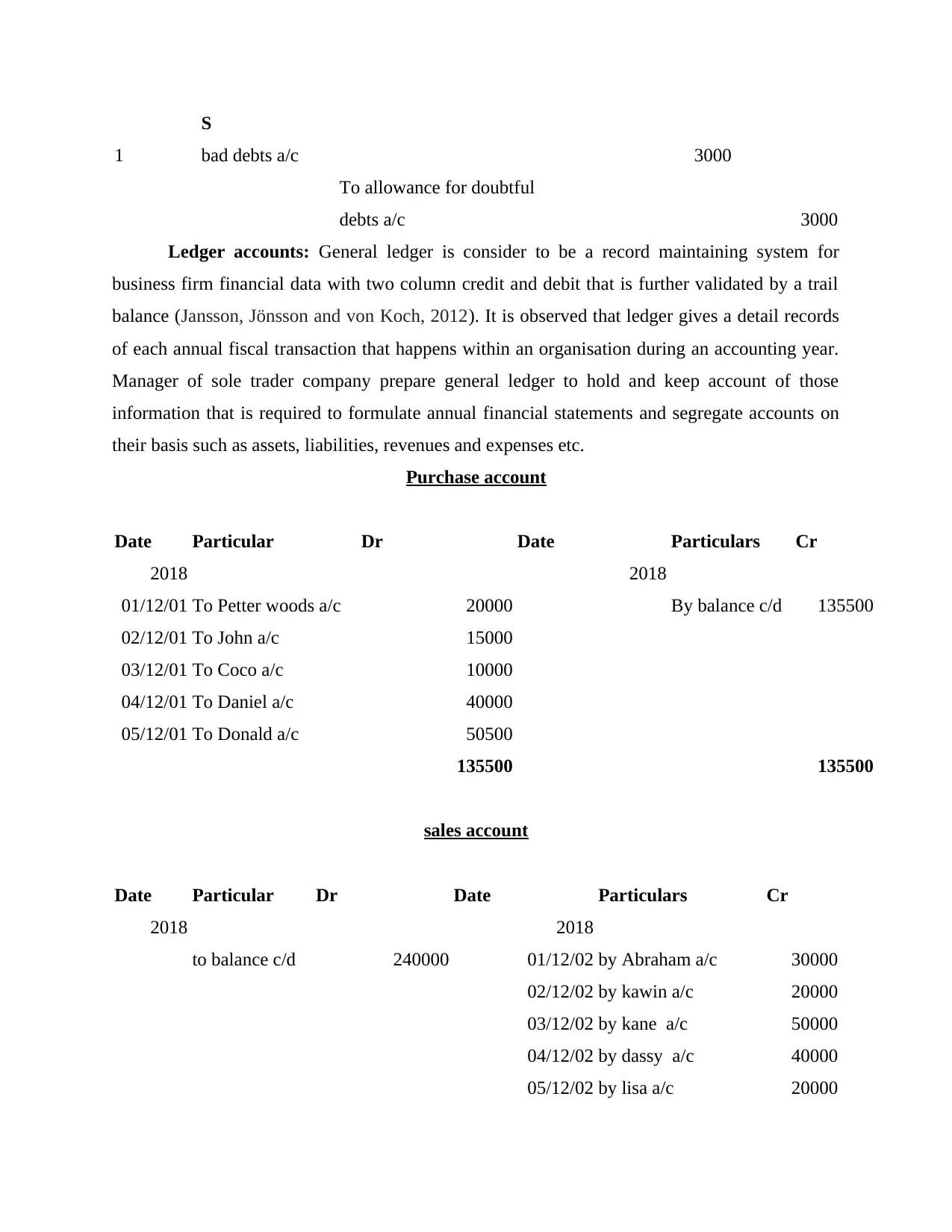

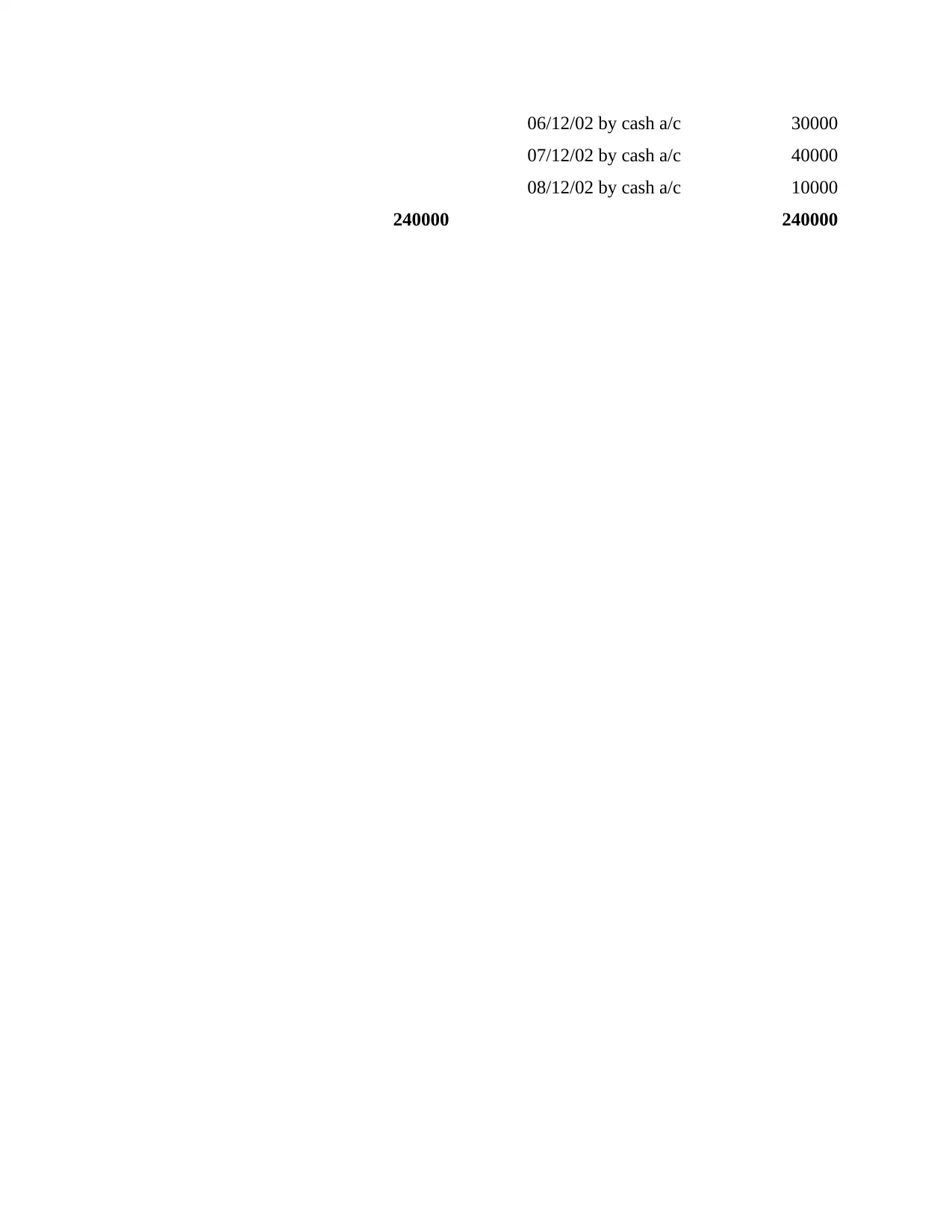

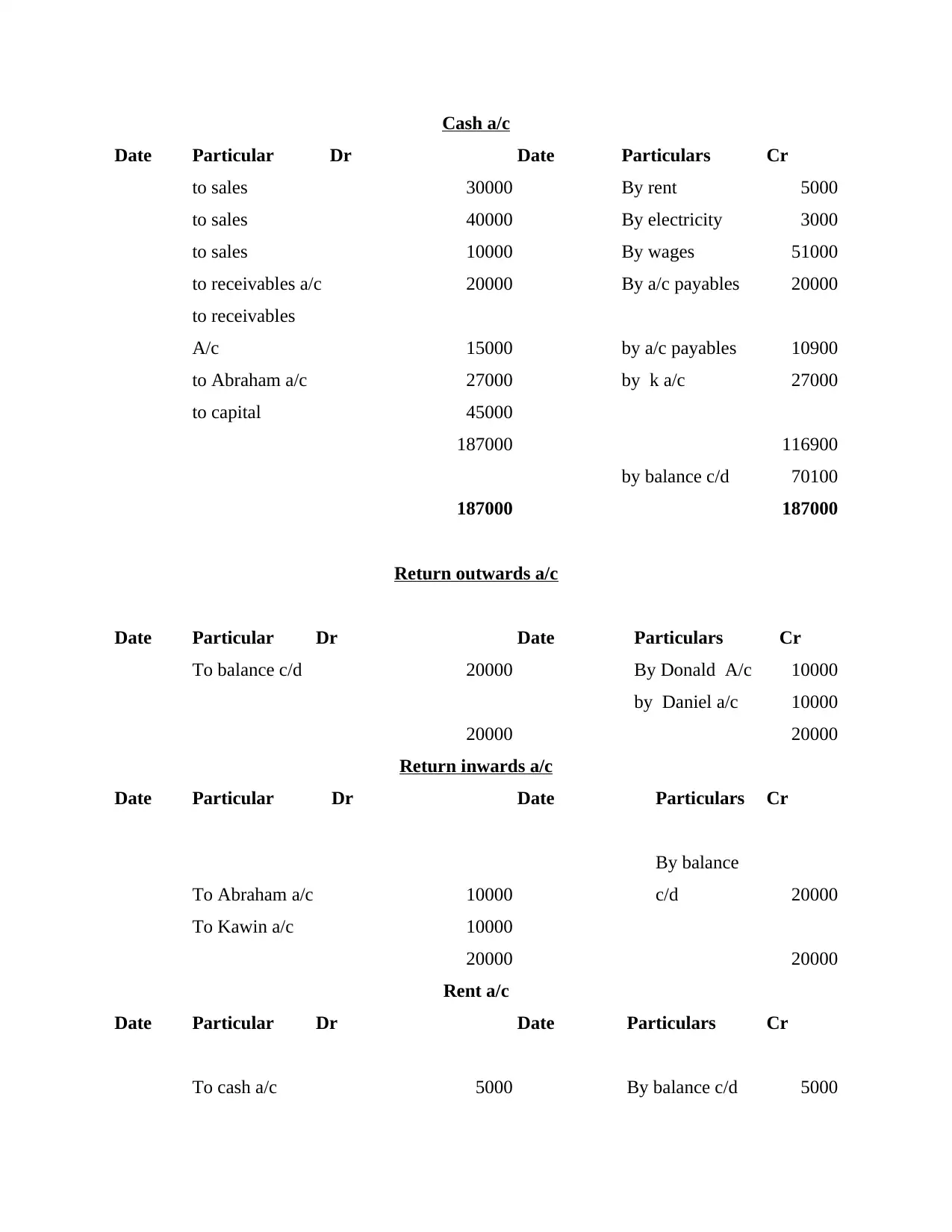

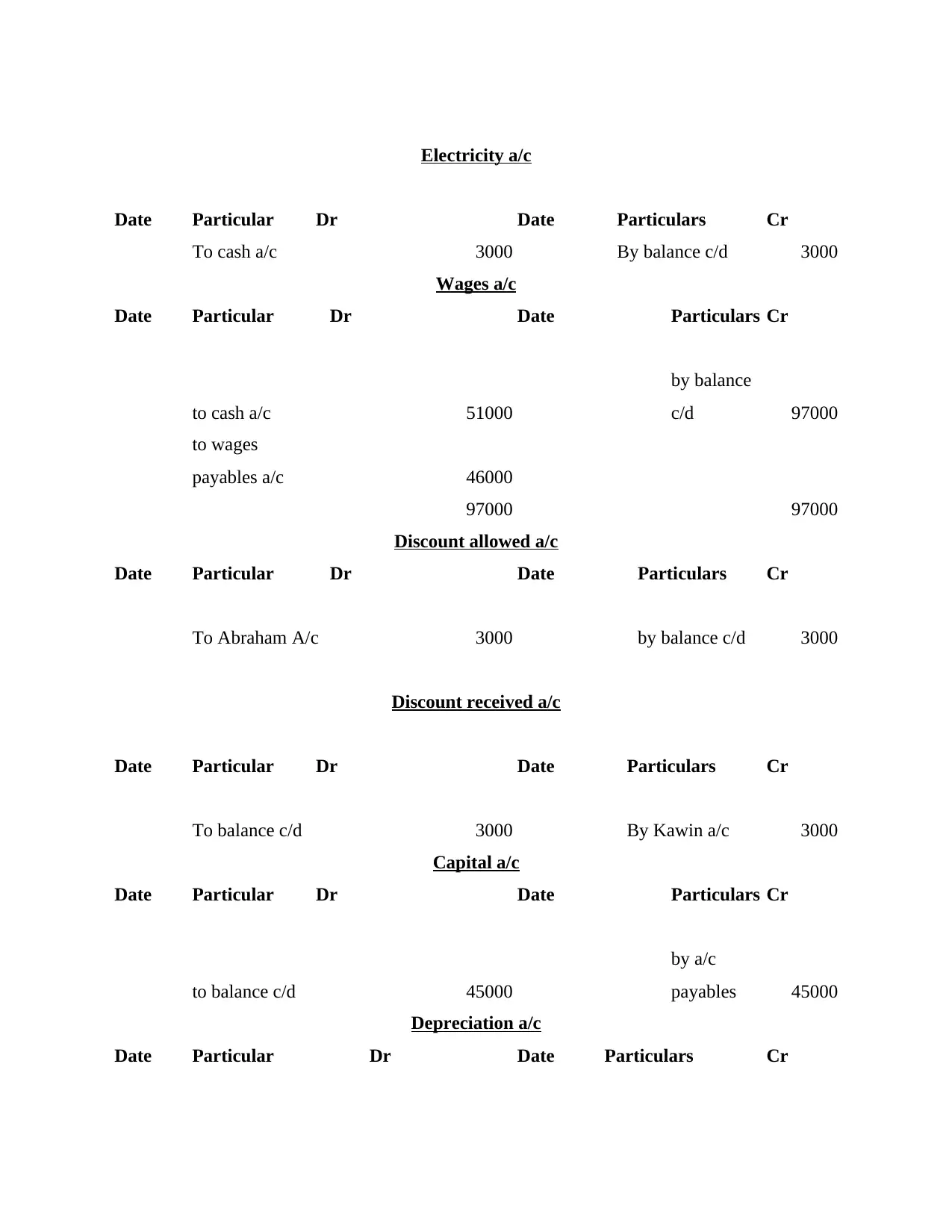

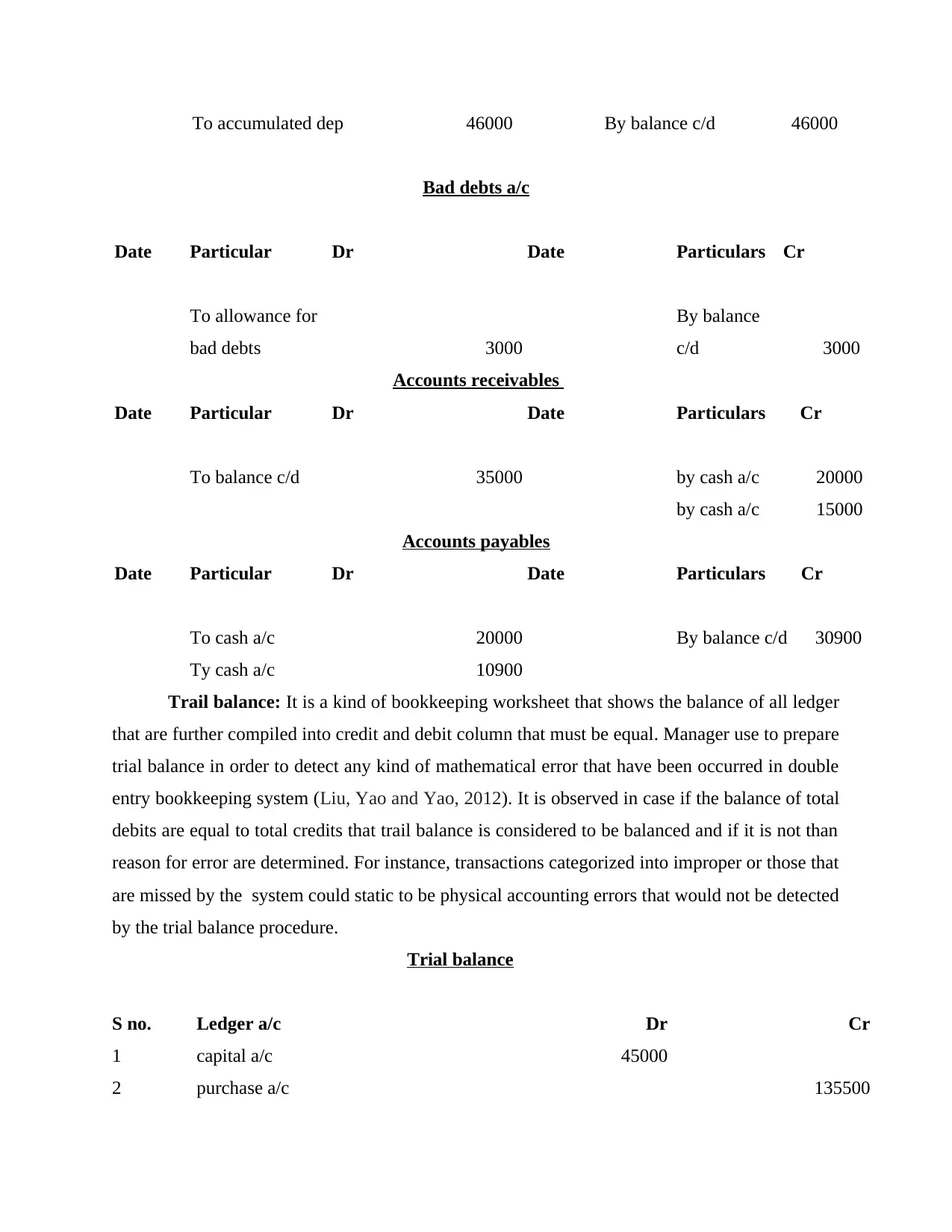

This assignment focuses on the financial accounting practices of a sole trader toy retailer named Conga. It begins with an introduction to financial accounting and its role in business decision-making, followed by the preparation of accounting records and financial statements, including journal entries, ledger accounts, and the creation of key financial reports. The assignment covers various transactions, such as purchases, sales, expenses, returns, payments, and receipts, along with adjustments for depreciation and doubtful debts. It also delves into the application of the prudence and accruals concepts, alongside the recording of Value Added Tax (VAT) in the accounting system. The solution demonstrates a comprehensive understanding of accounting principles and their practical application in a small business context, providing a detailed analysis of the financial performance and position of Conga. The assignment concludes with a summary of the key findings and a discussion of the importance of financial accounting for business management.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.