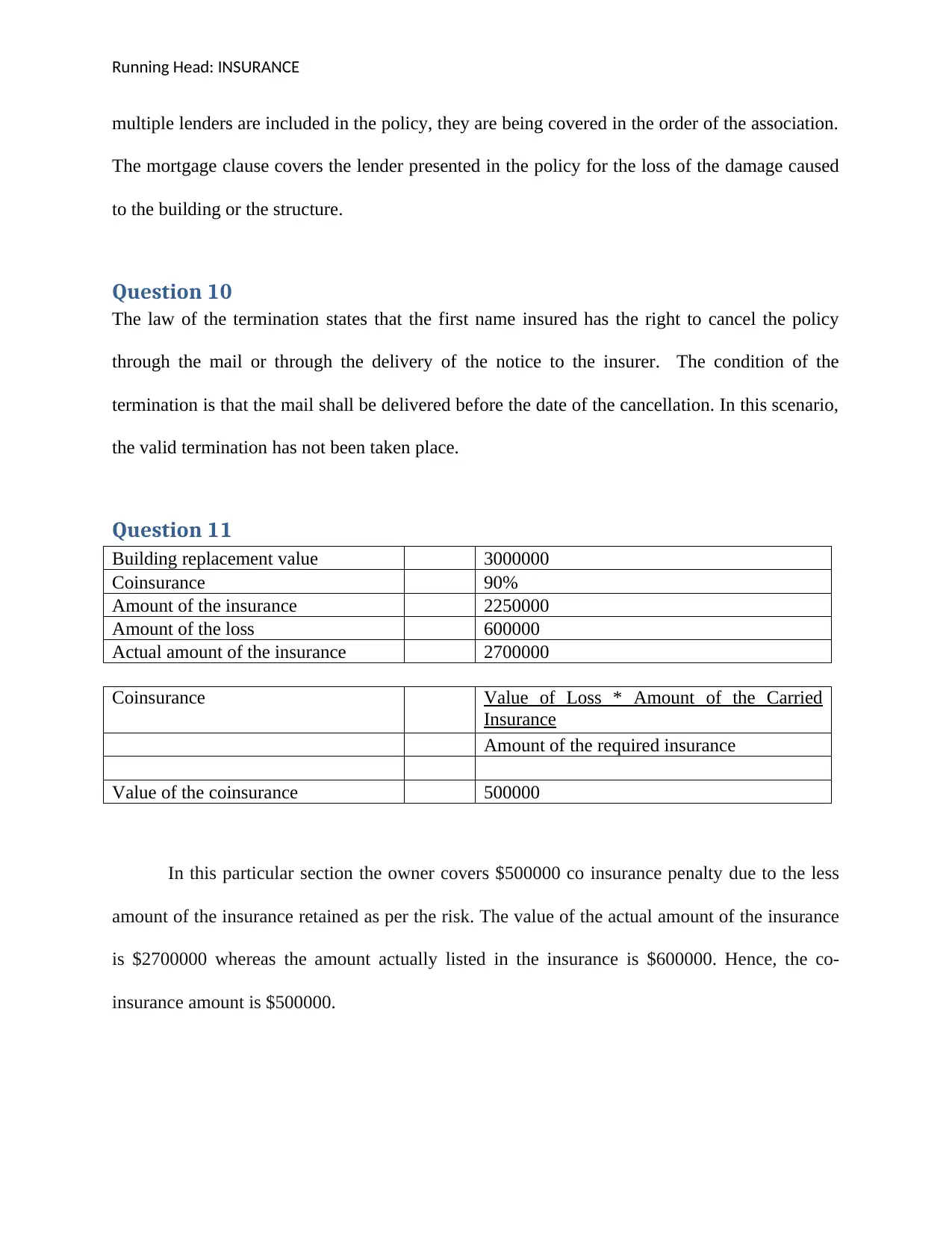

Comprehensive Assignment: FNSR2101 Introduction to Insurance

VerifiedAdded on 2022/10/10

|10

|1706

|20

Homework Assignment

AI Summary

This document presents a comprehensive solution to an insurance assignment for the FNSR2101 course, covering various aspects of insurance principles. Part I addresses insurable and non-insurable risks, providing examples such as rusting structures, genetic defects, cancer, computer obsolescence, and casino losses. Part II delves into contract validity, exploring scenarios of advertising as an invitation to treat and the liabilities of vehicle operation insurance. It also examines burglary insurance and the legal positions of insurers regarding policy coverage and exclusions. Part III addresses loss payee relationships, policy termination, and the coinsurance formula through case studies and scenarios. The assignment also includes a discussion on the Insurance Bureau of Canada's activities and their role in business insurance and risk management. The solution demonstrates an understanding of insurance concepts and their practical applications, along with relevant references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.