Introduction to Management Accounting: Costing, Budgeting, and JIT

VerifiedAdded on 2020/07/23

|14

|2756

|37

Report

AI Summary

This report provides an introduction to management accounting, detailing its role in organizations and differentiating it from financial accounting. It explores cost classification based on function, type, and behavior, including direct, indirect, fixed, variable, and stepped-fixed costs. The report critically analyzes the 'just-in-time' (JIT) inventory system, examining its advantages and disadvantages. It then evaluates the objectives of budgeting, including planning, communication, coordination, control, and efficiency, highlighting their importance in successful business operations. The report concludes that management accounting enhances internal efficiency and supports informed decision-making related to investments and business expansion.

INTRODUCTION TO

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Role of management accounting in the organisation and comparison with financial

accounting...............................................................................................................................1

2. Classification of cost by various terms...............................................................................2

3. Critically analysing 'just in time'........................................................................................5

4.Evaluating the objectives of budgeting...............................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

1. Role of management accounting in the organisation and comparison with financial

accounting...............................................................................................................................1

2. Classification of cost by various terms...............................................................................2

3. Critically analysing 'just in time'........................................................................................5

4.Evaluating the objectives of budgeting...............................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Index of Tables

Table 1: Differences between financial accounting and management accounting..........................2

Table 1: Differences between financial accounting and management accounting..........................2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration Index

Illustration 1: Fixed costs example..................................................................................................4

Illustration 2: Example of variable cost...........................................................................................4

Illustration 3: Example of Stepped Fixed costs...............................................................................5

Illustration 4: Just- in- time elements...............................................................................................6

Illustration 1: Fixed costs example..................................................................................................4

Illustration 2: Example of variable cost...........................................................................................4

Illustration 3: Example of Stepped Fixed costs...............................................................................5

Illustration 4: Just- in- time elements...............................................................................................6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting at the initial stage used for making fruitful decisions for

business. By undertaking the tools and techniques of management accounting higher level

managers can assess the areas that demand for cost control. Thus, managerial accounting reports

offer detailed information to the managers and help in taking strategic move that contributes in

the growth and success of business unit. In the present report there will be discussion based on

various managements accounting terms such as costing, budgeting which in turn helps the

organisation in improving the capital structure as well as enchaining the efficiency.

1. Role of management accounting in the organisation and comparison with financial accounting

The main objectives of management accounting in the business is to enhance the

competitive decision making with the help of collecting informations, analysing and measuring

them as well as communicating the end results to the top level managers or heads of the entity.

Hence, such data set will help in making adequate managerial decisions, Long term and short

term planning, budgets and costs over any operational activities (Hemmer and Labro, 2016).

However, such strategic planning helps them in enhancing the operational activities such

production, marketing, innovations, research and development as well as selling and distribution.

Other than operational activities the management accounting also helps in monitoring the

workforce efforts as well as performance done by them. It helps the managers to identify the

requirements of employees for the tasks or business activities as well as managing their pay-offs

which will be in accordance with their qualification and talent. Hence, it has the huge difference

in terms of making the adequate managements of the operations held in the premises as well as

controlling the costs or budgets for such business operations.

Moreover, the management accounting is the useful terms in context with analysing the

financial reports of the organisation such as income statement, balance sheet, cash flows and

various ratio analysis (Weetman, 2016). Hence, the functioning of management accounting is

quite different from the financial accounting. Thus, it can be understand by the help of below

listed table such as:

1

Management accounting at the initial stage used for making fruitful decisions for

business. By undertaking the tools and techniques of management accounting higher level

managers can assess the areas that demand for cost control. Thus, managerial accounting reports

offer detailed information to the managers and help in taking strategic move that contributes in

the growth and success of business unit. In the present report there will be discussion based on

various managements accounting terms such as costing, budgeting which in turn helps the

organisation in improving the capital structure as well as enchaining the efficiency.

1. Role of management accounting in the organisation and comparison with financial accounting

The main objectives of management accounting in the business is to enhance the

competitive decision making with the help of collecting informations, analysing and measuring

them as well as communicating the end results to the top level managers or heads of the entity.

Hence, such data set will help in making adequate managerial decisions, Long term and short

term planning, budgets and costs over any operational activities (Hemmer and Labro, 2016).

However, such strategic planning helps them in enhancing the operational activities such

production, marketing, innovations, research and development as well as selling and distribution.

Other than operational activities the management accounting also helps in monitoring the

workforce efforts as well as performance done by them. It helps the managers to identify the

requirements of employees for the tasks or business activities as well as managing their pay-offs

which will be in accordance with their qualification and talent. Hence, it has the huge difference

in terms of making the adequate managements of the operations held in the premises as well as

controlling the costs or budgets for such business operations.

Moreover, the management accounting is the useful terms in context with analysing the

financial reports of the organisation such as income statement, balance sheet, cash flows and

various ratio analysis (Weetman, 2016). Hence, the functioning of management accounting is

quite different from the financial accounting. Thus, it can be understand by the help of below

listed table such as:

1

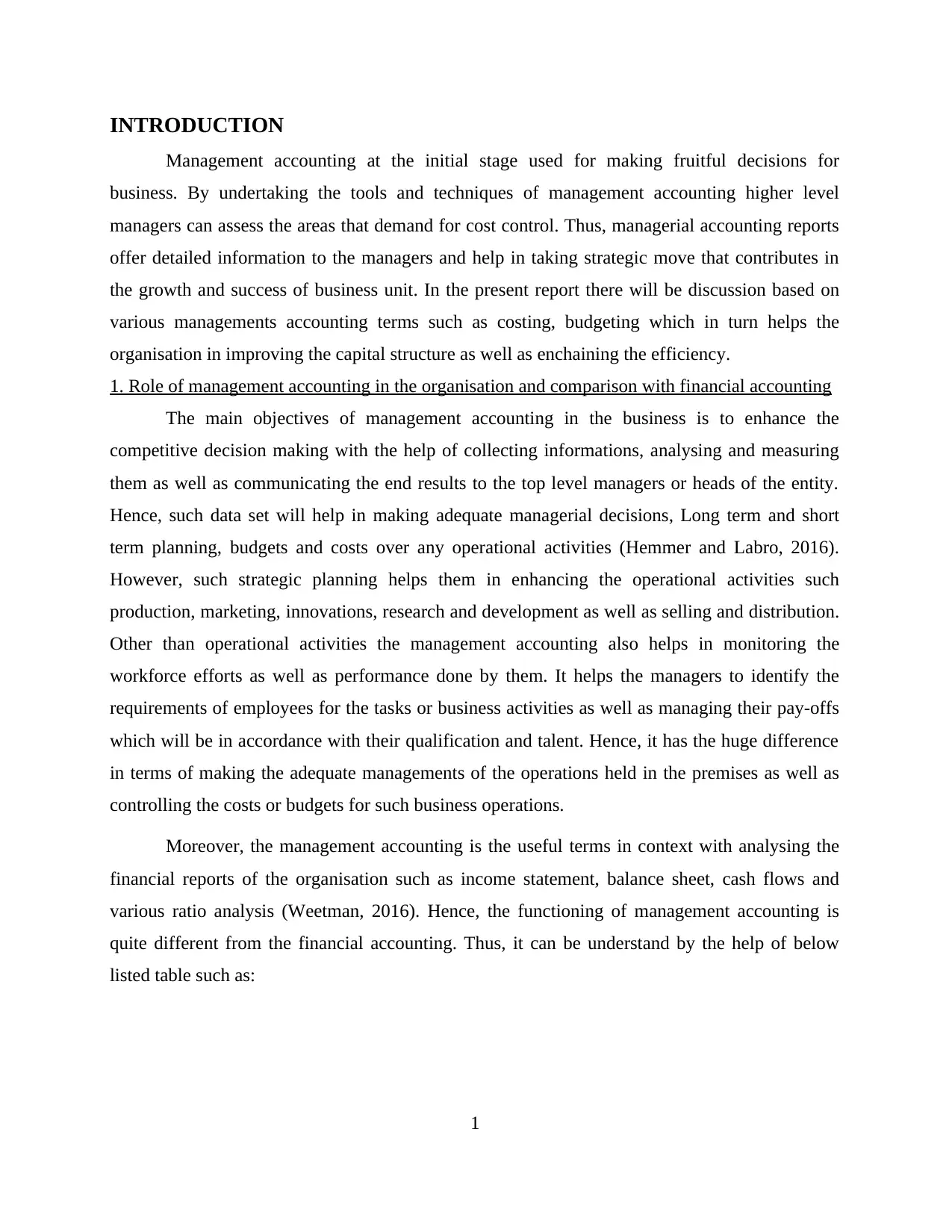

Basis Financial accounting Management accounting

Objective Presenting the financial position of

the business

Analysing the inner functional areas

and helps in decision making.

Users External users such as shareholders,

investors, regulators, taxation

authority, government etc.

Internal users such as managers,

directors, owners and the planning

and development heads.

Scope On the wide level such as

investment, expansion etc.

Narrow level, focuses over the

production, costing and budgeting.

Principles and

governance

Framework and norms set by GAAP,

IFRS and IASB.

There is no such rules or framework,

usually analysed by accountants or

other managerial heads.

Information It usually uses the qualitative data

(Lanen, 2016).

There will be use of qualitative and

quantitative concept.

Table 1: Differences between financial accounting and management accounting

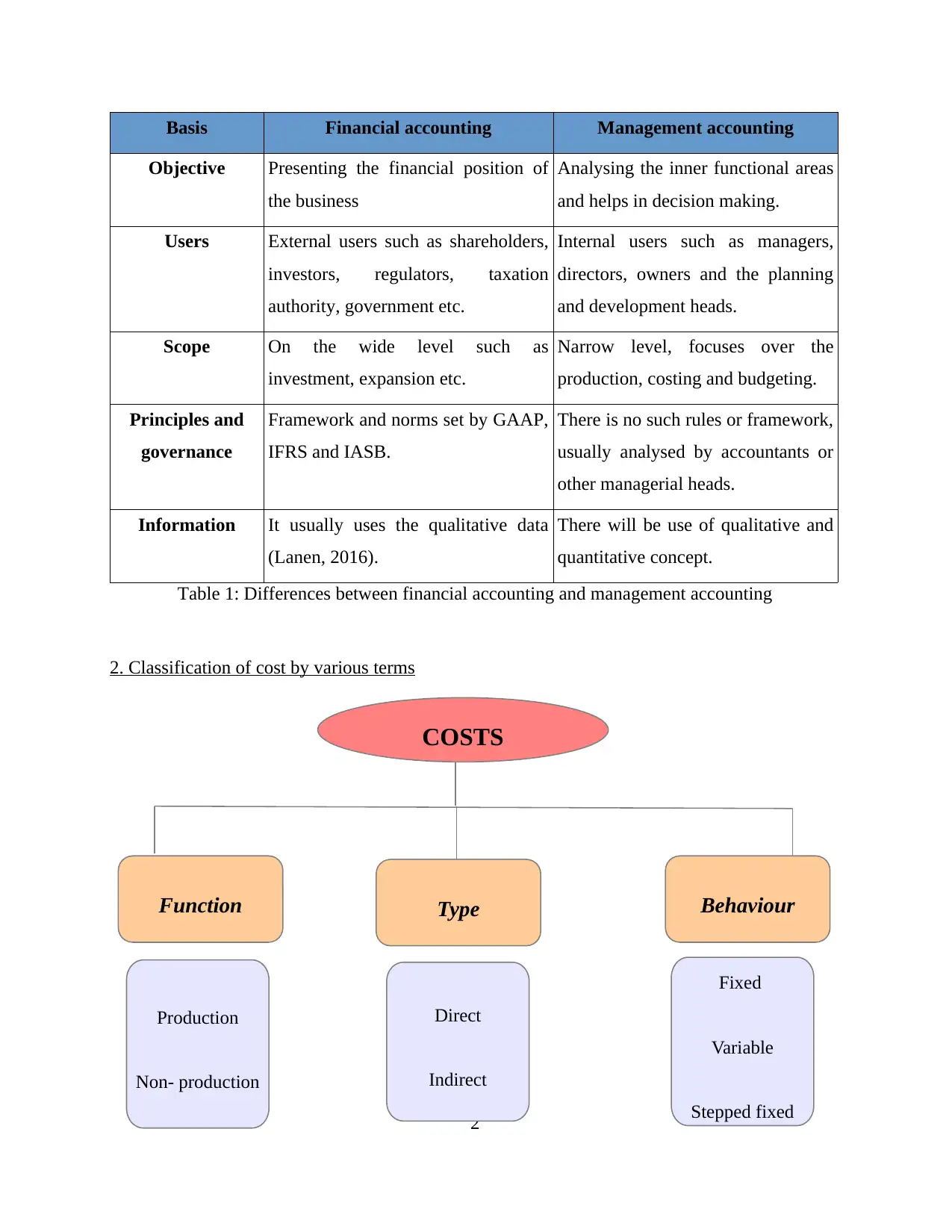

2. Classification of cost by various terms

2

COSTS

TypeFunction Behaviour

Production

Non- production

Direct

Indirect

Fixed

Variable

Stepped fixed

Objective Presenting the financial position of

the business

Analysing the inner functional areas

and helps in decision making.

Users External users such as shareholders,

investors, regulators, taxation

authority, government etc.

Internal users such as managers,

directors, owners and the planning

and development heads.

Scope On the wide level such as

investment, expansion etc.

Narrow level, focuses over the

production, costing and budgeting.

Principles and

governance

Framework and norms set by GAAP,

IFRS and IASB.

There is no such rules or framework,

usually analysed by accountants or

other managerial heads.

Information It usually uses the qualitative data

(Lanen, 2016).

There will be use of qualitative and

quantitative concept.

Table 1: Differences between financial accounting and management accounting

2. Classification of cost by various terms

2

COSTS

TypeFunction Behaviour

Production

Non- production

Direct

Indirect

Fixed

Variable

Stepped fixed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Classification of cost on the basis of function

Production: These are the costs which can be known as those costs which are other than

the manufacturing and factory overheads costs. Basically these are the costs which indirectly

levied over the process of manufacturing a unit such as indirect material, labour, wages to

managers or supervisors, electricity charges, insurance and other factory costs (Manufacturing

and non-manufacturing costs, 2012).

Non-production: This are the costs which have to be beard by manufacturing units thus,

these costs are indirectly affecting the operational functions of the business. Hence, these costs

includes the various expenses such as Marketing or advertising cots which are used to promote

the products or brand of the organisation. Selling and distribution expenses such as transportation

of goods and services (Hemmer and Labro, 2016). The administrative costs of the business which

includes warehouse expenses such as storage and use of various machineries for the perishable

nature of goods. However, such costs can be known as the by-production costs of business which

are not included in the manufacturing of a unit but these are helpful in delivering such products

to the end users (Bennett and James, eds., 2017).

Classification of cost on the basis of types:

Direct: These are the costs which are directly implicated over the production of the goods

and services such as direct labour, material and fewer expenses. However, this are the essential

expenditures which were used in production function as well as at the initial level of the

operational area of entity such as purchase of material, recruitment of the staff members, salary

or compensation to workers as well as selling and distributing goods (Uyar and Kuzey, 2016).

Indirect: These expenses incurred indirectly over the manufacturing a unit such as rent,

electricity, maintenance, repairs, heating charges etc.

Classification of cost on the basis of behaviour

3

Production: These are the costs which can be known as those costs which are other than

the manufacturing and factory overheads costs. Basically these are the costs which indirectly

levied over the process of manufacturing a unit such as indirect material, labour, wages to

managers or supervisors, electricity charges, insurance and other factory costs (Manufacturing

and non-manufacturing costs, 2012).

Non-production: This are the costs which have to be beard by manufacturing units thus,

these costs are indirectly affecting the operational functions of the business. Hence, these costs

includes the various expenses such as Marketing or advertising cots which are used to promote

the products or brand of the organisation. Selling and distribution expenses such as transportation

of goods and services (Hemmer and Labro, 2016). The administrative costs of the business which

includes warehouse expenses such as storage and use of various machineries for the perishable

nature of goods. However, such costs can be known as the by-production costs of business which

are not included in the manufacturing of a unit but these are helpful in delivering such products

to the end users (Bennett and James, eds., 2017).

Classification of cost on the basis of types:

Direct: These are the costs which are directly implicated over the production of the goods

and services such as direct labour, material and fewer expenses. However, this are the essential

expenditures which were used in production function as well as at the initial level of the

operational area of entity such as purchase of material, recruitment of the staff members, salary

or compensation to workers as well as selling and distributing goods (Uyar and Kuzey, 2016).

Indirect: These expenses incurred indirectly over the manufacturing a unit such as rent,

electricity, maintenance, repairs, heating charges etc.

Classification of cost on the basis of behaviour

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed: The expenses which are charging the fixed or constant charges over the goods and

services which have the fixed amount such as rent, telephone bills and the interest paid over any

loan or investments.

Illustration 1: Fixed costs example

Variable: These are the fluctuating and changing costs of the organisation which in turn

changes in accordance with the changing requirements and wants of consumers as well as

demands in the market. However, this includes selling and distribution charges, material

purchasing and selling charges etc.

Illustration 2: Example of variable cost

4

services which have the fixed amount such as rent, telephone bills and the interest paid over any

loan or investments.

Illustration 1: Fixed costs example

Variable: These are the fluctuating and changing costs of the organisation which in turn

changes in accordance with the changing requirements and wants of consumers as well as

demands in the market. However, this includes selling and distribution charges, material

purchasing and selling charges etc.

Illustration 2: Example of variable cost

4

Stepped Fixed: This costs are fixed in nature but at the time of certain events it reflects

the bulls in the prices of costs and then again stabilised for some period. There may be increase

or decrease of the prices and costs which in turn affect the manufacturing costs of the business.

Illustration 3: Example of Stepped Fixed costs

Source: (Step fixed cost, 2013)

3. Critically analysing 'just in time'

In accordance with Hirano, (2016), In order to make the sale of a good or services there is

need to make the adequate assumption about the demand to be generated by organisation. Thus,

after analysing requirements of products in market than the plans or decisions were made in

accordance with manufacturing such units. Hence, in this case the products were produced as

according to requirements of clients as well as per their satisfactory level. In context with the

Filippini and Forza, (2016), these systems helps in lowering down the carrying costs as well as

wastage incurred due to making storage of Inventories. Hence, with the help of such technique or

strategy the managers or professionals in business will have lower costs and have the adequate

returns over their investments.

Jung and et.al., (2016) criticised that, If there is no storage of adequate amount of

inventory than due to peek demand the business will not be able to meet such market

requirements which in turn affects the profitability as well as goodwill reputation of the firm.

Consumers will be dissatisfied and make switch to the another industry who fulfil their

5

the bulls in the prices of costs and then again stabilised for some period. There may be increase

or decrease of the prices and costs which in turn affect the manufacturing costs of the business.

Illustration 3: Example of Stepped Fixed costs

Source: (Step fixed cost, 2013)

3. Critically analysing 'just in time'

In accordance with Hirano, (2016), In order to make the sale of a good or services there is

need to make the adequate assumption about the demand to be generated by organisation. Thus,

after analysing requirements of products in market than the plans or decisions were made in

accordance with manufacturing such units. Hence, in this case the products were produced as

according to requirements of clients as well as per their satisfactory level. In context with the

Filippini and Forza, (2016), these systems helps in lowering down the carrying costs as well as

wastage incurred due to making storage of Inventories. Hence, with the help of such technique or

strategy the managers or professionals in business will have lower costs and have the adequate

returns over their investments.

Jung and et.al., (2016) criticised that, If there is no storage of adequate amount of

inventory than due to peek demand the business will not be able to meet such market

requirements which in turn affects the profitability as well as goodwill reputation of the firm.

Consumers will be dissatisfied and make switch to the another industry who fulfil their

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

requirements. Xu and Chen, (2016) insists that, this strategy will be beneficial in having

maximum returns over the investments of costs of production. Thus, there will not be that must

charges which are incurred in the manufacturing of the units on regular basis such as rent of the

storage home, electricity charges will be less, lower labour charges, low maintenance cots as well

as business will save such time in making the other operational plans for the future. Hence, it will

be fruitful in enhancing the efficiency of the business as well as optimum utilisations off

resources such as man material and machinery on such time.

Illustration 4: Just- in- time elements

Source: (What is just in time? Definition and meaning, 2017)

In context with Arifuddin and Kusumawati, (2017), This production systems will be

helpful in the case of lowering the down the wastage as well as costs but in the case of having the

excessive demand in the market there can be use of excessive amount of finance in order to

purchase the material. The process of such raw material will be fluctuating and it will be charged

6

maximum returns over the investments of costs of production. Thus, there will not be that must

charges which are incurred in the manufacturing of the units on regular basis such as rent of the

storage home, electricity charges will be less, lower labour charges, low maintenance cots as well

as business will save such time in making the other operational plans for the future. Hence, it will

be fruitful in enhancing the efficiency of the business as well as optimum utilisations off

resources such as man material and machinery on such time.

Illustration 4: Just- in- time elements

Source: (What is just in time? Definition and meaning, 2017)

In context with Arifuddin and Kusumawati, (2017), This production systems will be

helpful in the case of lowering the down the wastage as well as costs but in the case of having the

excessive demand in the market there can be use of excessive amount of finance in order to

purchase the material. The process of such raw material will be fluctuating and it will be charged

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

more to business. Hence, in terms or following such techniques then there is need to have the

operations which are belongs to the stable priced raw material such as steel, iron etc. For

instance, an automotive corporation will manufacture the vehicles as according to the demands in

the markets as well as requirements of buyers, in this case Just in time management systems will

be fruitful. While in case of food and beverages such techniques will not make any profitable

returns. Thus, there will be increase and decrease in demand with the sudden changes of sudden

requirements.

4.Evaluating the objectives of budgeting

To make the successful business operations s well as have the adequate funds for each

organisational operations managers in firm make plans and budgets to meet the requirements of

cots for such piece of work as well as demonstrate such requirements. However, there will be

various objectives of planning a budget of the business operations such as manufacturing,

purchasing, selling, marketing etc. Hence, this helps entity in enchaining the efficiency as well as

adequate utilisation of the resources. Therefore, there are many objectives of Budgets in the

organisation which can be evaluated as follows: Planning: The budgets were made in accordance with the previous outcomes and the

results of such past performances. However, the main objective or the initial stage of the

budget are based on the effective planning. It includes analysing the actual strength of the

firm as well as requirements or goals of the business. Thus, with the help of such

informations the team or professional generate new ideas and set procedure to implement

such changes such as presenting the idea, setting target, directing the workforce and make

the adequate budgetary control system. Communicating the thoughts and ideas: In terms of implementing such budget plans the

objective lies over communicating such ideas to the stakeholders in the firm such as

employees, managers, supervisors, directors and the owners. Thus, it will help in making

the adequate execution of such plans in the right track (Taylor and et.al., 2017). Building coordination:The coordination and collaboration of the workforces in the

premises will lead the successful operations of such plans. Hence, such techniques helps

in connecting all the units of the organisation as well as helps in presenting the

7

operations which are belongs to the stable priced raw material such as steel, iron etc. For

instance, an automotive corporation will manufacture the vehicles as according to the demands in

the markets as well as requirements of buyers, in this case Just in time management systems will

be fruitful. While in case of food and beverages such techniques will not make any profitable

returns. Thus, there will be increase and decrease in demand with the sudden changes of sudden

requirements.

4.Evaluating the objectives of budgeting

To make the successful business operations s well as have the adequate funds for each

organisational operations managers in firm make plans and budgets to meet the requirements of

cots for such piece of work as well as demonstrate such requirements. However, there will be

various objectives of planning a budget of the business operations such as manufacturing,

purchasing, selling, marketing etc. Hence, this helps entity in enchaining the efficiency as well as

adequate utilisation of the resources. Therefore, there are many objectives of Budgets in the

organisation which can be evaluated as follows: Planning: The budgets were made in accordance with the previous outcomes and the

results of such past performances. However, the main objective or the initial stage of the

budget are based on the effective planning. It includes analysing the actual strength of the

firm as well as requirements or goals of the business. Thus, with the help of such

informations the team or professional generate new ideas and set procedure to implement

such changes such as presenting the idea, setting target, directing the workforce and make

the adequate budgetary control system. Communicating the thoughts and ideas: In terms of implementing such budget plans the

objective lies over communicating such ideas to the stakeholders in the firm such as

employees, managers, supervisors, directors and the owners. Thus, it will help in making

the adequate execution of such plans in the right track (Taylor and et.al., 2017). Building coordination:The coordination and collaboration of the workforces in the

premises will lead the successful operations of such plans. Hence, such techniques helps

in connecting all the units of the organisation as well as helps in presenting the

7

beneficiary results. Thus, these in turn helps in managing the sales expectations,

productions requirement as well as purchasing of the goods for such activities. Controlling: If there is any loophole and inadequacy in the performance of budgets than

there is need to make the changes in such plans. Hence, it will be helpful for managers or

supervisor to make the proper control or execution of whole work process in the adequate

manner.

Provoke work efficiency: Employees of the organisation will be highly motivated and

enthusiastically follow the instructions and make their efforts for such business targets.

Hence, they will become able to perform their duties and tasks in correct manners and

play the main role in profitability earning for industry (Arifuddin and Kusumawati, 2017).

CONCLUSION

On the basis of this report it can be concluded that management accounting plays the

crucial role in enhancing the internal ability or firm as well as enhancing the efficiency of the

workforce. Thus, with the help of various costing techniques and budget objectives, organisation

will be beneficial in making investment decisions as well as plan to make expansion for the

business or operations in the premises. The report describes various elements of Just in time

inventory control system which will be fruitful for reducing the costs of the business as well as

helps in generating the adequate returns over such investments.

8

productions requirement as well as purchasing of the goods for such activities. Controlling: If there is any loophole and inadequacy in the performance of budgets than

there is need to make the changes in such plans. Hence, it will be helpful for managers or

supervisor to make the proper control or execution of whole work process in the adequate

manner.

Provoke work efficiency: Employees of the organisation will be highly motivated and

enthusiastically follow the instructions and make their efforts for such business targets.

Hence, they will become able to perform their duties and tasks in correct manners and

play the main role in profitability earning for industry (Arifuddin and Kusumawati, 2017).

CONCLUSION

On the basis of this report it can be concluded that management accounting plays the

crucial role in enhancing the internal ability or firm as well as enhancing the efficiency of the

workforce. Thus, with the help of various costing techniques and budget objectives, organisation

will be beneficial in making investment decisions as well as plan to make expansion for the

business or operations in the premises. The report describes various elements of Just in time

inventory control system which will be fruitful for reducing the costs of the business as well as

helps in generating the adequate returns over such investments.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.