Management Accounting: Costing Methods and Analysis Solutions

VerifiedAdded on 2021/06/17

|13

|2655

|23

Homework Assignment

AI Summary

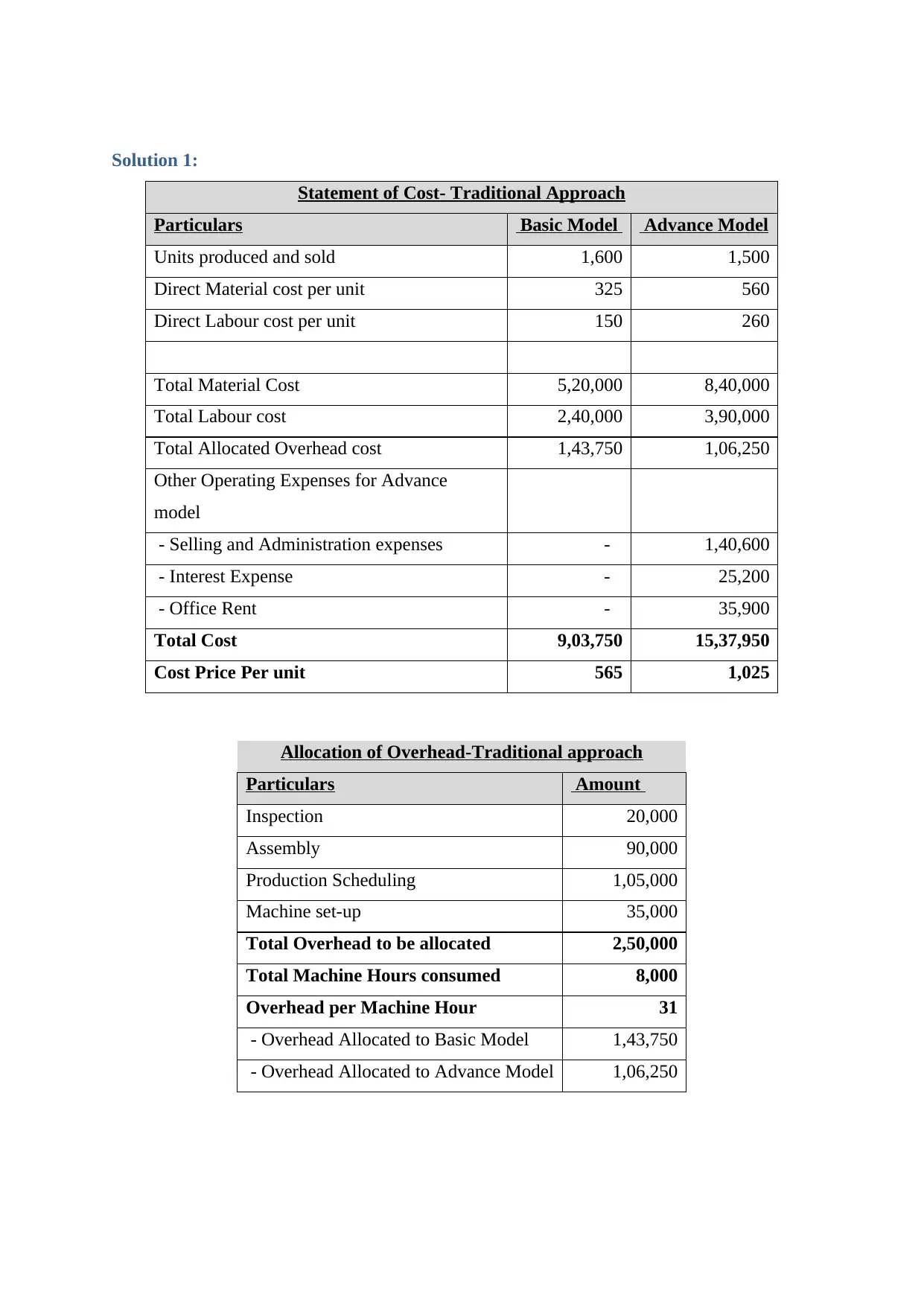

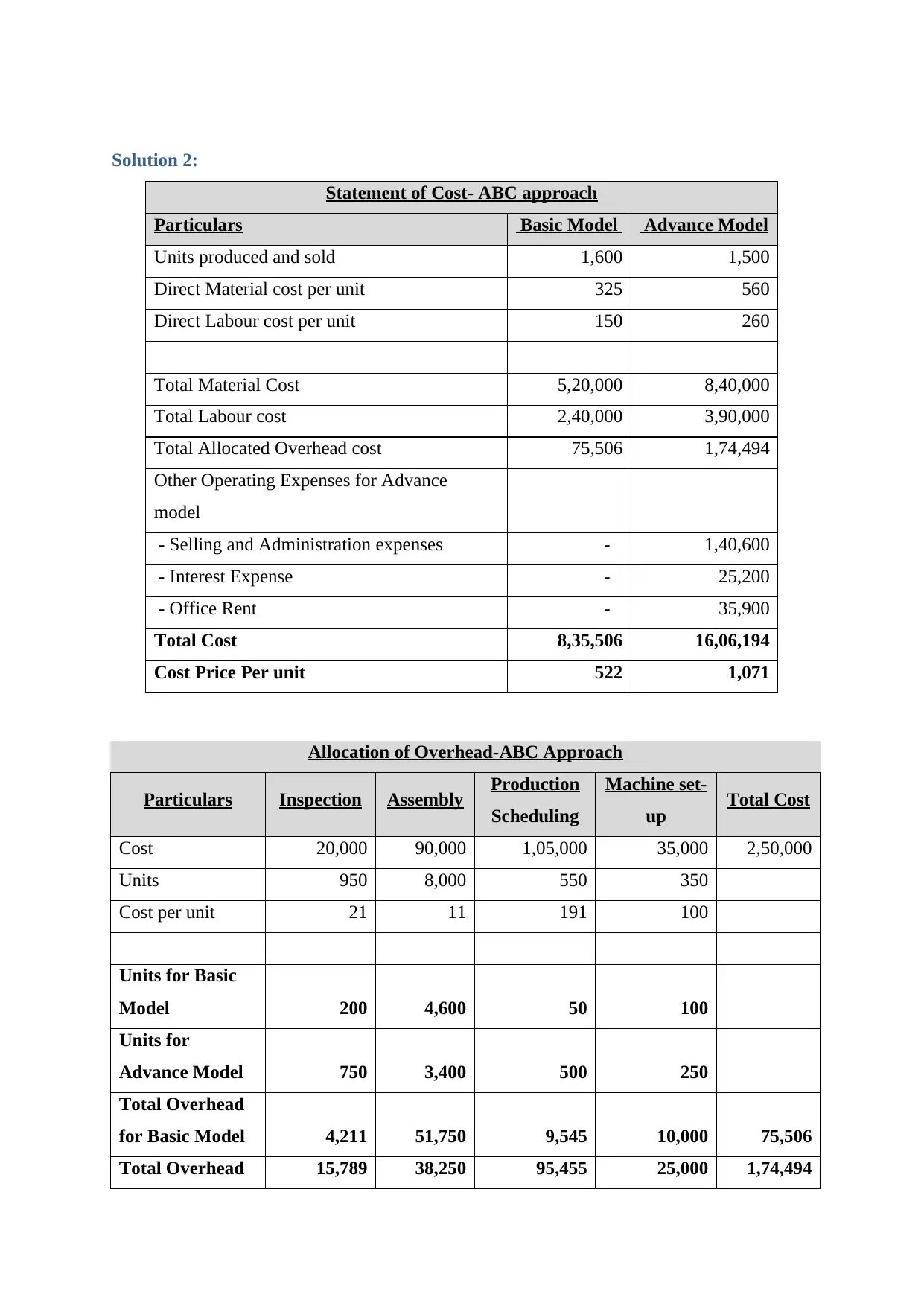

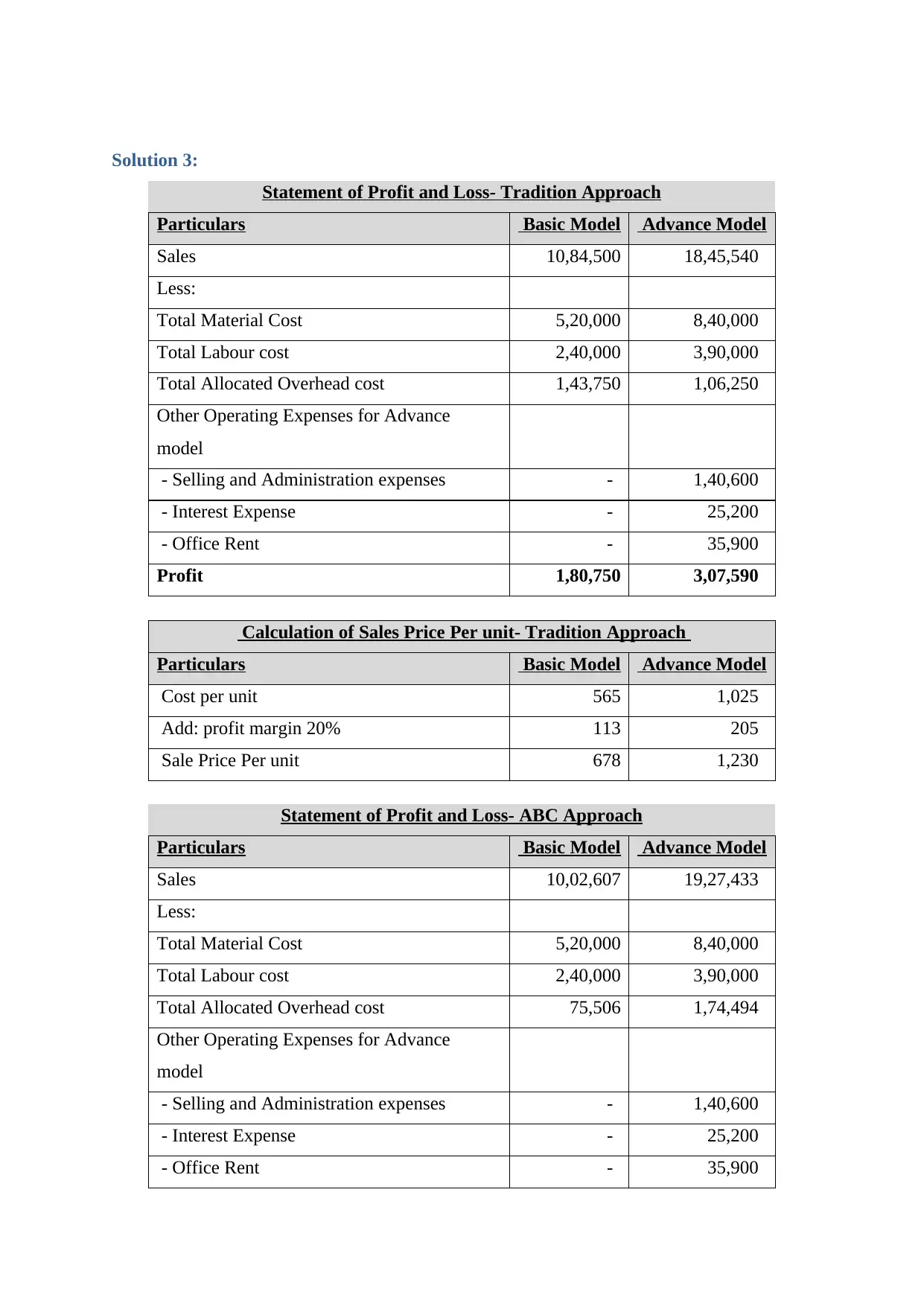

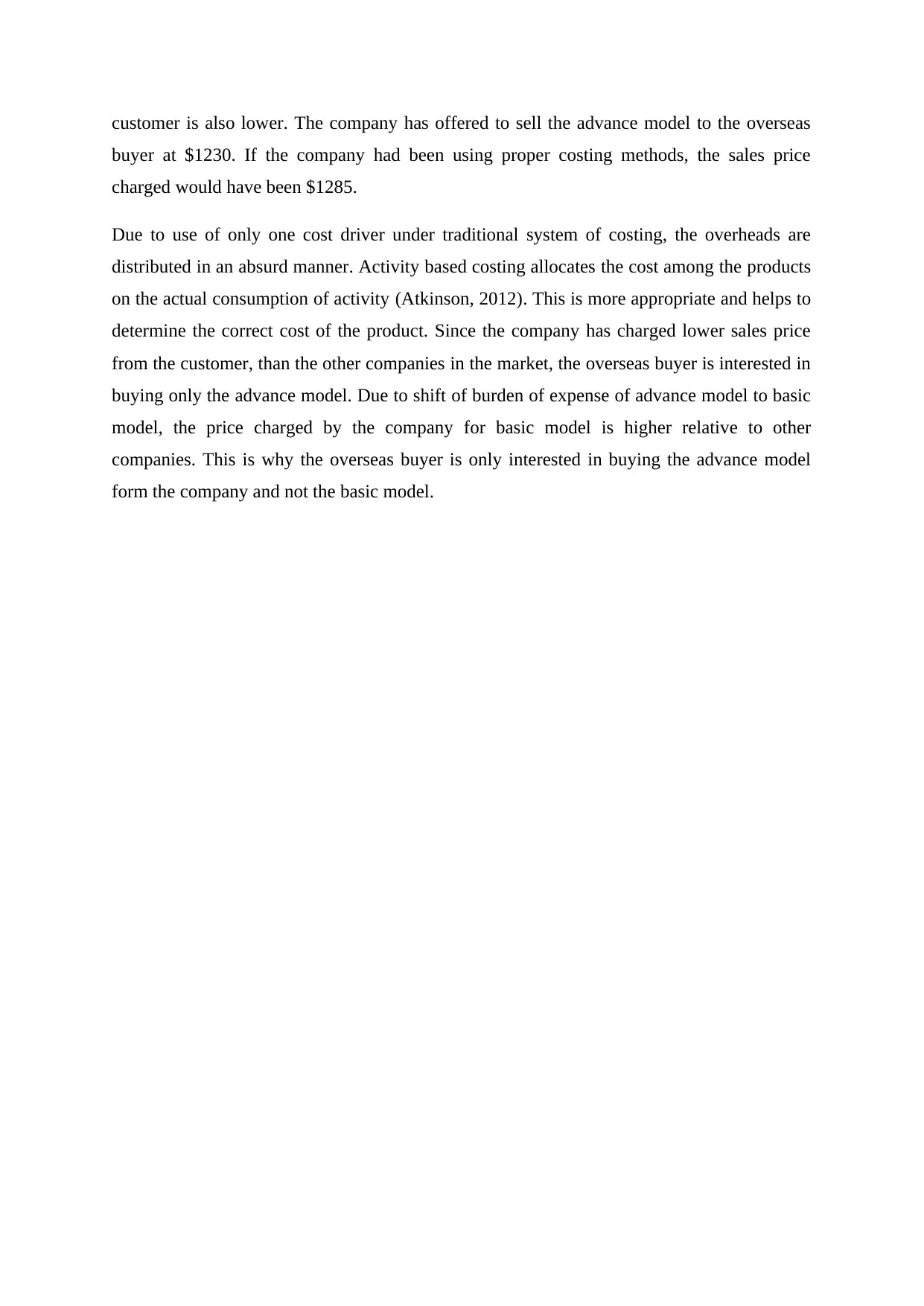

This document presents a comprehensive solution to a management accounting assignment, focusing on the application of different costing methods. It includes detailed calculations and comparisons of traditional and activity-based costing approaches, demonstrating how these methods impact cost allocation, profit and loss statements, and pricing decisions. The solution analyzes a case study involving a company's product sales, contrasting the outcomes under different costing systems. Furthermore, it explains overhead allocation methods, including absorption costing and activity-based costing, and discusses the implications of over or under-recovery of overheads. The document also outlines the advantages of activity-based costing, highlighting its role in accurate cost analysis, cost control, activity discovery, and decision-making. The solutions provide a deep understanding of cost accounting principles and their practical application in a business context.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.