University of Sunderland: Management Accounting Assignment - UGB106

VerifiedAdded on 2023/01/06

|21

|3763

|57

Homework Assignment

AI Summary

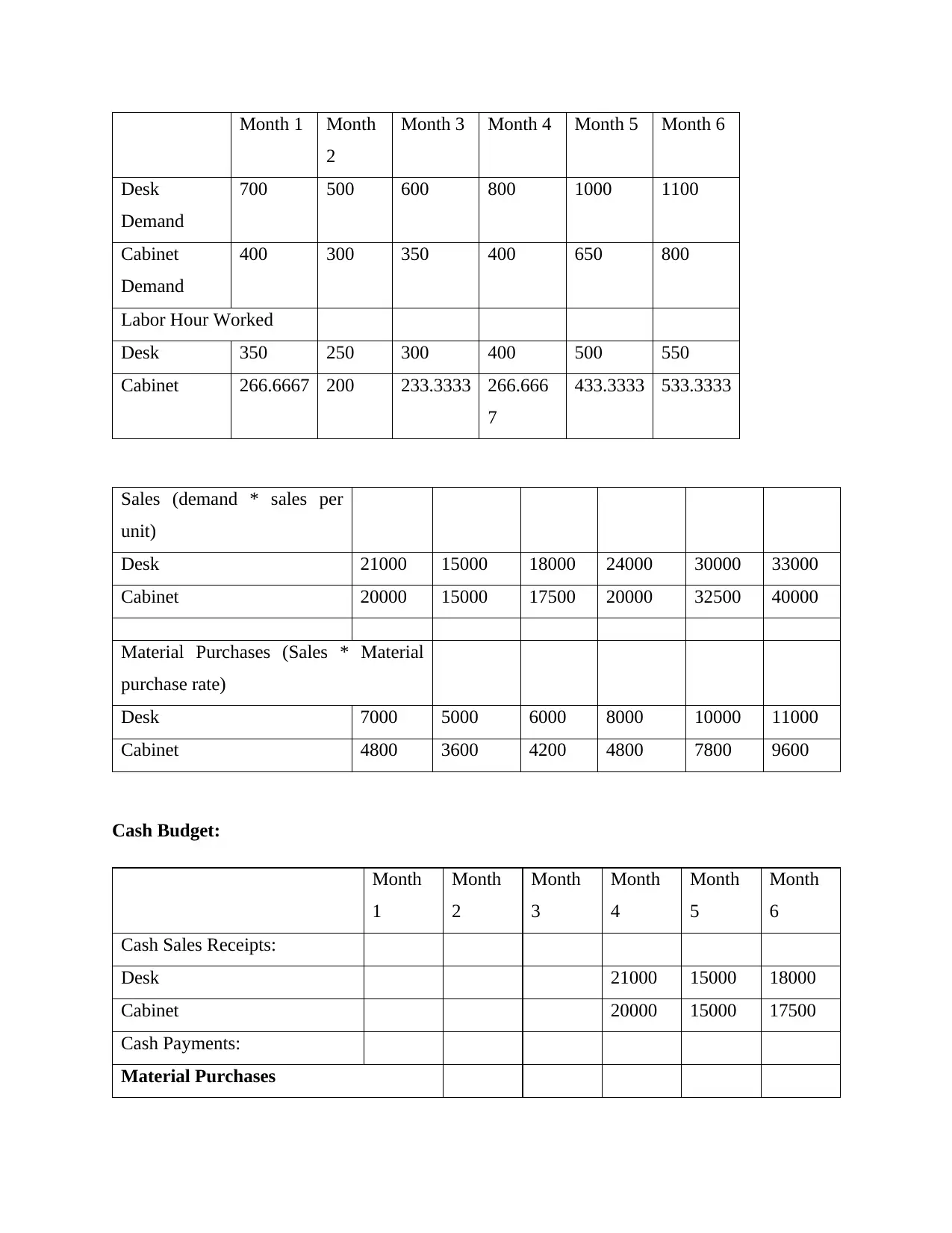

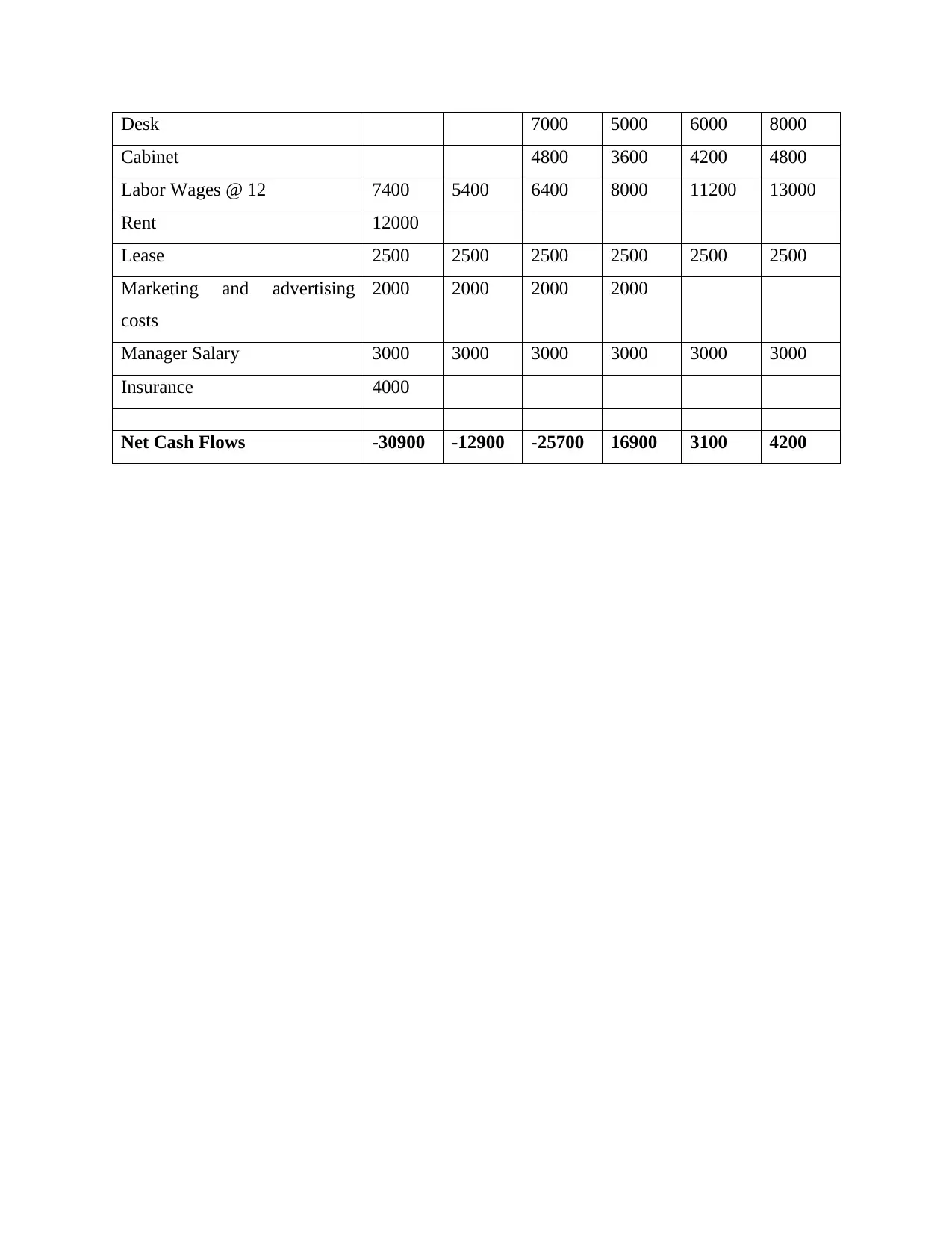

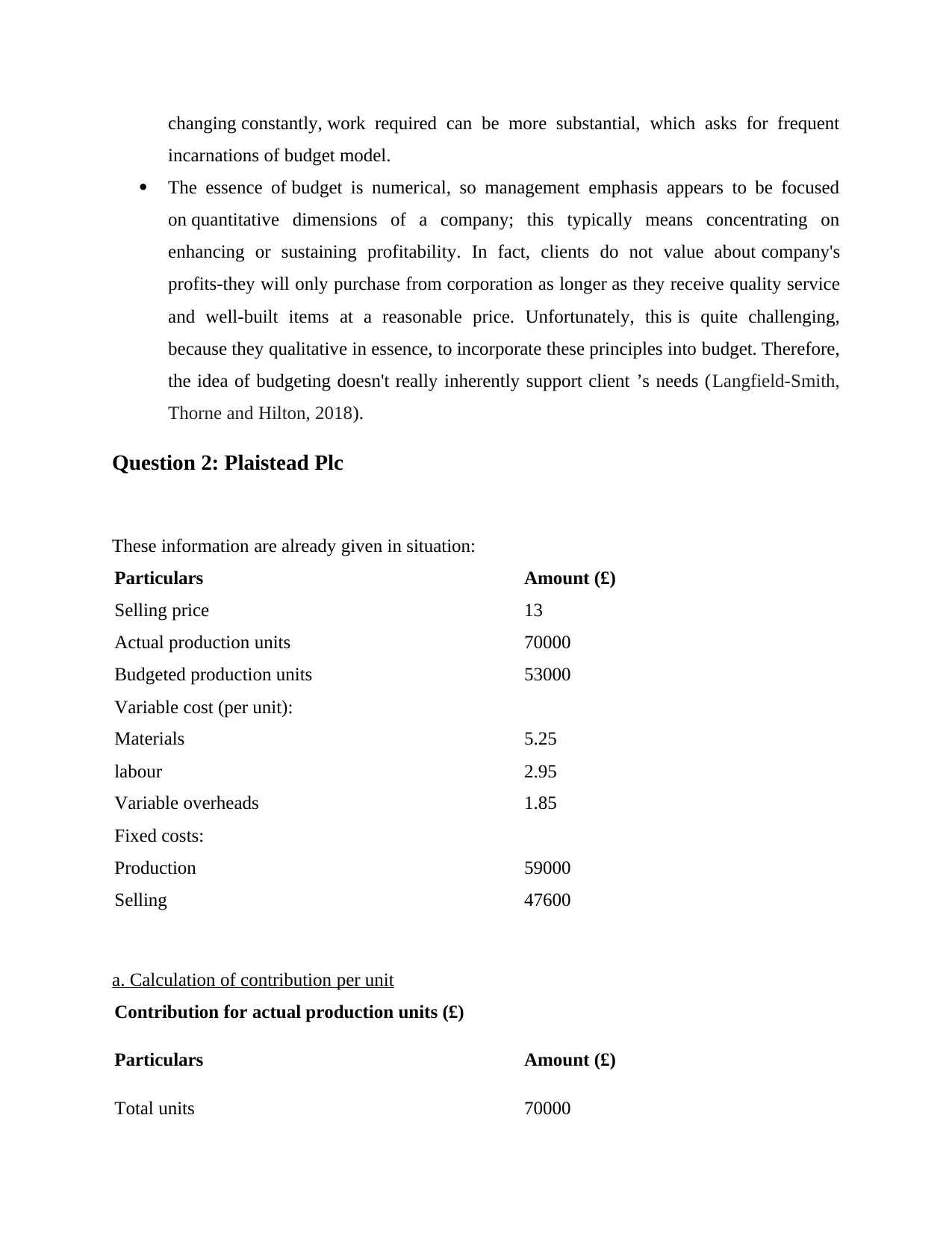

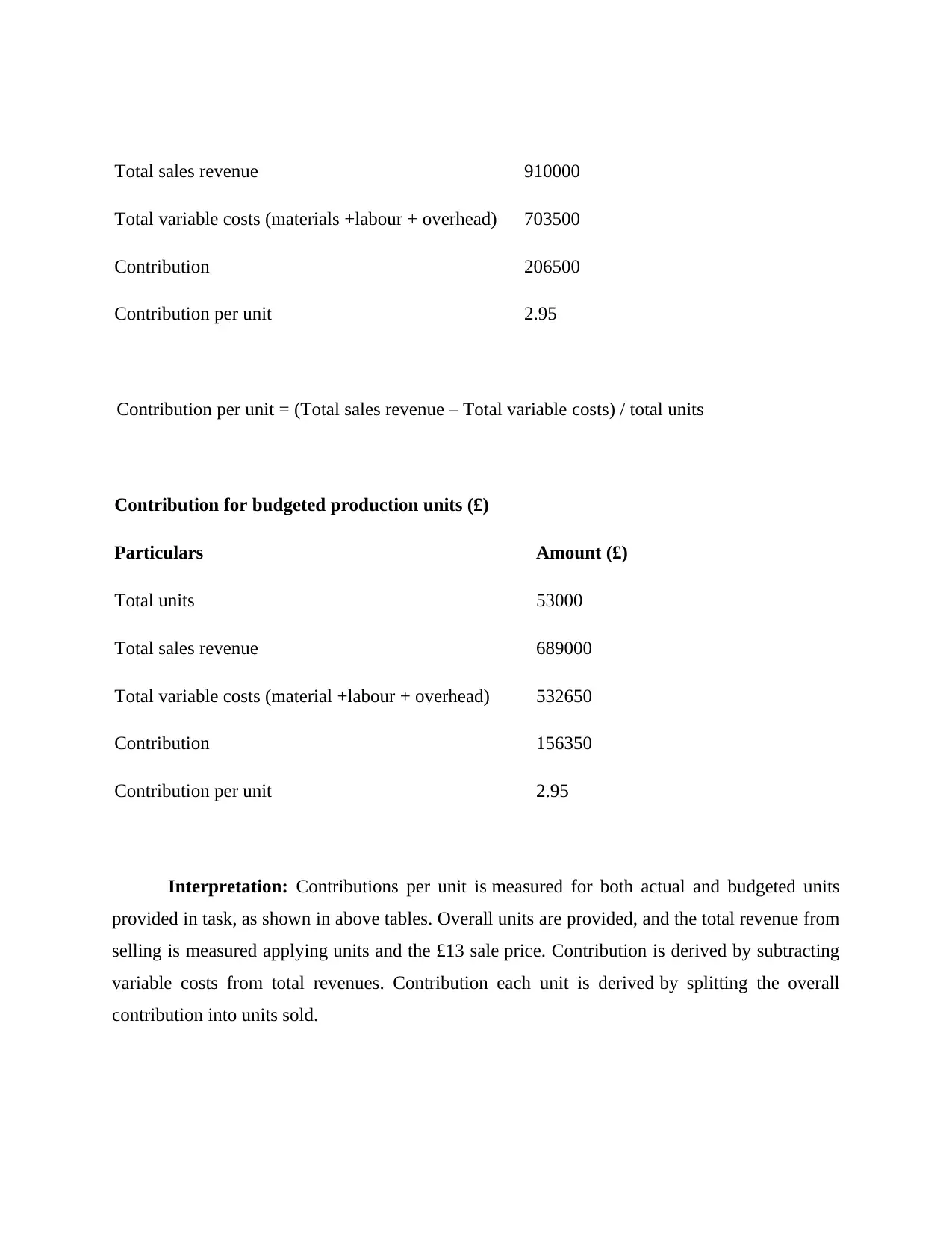

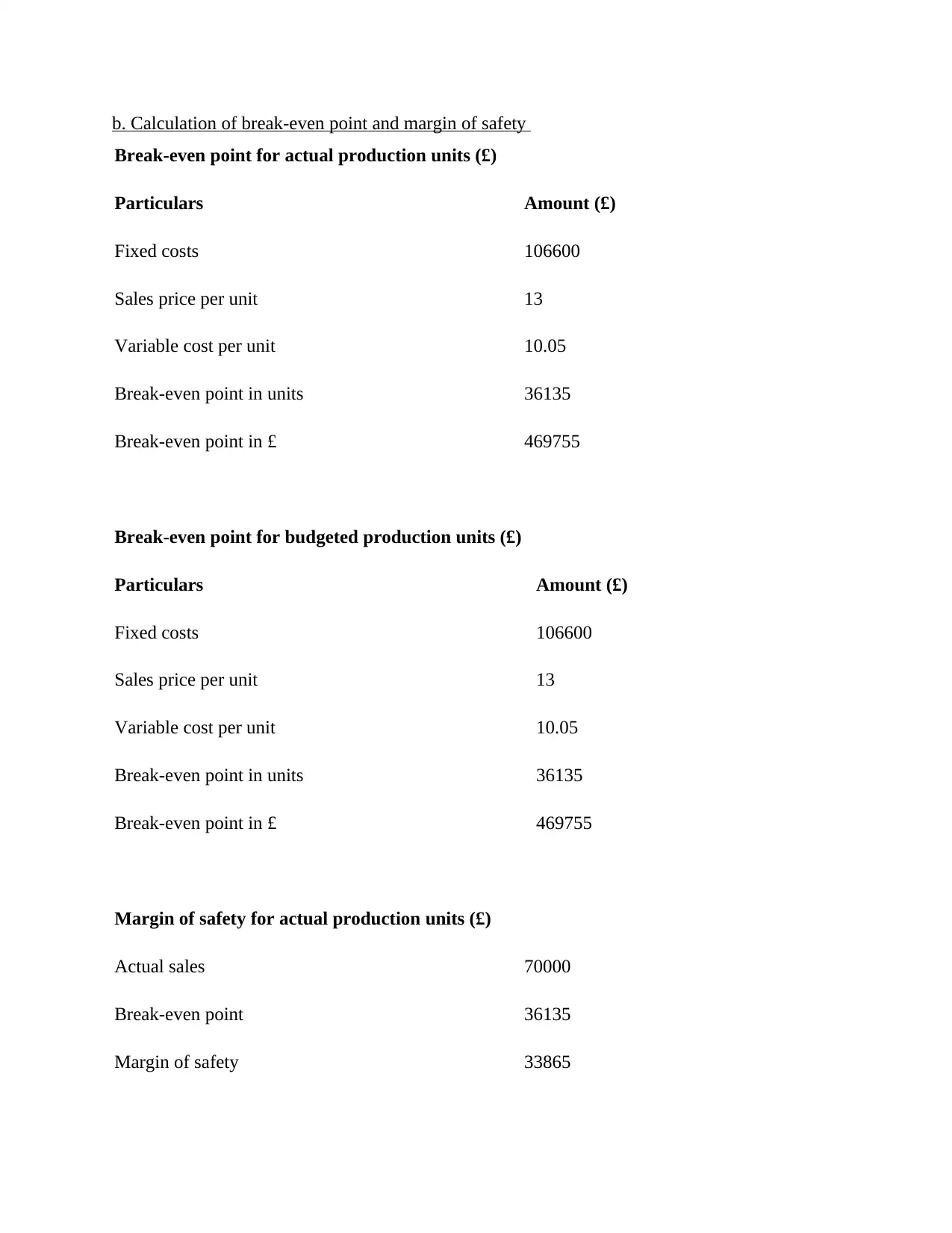

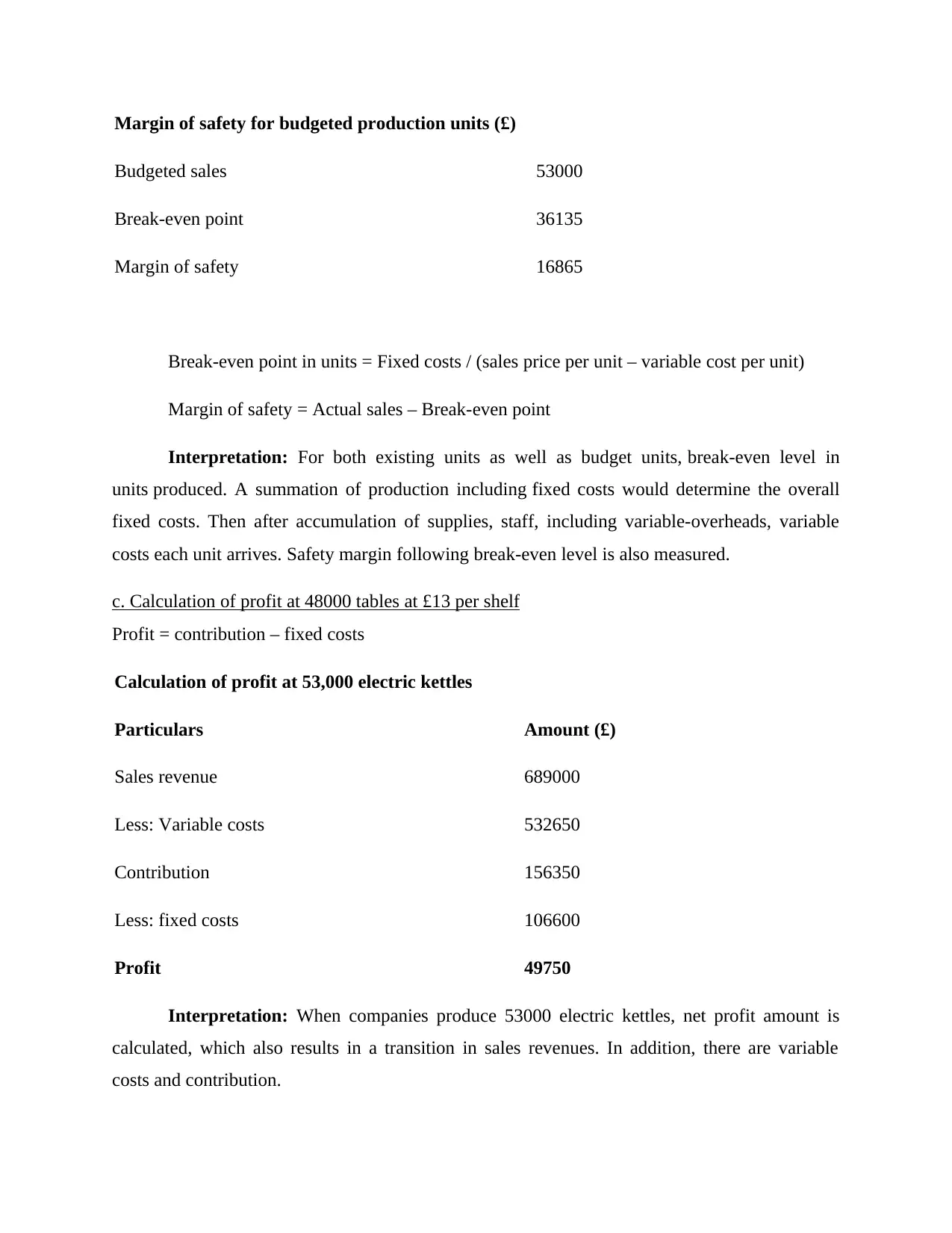

This document presents a comprehensive solution to an Introduction to Management Accounting assignment, focusing on practical applications and numerical problems. The assignment covers key concepts such as cash budgeting, break-even analysis, and variance analysis. Question 1 analyzes Woodrock Limited's cash flow through the preparation of a cash budget and provides recommendations for improvement. It also examines behavioral aspects of budgeting. Question 2 focuses on Plaistead Plc, calculating contribution per unit, break-even points, margin of safety, and profit projections under various scenarios, including a new marketing strategy. The solution also includes a discussion of the assumptions underlying the break-even model. Question 4 addresses standard costing, its purposes, key values, and limitations, linked with the application of variance analysis, providing a columnar statement. The assignment aims to help students understand the importance of management accounting in business decision-making.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.