Inventory Valuation and COGS Analysis: Accounting Report, University

VerifiedAdded on 2022/09/07

|5

|363

|187

Report

AI Summary

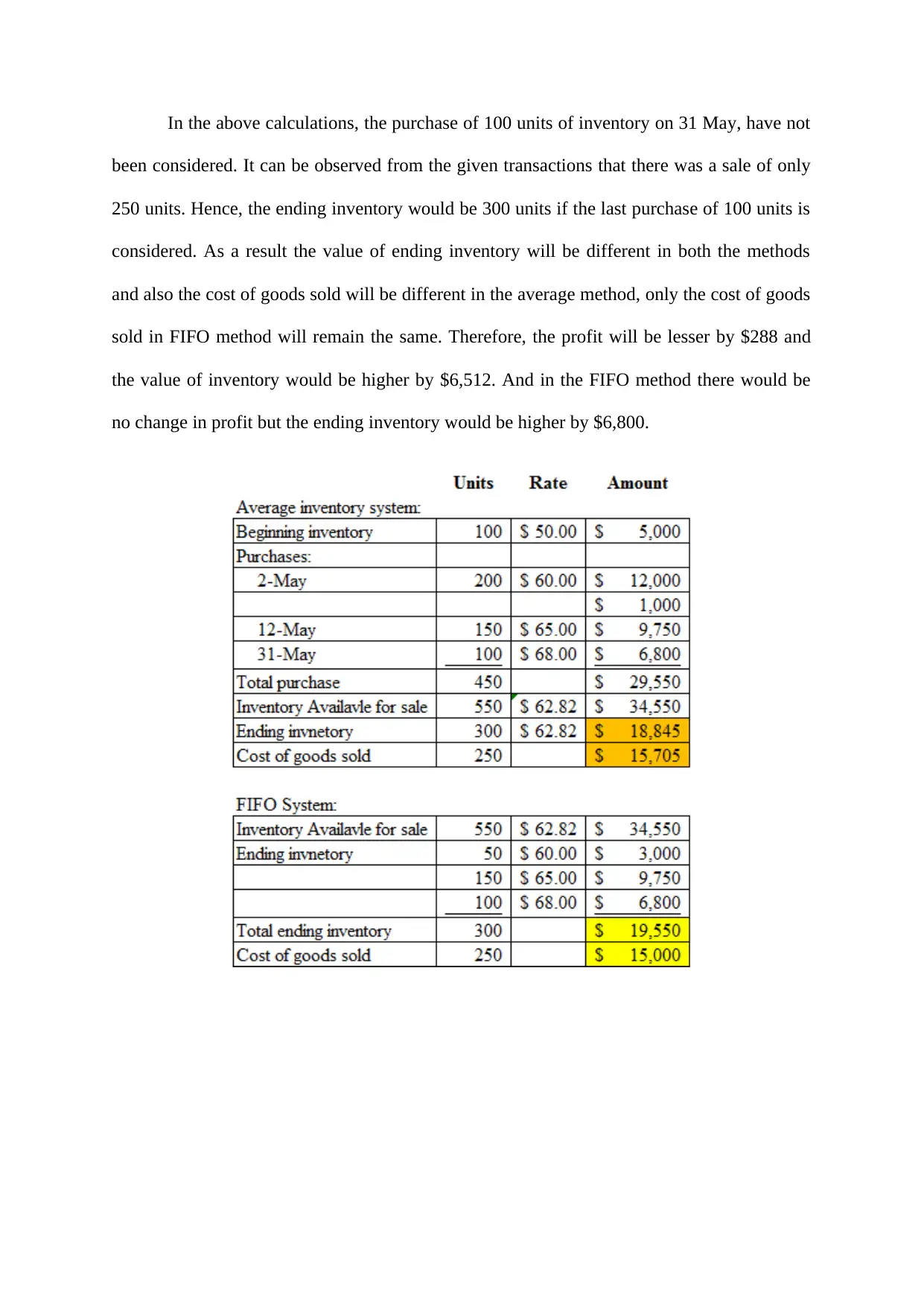

This report examines the impact of different inventory valuation methods, specifically the FIFO and average methods, on the Cost of Goods Sold (COGS) and the valuation of ending inventory. The analysis considers a scenario involving transactions related to inventory purchases and sales. The report highlights the differences in COGS and ending inventory values under the two methods, demonstrating how the choice of valuation method affects profitability and the balance sheet. It concludes that the average method results in a lower profit due to the higher cost of goods sold, while the FIFO method results in no change in profit. The report also includes a brief bibliography referencing relevant academic sources related to inventory management.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.