Analysis of Inventory and Depreciation Methods for Sheldon and Blair

VerifiedAdded on 2020/07/23

|9

|1591

|75

Homework Assignment

AI Summary

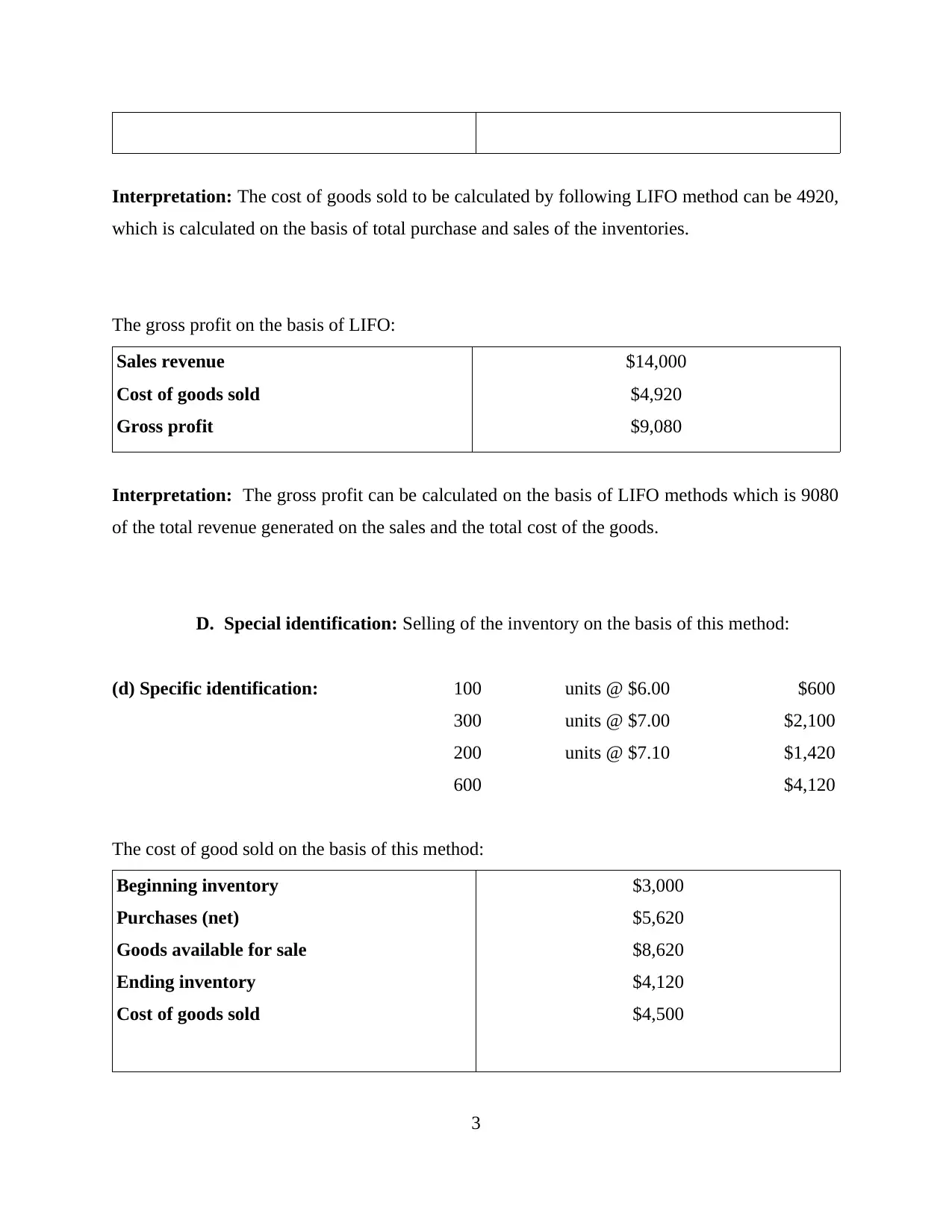

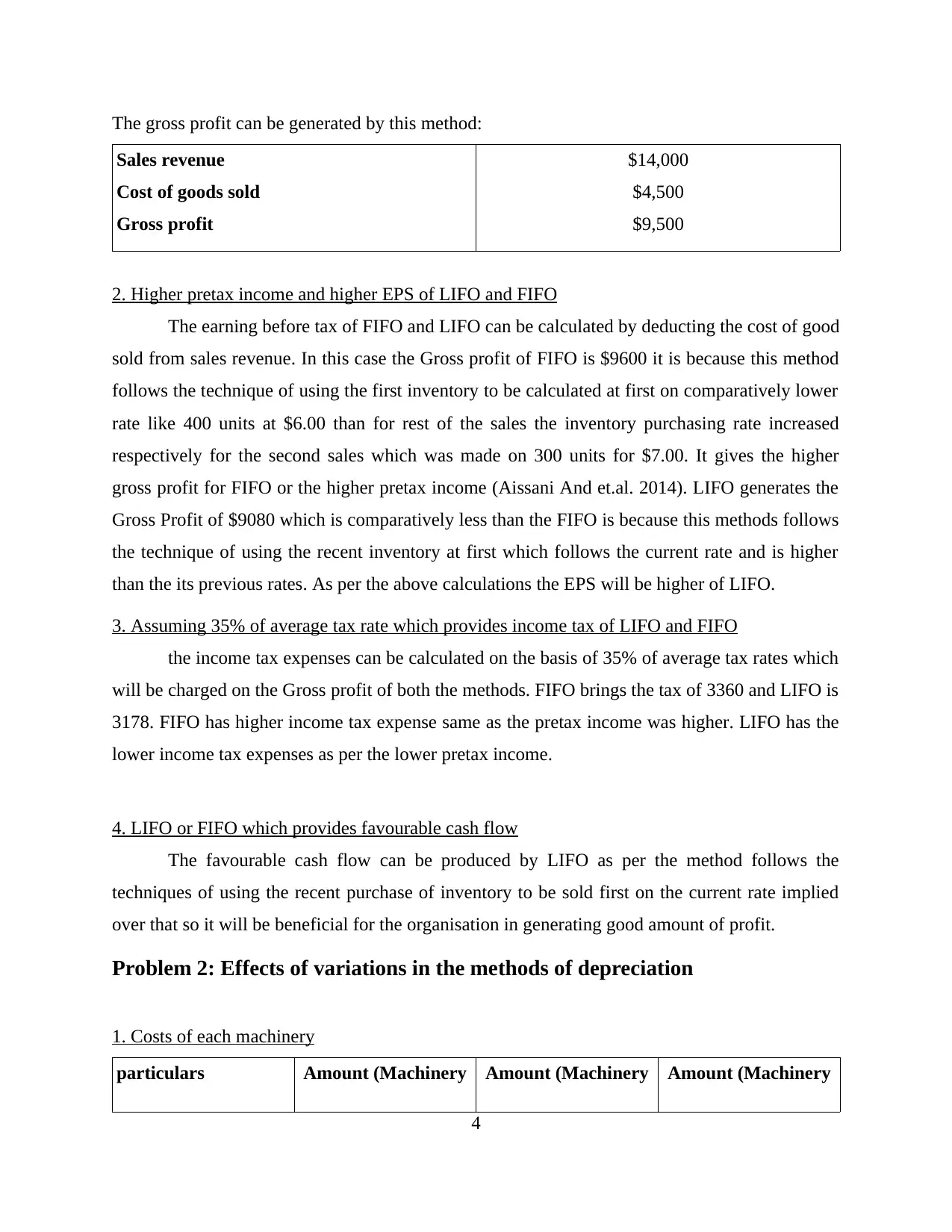

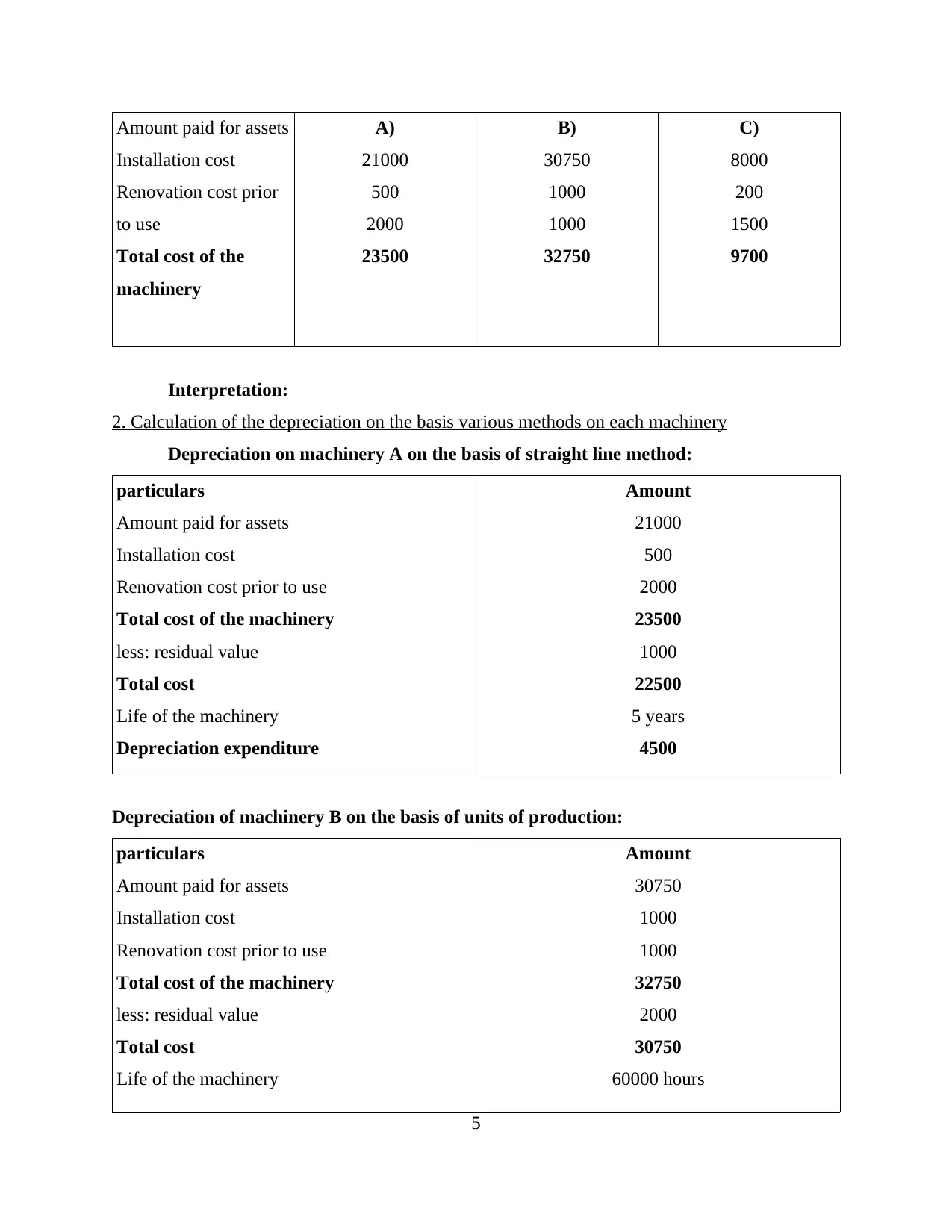

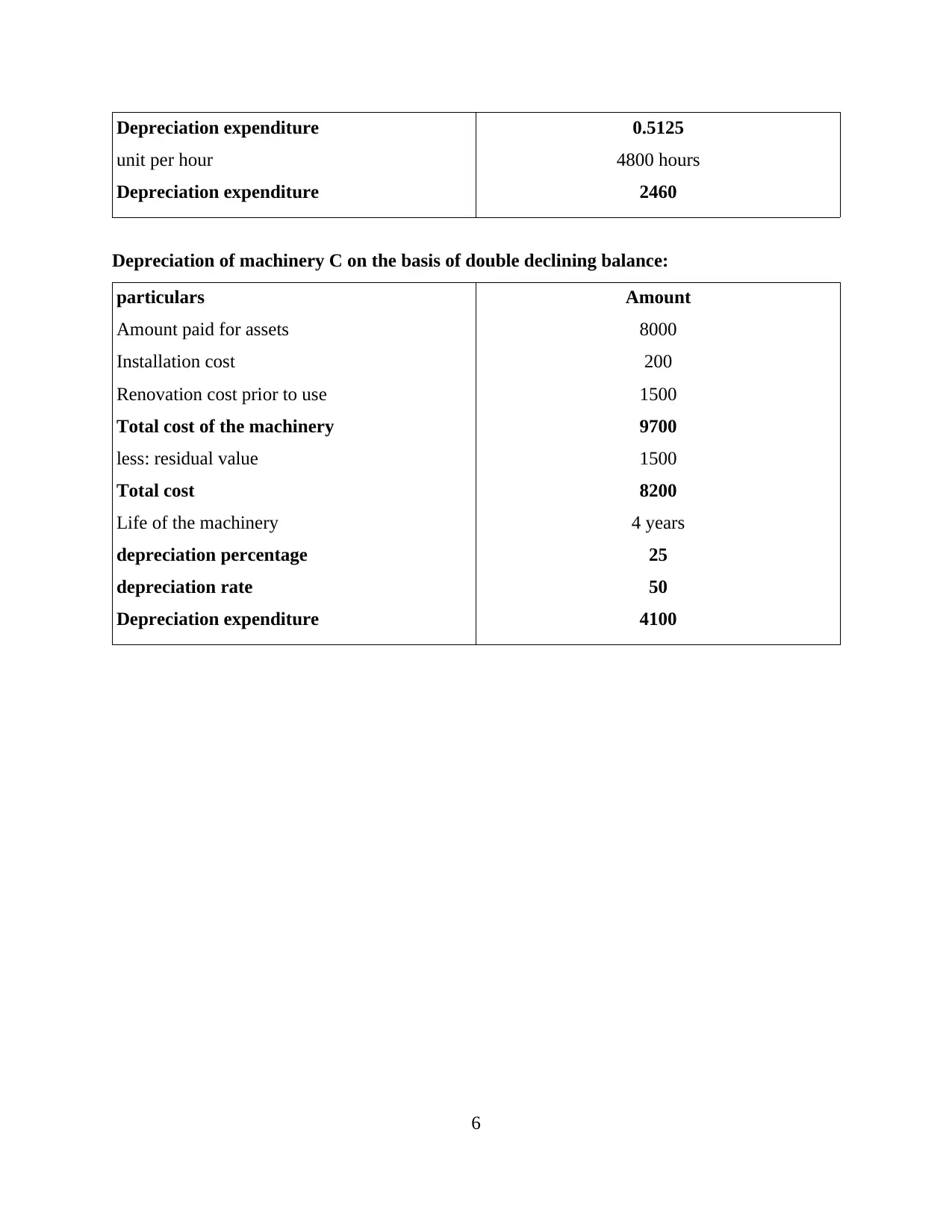

This homework assignment analyzes inventory valuation methods (FIFO, LIFO, and average cost) and depreciation techniques (straight-line, units of production, and double-declining balance). The assignment begins with a detailed examination of inventory computation under each method, including calculations of cost of goods sold and gross profit. It then compares the impact of FIFO and LIFO on pretax income, earnings per share, and income tax expenses, considering a 35% average tax rate. Furthermore, the analysis explores which method provides a more favorable cash flow. The second part of the assignment focuses on the effects of different depreciation methods on machinery, calculating depreciation expense for three machines using straight-line, units of production, and double-declining balance methods, respectively. The assignment provides interpretations of the calculations and concludes with a list of references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.