Fashion Haven's Accounting: Inventory and Bank Reconciliation Report

VerifiedAdded on 2023/06/04

|12

|1169

|140

Report

AI Summary

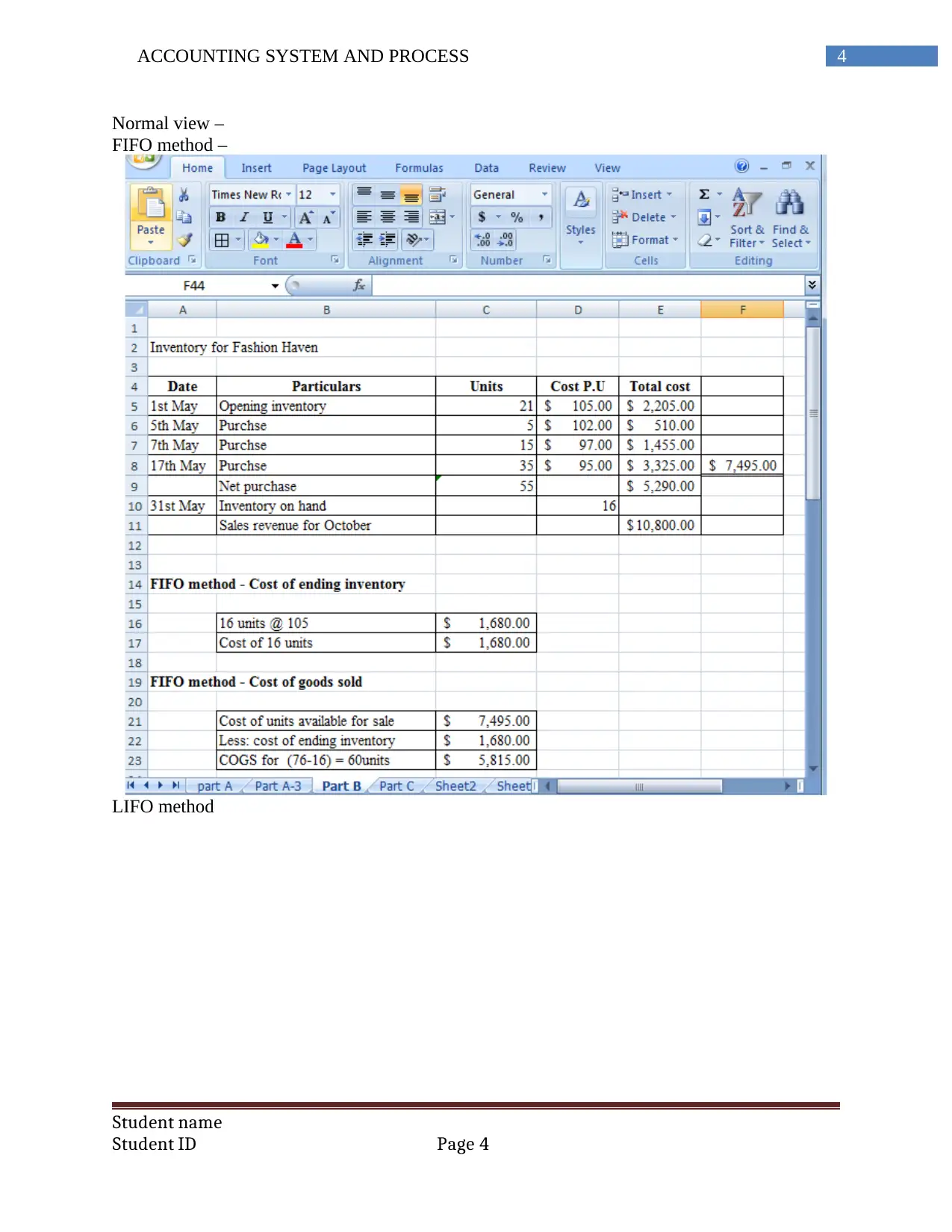

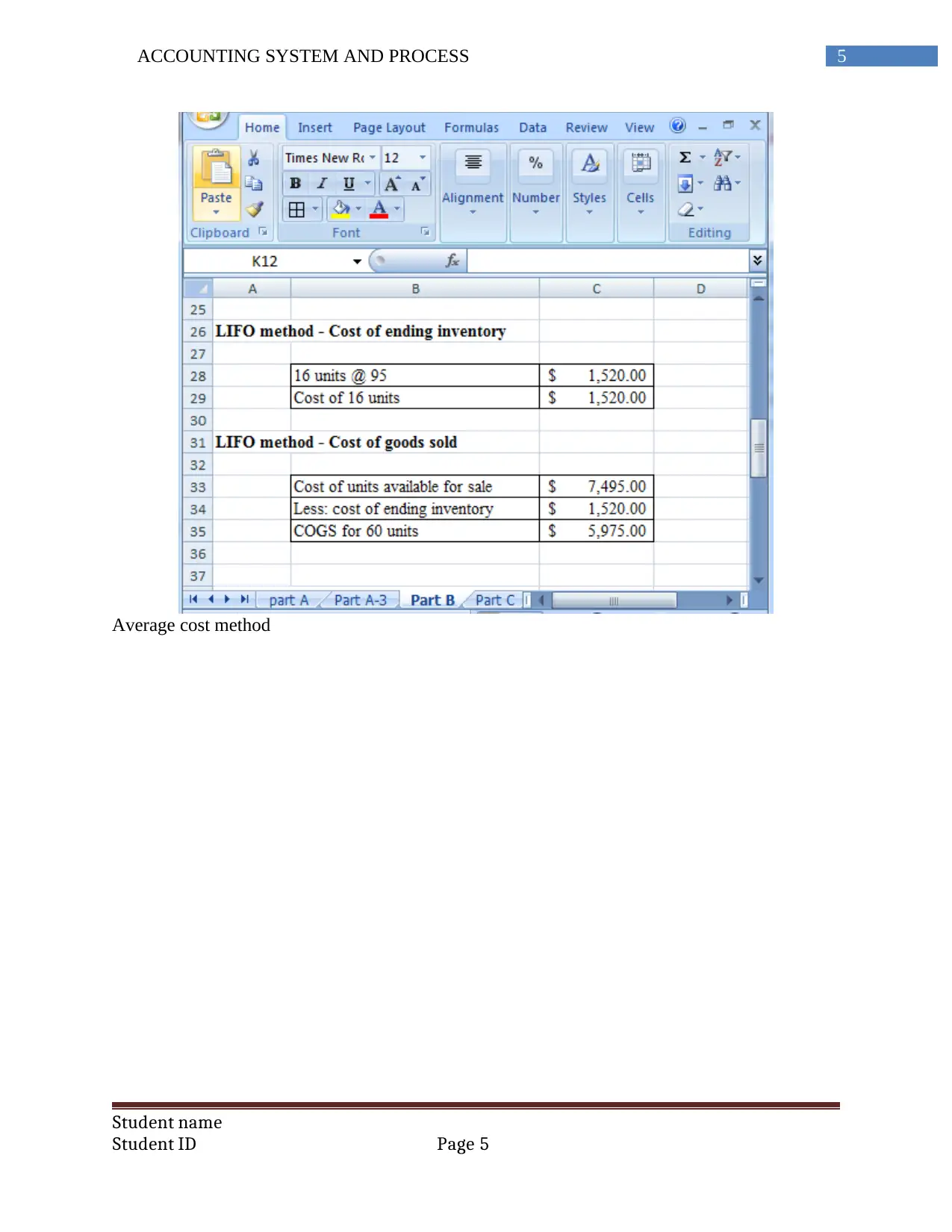

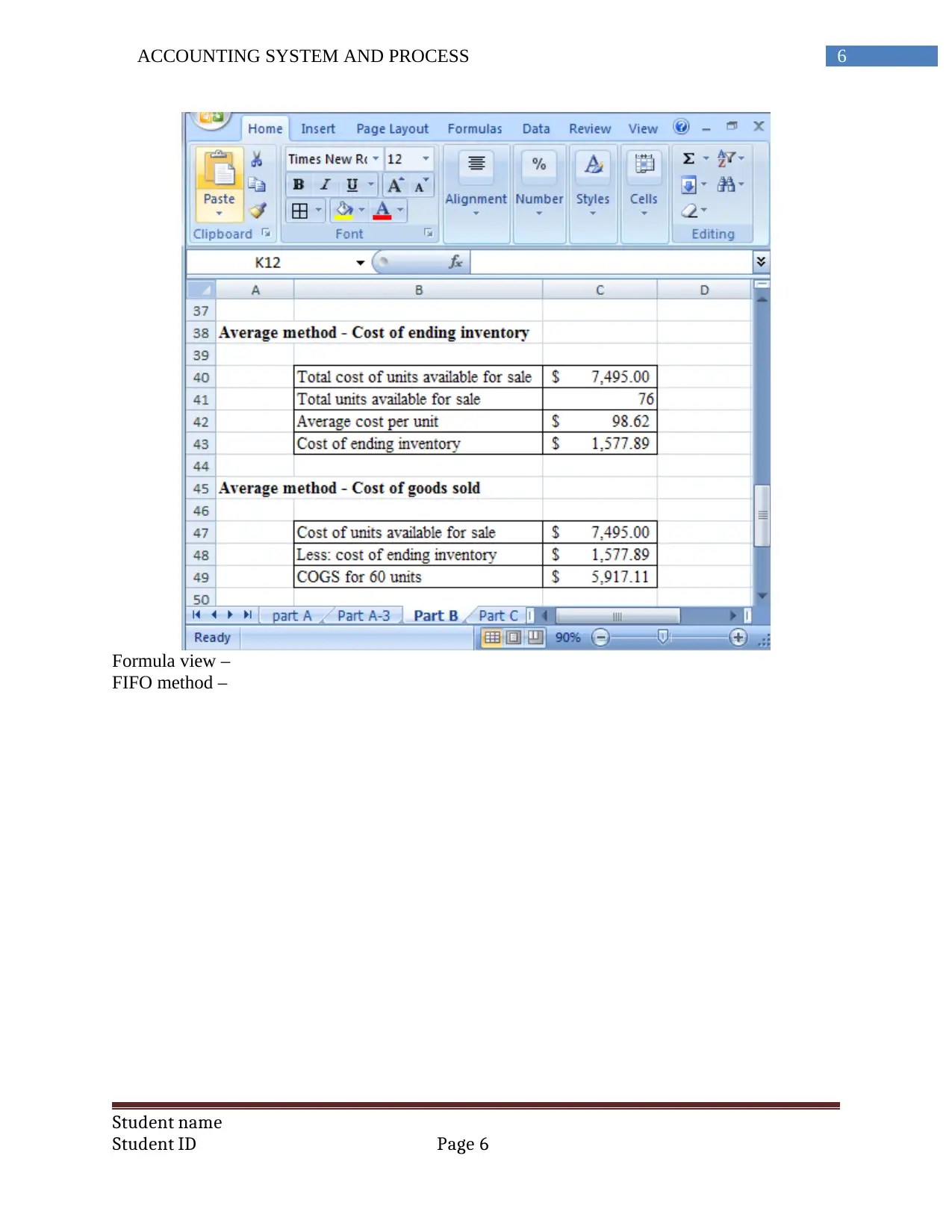

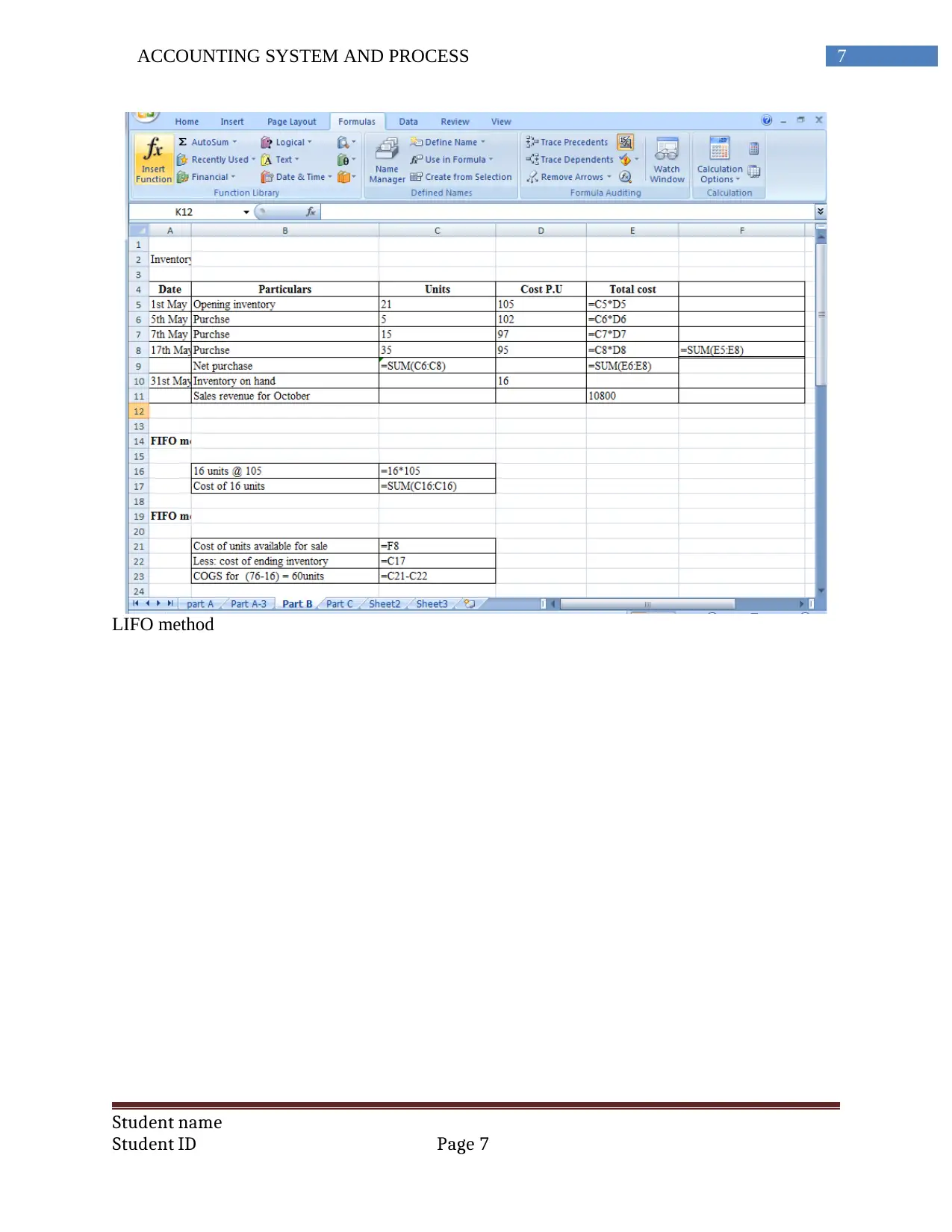

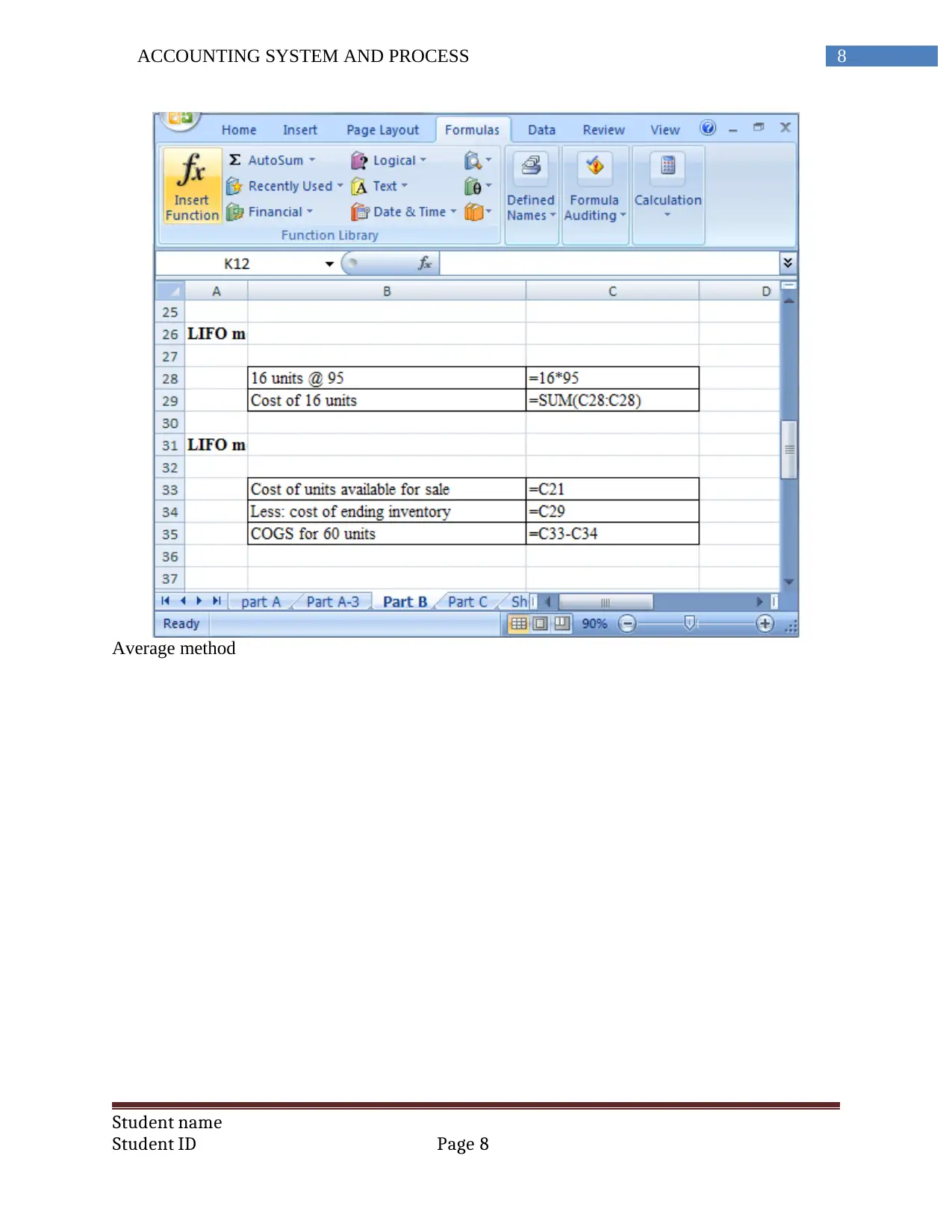

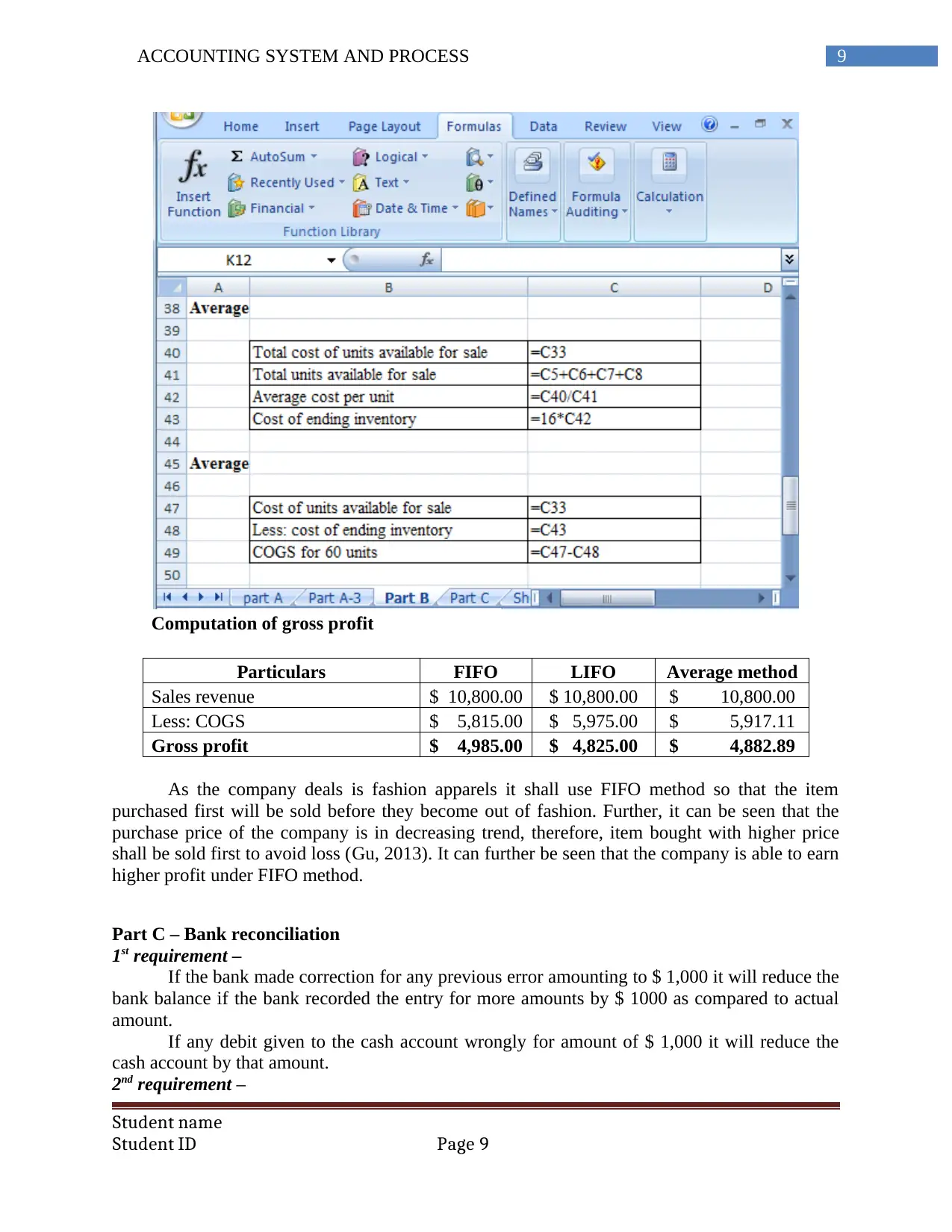

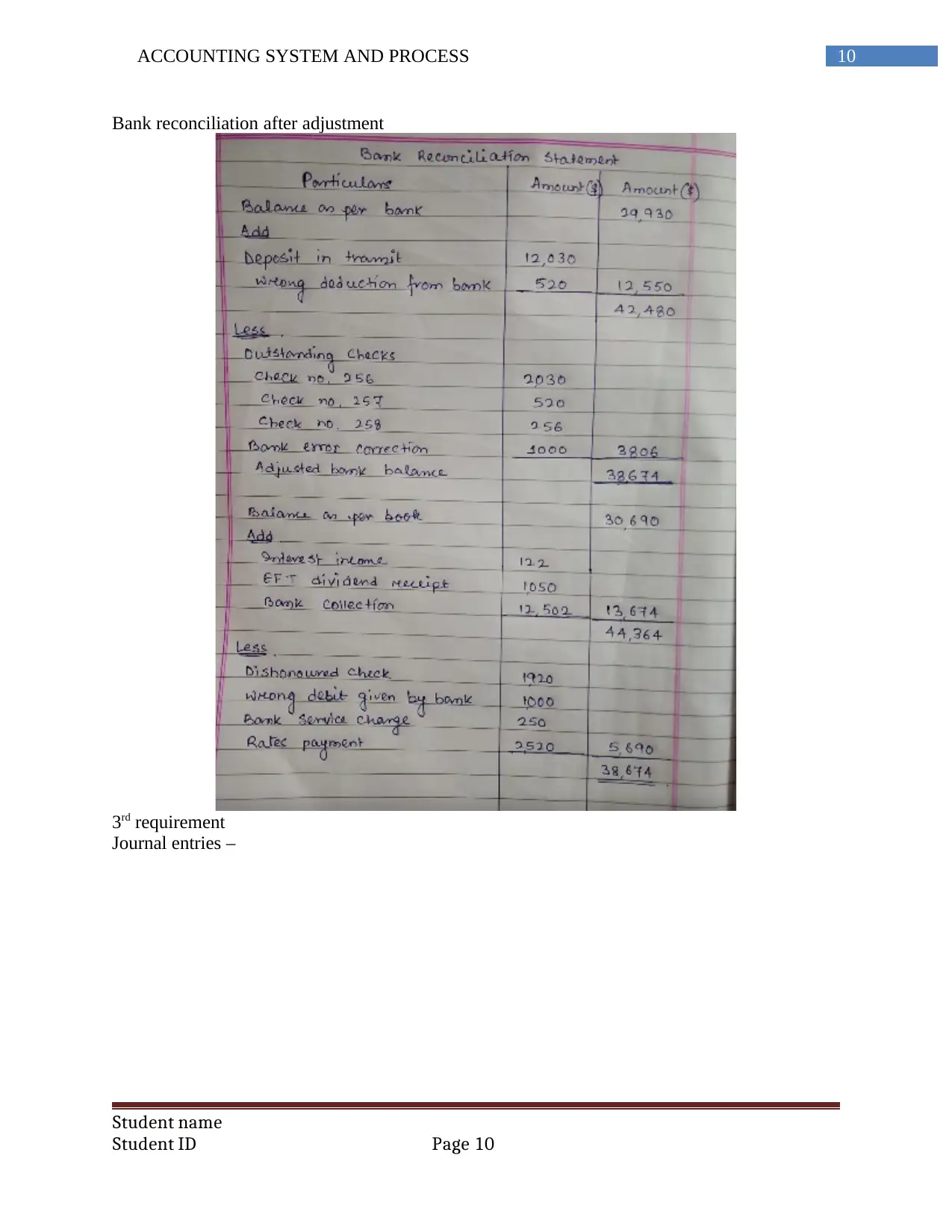

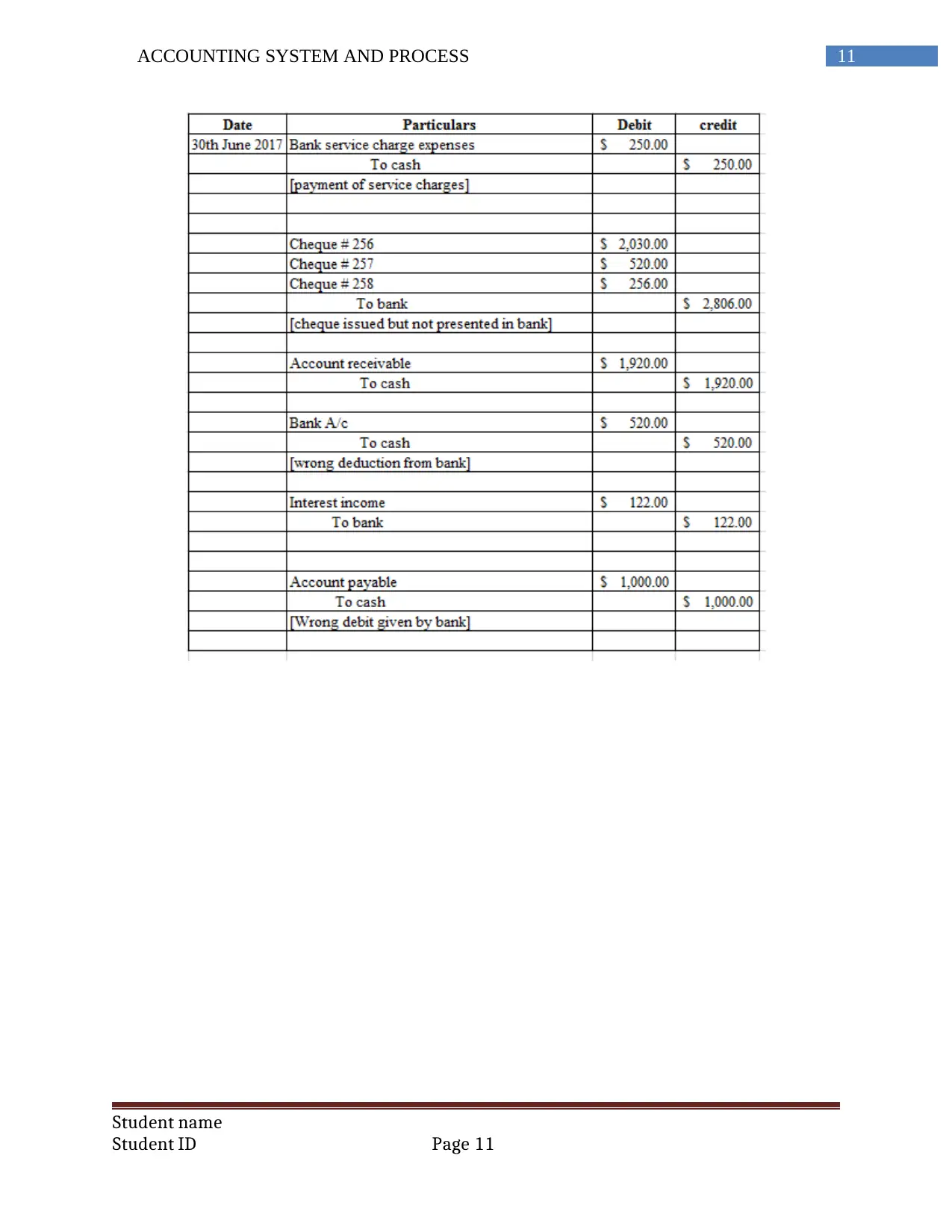

This report provides a comprehensive analysis of inventory management and bank reconciliation, focusing on Fashion Haven, a retail clothing shop in Australia. It differentiates between perpetual and periodic inventory systems, recommending the perpetual system for Fashion Haven due to its accuracy and automation. The report includes a calculation of ending inventory and cost of goods sold using FIFO, LIFO, and average cost methods, advocating for the FIFO method based on the company's context and profit maximization. Furthermore, it addresses bank reconciliation, presenting necessary adjustments and journal entries. The document is contributed by a student and available on Desklib, a platform offering a wide array of study resources.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.