Comparative Analysis of Investment Appraisal Methods and Techniques

VerifiedAdded on 2021/02/21

|12

|3005

|89

Report

AI Summary

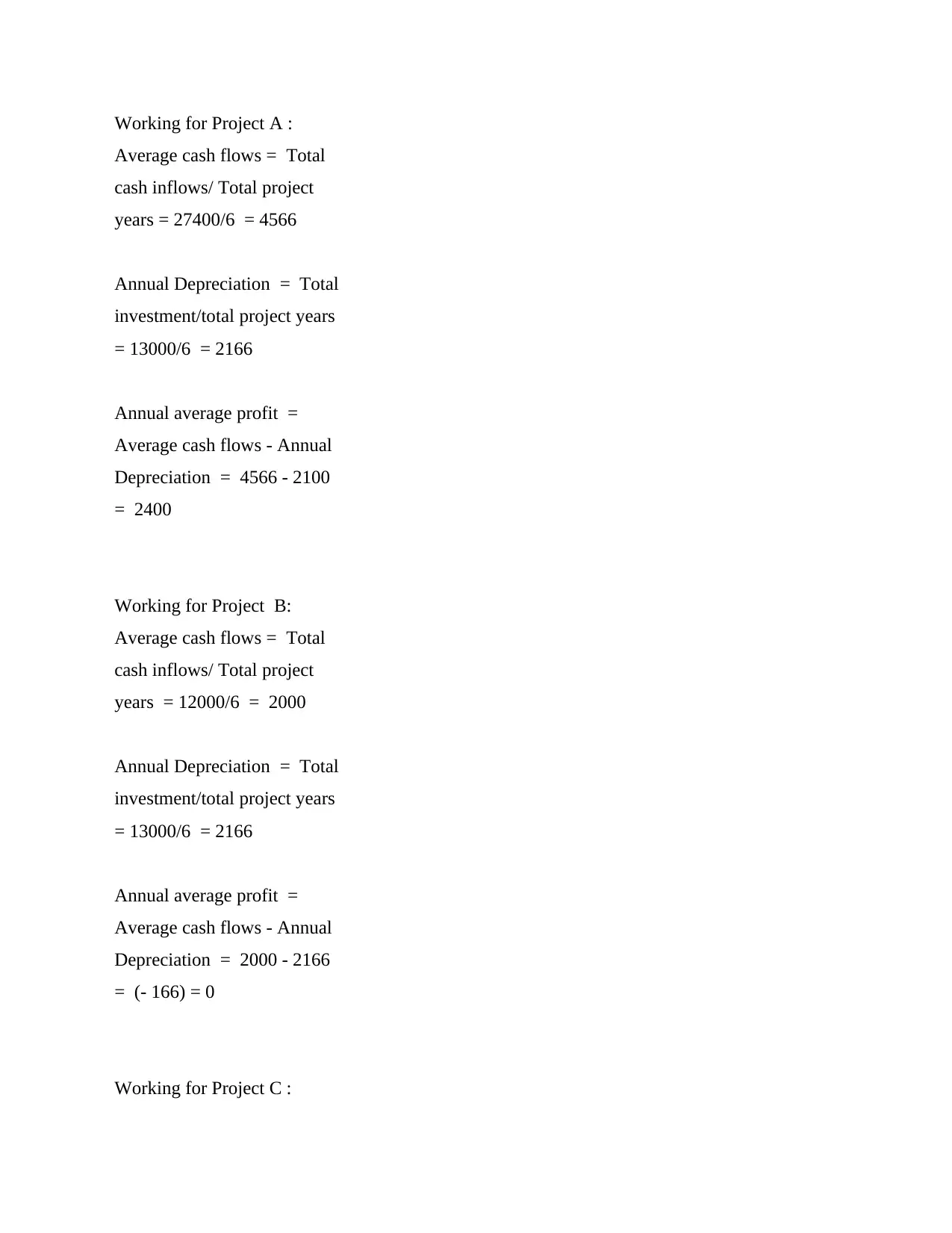

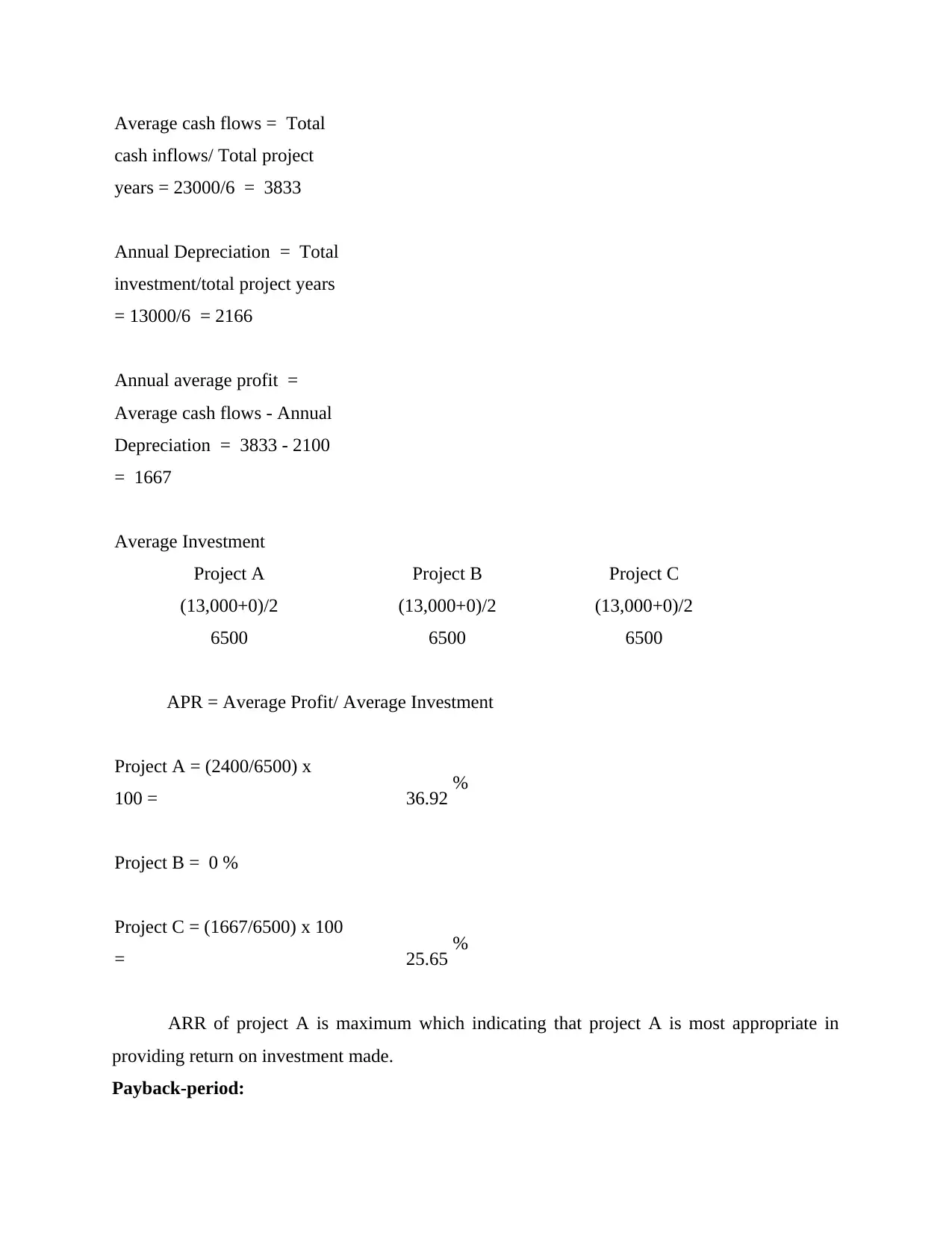

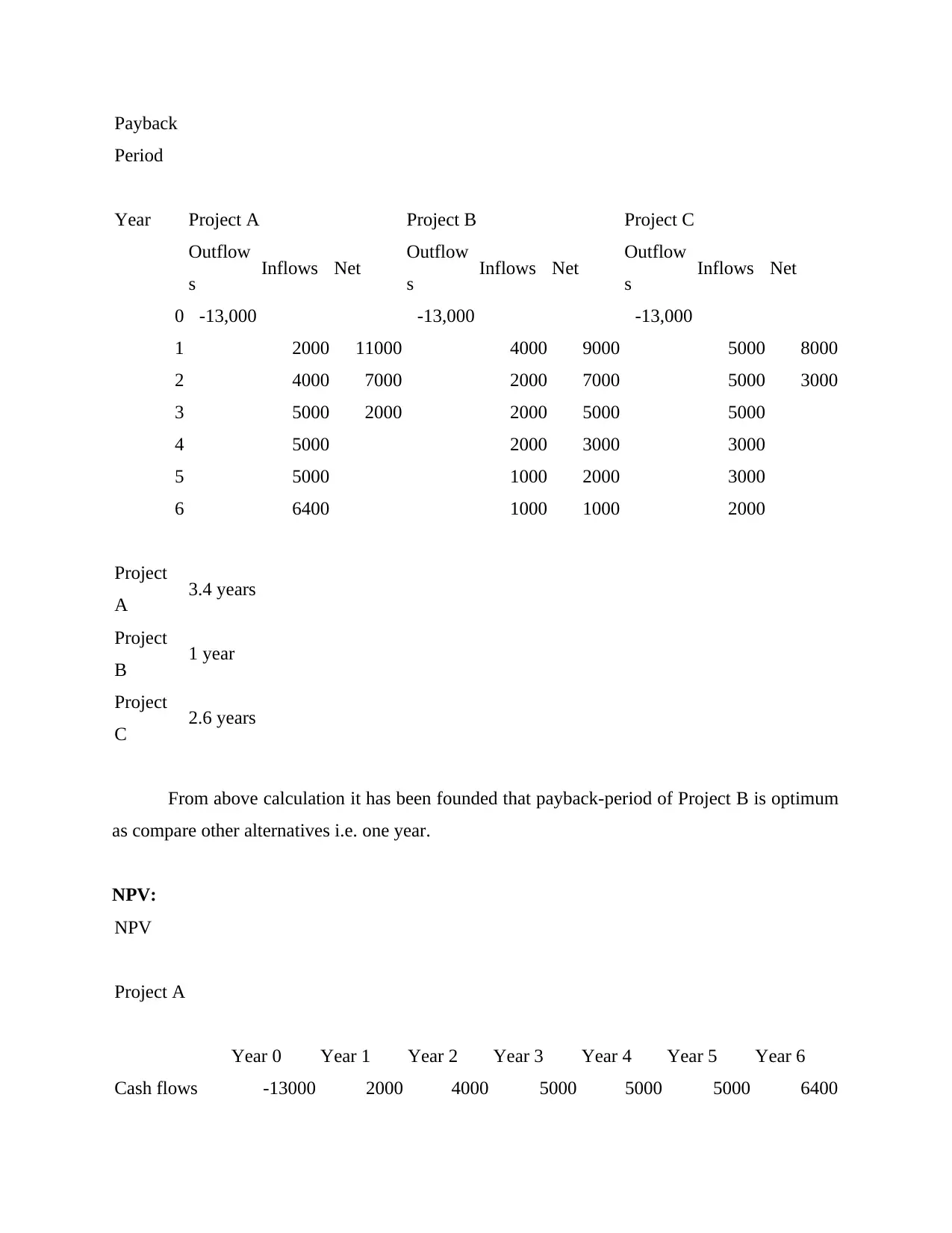

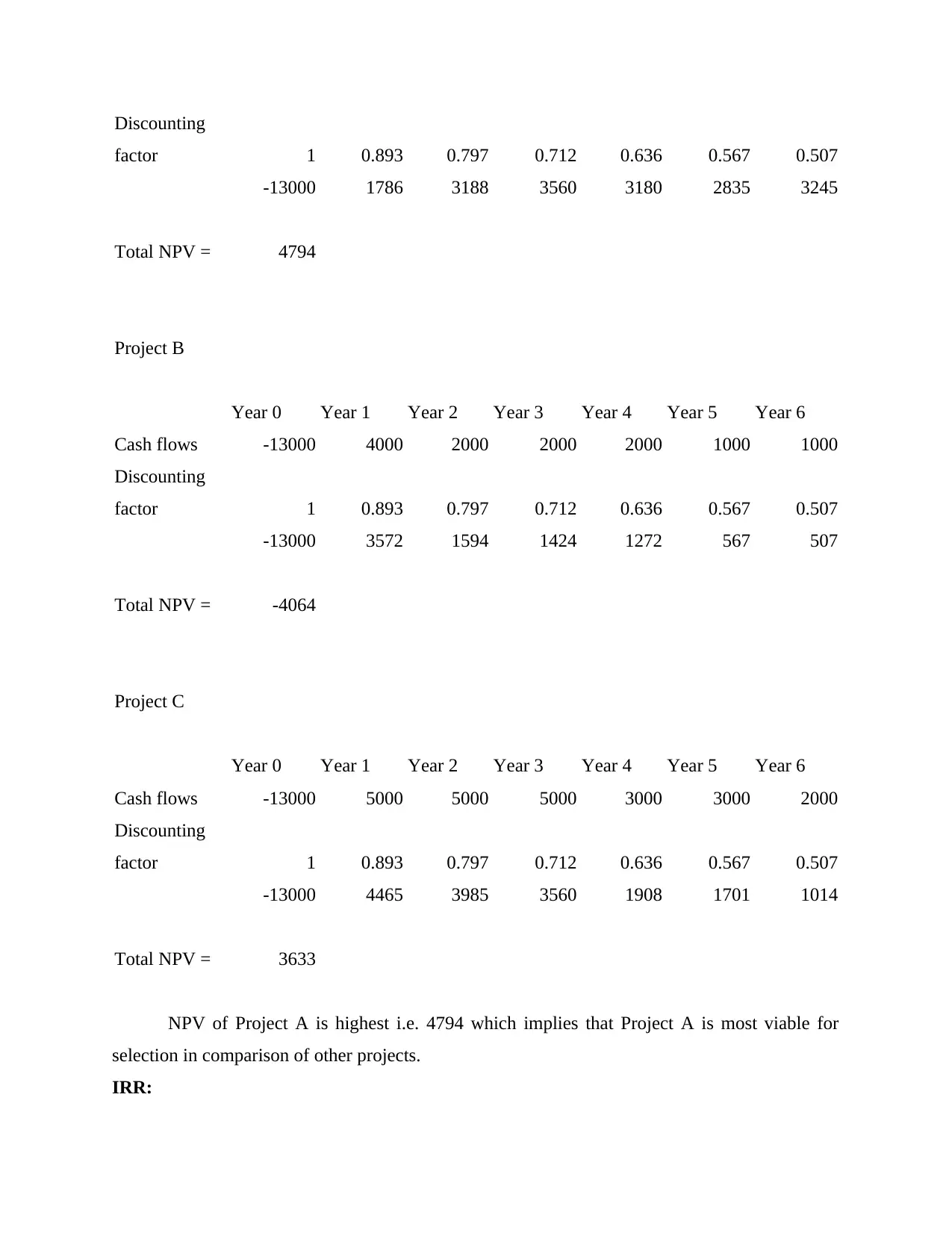

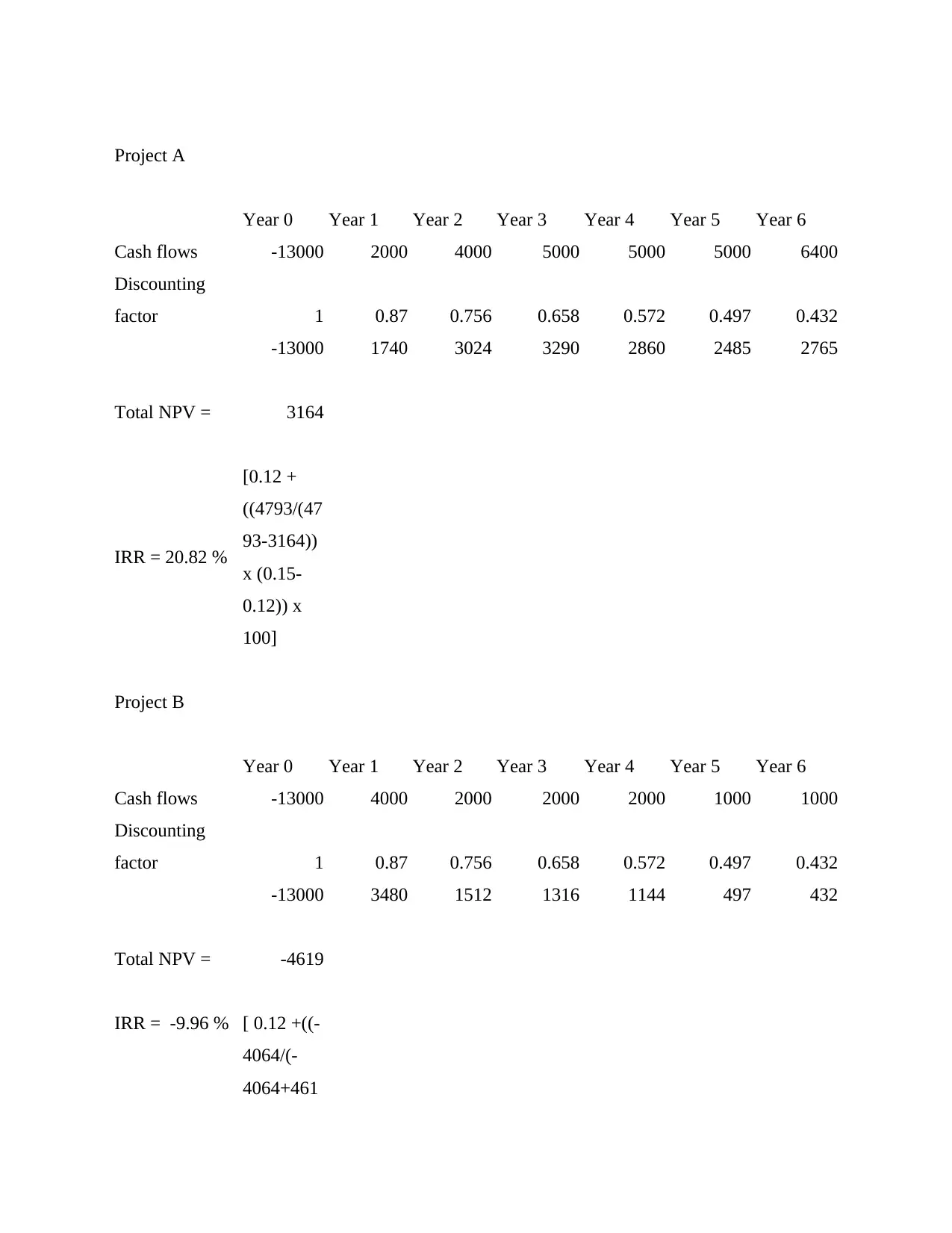

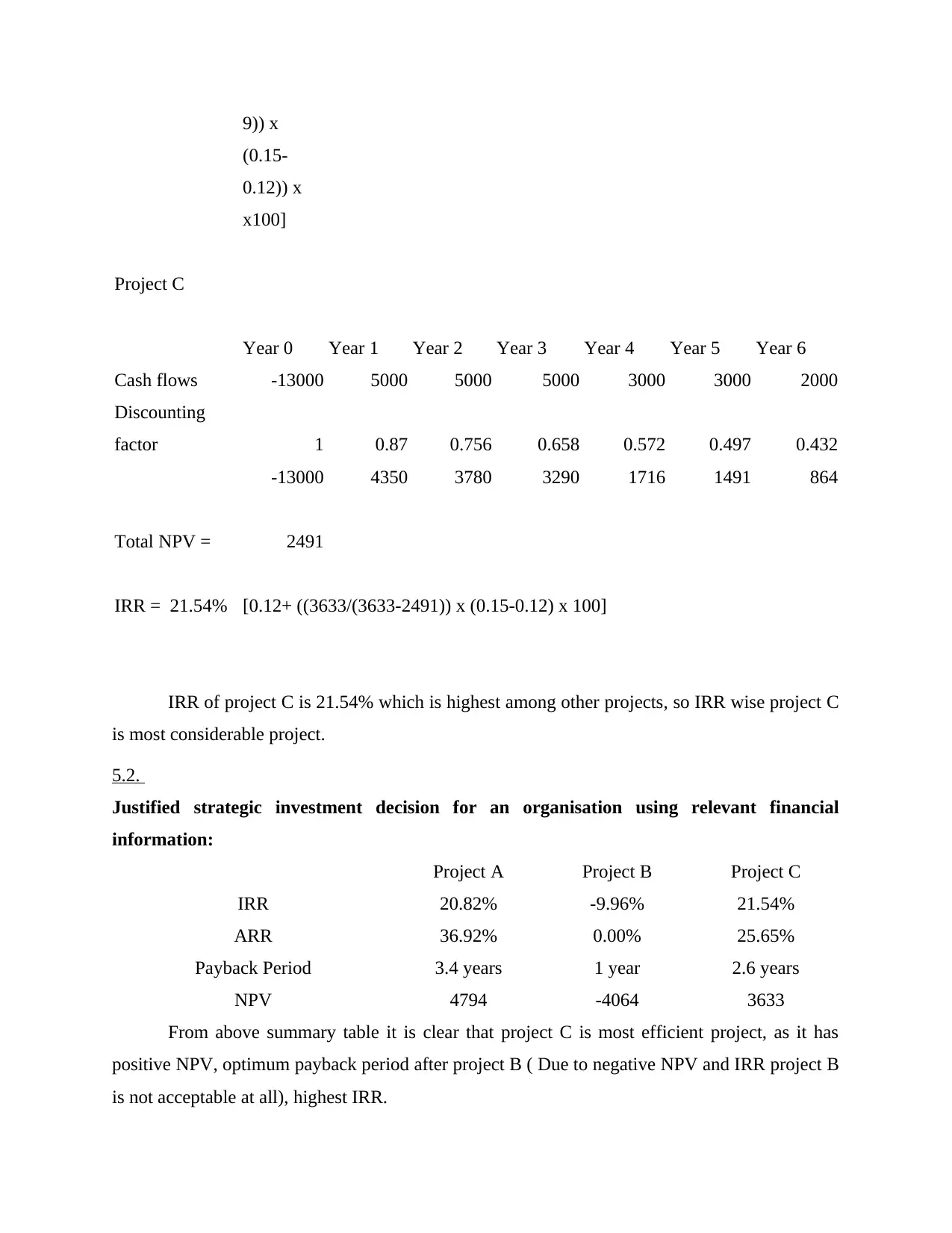

This report provides a comprehensive analysis of investment appraisal methods used to assess the attractiveness of investments. It explores various techniques, including Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR). The report delves into the application of forecasting techniques for making cost and revenue decisions within an organization. It includes detailed calculations and evaluations of example projects, comparing their financial viability based on the different appraisal methods. The analysis covers ARR, Payback Period, NPV, and IRR to determine the most suitable investment options. The report concludes with recommendations on how companies can efficiently obtain funds for financing projects, providing a valuable resource for understanding and applying investment appraisal techniques in both public and private sectors. The document is contributed by a student to be published on the website Desklib.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.