FIN205 Business Finance Report: Stock Market Analysis and Investment

VerifiedAdded on 2022/10/11

|13

|1614

|11

Report

AI Summary

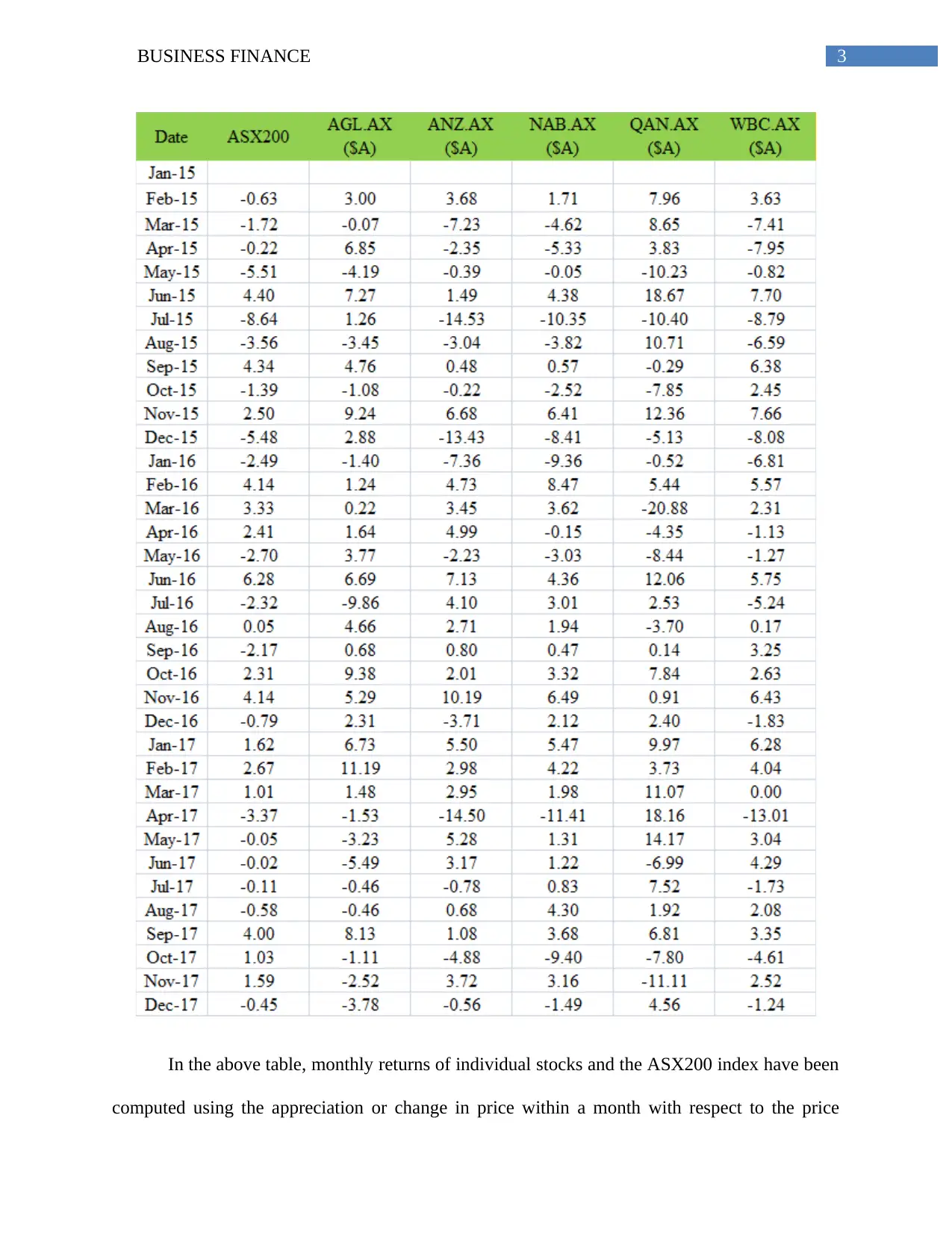

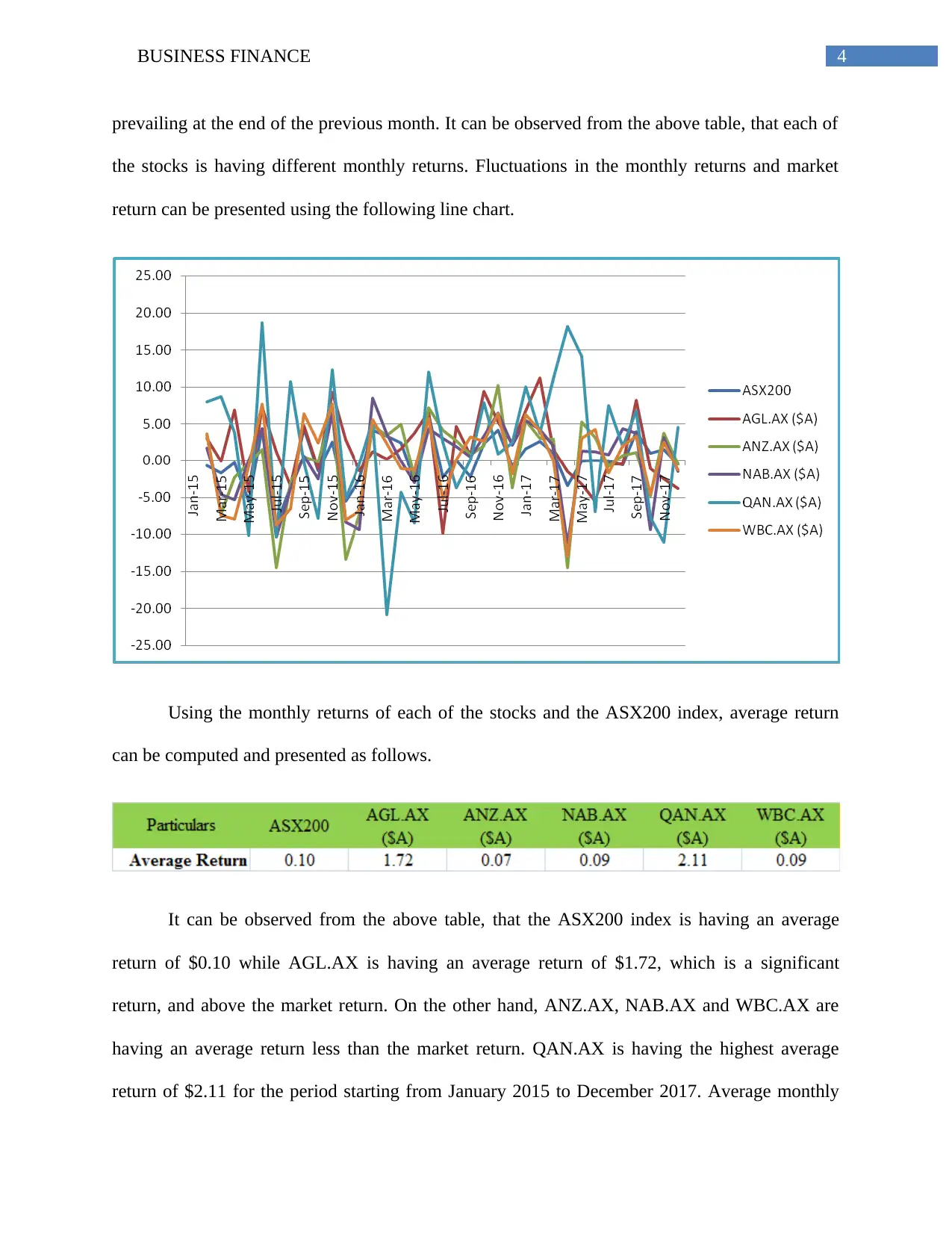

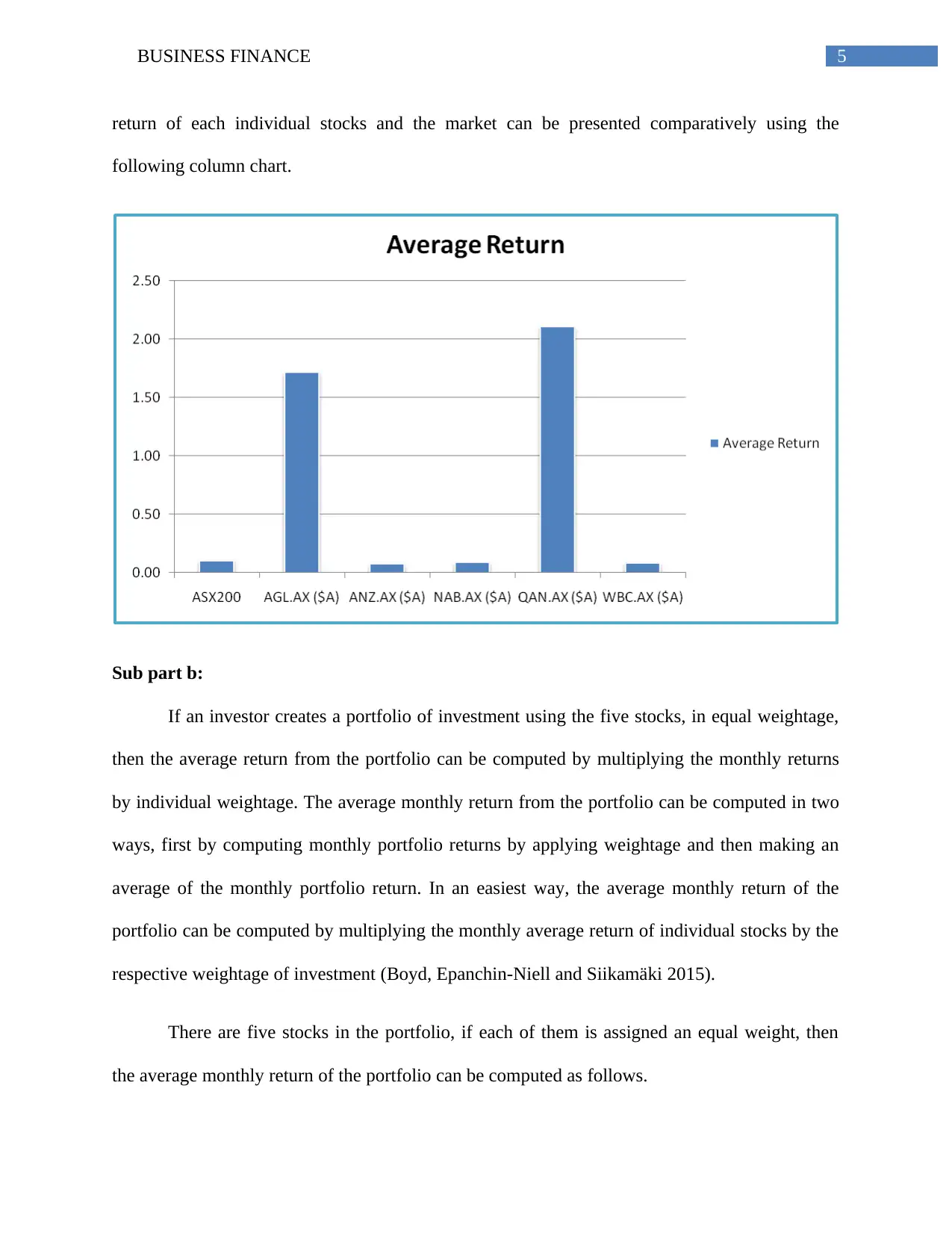

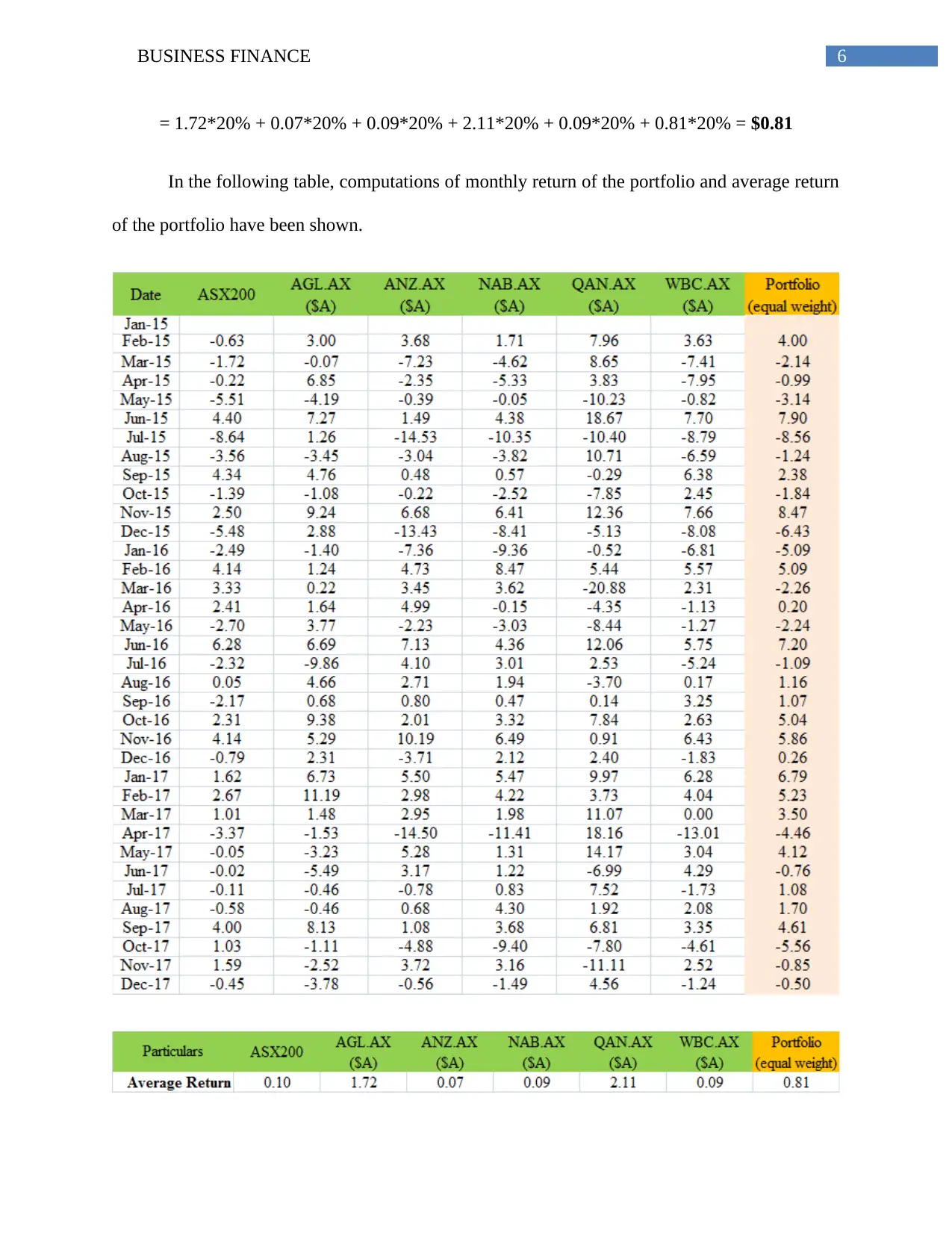

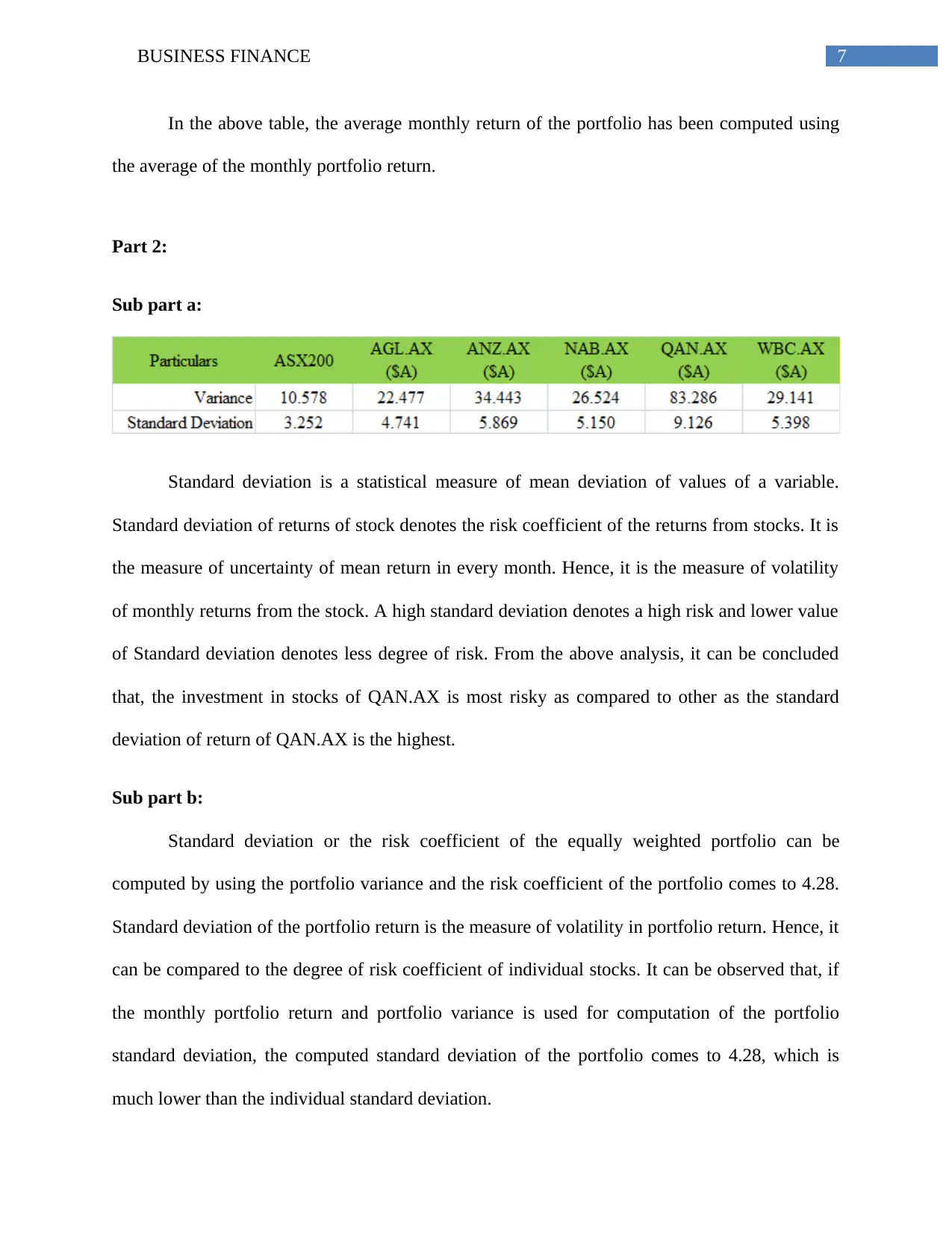

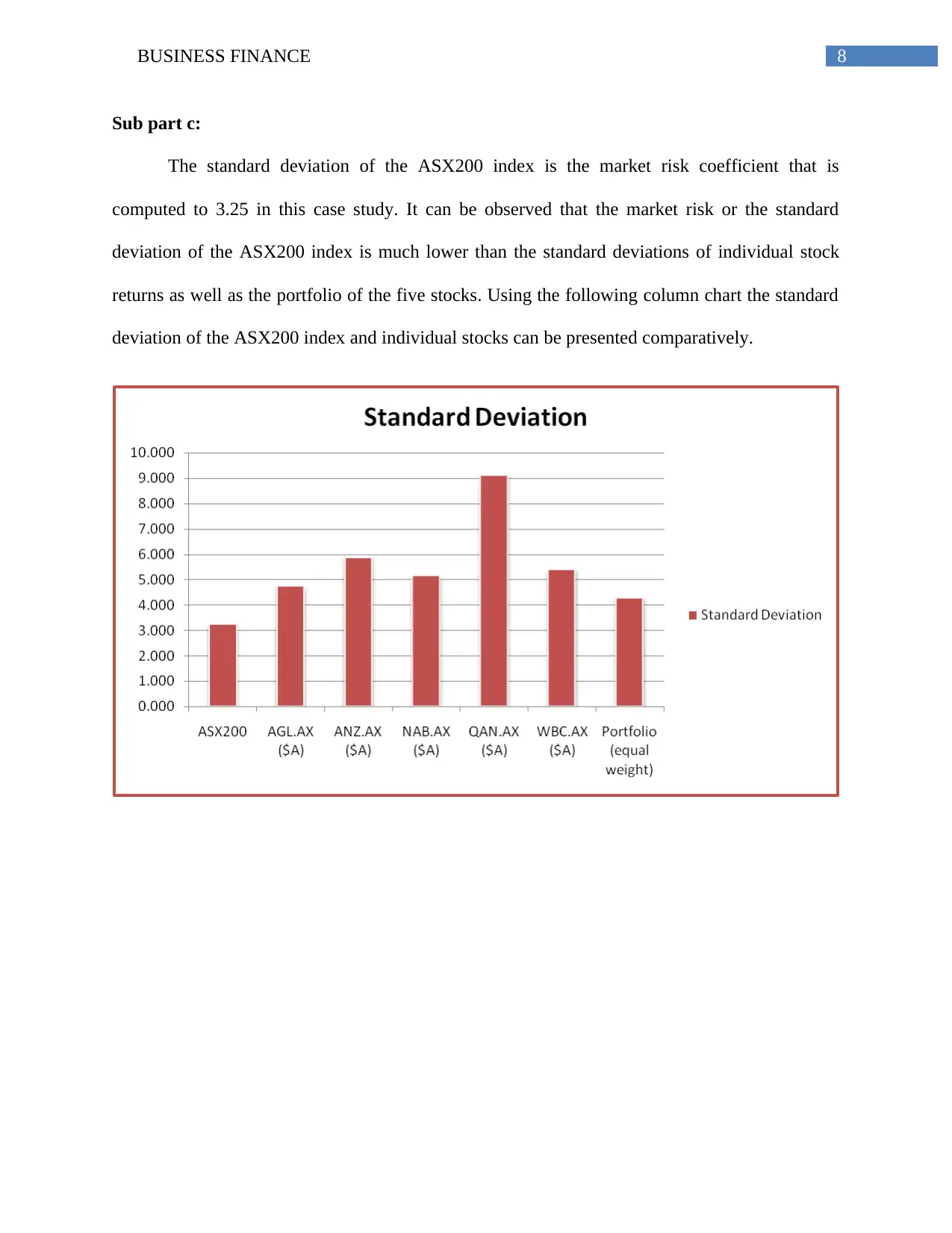

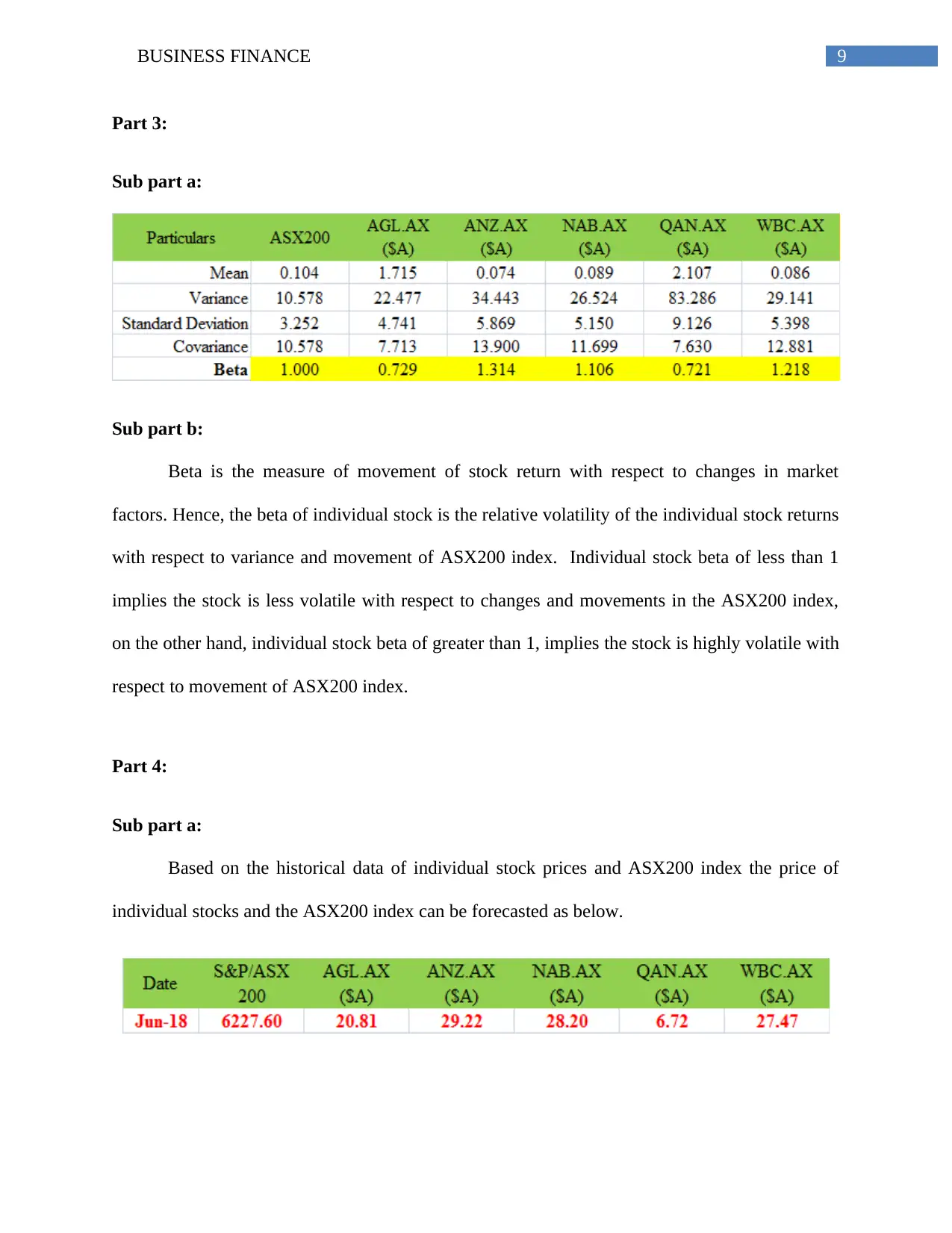

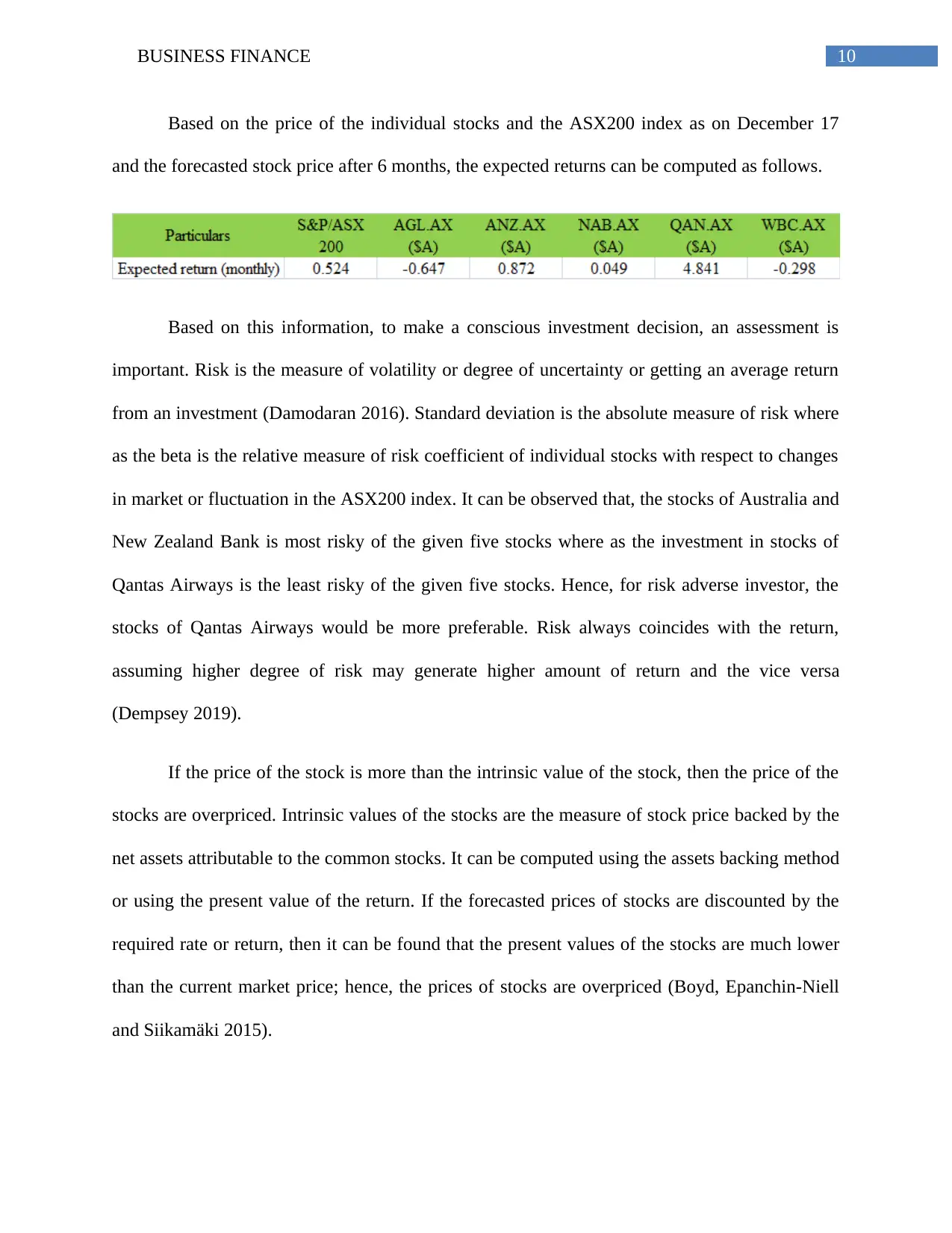

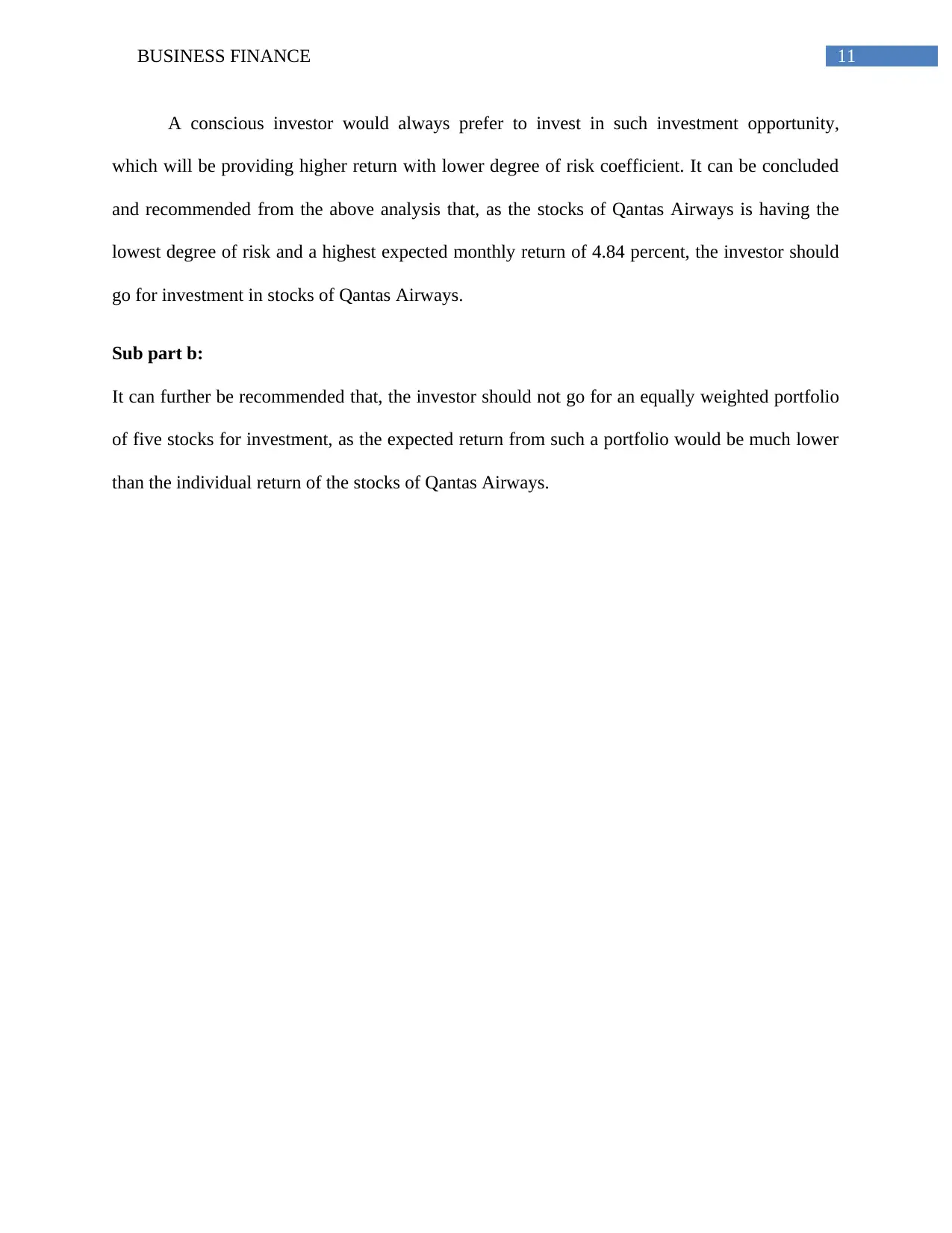

This report analyzes stock data from January 2015 to December 2017, focusing on individual stock returns and the ASX200 index. It computes average monthly returns, standard deviations, and betas for various stocks, including AGL.AX, ANZ.AX, NAB.AX, WBC.AX, QAN.AX. The report examines portfolio construction, risk assessment, and financial forecasting, providing insights into investment strategies and recommendations for investors. It calculates portfolio returns, standard deviations, and beta coefficients. Furthermore, it forecasts future stock prices and assesses investment risks, recommending investment in Qantas Airways due to its lower risk and higher expected return. The report also discusses the concept of intrinsic value and overpricing of stocks.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.