FIN200 Business Finance: Capital Budgeting and Investment Analysis

VerifiedAdded on 2023/04/26

|9

|1673

|61

Report

AI Summary

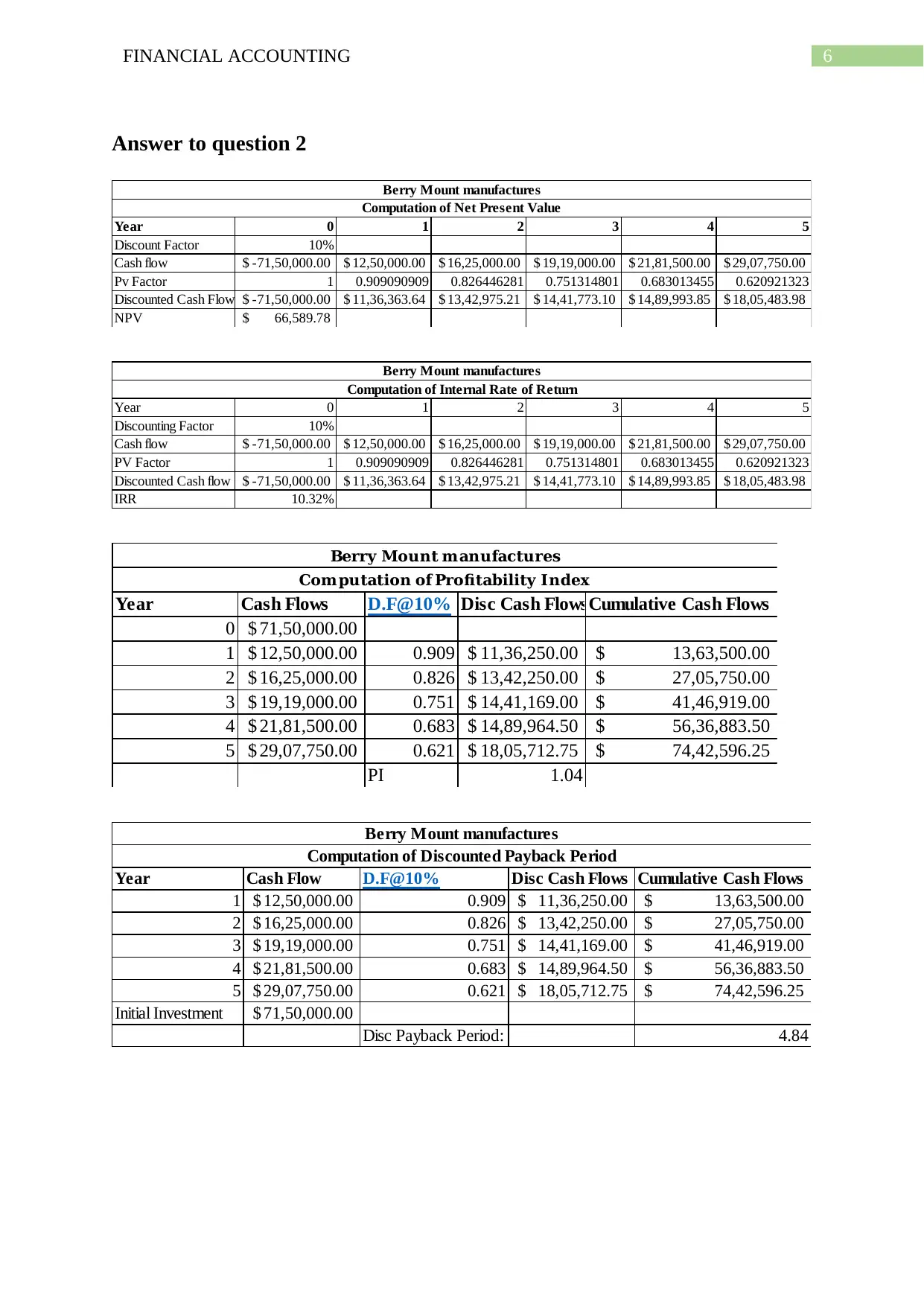

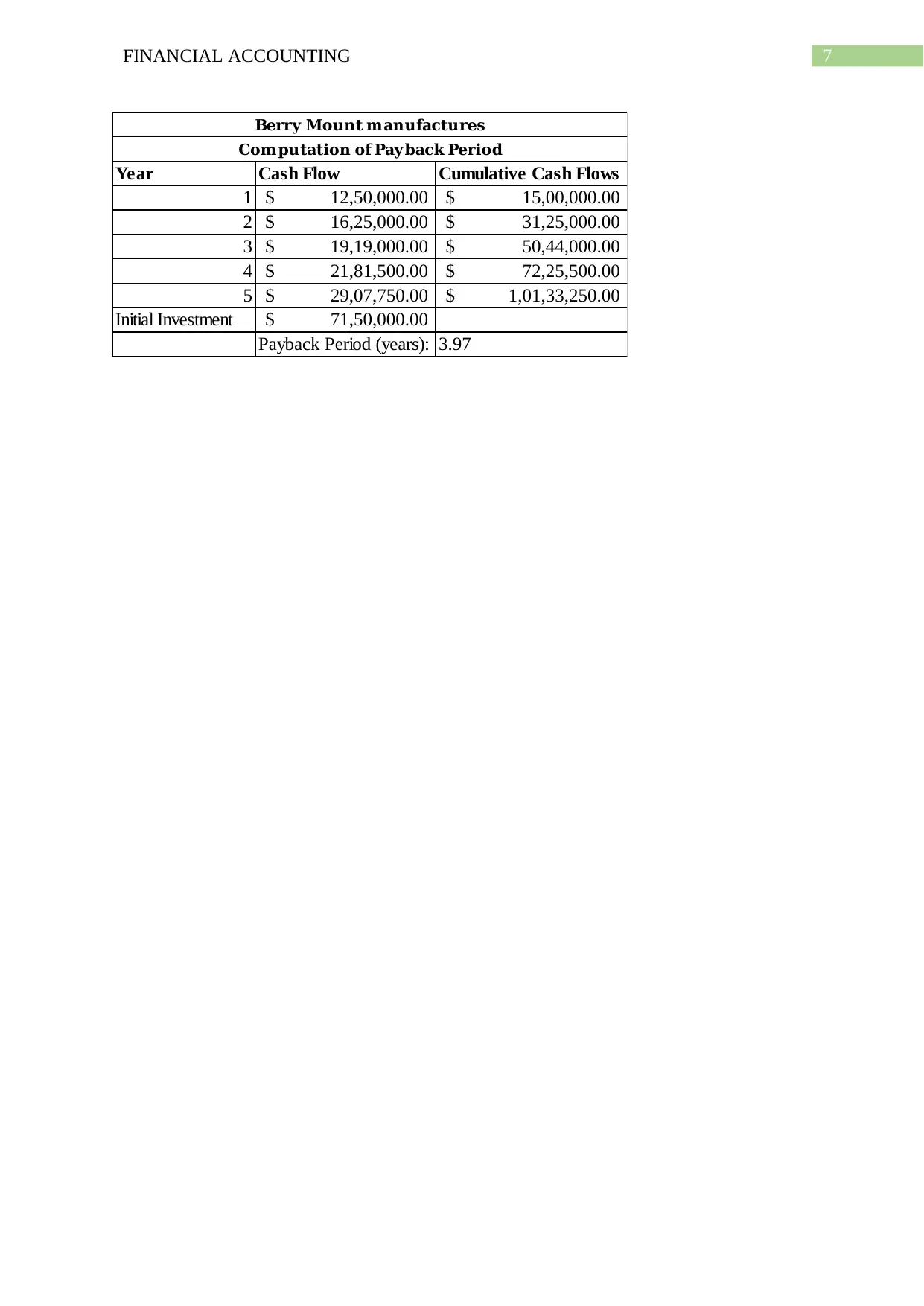

This report provides a comprehensive analysis of capital budgeting techniques, focusing on sensitivity analysis and scenario analysis. It explains how these methods are used to evaluate investment opportunities by considering various factors like cash flows, project life, and discounting factors. The report details the merits and demerits of each analysis, emphasizing the importance of identifying key variables and potential uncertainties in investment decisions. Additionally, the report includes a practical application of capital budgeting techniques to a case study involving Berry Mount, calculating Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index (PI), and payback periods to assess the viability of a new product launch. The analysis utilizes different discounting factors and cash flow projections to provide a thorough evaluation of the investment.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.