EPM5750 Project Investment Analysis: City Highrise Complex

VerifiedAdded on 2023/06/04

|23

|4698

|125

Report

AI Summary

This report presents a financial evaluation of the City Highrise project, involving the demolition of an existing building and the construction of a new complex. The evaluation incorporates income and cost approaches, analyzing development costs, cash expenditures, and risk assessments using scenario analysis to determine optimistic and pessimistic project outcomes. Key factors include the potential acquisition of the project by John Willey Pty Ltd at a 5% premium, the impact of changing financing structures, and a thorough risk assessment. The report forecasts revenue and costs, considering inflation rates of 4% and 6% at different project phases, and assesses the project's financial sustainability under various business and economic conditions. The analysis includes a letter of advice, an executive summary, and detailed discussions and recommendations based on the findings.

Running head: REAL ESTATE EVALAUTION

Real Estate Evaluation

Name of the Student:

Name of the University:

Author’s Note:

Real Estate Evaluation

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REAL ESTATE EVALUATION

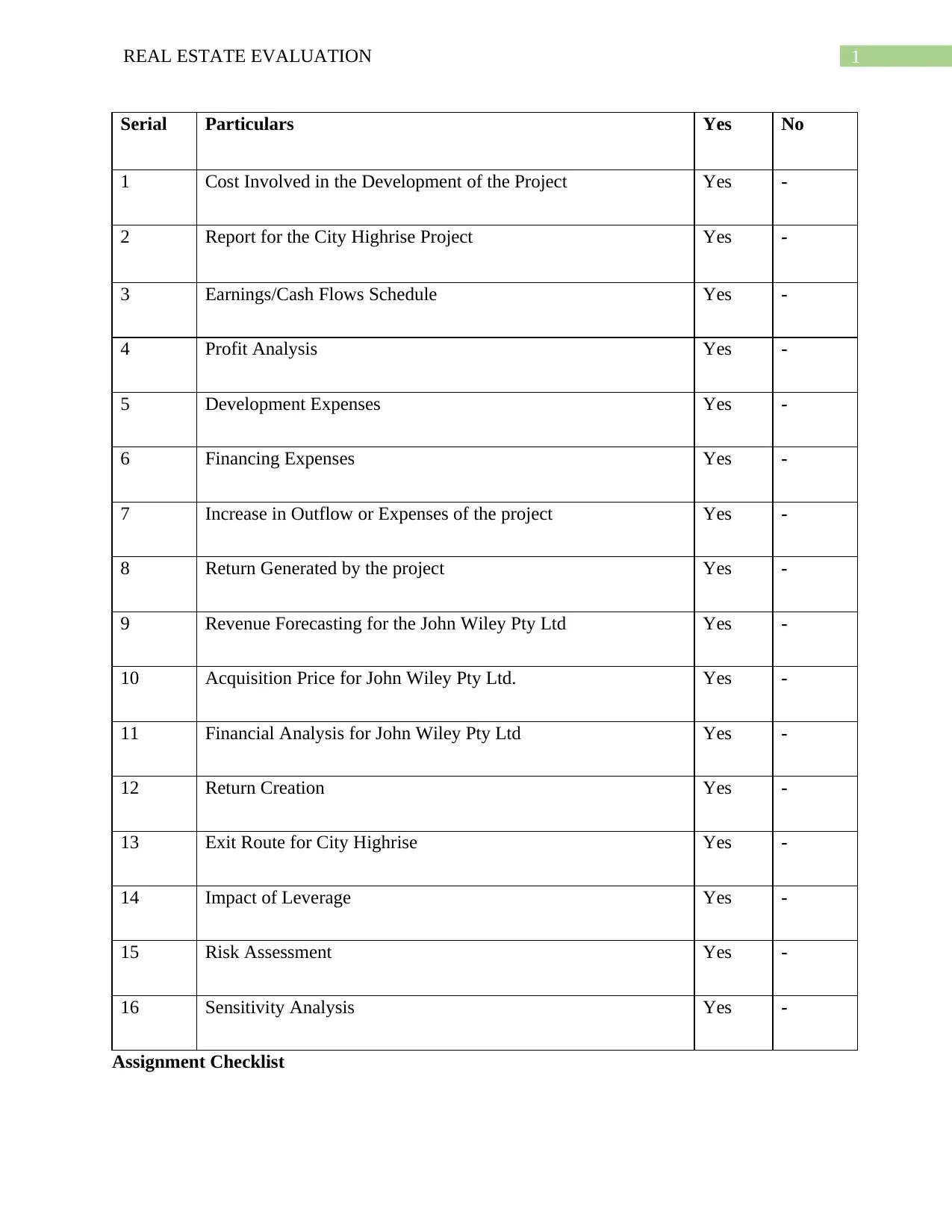

Serial Particulars Yes No

1 Cost Involved in the Development of the Project Yes -

2 Report for the City Highrise Project Yes -

3 Earnings/Cash Flows Schedule Yes -

4 Profit Analysis Yes -

5 Development Expenses Yes -

6 Financing Expenses Yes -

7 Increase in Outflow or Expenses of the project Yes -

8 Return Generated by the project Yes -

9 Revenue Forecasting for the John Wiley Pty Ltd Yes -

10 Acquisition Price for John Wiley Pty Ltd. Yes -

11 Financial Analysis for John Wiley Pty Ltd Yes -

12 Return Creation Yes -

13 Exit Route for City Highrise Yes -

14 Impact of Leverage Yes -

15 Risk Assessment Yes -

16 Sensitivity Analysis Yes -

Assignment Checklist

Serial Particulars Yes No

1 Cost Involved in the Development of the Project Yes -

2 Report for the City Highrise Project Yes -

3 Earnings/Cash Flows Schedule Yes -

4 Profit Analysis Yes -

5 Development Expenses Yes -

6 Financing Expenses Yes -

7 Increase in Outflow or Expenses of the project Yes -

8 Return Generated by the project Yes -

9 Revenue Forecasting for the John Wiley Pty Ltd Yes -

10 Acquisition Price for John Wiley Pty Ltd. Yes -

11 Financial Analysis for John Wiley Pty Ltd Yes -

12 Return Creation Yes -

13 Exit Route for City Highrise Yes -

14 Impact of Leverage Yes -

15 Risk Assessment Yes -

16 Sensitivity Analysis Yes -

Assignment Checklist

2REAL ESTATE EVALUATION

Table of Contents

Letter of Advice...............................................................................................................................3

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................6

Assumptions....................................................................................................................................6

Methodology....................................................................................................................................7

Spreadsheet and Evaluation of the Factors Evaluated.....................................................................8

Discussion and Recommendations................................................................................................13

Risks and Sensitivity Analysis................................................................................................13

Risk Evaluation of City Highrise project..............................................................................13

Exit Route Evaluation.............................................................................................................15

Annual Cash Flow for John Wiley Pty Ltd...........................................................................16

Analysis of the Project under Scenario 2 for John Wiley Pty Ltd......................................18

Return from Project under Scenario 2..................................................................................19

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

Table of Contents

Letter of Advice...............................................................................................................................3

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................6

Assumptions....................................................................................................................................6

Methodology....................................................................................................................................7

Spreadsheet and Evaluation of the Factors Evaluated.....................................................................8

Discussion and Recommendations................................................................................................13

Risks and Sensitivity Analysis................................................................................................13

Risk Evaluation of City Highrise project..............................................................................13

Exit Route Evaluation.............................................................................................................15

Annual Cash Flow for John Wiley Pty Ltd...........................................................................16

Analysis of the Project under Scenario 2 for John Wiley Pty Ltd......................................18

Return from Project under Scenario 2..................................................................................19

Conclusion.....................................................................................................................................19

Reference.......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REAL ESTATE EVALUATION

Letter of Advice

Melbourne, VIC 3000

Telephone 28 8 3215 5000

www.mckenzieandassociate.com.au

28th September 2018

Mr Con Gomes,

The Managing Director

City Highrise Complex Development Option.

Level 6, 510 King William Street,

Adelaide SA 5000

Dear Mr. Gomes,

Sir it is to bring under your notice that the Financial evaluation for the Project City high rise was

evaluated where the cost and the revenue analysis was done for the project. Total development

cost was even determined for the project which gave us the estimate for the total cost that will be

incurred in the project due course of time. The financial evaluation and analysis done was based

Letter of Advice

Melbourne, VIC 3000

Telephone 28 8 3215 5000

www.mckenzieandassociate.com.au

28th September 2018

Mr Con Gomes,

The Managing Director

City Highrise Complex Development Option.

Level 6, 510 King William Street,

Adelaide SA 5000

Dear Mr. Gomes,

Sir it is to bring under your notice that the Financial evaluation for the Project City high rise was

evaluated where the cost and the revenue analysis was done for the project. Total development

cost was even determined for the project which gave us the estimate for the total cost that will be

incurred in the project due course of time. The financial evaluation and analysis done was based

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REAL ESTATE EVALUATION

on assumptions and facts that the company may face at the time for the construction of the

project.

The different components and factors were evaluated on the base that the factors for

estimating the project revenue and expenses such as the construction expenses, development

expenses and the escalation and outgoing costs could have probable impacts on the project.

Present breakdowns and scenario project Investment Analysis was done on different

grounds and different scenarios where the project scenario could be determined under the

optimistic and pessimistic scenario. Scenario Analysis and the risk assessment and analysis

helped us gain an scenario under which the project could land up. The exit rout and the price for

selling the developed project to John Willey Pty Ltd Company and the developers profit arising

from the same were the key factors evaluated and included in the project.

Please feel free to get in touch with us in case of any concern or query.

Yours Sincerely

Financial Adviser

Real Estate Developer

on assumptions and facts that the company may face at the time for the construction of the

project.

The different components and factors were evaluated on the base that the factors for

estimating the project revenue and expenses such as the construction expenses, development

expenses and the escalation and outgoing costs could have probable impacts on the project.

Present breakdowns and scenario project Investment Analysis was done on different

grounds and different scenarios where the project scenario could be determined under the

optimistic and pessimistic scenario. Scenario Analysis and the risk assessment and analysis

helped us gain an scenario under which the project could land up. The exit rout and the price for

selling the developed project to John Willey Pty Ltd Company and the developers profit arising

from the same were the key factors evaluated and included in the project.

Please feel free to get in touch with us in case of any concern or query.

Yours Sincerely

Financial Adviser

Real Estate Developer

5REAL ESTATE EVALUATION

Executive Summary

The aim for the project is to evaluate a Real Estate project that is the City Highrise project. The

analysis and the evaluation of the project was done on the basis of the cost and the revenue

implied by the project. The City Highrise project has been divided into different scenarios where

the project commences with the demolition of the existing building and the construction and the

planning and the development of the new project. The approaches used for the valuation of the

project was the income and the cost approach for the City Highrise Project. The development

cost breakdown along with the cash expenditure involved for constructing the complex was

carefully analyzed. The risk assessment for the project was done by using the risk assessment

tools such as the scenario analysis, which gave us an optimistic and pessimistic scenario for

conducting and the final evaluation of the project.

Executive Summary

The aim for the project is to evaluate a Real Estate project that is the City Highrise project. The

analysis and the evaluation of the project was done on the basis of the cost and the revenue

implied by the project. The City Highrise project has been divided into different scenarios where

the project commences with the demolition of the existing building and the construction and the

planning and the development of the new project. The approaches used for the valuation of the

project was the income and the cost approach for the City Highrise Project. The development

cost breakdown along with the cash expenditure involved for constructing the complex was

carefully analyzed. The risk assessment for the project was done by using the risk assessment

tools such as the scenario analysis, which gave us an optimistic and pessimistic scenario for

conducting and the final evaluation of the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REAL ESTATE EVALUATION

Introduction

The project evaluation for the City Highrise Project is the main evaluation done under the

project. The project evaluation and assessment was based on the fact that the project will be

distributed in three major parts where each factor and scenario has its role to play. The

demolition phase, construction, planning and designing along with the cost involved with the

same were the key reasons that were evaluated while assessing the project. The financial

evaluation was done and the forecasting of revenue and the costs associated was performed on

the project to get a financial sustainability for the project. The project revenue breakdown along

with the costs associated such as development, construction were forecasted with the inflation

forecast, which was assumed to be 4% and 6% at the different phase of the project (Kuhle and

Lin 2018).

The other part of the project was evaluated on the basis of the fact that the project will be

acquired by the John Willey Pty Ltd which will acquire the project at 5% premium from the

Developer. The assumptions and factors considered for the same were highlighted in the same.

The other part of the project deals with the changing financing structure and the impact of the

changing financial leverage on the company and the associated financing costs (Pengyan and

Chao 2016). The final part of the project deals with the risk assessment of the undertaken project.

The key financial evaluation and assessment of the project with the above scenarios and

by distributing the projects into different phase helped us gain what the project forecast could be

depending on certain business, economic and other factors that may influence the project.

Introduction

The project evaluation for the City Highrise Project is the main evaluation done under the

project. The project evaluation and assessment was based on the fact that the project will be

distributed in three major parts where each factor and scenario has its role to play. The

demolition phase, construction, planning and designing along with the cost involved with the

same were the key reasons that were evaluated while assessing the project. The financial

evaluation was done and the forecasting of revenue and the costs associated was performed on

the project to get a financial sustainability for the project. The project revenue breakdown along

with the costs associated such as development, construction were forecasted with the inflation

forecast, which was assumed to be 4% and 6% at the different phase of the project (Kuhle and

Lin 2018).

The other part of the project was evaluated on the basis of the fact that the project will be

acquired by the John Willey Pty Ltd which will acquire the project at 5% premium from the

Developer. The assumptions and factors considered for the same were highlighted in the same.

The other part of the project deals with the changing financing structure and the impact of the

changing financial leverage on the company and the associated financing costs (Pengyan and

Chao 2016). The final part of the project deals with the risk assessment of the undertaken project.

The key financial evaluation and assessment of the project with the above scenarios and

by distributing the projects into different phase helped us gain what the project forecast could be

depending on certain business, economic and other factors that may influence the project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REAL ESTATE EVALUATION

Assumptions

The key assumptions used in the project was the inclusion of the construction cost, which is of

around 300 million that will be incurred in cash. The relevant financing costs and the interest

expense for the same will be applicable. The approach used for valuation of the project was the

cost approach and the approach used for assessing the income of the project was the use of the

income project (Wu and Kou 2016). The inflation forecast was broken down into two parts

where the inflation for the first year will be 4% p.a. for the total amount of the cost or the amount

spend that is the 40% of the total cost. The rest 60% of the total development costs will be

expensed at the rate of 6% per annum. The different phase of the project was divided into

different time period for the project, The distribution of the different time period for the complex

development project will be assessed based on the fact that the same will provide proper

distribution of the project. The relevant financing cost considered for the same was around 125

of the total amount of debt borrowed.

Methodology

The cash flow analysis for the project was based on the act that the revenue will be

escalated at 4%p.a and the annual increase in the revenue will be at 4% p.a for the first year

when the development expense will be around 40%. The remaining 60% of the total cost was

accounted with the fact that the inflation escalation will be at 6% p.a. The development cost and

the total cash expenditure paid for the development of the project was divided into factors, which

helped us asses the total cost. The final part of the project, which is the sale of the project to John

Willey Pty Ltd the cost at which the acquisition will be done. The acquisition will be done at 5%

per annum of the total development cost. The revenue forecast for the company was done for the

John Willey Pty Ltd was done at the 4% increase per year (Fu et al. 2015).

Assumptions

The key assumptions used in the project was the inclusion of the construction cost, which is of

around 300 million that will be incurred in cash. The relevant financing costs and the interest

expense for the same will be applicable. The approach used for valuation of the project was the

cost approach and the approach used for assessing the income of the project was the use of the

income project (Wu and Kou 2016). The inflation forecast was broken down into two parts

where the inflation for the first year will be 4% p.a. for the total amount of the cost or the amount

spend that is the 40% of the total cost. The rest 60% of the total development costs will be

expensed at the rate of 6% per annum. The different phase of the project was divided into

different time period for the project, The distribution of the different time period for the complex

development project will be assessed based on the fact that the same will provide proper

distribution of the project. The relevant financing cost considered for the same was around 125

of the total amount of debt borrowed.

Methodology

The cash flow analysis for the project was based on the act that the revenue will be

escalated at 4%p.a and the annual increase in the revenue will be at 4% p.a for the first year

when the development expense will be around 40%. The remaining 60% of the total cost was

accounted with the fact that the inflation escalation will be at 6% p.a. The development cost and

the total cash expenditure paid for the development of the project was divided into factors, which

helped us asses the total cost. The final part of the project, which is the sale of the project to John

Willey Pty Ltd the cost at which the acquisition will be done. The acquisition will be done at 5%

per annum of the total development cost. The revenue forecast for the company was done for the

John Willey Pty Ltd was done at the 4% increase per year (Fu et al. 2015).

8REAL ESTATE EVALUATION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REAL ESTATE EVALUATION

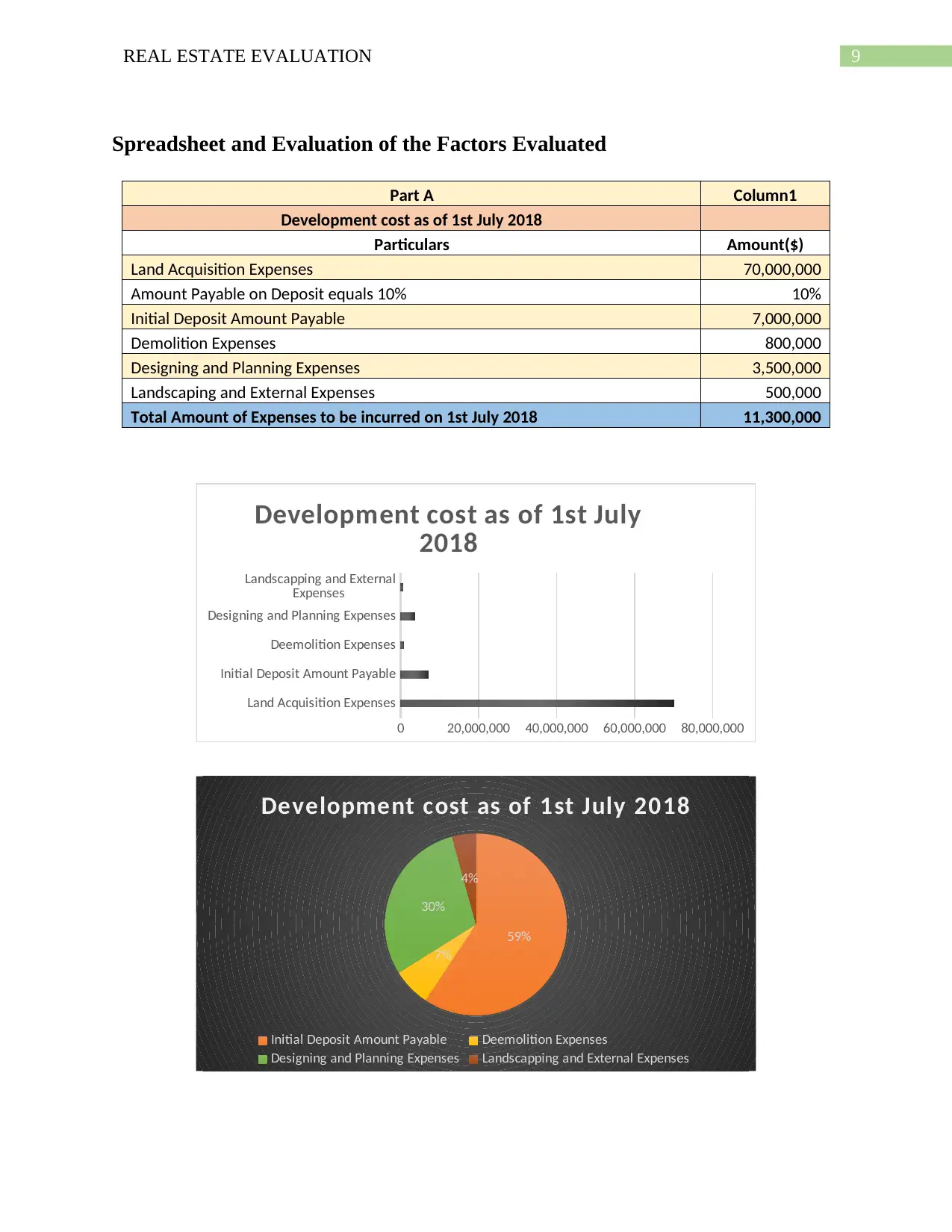

Spreadsheet and Evaluation of the Factors Evaluated

Part A Column1

Development cost as of 1st July 2018

Particulars Amount($)

Land Acquisition Expenses 70,000,000

Amount Payable on Deposit equals 10% 10%

Initial Deposit Amount Payable 7,000,000

Demolition Expenses 800,000

Designing and Planning Expenses 3,500,000

Landscaping and External Expenses 500,000

Total Amount of Expenses to be incurred on 1st July 2018 11,300,000

Land Acquisition Expenses

Initial Deposit Amount Payable

Deemolition Expenses

Designing and Planning Expenses

Landscapping and External

Expenses

0 20,000,000 40,000,000 60,000,000 80,000,000

Development cost as of 1st July

2018

59%

7%

30%

4%

Development cost as of 1st July 2018

Initial Deposit Amount Payable Deemolition Expenses

Designing and Planning Expenses Landscapping and External Expenses

Spreadsheet and Evaluation of the Factors Evaluated

Part A Column1

Development cost as of 1st July 2018

Particulars Amount($)

Land Acquisition Expenses 70,000,000

Amount Payable on Deposit equals 10% 10%

Initial Deposit Amount Payable 7,000,000

Demolition Expenses 800,000

Designing and Planning Expenses 3,500,000

Landscaping and External Expenses 500,000

Total Amount of Expenses to be incurred on 1st July 2018 11,300,000

Land Acquisition Expenses

Initial Deposit Amount Payable

Deemolition Expenses

Designing and Planning Expenses

Landscapping and External

Expenses

0 20,000,000 40,000,000 60,000,000 80,000,000

Development cost as of 1st July

2018

59%

7%

30%

4%

Development cost as of 1st July 2018

Initial Deposit Amount Payable Deemolition Expenses

Designing and Planning Expenses Landscapping and External Expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REAL ESTATE EVALUATION

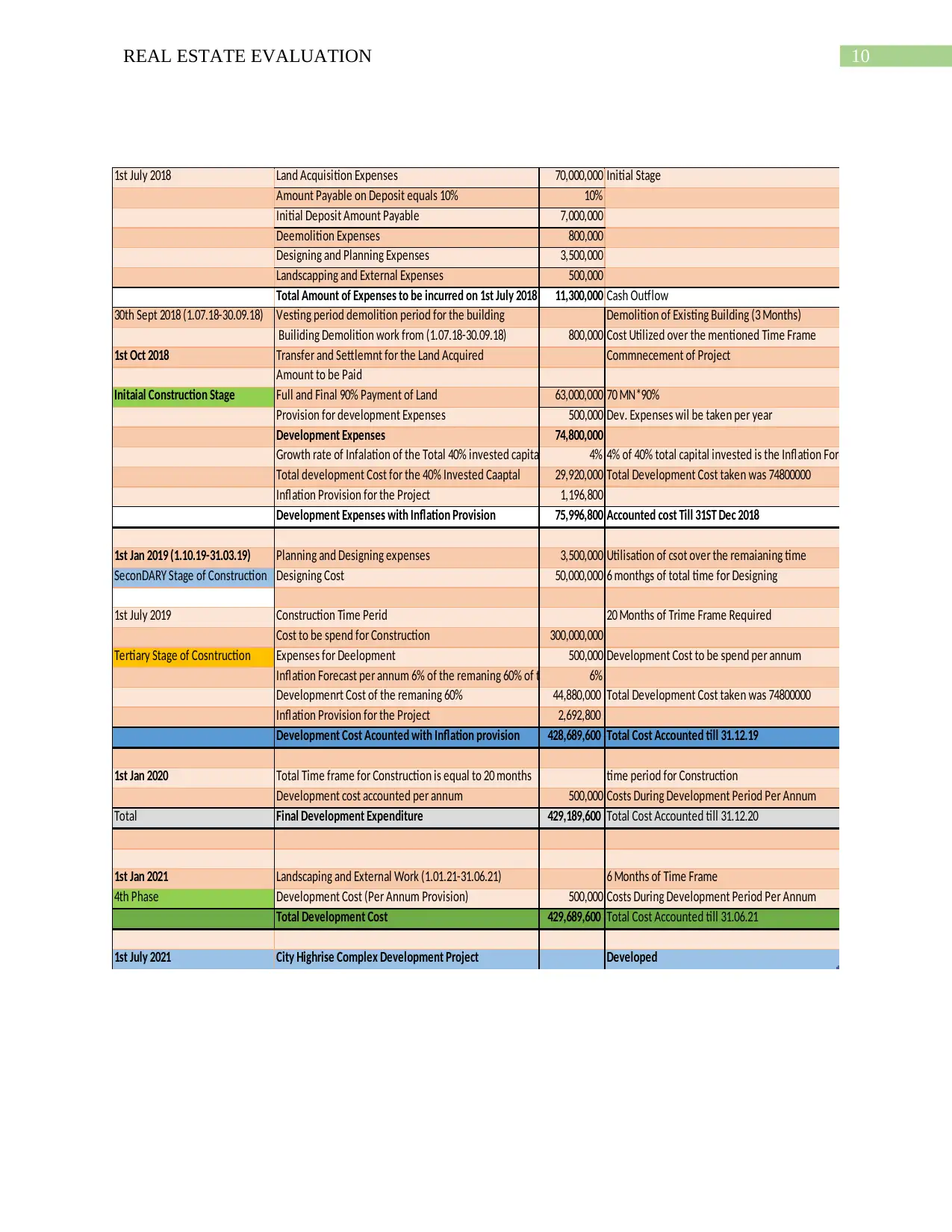

1st July 2018 Land Acquisition Expenses 70,000,000 Initial Stage

Amount Payable on Deposit equals 10% 10%

Initial Deposit Amount Payable 7,000,000

Deemolition Expenses 800,000

Designing and Planning Expenses 3,500,000

Landscapping and External Expenses 500,000

Total Amount of Expenses to be incurred on 1st July 2018 11,300,000 Cash Outflow

30th Sept 2018 (1.07.18-30.09.18) Vesting period demolition period for the building Demolition of Existing Building (3 Months)

Builiding Demolition work from (1.07.18-30.09.18) 800,000 Cost Utilized over the mentioned Time Frame

1st Oct 2018 Transfer and Settlemnt for the Land Acquired Commnecement of Project

Amount to be Paid

Initaial Construction Stage Full and Final 90% Payment of Land 63,000,000 70 MN*90%

Provision for development Expenses 500,000 Dev. Expenses wil be taken per year

Development Expenses 74,800,000

Growth rate of Infalation of the Total 40% invested capital 4% 4% of 40% total capital invested is the Inflation Forecast

Total development Cost for the 40% Invested Caaptal 29,920,000 Total Development Cost taken was 74800000

Inflation Provision for the Project 1,196,800

Development Expenses with Inflation Provision 75,996,800 Accounted cost Till 31ST Dec 2018

1st Jan 2019 (1.10.19-31.03.19) Planning and Designing expenses 3,500,000 Utilisation of csot over the remaianing time

SeconDARY Stage of Construction Designing Cost 50,000,000 6 monthgs of total time for Designing

1st July 2019 Construction Time Perid 20 Months of Trime Frame Required

Cost to be spend for Construction 300,000,000

Tertiary Stage of Cosntruction Expenses for Deelopment 500,000 Development Cost to be spend per annum

Inflation Forecast per annum 6% of the remaning 60% of total assignment6%

Developmenrt Cost of the remaning 60% 44,880,000 Total Development Cost taken was 74800000

Inflation Provision for the Project 2,692,800

Development Cost Acounted with Inflation provision 428,689,600 Total Cost Accounted till 31.12.19

1st Jan 2020 Total Time frame for Construction is equal to 20 months time period for Construction

Development cost accounted per annum 500,000 Costs During Development Period Per Annum

Total Final Development Expenditure 429,189,600 Total Cost Accounted till 31.12.20

1st Jan 2021 Landscaping and External Work (1.01.21-31.06.21) 6 Months of Time Frame

4th Phase Development Cost (Per Annum Provision) 500,000 Costs During Development Period Per Annum

Total Development Cost 429,689,600 Total Cost Accounted till 31.06.21

1st July 2021 City Highrise Complex Development Project Developed

1st July 2018 Land Acquisition Expenses 70,000,000 Initial Stage

Amount Payable on Deposit equals 10% 10%

Initial Deposit Amount Payable 7,000,000

Deemolition Expenses 800,000

Designing and Planning Expenses 3,500,000

Landscapping and External Expenses 500,000

Total Amount of Expenses to be incurred on 1st July 2018 11,300,000 Cash Outflow

30th Sept 2018 (1.07.18-30.09.18) Vesting period demolition period for the building Demolition of Existing Building (3 Months)

Builiding Demolition work from (1.07.18-30.09.18) 800,000 Cost Utilized over the mentioned Time Frame

1st Oct 2018 Transfer and Settlemnt for the Land Acquired Commnecement of Project

Amount to be Paid

Initaial Construction Stage Full and Final 90% Payment of Land 63,000,000 70 MN*90%

Provision for development Expenses 500,000 Dev. Expenses wil be taken per year

Development Expenses 74,800,000

Growth rate of Infalation of the Total 40% invested capital 4% 4% of 40% total capital invested is the Inflation Forecast

Total development Cost for the 40% Invested Caaptal 29,920,000 Total Development Cost taken was 74800000

Inflation Provision for the Project 1,196,800

Development Expenses with Inflation Provision 75,996,800 Accounted cost Till 31ST Dec 2018

1st Jan 2019 (1.10.19-31.03.19) Planning and Designing expenses 3,500,000 Utilisation of csot over the remaianing time

SeconDARY Stage of Construction Designing Cost 50,000,000 6 monthgs of total time for Designing

1st July 2019 Construction Time Perid 20 Months of Trime Frame Required

Cost to be spend for Construction 300,000,000

Tertiary Stage of Cosntruction Expenses for Deelopment 500,000 Development Cost to be spend per annum

Inflation Forecast per annum 6% of the remaning 60% of total assignment6%

Developmenrt Cost of the remaning 60% 44,880,000 Total Development Cost taken was 74800000

Inflation Provision for the Project 2,692,800

Development Cost Acounted with Inflation provision 428,689,600 Total Cost Accounted till 31.12.19

1st Jan 2020 Total Time frame for Construction is equal to 20 months time period for Construction

Development cost accounted per annum 500,000 Costs During Development Period Per Annum

Total Final Development Expenditure 429,189,600 Total Cost Accounted till 31.12.20

1st Jan 2021 Landscaping and External Work (1.01.21-31.06.21) 6 Months of Time Frame

4th Phase Development Cost (Per Annum Provision) 500,000 Costs During Development Period Per Annum

Total Development Cost 429,689,600 Total Cost Accounted till 31.06.21

1st July 2021 City Highrise Complex Development Project Developed

11REAL ESTATE EVALUATION

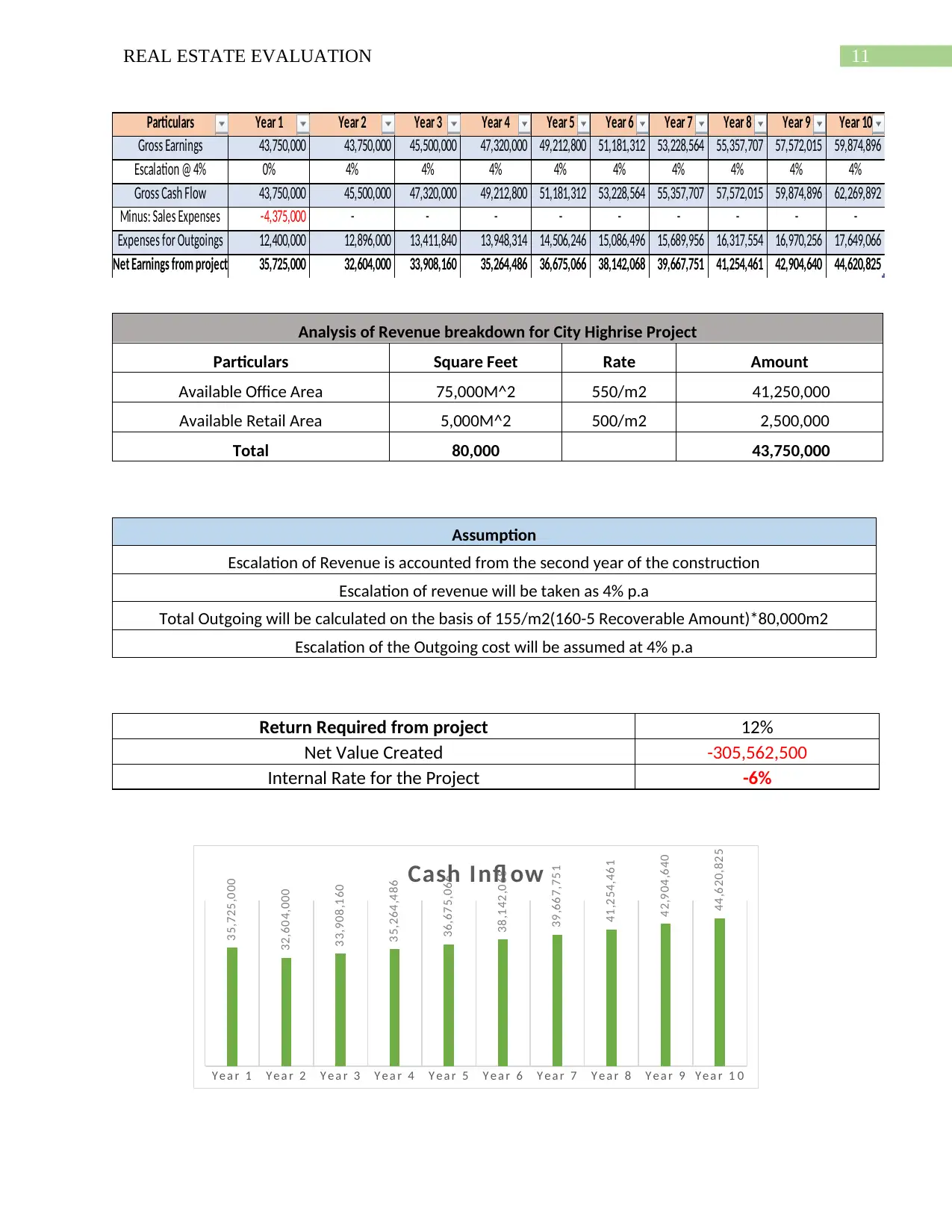

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Gross Earnings 43,750,000 43,750,000 45,500,000 47,320,000 49,212,800 51,181,312 53,228,564 55,357,707 57,572,015 59,874,896

Escalation @ 4% 0% 4% 4% 4% 4% 4% 4% 4% 4% 4%

Gross Cash Flow 43,750,000 45,500,000 47,320,000 49,212,800 51,181,312 53,228,564 55,357,707 57,572,015 59,874,896 62,269,892

Minus: Sales Expenses -4,375,000 - - - - - - - - -

Expenses for Outgoings 12,400,000 12,896,000 13,411,840 13,948,314 14,506,246 15,086,496 15,689,956 16,317,554 16,970,256 17,649,066

Net Earnings from project 35,725,000 32,604,000 33,908,160 35,264,486 36,675,066 38,142,068 39,667,751 41,254,461 42,904,640 44,620,825

Analysis of Revenue breakdown for City Highrise Project

Particulars Square Feet Rate Amount

Available Office Area 75,000M^2 550/m2 41,250,000

Available Retail Area 5,000M^2 500/m2 2,500,000

Total 80,000 43,750,000

Assumption

Escalation of Revenue is accounted from the second year of the construction

Escalation of revenue will be taken as 4% p.a

Total Outgoing will be calculated on the basis of 155/m2(160-5 Recoverable Amount)*80,000m2

Escalation of the Outgoing cost will be assumed at 4% p.a

Return Required from project 12%

Net Value Created -305,562,500

Internal Rate for the Project -6%

Y e a r 1 Y e a r 2 Y e a r 3 Y e a r 4 Y e a r 5 Y e a r 6 Y e a r 7 Y e a r 8 Y e a r 9 Y e a r 1 0

35,725,000

32,604,000

33,908,160

35,264,486

36,675,066

38,142,068

39,667,751

41,254,461

42,904,640

44,620,825

Cash Infl ow

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Gross Earnings 43,750,000 43,750,000 45,500,000 47,320,000 49,212,800 51,181,312 53,228,564 55,357,707 57,572,015 59,874,896

Escalation @ 4% 0% 4% 4% 4% 4% 4% 4% 4% 4% 4%

Gross Cash Flow 43,750,000 45,500,000 47,320,000 49,212,800 51,181,312 53,228,564 55,357,707 57,572,015 59,874,896 62,269,892

Minus: Sales Expenses -4,375,000 - - - - - - - - -

Expenses for Outgoings 12,400,000 12,896,000 13,411,840 13,948,314 14,506,246 15,086,496 15,689,956 16,317,554 16,970,256 17,649,066

Net Earnings from project 35,725,000 32,604,000 33,908,160 35,264,486 36,675,066 38,142,068 39,667,751 41,254,461 42,904,640 44,620,825

Analysis of Revenue breakdown for City Highrise Project

Particulars Square Feet Rate Amount

Available Office Area 75,000M^2 550/m2 41,250,000

Available Retail Area 5,000M^2 500/m2 2,500,000

Total 80,000 43,750,000

Assumption

Escalation of Revenue is accounted from the second year of the construction

Escalation of revenue will be taken as 4% p.a

Total Outgoing will be calculated on the basis of 155/m2(160-5 Recoverable Amount)*80,000m2

Escalation of the Outgoing cost will be assumed at 4% p.a

Return Required from project 12%

Net Value Created -305,562,500

Internal Rate for the Project -6%

Y e a r 1 Y e a r 2 Y e a r 3 Y e a r 4 Y e a r 5 Y e a r 6 Y e a r 7 Y e a r 8 Y e a r 9 Y e a r 1 0

35,725,000

32,604,000

33,908,160

35,264,486

36,675,066

38,142,068

39,667,751

41,254,461

42,904,640

44,620,825

Cash Infl ow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.