Investment Analysis Homework - Analyzing Bonds and Efficient Markets

VerifiedAdded on 2022/11/24

|7

|1522

|333

Homework Assignment

AI Summary

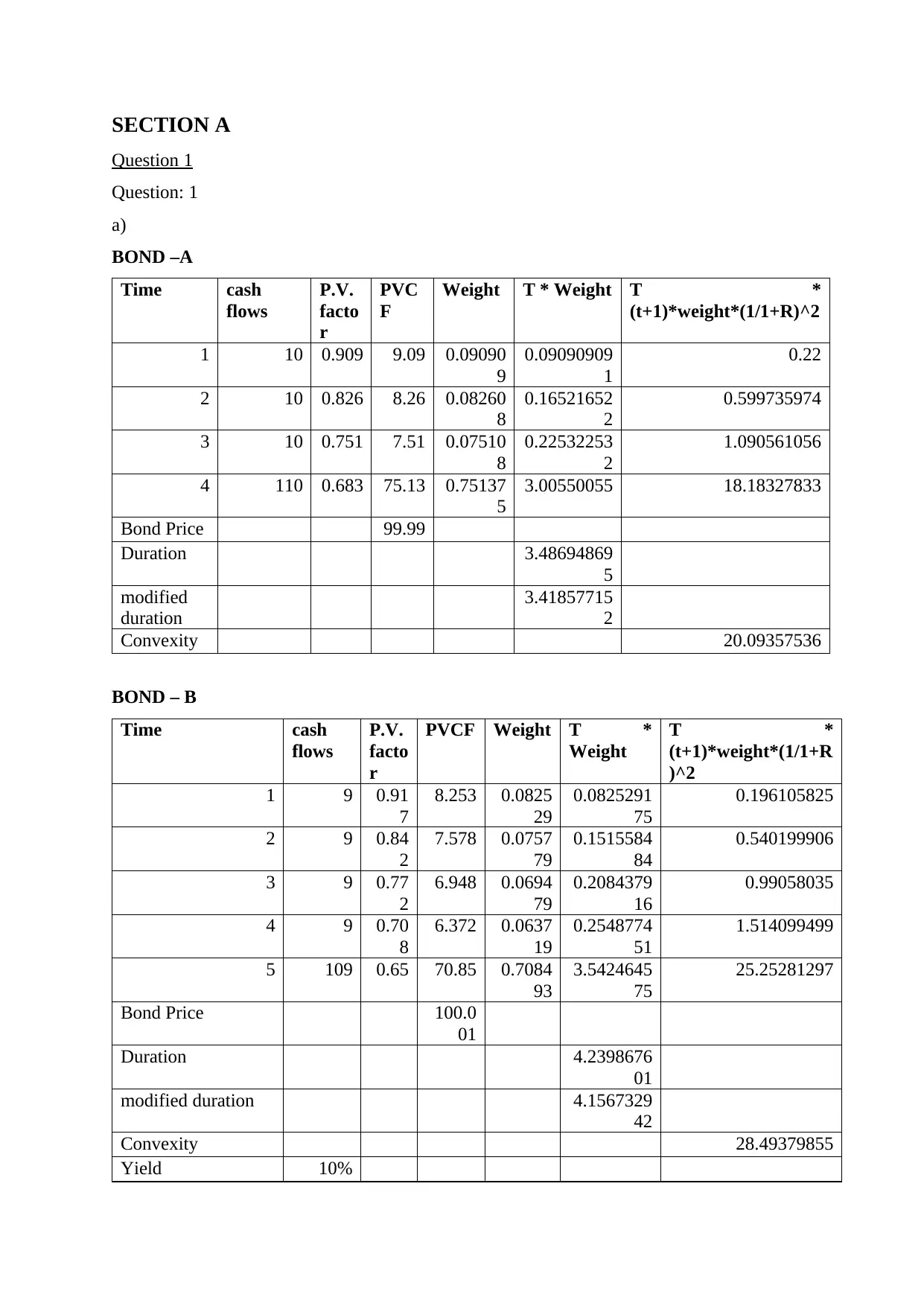

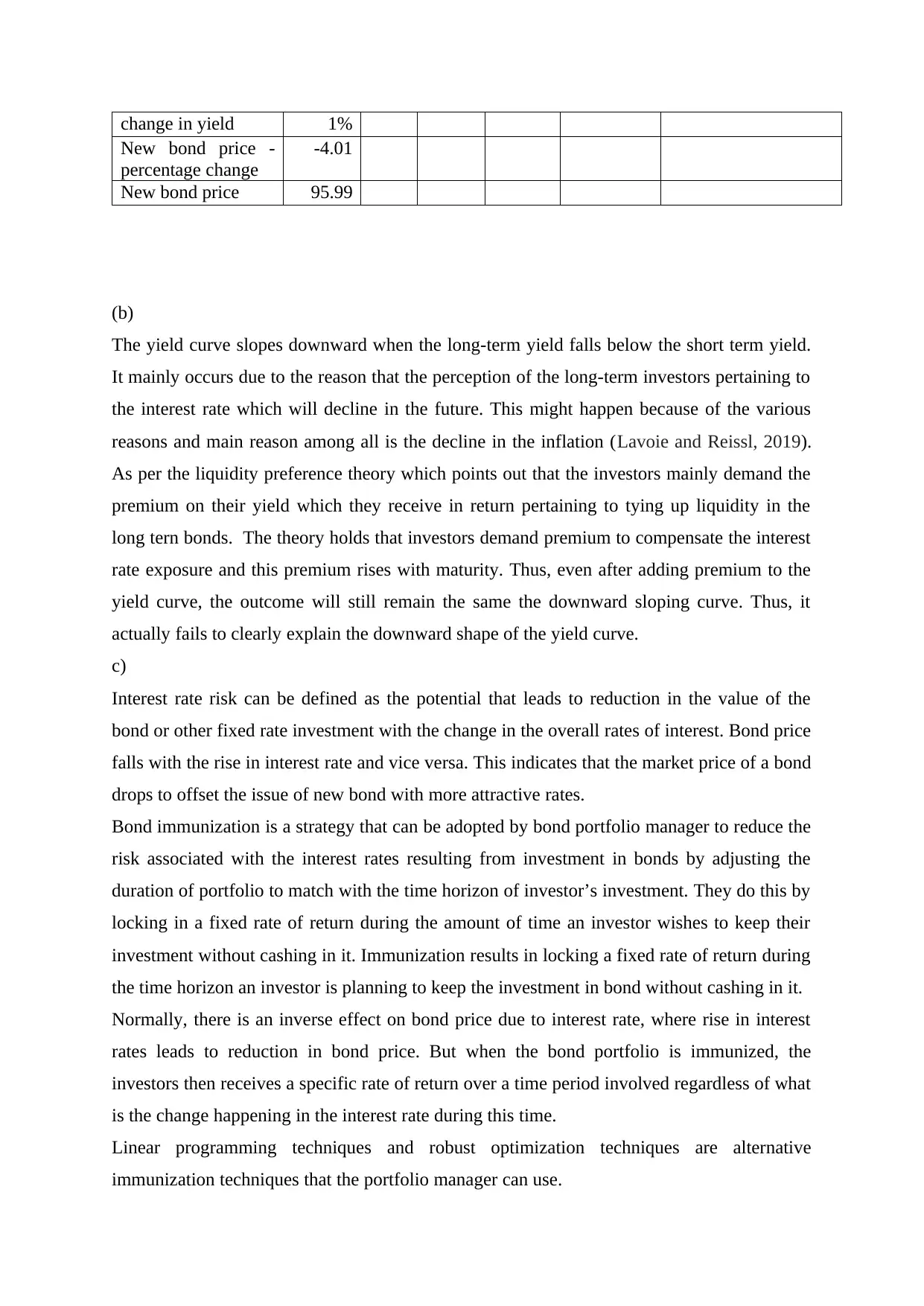

This document presents a detailed solution to an investment analysis homework assignment. Section A focuses on bond valuation, including calculations of bond price, duration, modified duration, and convexity for two different bonds. The analysis delves into the concept of yield curves, explaining downward sloping curves and their implications, as well as addressing interest rate risk and bond immunization strategies. Section B shifts to technical analysis, discussing the efficient market hypothesis and its implications for investment strategies. It examines the net present value of securities in an efficient market and explores the tenets of the efficient market, including weak, semi-strong, and strong forms, and how they relate to technical and fundamental analysis, and fund management activities. Finally, the solution outlines the roles of a portfolio manager in an efficient market, emphasizing diversification, tax considerations, and resource allocation to meet investor needs.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.