Investment Analysis & Portfolio Management: Five-Asset Classes

VerifiedAdded on 2023/03/31

|12

|2488

|276

Report

AI Summary

This report provides a comprehensive analysis of investment and portfolio management strategies, focusing on asset allocation, risk management, and the efficient frontier. It begins by discussing the risk and return characteristics of five asset classes using arithmetic mean, geometric mean, and standard deviation. The report then constructs an efficient portfolio, discussing the implications of the five-asset efficient frontier and the Capital Allocation Line (CAL). Finally, it provides a critical discussion of the results, explaining the appeal of the minimum variance portfolio among academics and practitioners, and highlighting the normative aspects of Modern Portfolio Theory (MPT). The analysis includes calculations of correlation and covariance matrices to optimize portfolio construction based on risk and return preferences.

Running head: INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Table of Contents

a. Discussing about the five-asset class by using their AM, GM and standard deviation, while

providing information about the risk and return characteristics of each stock:...............................2

b. Constructing the efficient portfolio and discussing the implications of the five asset efficient

frontier and CAL:............................................................................................................................5

c. Providing an in-depth and critical discussion of the results, while indicating why minimum

variance portfolio is still liked by academics and practitioners and MPT normative:....................8

References and Bibliography:........................................................................................................10

Table of Contents

a. Discussing about the five-asset class by using their AM, GM and standard deviation, while

providing information about the risk and return characteristics of each stock:...............................2

b. Constructing the efficient portfolio and discussing the implications of the five asset efficient

frontier and CAL:............................................................................................................................5

c. Providing an in-depth and critical discussion of the results, while indicating why minimum

variance portfolio is still liked by academics and practitioners and MPT normative:....................8

References and Bibliography:........................................................................................................10

2INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

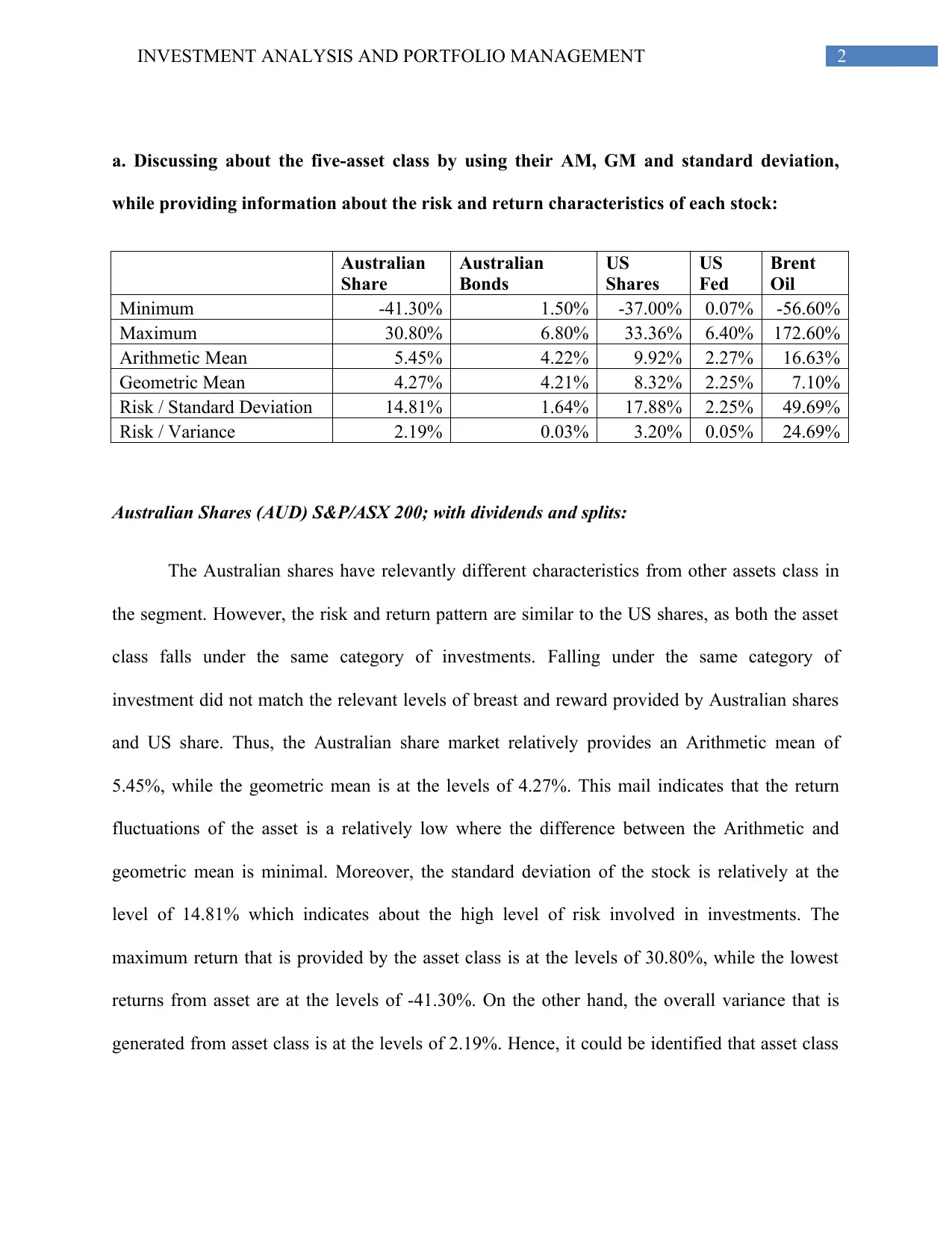

a. Discussing about the five-asset class by using their AM, GM and standard deviation,

while providing information about the risk and return characteristics of each stock:

Australian

Share

Australian

Bonds

US

Shares

US

Fed

Brent

Oil

Minimum -41.30% 1.50% -37.00% 0.07% -56.60%

Maximum 30.80% 6.80% 33.36% 6.40% 172.60%

Arithmetic Mean 5.45% 4.22% 9.92% 2.27% 16.63%

Geometric Mean 4.27% 4.21% 8.32% 2.25% 7.10%

Risk / Standard Deviation 14.81% 1.64% 17.88% 2.25% 49.69%

Risk / Variance 2.19% 0.03% 3.20% 0.05% 24.69%

Australian Shares (AUD) S&P/ASX 200; with dividends and splits:

The Australian shares have relevantly different characteristics from other assets class in

the segment. However, the risk and return pattern are similar to the US shares, as both the asset

class falls under the same category of investments. Falling under the same category of

investment did not match the relevant levels of breast and reward provided by Australian shares

and US share. Thus, the Australian share market relatively provides an Arithmetic mean of

5.45%, while the geometric mean is at the levels of 4.27%. This mail indicates that the return

fluctuations of the asset is a relatively low where the difference between the Arithmetic and

geometric mean is minimal. Moreover, the standard deviation of the stock is relatively at the

level of 14.81% which indicates about the high level of risk involved in investments. The

maximum return that is provided by the asset class is at the levels of 30.80%, while the lowest

returns from asset are at the levels of -41.30%. On the other hand, the overall variance that is

generated from asset class is at the levels of 2.19%. Hence, it could be identified that asset class

a. Discussing about the five-asset class by using their AM, GM and standard deviation,

while providing information about the risk and return characteristics of each stock:

Australian

Share

Australian

Bonds

US

Shares

US

Fed

Brent

Oil

Minimum -41.30% 1.50% -37.00% 0.07% -56.60%

Maximum 30.80% 6.80% 33.36% 6.40% 172.60%

Arithmetic Mean 5.45% 4.22% 9.92% 2.27% 16.63%

Geometric Mean 4.27% 4.21% 8.32% 2.25% 7.10%

Risk / Standard Deviation 14.81% 1.64% 17.88% 2.25% 49.69%

Risk / Variance 2.19% 0.03% 3.20% 0.05% 24.69%

Australian Shares (AUD) S&P/ASX 200; with dividends and splits:

The Australian shares have relevantly different characteristics from other assets class in

the segment. However, the risk and return pattern are similar to the US shares, as both the asset

class falls under the same category of investments. Falling under the same category of

investment did not match the relevant levels of breast and reward provided by Australian shares

and US share. Thus, the Australian share market relatively provides an Arithmetic mean of

5.45%, while the geometric mean is at the levels of 4.27%. This mail indicates that the return

fluctuations of the asset is a relatively low where the difference between the Arithmetic and

geometric mean is minimal. Moreover, the standard deviation of the stock is relatively at the

level of 14.81% which indicates about the high level of risk involved in investments. The

maximum return that is provided by the asset class is at the levels of 30.80%, while the lowest

returns from asset are at the levels of -41.30%. On the other hand, the overall variance that is

generated from asset class is at the levels of 2.19%. Hence, it could be identified that asset class

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

falls under growth stock, where both risk and return from the investment is relevantly high

(Doeswijk, Lam & Swinkels, 2014).

Australian Bonds (AUD) RBA cash rate in December:

Analysis of the Australian bond cash rate is relatively depicted in the above table where

the Arithmetic mean of the Asset classes at the levels of 4.22%, while Geometric mean is at

4.21%. The truncated difference between both Arithmetic and geometric mean directly indicates

about the low volatility present within the Asset class. The Australian bond market relatively

provides the significant return by reducing the level of risk involved in investment. The overall

standard deviation of the asset is at the levels of 1.64%, while the variance value is at 0.03%. The

low standard deviation and variance value of the asset indicates about the stability in the return

that is provided by the Australian bond market. Moreover, the minimum returns that is provided

by the Asset classes at the levels of 1.50%, while the highest return 6.80%. The low fluctuations

in the maximum and minimum returns of the Asset classes also indicate about the stability and

security that is provided by the Asset to the investors. Thus, the asset class can be classified as a

conservative investment option that can be used by the investors to minimize the risk involved in

investments (Hanlon, Maydew & Thornock, 2015).

US Shares (USD) S&P500: Total Annual Return with dividends:

The uses relatively comprise of the total returns provided by the capital market of United

States where the overall Arithmetic mean is actor levels of 9.92%, while the geometric mean is at

8.32%. There is significantly low difference between the return of geometric and Arithmetic for

US shares, which indicates about the limited volatility present within the Asset class. From the

relevant analysis, it could be identified that the standard deviation of the state is second highest

among all the Asset class which is at the levels of 17.88%, while the variance level is at 3.20%.

falls under growth stock, where both risk and return from the investment is relevantly high

(Doeswijk, Lam & Swinkels, 2014).

Australian Bonds (AUD) RBA cash rate in December:

Analysis of the Australian bond cash rate is relatively depicted in the above table where

the Arithmetic mean of the Asset classes at the levels of 4.22%, while Geometric mean is at

4.21%. The truncated difference between both Arithmetic and geometric mean directly indicates

about the low volatility present within the Asset class. The Australian bond market relatively

provides the significant return by reducing the level of risk involved in investment. The overall

standard deviation of the asset is at the levels of 1.64%, while the variance value is at 0.03%. The

low standard deviation and variance value of the asset indicates about the stability in the return

that is provided by the Australian bond market. Moreover, the minimum returns that is provided

by the Asset classes at the levels of 1.50%, while the highest return 6.80%. The low fluctuations

in the maximum and minimum returns of the Asset classes also indicate about the stability and

security that is provided by the Asset to the investors. Thus, the asset class can be classified as a

conservative investment option that can be used by the investors to minimize the risk involved in

investments (Hanlon, Maydew & Thornock, 2015).

US Shares (USD) S&P500: Total Annual Return with dividends:

The uses relatively comprise of the total returns provided by the capital market of United

States where the overall Arithmetic mean is actor levels of 9.92%, while the geometric mean is at

8.32%. There is significantly low difference between the return of geometric and Arithmetic for

US shares, which indicates about the limited volatility present within the Asset class. From the

relevant analysis, it could be identified that the standard deviation of the state is second highest

among all the Asset class which is at the levels of 17.88%, while the variance level is at 3.20%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

There is a relatively high difference between the minimum and maximum return that is generated

by the acid during the specified period. The maximum return generated by the asset is at the

levels of 33.36%, while the minimum return is -37%. This high difference between the minimum

and maximum returns directly indicates about the volatility that is present within the asset class.

Thus, US shares can be considered growth stock, which provide both risk and return to the

investors (Syriopoulos, Makram & Boubaker, 2015).

US Fed Funds Rate (USD) in December:

US Fed fund rate similar to Australian bonds, which is depicted in the above table, there

is situation in the relevant price action and return of the asset. The Arithmetic mean of the US

Fed the acid levels of 2.27%, while the geometric mean is at 2.25%. This relevantly indicates

about the low volatility present within the asset. The standard deviation is at the levels of 2.25%,

while the variance values at 0.05%. Thus, the low volatility present within the asset class mainly

indicates that the US fed asset is a conservative investment option. Being a conservative

investment option there is low difference between the minimum and maximum return of the

assets class, where the maximum return value is at 6.40%, while the minimum return value is at

the levels of 0.07%.

Brent Oil (USD):

In the similar instance, the evaluation of the above table directly provides information

about the overall risk and return attributes of Brent oil. The Arithmetic mean of the asset is

relatively at the levels of 16.63%, while the geometric mean is only at the levels of 7.10%. The

major difference between the Arithmetic mean and geometric mean indicates about the high

volatility that is present within the Asset class. The price fluctuations that are made by the Asset

classes directly delivered a low Geometric mean in comparison to the Arithmetic mean.

There is a relatively high difference between the minimum and maximum return that is generated

by the acid during the specified period. The maximum return generated by the asset is at the

levels of 33.36%, while the minimum return is -37%. This high difference between the minimum

and maximum returns directly indicates about the volatility that is present within the asset class.

Thus, US shares can be considered growth stock, which provide both risk and return to the

investors (Syriopoulos, Makram & Boubaker, 2015).

US Fed Funds Rate (USD) in December:

US Fed fund rate similar to Australian bonds, which is depicted in the above table, there

is situation in the relevant price action and return of the asset. The Arithmetic mean of the US

Fed the acid levels of 2.27%, while the geometric mean is at 2.25%. This relevantly indicates

about the low volatility present within the asset. The standard deviation is at the levels of 2.25%,

while the variance values at 0.05%. Thus, the low volatility present within the asset class mainly

indicates that the US fed asset is a conservative investment option. Being a conservative

investment option there is low difference between the minimum and maximum return of the

assets class, where the maximum return value is at 6.40%, while the minimum return value is at

the levels of 0.07%.

Brent Oil (USD):

In the similar instance, the evaluation of the above table directly provides information

about the overall risk and return attributes of Brent oil. The Arithmetic mean of the asset is

relatively at the levels of 16.63%, while the geometric mean is only at the levels of 7.10%. The

major difference between the Arithmetic mean and geometric mean indicates about the high

volatility that is present within the Asset class. The price fluctuations that are made by the Asset

classes directly delivered a low Geometric mean in comparison to the Arithmetic mean.

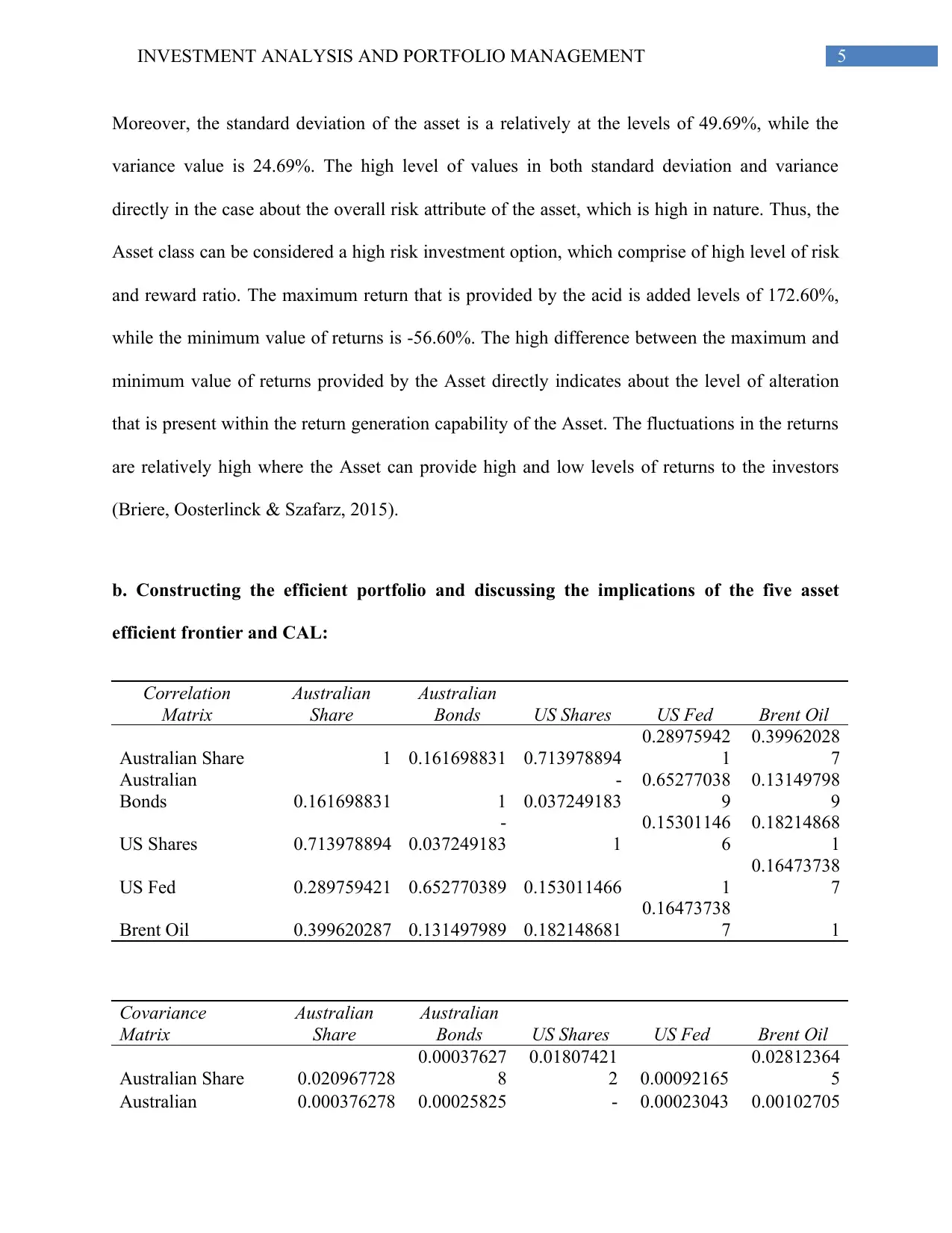

5INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Moreover, the standard deviation of the asset is a relatively at the levels of 49.69%, while the

variance value is 24.69%. The high level of values in both standard deviation and variance

directly in the case about the overall risk attribute of the asset, which is high in nature. Thus, the

Asset class can be considered a high risk investment option, which comprise of high level of risk

and reward ratio. The maximum return that is provided by the acid is added levels of 172.60%,

while the minimum value of returns is -56.60%. The high difference between the maximum and

minimum value of returns provided by the Asset directly indicates about the level of alteration

that is present within the return generation capability of the Asset. The fluctuations in the returns

are relatively high where the Asset can provide high and low levels of returns to the investors

(Briere, Oosterlinck & Szafarz, 2015).

b. Constructing the efficient portfolio and discussing the implications of the five asset

efficient frontier and CAL:

Correlation

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

Australian Share 1 0.161698831 0.713978894

0.28975942

1

0.39962028

7

Australian

Bonds 0.161698831 1

-

0.037249183

0.65277038

9

0.13149798

9

US Shares 0.713978894

-

0.037249183 1

0.15301146

6

0.18214868

1

US Fed 0.289759421 0.652770389 0.153011466 1

0.16473738

7

Brent Oil 0.399620287 0.131497989 0.182148681

0.16473738

7 1

Covariance

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

Australian Share 0.020967728

0.00037627

8

0.01807421

2 0.00092165

0.02812364

5

Australian 0.000376278 0.00025825 - 0.00023043 0.00102705

Moreover, the standard deviation of the asset is a relatively at the levels of 49.69%, while the

variance value is 24.69%. The high level of values in both standard deviation and variance

directly in the case about the overall risk attribute of the asset, which is high in nature. Thus, the

Asset class can be considered a high risk investment option, which comprise of high level of risk

and reward ratio. The maximum return that is provided by the acid is added levels of 172.60%,

while the minimum value of returns is -56.60%. The high difference between the maximum and

minimum value of returns provided by the Asset directly indicates about the level of alteration

that is present within the return generation capability of the Asset. The fluctuations in the returns

are relatively high where the Asset can provide high and low levels of returns to the investors

(Briere, Oosterlinck & Szafarz, 2015).

b. Constructing the efficient portfolio and discussing the implications of the five asset

efficient frontier and CAL:

Correlation

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

Australian Share 1 0.161698831 0.713978894

0.28975942

1

0.39962028

7

Australian

Bonds 0.161698831 1

-

0.037249183

0.65277038

9

0.13149798

9

US Shares 0.713978894

-

0.037249183 1

0.15301146

6

0.18214868

1

US Fed 0.289759421 0.652770389 0.153011466 1

0.16473738

7

Brent Oil 0.399620287 0.131497989 0.182148681

0.16473738

7 1

Covariance

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

Australian Share 0.020967728

0.00037627

8

0.01807421

2 0.00092165

0.02812364

5

Australian 0.000376278 0.00025825 - 0.00023043 0.00102705

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Bonds 7 0.00010465 5

US Shares 0.018074212

-

0.00010465

0.03056304

5

0.00058759

1

0.01547649

9

US Fed 0.00092165 0.00023043

0.00058759

1

0.00048250

9

0.00175870

5

Brent Oil 0.028123645

0.00102705

5

0.01547649

9

0.00175870

5

0.23620918

3

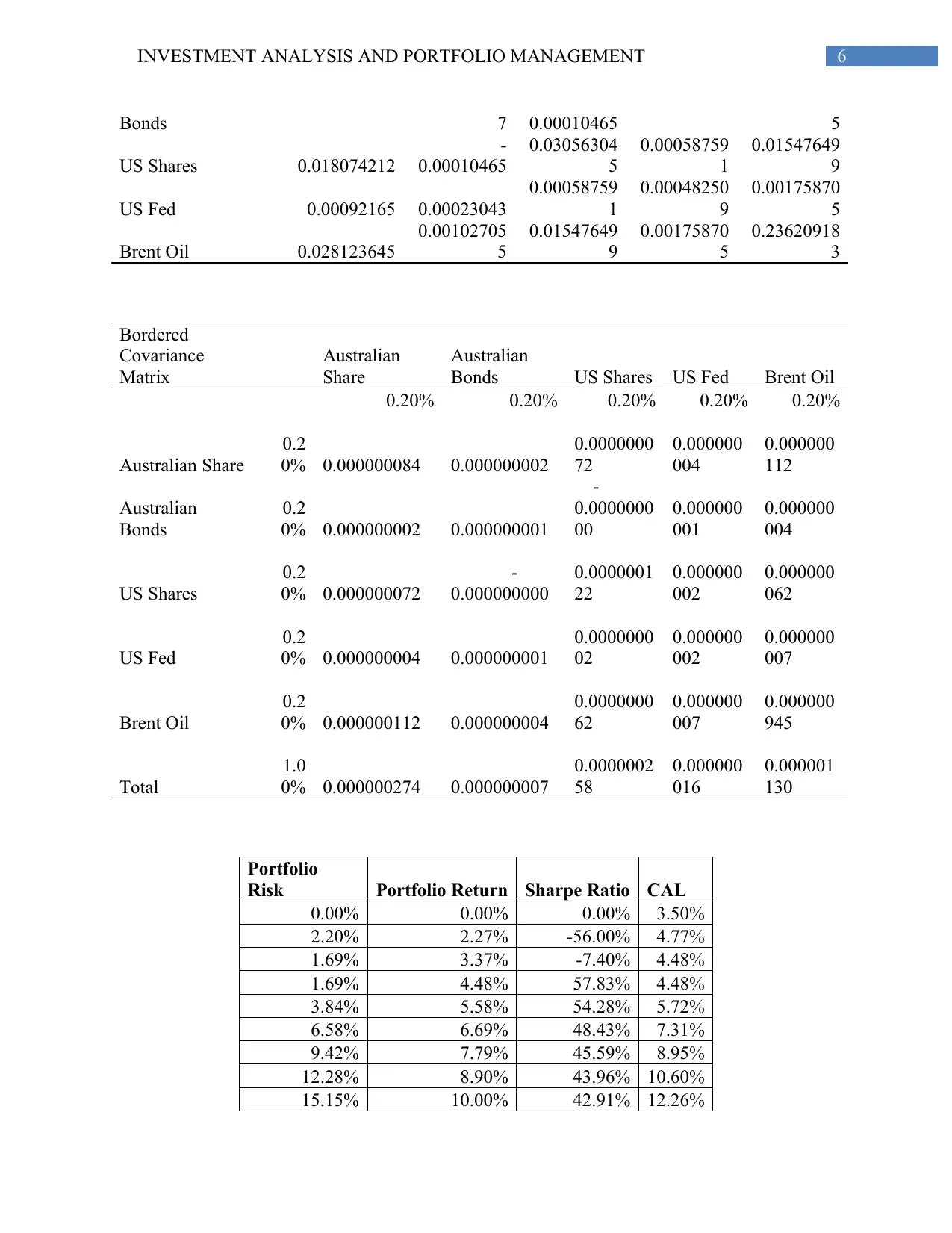

Bordered

Covariance

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

0.20% 0.20% 0.20% 0.20% 0.20%

Australian Share

0.2

0% 0.000000084 0.000000002

0.0000000

72

0.000000

004

0.000000

112

Australian

Bonds

0.2

0% 0.000000002 0.000000001

-

0.0000000

00

0.000000

001

0.000000

004

US Shares

0.2

0% 0.000000072

-

0.000000000

0.0000001

22

0.000000

002

0.000000

062

US Fed

0.2

0% 0.000000004 0.000000001

0.0000000

02

0.000000

002

0.000000

007

Brent Oil

0.2

0% 0.000000112 0.000000004

0.0000000

62

0.000000

007

0.000000

945

Total

1.0

0% 0.000000274 0.000000007

0.0000002

58

0.000000

016

0.000001

130

Portfolio

Risk Portfolio Return Sharpe Ratio CAL

0.00% 0.00% 0.00% 3.50%

2.20% 2.27% -56.00% 4.77%

1.69% 3.37% -7.40% 4.48%

1.69% 4.48% 57.83% 4.48%

3.84% 5.58% 54.28% 5.72%

6.58% 6.69% 48.43% 7.31%

9.42% 7.79% 45.59% 8.95%

12.28% 8.90% 43.96% 10.60%

15.15% 10.00% 42.91% 12.26%

Bonds 7 0.00010465 5

US Shares 0.018074212

-

0.00010465

0.03056304

5

0.00058759

1

0.01547649

9

US Fed 0.00092165 0.00023043

0.00058759

1

0.00048250

9

0.00175870

5

Brent Oil 0.028123645

0.00102705

5

0.01547649

9

0.00175870

5

0.23620918

3

Bordered

Covariance

Matrix

Australian

Share

Australian

Bonds US Shares US Fed Brent Oil

0.20% 0.20% 0.20% 0.20% 0.20%

Australian Share

0.2

0% 0.000000084 0.000000002

0.0000000

72

0.000000

004

0.000000

112

Australian

Bonds

0.2

0% 0.000000002 0.000000001

-

0.0000000

00

0.000000

001

0.000000

004

US Shares

0.2

0% 0.000000072

-

0.000000000

0.0000001

22

0.000000

002

0.000000

062

US Fed

0.2

0% 0.000000004 0.000000001

0.0000000

02

0.000000

002

0.000000

007

Brent Oil

0.2

0% 0.000000112 0.000000004

0.0000000

62

0.000000

007

0.000000

945

Total

1.0

0% 0.000000274 0.000000007

0.0000002

58

0.000000

016

0.000001

130

Portfolio

Risk Portfolio Return Sharpe Ratio CAL

0.00% 0.00% 0.00% 3.50%

2.20% 2.27% -56.00% 4.77%

1.69% 3.37% -7.40% 4.48%

1.69% 4.48% 57.83% 4.48%

3.84% 5.58% 54.28% 5.72%

6.58% 6.69% 48.43% 7.31%

9.42% 7.79% 45.59% 8.95%

12.28% 8.90% 43.96% 10.60%

15.15% 10.00% 42.91% 12.26%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

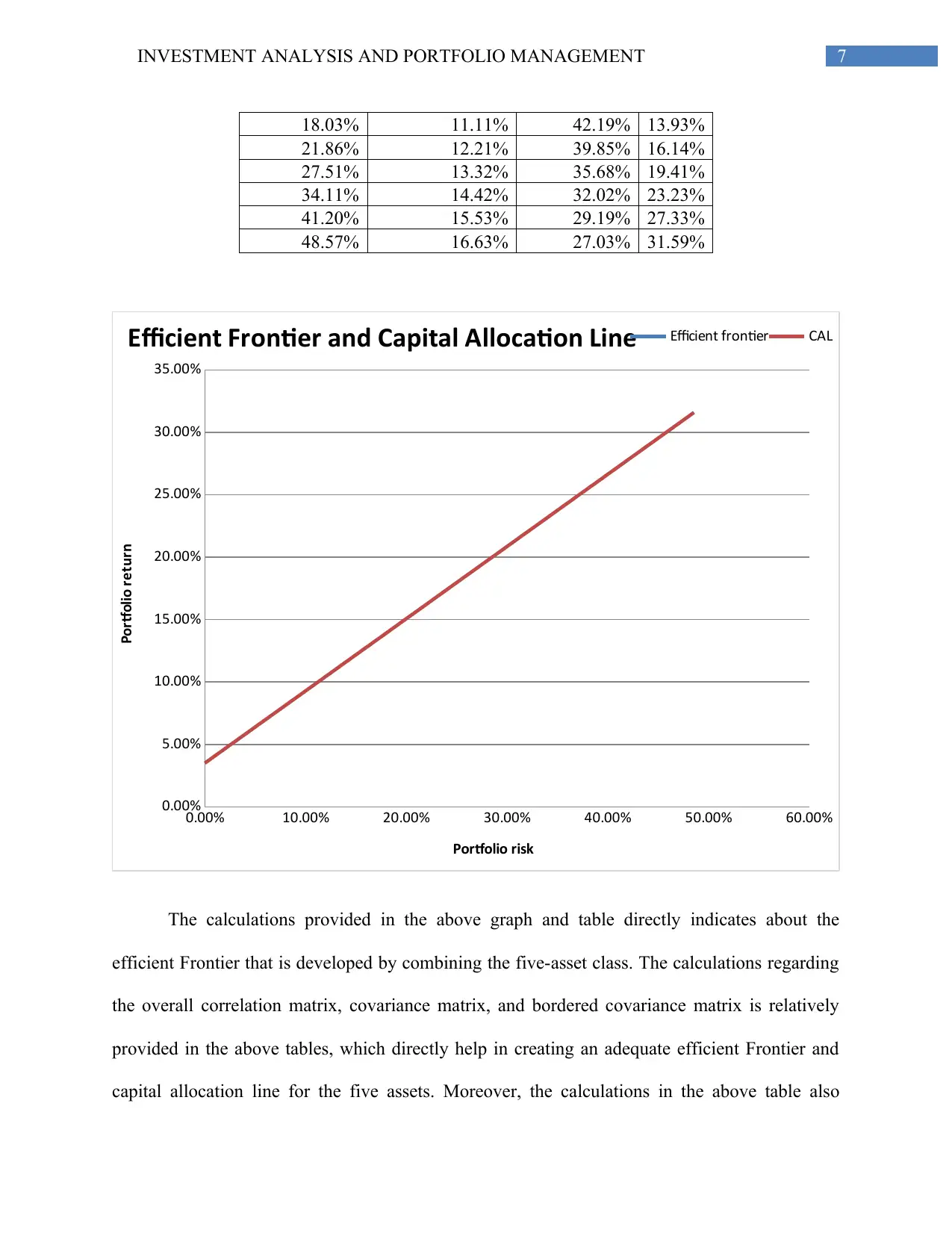

18.03% 11.11% 42.19% 13.93%

21.86% 12.21% 39.85% 16.14%

27.51% 13.32% 35.68% 19.41%

34.11% 14.42% 32.02% 23.23%

41.20% 15.53% 29.19% 27.33%

48.57% 16.63% 27.03% 31.59%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Efficient Frontier and Capital Allocation Line Efficient frontier CAL

Portfolio risk

Portfolio return

The calculations provided in the above graph and table directly indicates about the

efficient Frontier that is developed by combining the five-asset class. The calculations regarding

the overall correlation matrix, covariance matrix, and bordered covariance matrix is relatively

provided in the above tables, which directly help in creating an adequate efficient Frontier and

capital allocation line for the five assets. Moreover, the calculations in the above table also

18.03% 11.11% 42.19% 13.93%

21.86% 12.21% 39.85% 16.14%

27.51% 13.32% 35.68% 19.41%

34.11% 14.42% 32.02% 23.23%

41.20% 15.53% 29.19% 27.33%

48.57% 16.63% 27.03% 31.59%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Efficient Frontier and Capital Allocation Line Efficient frontier CAL

Portfolio risk

Portfolio return

The calculations provided in the above graph and table directly indicates about the

efficient Frontier that is developed by combining the five-asset class. The calculations regarding

the overall correlation matrix, covariance matrix, and bordered covariance matrix is relatively

provided in the above tables, which directly help in creating an adequate efficient Frontier and

capital allocation line for the five assets. Moreover, the calculations in the above table also

8INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

provide information about the portfolio risk, portfolio Returns, Sharpe ratio, and CAL, which has

been used for creating the graph of the efficient Frontier. From the relevant valuation it can be

identified that the overall efficient market hypothesis has been calculated on the basis of the

above data. Therefore, the relevant risk that is involved in investment relatively increases with

the increment in returns. Therefore, it could be understood that the investors demanding higher

returns will have to engage in high risk portfolio. Santacruz (2016) indicted that Efficient

Frontier provides information about the relevant weights and investments options that need to be

conducted by investors in certain assets to maximize the level of returns, while reducing the risk

attributes.

The above efficient Frontier directly indicates about the overall risk and return attributes

of the asset classes utilized in the investments. Therefore a minimum variance portfolio can also

be determined with the efficient Frontier where the investments will hold a total risk of 1.69%,

while the returns will be at the levels of 4.48%. Thus, the efficient frontier provides adequate

information about the overall risk and return attributes of the portfolio consisting of the 5-assets.

Hence, investments can be conducted in accordance with the risk and return attributes of the

investors.

c. Providing an in-depth and critical discussion of the results, while indicating why

minimum variance portfolio is still liked by academics and practitioners and MPT

normative:

Minimum variance

portfolio Value

Portfolio Risk 1.69%

Portfolio Return 4.48%

provide information about the portfolio risk, portfolio Returns, Sharpe ratio, and CAL, which has

been used for creating the graph of the efficient Frontier. From the relevant valuation it can be

identified that the overall efficient market hypothesis has been calculated on the basis of the

above data. Therefore, the relevant risk that is involved in investment relatively increases with

the increment in returns. Therefore, it could be understood that the investors demanding higher

returns will have to engage in high risk portfolio. Santacruz (2016) indicted that Efficient

Frontier provides information about the relevant weights and investments options that need to be

conducted by investors in certain assets to maximize the level of returns, while reducing the risk

attributes.

The above efficient Frontier directly indicates about the overall risk and return attributes

of the asset classes utilized in the investments. Therefore a minimum variance portfolio can also

be determined with the efficient Frontier where the investments will hold a total risk of 1.69%,

while the returns will be at the levels of 4.48%. Thus, the efficient frontier provides adequate

information about the overall risk and return attributes of the portfolio consisting of the 5-assets.

Hence, investments can be conducted in accordance with the risk and return attributes of the

investors.

c. Providing an in-depth and critical discussion of the results, while indicating why

minimum variance portfolio is still liked by academics and practitioners and MPT

normative:

Minimum variance

portfolio Value

Portfolio Risk 1.69%

Portfolio Return 4.48%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Modern portfolio theory and mean variance theory directly indicates about the overall

investment options that is considered by the investors while conducting relevant investment

decisions. The mean variance portfolio directly indicates about the low level of risk involved in

investments that is adopted by the investors, as it helps in minimizing the capital investment risk.

The mean variance portfolio theory directly indicates that investors should only invest in

portfolios that have the lowest risk from investment. Moreover, academic and practitioners

relatively like the minimum variance portfolio measure, as it allows the investor to minimize the

level of investment risk from the combination of the assets. The above table indicates about the

minimum variance portfolio, which states that the overall investments in the asset class will have

risk at the levels of 1.69%, while the returns would be 4.48%. This relatively indicates that the

overall investments in the minimum variance portfolio will provide any higher level of

investment security to the investors.

The efficient portfolio directly provides adequate information about the minimum

variance portfolio and the waves which require the investors to do the level of risk involved in

investment. Bodie, Kane and Marcus (2018) criticizes that the portfolio risk relatively increases

during an economic crisis where adequate returns and volatility overall asset class increases

exponentially. However, Page and Panariello (2018) stated that accommodation of risk free

assets in the portfolio directly allowed investors to effectively diversify their investments and

minimize the level of risk that is affecting their investment capital. Thus, Modern portfolio

theory is considered normative, as it helps in deriving an adequate investment option, which can

reduce the level of risk and increase returns from investments.

Modern portfolio theory and mean variance theory directly indicates about the overall

investment options that is considered by the investors while conducting relevant investment

decisions. The mean variance portfolio directly indicates about the low level of risk involved in

investments that is adopted by the investors, as it helps in minimizing the capital investment risk.

The mean variance portfolio theory directly indicates that investors should only invest in

portfolios that have the lowest risk from investment. Moreover, academic and practitioners

relatively like the minimum variance portfolio measure, as it allows the investor to minimize the

level of investment risk from the combination of the assets. The above table indicates about the

minimum variance portfolio, which states that the overall investments in the asset class will have

risk at the levels of 1.69%, while the returns would be 4.48%. This relatively indicates that the

overall investments in the minimum variance portfolio will provide any higher level of

investment security to the investors.

The efficient portfolio directly provides adequate information about the minimum

variance portfolio and the waves which require the investors to do the level of risk involved in

investment. Bodie, Kane and Marcus (2018) criticizes that the portfolio risk relatively increases

during an economic crisis where adequate returns and volatility overall asset class increases

exponentially. However, Page and Panariello (2018) stated that accommodation of risk free

assets in the portfolio directly allowed investors to effectively diversify their investments and

minimize the level of risk that is affecting their investment capital. Thus, Modern portfolio

theory is considered normative, as it helps in deriving an adequate investment option, which can

reduce the level of risk and increase returns from investments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

References and Bibliography:

Bodie, Z, Kane A & Marcus, AJ 2018, Investments, 11th edn, McGraw-Hill Education

Brandstetter, L., & Lehner, O. M. 2015. Opening the market for impact investments: The need

for adapted portfolio tools. Entrepreneurship Research Journal, 5(2), 87-107.

Briere, M., Oosterlinck, K., & Szafarz, A. 2015. Virtual currency, tangible return: Portfolio

diversification with bitcoin. Journal of Asset Management, 16(6), 365-373.

Chandra, P. 2017. Investment analysis and portfolio management. McGraw-Hill Education.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

2015. Quantitative investment analysis. John Wiley & Sons.

Doeswijk, R., Lam, T., & Swinkels, L. 2014. The global multi-asset market portfolio, 1959–

2012. Financial Analysts Journal, 70(2), 26-41.

Guidi, F., & Ugur, M. 2014. An analysis of South-Eastern European stock markets: Evidence on

cointegration and portfolio diversification benefits. Journal of International Financial Markets,

Institutions and Money, 30, 119-136.

Hammoudeh, S., Nguyen, D. K., Reboredo, J. C., & Wen, X. 2014. Dependence of stock and

commodity futures markets in China: Implications for portfolio investment. Emerging Markets

Review, 21, 183-200.

References and Bibliography:

Bodie, Z, Kane A & Marcus, AJ 2018, Investments, 11th edn, McGraw-Hill Education

Brandstetter, L., & Lehner, O. M. 2015. Opening the market for impact investments: The need

for adapted portfolio tools. Entrepreneurship Research Journal, 5(2), 87-107.

Briere, M., Oosterlinck, K., & Szafarz, A. 2015. Virtual currency, tangible return: Portfolio

diversification with bitcoin. Journal of Asset Management, 16(6), 365-373.

Chandra, P. 2017. Investment analysis and portfolio management. McGraw-Hill Education.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

2015. Quantitative investment analysis. John Wiley & Sons.

Doeswijk, R., Lam, T., & Swinkels, L. 2014. The global multi-asset market portfolio, 1959–

2012. Financial Analysts Journal, 70(2), 26-41.

Guidi, F., & Ugur, M. 2014. An analysis of South-Eastern European stock markets: Evidence on

cointegration and portfolio diversification benefits. Journal of International Financial Markets,

Institutions and Money, 30, 119-136.

Hammoudeh, S., Nguyen, D. K., Reboredo, J. C., & Wen, X. 2014. Dependence of stock and

commodity futures markets in China: Implications for portfolio investment. Emerging Markets

Review, 21, 183-200.

11INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Hanlon, M., Maydew, E. L., & Thornock, J. R. 2015. Taking the long way home: US tax evasion

and offshore investments in US equity and debt markets. The Journal of Finance, 70(1), 257-

287.

Hoesli, M., & MacGregor, B. D. 2014. Property investment: principles and practice of portfolio

management. Routledge.

Jordan, B. D., Miller, T. W., & Dolvin, S. D. 2015. Fundamentals of investments: valuation and

management. McGraw-Hill Education.

McKay, S, Shaoiro, R & Thomas, R. 2018, ‘What free lunch? The costs of

overdiversification’, Financial Analysts Journal, vol. 74, no. 1, pp. 44-57.

Page, S & Panariello, RA 2018, ‘When diversification fails’, Financial Analysts Journal, vol. 74,

no. 3, pp. 19-32.

Santacruz, L 2016, ‘Asset allocation theory and practice in Australian investment

management’, The Journal of Wealth Management, vol. 19, no. 2, pp. 47-67.

Syriopoulos, T., Makram, B., & Boubaker, A. 2015. Stock market volatility spillovers and

portfolio hedging: BRICS and the financial crisis. International Review of Financial

Analysis, 39, 7-18.

Hanlon, M., Maydew, E. L., & Thornock, J. R. 2015. Taking the long way home: US tax evasion

and offshore investments in US equity and debt markets. The Journal of Finance, 70(1), 257-

287.

Hoesli, M., & MacGregor, B. D. 2014. Property investment: principles and practice of portfolio

management. Routledge.

Jordan, B. D., Miller, T. W., & Dolvin, S. D. 2015. Fundamentals of investments: valuation and

management. McGraw-Hill Education.

McKay, S, Shaoiro, R & Thomas, R. 2018, ‘What free lunch? The costs of

overdiversification’, Financial Analysts Journal, vol. 74, no. 1, pp. 44-57.

Page, S & Panariello, RA 2018, ‘When diversification fails’, Financial Analysts Journal, vol. 74,

no. 3, pp. 19-32.

Santacruz, L 2016, ‘Asset allocation theory and practice in Australian investment

management’, The Journal of Wealth Management, vol. 19, no. 2, pp. 47-67.

Syriopoulos, T., Makram, B., & Boubaker, A. 2015. Stock market volatility spillovers and

portfolio hedging: BRICS and the financial crisis. International Review of Financial

Analysis, 39, 7-18.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.