Investment Analysis and Portfolio Management Project - Finance Course

VerifiedAdded on 2022/08/24

|12

|3034

|17

Project

AI Summary

This project analyzes investment strategies and portfolio management techniques using historical stock data. The analysis includes calculating annualized returns, standard deviations, and correlations for two selected companies over a five-year period. The project constructs an investment opportunity set and an efficient frontier to identify optimal portfolios based on risk and return. It also explores the concept of a minimum variance portfolio and the application of diversification to mitigate investment risk. The analysis involves calculating Sharpe ratios to evaluate portfolio performance and demonstrates how diversification can stabilize returns and reduce overall risk. The project highlights the importance of understanding risk-return trade-offs and the benefits of portfolio diversification in achieving long-term financial goals. The project uses investment proportions for the two stocks ranging from 0% to 100% using intervals of 5% and plots the investment opportunity set.

Running head: INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Author’s Note:

Investment Analysis and Portfolio Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Historical Data.............................................................................................................................2

Investment Opportunity Set.........................................................................................................3

Efficient Frontier.........................................................................................................................5

Minimum Variance Portfolio.......................................................................................................7

Diversification in Portfolio..........................................................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Historical Data.............................................................................................................................2

Investment Opportunity Set.........................................................................................................3

Efficient Frontier.........................................................................................................................5

Minimum Variance Portfolio.......................................................................................................7

Diversification in Portfolio..........................................................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

2INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

Introduction

The financial analysis of the stock prices of the company has been well done for the

purpose of well analyzing the stock returns that have been generated by the company. The

companies have been well analyzed for a sum of five years in which the changes have been well

kept into consideration with respect to the price trend observed. The analysis of the stocks has

been done from a portfolio perspective in which we have analyzed the appropriate weights that

should be ideal for the stocks for the purpose of investment. Risk and Return are the key

important characteristics of an investment and the same has been well analyzed based on the

given set of criteria for the portfolio designed. The application of diversification has been well

discussed from the application of portfolio management and how the same can well result in the

reduction of the overall risk that is associated with a portfolio (Benedetti et al., 2019).

Discussion and Analysis

Historical Data

The stock price of different companies have been well selected for a sum of five years

whereby monthly changes have been well recorded down. The monthly closing prices has been

well considered for a sum of five years in which both the company average monthly return as

well as annual return has been calculated. In order to view and analyze the risk associated with

the same the Standard deviation for both the stocks were analyzed on a monthly and annual

basis. The data for both the stock prices have been well considered from a period of January

2015 to December 2019 (Tu et al., 2019). The annualized mean return for UOB was calculated to

be around 3.58% and for Wilmar International it was calculated to be around 5.90%. From a

Introduction

The financial analysis of the stock prices of the company has been well done for the

purpose of well analyzing the stock returns that have been generated by the company. The

companies have been well analyzed for a sum of five years in which the changes have been well

kept into consideration with respect to the price trend observed. The analysis of the stocks has

been done from a portfolio perspective in which we have analyzed the appropriate weights that

should be ideal for the stocks for the purpose of investment. Risk and Return are the key

important characteristics of an investment and the same has been well analyzed based on the

given set of criteria for the portfolio designed. The application of diversification has been well

discussed from the application of portfolio management and how the same can well result in the

reduction of the overall risk that is associated with a portfolio (Benedetti et al., 2019).

Discussion and Analysis

Historical Data

The stock price of different companies have been well selected for a sum of five years

whereby monthly changes have been well recorded down. The monthly closing prices has been

well considered for a sum of five years in which both the company average monthly return as

well as annual return has been calculated. In order to view and analyze the risk associated with

the same the Standard deviation for both the stocks were analyzed on a monthly and annual

basis. The data for both the stock prices have been well considered from a period of January

2015 to December 2019 (Tu et al., 2019). The annualized mean return for UOB was calculated to

be around 3.58% and for Wilmar International it was calculated to be around 5.90%. From a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

return basis it can be well seen that Wilmar International has provided a comparative better set of

returns. From a risk perspective showing the movement or the volatility in the data set captured

by the Standard Deviation for the stock has been around 18.39% for UOB and was around

21.15% for Wilmar International. The return to risk ratio for UOB has been around 0.23 and for

Wilmar International the same has been around 0.33 times. The ratio well depicts the amount of

return that the stocks is generating for a single unit of risk that is taken by the investors (Padma

and Rambabu 2017). The ratio has been rewarding for the investors in the case of Wilmar

International. Correlation on the other hand, well helps the analyst and portfolio manager well

asses the relationship that is associated between two data sets that would be further used or

utilized for portfolio perspective. The correlation between the stocks has been around 0.53 times,

this go to well shows that the stocks returns are not closely related with each other. However, it

is important to note that at the same time that a correlation of 1 or close to 1 well implies that the

relationship between the two data set observed is strong and in turn could affect the portfolio

creation and analysis process (Davis 2018). Stocks which have high correlation or correlation

close to 1 goes to well show that portfolio creation would not be benefitting the investors at all.

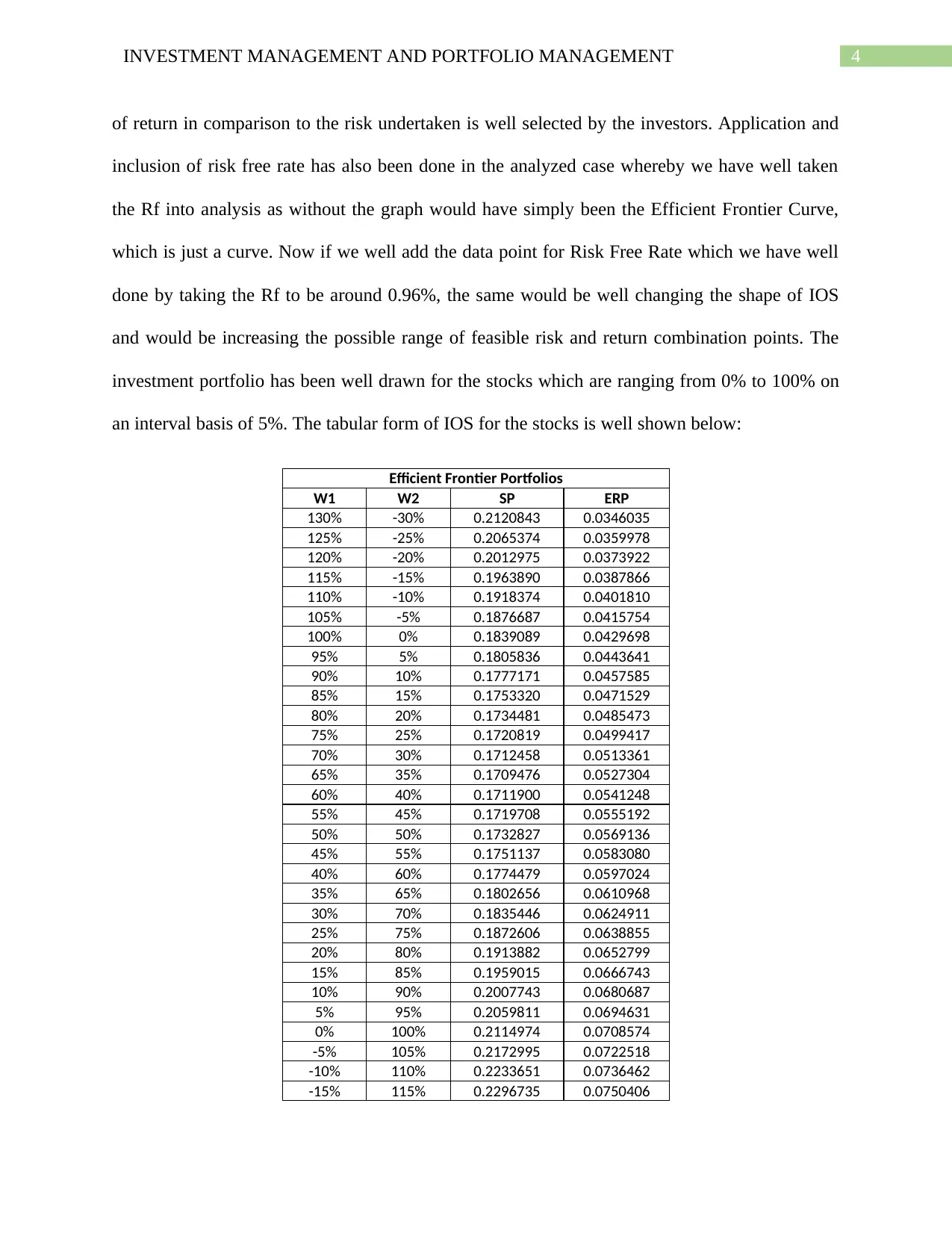

Investment Opportunity Set

The Investment Opportunity Set goes to well show the number of choices or alternatives

that are well available with an investors for the purpose of investing. All of the investments that

an investors can well make with the change in the weights of stocks in the portfolio is well

marked by IOS (Shimizu and Shiohama 2019). The opportunity set goes to well show the set of

all portfolio that one can well construct with the help of given asset class (Branch, Goldberg and

Hand 2020). Investors can well create portfolio based on high or low risk with the help of

presented opportunity set. The set of weights which gives the investors with the highest amount

return basis it can be well seen that Wilmar International has provided a comparative better set of

returns. From a risk perspective showing the movement or the volatility in the data set captured

by the Standard Deviation for the stock has been around 18.39% for UOB and was around

21.15% for Wilmar International. The return to risk ratio for UOB has been around 0.23 and for

Wilmar International the same has been around 0.33 times. The ratio well depicts the amount of

return that the stocks is generating for a single unit of risk that is taken by the investors (Padma

and Rambabu 2017). The ratio has been rewarding for the investors in the case of Wilmar

International. Correlation on the other hand, well helps the analyst and portfolio manager well

asses the relationship that is associated between two data sets that would be further used or

utilized for portfolio perspective. The correlation between the stocks has been around 0.53 times,

this go to well shows that the stocks returns are not closely related with each other. However, it

is important to note that at the same time that a correlation of 1 or close to 1 well implies that the

relationship between the two data set observed is strong and in turn could affect the portfolio

creation and analysis process (Davis 2018). Stocks which have high correlation or correlation

close to 1 goes to well show that portfolio creation would not be benefitting the investors at all.

Investment Opportunity Set

The Investment Opportunity Set goes to well show the number of choices or alternatives

that are well available with an investors for the purpose of investing. All of the investments that

an investors can well make with the change in the weights of stocks in the portfolio is well

marked by IOS (Shimizu and Shiohama 2019). The opportunity set goes to well show the set of

all portfolio that one can well construct with the help of given asset class (Branch, Goldberg and

Hand 2020). Investors can well create portfolio based on high or low risk with the help of

presented opportunity set. The set of weights which gives the investors with the highest amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

of return in comparison to the risk undertaken is well selected by the investors. Application and

inclusion of risk free rate has also been done in the analyzed case whereby we have well taken

the Rf into analysis as without the graph would have simply been the Efficient Frontier Curve,

which is just a curve. Now if we well add the data point for Risk Free Rate which we have well

done by taking the Rf to be around 0.96%, the same would be well changing the shape of IOS

and would be increasing the possible range of feasible risk and return combination points. The

investment portfolio has been well drawn for the stocks which are ranging from 0% to 100% on

an interval basis of 5%. The tabular form of IOS for the stocks is well shown below:

Efficient Frontier Portfolios

W1 W2 SP ERP

130% -30% 0.2120843 0.0346035

125% -25% 0.2065374 0.0359978

120% -20% 0.2012975 0.0373922

115% -15% 0.1963890 0.0387866

110% -10% 0.1918374 0.0401810

105% -5% 0.1876687 0.0415754

100% 0% 0.1839089 0.0429698

95% 5% 0.1805836 0.0443641

90% 10% 0.1777171 0.0457585

85% 15% 0.1753320 0.0471529

80% 20% 0.1734481 0.0485473

75% 25% 0.1720819 0.0499417

70% 30% 0.1712458 0.0513361

65% 35% 0.1709476 0.0527304

60% 40% 0.1711900 0.0541248

55% 45% 0.1719708 0.0555192

50% 50% 0.1732827 0.0569136

45% 55% 0.1751137 0.0583080

40% 60% 0.1774479 0.0597024

35% 65% 0.1802656 0.0610968

30% 70% 0.1835446 0.0624911

25% 75% 0.1872606 0.0638855

20% 80% 0.1913882 0.0652799

15% 85% 0.1959015 0.0666743

10% 90% 0.2007743 0.0680687

5% 95% 0.2059811 0.0694631

0% 100% 0.2114974 0.0708574

-5% 105% 0.2172995 0.0722518

-10% 110% 0.2233651 0.0736462

-15% 115% 0.2296735 0.0750406

of return in comparison to the risk undertaken is well selected by the investors. Application and

inclusion of risk free rate has also been done in the analyzed case whereby we have well taken

the Rf into analysis as without the graph would have simply been the Efficient Frontier Curve,

which is just a curve. Now if we well add the data point for Risk Free Rate which we have well

done by taking the Rf to be around 0.96%, the same would be well changing the shape of IOS

and would be increasing the possible range of feasible risk and return combination points. The

investment portfolio has been well drawn for the stocks which are ranging from 0% to 100% on

an interval basis of 5%. The tabular form of IOS for the stocks is well shown below:

Efficient Frontier Portfolios

W1 W2 SP ERP

130% -30% 0.2120843 0.0346035

125% -25% 0.2065374 0.0359978

120% -20% 0.2012975 0.0373922

115% -15% 0.1963890 0.0387866

110% -10% 0.1918374 0.0401810

105% -5% 0.1876687 0.0415754

100% 0% 0.1839089 0.0429698

95% 5% 0.1805836 0.0443641

90% 10% 0.1777171 0.0457585

85% 15% 0.1753320 0.0471529

80% 20% 0.1734481 0.0485473

75% 25% 0.1720819 0.0499417

70% 30% 0.1712458 0.0513361

65% 35% 0.1709476 0.0527304

60% 40% 0.1711900 0.0541248

55% 45% 0.1719708 0.0555192

50% 50% 0.1732827 0.0569136

45% 55% 0.1751137 0.0583080

40% 60% 0.1774479 0.0597024

35% 65% 0.1802656 0.0610968

30% 70% 0.1835446 0.0624911

25% 75% 0.1872606 0.0638855

20% 80% 0.1913882 0.0652799

15% 85% 0.1959015 0.0666743

10% 90% 0.2007743 0.0680687

5% 95% 0.2059811 0.0694631

0% 100% 0.2114974 0.0708574

-5% 105% 0.2172995 0.0722518

-10% 110% 0.2233651 0.0736462

-15% 115% 0.2296735 0.0750406

5INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

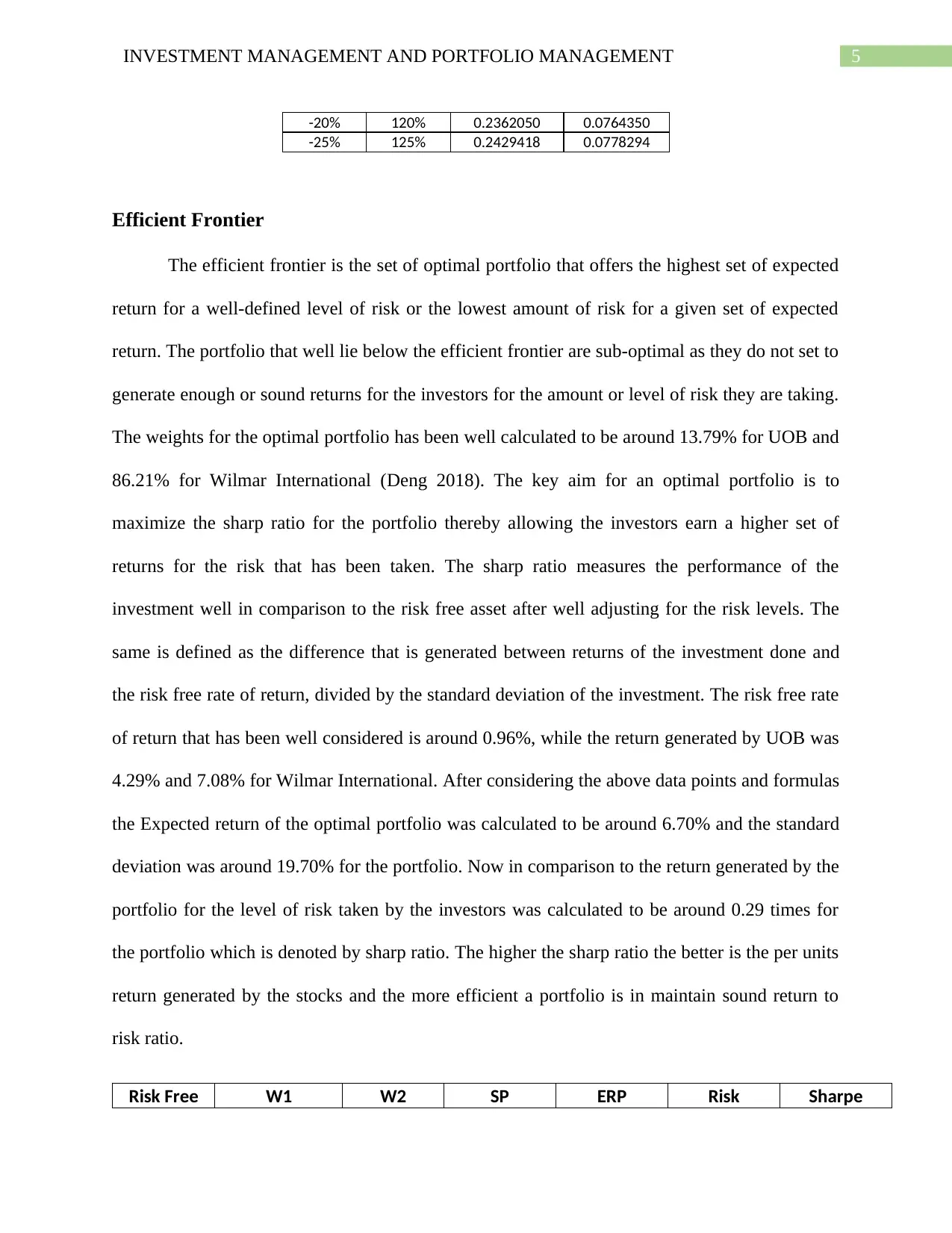

-20% 120% 0.2362050 0.0764350

-25% 125% 0.2429418 0.0778294

Efficient Frontier

The efficient frontier is the set of optimal portfolio that offers the highest set of expected

return for a well-defined level of risk or the lowest amount of risk for a given set of expected

return. The portfolio that well lie below the efficient frontier are sub-optimal as they do not set to

generate enough or sound returns for the investors for the amount or level of risk they are taking.

The weights for the optimal portfolio has been well calculated to be around 13.79% for UOB and

86.21% for Wilmar International (Deng 2018). The key aim for an optimal portfolio is to

maximize the sharp ratio for the portfolio thereby allowing the investors earn a higher set of

returns for the risk that has been taken. The sharp ratio measures the performance of the

investment well in comparison to the risk free asset after well adjusting for the risk levels. The

same is defined as the difference that is generated between returns of the investment done and

the risk free rate of return, divided by the standard deviation of the investment. The risk free rate

of return that has been well considered is around 0.96%, while the return generated by UOB was

4.29% and 7.08% for Wilmar International. After considering the above data points and formulas

the Expected return of the optimal portfolio was calculated to be around 6.70% and the standard

deviation was around 19.70% for the portfolio. Now in comparison to the return generated by the

portfolio for the level of risk taken by the investors was calculated to be around 0.29 times for

the portfolio which is denoted by sharp ratio. The higher the sharp ratio the better is the per units

return generated by the stocks and the more efficient a portfolio is in maintain sound return to

risk ratio.

Risk Free W1 W2 SP ERP Risk Sharpe

-20% 120% 0.2362050 0.0764350

-25% 125% 0.2429418 0.0778294

Efficient Frontier

The efficient frontier is the set of optimal portfolio that offers the highest set of expected

return for a well-defined level of risk or the lowest amount of risk for a given set of expected

return. The portfolio that well lie below the efficient frontier are sub-optimal as they do not set to

generate enough or sound returns for the investors for the amount or level of risk they are taking.

The weights for the optimal portfolio has been well calculated to be around 13.79% for UOB and

86.21% for Wilmar International (Deng 2018). The key aim for an optimal portfolio is to

maximize the sharp ratio for the portfolio thereby allowing the investors earn a higher set of

returns for the risk that has been taken. The sharp ratio measures the performance of the

investment well in comparison to the risk free asset after well adjusting for the risk levels. The

same is defined as the difference that is generated between returns of the investment done and

the risk free rate of return, divided by the standard deviation of the investment. The risk free rate

of return that has been well considered is around 0.96%, while the return generated by UOB was

4.29% and 7.08% for Wilmar International. After considering the above data points and formulas

the Expected return of the optimal portfolio was calculated to be around 6.70% and the standard

deviation was around 19.70% for the portfolio. Now in comparison to the return generated by the

portfolio for the level of risk taken by the investors was calculated to be around 0.29 times for

the portfolio which is denoted by sharp ratio. The higher the sharp ratio the better is the per units

return generated by the stocks and the more efficient a portfolio is in maintain sound return to

risk ratio.

Risk Free W1 W2 SP ERP Risk Sharpe

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

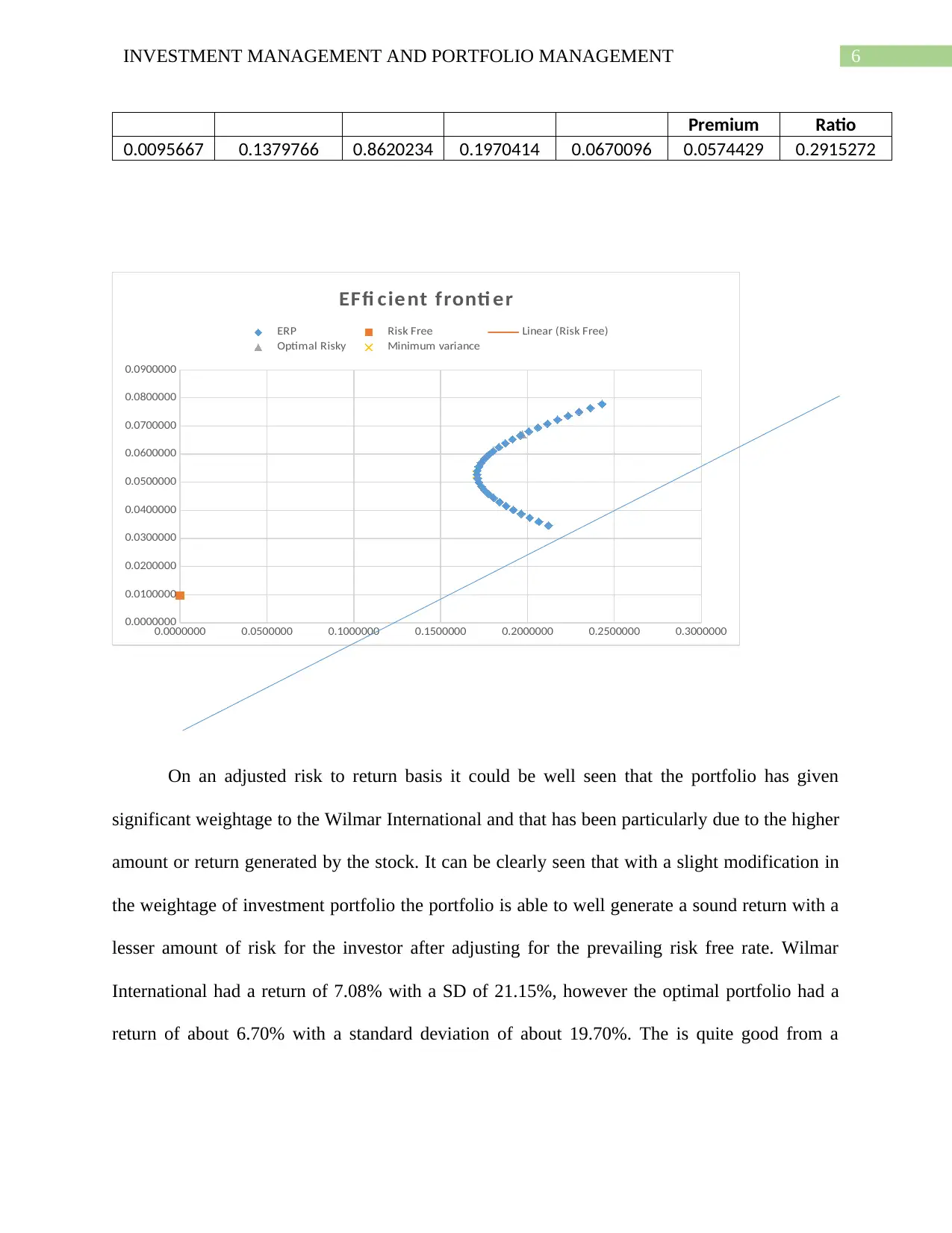

Premium Ratio

0.0095667 0.1379766 0.8620234 0.1970414 0.0670096 0.0574429 0.2915272

0.0000000 0.0500000 0.1000000 0.1500000 0.2000000 0.2500000 0.3000000

0.0000000

0.0100000

0.0200000

0.0300000

0.0400000

0.0500000

0.0600000

0.0700000

0.0800000

0.0900000

EFfi cient fronti er

ERP Risk Free Linear (Risk Free)

Optimal Risky Minimum variance

On an adjusted risk to return basis it could be well seen that the portfolio has given

significant weightage to the Wilmar International and that has been particularly due to the higher

amount or return generated by the stock. It can be clearly seen that with a slight modification in

the weightage of investment portfolio the portfolio is able to well generate a sound return with a

lesser amount of risk for the investor after adjusting for the prevailing risk free rate. Wilmar

International had a return of 7.08% with a SD of 21.15%, however the optimal portfolio had a

return of about 6.70% with a standard deviation of about 19.70%. The is quite good from a

Premium Ratio

0.0095667 0.1379766 0.8620234 0.1970414 0.0670096 0.0574429 0.2915272

0.0000000 0.0500000 0.1000000 0.1500000 0.2000000 0.2500000 0.3000000

0.0000000

0.0100000

0.0200000

0.0300000

0.0400000

0.0500000

0.0600000

0.0700000

0.0800000

0.0900000

EFfi cient fronti er

ERP Risk Free Linear (Risk Free)

Optimal Risky Minimum variance

On an adjusted risk to return basis it could be well seen that the portfolio has given

significant weightage to the Wilmar International and that has been particularly due to the higher

amount or return generated by the stock. It can be clearly seen that with a slight modification in

the weightage of investment portfolio the portfolio is able to well generate a sound return with a

lesser amount of risk for the investor after adjusting for the prevailing risk free rate. Wilmar

International had a return of 7.08% with a SD of 21.15%, however the optimal portfolio had a

return of about 6.70% with a standard deviation of about 19.70%. The is quite good from a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

portfolio perspective as the same would not only be allowing diversification benefits but would

also remove the concentration risk that is attached with a single stock investment.

Minimum Variance Portfolio

A minimum variance portfolio is set of portfolio that is well diversified which consist of

individually risky assets, which are hedged when the same are together traded and the same

results in the lowest possible set of risks for the return that is expected by the investors. The

minimum variance portfolio has been well designed by us with the help of the two stocks in

which we have well determined the weight for UOB to be around 64.74% and around 35.25% for

Wilmar International (Ceria, Sivaramakrishnan and Stubbs 2017). The expected rate of return

that would be well achieved by the created portfolio would be around 5.28% and the expected

standard deviation for the stock was calculated to be around 17.09%.

Minimum Variance Portfolio

W1 W2 MV SP MV ERP

0.6474157 0.3525843 0.1709469 0.0528025

The graph drawn above well shows the minimum variance portfolio or mark which has

been drawn within the efficient frontier curve reflecting the maximum amount of return that the

investors will be able to well generate with the minimum amount of risk level.

Diversification in Portfolio

Diversification in portfolio can be well viewed within the context of risk management

process that is well used by investors and portfolio managers in order to well mitigate the risk

that is associated with the investment (Henriksson eta al., 2019). The key rationale behind this

set of technique is that the constructed portfolio for a wide variety of assets on an average would

portfolio perspective as the same would not only be allowing diversification benefits but would

also remove the concentration risk that is attached with a single stock investment.

Minimum Variance Portfolio

A minimum variance portfolio is set of portfolio that is well diversified which consist of

individually risky assets, which are hedged when the same are together traded and the same

results in the lowest possible set of risks for the return that is expected by the investors. The

minimum variance portfolio has been well designed by us with the help of the two stocks in

which we have well determined the weight for UOB to be around 64.74% and around 35.25% for

Wilmar International (Ceria, Sivaramakrishnan and Stubbs 2017). The expected rate of return

that would be well achieved by the created portfolio would be around 5.28% and the expected

standard deviation for the stock was calculated to be around 17.09%.

Minimum Variance Portfolio

W1 W2 MV SP MV ERP

0.6474157 0.3525843 0.1709469 0.0528025

The graph drawn above well shows the minimum variance portfolio or mark which has

been drawn within the efficient frontier curve reflecting the maximum amount of return that the

investors will be able to well generate with the minimum amount of risk level.

Diversification in Portfolio

Diversification in portfolio can be well viewed within the context of risk management

process that is well used by investors and portfolio managers in order to well mitigate the risk

that is associated with the investment (Henriksson eta al., 2019). The key rationale behind this

set of technique is that the constructed portfolio for a wide variety of assets on an average would

8INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

be yielding a higher and a better long-term set of returns and in turn would also be lowering

down the risk for any individual holding or security. The application of diversification has also

been done in the portfolio constructed whereby we have well taken two key stocks for the

purpose of investment rather than investing into a single stock. The purpose of the same was to

well reduce to lower down the risk that is associated and at the same time modifying the risk

level that is associated with the investment (Chandra and Leong 2016). The application of

portfolio is mostly done by investment professionals in order to well reach a long-term sound

range of financial goals that would be well acting for minimizing the risks associated with the

portfolio. The key takeaways and important points that can be well related to portfolio

diversification are as follows:

The application of diversification in the portfolio management process would be

reducing the risk associated with the investment which can well comes by investing into

different kind s of assets class, industries and other set of categories.

The identified risk in investment can be in the form of Systematic risk as well as

unsystematic risk or diversifiable risk.

Investors can create a well diversified set of portfolio which help them stabilize the

returns and reduce the risk.

The application of diversification is generally considered when there are more than one

asset class in an portfolio for investment and the same process or approach has been followed in

the above set drawn. It can be clearly seen that with a slight modification in the weightage of

investment portfolio the portfolio is able to well generate a sound return with a lesser amount of

risk for the investor after adjusting for the prevailing risk free rate. Wilmar International had a

return of 7.08% with a SD of 21.14%, however the optimal portfolio had a return of about 6.70%

be yielding a higher and a better long-term set of returns and in turn would also be lowering

down the risk for any individual holding or security. The application of diversification has also

been done in the portfolio constructed whereby we have well taken two key stocks for the

purpose of investment rather than investing into a single stock. The purpose of the same was to

well reduce to lower down the risk that is associated and at the same time modifying the risk

level that is associated with the investment (Chandra and Leong 2016). The application of

portfolio is mostly done by investment professionals in order to well reach a long-term sound

range of financial goals that would be well acting for minimizing the risks associated with the

portfolio. The key takeaways and important points that can be well related to portfolio

diversification are as follows:

The application of diversification in the portfolio management process would be

reducing the risk associated with the investment which can well comes by investing into

different kind s of assets class, industries and other set of categories.

The identified risk in investment can be in the form of Systematic risk as well as

unsystematic risk or diversifiable risk.

Investors can create a well diversified set of portfolio which help them stabilize the

returns and reduce the risk.

The application of diversification is generally considered when there are more than one

asset class in an portfolio for investment and the same process or approach has been followed in

the above set drawn. It can be clearly seen that with a slight modification in the weightage of

investment portfolio the portfolio is able to well generate a sound return with a lesser amount of

risk for the investor after adjusting for the prevailing risk free rate. Wilmar International had a

return of 7.08% with a SD of 21.14%, however the optimal portfolio had a return of about 6.70%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

with a standard deviation of about 19.70%. The is quite good from a portfolio perspective as the

same would not only be allowing diversification benefits but would also remove the

concentration risk that is attached with a single stock investment.

Conclusion

The investment analysis has been done for two stocks by well constructing the returns

that have been observed for these stocks over a trend of five years in which average annual

return and risks were some of the ley set of observation that were considered for constructing the

portfolio. The investment opportunity set of portfolio created for the investor goes to well show

the maximum amount of sharp ratio or the excess return that it can earn by well changing the

weights associated with the weights for the two stocks. While the minimum variance portfolio

for the stocks was created with an aim of reducing the standard deviation for the portfolio.

Finally the concept of diversification has been discussed and how the same can be well applied

in the context of portfolio was further discussed. It is also recommended that the constructed

portfolio well includes more than two securities in the portfolio constructed so that the risks

associated can be well diversified. Finally the portfolio considered should be well checked with

the performance of an benchmark index which can be well done with the help of expected return

from the portfolio and the actual return that the portfolio generates. Beta on the other hand, can

be a key and a significant tool which could be well used for checking or assessing the sensitivity

of portfolio with the benchmark index.

with a standard deviation of about 19.70%. The is quite good from a portfolio perspective as the

same would not only be allowing diversification benefits but would also remove the

concentration risk that is attached with a single stock investment.

Conclusion

The investment analysis has been done for two stocks by well constructing the returns

that have been observed for these stocks over a trend of five years in which average annual

return and risks were some of the ley set of observation that were considered for constructing the

portfolio. The investment opportunity set of portfolio created for the investor goes to well show

the maximum amount of sharp ratio or the excess return that it can earn by well changing the

weights associated with the weights for the two stocks. While the minimum variance portfolio

for the stocks was created with an aim of reducing the standard deviation for the portfolio.

Finally the concept of diversification has been discussed and how the same can be well applied

in the context of portfolio was further discussed. It is also recommended that the constructed

portfolio well includes more than two securities in the portfolio constructed so that the risks

associated can be well diversified. Finally the portfolio considered should be well checked with

the performance of an benchmark index which can be well done with the help of expected return

from the portfolio and the actual return that the portfolio generates. Beta on the other hand, can

be a key and a significant tool which could be well used for checking or assessing the sensitivity

of portfolio with the benchmark index.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

References

Adams, S.B., 2018. A Diversified Portfolio: Resources Fueling Silicon Valley Before Venture

Capital. In Business History Conference. Business and Economic History On-line: Papers

Presented at the BHC Annual Meeting (Vol. 16, pp. 1-14). Business History Conference.

Avagyan, V. and Mei, X., 2019. Precision matrix estimation under data contamination with an

application to minimum variance portfolio selection. Communications in Statistics-Simulation

and Computation, pp.1-20.

Benedetti, D., Biffis, E., Chatzimichalakis, F., Fedele, L.L. and Simm, I., 2019. Climate change

investment risk: optimal portfolio construction ahead of the transition to a lower-carbon

economy. Annals of Operations Research, pp.1-25.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-390.

Branch, M., Goldberg, L. and Hand, P., 2020. Practical Applications of A Guide to ESG

Portfolio Construction. Practical Applications, 7(3), pp.1-6.

Calvo, C., Ivorra, C. and Liern, V., 2016. Fuzzy portfolio selection with non-financial goals:

exploring the efficient frontier. Annals of Operations Research, 245(1-2), pp.31-46.

Ceria, S., Sivaramakrishnan, K. and Stubbs, R.A., 2017. Alpha construction in a consistent

investment process. In Portfolio Construction, Measurement, and Efficiency (pp. 257-274).

Springer, Cham.

References

Adams, S.B., 2018. A Diversified Portfolio: Resources Fueling Silicon Valley Before Venture

Capital. In Business History Conference. Business and Economic History On-line: Papers

Presented at the BHC Annual Meeting (Vol. 16, pp. 1-14). Business History Conference.

Avagyan, V. and Mei, X., 2019. Precision matrix estimation under data contamination with an

application to minimum variance portfolio selection. Communications in Statistics-Simulation

and Computation, pp.1-20.

Benedetti, D., Biffis, E., Chatzimichalakis, F., Fedele, L.L. and Simm, I., 2019. Climate change

investment risk: optimal portfolio construction ahead of the transition to a lower-carbon

economy. Annals of Operations Research, pp.1-25.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-390.

Branch, M., Goldberg, L. and Hand, P., 2020. Practical Applications of A Guide to ESG

Portfolio Construction. Practical Applications, 7(3), pp.1-6.

Calvo, C., Ivorra, C. and Liern, V., 2016. Fuzzy portfolio selection with non-financial goals:

exploring the efficient frontier. Annals of Operations Research, 245(1-2), pp.31-46.

Ceria, S., Sivaramakrishnan, K. and Stubbs, R.A., 2017. Alpha construction in a consistent

investment process. In Portfolio Construction, Measurement, and Efficiency (pp. 257-274).

Springer, Cham.

11INVESTMENT MANAGEMENT AND PORTFOLIO MANAGEMENT

Chandra, S. and Leong, F.T., 2016. A diversified portfolio model of adaptability. American

Psychologist, 71(9), p.847.

Clark, B.J., Feinstein, Z. and Simaan, M., 2020. A Machine Learning Efficient

Frontier. Available at SSRN 3541387.

Davis, B.J., 2018. Does financial well-being affect portfolio construction? Evidence from an

online survey. Economics Bulletin, 38(1), pp.362-366.

Deng, Y., 2018. Asset Investment and Portfolio Management of Sustainable Infrastructure

Systems: Optimization and Real-Options Approaches.

Henriksson, R., Livnat, J., Pfeifer, P. and Stumpp, M., 2019. Integrating ESG in portfolio

construction. The Journal of Portfolio Management, 45(4), pp.67-81.

Padma, A. and Rambabu, G., 2017. Optimal Portfolio Construction by Using Sharpe Single

Index Model. Sumedha Journal of Management, 6(4), pp.57-65.

Shimizu, H. and Shiohama, T., 2019. Multifactor Portfolio Construction by Factor Risk Parity

Strategies: An Empirical Comparison of Global Stock Markets. Asia-Pacific Financial

Markets, 26(4), pp.453-477.

Tu, Y.J., Huang, Y.H., Strader, T.J., Subramanyam, R. and Shaw, M.J., 2019. Candidate

diversity and granularity in IT portfolio construction. Information Technology and Management,

pp.1-12.

Chandra, S. and Leong, F.T., 2016. A diversified portfolio model of adaptability. American

Psychologist, 71(9), p.847.

Clark, B.J., Feinstein, Z. and Simaan, M., 2020. A Machine Learning Efficient

Frontier. Available at SSRN 3541387.

Davis, B.J., 2018. Does financial well-being affect portfolio construction? Evidence from an

online survey. Economics Bulletin, 38(1), pp.362-366.

Deng, Y., 2018. Asset Investment and Portfolio Management of Sustainable Infrastructure

Systems: Optimization and Real-Options Approaches.

Henriksson, R., Livnat, J., Pfeifer, P. and Stumpp, M., 2019. Integrating ESG in portfolio

construction. The Journal of Portfolio Management, 45(4), pp.67-81.

Padma, A. and Rambabu, G., 2017. Optimal Portfolio Construction by Using Sharpe Single

Index Model. Sumedha Journal of Management, 6(4), pp.57-65.

Shimizu, H. and Shiohama, T., 2019. Multifactor Portfolio Construction by Factor Risk Parity

Strategies: An Empirical Comparison of Global Stock Markets. Asia-Pacific Financial

Markets, 26(4), pp.453-477.

Tu, Y.J., Huang, Y.H., Strader, T.J., Subramanyam, R. and Shaw, M.J., 2019. Candidate

diversity and granularity in IT portfolio construction. Information Technology and Management,

pp.1-12.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.