25503 Investment Analysis Assignment Part II: Portfolio Analysis

VerifiedAdded on 2023/04/24

|10

|872

|212

Report

AI Summary

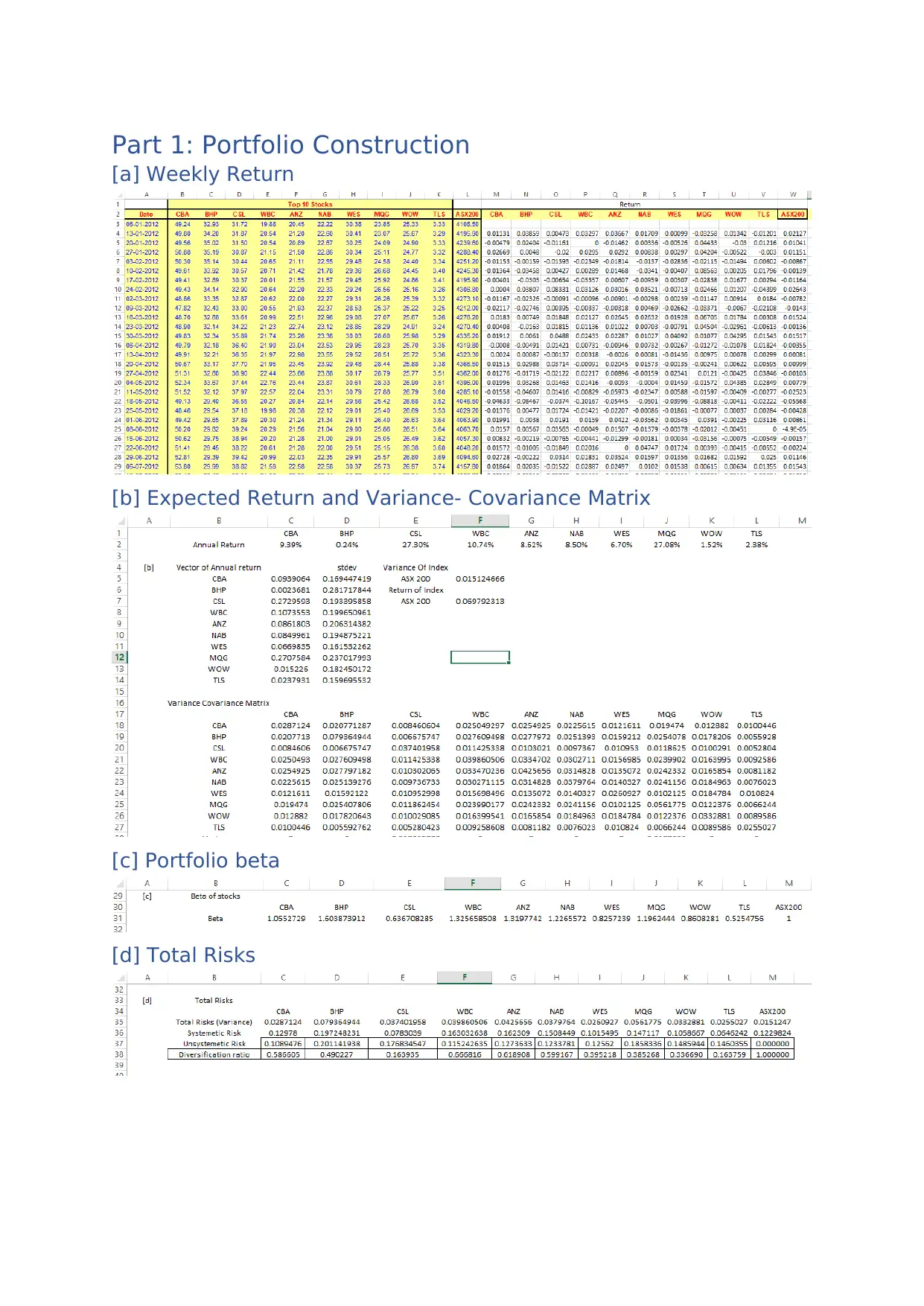

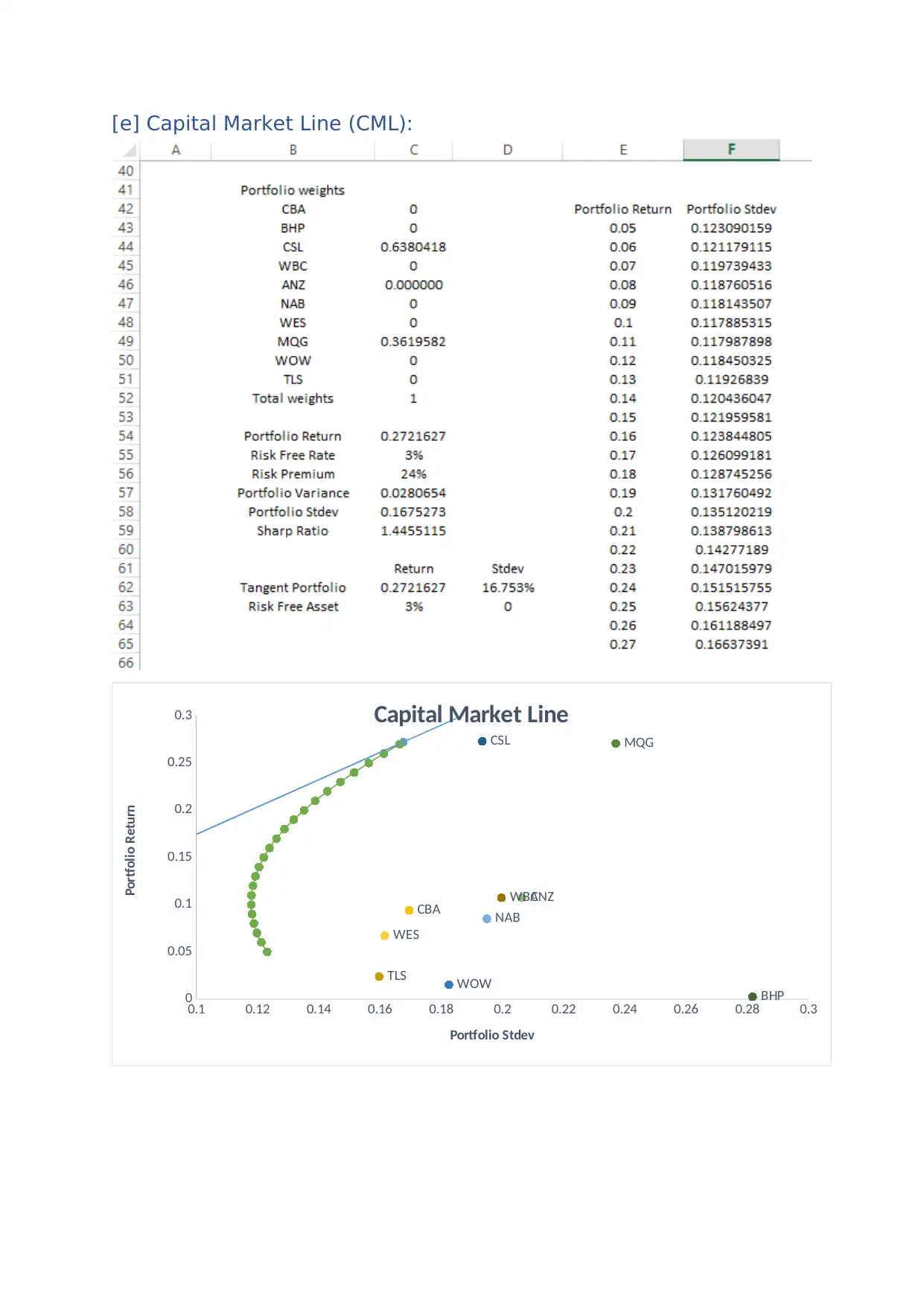

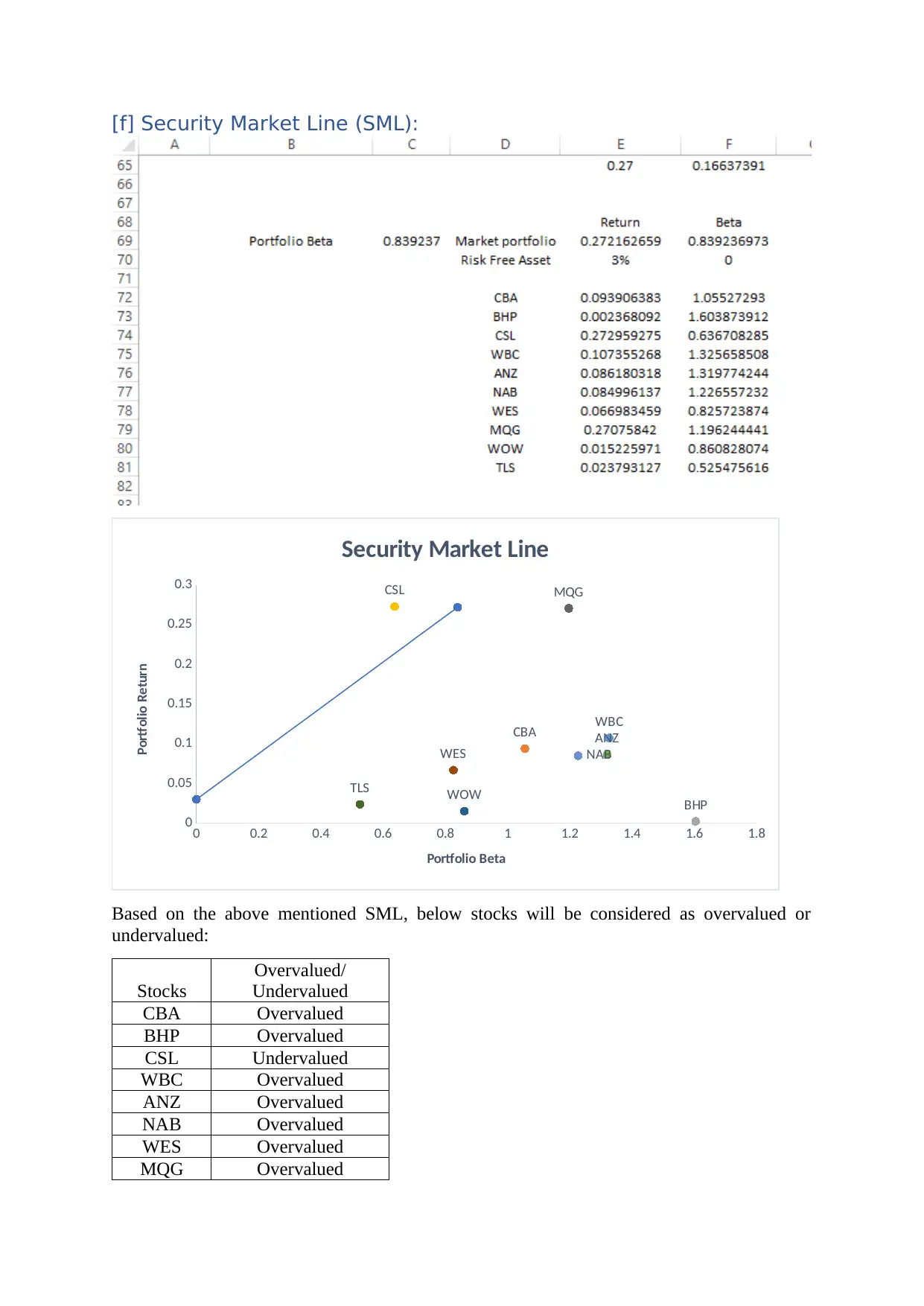

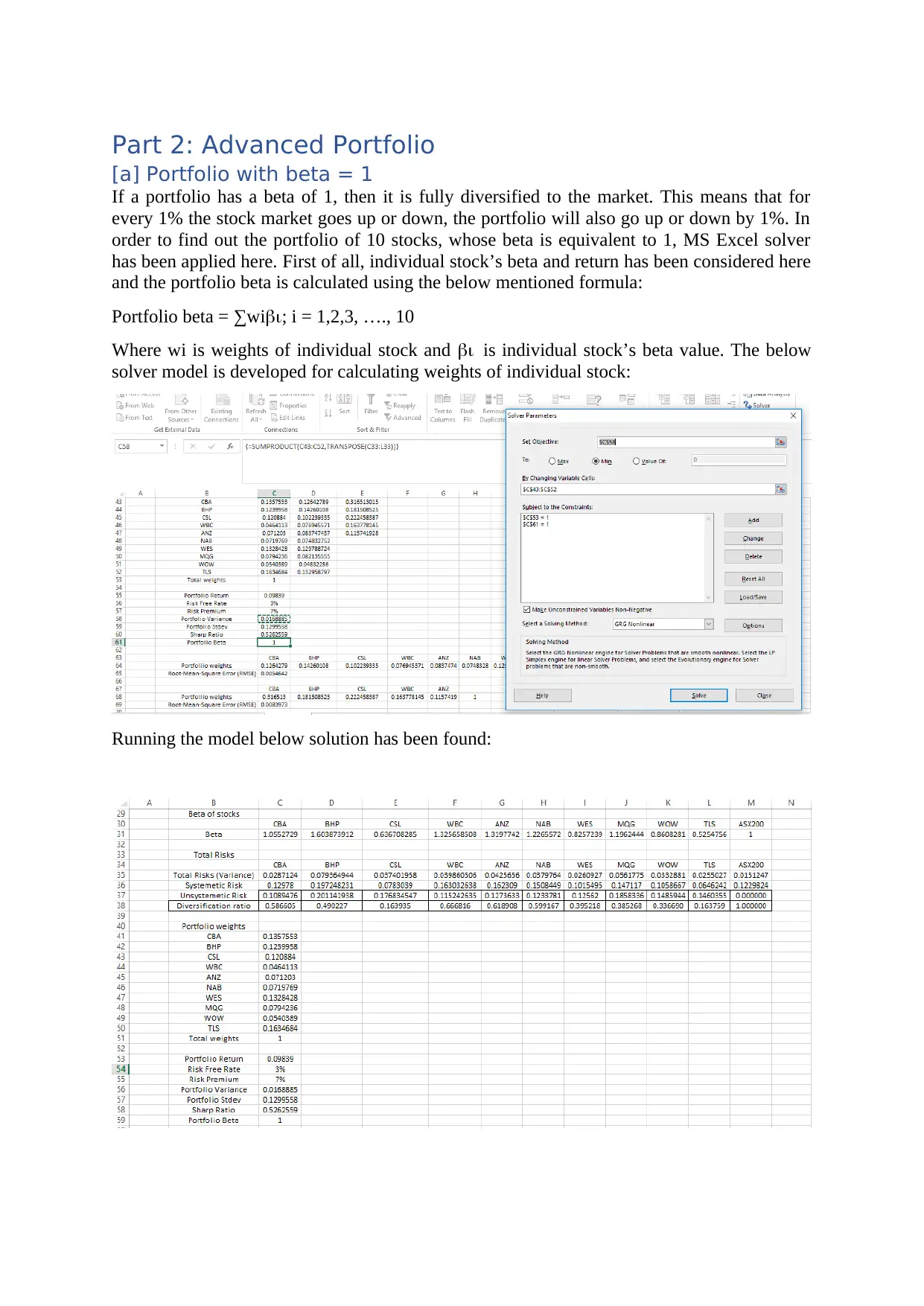

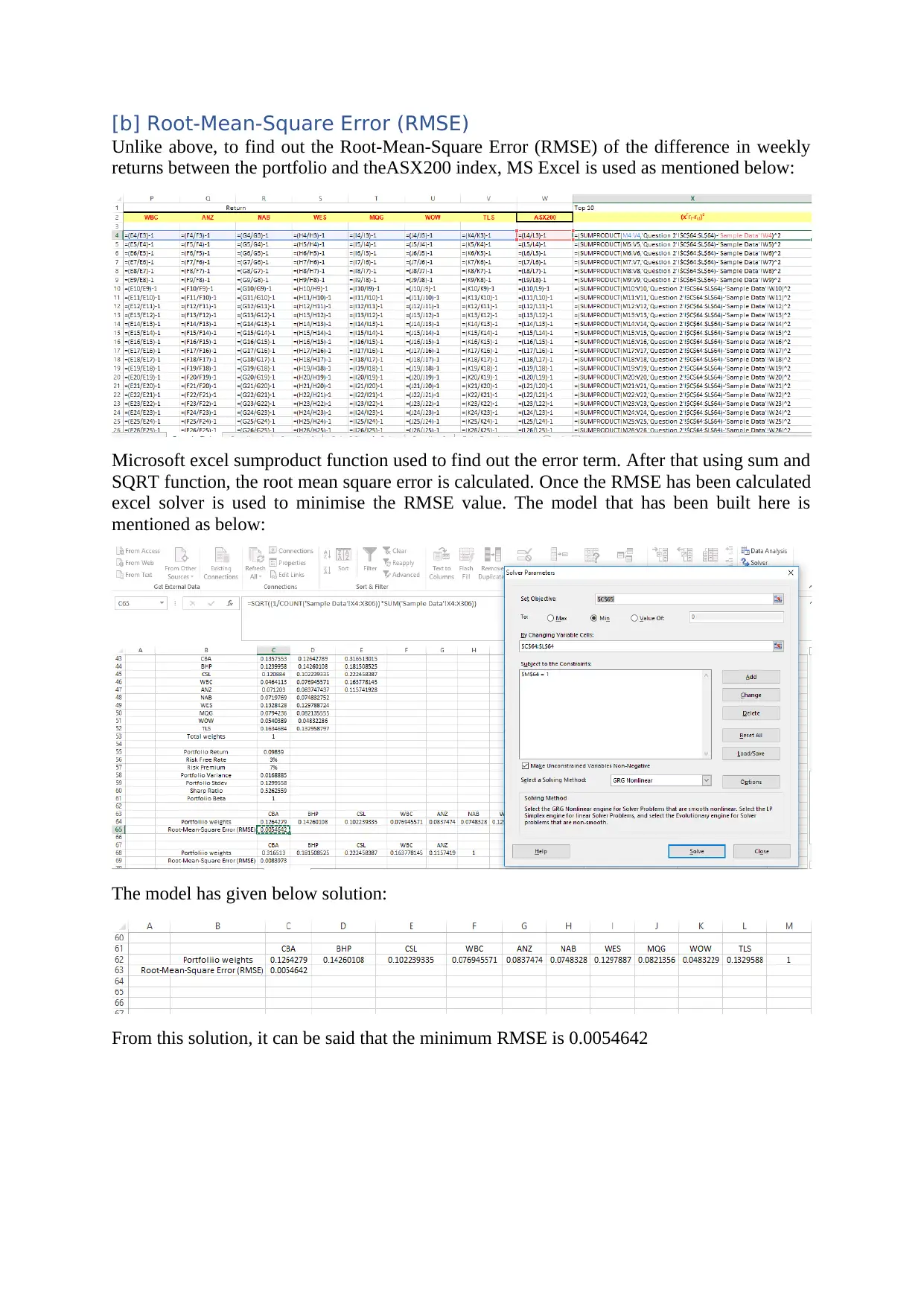

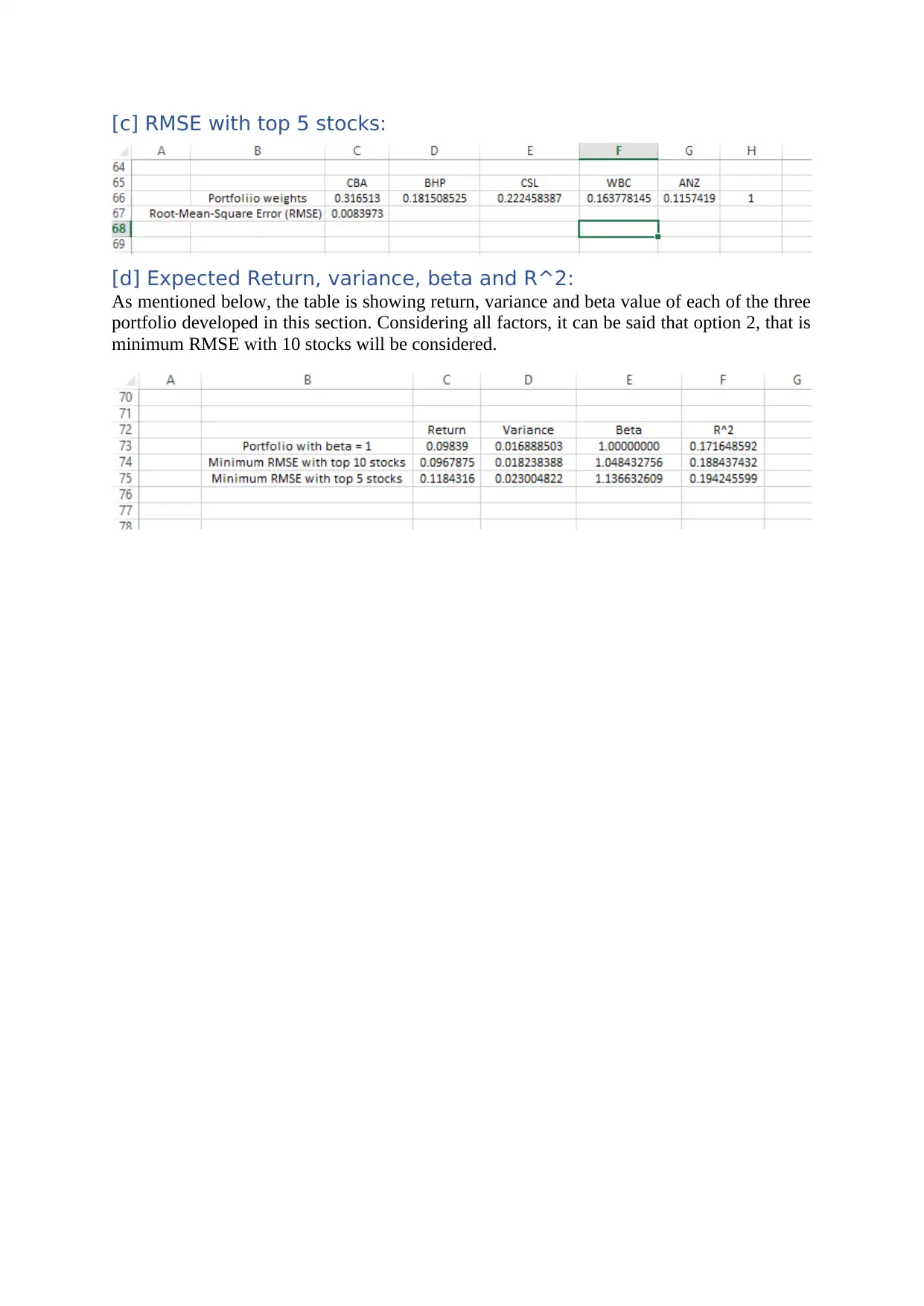

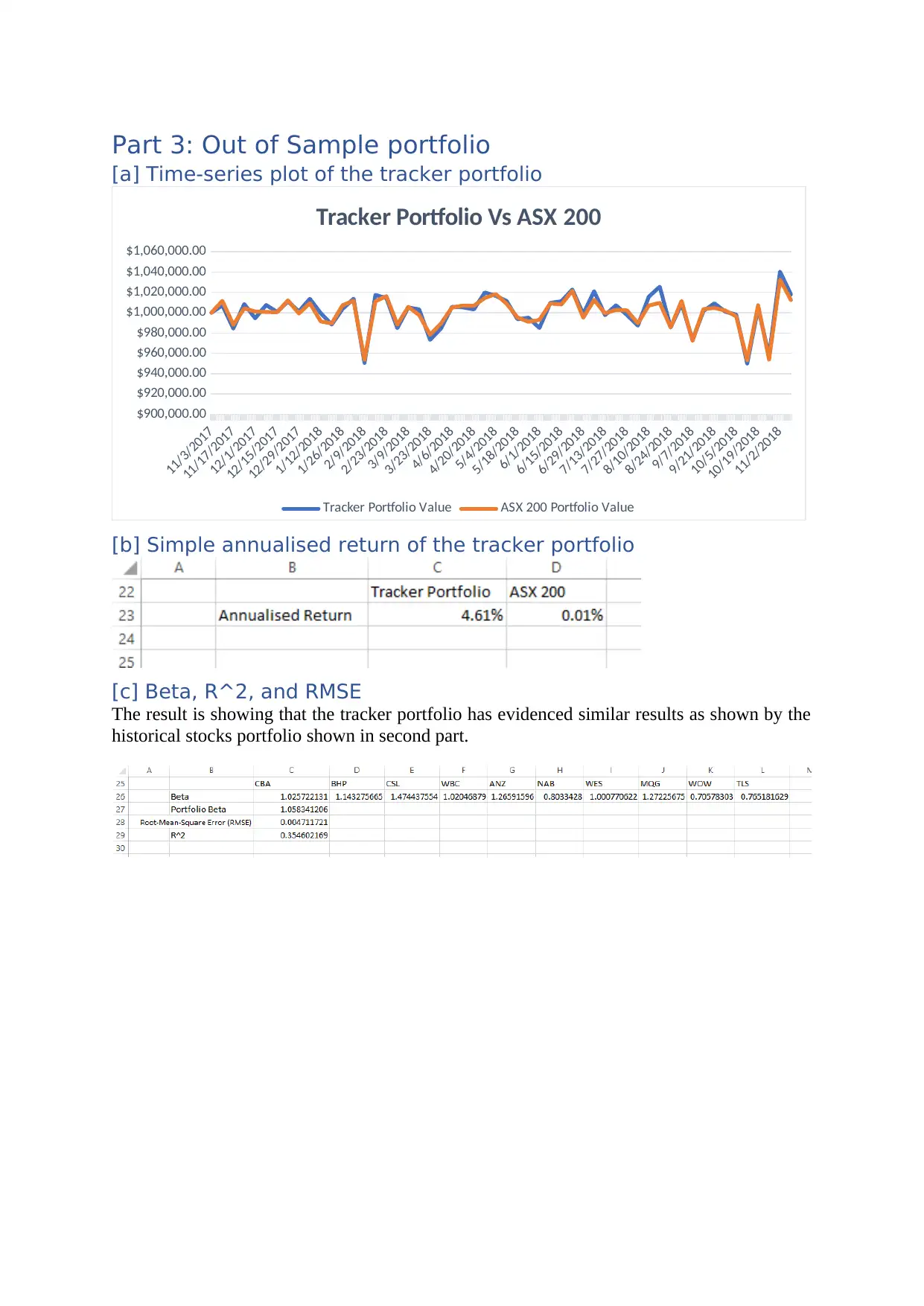

This report provides a detailed analysis of portfolio construction and performance, focusing on key aspects such as weekly returns, expected returns, variance-covariance matrix, portfolio beta, and total risks. It evaluates the Capital Market Line (CML) and Security Market Line (SML) to identify overvalued and undervalued stocks. The report also explores advanced portfolio strategies, including constructing a portfolio with a beta of 1 and minimizing the Root-Mean-Square Error (RMSE) to track the ASX200 index. Furthermore, it examines an out-of-sample tracker portfolio, assessing its annualized return, beta, R^2, and RMSE, comparing its performance against historical stock portfolios. The analysis leverages tools like MS Excel and solver models to optimize portfolio weights and minimize errors, providing a comprehensive evaluation of investment strategies and risk management.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.