Financial Decision Making Report: IKEA Investment Appraisal Techniques

VerifiedAdded on 2019/12/04

|11

|2549

|146

Report

AI Summary

This report delves into the financial decision-making processes of IKEA, focusing on investment appraisal techniques and risk management. It begins by explaining and evaluating various investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback period, illustrating their applicability and limitations through tables and examples. The report then evaluates risk management techniques, including sensitivity analysis, probability analysis, and the use of expected value and decision trees, to assess and mitigate the risks associated with investment projects. The analysis includes a comparative study of different investment options for IKEA, highlighting the importance of selecting projects that maximize profitability and minimize financial risks. The report concludes that a combination of these techniques is crucial for making sound financial decisions and ensuring the long-term success of IKEA's investments.

Financial and Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Explanation and evaluation of investment appraisal techniques.................................................1

Evaluation of risk management techniques in investment appraisal..........................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Explanation and evaluation of investment appraisal techniques.................................................1

Evaluation of risk management techniques in investment appraisal..........................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

Index of Tables

Table 1: NPV and IRR table............................................................................................................2

Table 2: Payback period table..........................................................................................................4

Table 1: NPV and IRR table............................................................................................................2

Table 2: Payback period table..........................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial decision making studies the information from balance sheets, income

statements and cash flow statements to help in management in making plans and strategies. It is

helpful for a company in mapping out their long term ans short term objectives (Francis and

et.al., 2015). The report includes evaluation of investment appraisal techniques and their

applicability. In order to fulfil the objective of the study IKEA Company has been taken in the

report. Furthermore NPV, IRR and Payback period methods have been used for the analysing the

viability of the project. IKEA is a multinational company which sells and designs furnitures,

home accessories and appliances. It is the world's largest furniture manufacturing company and

has more than 12,000 products in its portfolio.

Explanation and evaluation of investment appraisal techniques

Investment appraisal techniques studies the profitability of an investment project. IKEA

has been planning for a major investment in capital equipment. Investment is a long term

decision and it requires huge funds (Graham, Harvey and Puri, 2015). It would be beneficial for

a company to study the cost of investment, returns, payback period and profits from the capital

investment. IKEA may have to raise debt or equity to finance the project. If the project fails and

does not generate enough profits then the company would not be able to pay dividends or interest

to the the people (Götze, Northcott and Schuster, 2015). So, it is essential for IKEA to

understand the impacts of a project on the financial capacity of the company. Some of the major

investment appraisal techniques are:

NPV (Net present value)

Applicability

Net present value is applicable in the analysis and calculation of business value (Sims,

Powell and Vidgen, 2015). It uses the forecast of cash inflows of the projects and their present

value to fin out the profitability of the investment.

Assumptions

It is assumed that all the cash flows have occurred at the end of the year (Dittrich,

Wreford and Moran, 2016).

The cash inflows are reinvested in the business that generates income for the company.

The market is assumed to be a perfect capital market. The cash flows related to the investment are treated as if there is no uncertainty.

1

Financial decision making studies the information from balance sheets, income

statements and cash flow statements to help in management in making plans and strategies. It is

helpful for a company in mapping out their long term ans short term objectives (Francis and

et.al., 2015). The report includes evaluation of investment appraisal techniques and their

applicability. In order to fulfil the objective of the study IKEA Company has been taken in the

report. Furthermore NPV, IRR and Payback period methods have been used for the analysing the

viability of the project. IKEA is a multinational company which sells and designs furnitures,

home accessories and appliances. It is the world's largest furniture manufacturing company and

has more than 12,000 products in its portfolio.

Explanation and evaluation of investment appraisal techniques

Investment appraisal techniques studies the profitability of an investment project. IKEA

has been planning for a major investment in capital equipment. Investment is a long term

decision and it requires huge funds (Graham, Harvey and Puri, 2015). It would be beneficial for

a company to study the cost of investment, returns, payback period and profits from the capital

investment. IKEA may have to raise debt or equity to finance the project. If the project fails and

does not generate enough profits then the company would not be able to pay dividends or interest

to the the people (Götze, Northcott and Schuster, 2015). So, it is essential for IKEA to

understand the impacts of a project on the financial capacity of the company. Some of the major

investment appraisal techniques are:

NPV (Net present value)

Applicability

Net present value is applicable in the analysis and calculation of business value (Sims,

Powell and Vidgen, 2015). It uses the forecast of cash inflows of the projects and their present

value to fin out the profitability of the investment.

Assumptions

It is assumed that all the cash flows have occurred at the end of the year (Dittrich,

Wreford and Moran, 2016).

The cash inflows are reinvested in the business that generates income for the company.

The market is assumed to be a perfect capital market. The cash flows related to the investment are treated as if there is no uncertainty.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

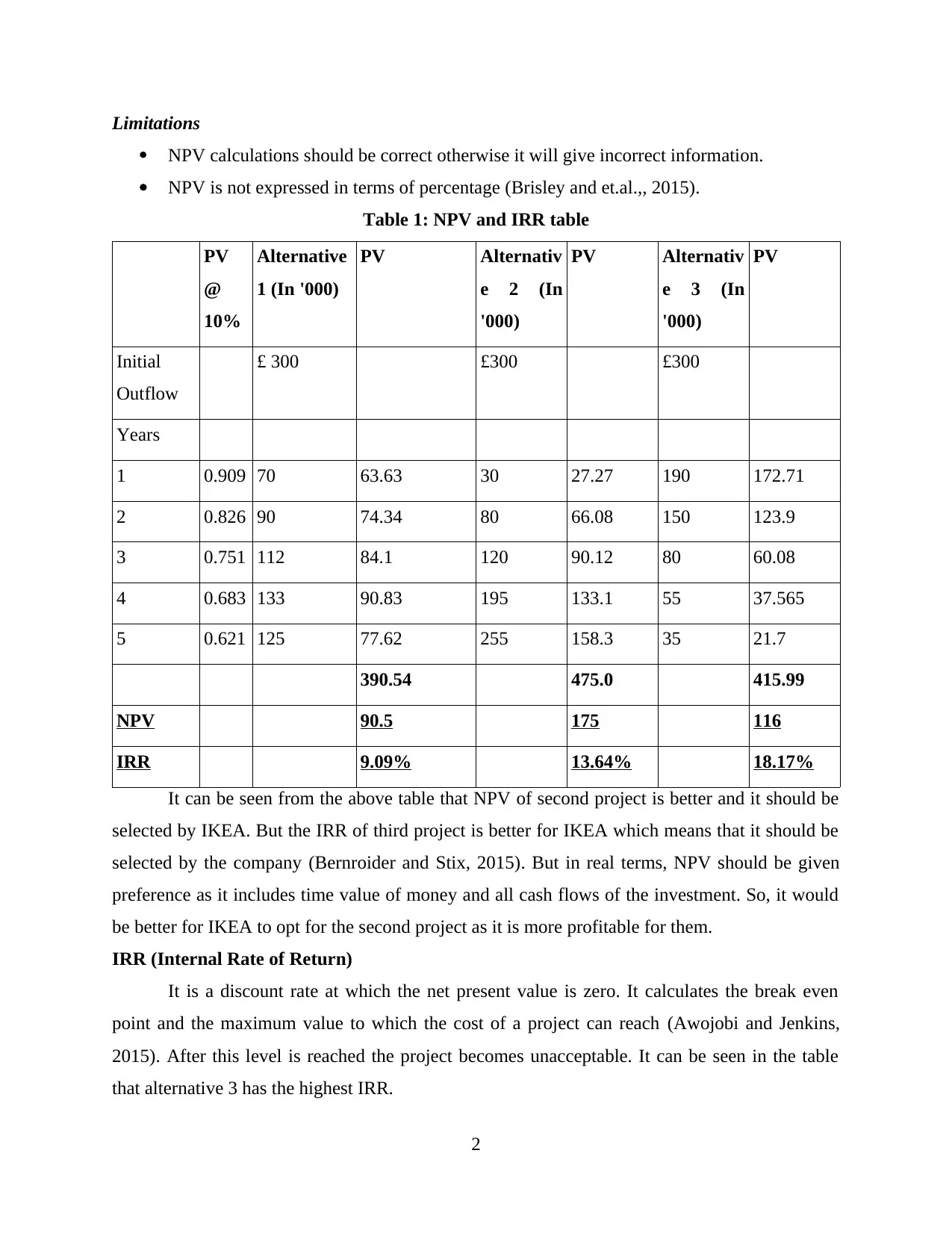

Limitations

NPV calculations should be correct otherwise it will give incorrect information.

NPV is not expressed in terms of percentage (Brisley and et.al.,, 2015).

Table 1: NPV and IRR table

PV

@

10%

Alternative

1 (In '000)

PV Alternativ

e 2 (In

'000)

PV Alternativ

e 3 (In

'000)

PV

Initial

Outflow

£ 300 £300 £300

Years

1 0.909 70 63.63 30 27.27 190 172.71

2 0.826 90 74.34 80 66.08 150 123.9

3 0.751 112 84.1 120 90.12 80 60.08

4 0.683 133 90.83 195 133.1 55 37.565

5 0.621 125 77.62 255 158.3 35 21.7

390.54 475.0 415.99

NPV 90.5 175 116

IRR 9.09% 13.64% 18.17%

It can be seen from the above table that NPV of second project is better and it should be

selected by IKEA. But the IRR of third project is better for IKEA which means that it should be

selected by the company (Bernroider and Stix, 2015). But in real terms, NPV should be given

preference as it includes time value of money and all cash flows of the investment. So, it would

be better for IKEA to opt for the second project as it is more profitable for them.

IRR (Internal Rate of Return)

It is a discount rate at which the net present value is zero. It calculates the break even

point and the maximum value to which the cost of a project can reach (Awojobi and Jenkins,

2015). After this level is reached the project becomes unacceptable. It can be seen in the table

that alternative 3 has the highest IRR.

2

NPV calculations should be correct otherwise it will give incorrect information.

NPV is not expressed in terms of percentage (Brisley and et.al.,, 2015).

Table 1: NPV and IRR table

PV

@

10%

Alternative

1 (In '000)

PV Alternativ

e 2 (In

'000)

PV Alternativ

e 3 (In

'000)

PV

Initial

Outflow

£ 300 £300 £300

Years

1 0.909 70 63.63 30 27.27 190 172.71

2 0.826 90 74.34 80 66.08 150 123.9

3 0.751 112 84.1 120 90.12 80 60.08

4 0.683 133 90.83 195 133.1 55 37.565

5 0.621 125 77.62 255 158.3 35 21.7

390.54 475.0 415.99

NPV 90.5 175 116

IRR 9.09% 13.64% 18.17%

It can be seen from the above table that NPV of second project is better and it should be

selected by IKEA. But the IRR of third project is better for IKEA which means that it should be

selected by the company (Bernroider and Stix, 2015). But in real terms, NPV should be given

preference as it includes time value of money and all cash flows of the investment. So, it would

be better for IKEA to opt for the second project as it is more profitable for them.

IRR (Internal Rate of Return)

It is a discount rate at which the net present value is zero. It calculates the break even

point and the maximum value to which the cost of a project can reach (Awojobi and Jenkins,

2015). After this level is reached the project becomes unacceptable. It can be seen in the table

that alternative 3 has the highest IRR.

2

Applicability

It can be used by IKEA to compare its capital investment projects. It can compare the

expansion wit the opening up of a new branch (Brzozowska, 2015). The investment with higher

IRR should be selected by the company. It can be useful in buyback programs of the company as

well. IRR considers all the cash flows unlike payback period and it is easy to communicate as it

is represented in percentage. It can be used to evaluate the venture capital, IPO, M & A and

private equity.

Assumptions

It is assumed the money is reinvested in the business (Crosetto and Filippin, 2015).

Interim cash flow are also invested in the business. Projects are not mutually exclusive.

Limitations

IRR does not give correct indication of scale.

Negative cash flow can affect the calculation of IRR as it may show more than one values

(Götze, Northcott and Schuster, 2015).

IRR would show incorrect results if there are not normal cash flow streams in the project.

It cannot be used in mutually exclusive projects.

Payback period

Payback period calculates the time length of cash inflows and the initial investment. A

project which has less payback period should be selected as it will be more profitable for the

company (Payback Method, 2016). A manager needs details about the payback period of an

investment rather than the time value of money. The time period of the project can be a variable

to evaluate the viability of the project.

3

It can be used by IKEA to compare its capital investment projects. It can compare the

expansion wit the opening up of a new branch (Brzozowska, 2015). The investment with higher

IRR should be selected by the company. It can be useful in buyback programs of the company as

well. IRR considers all the cash flows unlike payback period and it is easy to communicate as it

is represented in percentage. It can be used to evaluate the venture capital, IPO, M & A and

private equity.

Assumptions

It is assumed the money is reinvested in the business (Crosetto and Filippin, 2015).

Interim cash flow are also invested in the business. Projects are not mutually exclusive.

Limitations

IRR does not give correct indication of scale.

Negative cash flow can affect the calculation of IRR as it may show more than one values

(Götze, Northcott and Schuster, 2015).

IRR would show incorrect results if there are not normal cash flow streams in the project.

It cannot be used in mutually exclusive projects.

Payback period

Payback period calculates the time length of cash inflows and the initial investment. A

project which has less payback period should be selected as it will be more profitable for the

company (Payback Method, 2016). A manager needs details about the payback period of an

investment rather than the time value of money. The time period of the project can be a variable

to evaluate the viability of the project.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

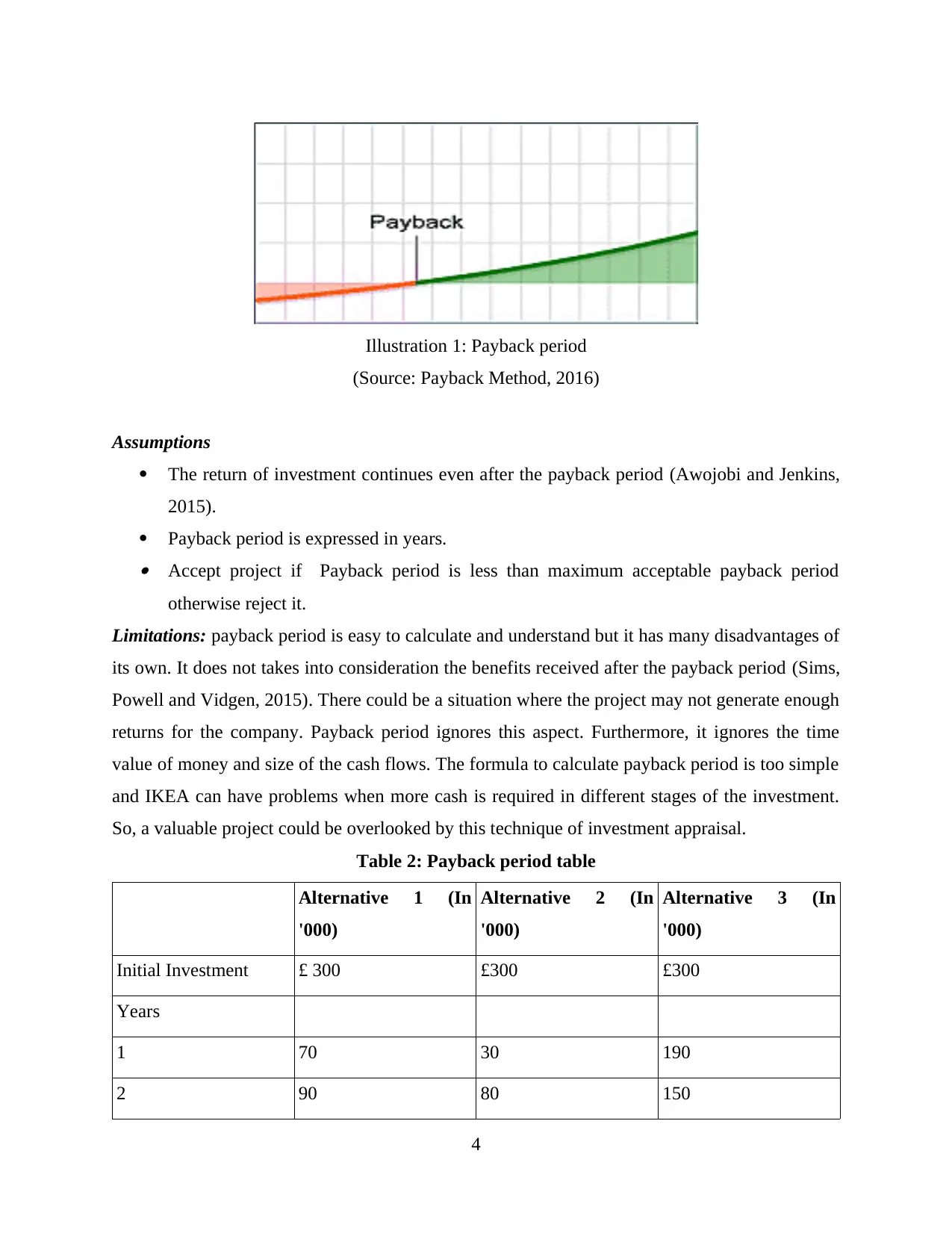

Assumptions

The return of investment continues even after the payback period (Awojobi and Jenkins,

2015).

Payback period is expressed in years. Accept project if Payback period is less than maximum acceptable payback period

otherwise reject it.

Limitations: payback period is easy to calculate and understand but it has many disadvantages of

its own. It does not takes into consideration the benefits received after the payback period (Sims,

Powell and Vidgen, 2015). There could be a situation where the project may not generate enough

returns for the company. Payback period ignores this aspect. Furthermore, it ignores the time

value of money and size of the cash flows. The formula to calculate payback period is too simple

and IKEA can have problems when more cash is required in different stages of the investment.

So, a valuable project could be overlooked by this technique of investment appraisal.

Table 2: Payback period table

Alternative 1 (In

'000)

Alternative 2 (In

'000)

Alternative 3 (In

'000)

Initial Investment £ 300 £300 £300

Years

1 70 30 190

2 90 80 150

4

Illustration 1: Payback period

(Source: Payback Method, 2016)

The return of investment continues even after the payback period (Awojobi and Jenkins,

2015).

Payback period is expressed in years. Accept project if Payback period is less than maximum acceptable payback period

otherwise reject it.

Limitations: payback period is easy to calculate and understand but it has many disadvantages of

its own. It does not takes into consideration the benefits received after the payback period (Sims,

Powell and Vidgen, 2015). There could be a situation where the project may not generate enough

returns for the company. Payback period ignores this aspect. Furthermore, it ignores the time

value of money and size of the cash flows. The formula to calculate payback period is too simple

and IKEA can have problems when more cash is required in different stages of the investment.

So, a valuable project could be overlooked by this technique of investment appraisal.

Table 2: Payback period table

Alternative 1 (In

'000)

Alternative 2 (In

'000)

Alternative 3 (In

'000)

Initial Investment £ 300 £300 £300

Years

1 70 30 190

2 90 80 150

4

Illustration 1: Payback period

(Source: Payback Method, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

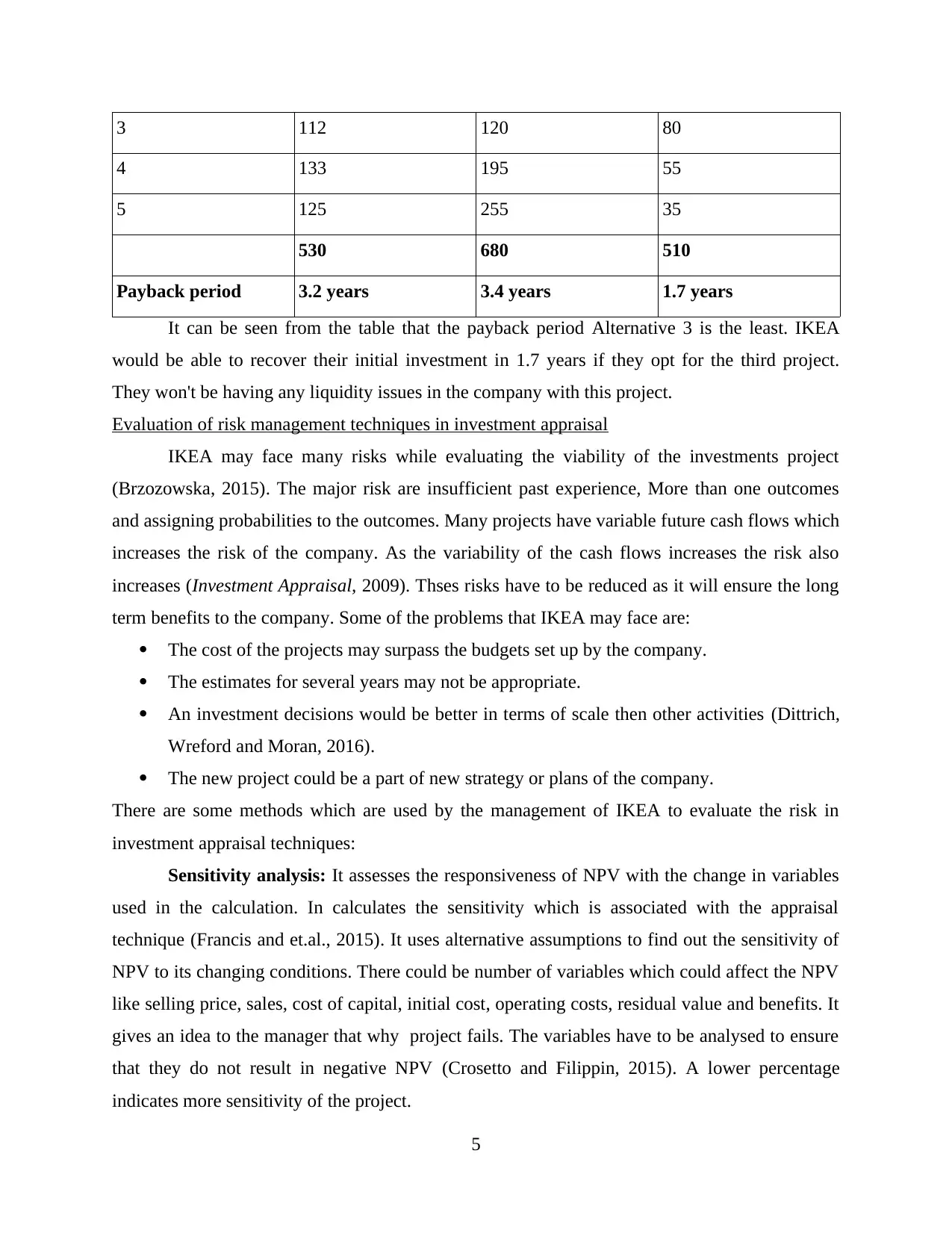

3 112 120 80

4 133 195 55

5 125 255 35

530 680 510

Payback period 3.2 years 3.4 years 1.7 years

It can be seen from the table that the payback period Alternative 3 is the least. IKEA

would be able to recover their initial investment in 1.7 years if they opt for the third project.

They won't be having any liquidity issues in the company with this project.

Evaluation of risk management techniques in investment appraisal

IKEA may face many risks while evaluating the viability of the investments project

(Brzozowska, 2015). The major risk are insufficient past experience, More than one outcomes

and assigning probabilities to the outcomes. Many projects have variable future cash flows which

increases the risk of the company. As the variability of the cash flows increases the risk also

increases (Investment Appraisal, 2009). Thses risks have to be reduced as it will ensure the long

term benefits to the company. Some of the problems that IKEA may face are:

The cost of the projects may surpass the budgets set up by the company.

The estimates for several years may not be appropriate.

An investment decisions would be better in terms of scale then other activities (Dittrich,

Wreford and Moran, 2016).

The new project could be a part of new strategy or plans of the company.

There are some methods which are used by the management of IKEA to evaluate the risk in

investment appraisal techniques:

Sensitivity analysis: It assesses the responsiveness of NPV with the change in variables

used in the calculation. In calculates the sensitivity which is associated with the appraisal

technique (Francis and et.al., 2015). It uses alternative assumptions to find out the sensitivity of

NPV to its changing conditions. There could be number of variables which could affect the NPV

like selling price, sales, cost of capital, initial cost, operating costs, residual value and benefits. It

gives an idea to the manager that why project fails. The variables have to be analysed to ensure

that they do not result in negative NPV (Crosetto and Filippin, 2015). A lower percentage

indicates more sensitivity of the project.

5

4 133 195 55

5 125 255 35

530 680 510

Payback period 3.2 years 3.4 years 1.7 years

It can be seen from the table that the payback period Alternative 3 is the least. IKEA

would be able to recover their initial investment in 1.7 years if they opt for the third project.

They won't be having any liquidity issues in the company with this project.

Evaluation of risk management techniques in investment appraisal

IKEA may face many risks while evaluating the viability of the investments project

(Brzozowska, 2015). The major risk are insufficient past experience, More than one outcomes

and assigning probabilities to the outcomes. Many projects have variable future cash flows which

increases the risk of the company. As the variability of the cash flows increases the risk also

increases (Investment Appraisal, 2009). Thses risks have to be reduced as it will ensure the long

term benefits to the company. Some of the problems that IKEA may face are:

The cost of the projects may surpass the budgets set up by the company.

The estimates for several years may not be appropriate.

An investment decisions would be better in terms of scale then other activities (Dittrich,

Wreford and Moran, 2016).

The new project could be a part of new strategy or plans of the company.

There are some methods which are used by the management of IKEA to evaluate the risk in

investment appraisal techniques:

Sensitivity analysis: It assesses the responsiveness of NPV with the change in variables

used in the calculation. In calculates the sensitivity which is associated with the appraisal

technique (Francis and et.al., 2015). It uses alternative assumptions to find out the sensitivity of

NPV to its changing conditions. There could be number of variables which could affect the NPV

like selling price, sales, cost of capital, initial cost, operating costs, residual value and benefits. It

gives an idea to the manager that why project fails. The variables have to be analysed to ensure

that they do not result in negative NPV (Crosetto and Filippin, 2015). A lower percentage

indicates more sensitivity of the project.

5

Sensitivity (%)=NPV / (Present value of project variables)

Probability analysis: Probability analysis can also be used to calculate NPV and risk.

The probability distribution of cash flow can estimated and the results could be evaluated.

Initially the expected value of the NPV is calculated (Dittrich, Wreford and Moran, 2016). All

the risks associated with the business is evaluated and probabilities are computed. After that

NPV and standard deviation is calculated for he project. It can be a complex procedure for a

manager as it requires many calculations. But it will allow IKEA to reduce the risks of the

investment appraisal techniques.

Expected value and decision tree: These are management tools which are used to

calculate the risk of the investment appraisal techniques. It considers all those factors which are

seasonal in nature. It uses averages for a long term repetitive events (Graham, Harvey and Puri,

2015).

Apart form these techniques, IKEA can use maximin and minimax approach for reducing

the risk. It basic idea behind this technique is to maximize the possible returns of the project and

ignore the consequences of the project (Investment Appraisal, 2009). While minimax is opposite

of maximin and it takes into consideration the worst consequences from all the projects. It is a

pessimistic approach of evaluation of risk but it is very beneficial for the invest appraisal

technique of IKEA.

CONCLUSION

The report concludes that IKEA has to use investment appraisal techniques like NPV,

IRR and payback period to ensure that their investments are profitable. These techniques allow

them to choose the best alternative from the given investment opportunities. So, it reduce the risk

of failure of the project as the future profitability can be calculated with the help of it. There are

certain limitations of IRR, NPV and payback methods which has to be considered before using

them. The management of IKEA has to adopt same risk evaluation methods so as to reduce these

risks and uncertainties.

6

Probability analysis: Probability analysis can also be used to calculate NPV and risk.

The probability distribution of cash flow can estimated and the results could be evaluated.

Initially the expected value of the NPV is calculated (Dittrich, Wreford and Moran, 2016). All

the risks associated with the business is evaluated and probabilities are computed. After that

NPV and standard deviation is calculated for he project. It can be a complex procedure for a

manager as it requires many calculations. But it will allow IKEA to reduce the risks of the

investment appraisal techniques.

Expected value and decision tree: These are management tools which are used to

calculate the risk of the investment appraisal techniques. It considers all those factors which are

seasonal in nature. It uses averages for a long term repetitive events (Graham, Harvey and Puri,

2015).

Apart form these techniques, IKEA can use maximin and minimax approach for reducing

the risk. It basic idea behind this technique is to maximize the possible returns of the project and

ignore the consequences of the project (Investment Appraisal, 2009). While minimax is opposite

of maximin and it takes into consideration the worst consequences from all the projects. It is a

pessimistic approach of evaluation of risk but it is very beneficial for the invest appraisal

technique of IKEA.

CONCLUSION

The report concludes that IKEA has to use investment appraisal techniques like NPV,

IRR and payback period to ensure that their investments are profitable. These techniques allow

them to choose the best alternative from the given investment opportunities. So, it reduce the risk

of failure of the project as the future profitability can be calculated with the help of it. There are

certain limitations of IRR, NPV and payback methods which has to be considered before using

them. The management of IKEA has to adopt same risk evaluation methods so as to reduce these

risks and uncertainties.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journal

Awojobi, O. and Jenkins, G., 2015. Managing the Cost Overrun Risks of Hydroelectric Dams:

An Application of Reference Class Forecasting Techniques (No. 2015-06). JDI Executive

Programs.

Bernroider, E.W. and Stix, V., 2015. On The Applicability of Data Envelopment Analysis for

Multiple Attriliute Decision Making in the Context of Information Systems

Appraisals. Communications of the IIMA, 6(2), p.13.

Brisley, R. and et.al.,, 2015. Techniques for valuing adaptive capacity in flood risk

management.Proceedings of the ICE-Water Management.

Brzozowska, K., 2015. Cost-Benefit Analysis in Public Project Appraisal.Engineering

Economics, 53(3).

Crosetto, P. and Filippin, A., 2015. A theoretical and experimental appraisal of four risk

elicitation methods. Experimental Economics, pp.1-29.

Dittrich, R., Wreford, A. and Moran, D., 2016. A survey of decision-making approaches for

climate change adaptation: Are robust methods the way forward?. Ecological

Economics, 122, pp.79-89.

Francis, B. and et.al., 2015. Gender differences in financial reporting decision making: Evidence

from accounting conservatism.Contemporary Accounting Research. 32(3). pp.1285-1318.

Götze, U., Northcott, D. and Schuster, P., 2015. Capital Budgeting and Investment Decisions.

In Investment Appraisal (pp. 3-26). Springer Berlin Heidelberg.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Sims, J., Powell, P. and Vidgen, R., 2015. Investment appraisal and evaluation: preserving tacit

knowledge and competitive advantage.International Journal of Business and Systems

Research, 9(1), pp.86-103.

Online

Investment Appraisal. 2009. [Online] Available through:

<https://www.icaew.com/~/media/corporate/files/technical/business%20and%20financial

%20management/special%20reports%20archive/sr27%20investment%20appraisal.ashx>.

[Accessed on 4th May 2016].

7

Books and journal

Awojobi, O. and Jenkins, G., 2015. Managing the Cost Overrun Risks of Hydroelectric Dams:

An Application of Reference Class Forecasting Techniques (No. 2015-06). JDI Executive

Programs.

Bernroider, E.W. and Stix, V., 2015. On The Applicability of Data Envelopment Analysis for

Multiple Attriliute Decision Making in the Context of Information Systems

Appraisals. Communications of the IIMA, 6(2), p.13.

Brisley, R. and et.al.,, 2015. Techniques for valuing adaptive capacity in flood risk

management.Proceedings of the ICE-Water Management.

Brzozowska, K., 2015. Cost-Benefit Analysis in Public Project Appraisal.Engineering

Economics, 53(3).

Crosetto, P. and Filippin, A., 2015. A theoretical and experimental appraisal of four risk

elicitation methods. Experimental Economics, pp.1-29.

Dittrich, R., Wreford, A. and Moran, D., 2016. A survey of decision-making approaches for

climate change adaptation: Are robust methods the way forward?. Ecological

Economics, 122, pp.79-89.

Francis, B. and et.al., 2015. Gender differences in financial reporting decision making: Evidence

from accounting conservatism.Contemporary Accounting Research. 32(3). pp.1285-1318.

Götze, U., Northcott, D. and Schuster, P., 2015. Capital Budgeting and Investment Decisions.

In Investment Appraisal (pp. 3-26). Springer Berlin Heidelberg.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Sims, J., Powell, P. and Vidgen, R., 2015. Investment appraisal and evaluation: preserving tacit

knowledge and competitive advantage.International Journal of Business and Systems

Research, 9(1), pp.86-103.

Online

Investment Appraisal. 2009. [Online] Available through:

<https://www.icaew.com/~/media/corporate/files/technical/business%20and%20financial

%20management/special%20reports%20archive/sr27%20investment%20appraisal.ashx>.

[Accessed on 4th May 2016].

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payback Method. 2016. [Online] Available through: <http://www.accountingtools.com/payback-

period-formula>. [Accessed on 4th May 2016].

8

period-formula>. [Accessed on 4th May 2016].

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.