Investment Appraisal Report: Financial and Management Accounting IY049

VerifiedAdded on 2022/12/15

|8

|1602

|221

Report

AI Summary

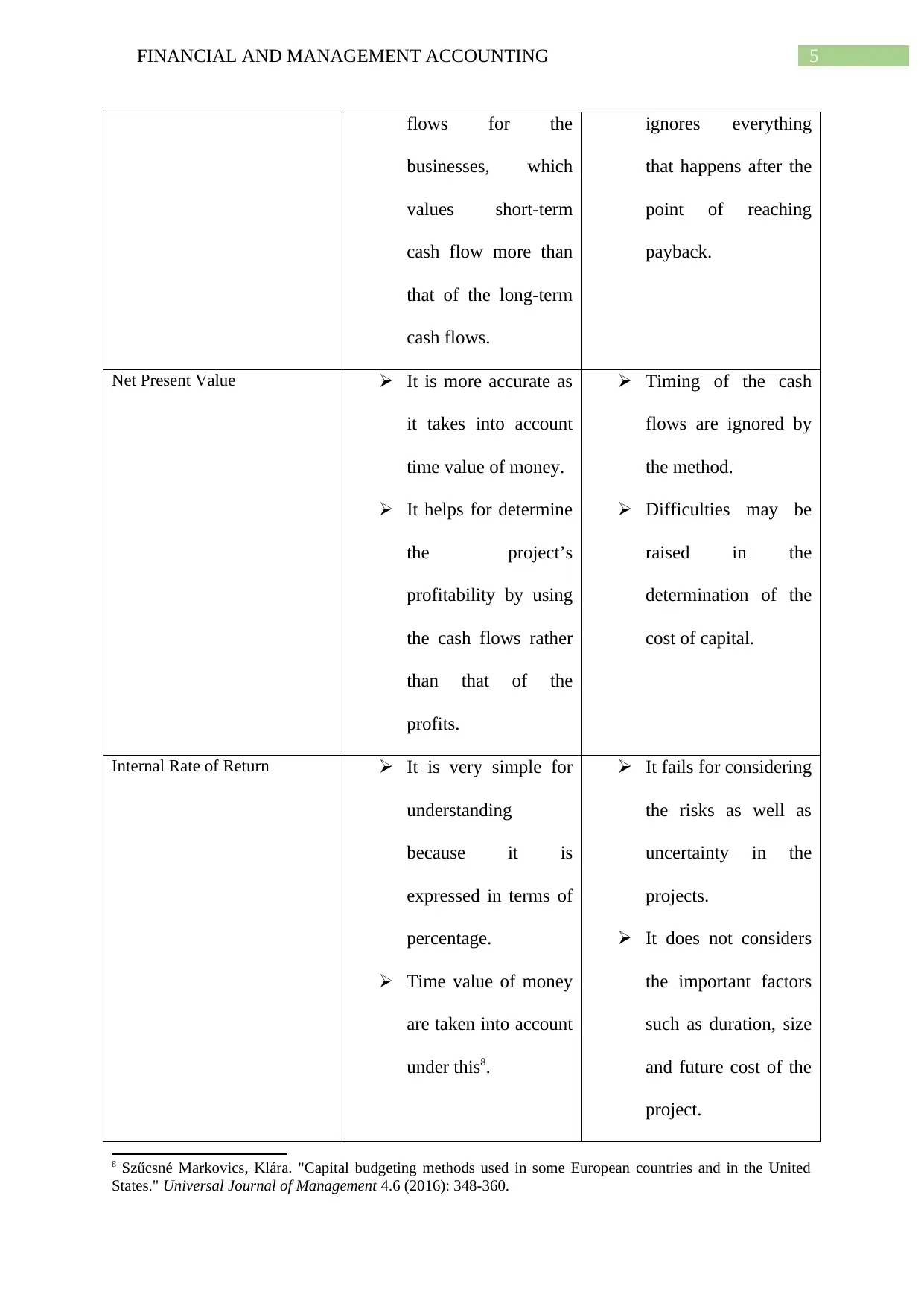

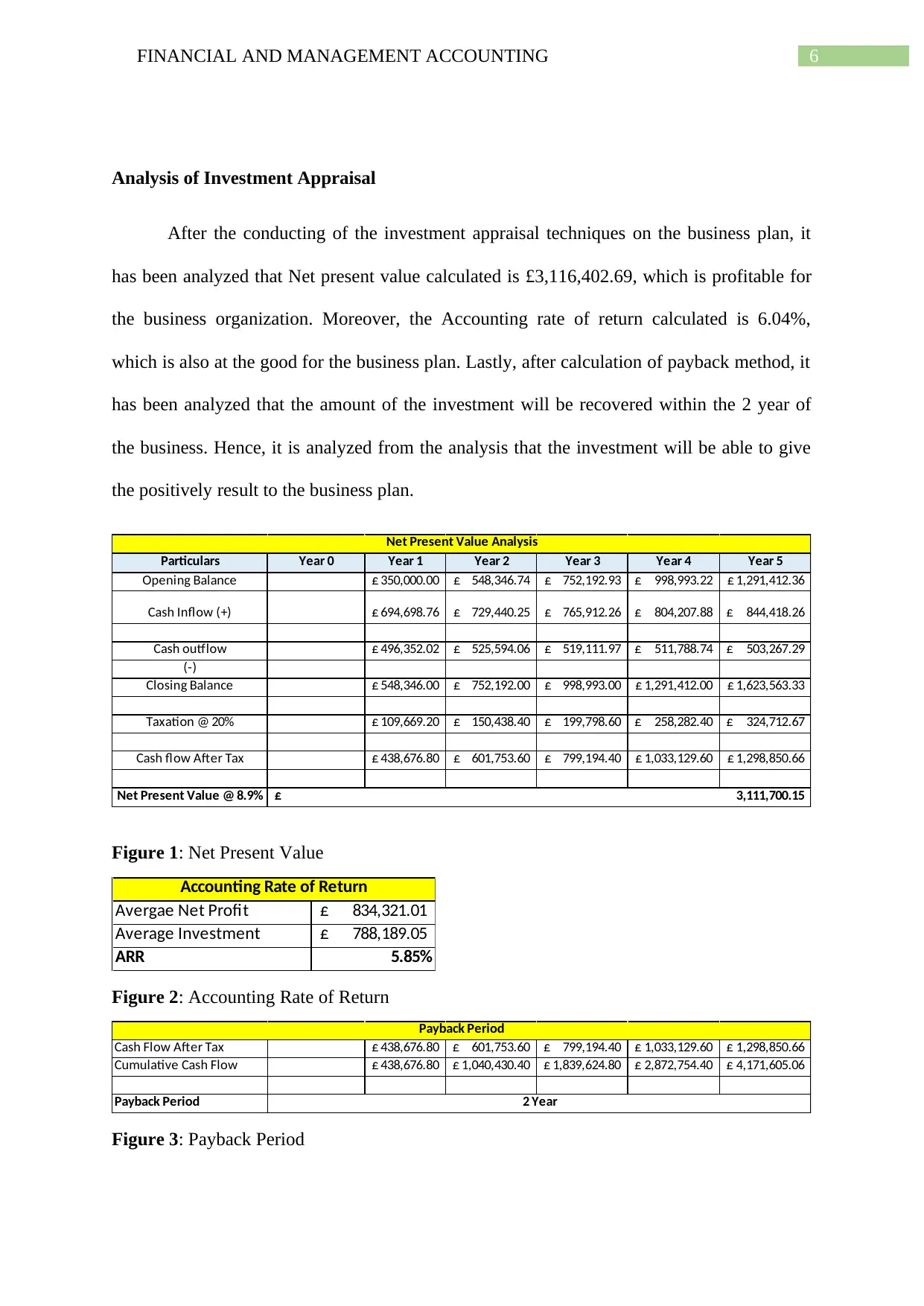

This report delves into the critical area of investment appraisal, a cornerstone of financial and management accounting. It begins by defining investment appraisal and its purpose: to assess the viability of potential investments, projects, or programs, and to determine the value they generate. The report outlines the various factors considered in investment appraisal, including financial, legal, environmental, social, and operational aspects, with a primary focus on financial appraisal for quantifiable benefits. It emphasizes the importance of investment appraisal for businesses, particularly when considering new ventures or investments, as it helps in understanding the feasibility of strategic and tactical objectives. The report then explores the key techniques of investment appraisal, such as Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR), detailing their methodologies, advantages, and disadvantages. The analysis section applies these techniques to a hypothetical business plan, calculating NPV, ARR, and payback period to determine the investment's potential profitability and the time required to recover the initial investment. The report concludes by highlighting the significance of these techniques in making informed investment decisions and ensuring alignment with the strategic goals of the company. It also references several sources used for the report.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.