UGB223 Business Finance: Evaluating Investments and Financial Health

VerifiedAdded on 2023/06/18

|15

|1257

|177

Homework Assignment

AI Summary

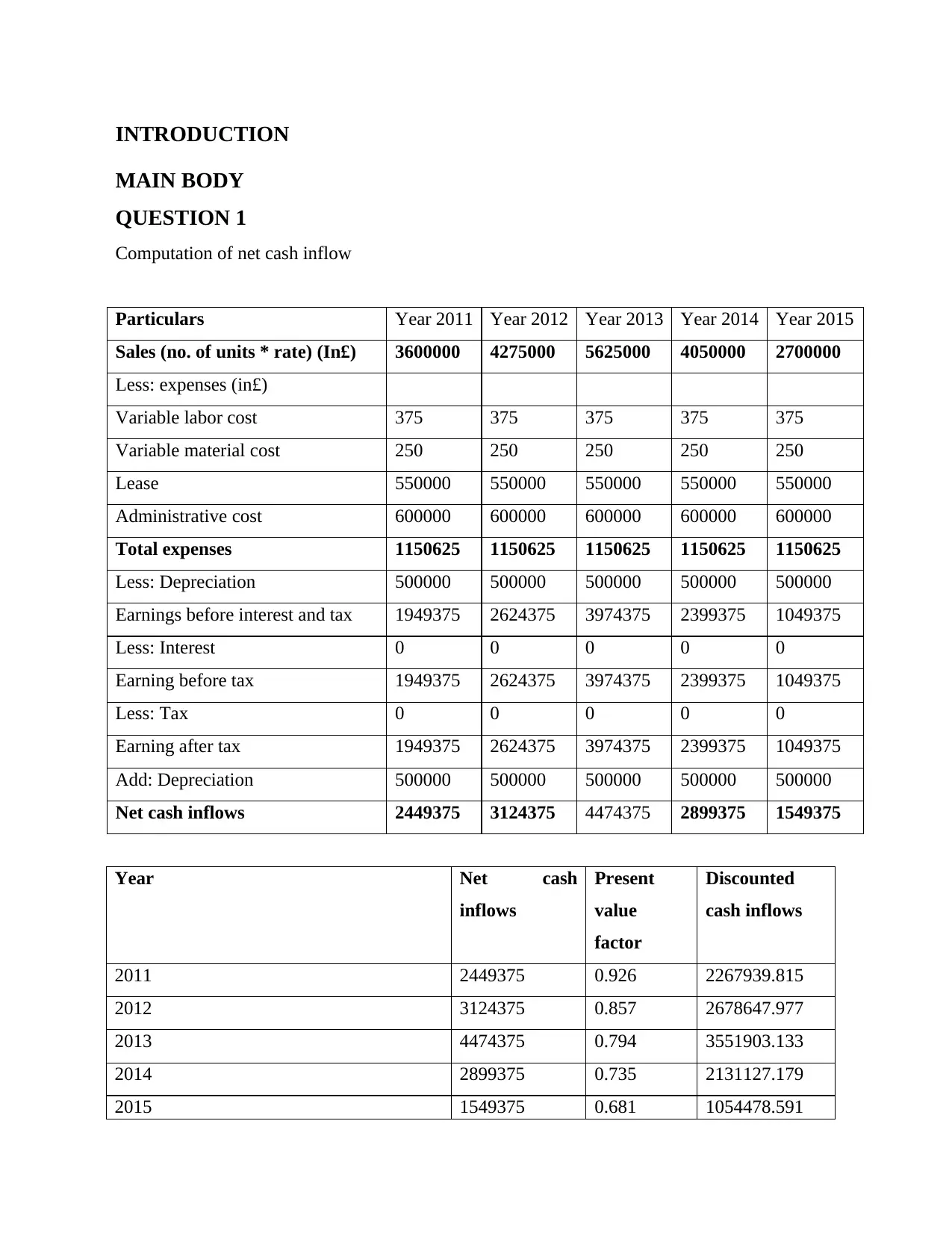

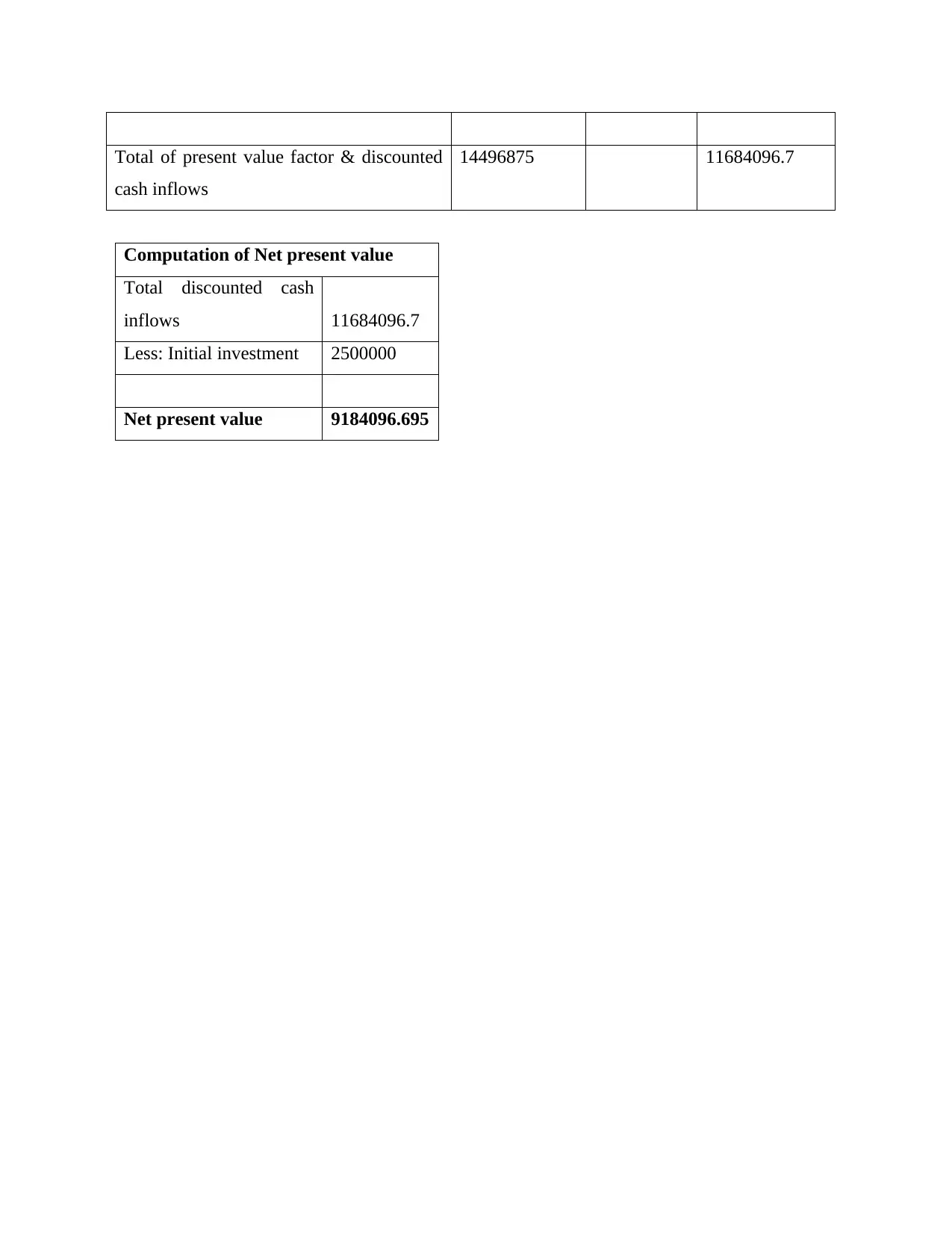

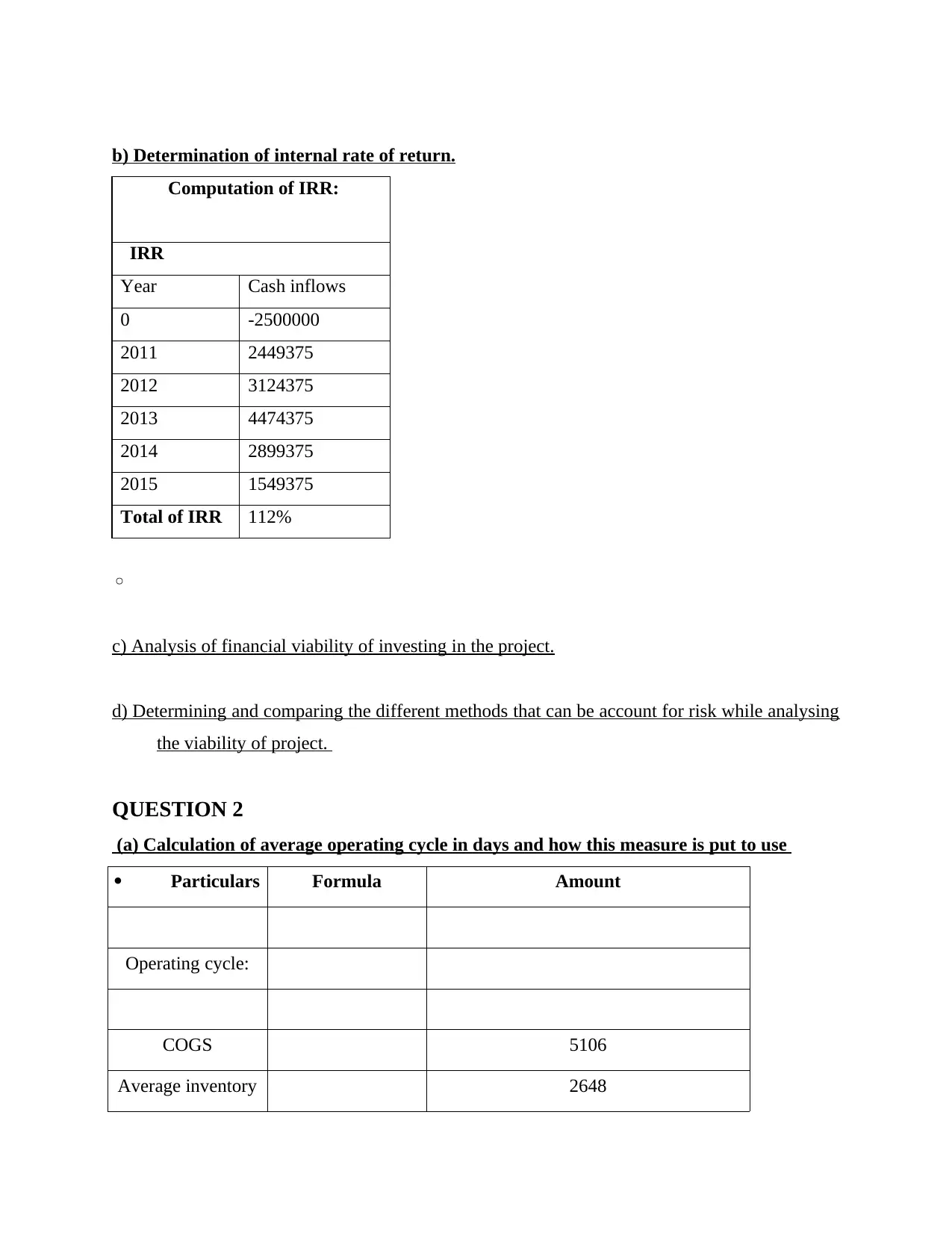

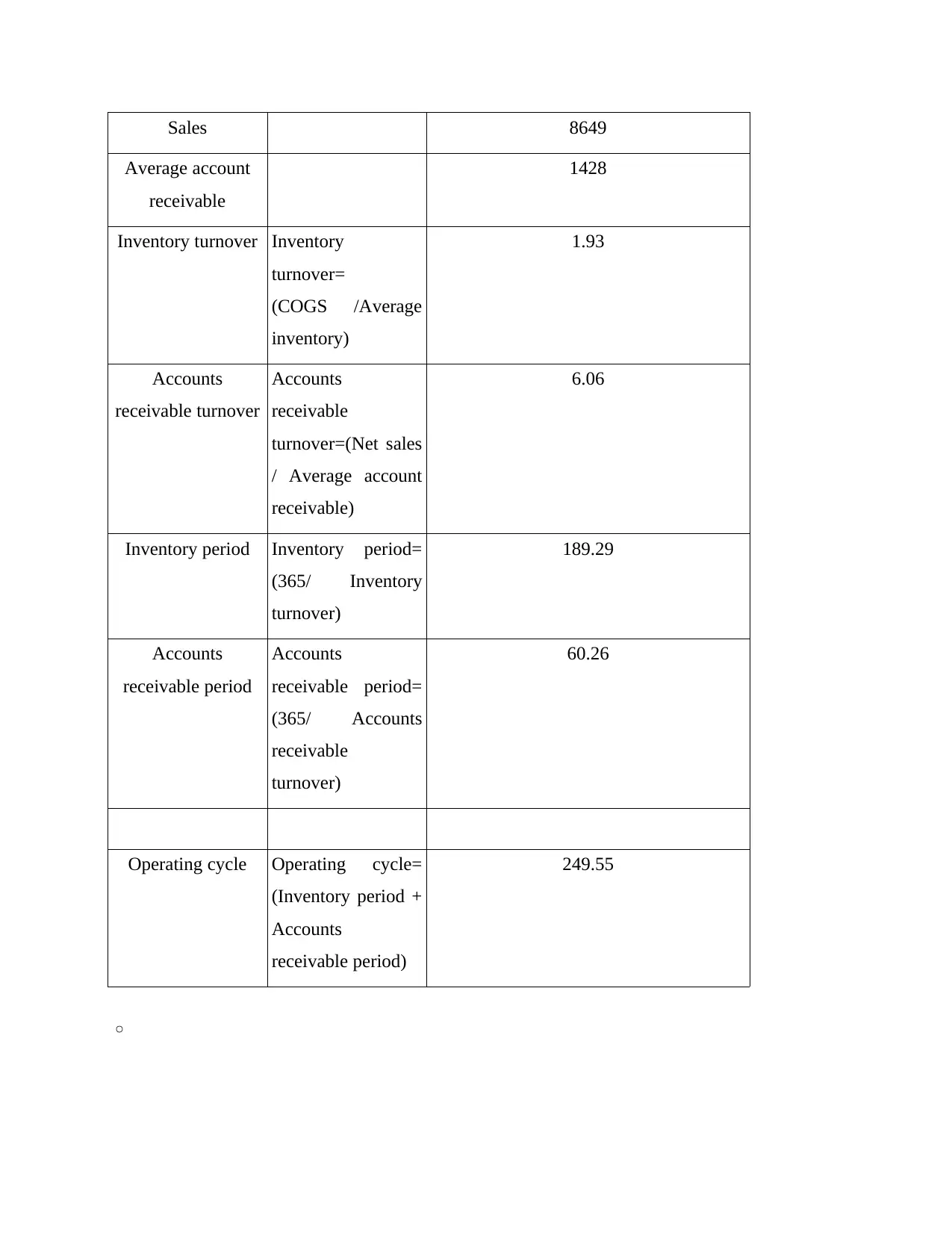

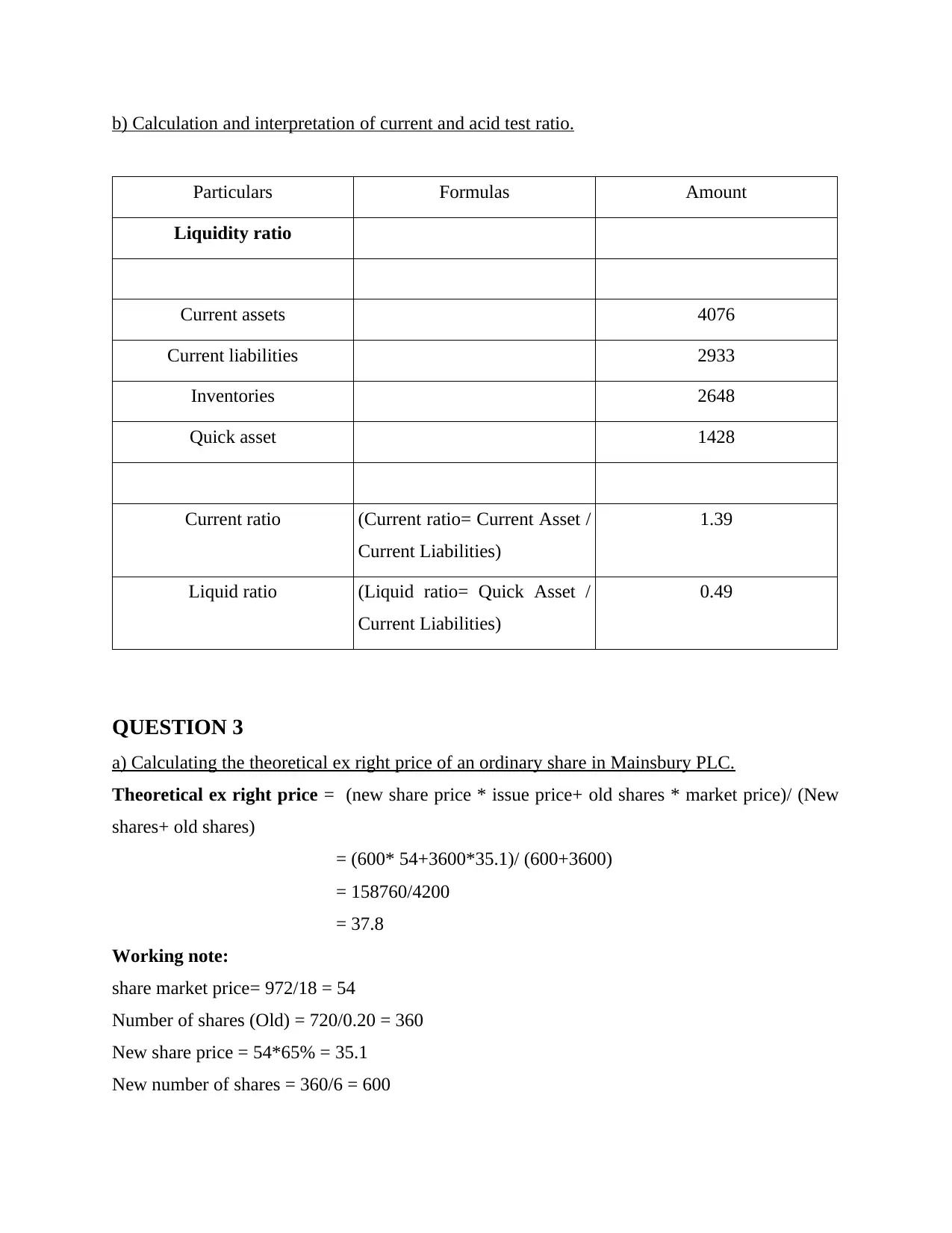

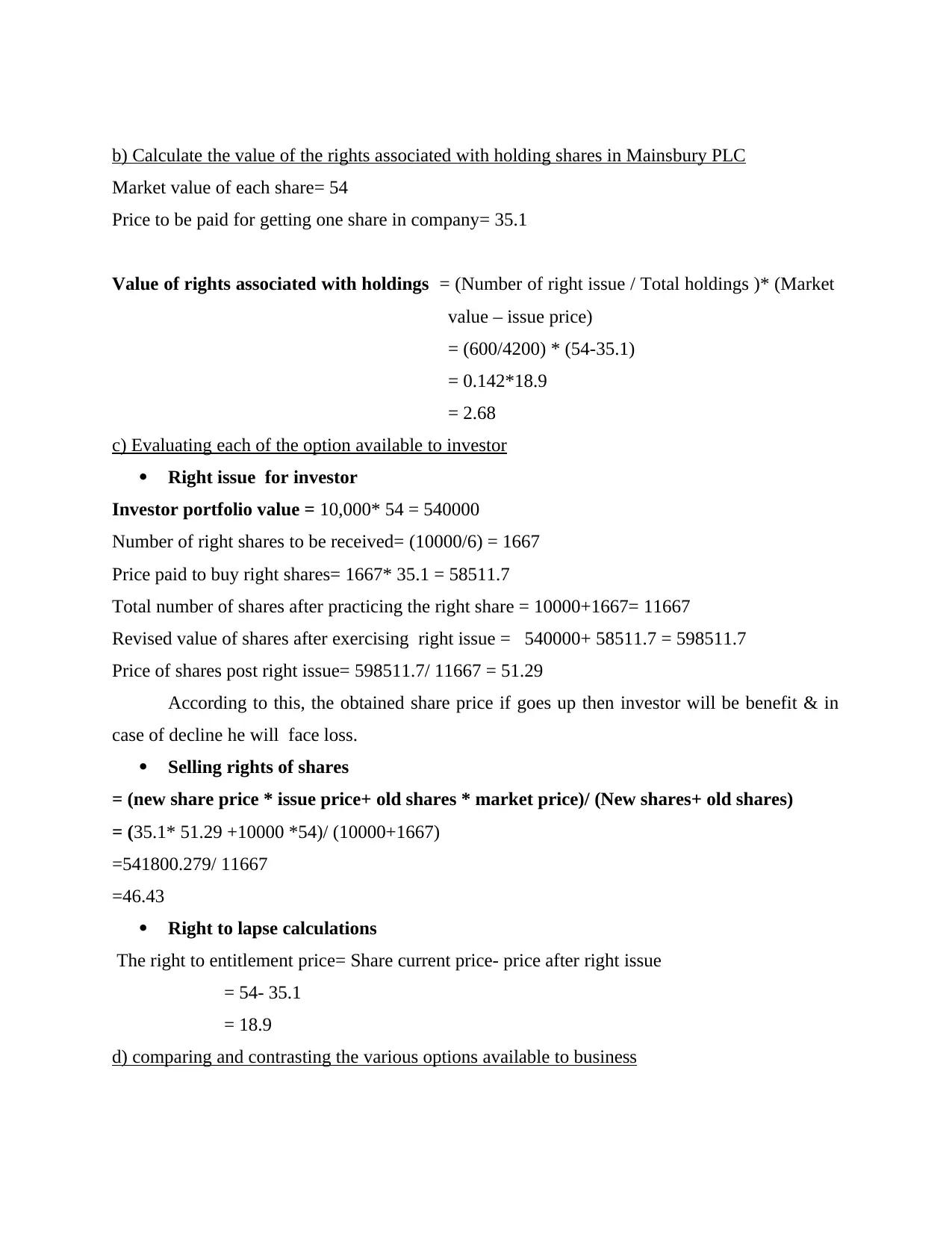

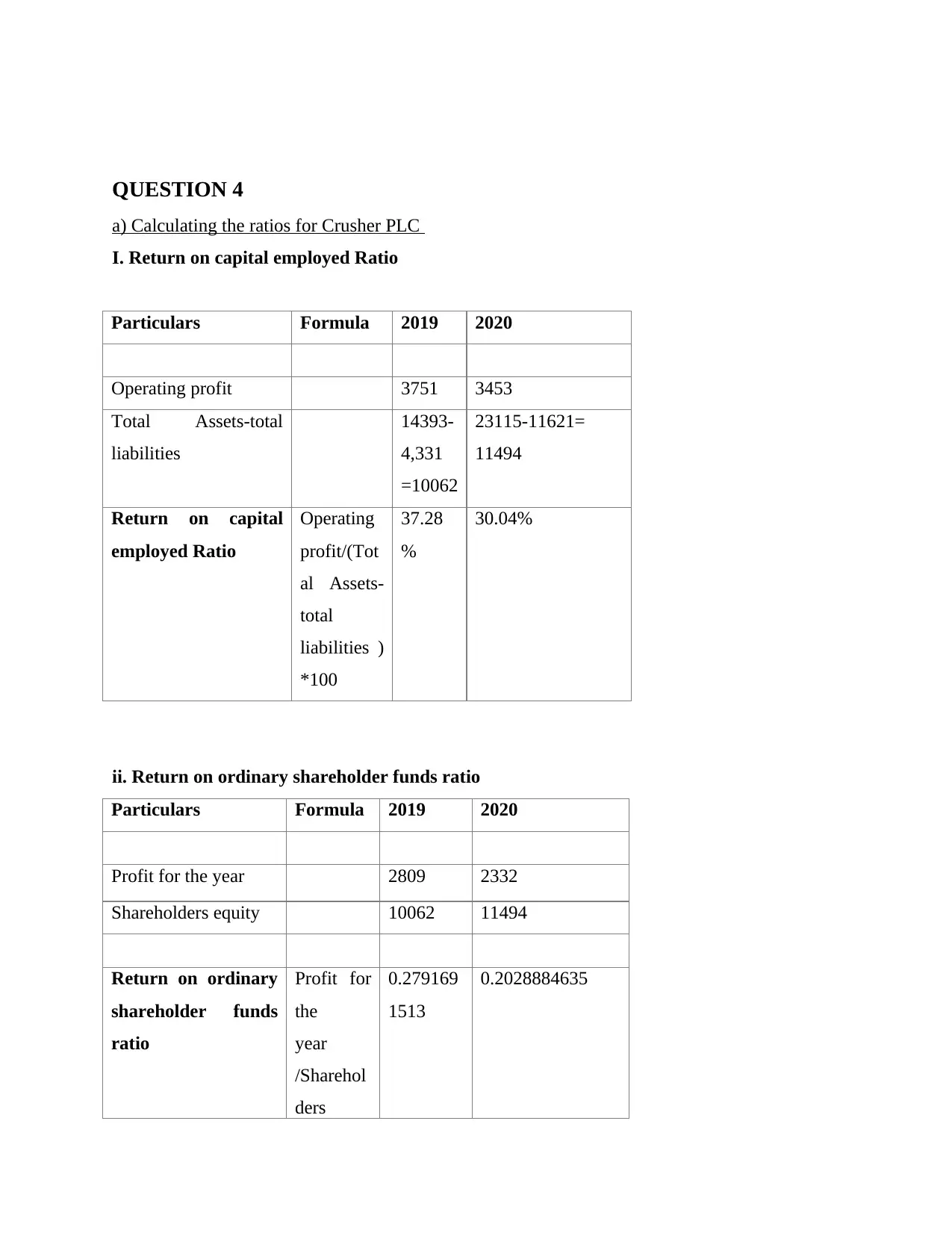

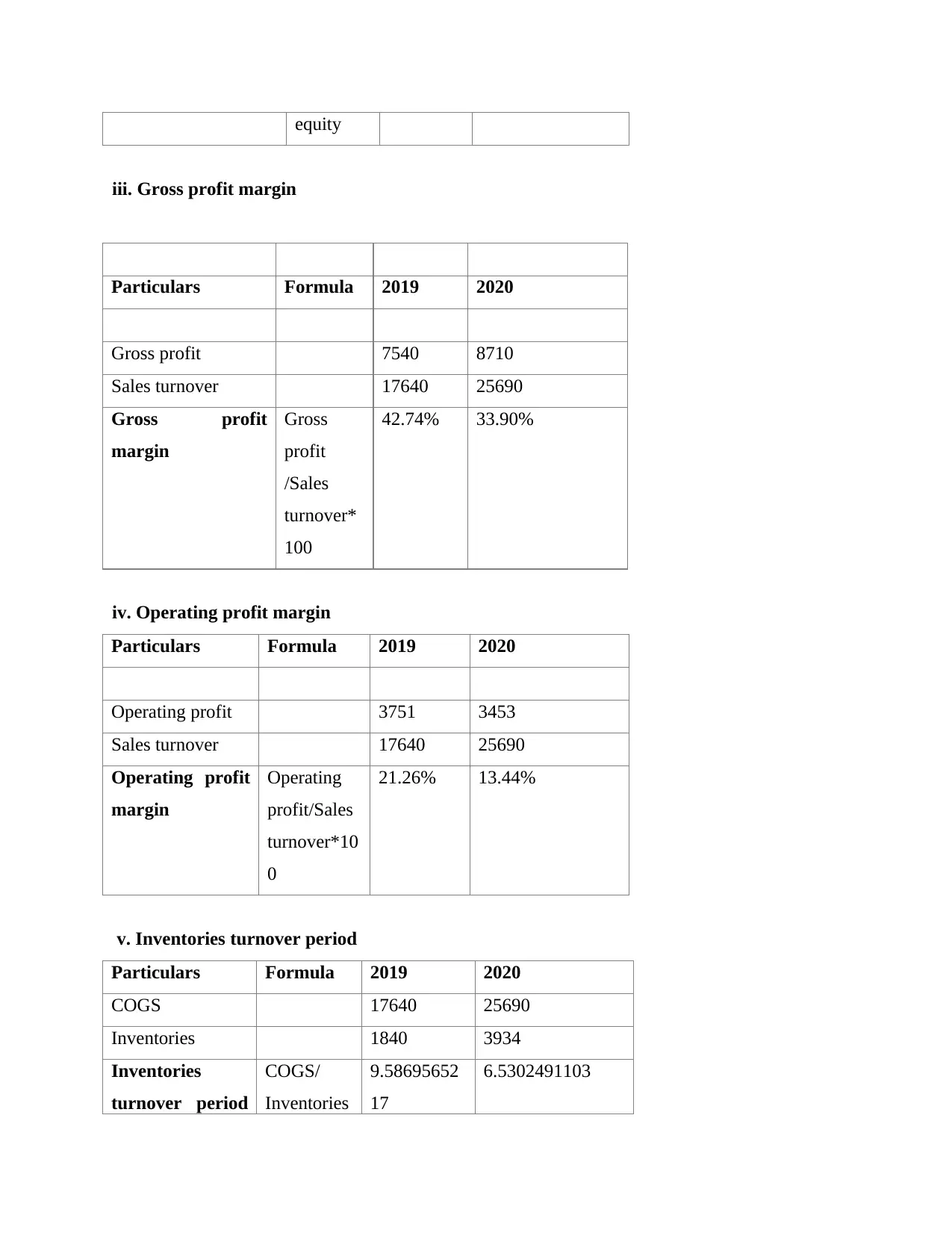

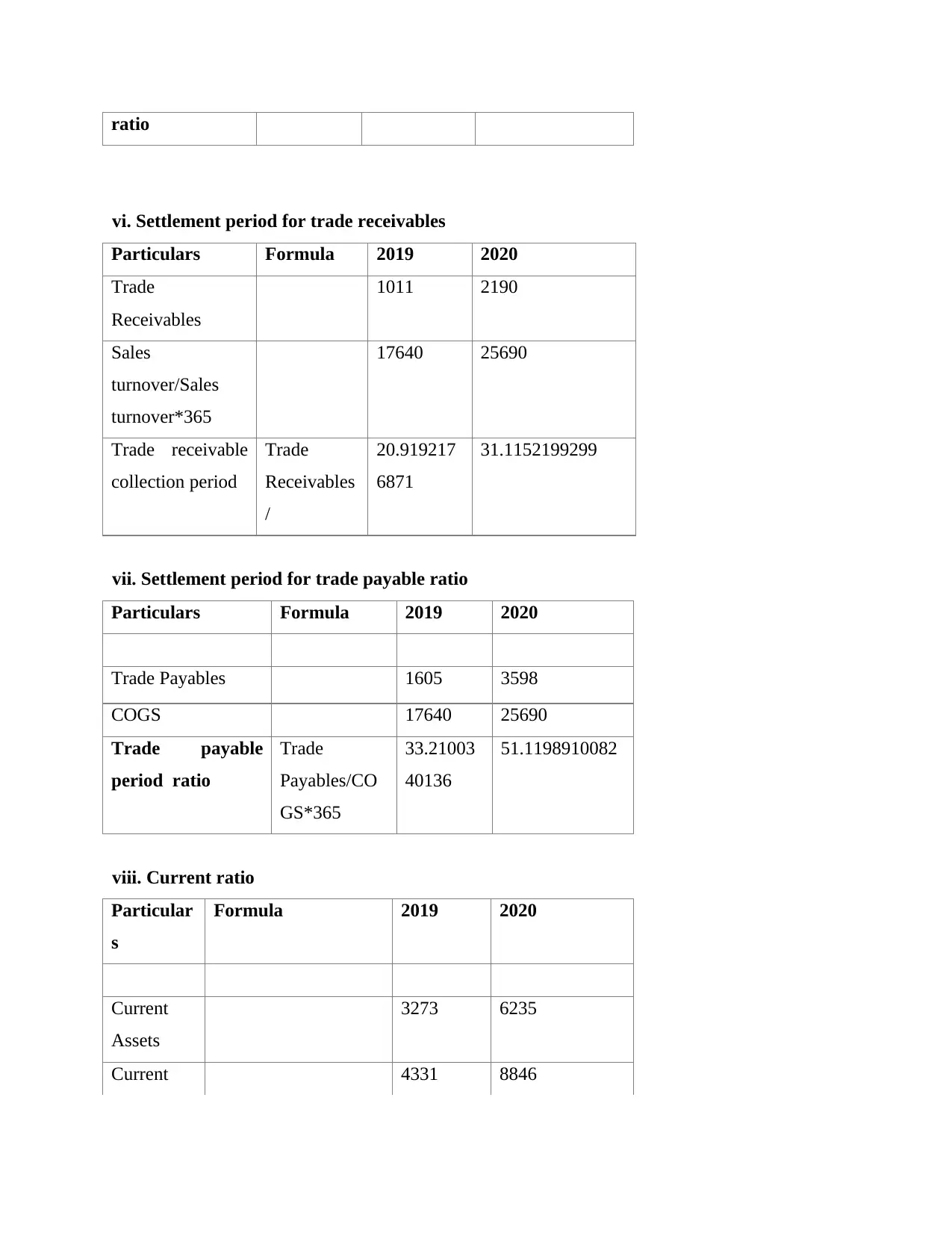

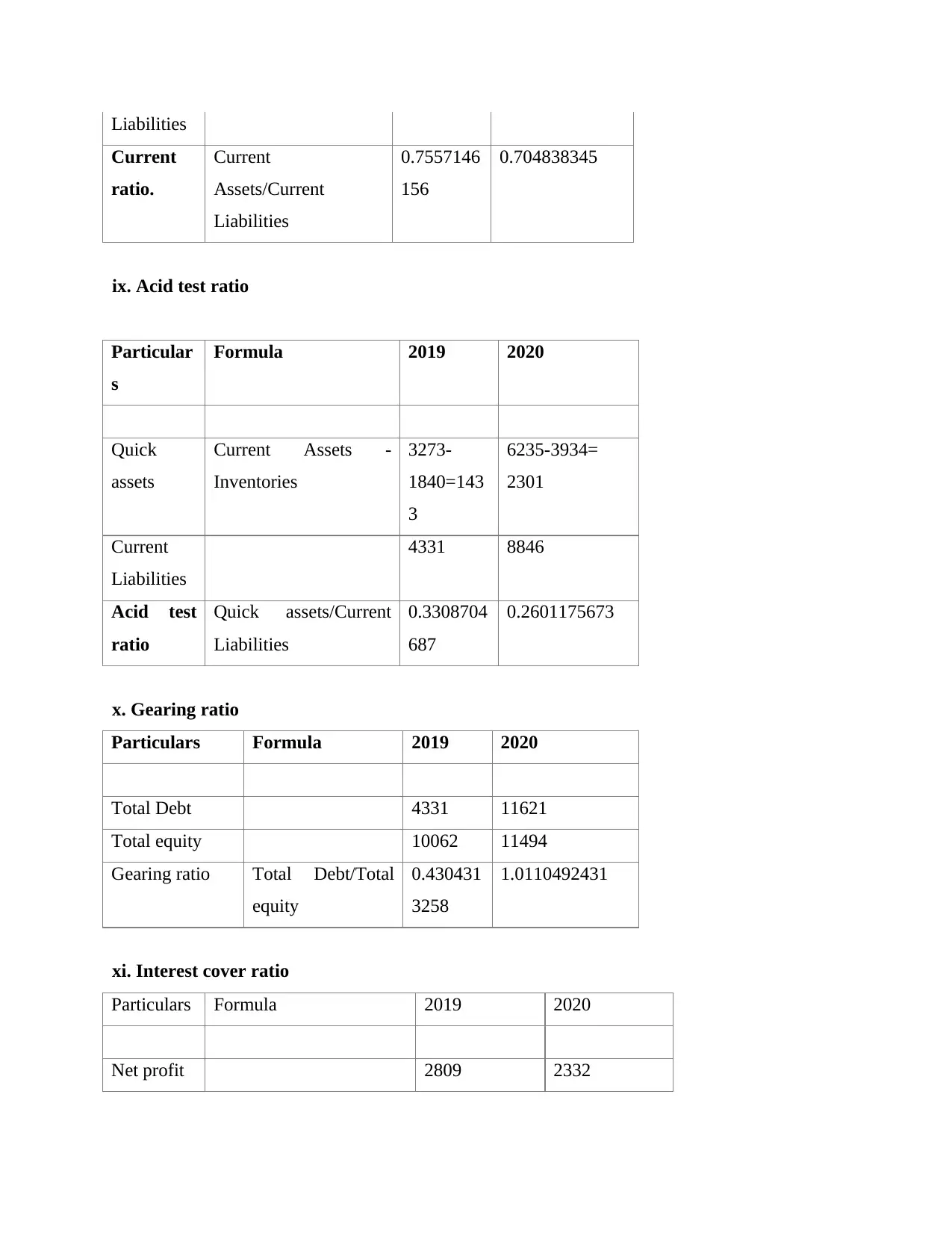

This assignment solution covers key concepts in business finance, including investment appraisal techniques and financial ratio analysis. It begins with the computation of net cash inflows, net present value (NPV), and internal rate of return (IRR) for a project, followed by an analysis of its financial viability and a comparison of different methods for accounting for risk. The solution then calculates and interprets the average operating cycle, current ratio, and acid test ratio. Furthermore, it calculates the theoretical ex-right price of an ordinary share and evaluates various investment options related to rights issues. Finally, the assignment calculates and analyzes several financial ratios for Crusher PLC, including return on capital employed, return on ordinary shareholder funds, gross profit margin, operating profit margin, inventory turnover period, settlement periods for trade receivables and payables, current ratio, acid test ratio, gearing ratio, interest cover ratio, earnings per share, and dividend cover ratio, providing a comprehensive assessment of the company's financial position. Desklib provides a platform for students to access similar solved assignments and past papers.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.