Financial Management: Investment Appraisal Report for M&R PLC

VerifiedAdded on 2023/06/15

|11

|2225

|373

Report

AI Summary

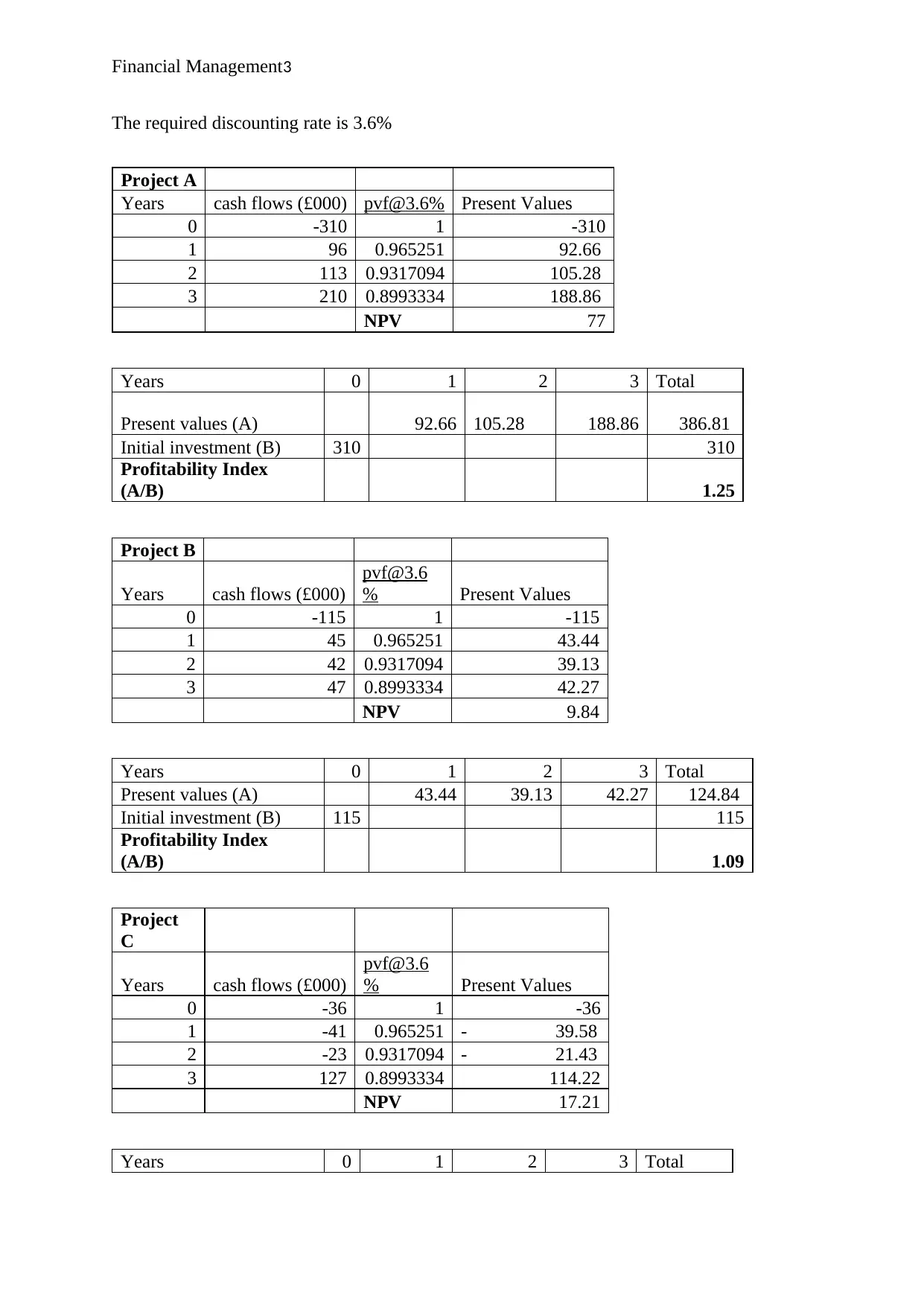

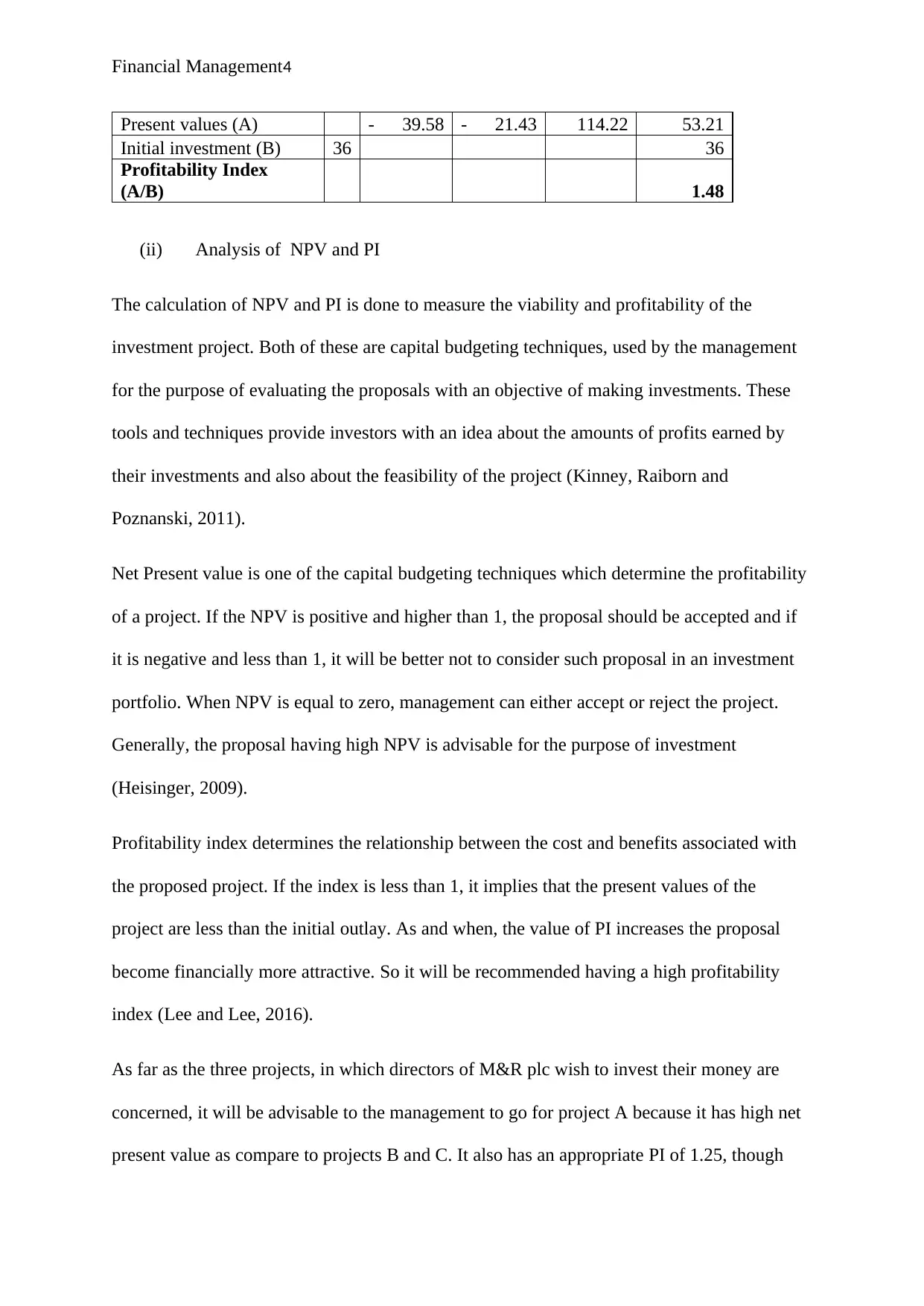

This report provides a comprehensive analysis of investment options for M&R PLC, utilizing capital budgeting techniques such as Net Present Value (NPV) and Profitability Index (PI). The first part evaluates two investment options, considering the impact of inflation and comparing nominal and real approaches to investment assessment. It includes calculations of NPV and PI for three projects, recommending the most viable investment based on these metrics. The second part consists of true/false and multiple-choice questions related to capital budgeting principles. The report concludes by emphasizing the importance of sound investment decisions and the effective use of capital budgeting tools for enhancing profitability and managing risk, highlighting how organizations can improve their financial performance through strategic investment choices.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.